Comprehensive Financial Analysis Report: Cherry Hotels Ltd Performance

VerifiedAdded on 2023/01/04

|12

|2596

|81

Report

AI Summary

This report presents a financial analysis of Cherry Hotels Ltd, encompassing an income statement, statement of financial position, and key ratio analysis. Task 1 involves preparing financial statements from a trial balance, including adjustments for depreciation, prepaid rent, and provisions for bad debts. Task 2 delves into the calculation and interpretation of Return on Capital Employed (ROCE), Acid Test Ratio, and Cash Operating Cycle for the years 2018, 2019, and 2020. The report provides insights into the company's profitability, liquidity, and efficiency, highlighting trends and implications of the financial data.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................5

References......................................................................................................................................12

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................5

References......................................................................................................................................12

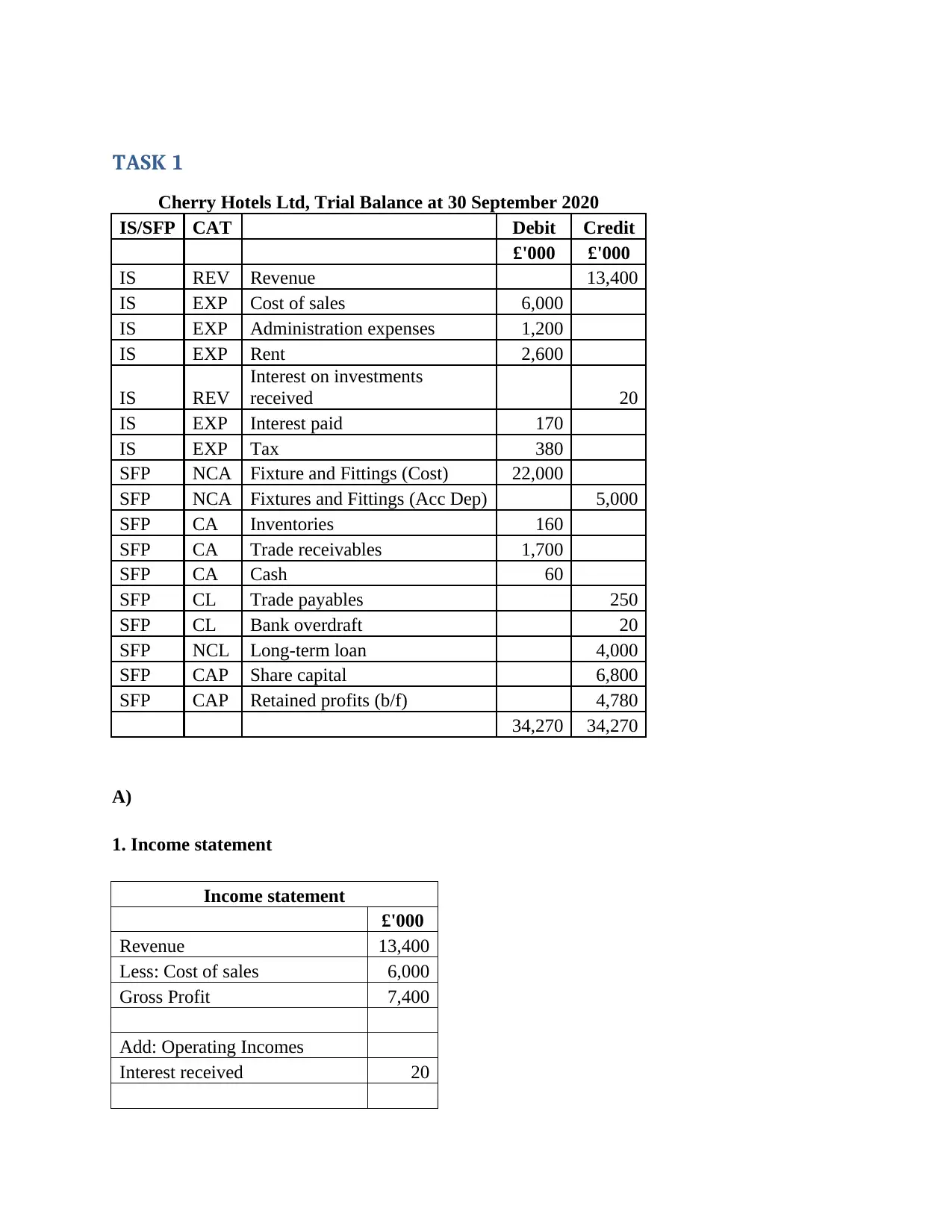

TASK 1

Cherry Hotels Ltd, Trial Balance at 30 September 2020

IS/SFP CAT Debit Credit

£'000 £'000

IS REV Revenue 13,400

IS EXP Cost of sales 6,000

IS EXP Administration expenses 1,200

IS EXP Rent 2,600

IS REV

Interest on investments

received 20

IS EXP Interest paid 170

IS EXP Tax 380

SFP NCA Fixture and Fittings (Cost) 22,000

SFP NCA Fixtures and Fittings (Acc Dep) 5,000

SFP CA Inventories 160

SFP CA Trade receivables 1,700

SFP CA Cash 60

SFP CL Trade payables 250

SFP CL Bank overdraft 20

SFP NCL Long-term loan 4,000

SFP CAP Share capital 6,800

SFP CAP Retained profits (b/f) 4,780

34,270 34,270

A)

1. Income statement

Income statement

£'000

Revenue 13,400

Less: Cost of sales 6,000

Gross Profit 7,400

Add: Operating Incomes

Interest received 20

Cherry Hotels Ltd, Trial Balance at 30 September 2020

IS/SFP CAT Debit Credit

£'000 £'000

IS REV Revenue 13,400

IS EXP Cost of sales 6,000

IS EXP Administration expenses 1,200

IS EXP Rent 2,600

IS REV

Interest on investments

received 20

IS EXP Interest paid 170

IS EXP Tax 380

SFP NCA Fixture and Fittings (Cost) 22,000

SFP NCA Fixtures and Fittings (Acc Dep) 5,000

SFP CA Inventories 160

SFP CA Trade receivables 1,700

SFP CA Cash 60

SFP CL Trade payables 250

SFP CL Bank overdraft 20

SFP NCL Long-term loan 4,000

SFP CAP Share capital 6,800

SFP CAP Retained profits (b/f) 4,780

34,270 34,270

A)

1. Income statement

Income statement

£'000

Revenue 13,400

Less: Cost of sales 6,000

Gross Profit 7,400

Add: Operating Incomes

Interest received 20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Operating expenses

Administration expenses 965

Electricity 235

Depreciation 2,000

Rent 2,600

Less: Prepaid rent 350 2,250

Interest paid 170

Bad debts 200

Provision for Doubtful debts 30

Net Profit before tax 1,570

Less: Income tax 380

Net Profit after tax 1,190

Add: Depreciation 2,000

Net Profit after Depreciation 3,190

2. Statement of financial position

Financial Position

£'000 £'000

Assets

Non Current Assets

Fixture and Fittings 22,000

Less: Accumulated dep. 7,000 15,000

Current Assets

Inventories 160

Trade receivables 1,700

Less: Bad debts 200

Less: Provision for doubtful debts 30 1,470

Cash 60

Prepaid rent 205 1,895

Total Assets 16,895

Owner's equities and liabilities

Equity:

Share Capital 6,800

Add: Retained Profits 4,780

Add: Net Profit after tax 1,045 12,625

Administration expenses 965

Electricity 235

Depreciation 2,000

Rent 2,600

Less: Prepaid rent 350 2,250

Interest paid 170

Bad debts 200

Provision for Doubtful debts 30

Net Profit before tax 1,570

Less: Income tax 380

Net Profit after tax 1,190

Add: Depreciation 2,000

Net Profit after Depreciation 3,190

2. Statement of financial position

Financial Position

£'000 £'000

Assets

Non Current Assets

Fixture and Fittings 22,000

Less: Accumulated dep. 7,000 15,000

Current Assets

Inventories 160

Trade receivables 1,700

Less: Bad debts 200

Less: Provision for doubtful debts 30 1,470

Cash 60

Prepaid rent 205 1,895

Total Assets 16,895

Owner's equities and liabilities

Equity:

Share Capital 6,800

Add: Retained Profits 4,780

Add: Net Profit after tax 1,045 12,625

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

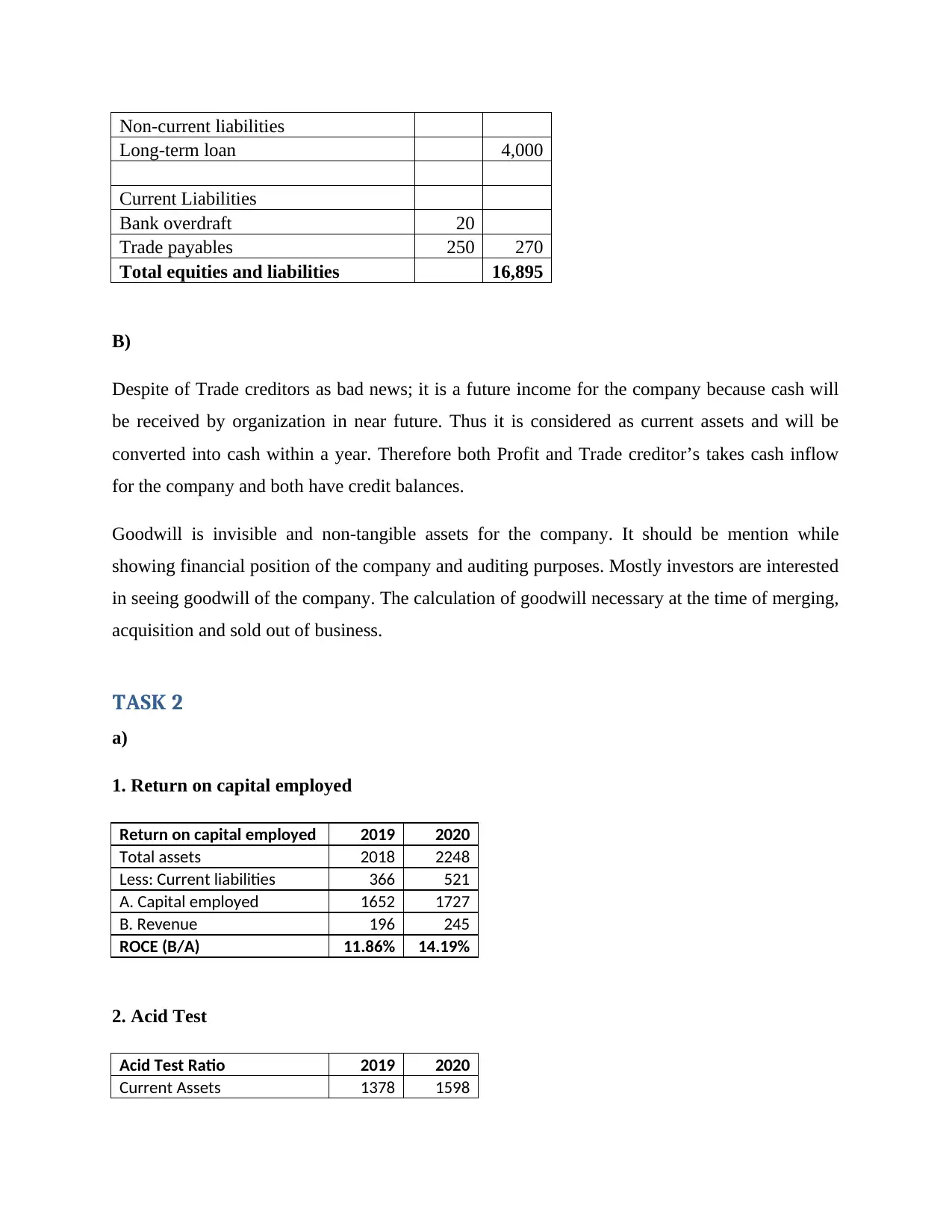

Non-current liabilities

Long-term loan 4,000

Current Liabilities

Bank overdraft 20

Trade payables 250 270

Total equities and liabilities 16,895

B)

Despite of Trade creditors as bad news; it is a future income for the company because cash will

be received by organization in near future. Thus it is considered as current assets and will be

converted into cash within a year. Therefore both Profit and Trade creditor’s takes cash inflow

for the company and both have credit balances.

Goodwill is invisible and non-tangible assets for the company. It should be mention while

showing financial position of the company and auditing purposes. Mostly investors are interested

in seeing goodwill of the company. The calculation of goodwill necessary at the time of merging,

acquisition and sold out of business.

TASK 2

a)

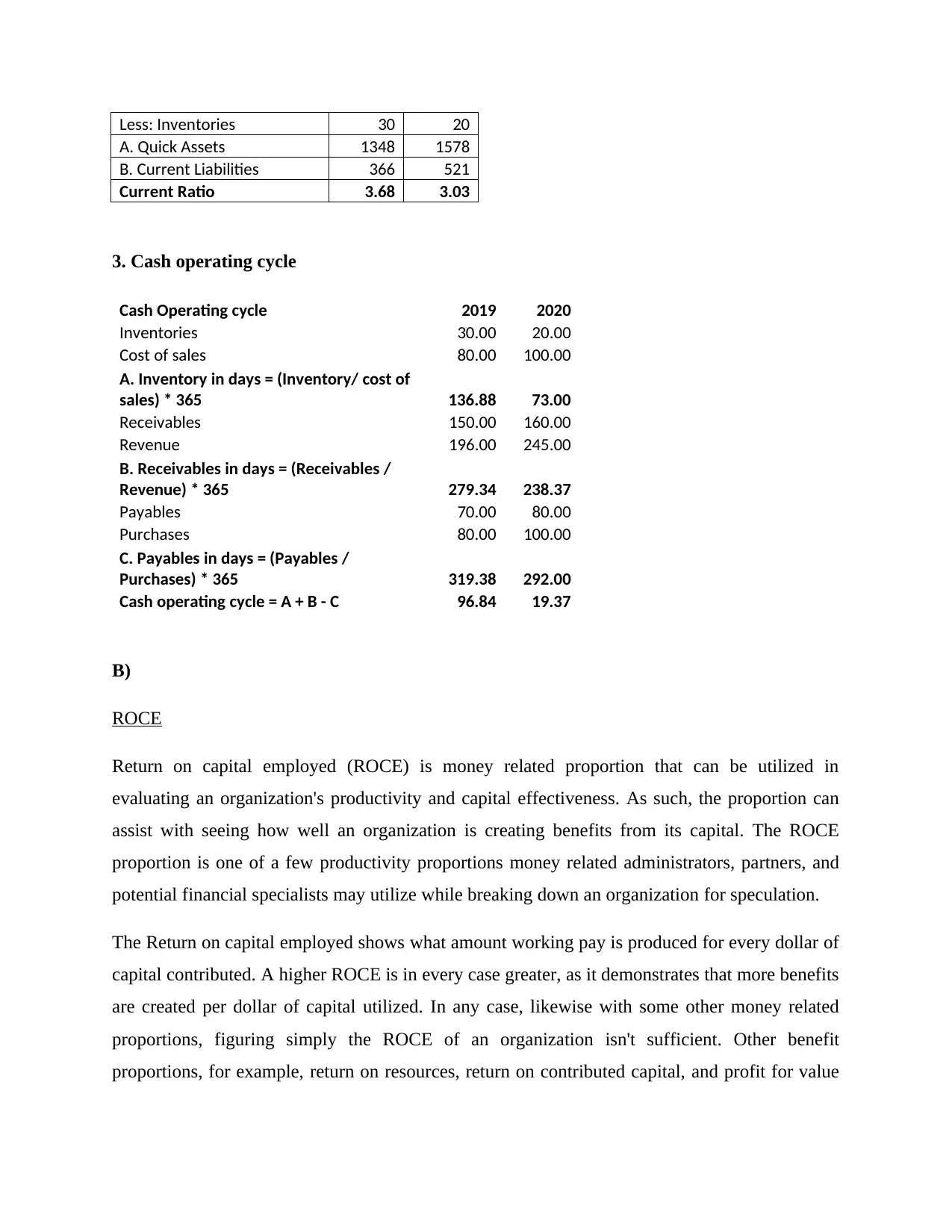

1. Return on capital employed

Return on capital employed 2019 2020

Total assets 2018 2248

Less: Current liabilities 366 521

A. Capital employed 1652 1727

B. Revenue 196 245

ROCE (B/A) 11.86% 14.19%

2. Acid Test

Acid Test Ratio 2019 2020

Current Assets 1378 1598

Long-term loan 4,000

Current Liabilities

Bank overdraft 20

Trade payables 250 270

Total equities and liabilities 16,895

B)

Despite of Trade creditors as bad news; it is a future income for the company because cash will

be received by organization in near future. Thus it is considered as current assets and will be

converted into cash within a year. Therefore both Profit and Trade creditor’s takes cash inflow

for the company and both have credit balances.

Goodwill is invisible and non-tangible assets for the company. It should be mention while

showing financial position of the company and auditing purposes. Mostly investors are interested

in seeing goodwill of the company. The calculation of goodwill necessary at the time of merging,

acquisition and sold out of business.

TASK 2

a)

1. Return on capital employed

Return on capital employed 2019 2020

Total assets 2018 2248

Less: Current liabilities 366 521

A. Capital employed 1652 1727

B. Revenue 196 245

ROCE (B/A) 11.86% 14.19%

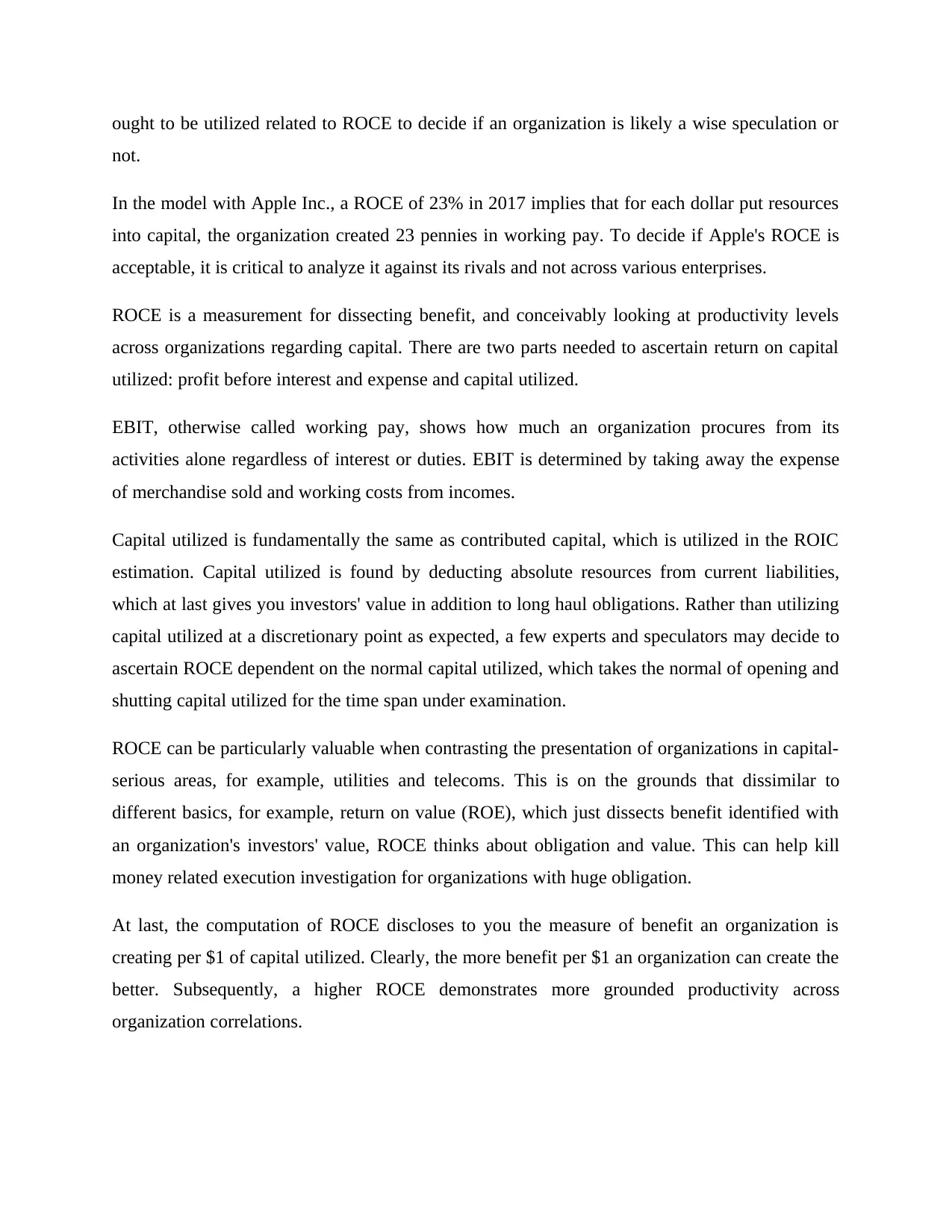

2. Acid Test

Acid Test Ratio 2019 2020

Current Assets 1378 1598

Less: Inventories 30 20

A. Quick Assets 1348 1578

B. Current Liabilities 366 521

Current Ratio 3.68 3.03

3. Cash operating cycle

Cash Operating cycle 2019 2020

Inventories 30.00 20.00

Cost of sales 80.00 100.00

A. Inventory in days = (Inventory/ cost of

sales) * 365 136.88 73.00

Receivables 150.00 160.00

Revenue 196.00 245.00

B. Receivables in days = (Receivables /

Revenue) * 365 279.34 238.37

Payables 70.00 80.00

Purchases 80.00 100.00

C. Payables in days = (Payables /

Purchases) * 365 319.38 292.00

Cash operating cycle = A + B - C 96.84 19.37

B)

ROCE

Return on capital employed (ROCE) is money related proportion that can be utilized in

evaluating an organization's productivity and capital effectiveness. As such, the proportion can

assist with seeing how well an organization is creating benefits from its capital. The ROCE

proportion is one of a few productivity proportions money related administrators, partners, and

potential financial specialists may utilize while breaking down an organization for speculation.

The Return on capital employed shows what amount working pay is produced for every dollar of

capital contributed. A higher ROCE is in every case greater, as it demonstrates that more benefits

are created per dollar of capital utilized. In any case, likewise with some other money related

proportions, figuring simply the ROCE of an organization isn't sufficient. Other benefit

proportions, for example, return on resources, return on contributed capital, and profit for value

A. Quick Assets 1348 1578

B. Current Liabilities 366 521

Current Ratio 3.68 3.03

3. Cash operating cycle

Cash Operating cycle 2019 2020

Inventories 30.00 20.00

Cost of sales 80.00 100.00

A. Inventory in days = (Inventory/ cost of

sales) * 365 136.88 73.00

Receivables 150.00 160.00

Revenue 196.00 245.00

B. Receivables in days = (Receivables /

Revenue) * 365 279.34 238.37

Payables 70.00 80.00

Purchases 80.00 100.00

C. Payables in days = (Payables /

Purchases) * 365 319.38 292.00

Cash operating cycle = A + B - C 96.84 19.37

B)

ROCE

Return on capital employed (ROCE) is money related proportion that can be utilized in

evaluating an organization's productivity and capital effectiveness. As such, the proportion can

assist with seeing how well an organization is creating benefits from its capital. The ROCE

proportion is one of a few productivity proportions money related administrators, partners, and

potential financial specialists may utilize while breaking down an organization for speculation.

The Return on capital employed shows what amount working pay is produced for every dollar of

capital contributed. A higher ROCE is in every case greater, as it demonstrates that more benefits

are created per dollar of capital utilized. In any case, likewise with some other money related

proportions, figuring simply the ROCE of an organization isn't sufficient. Other benefit

proportions, for example, return on resources, return on contributed capital, and profit for value

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ought to be utilized related to ROCE to decide if an organization is likely a wise speculation or

not.

In the model with Apple Inc., a ROCE of 23% in 2017 implies that for each dollar put resources

into capital, the organization created 23 pennies in working pay. To decide if Apple's ROCE is

acceptable, it is critical to analyze it against its rivals and not across various enterprises.

ROCE is a measurement for dissecting benefit, and conceivably looking at productivity levels

across organizations regarding capital. There are two parts needed to ascertain return on capital

utilized: profit before interest and expense and capital utilized.

EBIT, otherwise called working pay, shows how much an organization procures from its

activities alone regardless of interest or duties. EBIT is determined by taking away the expense

of merchandise sold and working costs from incomes.

Capital utilized is fundamentally the same as contributed capital, which is utilized in the ROIC

estimation. Capital utilized is found by deducting absolute resources from current liabilities,

which at last gives you investors' value in addition to long haul obligations. Rather than utilizing

capital utilized at a discretionary point as expected, a few experts and speculators may decide to

ascertain ROCE dependent on the normal capital utilized, which takes the normal of opening and

shutting capital utilized for the time span under examination.

ROCE can be particularly valuable when contrasting the presentation of organizations in capital-

serious areas, for example, utilities and telecoms. This is on the grounds that dissimilar to

different basics, for example, return on value (ROE), which just dissects benefit identified with

an organization's investors' value, ROCE thinks about obligation and value. This can help kill

money related execution investigation for organizations with huge obligation.

At last, the computation of ROCE discloses to you the measure of benefit an organization is

creating per $1 of capital utilized. Clearly, the more benefit per $1 an organization can create the

better. Subsequently, a higher ROCE demonstrates more grounded productivity across

organization correlations.

not.

In the model with Apple Inc., a ROCE of 23% in 2017 implies that for each dollar put resources

into capital, the organization created 23 pennies in working pay. To decide if Apple's ROCE is

acceptable, it is critical to analyze it against its rivals and not across various enterprises.

ROCE is a measurement for dissecting benefit, and conceivably looking at productivity levels

across organizations regarding capital. There are two parts needed to ascertain return on capital

utilized: profit before interest and expense and capital utilized.

EBIT, otherwise called working pay, shows how much an organization procures from its

activities alone regardless of interest or duties. EBIT is determined by taking away the expense

of merchandise sold and working costs from incomes.

Capital utilized is fundamentally the same as contributed capital, which is utilized in the ROIC

estimation. Capital utilized is found by deducting absolute resources from current liabilities,

which at last gives you investors' value in addition to long haul obligations. Rather than utilizing

capital utilized at a discretionary point as expected, a few experts and speculators may decide to

ascertain ROCE dependent on the normal capital utilized, which takes the normal of opening and

shutting capital utilized for the time span under examination.

ROCE can be particularly valuable when contrasting the presentation of organizations in capital-

serious areas, for example, utilities and telecoms. This is on the grounds that dissimilar to

different basics, for example, return on value (ROE), which just dissects benefit identified with

an organization's investors' value, ROCE thinks about obligation and value. This can help kill

money related execution investigation for organizations with huge obligation.

At last, the computation of ROCE discloses to you the measure of benefit an organization is

creating per $1 of capital utilized. Clearly, the more benefit per $1 an organization can create the

better. Subsequently, a higher ROCE demonstrates more grounded productivity across

organization correlations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For an organization, the ROCE pattern throughout the years can likewise be a significant marker

of execution. By and large, speculators will in general support organizations with steady and

rising ROCE levels over organizations where ROCE is unpredictable or moving lower.

While dissecting benefit proficiency regarding capital, both ROIC and ROCE can be utilized.

The two measurements are comparative in that they give a proportion of benefit for each

absolute capital of the firm. By and large, both the ROIC and ROCE ought to be higher than an

organization's weighted normal expense of capital (WACC) all together for the organization to

be productive over the long haul. ROIC is commonly founded on a similar idea as ROCE, yet its

parts are marginally extraordinary.

The result shows that Return on capital employed has been increased from 11.86% to 14.19%.

This shows improvement in current performance of the business compared to previous years

performance.

Acid Test Ratio

The acid-test ratio utilizes an association's accounting report information as a marker of whether

it has adequate transient resources for cover its momentary liabilities. This measurement is more

helpful in specific circumstances than the current proportion, otherwise called the working

capital proportion, since it disregards resources, for example, stock, which might be hard to

rapidly exchange.

The numerator of the basic analysis proportion can be characterized in different manners, yet the

principle thought ought to increase a practical perspective on the organization's fluid resources.

Money and money counterparts should be incorporated, as should momentary speculations, for

example, attractive protections.

Records receivable are commonly included, yet this isn't suitable for each industry. In the

development business, for instance, records of sales may set aside considerably more effort to

recuperate than is standard practice in different enterprises, so including it could cause a

company's monetary situation to appear to be significantly more secure than it is actually.

Another approach to ascertain the numerator is to take all current resources and deduct illiquid

resources. Above all, stock ought to be deducted, remembering that this will adversely slant the

of execution. By and large, speculators will in general support organizations with steady and

rising ROCE levels over organizations where ROCE is unpredictable or moving lower.

While dissecting benefit proficiency regarding capital, both ROIC and ROCE can be utilized.

The two measurements are comparative in that they give a proportion of benefit for each

absolute capital of the firm. By and large, both the ROIC and ROCE ought to be higher than an

organization's weighted normal expense of capital (WACC) all together for the organization to

be productive over the long haul. ROIC is commonly founded on a similar idea as ROCE, yet its

parts are marginally extraordinary.

The result shows that Return on capital employed has been increased from 11.86% to 14.19%.

This shows improvement in current performance of the business compared to previous years

performance.

Acid Test Ratio

The acid-test ratio utilizes an association's accounting report information as a marker of whether

it has adequate transient resources for cover its momentary liabilities. This measurement is more

helpful in specific circumstances than the current proportion, otherwise called the working

capital proportion, since it disregards resources, for example, stock, which might be hard to

rapidly exchange.

The numerator of the basic analysis proportion can be characterized in different manners, yet the

principle thought ought to increase a practical perspective on the organization's fluid resources.

Money and money counterparts should be incorporated, as should momentary speculations, for

example, attractive protections.

Records receivable are commonly included, yet this isn't suitable for each industry. In the

development business, for instance, records of sales may set aside considerably more effort to

recuperate than is standard practice in different enterprises, so including it could cause a

company's monetary situation to appear to be significantly more secure than it is actually.

Another approach to ascertain the numerator is to take all current resources and deduct illiquid

resources. Above all, stock ought to be deducted, remembering that this will adversely slant the

image for retail organizations in light of the measure of stock they convey. Different components

that show up as resources on an accounting report ought to be deducted on the off chance that

they can't be utilized to cover liabilities temporarily, for example, advances to providers,

prepayments, and conceded charge resources.

The proportion's denominator ought to incorporate every current risk, which are obligations and

commitments that are expected inside one year. Note that time isn't figured into the analysis

proportion. In the event that an organization's records payable are almost due yet its receivables

won't come in for quite a long time, that organization could be on a lot shakier ground than its

proportion would show. The inverse can likewise be valid.

Organizations with an analysis proportion of under 1 need more fluid resources for pay their

present liabilities and ought to be treated with alert. In the event that the analysis proportion is a

lot of lower than the current proportion, it implies that an organization's present resources are

profoundly reliant on stock.

This is definitely not a terrible sign in all cases, notwithstanding, as some plans of action are

naturally subject to stock. Retail locations, for instance, may have low analysis proportions

without fundamentally being in harm's way.

Acid test of both the year are higher than 3; which is much higher than ideal ratio (1:1) and it

shows inefficiency of business to better utilize its current assets into production and return on

ideal cash.

Cash operating cycle

The cash conversion cycle (CCC) is a metric that communicates the time (estimated in days) it

takes for an organization to change over its interests in stock and different assets into incomes

from deals. Likewise called the Net Operating Cycle or basically Cash Cycle, CCC endeavors to

gauge how long each net information dollar is tied up in the creation and deals measure before it

gets changed over into money gotten.

that show up as resources on an accounting report ought to be deducted on the off chance that

they can't be utilized to cover liabilities temporarily, for example, advances to providers,

prepayments, and conceded charge resources.

The proportion's denominator ought to incorporate every current risk, which are obligations and

commitments that are expected inside one year. Note that time isn't figured into the analysis

proportion. In the event that an organization's records payable are almost due yet its receivables

won't come in for quite a long time, that organization could be on a lot shakier ground than its

proportion would show. The inverse can likewise be valid.

Organizations with an analysis proportion of under 1 need more fluid resources for pay their

present liabilities and ought to be treated with alert. In the event that the analysis proportion is a

lot of lower than the current proportion, it implies that an organization's present resources are

profoundly reliant on stock.

This is definitely not a terrible sign in all cases, notwithstanding, as some plans of action are

naturally subject to stock. Retail locations, for instance, may have low analysis proportions

without fundamentally being in harm's way.

Acid test of both the year are higher than 3; which is much higher than ideal ratio (1:1) and it

shows inefficiency of business to better utilize its current assets into production and return on

ideal cash.

Cash operating cycle

The cash conversion cycle (CCC) is a metric that communicates the time (estimated in days) it

takes for an organization to change over its interests in stock and different assets into incomes

from deals. Likewise called the Net Operating Cycle or basically Cash Cycle, CCC endeavors to

gauge how long each net information dollar is tied up in the creation and deals measure before it

gets changed over into money gotten.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This measurement considers how long the organization needs to sell its stock, how long it

requires to gather receivables, and how long it needs to take care of its bills without bringing

about punishments.

CCC is one of a few quantitative measures that help assess the productivity of an organization's

activities and the board. A pattern of diminishing or consistent CCC qualities over different

periods is a decent sign while rising ones should prompt more examination and investigation

dependent on different components. One should remember that CCC applies just to choose areas

subject to stock administration and related tasks.

An Operating Cycle (OC) alludes to the days needed for a business to get stock, sell the stock,

and gather money from the offer of the stock. This cycle assumes a significant function in

deciding the productivity of a business.

The OC offers a knowledge into an organization's working effectiveness. A more limited cycle is

liked and shows a more effective and fruitful business. A more limited cycle shows that an

organization can recuperate its stock venture rapidly and has enough money to meet

commitments. In the event that an organization's OC is long, it can make income issues.

This pattern of crude material change to money is called working or working capital cycle.

Regarding time, it is the time taken after the acquisition of crude material till its interpretation

into money. The all out of stock holding period and a receivable assortment time of a firm is the

working process duration of that firm. Working cycle and money working cycle are utilized

reciprocally however it's a misinterpretation. They are distinctive just barely however that has a

major effect.

Like working capital, working cycle can likewise be gross working cycle (working cycle) and

net working cycle (money working cycle). Money working cycle is gross working cycle less

leaser's assortment period. It is the time span for which the working capital is required.

Working cycle is critical on the grounds that business is about the running the working cycle

easily. In the event that it is running easily, nearly all that will be smooth. On the off chance that

any portion of the working cycle is trapped, the entire business gets upset. For a director to

requires to gather receivables, and how long it needs to take care of its bills without bringing

about punishments.

CCC is one of a few quantitative measures that help assess the productivity of an organization's

activities and the board. A pattern of diminishing or consistent CCC qualities over different

periods is a decent sign while rising ones should prompt more examination and investigation

dependent on different components. One should remember that CCC applies just to choose areas

subject to stock administration and related tasks.

An Operating Cycle (OC) alludes to the days needed for a business to get stock, sell the stock,

and gather money from the offer of the stock. This cycle assumes a significant function in

deciding the productivity of a business.

The OC offers a knowledge into an organization's working effectiveness. A more limited cycle is

liked and shows a more effective and fruitful business. A more limited cycle shows that an

organization can recuperate its stock venture rapidly and has enough money to meet

commitments. In the event that an organization's OC is long, it can make income issues.

This pattern of crude material change to money is called working or working capital cycle.

Regarding time, it is the time taken after the acquisition of crude material till its interpretation

into money. The all out of stock holding period and a receivable assortment time of a firm is the

working process duration of that firm. Working cycle and money working cycle are utilized

reciprocally however it's a misinterpretation. They are distinctive just barely however that has a

major effect.

Like working capital, working cycle can likewise be gross working cycle (working cycle) and

net working cycle (money working cycle). Money working cycle is gross working cycle less

leaser's assortment period. It is the time span for which the working capital is required.

Working cycle is critical on the grounds that business is about the running the working cycle

easily. In the event that it is running easily, nearly all that will be smooth. On the off chance that

any portion of the working cycle is trapped, the entire business gets upset. For a director to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

viably deal with the business, he ought to have a profound comprehension of his business cycle

and likely dangers and dangers to it. Proactively, he ought to have available resources to alleviate

those dangers and dangers.

Banks accept this as a base for subsidizing their customer. An administrator taking care of

money should zero in on decreasing the money cycle as that will spare him the premium

expense. Diminishing this cycle implies decreasing the stock holding time frame and expanding

the provider's installment time frame. Other than typical methodologies, Japanese strategies

'Without a moment to spare (JIT)' can decrease the stock holding time for all intents and

purposes zero. Greater organizations are attempting to receive JIT with the assistance of devices

like provider framework reconciliation and so on

Cash operating cycle has been declined from year 2019 to 2020; it is bad news for the business

because earlier; firm requires cash after average 97 days but in 2020; it requires cash after 19

days.

and likely dangers and dangers to it. Proactively, he ought to have available resources to alleviate

those dangers and dangers.

Banks accept this as a base for subsidizing their customer. An administrator taking care of

money should zero in on decreasing the money cycle as that will spare him the premium

expense. Diminishing this cycle implies decreasing the stock holding time frame and expanding

the provider's installment time frame. Other than typical methodologies, Japanese strategies

'Without a moment to spare (JIT)' can decrease the stock holding time for all intents and

purposes zero. Greater organizations are attempting to receive JIT with the assistance of devices

like provider framework reconciliation and so on

Cash operating cycle has been declined from year 2019 to 2020; it is bad news for the business

because earlier; firm requires cash after average 97 days but in 2020; it requires cash after 19

days.

References

Shaikh, S., 2020. MCQ Ratio Analysis of Financial Statements.

Dawar, V., 2017. Amtek auto: Analysis of financial statements. SAGE Publications: SAGE

Business Cases Originals.

ÖZEVİN, O., 2020. A Model Recommendation On Determination Of Manipulation Risk In

Financial Statements: BIST Application. Journal of Accounting & Finance, (87).

Pokale, V., 2020. ANALYSIS OF FINANCIAL STATEMENTS.

Maisharoh, T. and Riyanto, S., 2020. Financial Statements Analysis in Measuring Financial

Performance of the PT. Mayora Indah Tbk, Period 2014-2018. Journal of Contemporary

Information Technology, Management, and Accounting, 1(2), pp.63-71.

Shaikh, S., 2020. MCQ Ratio Analysis of Financial Statements.

Dawar, V., 2017. Amtek auto: Analysis of financial statements. SAGE Publications: SAGE

Business Cases Originals.

ÖZEVİN, O., 2020. A Model Recommendation On Determination Of Manipulation Risk In

Financial Statements: BIST Application. Journal of Accounting & Finance, (87).

Pokale, V., 2020. ANALYSIS OF FINANCIAL STATEMENTS.

Maisharoh, T. and Riyanto, S., 2020. Financial Statements Analysis in Measuring Financial

Performance of the PT. Mayora Indah Tbk, Period 2014-2018. Journal of Contemporary

Information Technology, Management, and Accounting, 1(2), pp.63-71.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.