Accounting Principles: Functions, Budgeting, and Financial Analysis

VerifiedAdded on 2023/06/10

|26

|6995

|462

Report

AI Summary

This report discusses accounting principles, which are rules and guidelines followed by organizations when presenting financial data. It covers the purposes and functions of accounting within regulatory and ethical constraints, along with the benefits and limitations of budgeting and budgetary planning. It includes the preparation of a cash budget and the creation of financial statements for sole proprietorships, partnerships, and non-profit organizations. Furthermore, it involves calculating important financial ratios and comparing an organization's performance over time using these ratios. The report also identifies various career opportunities in accounting, such as financial accountant, forensic accountant, management accountant, tax accountant, and project accountant, highlighting the skills required for these positions, including analytical skills, problem-solving abilities, integrity, numerical skills, negotiation skills, and customer service.

Accounting Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

P1. Purpose of the Accounting Functions Within an Organisation........................................3

P2. Assessment of the Accounting Functions in Context of Regulatory and Ethical Constraints

................................................................................................................................................6

P6. Construct a memorandum on Cash Budget......................................................................8

P7. Elaborate the benefits and limitation of budget, budgetary control and planning of the

business organisation............................................................................................................10

Task B............................................................................................................................................12

P4. Prepare financial statements of sole traders, partnerships and not-for-profit organizations.

..............................................................................................................................................12

P5,6. Write a letter for the calculations of the financial ratios from a set of final accounts 20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................24

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

P1. Purpose of the Accounting Functions Within an Organisation........................................3

P2. Assessment of the Accounting Functions in Context of Regulatory and Ethical Constraints

................................................................................................................................................6

P6. Construct a memorandum on Cash Budget......................................................................8

P7. Elaborate the benefits and limitation of budget, budgetary control and planning of the

business organisation............................................................................................................10

Task B............................................................................................................................................12

P4. Prepare financial statements of sole traders, partnerships and not-for-profit organizations.

..............................................................................................................................................12

P5,6. Write a letter for the calculations of the financial ratios from a set of final accounts 20

CONCLUSION..............................................................................................................................22

REFERENCES..............................................................................................................................24

INTRODUCTION

In this report, accounting principles are discussed. Accounting principles are rules and

principles which are followed by the organisations while presenting financial data to

stakeholders (Almagtome, 2021). This report mainly discusses the concepts of accounting. In

first part of this report, various purposes and functions of accounting are considered in details in

the context of the regulatory and ethical constraints. Further in this report, benefits and

limitations of the budget and budgetary planning, and control for an organisation are discussed

along-with preparation of a cash budget. In the second part of report, financial statements for a

sole proprietary business, a partnership and a non-for-profit organisation and interpret them as

well. Afterwards, important financial ratios are calculated and a comparison of the organisation's

performance over the time using financial ratios are done.

PART A

P1. Purpose of the Accounting Functions Within an Organisation

The main purpose of the accounting is to provide assistance to the owners and managers

so that they will be able to take decisions in the best interest of the business entity. The primary

purpose of the accounting is to provide aid to the governing body of the organisation in

identifying the areas which require special consideration and efforts so that it will be beneficial

for the organisation as a whole (Eebo, 2020). Similarly, the main purpose of the accounting

functions is to provide feasibility to the business which will help it ultimately in preparing

necessary and useful qualitative reports to the governing body of the business. Reports are

generated in the form of financial statements of the organisation to the internal and external users

of the financial information.

Career opportunities in Accounting

Financial accountant: The financial accountant is responsible for focusing upon the

preparation of monthly, quarterly and annual reports for the company. For conducting

annual audits, budgeting and management of the tax payments of the organization. The

financial analyst also acts as a consultant of the senior business managers to help them in

preparing reports regarding the conduction of cost and revenue analysis in the business.

Forensic Accountant: The forensic accountant in an organization is responsible for

carrying out many detailed and in depth investigations and analysis regarding accounting,

In this report, accounting principles are discussed. Accounting principles are rules and

principles which are followed by the organisations while presenting financial data to

stakeholders (Almagtome, 2021). This report mainly discusses the concepts of accounting. In

first part of this report, various purposes and functions of accounting are considered in details in

the context of the regulatory and ethical constraints. Further in this report, benefits and

limitations of the budget and budgetary planning, and control for an organisation are discussed

along-with preparation of a cash budget. In the second part of report, financial statements for a

sole proprietary business, a partnership and a non-for-profit organisation and interpret them as

well. Afterwards, important financial ratios are calculated and a comparison of the organisation's

performance over the time using financial ratios are done.

PART A

P1. Purpose of the Accounting Functions Within an Organisation

The main purpose of the accounting is to provide assistance to the owners and managers

so that they will be able to take decisions in the best interest of the business entity. The primary

purpose of the accounting is to provide aid to the governing body of the organisation in

identifying the areas which require special consideration and efforts so that it will be beneficial

for the organisation as a whole (Eebo, 2020). Similarly, the main purpose of the accounting

functions is to provide feasibility to the business which will help it ultimately in preparing

necessary and useful qualitative reports to the governing body of the business. Reports are

generated in the form of financial statements of the organisation to the internal and external users

of the financial information.

Career opportunities in Accounting

Financial accountant: The financial accountant is responsible for focusing upon the

preparation of monthly, quarterly and annual reports for the company. For conducting

annual audits, budgeting and management of the tax payments of the organization. The

financial analyst also acts as a consultant of the senior business managers to help them in

preparing reports regarding the conduction of cost and revenue analysis in the business.

Forensic Accountant: The forensic accountant in an organization is responsible for

carrying out many detailed and in depth investigations and analysis regarding accounting,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

auditing activities in the business. The investigations relate to the finding regarding the

irregularities which are present in company's financial documents, reports and books

maintained. It also includes checking upon the losses that the company incurred and also

to recover all the unlawful or illicit finds that the company has (Kovtun, Kopytina and

Pavlyuchenko, 2018).

Management Accountant: The responsibilities of a management accountant involve

presenting the financial reports of the organization to all the senior managers in the

company to give them an overview and an insight of the financial performance and

situation of the company. The skills such as analytical and problem solving abilities help

them in managing the financial health and assist the senior business managers to plan,

strategize and make informed, correct decisions.

Tax Accountant: the tax accountant in an organization is solely responsible for

maintaining all tax-related obligations and duties of the company. It includes preparing

tax provisions schedules, returns, reports and maintain the database of the organization.

Finding the errors and mistakes committed while in the preparation of the company's tax

filings is also to be evaluated and checked by the tax accountant of the company.

Project Accountant: the responsibilities of a project accountant include managing the

operating budget of the company and to forecast and predict upon the process involved in

the projects. It also includes reviewing and analyzing the performance and of the project

to measure its success rate with the company management and stakeholders of the

enterprise.

Skills required for a position in accounting and finance:

Analytical skills: The analytical skills involve the quality of an individual to analyze data

sets, make critical decisions for an organization in terms of its accounting related issues,

solve for the complex and difficult problem situations in the business so that to provide

for taking in all the necessary information and data relating to the company and mentally

process and analyze the same data in order to assess and determine solutions necessary

for the respective problems (Mulawarman and Kamayanti, 2018).

Problem Solving: This skill helps accountant in an organization to understand and

interpret the business problems in order to provide for the suitable and reasonable

irregularities which are present in company's financial documents, reports and books

maintained. It also includes checking upon the losses that the company incurred and also

to recover all the unlawful or illicit finds that the company has (Kovtun, Kopytina and

Pavlyuchenko, 2018).

Management Accountant: The responsibilities of a management accountant involve

presenting the financial reports of the organization to all the senior managers in the

company to give them an overview and an insight of the financial performance and

situation of the company. The skills such as analytical and problem solving abilities help

them in managing the financial health and assist the senior business managers to plan,

strategize and make informed, correct decisions.

Tax Accountant: the tax accountant in an organization is solely responsible for

maintaining all tax-related obligations and duties of the company. It includes preparing

tax provisions schedules, returns, reports and maintain the database of the organization.

Finding the errors and mistakes committed while in the preparation of the company's tax

filings is also to be evaluated and checked by the tax accountant of the company.

Project Accountant: the responsibilities of a project accountant include managing the

operating budget of the company and to forecast and predict upon the process involved in

the projects. It also includes reviewing and analyzing the performance and of the project

to measure its success rate with the company management and stakeholders of the

enterprise.

Skills required for a position in accounting and finance:

Analytical skills: The analytical skills involve the quality of an individual to analyze data

sets, make critical decisions for an organization in terms of its accounting related issues,

solve for the complex and difficult problem situations in the business so that to provide

for taking in all the necessary information and data relating to the company and mentally

process and analyze the same data in order to assess and determine solutions necessary

for the respective problems (Mulawarman and Kamayanti, 2018).

Problem Solving: This skill helps accountant in an organization to understand and

interpret the business problems in order to provide for the suitable and reasonable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

solutions to those. It involves thinking of the creative and effective ideas which can solve

for those problems and propose the necessary solutions helping an organization to

successfully solve for those problems.

Integrity: It is one of the most fundamental and essential skill for an accountant as it

demands the accountant to be honest, straightforward and real with the client and the

financial information of the respective client so that they could do justice to the work

assigned. The accountant is also responsible for any personal gains or benefits with the

misuse of the information that they have of the client (Srivastava and Shabi, 2019).

Numerical Skills: These skills establish for the base of accounting as a subject. As the

accountant is required to make tough calculations, work through the numerical queries

and support the results received with the required supporting information. Various

mathematical explanations, concepts and theories are applied and used in accounting to

reach to a numerical conclusion for interpreting the data in an efficient and useful

manner.

Negotiation skills: It is one of the critical and essential skill for the accountants as it plays

a crucial role when they negotiate for monetary or the non- monetary issues with their

clients and their respective issues. This skill assists the accountant to get the work done,

establish greater relationships and help in achieving the objectives of the business.

Customer Service: This skill plays an important role in assisting the accountant to help

clients in resolving their problems and issues, provide for licenses and permits and

promote relationship building skills while performing the necessary responsibilities

towards the organization and the client.

Accounting Function within the organization

Accounts Receivable: It is the balance of the money which is due to a business enterprise

for the commodities or services which are delivered or have been utilised by the customer

or client but the payment for the same has not been made from their side. It is a form of

current asset to the organization and is mentioned below the same head in the company's

balance sheet (Butaev and Radjabov 2021).

Accounts Payable: It is an accounting term used to explain the amount which is owned by

the firm to its creditors, vendors or the suppliers of the goods, services that the business

has purchased in terms of credit and have not made the payment for the same. It is the

for those problems and propose the necessary solutions helping an organization to

successfully solve for those problems.

Integrity: It is one of the most fundamental and essential skill for an accountant as it

demands the accountant to be honest, straightforward and real with the client and the

financial information of the respective client so that they could do justice to the work

assigned. The accountant is also responsible for any personal gains or benefits with the

misuse of the information that they have of the client (Srivastava and Shabi, 2019).

Numerical Skills: These skills establish for the base of accounting as a subject. As the

accountant is required to make tough calculations, work through the numerical queries

and support the results received with the required supporting information. Various

mathematical explanations, concepts and theories are applied and used in accounting to

reach to a numerical conclusion for interpreting the data in an efficient and useful

manner.

Negotiation skills: It is one of the critical and essential skill for the accountants as it plays

a crucial role when they negotiate for monetary or the non- monetary issues with their

clients and their respective issues. This skill assists the accountant to get the work done,

establish greater relationships and help in achieving the objectives of the business.

Customer Service: This skill plays an important role in assisting the accountant to help

clients in resolving their problems and issues, provide for licenses and permits and

promote relationship building skills while performing the necessary responsibilities

towards the organization and the client.

Accounting Function within the organization

Accounts Receivable: It is the balance of the money which is due to a business enterprise

for the commodities or services which are delivered or have been utilised by the customer

or client but the payment for the same has not been made from their side. It is a form of

current asset to the organization and is mentioned below the same head in the company's

balance sheet (Butaev and Radjabov 2021).

Accounts Payable: It is an accounting term used to explain the amount which is owned by

the firm to its creditors, vendors or the suppliers of the goods, services that the business

has purchased in terms of credit and have not made the payment for the same. It is the

current liability of the organization which owns this amount which is to be settled by

making payments.

Inventory Account: Inventory accounting is the sphere of accounting which has dealings

relating to the stock management and the frequent valuations necessary in the inventory

management. It also manages upon the different values of changes and differences that

take place in the organizations inventory assets.

Payroll Account: It is a type of separate bank account which is maintained to check and

manage the payroll transactions of the business. As the organizations make sure that to

avoid confusions they utilise this account only for the purpose of making the wage

payments to the employees of the business (Suleymanov and et.al., 2018).

Fixed Asset Account: This account is exclusively maintained to keep a check regarding

all the long term fixed assets of the organization. It keeps a record of all the capital assets

of the business, the details regarding their lifecycle and usage in the business.

Cash Account: A cash account is a kind of business to business or business to consumer

account which is maintained to make the immediate payments in the organization. This

keeps a check of all the cash payments made by the organization for the requisite

necessary time period and provides for all the transactions which took place in that

tenure.

P2. Assessment of the Accounting Functions in Context of Regulatory and Ethical Constraints

Accounting functions are required to perform to accomplish the ultimate purposes of the

accounting process of the organisation. Various accounting functions are identified above let us

take a detailed analysis of each function, which are as follows: Integrity: A professional accountant should be to the point and trustworthy in all

professional and organisational relations. An accountant should not be related with

reports, return or any other information where they assumed that data includes a

materially wrong or deceptive statement or it contains statements which are provided

carelessly or excludes information which is needed to be concluded. Objectivity: An accountant should not permit partiality, dispute regarding interest or

excessive impact of others to overrule professional or organisational judgements.

Accountant is unprotected towards circumstances that can harm objectivity. It is not

making payments.

Inventory Account: Inventory accounting is the sphere of accounting which has dealings

relating to the stock management and the frequent valuations necessary in the inventory

management. It also manages upon the different values of changes and differences that

take place in the organizations inventory assets.

Payroll Account: It is a type of separate bank account which is maintained to check and

manage the payroll transactions of the business. As the organizations make sure that to

avoid confusions they utilise this account only for the purpose of making the wage

payments to the employees of the business (Suleymanov and et.al., 2018).

Fixed Asset Account: This account is exclusively maintained to keep a check regarding

all the long term fixed assets of the organization. It keeps a record of all the capital assets

of the business, the details regarding their lifecycle and usage in the business.

Cash Account: A cash account is a kind of business to business or business to consumer

account which is maintained to make the immediate payments in the organization. This

keeps a check of all the cash payments made by the organization for the requisite

necessary time period and provides for all the transactions which took place in that

tenure.

P2. Assessment of the Accounting Functions in Context of Regulatory and Ethical Constraints

Accounting functions are required to perform to accomplish the ultimate purposes of the

accounting process of the organisation. Various accounting functions are identified above let us

take a detailed analysis of each function, which are as follows: Integrity: A professional accountant should be to the point and trustworthy in all

professional and organisational relations. An accountant should not be related with

reports, return or any other information where they assumed that data includes a

materially wrong or deceptive statement or it contains statements which are provided

carelessly or excludes information which is needed to be concluded. Objectivity: An accountant should not permit partiality, dispute regarding interest or

excessive impact of others to overrule professional or organisational judgements.

Accountant is unprotected towards circumstances that can harm objectivity. It is not

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

possible to describe all such situations. Relations that are bias and effect professional

judgements should be ignored. Professional Competence and Due Care: A professional accountant has a consistent

obligation to keep professional knowledge and competency at the stage which is required

to insure that a client or employee acquires competent professional service depended on

recent developments in practice, governance and methods. A professional accountant

should behave actively and according to applied technical and professional standards

while delivering professional services (Ferry and Ahrens 2021). Confidentiality: An accountant should honour the discretion and privacy of data obtained

as an outcome of professional and business interconnections a should not unwrap or

expose any such information to outsiders without adequate and specific governance

except there is a legal or professional right or obligation for such exposure.

Professional Behaviour: A professional accountant should follow all the application

rules and regulations and should ignore any activities that dishonour the profession.

Assessment of accounting functions within the business in the respect of regulatory

constraints: Duty to keep accounting records: Every organisation must keep proper accounting

records. Proper accounting records means records that are adequate to present and

elaborate the organisation's transactions, to Disclose the financial position of company

with adequate accuracy at any point of time and to authorise the directors to insure that

any account prepared, must comply the requirements or regulations. Where and how long are reports to be kept: The main objective behind preserving

reports is to balance the books and accounts for flow of cash by an organisation. It is

initially done in large organisations which assist them in finding errors and frauds. The

minimum time to keep business records is 7 years while employment tax records are to

be kept for minimum 4 years from the date they were paid off. Accountants to give true and fair view: A true and fair view in accounting refers that a

financial statement is free from material misstatements and devotedly depicts the

financial performance of an organisation. In most of circumstances, a true and fair view is

accomplished by complying with accounting standards as the standards are planned to

judgements should be ignored. Professional Competence and Due Care: A professional accountant has a consistent

obligation to keep professional knowledge and competency at the stage which is required

to insure that a client or employee acquires competent professional service depended on

recent developments in practice, governance and methods. A professional accountant

should behave actively and according to applied technical and professional standards

while delivering professional services (Ferry and Ahrens 2021). Confidentiality: An accountant should honour the discretion and privacy of data obtained

as an outcome of professional and business interconnections a should not unwrap or

expose any such information to outsiders without adequate and specific governance

except there is a legal or professional right or obligation for such exposure.

Professional Behaviour: A professional accountant should follow all the application

rules and regulations and should ignore any activities that dishonour the profession.

Assessment of accounting functions within the business in the respect of regulatory

constraints: Duty to keep accounting records: Every organisation must keep proper accounting

records. Proper accounting records means records that are adequate to present and

elaborate the organisation's transactions, to Disclose the financial position of company

with adequate accuracy at any point of time and to authorise the directors to insure that

any account prepared, must comply the requirements or regulations. Where and how long are reports to be kept: The main objective behind preserving

reports is to balance the books and accounts for flow of cash by an organisation. It is

initially done in large organisations which assist them in finding errors and frauds. The

minimum time to keep business records is 7 years while employment tax records are to

be kept for minimum 4 years from the date they were paid off. Accountants to give true and fair view: A true and fair view in accounting refers that a

financial statement is free from material misstatements and devotedly depicts the

financial performance of an organisation. In most of circumstances, a true and fair view is

accomplished by complying with accounting standards as the standards are planned to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

give acknowledgement, measurement, presentation and disclosure for particular features

of financial reporting in a manner that review economic Reality.

P6. Construct a memorandum on Cash Budget

To: The firm

FROM: Graduate Trainee

SUBJECT: Budget for the year ended 31st December 2023.

DATE:

The estimation of cash inflow and outflow in a business is known as cash budget. It can

be prepared monthly, quarterly, weekly and yearly. To use of cash budget can be identify how

much cash available to continue the business. It is two type short term and long term. Using

Short term cash budget can be determined the cash is needed for monthly and weekly, long term

cash budget can be determined the cash is needed for long time. On the basis of this budget to

determine the surplus cash can invest in marketable securities.

The cash budget for the month of Jan2023-Dec2023

of financial reporting in a manner that review economic Reality.

P6. Construct a memorandum on Cash Budget

To: The firm

FROM: Graduate Trainee

SUBJECT: Budget for the year ended 31st December 2023.

DATE:

The estimation of cash inflow and outflow in a business is known as cash budget. It can

be prepared monthly, quarterly, weekly and yearly. To use of cash budget can be identify how

much cash available to continue the business. It is two type short term and long term. Using

Short term cash budget can be determined the cash is needed for monthly and weekly, long term

cash budget can be determined the cash is needed for long time. On the basis of this budget to

determine the surplus cash can invest in marketable securities.

The cash budget for the month of Jan2023-Dec2023

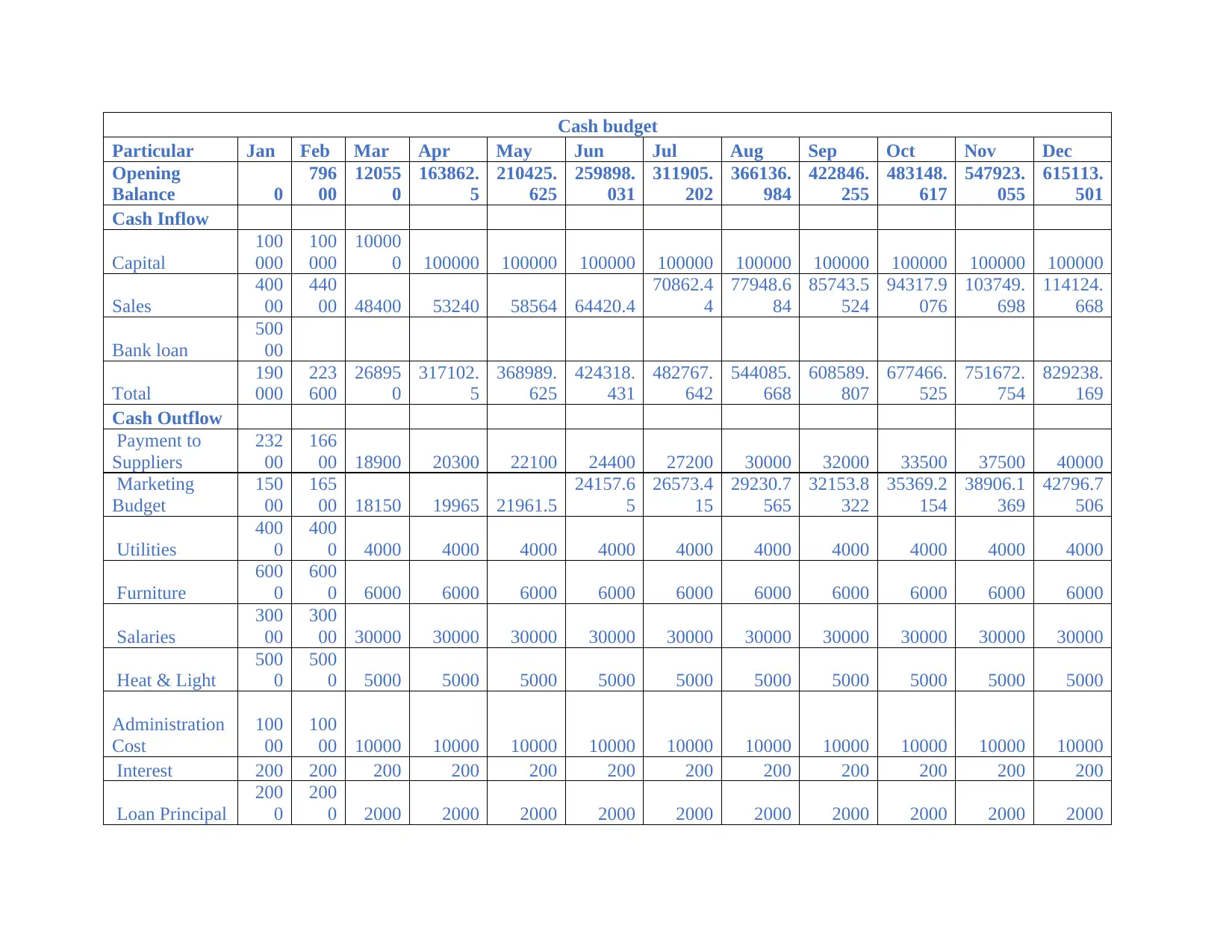

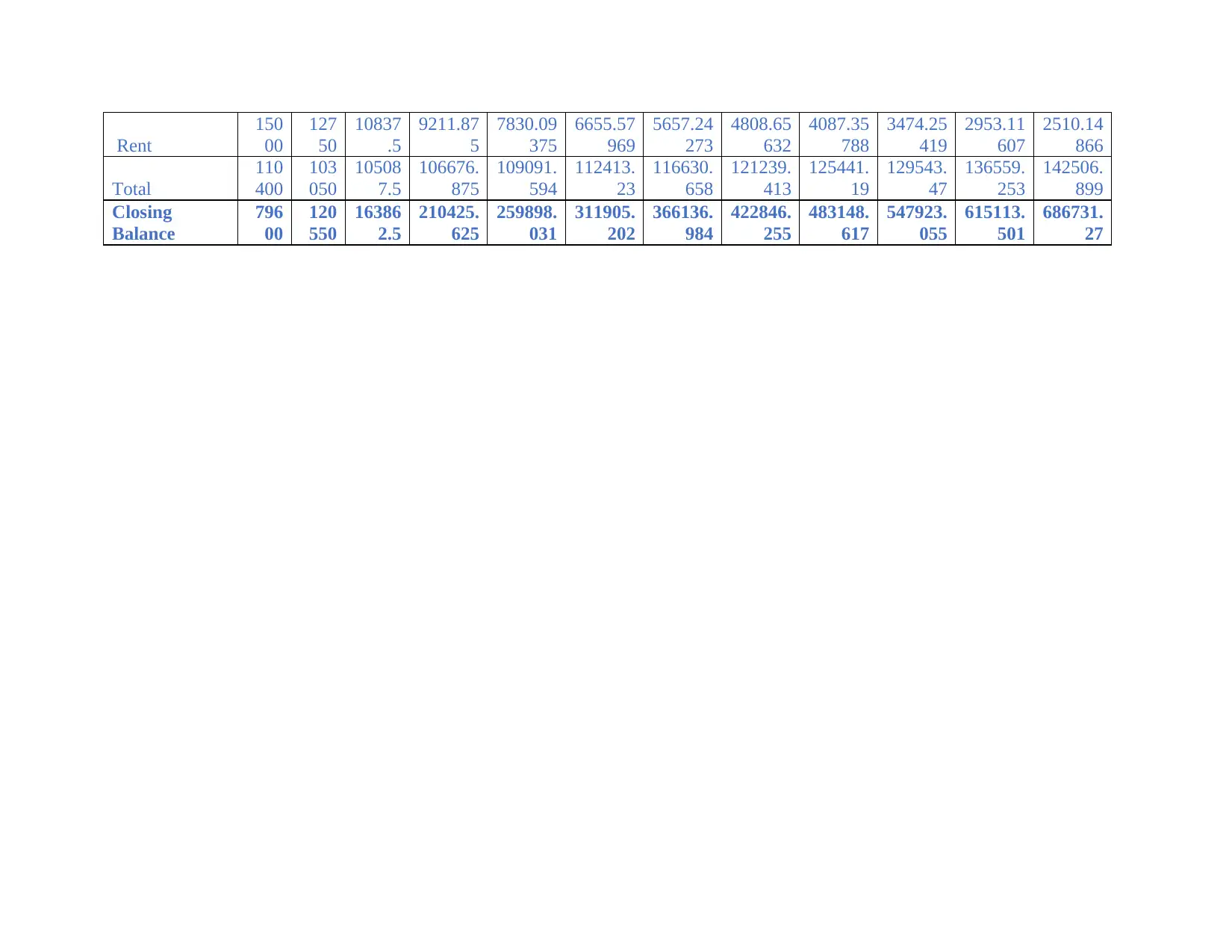

Cash budget

Particular Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Opening

Balance 0

796

00

12055

0

163862.

5

210425.

625

259898.

031

311905.

202

366136.

984

422846.

255

483148.

617

547923.

055

615113.

501

Cash Inflow

Capital

100

000

100

000

10000

0 100000 100000 100000 100000 100000 100000 100000 100000 100000

Sales

400

00

440

00 48400 53240 58564 64420.4

70862.4

4

77948.6

84

85743.5

524

94317.9

076

103749.

698

114124.

668

Bank loan

500

00

Total

190

000

223

600

26895

0

317102.

5

368989.

625

424318.

431

482767.

642

544085.

668

608589.

807

677466.

525

751672.

754

829238.

169

Cash Outflow

Payment to

Suppliers

232

00

166

00 18900 20300 22100 24400 27200 30000 32000 33500 37500 40000

Marketing

Budget

150

00

165

00 18150 19965 21961.5

24157.6

5

26573.4

15

29230.7

565

32153.8

322

35369.2

154

38906.1

369

42796.7

506

Utilities

400

0

400

0 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Furniture

600

0

600

0 6000 6000 6000 6000 6000 6000 6000 6000 6000 6000

Salaries

300

00

300

00 30000 30000 30000 30000 30000 30000 30000 30000 30000 30000

Heat & Light

500

0

500

0 5000 5000 5000 5000 5000 5000 5000 5000 5000 5000

Administration

Cost

100

00

100

00 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000

Interest 200 200 200 200 200 200 200 200 200 200 200 200

Loan Principal

200

0

200

0 2000 2000 2000 2000 2000 2000 2000 2000 2000 2000

Particular Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Opening

Balance 0

796

00

12055

0

163862.

5

210425.

625

259898.

031

311905.

202

366136.

984

422846.

255

483148.

617

547923.

055

615113.

501

Cash Inflow

Capital

100

000

100

000

10000

0 100000 100000 100000 100000 100000 100000 100000 100000 100000

Sales

400

00

440

00 48400 53240 58564 64420.4

70862.4

4

77948.6

84

85743.5

524

94317.9

076

103749.

698

114124.

668

Bank loan

500

00

Total

190

000

223

600

26895

0

317102.

5

368989.

625

424318.

431

482767.

642

544085.

668

608589.

807

677466.

525

751672.

754

829238.

169

Cash Outflow

Payment to

Suppliers

232

00

166

00 18900 20300 22100 24400 27200 30000 32000 33500 37500 40000

Marketing

Budget

150

00

165

00 18150 19965 21961.5

24157.6

5

26573.4

15

29230.7

565

32153.8

322

35369.2

154

38906.1

369

42796.7

506

Utilities

400

0

400

0 4000 4000 4000 4000 4000 4000 4000 4000 4000 4000

Furniture

600

0

600

0 6000 6000 6000 6000 6000 6000 6000 6000 6000 6000

Salaries

300

00

300

00 30000 30000 30000 30000 30000 30000 30000 30000 30000 30000

Heat & Light

500

0

500

0 5000 5000 5000 5000 5000 5000 5000 5000 5000 5000

Administration

Cost

100

00

100

00 10000 10000 10000 10000 10000 10000 10000 10000 10000 10000

Interest 200 200 200 200 200 200 200 200 200 200 200 200

Loan Principal

200

0

200

0 2000 2000 2000 2000 2000 2000 2000 2000 2000 2000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Rent

150

00

127

50

10837

.5

9211.87

5

7830.09

375

6655.57

969

5657.24

273

4808.65

632

4087.35

788

3474.25

419

2953.11

607

2510.14

866

Total

110

400

103

050

10508

7.5

106676.

875

109091.

594

112413.

23

116630.

658

121239.

413

125441.

19

129543.

47

136559.

253

142506.

899

Closing

Balance

796

00

120

550

16386

2.5

210425.

625

259898.

031

311905.

202

366136.

984

422846.

255

483148.

617

547923.

055

615113.

501

686731.

27

150

00

127

50

10837

.5

9211.87

5

7830.09

375

6655.57

969

5657.24

273

4808.65

632

4087.35

788

3474.25

419

2953.11

607

2510.14

866

Total

110

400

103

050

10508

7.5

106676.

875

109091.

594

112413.

23

116630.

658

121239.

413

125441.

19

129543.

47

136559.

253

142506.

899

Closing

Balance

796

00

120

550

16386

2.5

210425.

625

259898.

031

311905.

202

366136.

984

422846.

255

483148.

617

547923.

055

615113.

501

686731.

27

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P7. Elaborate the benefits and limitation of budget, budgetary control and planning of the

business organisation.

Budget shows the status of financial position in a company at any point of time. Budget

helps in controlling the money in future. Budget can be preparing a group, individual and

company to shows cash inflow and outflow in future (Wong, George and Tanima, 2018).

Benefits of budgeting as a tool of budgetary planning, and control

Helps in planning- Budgets are pre-determined plans that are made on various estimation

and proper analysis. It helps the organisation to know the expected earning and

expenditure according to which operations can be planned.

Enhanced efficiency- When everything is pre planned and decided, duties are allotted to

the accountable person it becomes easy for operating. This is good method for controlling

waste and eliminate unnecessary expenses.

Proper communication- Budgets are pre-determined estimation of operation of the

organisation. The budgets are prepared taking consideration from each level. Thus it

maintains proper relation and coordination between all the level operating in the business

entity.

Control- Budgets are desired results that organisation wants for its company. The actual

results are compared with budgeted performance. The deviation from the performed and

estimated activity is analysed based on performance.

Delegation of authority- Budgets are set of predetermined standards that encourages

delegation of authority. It sets timelines and period to complete task which call for

sharing responsibilities so that works gets completed on time.

Limitations of budgeting as a tool of budgetary planning, and control

Rigidity- Budgets are meant to set limits to the operation, which fixes time and cost

required for completion. Due to changing environment factors it is sometimes impossible

to achieve the desired results. Also there are time when things are overestimated, but

employees do the work in overestimated cost to meet the budgets requirements.

Inaccuracy- Budgets are prepared on past trends analysis which are always good method

of estimation. Because dynamic environment does not follow trend therefore the budget

prepared based on the past analysis are often inaccurate and delivers inefficient results.

business organisation.

Budget shows the status of financial position in a company at any point of time. Budget

helps in controlling the money in future. Budget can be preparing a group, individual and

company to shows cash inflow and outflow in future (Wong, George and Tanima, 2018).

Benefits of budgeting as a tool of budgetary planning, and control

Helps in planning- Budgets are pre-determined plans that are made on various estimation

and proper analysis. It helps the organisation to know the expected earning and

expenditure according to which operations can be planned.

Enhanced efficiency- When everything is pre planned and decided, duties are allotted to

the accountable person it becomes easy for operating. This is good method for controlling

waste and eliminate unnecessary expenses.

Proper communication- Budgets are pre-determined estimation of operation of the

organisation. The budgets are prepared taking consideration from each level. Thus it

maintains proper relation and coordination between all the level operating in the business

entity.

Control- Budgets are desired results that organisation wants for its company. The actual

results are compared with budgeted performance. The deviation from the performed and

estimated activity is analysed based on performance.

Delegation of authority- Budgets are set of predetermined standards that encourages

delegation of authority. It sets timelines and period to complete task which call for

sharing responsibilities so that works gets completed on time.

Limitations of budgeting as a tool of budgetary planning, and control

Rigidity- Budgets are meant to set limits to the operation, which fixes time and cost

required for completion. Due to changing environment factors it is sometimes impossible

to achieve the desired results. Also there are time when things are overestimated, but

employees do the work in overestimated cost to meet the budgets requirements.

Inaccuracy- Budgets are prepared on past trends analysis which are always good method

of estimation. Because dynamic environment does not follow trend therefore the budget

prepared based on the past analysis are often inaccurate and delivers inefficient results.

Conflicts among different departments- Budgets are made on consideration given by

different departments, and it requires to complete a task with coordination. When the

actual performance does not meet the desired results the departments starts to blame each

other for the mistakes. Hence conflicts starts to take place in the organisation.

Expensive- Budgets are made on whereas estimation and studies which requires lot of

time and expertise. Thus in a current business environment n organisation which is

earning a good amount of turnover can only afford preparing budgets.

Discourages efficient employees- first and foremost budgets are made with most

discretion of the top level management there are manipulative and inaccurate,

overestimation and underestimation of results are very harmful for the productivity of the

organisation. The worker who can perform better than the budgets is demotivated and

inefficient and the one who is not able to achieve task but is a faithful employee may be

lost due to the results.

Budgetary Control is a method to prepare budget using various technique and activities and

compare the results with actual and if any deviation comes, rectify the budget this whole method

is known as Budgetary Control. It is a continuous process to planning and coordinating.

Budgetary control responsibility centre

Revenue Centre: The original units are compared in monetary terms not compared in

input cost

Expense Centre: Units are compared in previous budget not compare in actual output.

Profit Centres: The differences have found in revenue and expense then inter department

is using in transfer price that is cost plus profit price.

Investment Centres: producing rate of interest when output compared with assets.

Budgetary control process

Step 1: Budget Preparation – Collecting information’s from different sources, budget maker

analysis trend and details from the past. He also estimates and predict future events that might

takes place. According to which budgets are prepared for profit, expenses and credits.

Step 2: Comparison of actual results and budgeted data- When the budgets are prepared and

applied in the organisation duties are assigned and persons are given the task to perform. In a

period of 3 or 6 months the actual results are compared with desired performance. Deviation

from income and variance from expenditures must be studied. And the reason behind the

different departments, and it requires to complete a task with coordination. When the

actual performance does not meet the desired results the departments starts to blame each

other for the mistakes. Hence conflicts starts to take place in the organisation.

Expensive- Budgets are made on whereas estimation and studies which requires lot of

time and expertise. Thus in a current business environment n organisation which is

earning a good amount of turnover can only afford preparing budgets.

Discourages efficient employees- first and foremost budgets are made with most

discretion of the top level management there are manipulative and inaccurate,

overestimation and underestimation of results are very harmful for the productivity of the

organisation. The worker who can perform better than the budgets is demotivated and

inefficient and the one who is not able to achieve task but is a faithful employee may be

lost due to the results.

Budgetary Control is a method to prepare budget using various technique and activities and

compare the results with actual and if any deviation comes, rectify the budget this whole method

is known as Budgetary Control. It is a continuous process to planning and coordinating.

Budgetary control responsibility centre

Revenue Centre: The original units are compared in monetary terms not compared in

input cost

Expense Centre: Units are compared in previous budget not compare in actual output.

Profit Centres: The differences have found in revenue and expense then inter department

is using in transfer price that is cost plus profit price.

Investment Centres: producing rate of interest when output compared with assets.

Budgetary control process

Step 1: Budget Preparation – Collecting information’s from different sources, budget maker

analysis trend and details from the past. He also estimates and predict future events that might

takes place. According to which budgets are prepared for profit, expenses and credits.

Step 2: Comparison of actual results and budgeted data- When the budgets are prepared and

applied in the organisation duties are assigned and persons are given the task to perform. In a

period of 3 or 6 months the actual results are compared with desired performance. Deviation

from income and variance from expenditures must be studied. And the reason behind the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.