Accounting Assignment Solution - Lease and Depreciation

VerifiedAdded on 2022/08/20

|10

|815

|19

Homework Assignment

AI Summary

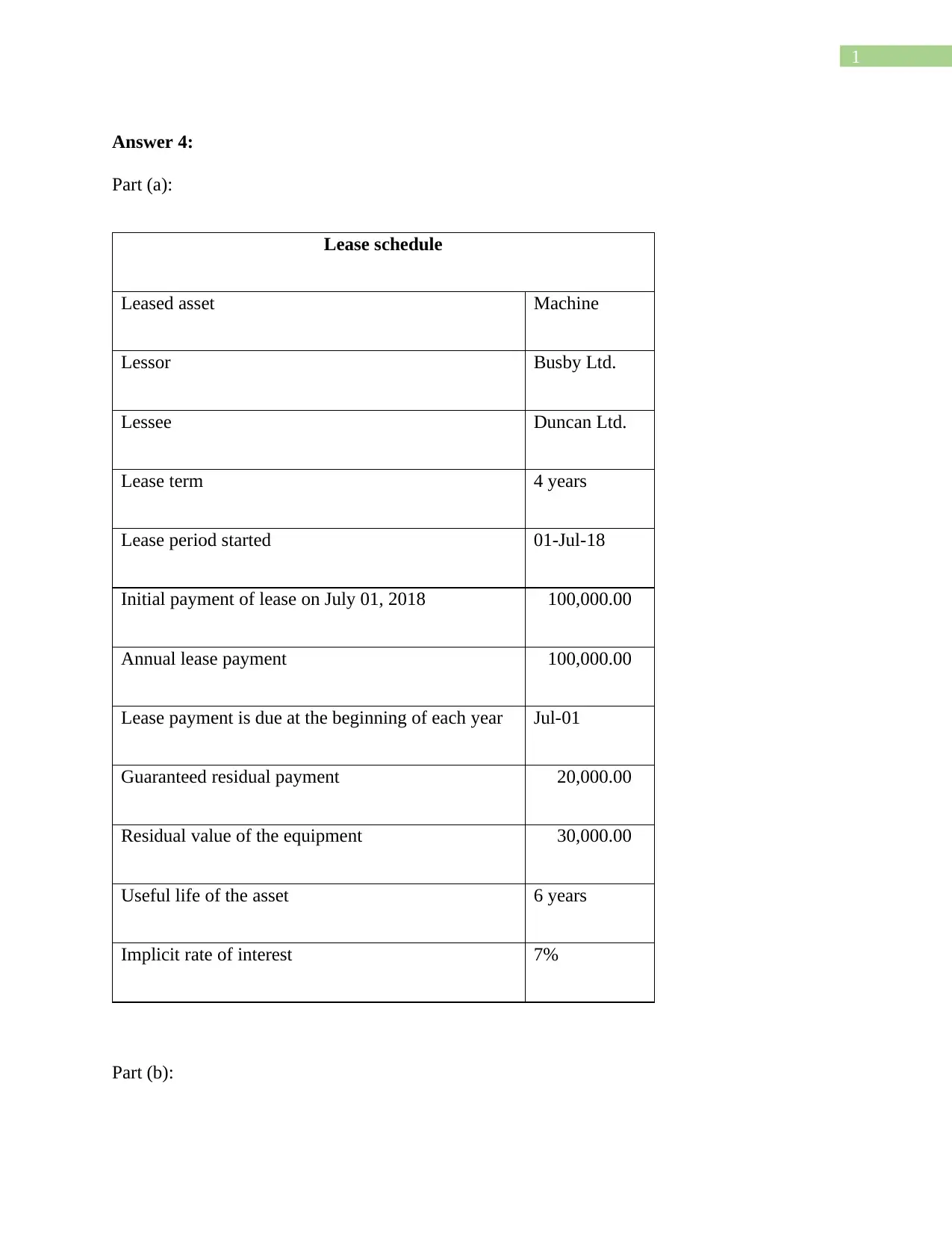

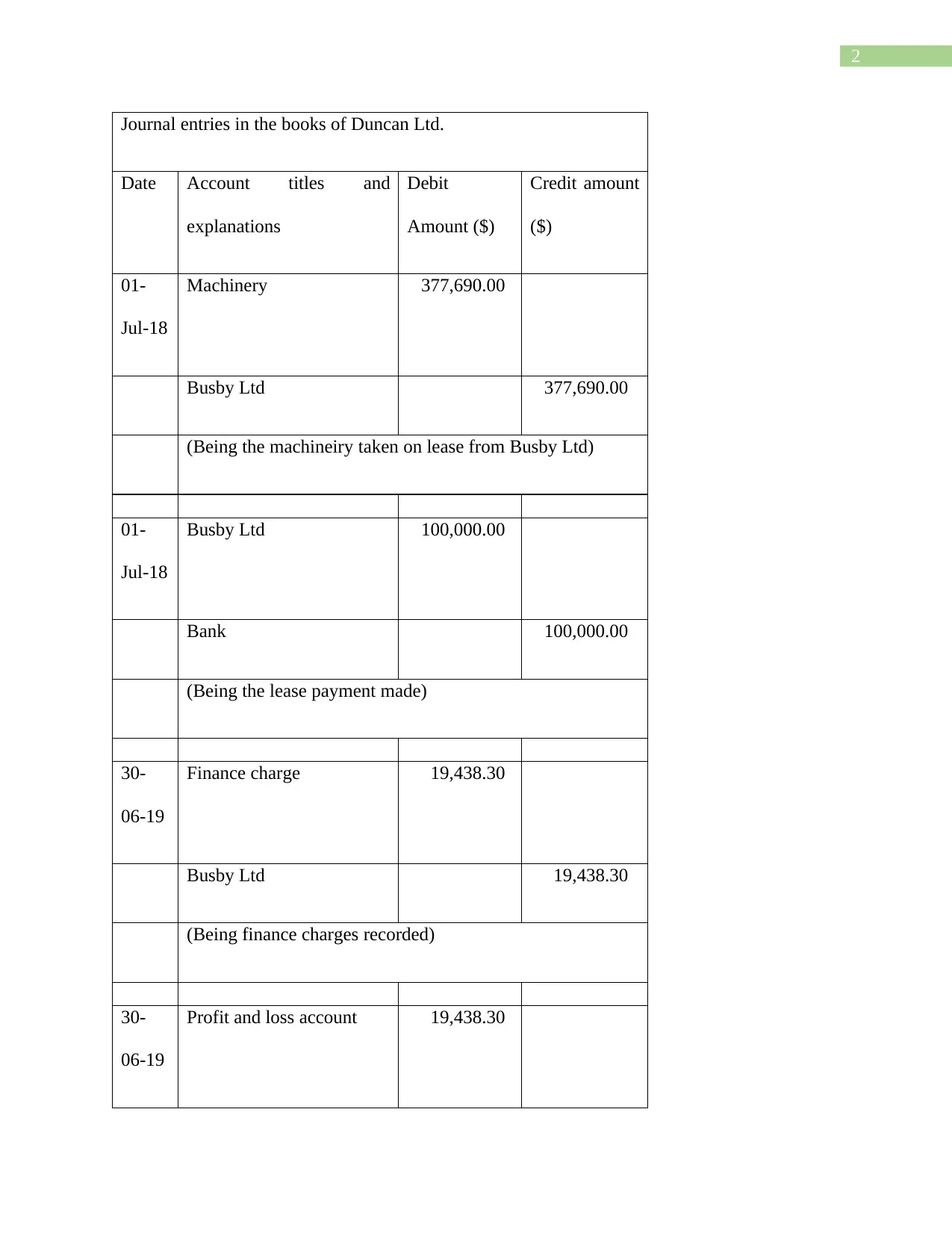

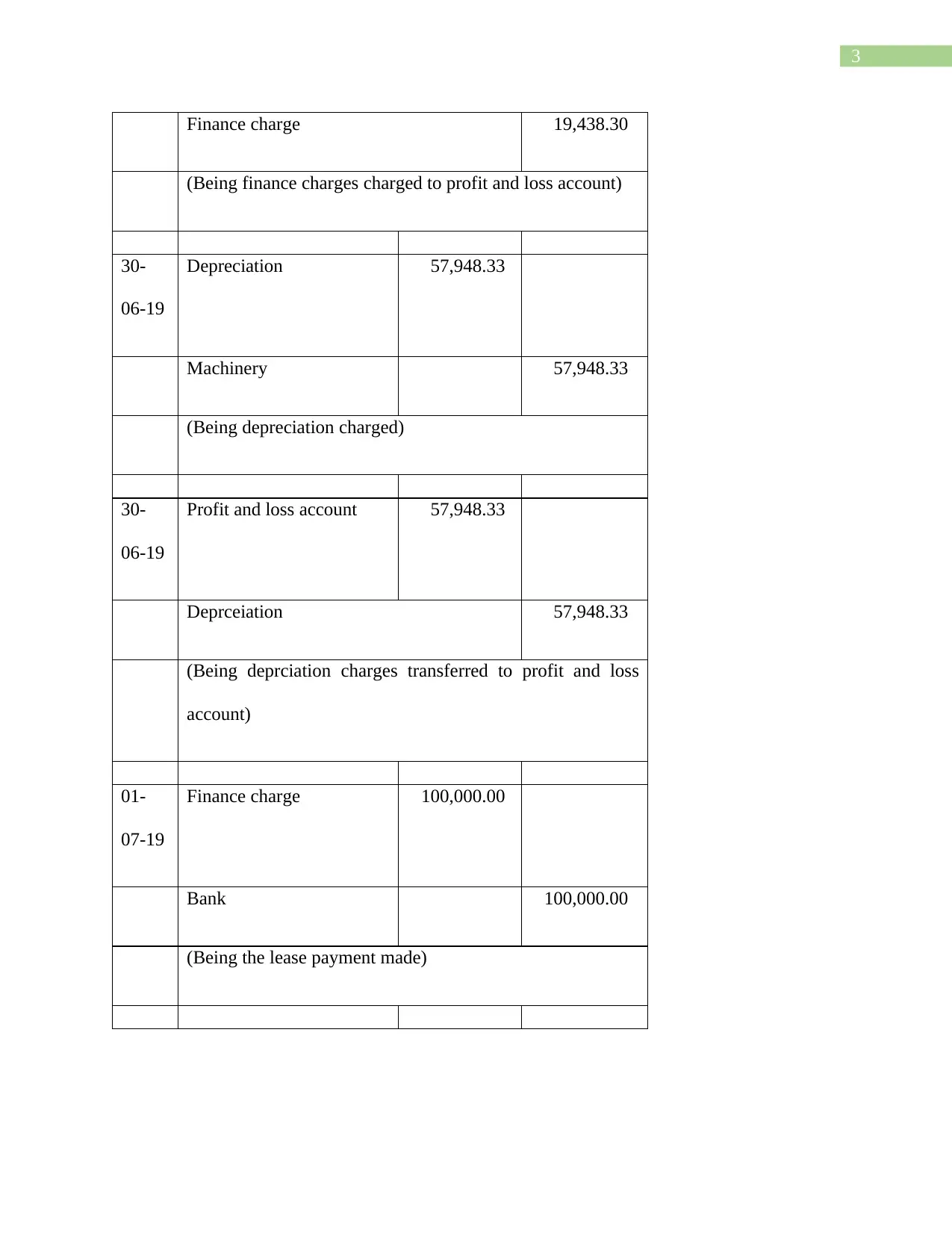

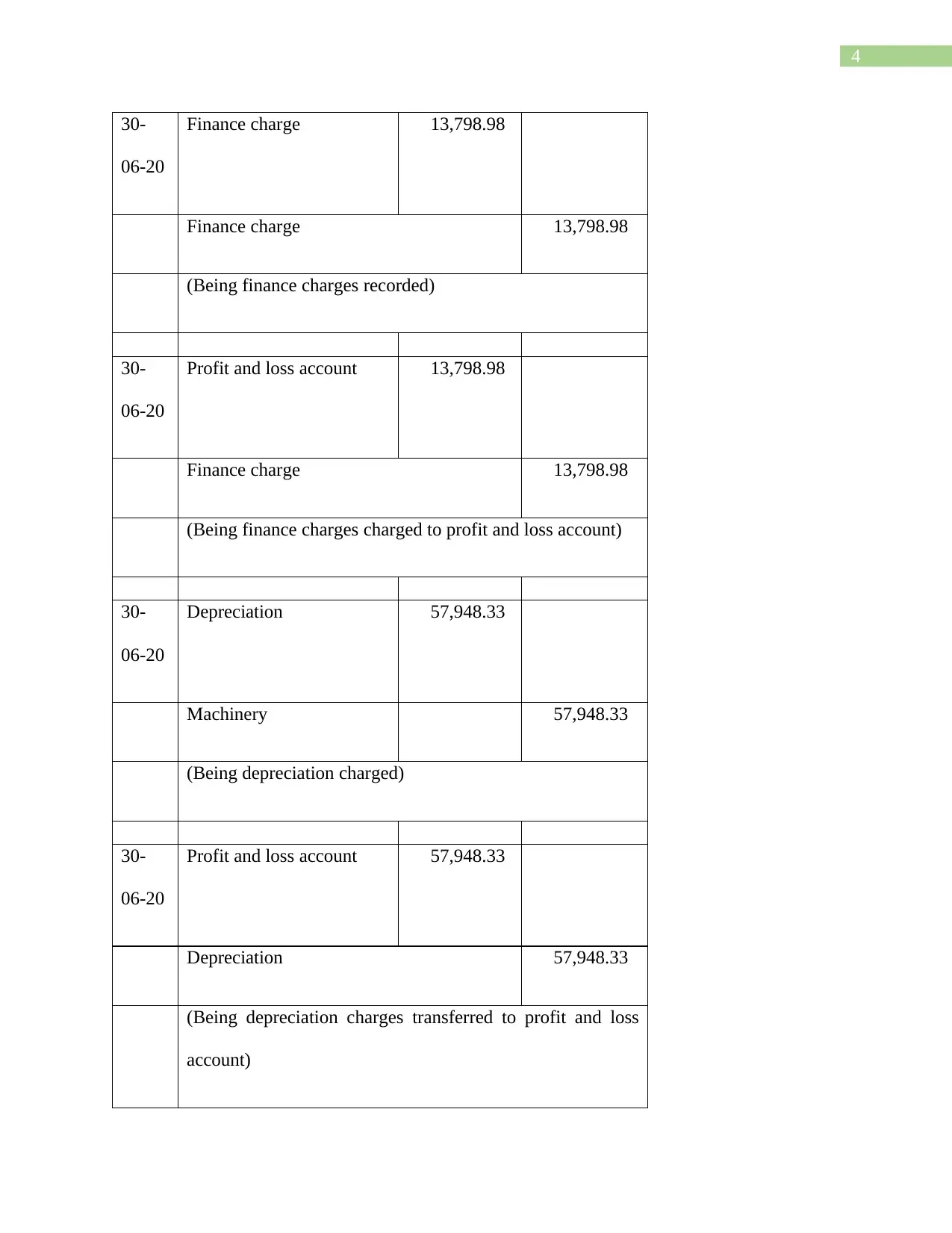

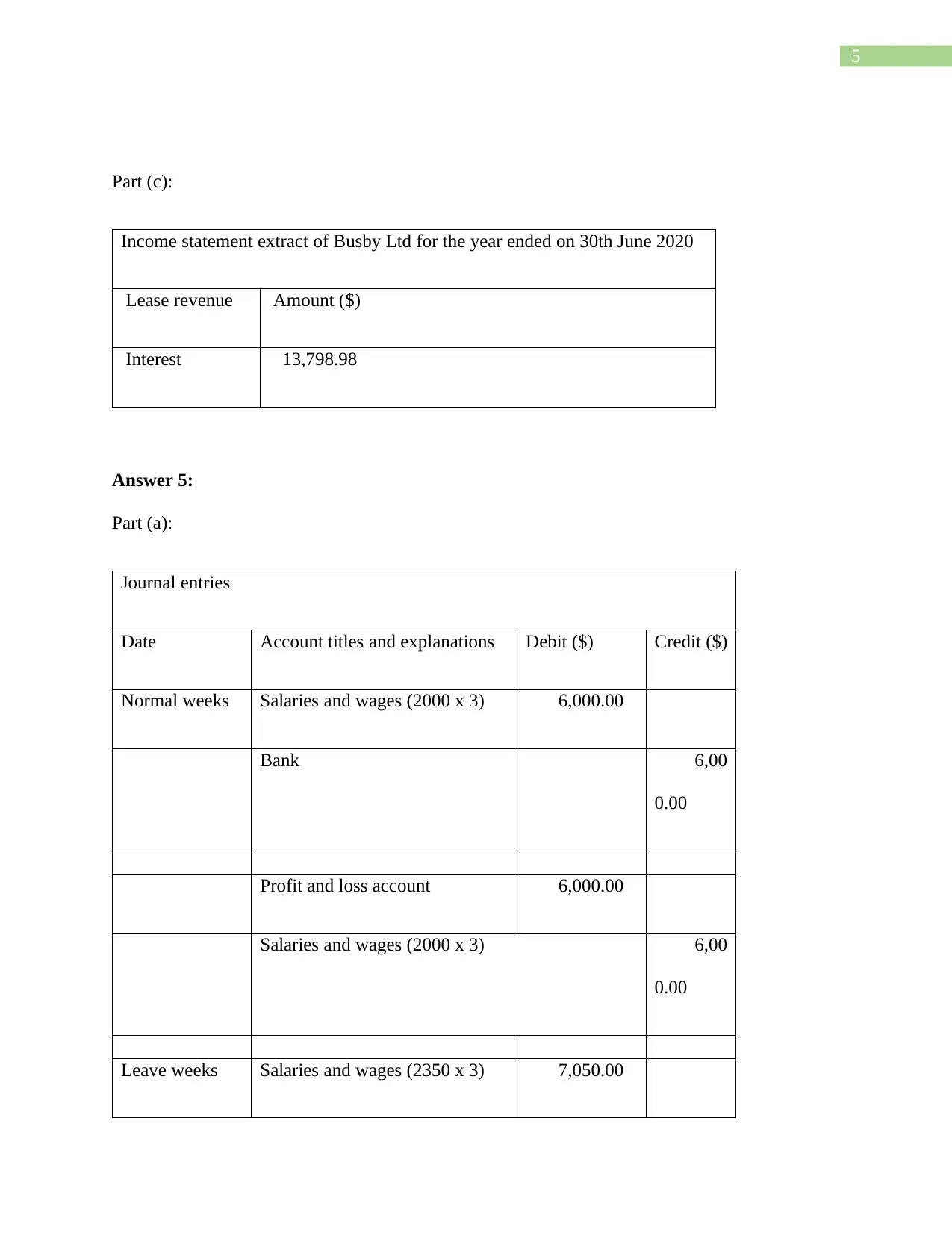

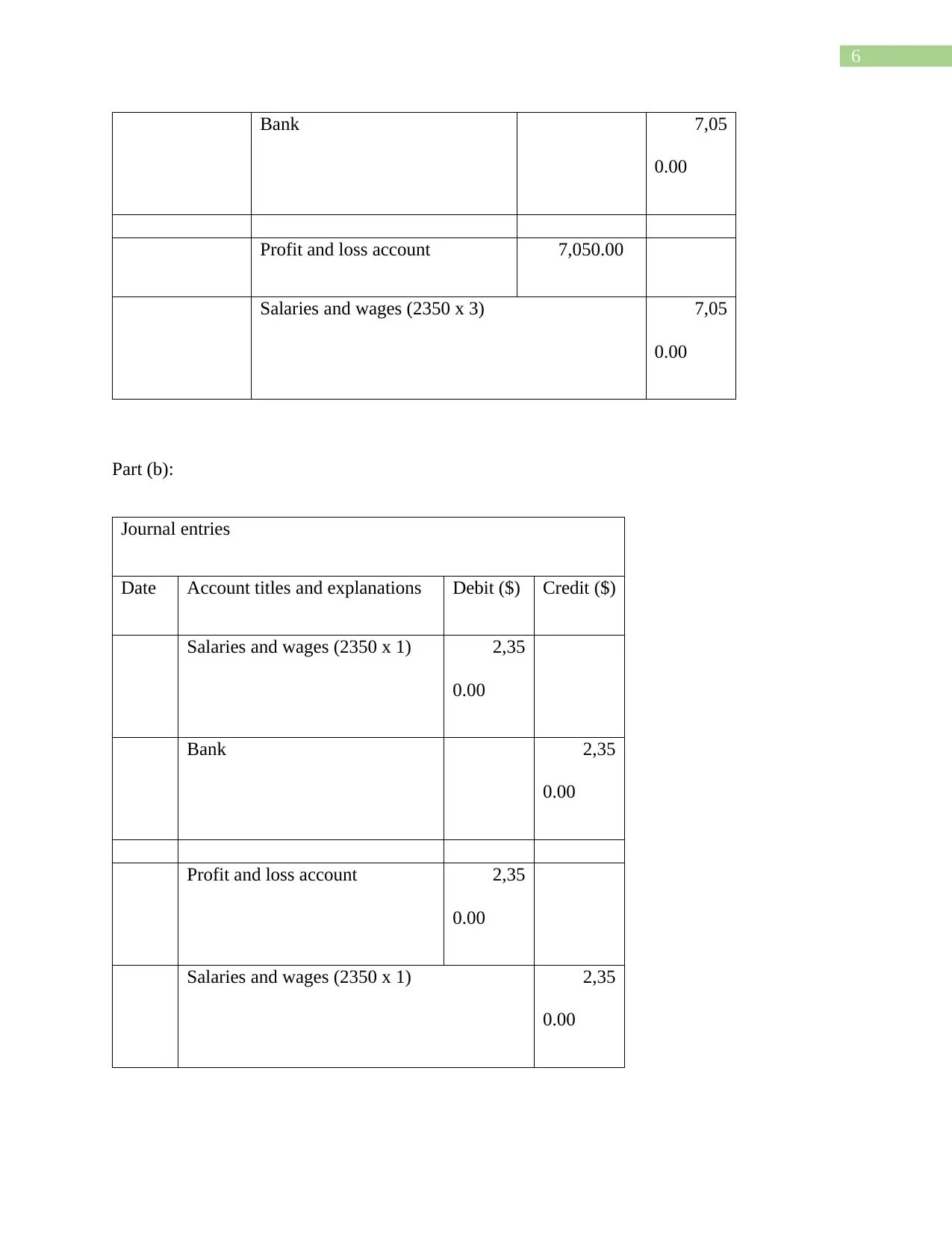

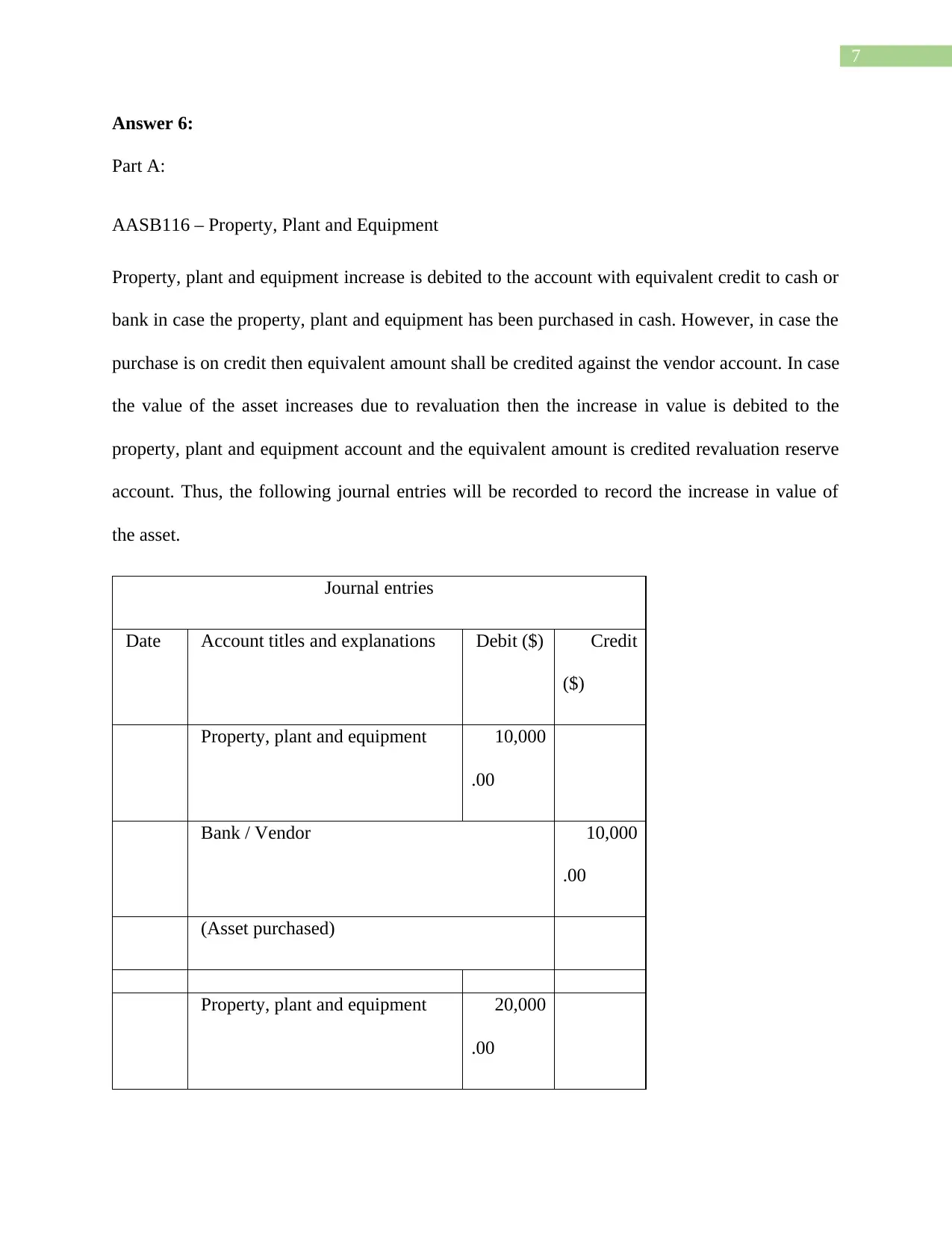

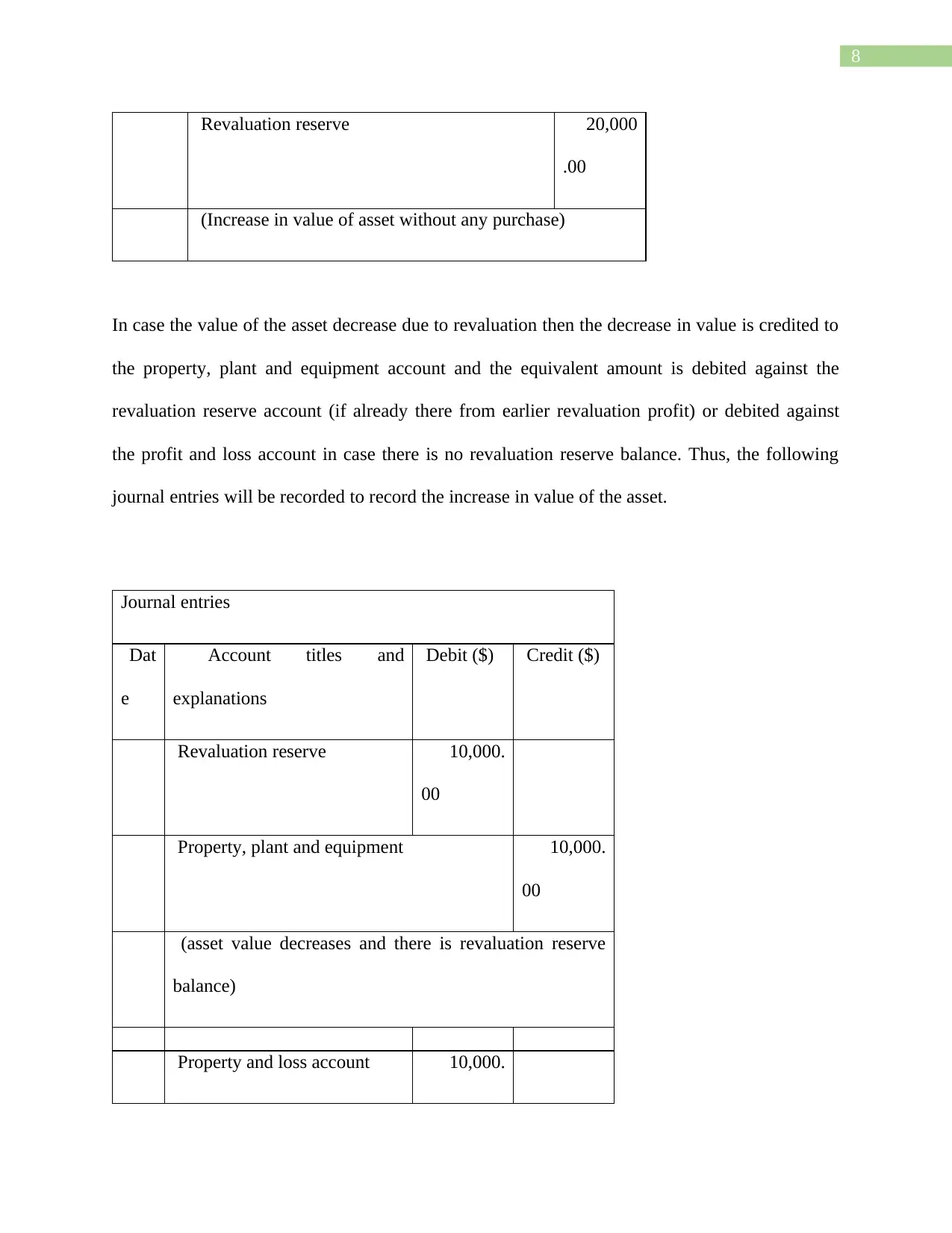

This accounting assignment solution addresses various accounting concepts, including lease accounting, depreciation, journal entries, and inventory valuation. The solution includes a lease schedule, journal entries for a lessee, and an income statement extract for a lessor. It also covers salary and wage calculations, and the application of accounting standards like AASB116 for Property, Plant, and Equipment, and the treatment of research and development expenditure. The assignment provides detailed explanations and calculations to illustrate the accounting principles involved, making it a useful resource for students studying accounting.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.