Accounting Processes and Systems

VerifiedAdded on 2023/01/16

|19

|4063

|99

AI Summary

This document provides detailed information about accounting processes and systems. It includes journal entries, ledger accounts, trial balance, adjusting journal entries, income statement, balance sheet, and more. The content is relevant for students studying accounting or related courses.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING PROCESSES AND SYSTEMS

1

ACCOUNTING PROCESSES AND SYSTEMS

1

ACCOUNTING PROCESSES AND SYSTEMS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING PROCESSES AND SYSTEMS 2

Table of Contents

Question 1...................................................................................................................................................3

1...............................................................................................................................................................3

2...............................................................................................................................................................5

3...............................................................................................................................................................8

4...............................................................................................................................................................9

5.............................................................................................................................................................10

6.............................................................................................................................................................10

7.............................................................................................................................................................11

Question 2.................................................................................................................................................11

Importance of Double Entry Bookkeeping.............................................................................................12

Question 3.................................................................................................................................................14

1.............................................................................................................................................................14

Accounting issues..................................................................................................................................15

Related party Transactions....................................................................................................................15

Opaque Operations................................................................................................................................15

Poor strategic planning and expansion...................................................................................................16

2.............................................................................................................................................................16

Ethical issues.........................................................................................................................................16

References.................................................................................................................................................18

Table of Contents

Question 1...................................................................................................................................................3

1...............................................................................................................................................................3

2...............................................................................................................................................................5

3...............................................................................................................................................................8

4...............................................................................................................................................................9

5.............................................................................................................................................................10

6.............................................................................................................................................................10

7.............................................................................................................................................................11

Question 2.................................................................................................................................................11

Importance of Double Entry Bookkeeping.............................................................................................12

Question 3.................................................................................................................................................14

1.............................................................................................................................................................14

Accounting issues..................................................................................................................................15

Related party Transactions....................................................................................................................15

Opaque Operations................................................................................................................................15

Poor strategic planning and expansion...................................................................................................16

2.............................................................................................................................................................16

Ethical issues.........................................................................................................................................16

References.................................................................................................................................................18

ACCOUNTING PROCESSES AND SYSTEMS 3

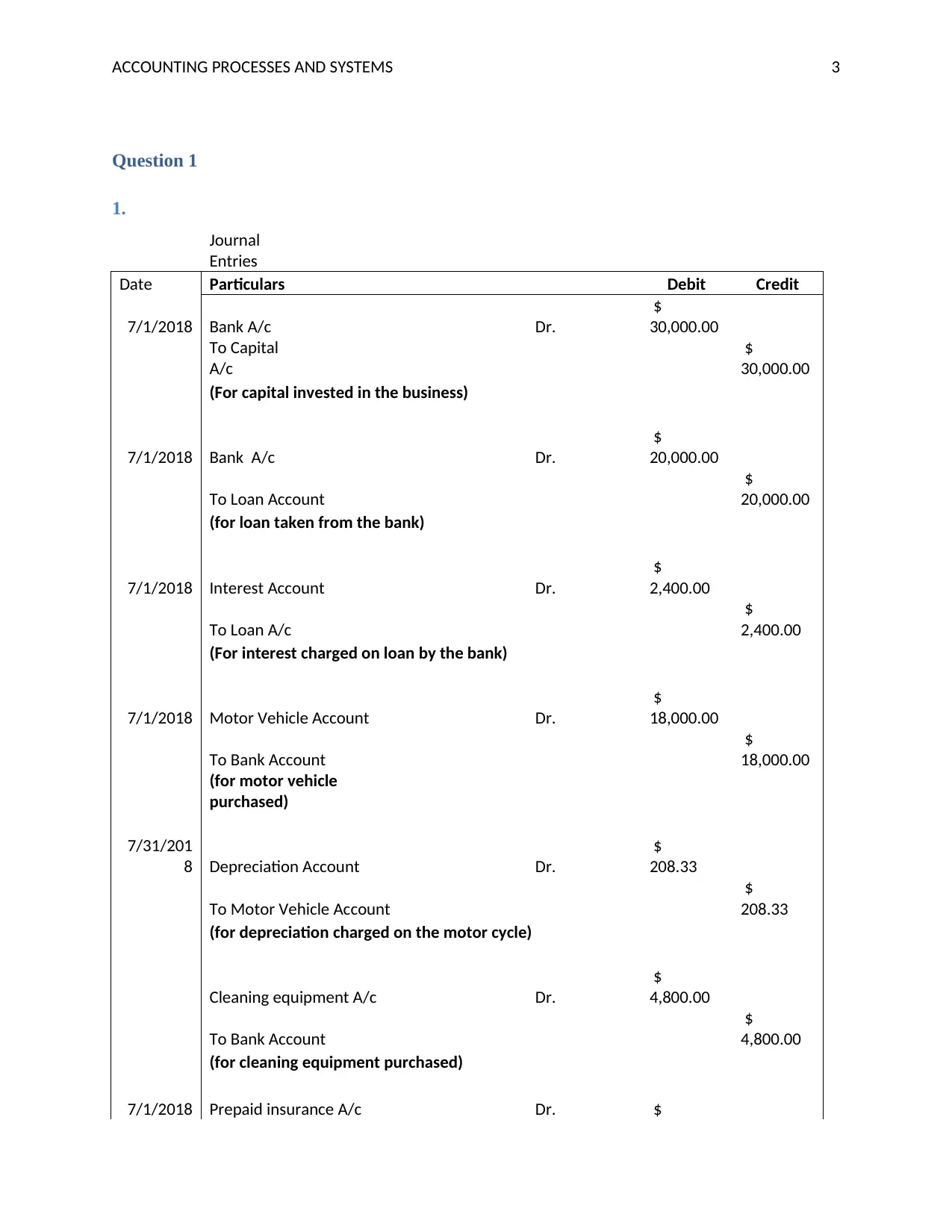

Question 1

1.

Journal

Entries

Date Particulars Debit Credit

7/1/2018 Bank A/c Dr.

$

30,000.00

To Capital

A/c

$

30,000.00

(For capital invested in the business)

7/1/2018 Bank A/c Dr.

$

20,000.00

To Loan Account

$

20,000.00

(for loan taken from the bank)

7/1/2018 Interest Account Dr.

$

2,400.00

To Loan A/c

$

2,400.00

(For interest charged on loan by the bank)

7/1/2018 Motor Vehicle Account Dr.

$

18,000.00

To Bank Account

$

18,000.00

(for motor vehicle

purchased)

7/31/201

8 Depreciation Account Dr.

$

208.33

To Motor Vehicle Account

$

208.33

(for depreciation charged on the motor cycle)

Cleaning equipment A/c Dr.

$

4,800.00

To Bank Account

$

4,800.00

(for cleaning equipment purchased)

7/1/2018 Prepaid insurance A/c Dr. $

Question 1

1.

Journal

Entries

Date Particulars Debit Credit

7/1/2018 Bank A/c Dr.

$

30,000.00

To Capital

A/c

$

30,000.00

(For capital invested in the business)

7/1/2018 Bank A/c Dr.

$

20,000.00

To Loan Account

$

20,000.00

(for loan taken from the bank)

7/1/2018 Interest Account Dr.

$

2,400.00

To Loan A/c

$

2,400.00

(For interest charged on loan by the bank)

7/1/2018 Motor Vehicle Account Dr.

$

18,000.00

To Bank Account

$

18,000.00

(for motor vehicle

purchased)

7/31/201

8 Depreciation Account Dr.

$

208.33

To Motor Vehicle Account

$

208.33

(for depreciation charged on the motor cycle)

Cleaning equipment A/c Dr.

$

4,800.00

To Bank Account

$

4,800.00

(for cleaning equipment purchased)

7/1/2018 Prepaid insurance A/c Dr. $

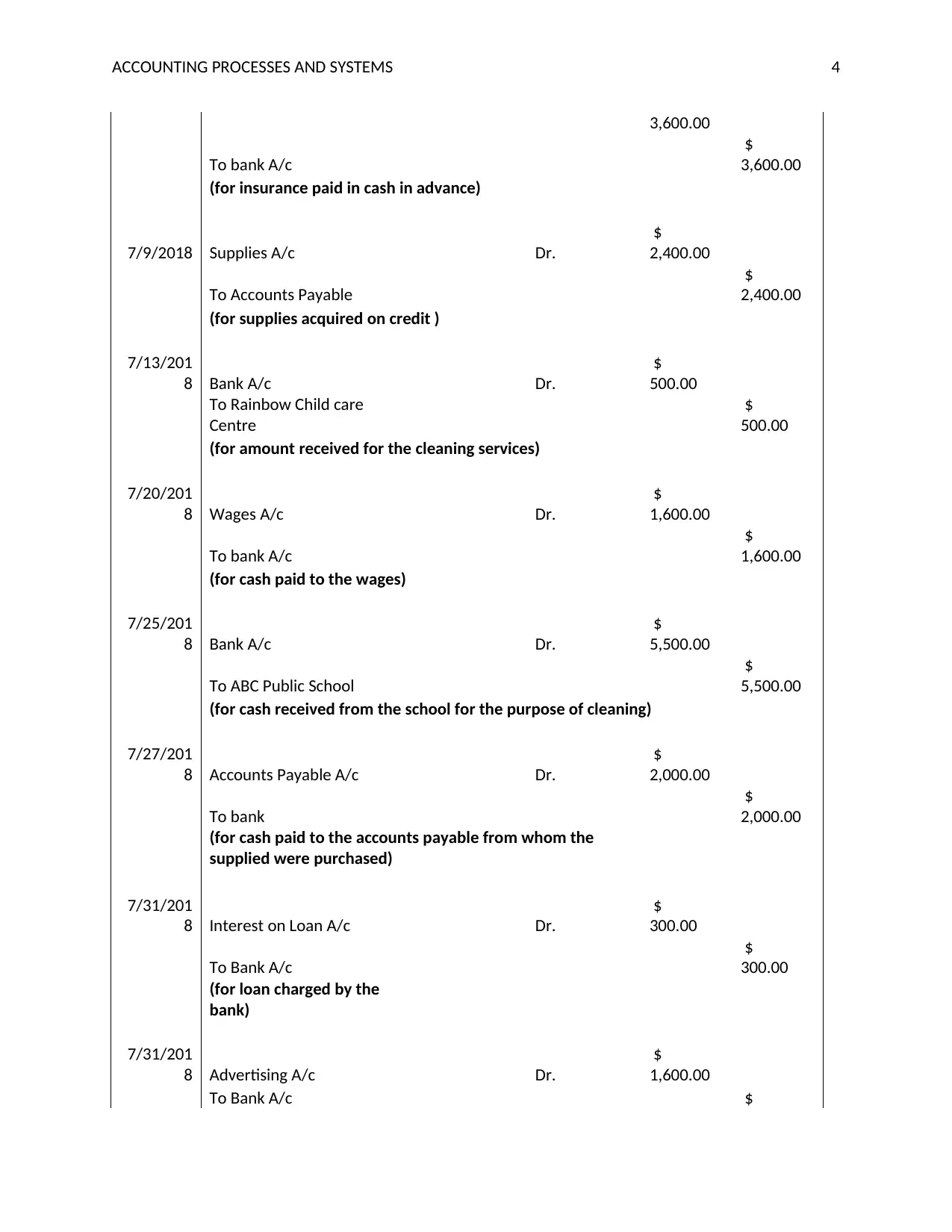

ACCOUNTING PROCESSES AND SYSTEMS 4

3,600.00

To bank A/c

$

3,600.00

(for insurance paid in cash in advance)

7/9/2018 Supplies A/c Dr.

$

2,400.00

To Accounts Payable

$

2,400.00

(for supplies acquired on credit )

7/13/201

8 Bank A/c Dr.

$

500.00

To Rainbow Child care

Centre

$

500.00

(for amount received for the cleaning services)

7/20/201

8 Wages A/c Dr.

$

1,600.00

To bank A/c

$

1,600.00

(for cash paid to the wages)

7/25/201

8 Bank A/c Dr.

$

5,500.00

To ABC Public School

$

5,500.00

(for cash received from the school for the purpose of cleaning)

7/27/201

8 Accounts Payable A/c Dr.

$

2,000.00

To bank

$

2,000.00

(for cash paid to the accounts payable from whom the

supplied were purchased)

7/31/201

8 Interest on Loan A/c Dr.

$

300.00

To Bank A/c

$

300.00

(for loan charged by the

bank)

7/31/201

8 Advertising A/c Dr.

$

1,600.00

To Bank A/c $

3,600.00

To bank A/c

$

3,600.00

(for insurance paid in cash in advance)

7/9/2018 Supplies A/c Dr.

$

2,400.00

To Accounts Payable

$

2,400.00

(for supplies acquired on credit )

7/13/201

8 Bank A/c Dr.

$

500.00

To Rainbow Child care

Centre

$

500.00

(for amount received for the cleaning services)

7/20/201

8 Wages A/c Dr.

$

1,600.00

To bank A/c

$

1,600.00

(for cash paid to the wages)

7/25/201

8 Bank A/c Dr.

$

5,500.00

To ABC Public School

$

5,500.00

(for cash received from the school for the purpose of cleaning)

7/27/201

8 Accounts Payable A/c Dr.

$

2,000.00

To bank

$

2,000.00

(for cash paid to the accounts payable from whom the

supplied were purchased)

7/31/201

8 Interest on Loan A/c Dr.

$

300.00

To Bank A/c

$

300.00

(for loan charged by the

bank)

7/31/201

8 Advertising A/c Dr.

$

1,600.00

To Bank A/c $

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING PROCESSES AND SYSTEMS 5

1,600.00

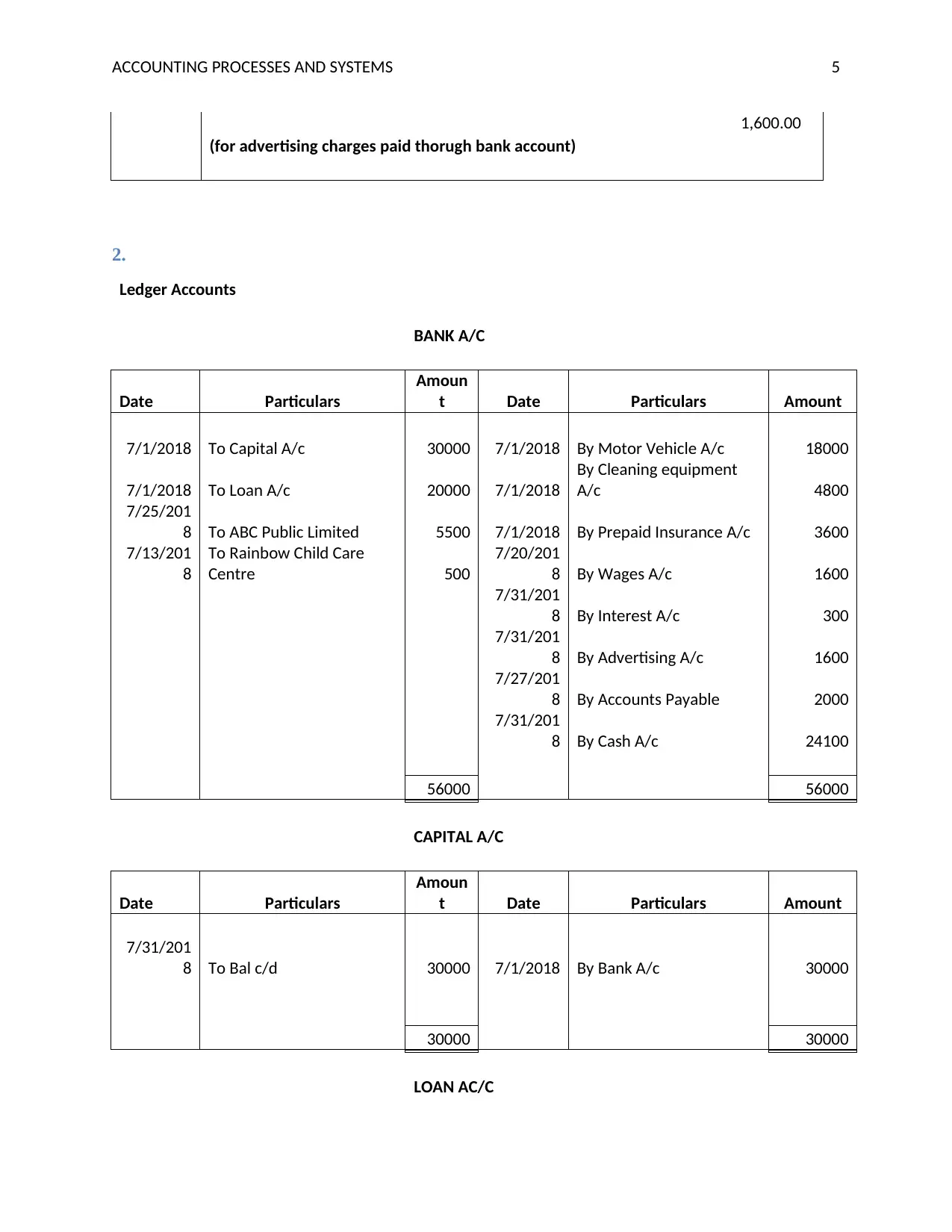

(for advertising charges paid thorugh bank account)

2.

Ledger Accounts

BANK A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Capital A/c 30000 7/1/2018 By Motor Vehicle A/c 18000

7/1/2018 To Loan A/c 20000 7/1/2018

By Cleaning equipment

A/c 4800

7/25/201

8 To ABC Public Limited 5500 7/1/2018 By Prepaid Insurance A/c 3600

7/13/201

8

To Rainbow Child Care

Centre 500

7/20/201

8 By Wages A/c 1600

7/31/201

8 By Interest A/c 300

7/31/201

8 By Advertising A/c 1600

7/27/201

8 By Accounts Payable 2000

7/31/201

8 By Cash A/c 24100

56000 56000

CAPITAL A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 30000 7/1/2018 By Bank A/c 30000

30000 30000

LOAN AC/C

1,600.00

(for advertising charges paid thorugh bank account)

2.

Ledger Accounts

BANK A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Capital A/c 30000 7/1/2018 By Motor Vehicle A/c 18000

7/1/2018 To Loan A/c 20000 7/1/2018

By Cleaning equipment

A/c 4800

7/25/201

8 To ABC Public Limited 5500 7/1/2018 By Prepaid Insurance A/c 3600

7/13/201

8

To Rainbow Child Care

Centre 500

7/20/201

8 By Wages A/c 1600

7/31/201

8 By Interest A/c 300

7/31/201

8 By Advertising A/c 1600

7/27/201

8 By Accounts Payable 2000

7/31/201

8 By Cash A/c 24100

56000 56000

CAPITAL A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 30000 7/1/2018 By Bank A/c 30000

30000 30000

LOAN AC/C

ACCOUNTING PROCESSES AND SYSTEMS 6

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 20000 7/1/2018 By Bank A/c 20000

20000 20000

INTEREST A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 300

7/31/201

8 By Bal c/d 300

300 300

MOTOR VEHICLE

A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Bank A/c 18000

7/31/201

8 By Depreciation A/c 208.33

7/31/201

8 By Bal c/d 17791.67

18000 18000

DEPRECIATION A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Motor Vehicle 208.33

7/31/201

8 By Bal c/d 208.33

208.33 208.33

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 20000 7/1/2018 By Bank A/c 20000

20000 20000

INTEREST A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 300

7/31/201

8 By Bal c/d 300

300 300

MOTOR VEHICLE

A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Bank A/c 18000

7/31/201

8 By Depreciation A/c 208.33

7/31/201

8 By Bal c/d 17791.67

18000 18000

DEPRECIATION A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Motor Vehicle 208.33

7/31/201

8 By Bal c/d 208.33

208.33 208.33

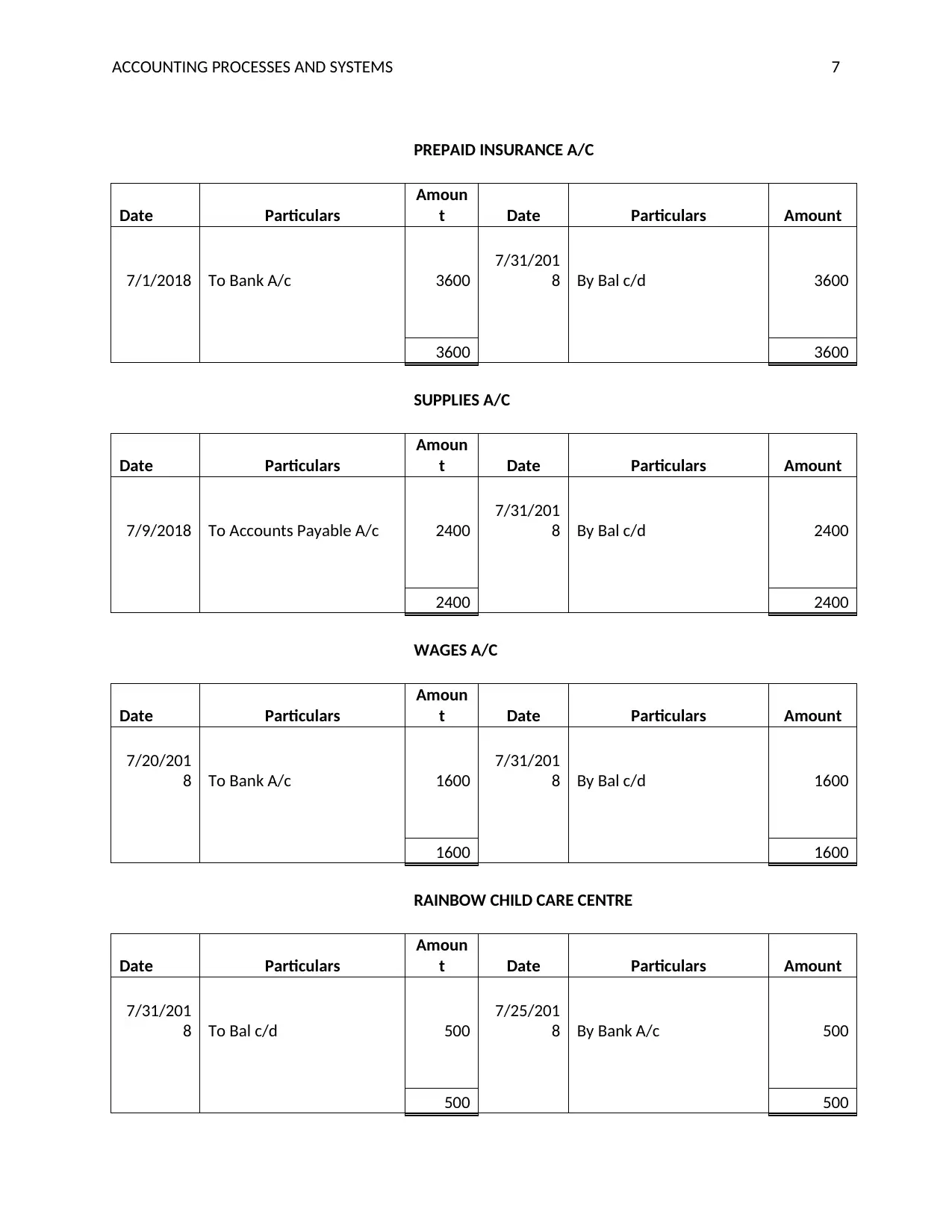

ACCOUNTING PROCESSES AND SYSTEMS 7

PREPAID INSURANCE A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Bank A/c 3600

7/31/201

8 By Bal c/d 3600

3600 3600

SUPPLIES A/C

Date Particulars

Amoun

t Date Particulars Amount

7/9/2018 To Accounts Payable A/c 2400

7/31/201

8 By Bal c/d 2400

2400 2400

WAGES A/C

Date Particulars

Amoun

t Date Particulars Amount

7/20/201

8 To Bank A/c 1600

7/31/201

8 By Bal c/d 1600

1600 1600

RAINBOW CHILD CARE CENTRE

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 500

7/25/201

8 By Bank A/c 500

500 500

PREPAID INSURANCE A/C

Date Particulars

Amoun

t Date Particulars Amount

7/1/2018 To Bank A/c 3600

7/31/201

8 By Bal c/d 3600

3600 3600

SUPPLIES A/C

Date Particulars

Amoun

t Date Particulars Amount

7/9/2018 To Accounts Payable A/c 2400

7/31/201

8 By Bal c/d 2400

2400 2400

WAGES A/C

Date Particulars

Amoun

t Date Particulars Amount

7/20/201

8 To Bank A/c 1600

7/31/201

8 By Bal c/d 1600

1600 1600

RAINBOW CHILD CARE CENTRE

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 500

7/25/201

8 By Bank A/c 500

500 500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING PROCESSES AND SYSTEMS 8

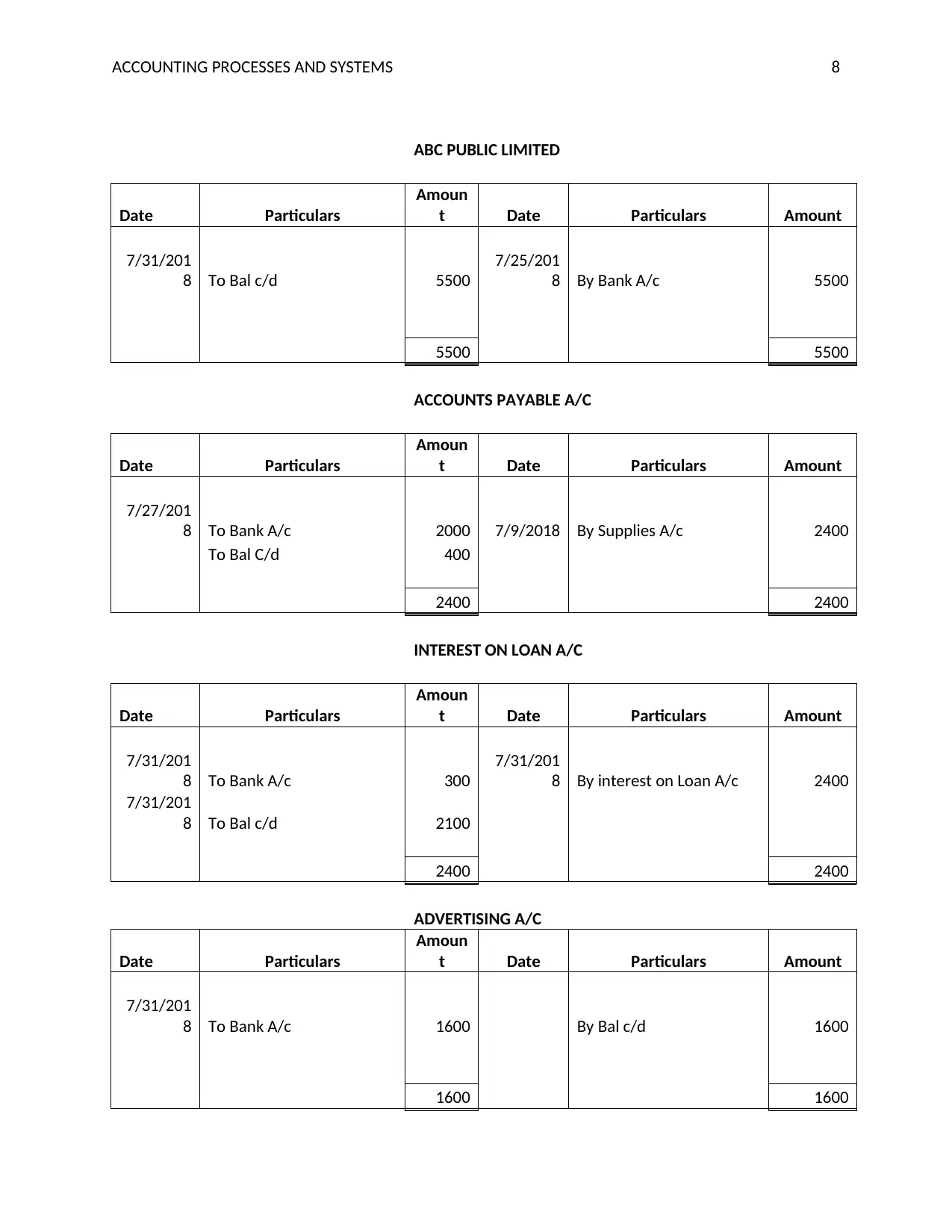

ABC PUBLIC LIMITED

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 5500

7/25/201

8 By Bank A/c 5500

5500 5500

ACCOUNTS PAYABLE A/C

Date Particulars

Amoun

t Date Particulars Amount

7/27/201

8 To Bank A/c 2000 7/9/2018 By Supplies A/c 2400

To Bal C/d 400

2400 2400

INTEREST ON LOAN A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 300

7/31/201

8 By interest on Loan A/c 2400

7/31/201

8 To Bal c/d 2100

2400 2400

ADVERTISING A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 1600 By Bal c/d 1600

1600 1600

ABC PUBLIC LIMITED

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bal c/d 5500

7/25/201

8 By Bank A/c 5500

5500 5500

ACCOUNTS PAYABLE A/C

Date Particulars

Amoun

t Date Particulars Amount

7/27/201

8 To Bank A/c 2000 7/9/2018 By Supplies A/c 2400

To Bal C/d 400

2400 2400

INTEREST ON LOAN A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 300

7/31/201

8 By interest on Loan A/c 2400

7/31/201

8 To Bal c/d 2100

2400 2400

ADVERTISING A/C

Date Particulars

Amoun

t Date Particulars Amount

7/31/201

8 To Bank A/c 1600 By Bal c/d 1600

1600 1600

ACCOUNTING PROCESSES AND SYSTEMS 9

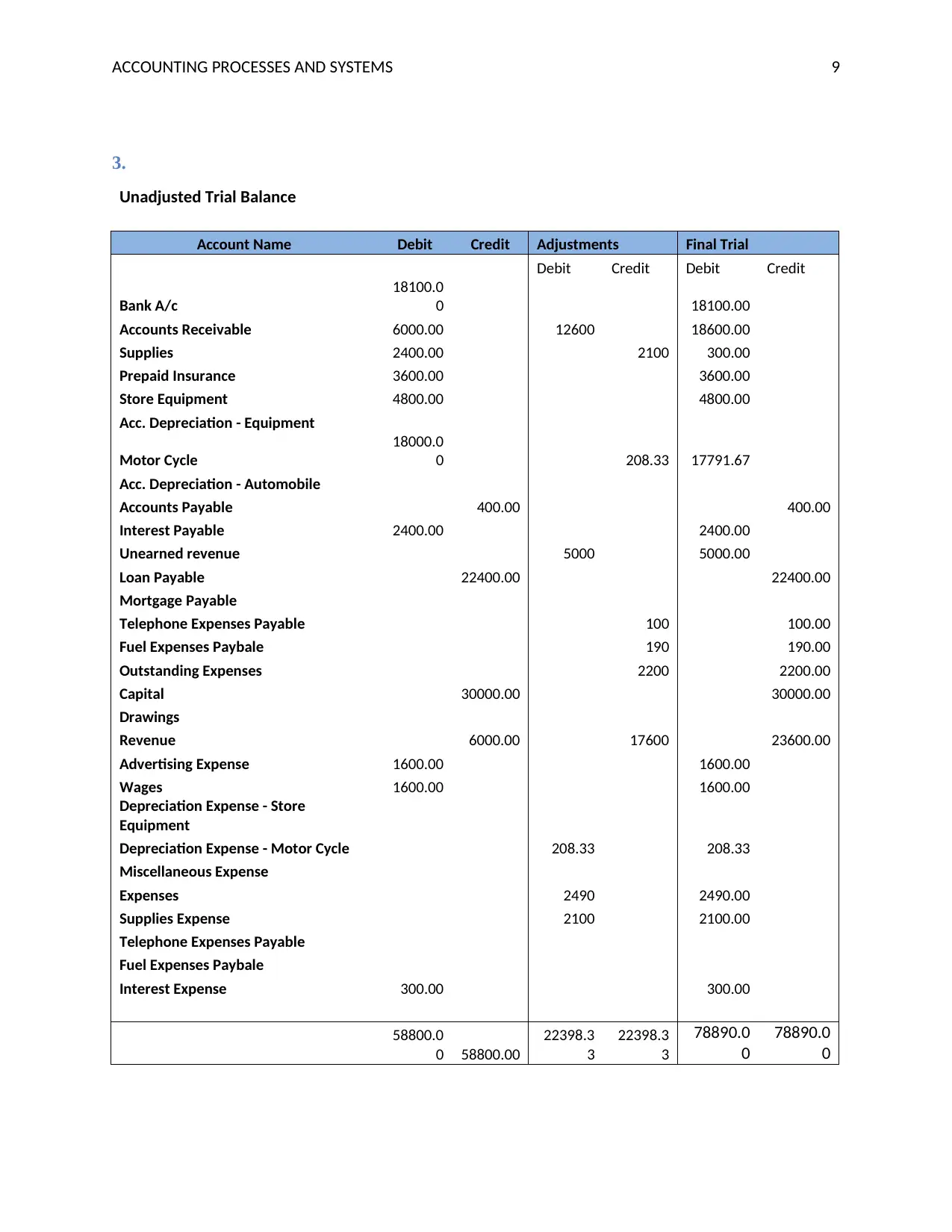

3.

Unadjusted Trial Balance

Account Name Debit Credit Adjustments Final Trial

Debit Credit Debit Credit

Bank A/c

18100.0

0 18100.00

Accounts Receivable 6000.00 12600 18600.00

Supplies 2400.00 2100 300.00

Prepaid Insurance 3600.00 3600.00

Store Equipment 4800.00 4800.00

Acc. Depreciation - Equipment

Motor Cycle

18000.0

0 208.33 17791.67

Acc. Depreciation - Automobile

Accounts Payable 400.00 400.00

Interest Payable 2400.00 2400.00

Unearned revenue 5000 5000.00

Loan Payable 22400.00 22400.00

Mortgage Payable

Telephone Expenses Payable 100 100.00

Fuel Expenses Paybale 190 190.00

Outstanding Expenses 2200 2200.00

Capital 30000.00 30000.00

Drawings

Revenue 6000.00 17600 23600.00

Advertising Expense 1600.00 1600.00

Wages 1600.00 1600.00

Depreciation Expense - Store

Equipment

Depreciation Expense - Motor Cycle 208.33 208.33

Miscellaneous Expense

Expenses 2490 2490.00

Supplies Expense 2100 2100.00

Telephone Expenses Payable

Fuel Expenses Paybale

Interest Expense 300.00 300.00

58800.0

0 58800.00

22398.3

3

22398.3

3

78890.0

0

78890.0

0

3.

Unadjusted Trial Balance

Account Name Debit Credit Adjustments Final Trial

Debit Credit Debit Credit

Bank A/c

18100.0

0 18100.00

Accounts Receivable 6000.00 12600 18600.00

Supplies 2400.00 2100 300.00

Prepaid Insurance 3600.00 3600.00

Store Equipment 4800.00 4800.00

Acc. Depreciation - Equipment

Motor Cycle

18000.0

0 208.33 17791.67

Acc. Depreciation - Automobile

Accounts Payable 400.00 400.00

Interest Payable 2400.00 2400.00

Unearned revenue 5000 5000.00

Loan Payable 22400.00 22400.00

Mortgage Payable

Telephone Expenses Payable 100 100.00

Fuel Expenses Paybale 190 190.00

Outstanding Expenses 2200 2200.00

Capital 30000.00 30000.00

Drawings

Revenue 6000.00 17600 23600.00

Advertising Expense 1600.00 1600.00

Wages 1600.00 1600.00

Depreciation Expense - Store

Equipment

Depreciation Expense - Motor Cycle 208.33 208.33

Miscellaneous Expense

Expenses 2490 2490.00

Supplies Expense 2100 2100.00

Telephone Expenses Payable

Fuel Expenses Paybale

Interest Expense 300.00 300.00

58800.0

0 58800.00

22398.3

3

22398.3

3

78890.0

0

78890.0

0

ACCOUNTING PROCESSES AND SYSTEMS 10

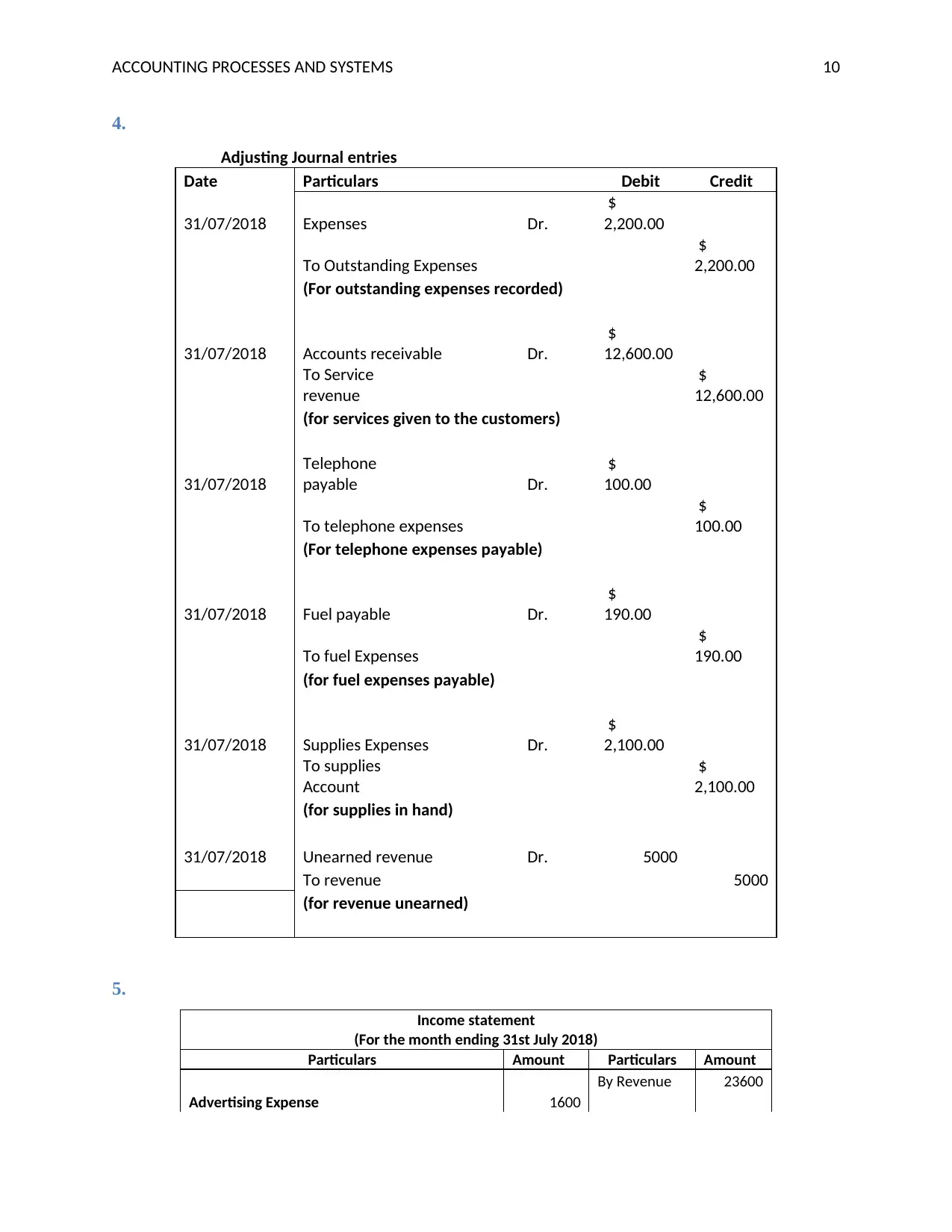

4.

Adjusting Journal entries

Date Particulars Debit Credit

31/07/2018 Expenses Dr.

$

2,200.00

To Outstanding Expenses

$

2,200.00

(For outstanding expenses recorded)

31/07/2018 Accounts receivable Dr.

$

12,600.00

To Service

revenue

$

12,600.00

(for services given to the customers)

31/07/2018

Telephone

payable Dr.

$

100.00

To telephone expenses

$

100.00

(For telephone expenses payable)

31/07/2018 Fuel payable Dr.

$

190.00

To fuel Expenses

$

190.00

(for fuel expenses payable)

31/07/2018 Supplies Expenses Dr.

$

2,100.00

To supplies

Account

$

2,100.00

(for supplies in hand)

31/07/2018 Unearned revenue Dr. 5000

To revenue 5000

(for revenue unearned)

5.

Income statement

(For the month ending 31st July 2018)

Particulars Amount Particulars Amount

By Revenue 23600

Advertising Expense 1600

4.

Adjusting Journal entries

Date Particulars Debit Credit

31/07/2018 Expenses Dr.

$

2,200.00

To Outstanding Expenses

$

2,200.00

(For outstanding expenses recorded)

31/07/2018 Accounts receivable Dr.

$

12,600.00

To Service

revenue

$

12,600.00

(for services given to the customers)

31/07/2018

Telephone

payable Dr.

$

100.00

To telephone expenses

$

100.00

(For telephone expenses payable)

31/07/2018 Fuel payable Dr.

$

190.00

To fuel Expenses

$

190.00

(for fuel expenses payable)

31/07/2018 Supplies Expenses Dr.

$

2,100.00

To supplies

Account

$

2,100.00

(for supplies in hand)

31/07/2018 Unearned revenue Dr. 5000

To revenue 5000

(for revenue unearned)

5.

Income statement

(For the month ending 31st July 2018)

Particulars Amount Particulars Amount

By Revenue 23600

Advertising Expense 1600

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING PROCESSES AND SYSTEMS 11

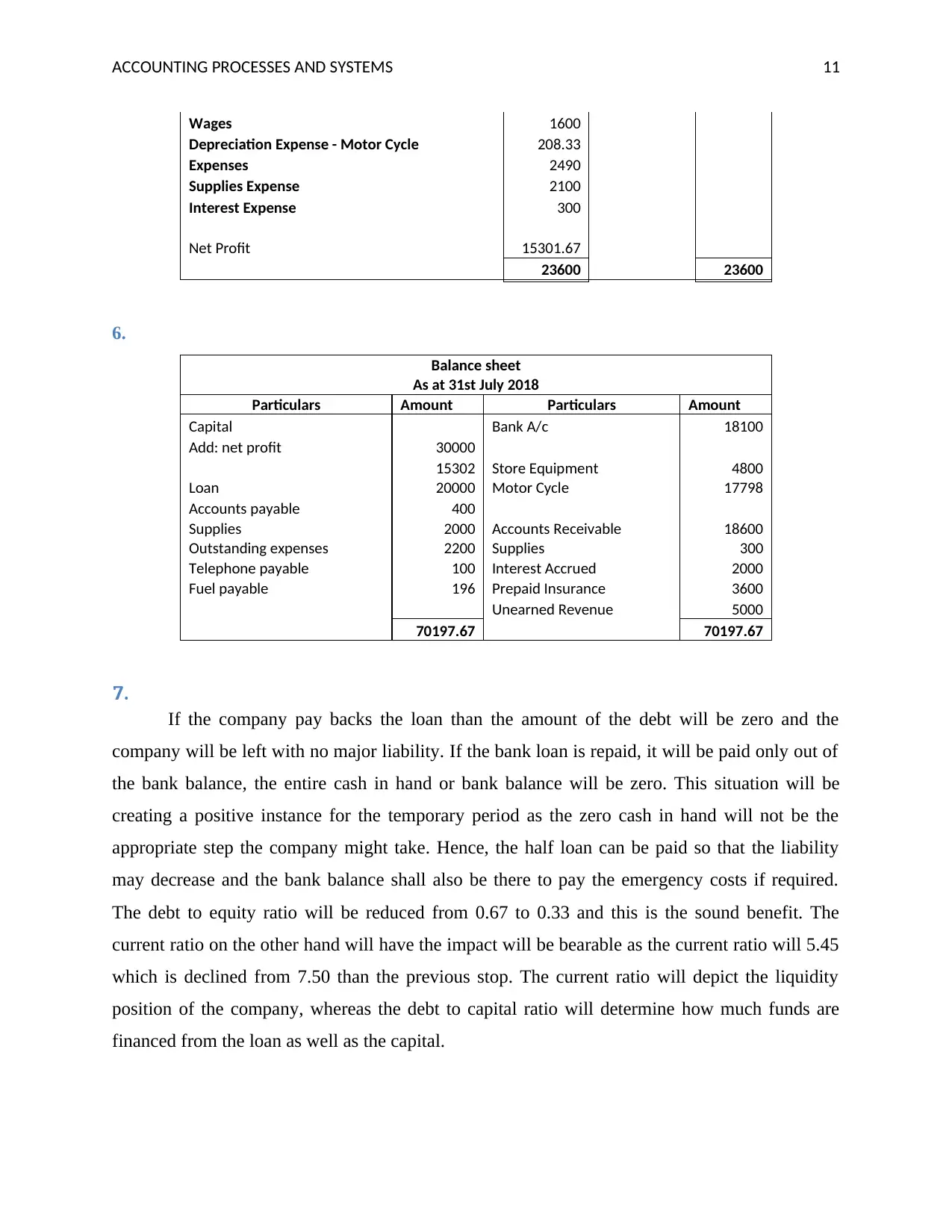

Wages 1600

Depreciation Expense - Motor Cycle 208.33

Expenses 2490

Supplies Expense 2100

Interest Expense 300

Net Profit 15301.67

23600 23600

6.

Balance sheet

As at 31st July 2018

Particulars Amount Particulars Amount

Capital Bank A/c 18100

Add: net profit 30000

15302 Store Equipment 4800

Loan 20000 Motor Cycle 17798

Accounts payable 400

Supplies 2000 Accounts Receivable 18600

Outstanding expenses 2200 Supplies 300

Telephone payable 100 Interest Accrued 2000

Fuel payable 196 Prepaid Insurance 3600

Unearned Revenue 5000

70197.67 70197.67

7.

If the company pay backs the loan than the amount of the debt will be zero and the

company will be left with no major liability. If the bank loan is repaid, it will be paid only out of

the bank balance, the entire cash in hand or bank balance will be zero. This situation will be

creating a positive instance for the temporary period as the zero cash in hand will not be the

appropriate step the company might take. Hence, the half loan can be paid so that the liability

may decrease and the bank balance shall also be there to pay the emergency costs if required.

The debt to equity ratio will be reduced from 0.67 to 0.33 and this is the sound benefit. The

current ratio on the other hand will have the impact will be bearable as the current ratio will 5.45

which is declined from 7.50 than the previous stop. The current ratio will depict the liquidity

position of the company, whereas the debt to capital ratio will determine how much funds are

financed from the loan as well as the capital.

Wages 1600

Depreciation Expense - Motor Cycle 208.33

Expenses 2490

Supplies Expense 2100

Interest Expense 300

Net Profit 15301.67

23600 23600

6.

Balance sheet

As at 31st July 2018

Particulars Amount Particulars Amount

Capital Bank A/c 18100

Add: net profit 30000

15302 Store Equipment 4800

Loan 20000 Motor Cycle 17798

Accounts payable 400

Supplies 2000 Accounts Receivable 18600

Outstanding expenses 2200 Supplies 300

Telephone payable 100 Interest Accrued 2000

Fuel payable 196 Prepaid Insurance 3600

Unearned Revenue 5000

70197.67 70197.67

7.

If the company pay backs the loan than the amount of the debt will be zero and the

company will be left with no major liability. If the bank loan is repaid, it will be paid only out of

the bank balance, the entire cash in hand or bank balance will be zero. This situation will be

creating a positive instance for the temporary period as the zero cash in hand will not be the

appropriate step the company might take. Hence, the half loan can be paid so that the liability

may decrease and the bank balance shall also be there to pay the emergency costs if required.

The debt to equity ratio will be reduced from 0.67 to 0.33 and this is the sound benefit. The

current ratio on the other hand will have the impact will be bearable as the current ratio will 5.45

which is declined from 7.50 than the previous stop. The current ratio will depict the liquidity

position of the company, whereas the debt to capital ratio will determine how much funds are

financed from the loan as well as the capital.

ACCOUNTING PROCESSES AND SYSTEMS 12

Question 2

Double entry bookkeeping is said to be a concept that is applicable and followed in all the

transactions in the account. According to this concept, all the accounting transactions have two

effects on the financial aspects of the business. The general ledger is used to record the two sides

of every transaction takes in an organization. It a business vends its services or products, the

revenue of the company increases and cash also increased by the same amount. The time a

business borrows some funds from its creditor, the cash balance of the company increased

however the debt balance of the business also increases with the same amount (Walshaw, 2018).

The system of double-entry results in creating a balance sheet comprised of equity,

liabilities, and assets. The sheet is said to be balanced since the assets of the company always

remain equal to liabilities plus equity. Assets of the company are comprised of a list of items

such as machinery, inventory, cash and intangible assets like patents. Liabilities of the company

highlights all the items that business owns to someone else, like long-term notes payable and

short term accounts payable. Equity highlights the stake of the owner in the business. Equity can

also be the owner's contribution to the business, plus profits or minus losses of the company.

Every entry possesses a credit side and a debit side that is recorded by the accountant of the

company in the general ledger (Bragg, 2011).

The double entry system book was first presented by Fra Luca Pacioli and Leonardo da

Vinci the Italian mathematicians. The book was published in the year 1994, with the title

“Summa de arithmetical, geometric, proportion et proportionality”. da Vinci and Pacioli do not

call themselves the inventors of this system but have discovered the way concepts can be utilized

in an effective and planned manner.

Da Vinci is responsible for drawing the practical examples and Pacioli is responsible for

writing text in order to assist in understanding the book. The book was separated into the diverse

segment and the part that illustrates double entry system was titled with the name “Particularis de

computis et scripturis”. The book was further separated into different small sections or chapters

that recite about trial balance, income statement, double entry, balance sheet, journals, and

different techniques and tools successively accepted by a number of traders and accountants.

Question 2

Double entry bookkeeping is said to be a concept that is applicable and followed in all the

transactions in the account. According to this concept, all the accounting transactions have two

effects on the financial aspects of the business. The general ledger is used to record the two sides

of every transaction takes in an organization. It a business vends its services or products, the

revenue of the company increases and cash also increased by the same amount. The time a

business borrows some funds from its creditor, the cash balance of the company increased

however the debt balance of the business also increases with the same amount (Walshaw, 2018).

The system of double-entry results in creating a balance sheet comprised of equity,

liabilities, and assets. The sheet is said to be balanced since the assets of the company always

remain equal to liabilities plus equity. Assets of the company are comprised of a list of items

such as machinery, inventory, cash and intangible assets like patents. Liabilities of the company

highlights all the items that business owns to someone else, like long-term notes payable and

short term accounts payable. Equity highlights the stake of the owner in the business. Equity can

also be the owner's contribution to the business, plus profits or minus losses of the company.

Every entry possesses a credit side and a debit side that is recorded by the accountant of the

company in the general ledger (Bragg, 2011).

The double entry system book was first presented by Fra Luca Pacioli and Leonardo da

Vinci the Italian mathematicians. The book was published in the year 1994, with the title

“Summa de arithmetical, geometric, proportion et proportionality”. da Vinci and Pacioli do not

call themselves the inventors of this system but have discovered the way concepts can be utilized

in an effective and planned manner.

Da Vinci is responsible for drawing the practical examples and Pacioli is responsible for

writing text in order to assist in understanding the book. The book was separated into the diverse

segment and the part that illustrates double entry system was titled with the name “Particularis de

computis et scripturis”. The book was further separated into different small sections or chapters

that recite about trial balance, income statement, double entry, balance sheet, journals, and

different techniques and tools successively accepted by a number of traders and accountants.

ACCOUNTING PROCESSES AND SYSTEMS 13

Importance of Double Entry Bookkeeping

It is very important to keep a precise financial system; therefore companies make use of

double entry system since it assists in precise financial reporting and eliminates errors and

dishonest activity. Some of the ways double entry system is important for the businesses are:

Accuracy – Double entry booking system offers more precise information regarding the financial

position of the company in comparison to the single-entry system. The main reason for this is

because the double entry system adheres to the matching principle of accounting. The matching

principle follows accrual accounting guidelines in order to record revenue and expenses linked to

the revenue. Maintaining the record of revenue and expenses offers a precise calculation of

losses and profits (Jeffrey, 2018).

Error Reduction – Human errors can result in a misrepresentation of the financial position of the

company. Double entry system eliminates the chances of errors as it includes balances and

checks. With the technology advancement, a number of software programs for accounting

mechanically offer double-entry bookkeeping the time an accounting event or transaction is

entered. It eliminated the chances of wrongly posting of any transaction in the wrong offsetting

account (Hussey, 2014). Errors could be simply trapped with double entry system by enduring an

equal amount of debit and credit side.

Preparation of the Financial Statements - Financial statements can be easily presented in the

organization with the help of the double-entry bookkeeping system since information is collected

straight from the transaction of the double entry booking. It is essential for businesses to create a

precise, efficient, and quick financial statement. Users of the internet like management of the

company rely on the financial statements in order to identify where the company stands in

financial terms and to prepare operational budgets. External users, like vendors, investors

majorly rely on financial statements in order to define the creditworthiness of the company.

Leaves an Audit Trail – Double-entry system of bookkeeping eliminated the chances of

fraudulent activities by leaving an adult trail. The audit trail permits business to track the journal

entries transactions that are posted in the general ledger. For instance, when the cash balance of

the business in the balance sheet appears to be going high, then the department of the company

can trace back all the transactions done in the cash account and check the accuracy (Johnson,

Importance of Double Entry Bookkeeping

It is very important to keep a precise financial system; therefore companies make use of

double entry system since it assists in precise financial reporting and eliminates errors and

dishonest activity. Some of the ways double entry system is important for the businesses are:

Accuracy – Double entry booking system offers more precise information regarding the financial

position of the company in comparison to the single-entry system. The main reason for this is

because the double entry system adheres to the matching principle of accounting. The matching

principle follows accrual accounting guidelines in order to record revenue and expenses linked to

the revenue. Maintaining the record of revenue and expenses offers a precise calculation of

losses and profits (Jeffrey, 2018).

Error Reduction – Human errors can result in a misrepresentation of the financial position of the

company. Double entry system eliminates the chances of errors as it includes balances and

checks. With the technology advancement, a number of software programs for accounting

mechanically offer double-entry bookkeeping the time an accounting event or transaction is

entered. It eliminated the chances of wrongly posting of any transaction in the wrong offsetting

account (Hussey, 2014). Errors could be simply trapped with double entry system by enduring an

equal amount of debit and credit side.

Preparation of the Financial Statements - Financial statements can be easily presented in the

organization with the help of the double-entry bookkeeping system since information is collected

straight from the transaction of the double entry booking. It is essential for businesses to create a

precise, efficient, and quick financial statement. Users of the internet like management of the

company rely on the financial statements in order to identify where the company stands in

financial terms and to prepare operational budgets. External users, like vendors, investors

majorly rely on financial statements in order to define the creditworthiness of the company.

Leaves an Audit Trail – Double-entry system of bookkeeping eliminated the chances of

fraudulent activities by leaving an adult trail. The audit trail permits business to track the journal

entries transactions that are posted in the general ledger. For instance, when the cash balance of

the business in the balance sheet appears to be going high, then the department of the company

can trace back all the transactions done in the cash account and check the accuracy (Johnson,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING PROCESSES AND SYSTEMS 14

2019). The business can get precise information about which account is influenced by posting

the transactions. Double entry system makes use of reference numbers and present short

descriptions with all the entry.

Cost Control – Double entry system maintains comprehensive information about the financial

transaction of the business. Hence, the financial transaction recording in the books offers

important data or information for controlling the cost.

Difference between Double Entry Bookkeeping and Single Entry System (Conventional Methos)

Single entry bookkeeping system is inexpensive however it is not scientific since it does

not maintain the records of every transaction in its place it maintains the record of limited

transactions and few of them are recorded incompletely. On the other side, double entry

bookkeeping system is dependent on necessary accounting principles and therefore it keeps the

records of all transaction aspects (Suntook, 2010).

Basis Double-Entry Bookkeeping

System

Single-Entry Bookkeeping

System (Conventional

method)

Meaning Under this system, all the

transactions affect two

accounts at the same time.

Under this system, only

single sided entry is needed

in order to record the

transactions (Surbhi, 2015)

Recording Complete Incomplete

Ledger Nominal, real, and personal

account

Cash and personal account

Suitability for tax Yes No

Nature Complex Simple

Errors Simple to locate Difficult to locate

Preferred by Big organizations Small businesses

Accuracy Guaranteed arithmetical

precision

Unsure arithmetical precision

Number of accounts Subsidiary books, journals, Cash book and ledger

2019). The business can get precise information about which account is influenced by posting

the transactions. Double entry system makes use of reference numbers and present short

descriptions with all the entry.

Cost Control – Double entry system maintains comprehensive information about the financial

transaction of the business. Hence, the financial transaction recording in the books offers

important data or information for controlling the cost.

Difference between Double Entry Bookkeeping and Single Entry System (Conventional Methos)

Single entry bookkeeping system is inexpensive however it is not scientific since it does

not maintain the records of every transaction in its place it maintains the record of limited

transactions and few of them are recorded incompletely. On the other side, double entry

bookkeeping system is dependent on necessary accounting principles and therefore it keeps the

records of all transaction aspects (Suntook, 2010).

Basis Double-Entry Bookkeeping

System

Single-Entry Bookkeeping

System (Conventional

method)

Meaning Under this system, all the

transactions affect two

accounts at the same time.

Under this system, only

single sided entry is needed

in order to record the

transactions (Surbhi, 2015)

Recording Complete Incomplete

Ledger Nominal, real, and personal

account

Cash and personal account

Suitability for tax Yes No

Nature Complex Simple

Errors Simple to locate Difficult to locate

Preferred by Big organizations Small businesses

Accuracy Guaranteed arithmetical

precision

Unsure arithmetical precision

Number of accounts Subsidiary books, journals, Cash book and ledger

ACCOUNTING PROCESSES AND SYSTEMS 15

and ledger

Coverage Detailed information is

covered under double entry

bookkeeping system

Cover limited details

Question 3

1.

ABC learning is considered as one of the most renowned and the established institute of

learning, by far the largest chain of the corporate child care in Australia. Though it was

established in the year 1988, yet the company has experienced a rapid growth in recent years.

There are several reasons for the failure of the ABC Learning and some of them have been listed

below (Neelon, Mayhew, O’Neill, Neelon & Pate, 2016).

First to record the failure the company was performing well enough, when in March

2006, its market capitalization reached A$2.5 billion in the year 2007 and it reported a net profit

after tax of A$143.1 million and revenues of A$ 1.7 billion. Thereafter the entire scenario

changed for the company when peer shaped. ABC was overwhelmed by its debts and had to sell

almost 60% of the US subsidiary. The last traded price recorded was A$0.54. The several issues

have been bifurcated on the basis of accounting issues, related party transactions, and damages

on liquidation, operating at opaque level (Kruger, 2009).

Accounting issues

The major accounting issue for the ABC was the valuation of the assets which became

difficult for the auditors to value at times. Without any doubt there have been fundamental flaws

in keeping and recording the accounting transactions correctly. There seems to be the different

level of the discrepancies in the profits, revenues and the pretax earnings were inconclusive.

ABC’s external auditors, Pitcher Partners are, gave unqualified opinions since the year 2003 and

the management took no action and they resigned. Thereafter when the company appointed new

auditors E & Y, stated that the accounts were highly manipulated and that there was a deep need

to reinstate the accounts (Islam, 2017).

and ledger

Coverage Detailed information is

covered under double entry

bookkeeping system

Cover limited details

Question 3

1.

ABC learning is considered as one of the most renowned and the established institute of

learning, by far the largest chain of the corporate child care in Australia. Though it was

established in the year 1988, yet the company has experienced a rapid growth in recent years.

There are several reasons for the failure of the ABC Learning and some of them have been listed

below (Neelon, Mayhew, O’Neill, Neelon & Pate, 2016).

First to record the failure the company was performing well enough, when in March

2006, its market capitalization reached A$2.5 billion in the year 2007 and it reported a net profit

after tax of A$143.1 million and revenues of A$ 1.7 billion. Thereafter the entire scenario

changed for the company when peer shaped. ABC was overwhelmed by its debts and had to sell

almost 60% of the US subsidiary. The last traded price recorded was A$0.54. The several issues

have been bifurcated on the basis of accounting issues, related party transactions, and damages

on liquidation, operating at opaque level (Kruger, 2009).

Accounting issues

The major accounting issue for the ABC was the valuation of the assets which became

difficult for the auditors to value at times. Without any doubt there have been fundamental flaws

in keeping and recording the accounting transactions correctly. There seems to be the different

level of the discrepancies in the profits, revenues and the pretax earnings were inconclusive.

ABC’s external auditors, Pitcher Partners are, gave unqualified opinions since the year 2003 and

the management took no action and they resigned. Thereafter when the company appointed new

auditors E & Y, stated that the accounts were highly manipulated and that there was a deep need

to reinstate the accounts (Islam, 2017).

ACCOUNTING PROCESSES AND SYSTEMS 16

Related party Transactions

After doing the investigations in depth, it was found that after the E and Y was being

appointed the CEO of the company, Mr Eddy Groves appointed Queensland Maintenance

Services, the company which belonged to his former brother in law Frank Zullo for $74 million.

The related party transactions also played a vital role in making the situations worse. Payments

from several developers that subsidized loss-making centers through the funds - and hid the basic

fact that the loss was faced whereas in return the situation was equally reversed and the money

was right below their fists (O’Neill, Dowda, Benjamin Neelon, Neelon & Pate, 2017).

Opaque Operations

Furthermore, the business operations of the ABC, Learning was not transparent either.

The main issue was also related to the policies and the guidelines that were not clear and the

division was also in vain. The costs that were allocated with each center were also opaque in

nature and therefore it was one of the non-feasible matters which created havoc for the ABC

learning. This way the performance of the each center also went down and this eventually led to

a fall in the entire ABC centre (Governance for stakeholders, 2012).

Poor strategic planning and expansion

There were rapid international expansions made by the company and this did make the

company as one of the high levered company. The company also crossed the international

boundaries and took over many daycare and child care providers in New Zealand, USA and UK.

At this moment the company was having huge loan and the loans were raised to such an extent

that the company could not repay those. Also the debt raised when the ABC opted the multi

option facility for A$1.48 million and due to this the profit fell by 42% and the covenants of the

debt amounted to A$1.2 billion were also breached (Youtube, 2018).

2.

Ethical issues

The first ethical issue faced by the company was the payment of the low wages to the

employees and which incur the low cost and generate more profits for the organization. To

capturing the market share, settle rivals and the profits, ABC employees were giving the low rate

of wages. Also in 2004, ABC was found guilty in paying the low wages which are not even in

Related party Transactions

After doing the investigations in depth, it was found that after the E and Y was being

appointed the CEO of the company, Mr Eddy Groves appointed Queensland Maintenance

Services, the company which belonged to his former brother in law Frank Zullo for $74 million.

The related party transactions also played a vital role in making the situations worse. Payments

from several developers that subsidized loss-making centers through the funds - and hid the basic

fact that the loss was faced whereas in return the situation was equally reversed and the money

was right below their fists (O’Neill, Dowda, Benjamin Neelon, Neelon & Pate, 2017).

Opaque Operations

Furthermore, the business operations of the ABC, Learning was not transparent either.

The main issue was also related to the policies and the guidelines that were not clear and the

division was also in vain. The costs that were allocated with each center were also opaque in

nature and therefore it was one of the non-feasible matters which created havoc for the ABC

learning. This way the performance of the each center also went down and this eventually led to

a fall in the entire ABC centre (Governance for stakeholders, 2012).

Poor strategic planning and expansion

There were rapid international expansions made by the company and this did make the

company as one of the high levered company. The company also crossed the international

boundaries and took over many daycare and child care providers in New Zealand, USA and UK.

At this moment the company was having huge loan and the loans were raised to such an extent

that the company could not repay those. Also the debt raised when the ABC opted the multi

option facility for A$1.48 million and due to this the profit fell by 42% and the covenants of the

debt amounted to A$1.2 billion were also breached (Youtube, 2018).

2.

Ethical issues

The first ethical issue faced by the company was the payment of the low wages to the

employees and which incur the low cost and generate more profits for the organization. To

capturing the market share, settle rivals and the profits, ABC employees were giving the low rate

of wages. Also in 2004, ABC was found guilty in paying the low wages which are not even in

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING PROCESSES AND SYSTEMS 17

alignment with the Australian accounting standards. The worst case scenario was when the ABC

learning forced the employees to cleanse the toilets and purchase the regular uniform on its own

(Youtube, 2018).

The second issue that has been faced by the company was the misstating of the reports by

the auditors of the company. The cash flows and the misappropriation in financial statements

were the major reasons for the collapse and also for the ethical issues faced by the company. The

company was involved with the men such as politicians who have no idea about the child care

industry. They are not having any idea of how to read and analyze the financial statements.

Lastly the valuation of the assets was not proper and no other methods were chosen to

overcome the problem. In child care center the infrastructure plays a vital and the crucial role in

determining the ethical decisions. The open field, the sleeping rooms, the dining area, bathrooms

for the toddlers, developmental toys were not able to be valued because the purchase was in bulk

and some of them were being used for the personal use. Further at the beginning of the year

2006/7 financial year, there was A$37.4 million in goodwill and A$647.6 million in child care.

Goodwill rose to A$271 million and licenses to A$2.4 billion by the end of the financial year

2007/08. The impairment charges were so high that the intangibles were becoming worthless.

Also the inherent risk associated with the valuation of the assets tends to be more enormous.

This situation was counted as the red flag (Islam, 2017).

alignment with the Australian accounting standards. The worst case scenario was when the ABC

learning forced the employees to cleanse the toilets and purchase the regular uniform on its own

(Youtube, 2018).

The second issue that has been faced by the company was the misstating of the reports by

the auditors of the company. The cash flows and the misappropriation in financial statements

were the major reasons for the collapse and also for the ethical issues faced by the company. The

company was involved with the men such as politicians who have no idea about the child care

industry. They are not having any idea of how to read and analyze the financial statements.

Lastly the valuation of the assets was not proper and no other methods were chosen to

overcome the problem. In child care center the infrastructure plays a vital and the crucial role in

determining the ethical decisions. The open field, the sleeping rooms, the dining area, bathrooms

for the toddlers, developmental toys were not able to be valued because the purchase was in bulk

and some of them were being used for the personal use. Further at the beginning of the year

2006/7 financial year, there was A$37.4 million in goodwill and A$647.6 million in child care.

Goodwill rose to A$271 million and licenses to A$2.4 billion by the end of the financial year

2007/08. The impairment charges were so high that the intangibles were becoming worthless.

Also the inherent risk associated with the valuation of the assets tends to be more enormous.

This situation was counted as the red flag (Islam, 2017).

ACCOUNTING PROCESSES AND SYSTEMS 18

References

Bragg, S.M. (2011). Bookkeeping Essentials: How to Succeed as a Bookkeeper 1st ed. U.K: John

Wiley & Sons.

Governance for stakeholders, (2012). The ABC of a corporate collapse. Retrieved from

https://governanceforstakeholders.com/2012/12/28/the-abc-of-a-corporate-collapse/

Hussey, R. (2014). MBA Accounting 1st ed. U.K: Macmillan International Higher Education.

Islam, (2017). ABC Learning :: Collapse of an Entrepreneurial Venture. Retrieved from

http://dspace.bracu.ac.bd/xmlui/bitstream/handle/10361/9144/12164006.pdf?

sequence=1&isAllowed=y

Jeffrey, J. (2018). Research on Professional Responsibility and Ethics in Accounting 1st ed. U.K:

Emerald Group Publishing.

Johnson, R. (2019). The Importance of Double-Entry Bookkeeping. Retrieved from

https://bizfluent.com/info-8691783-importance-doubleentry-bookkeeping.html

Kruger, C. (2009). Lessons to be learnt from ABC Learning's collapse. Retrieved from

https://www.smh.com.au/business/lessons-to-be-learnt-from-abc-learnings-collapse-20090101-

78f8.html

Neelon, S. E. B., Mayhew, M., O’Neill, J. R., Neelon, B., Li, F., & Pate, R. R. (2016).

Comparative evaluation of a South Carolina policy to improve nutrition in child care. Journal of

the Academy of Nutrition and Dietetics, 116(6), 949-956.

O’Neill, J. R., Dowda, M., Benjamin Neelon, S. E., Neelon, B., & Pate, R. R. (2017). Effects of a

new state policy on physical activity practices in child care centers in South Carolina. American

journal of public health, 107(1), 144-146.

Suntook, Z. (2010). Learning Accountancy: The Novel Way 1st ed. U.S: Cambridge Scholars

Publishing.

References

Bragg, S.M. (2011). Bookkeeping Essentials: How to Succeed as a Bookkeeper 1st ed. U.K: John

Wiley & Sons.

Governance for stakeholders, (2012). The ABC of a corporate collapse. Retrieved from

https://governanceforstakeholders.com/2012/12/28/the-abc-of-a-corporate-collapse/

Hussey, R. (2014). MBA Accounting 1st ed. U.K: Macmillan International Higher Education.

Islam, (2017). ABC Learning :: Collapse of an Entrepreneurial Venture. Retrieved from

http://dspace.bracu.ac.bd/xmlui/bitstream/handle/10361/9144/12164006.pdf?

sequence=1&isAllowed=y

Jeffrey, J. (2018). Research on Professional Responsibility and Ethics in Accounting 1st ed. U.K:

Emerald Group Publishing.

Johnson, R. (2019). The Importance of Double-Entry Bookkeeping. Retrieved from

https://bizfluent.com/info-8691783-importance-doubleentry-bookkeeping.html

Kruger, C. (2009). Lessons to be learnt from ABC Learning's collapse. Retrieved from

https://www.smh.com.au/business/lessons-to-be-learnt-from-abc-learnings-collapse-20090101-

78f8.html

Neelon, S. E. B., Mayhew, M., O’Neill, J. R., Neelon, B., Li, F., & Pate, R. R. (2016).

Comparative evaluation of a South Carolina policy to improve nutrition in child care. Journal of

the Academy of Nutrition and Dietetics, 116(6), 949-956.

O’Neill, J. R., Dowda, M., Benjamin Neelon, S. E., Neelon, B., & Pate, R. R. (2017). Effects of a

new state policy on physical activity practices in child care centers in South Carolina. American

journal of public health, 107(1), 144-146.

Suntook, Z. (2010). Learning Accountancy: The Novel Way 1st ed. U.S: Cambridge Scholars

Publishing.

ACCOUNTING PROCESSES AND SYSTEMS 19

Surbhi, S. (2015). Difference Between Single Entry System and Double Entry System. Retrieved

from https://keydifferences.com/difference-between-single-entry-system-and-double-entry-

system.html

Walshaw, T. (2018). Double Entry Bookkeeping 2nd ed. U.S: Lulu.com.

Youtube, (2018). The ABC of a Corporate Collapse - Chapter 1 Foundations and Growth.

Retrieved from https://www.youtube.com/watch?

v=YYF6JW9vJKo&list=PL12C0ADD577F6B741&index=2&t=0s

Youtube, (2018). The ABC of a Corporate Collapse - Chapter 3 (part 1) The Balance Sheet.

Retrieved from https://www.youtube.com/watch?

v=sMZExHXNlJQ&list=PL12C0ADD577F6B741&index=3

Surbhi, S. (2015). Difference Between Single Entry System and Double Entry System. Retrieved

from https://keydifferences.com/difference-between-single-entry-system-and-double-entry-

system.html

Walshaw, T. (2018). Double Entry Bookkeeping 2nd ed. U.S: Lulu.com.

Youtube, (2018). The ABC of a Corporate Collapse - Chapter 1 Foundations and Growth.

Retrieved from https://www.youtube.com/watch?

v=YYF6JW9vJKo&list=PL12C0ADD577F6B741&index=2&t=0s

Youtube, (2018). The ABC of a Corporate Collapse - Chapter 3 (part 1) The Balance Sheet.

Retrieved from https://www.youtube.com/watch?

v=sMZExHXNlJQ&list=PL12C0ADD577F6B741&index=3

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.