Accounting Questions and Answers | Study

VerifiedAdded on 2022/09/01

|17

|3322

|21

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: REPORT 0

ACCOUNTING

JANUARY 8, 2020

STUDENT DETAILS:

ACCOUNTING

JANUARY 8, 2020

STUDENT DETAILS:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REPORT 1

Part-A

Answer 1:

After receiving the copy of the financial statements of PepsiCo for periods ending December 31,

2013 as well as 2014, I will take following decisions in the different situations -

(a) The requirement of data from the financial statement of PepsiCo in case of the

banker –

The bankers will require the financial statement to assess loan as well as abilities of the

interests payable. It will require to evaluate the debt services coverage ratios, amount of

the loan, financial strength such as debt equity ratio as well as Bankers would need

financial statements to analyze the loan and interest payable capabilities. It is required to

evaluate debt service coverage ratio, amount of other loans, financial strength like

current ratio as well as debt equity ratio. The current ratio is also considered as the

liquidity ratio. It evaluates whether the organisation has sufficient sources to fulfil the

short-term obligation. The debt equity ratio indicates the relative part of the equity and

debt utilised to finance the asset of entity.

(b) A need of data from the financial statement of PepsiCo in case of potential investor

–

The Investor will require the data such as the net profit of an organisation, proportion of

dividend paid as well as the capital structure.

Part-A

Answer 1:

After receiving the copy of the financial statements of PepsiCo for periods ending December 31,

2013 as well as 2014, I will take following decisions in the different situations -

(a) The requirement of data from the financial statement of PepsiCo in case of the

banker –

The bankers will require the financial statement to assess loan as well as abilities of the

interests payable. It will require to evaluate the debt services coverage ratios, amount of

the loan, financial strength such as debt equity ratio as well as Bankers would need

financial statements to analyze the loan and interest payable capabilities. It is required to

evaluate debt service coverage ratio, amount of other loans, financial strength like

current ratio as well as debt equity ratio. The current ratio is also considered as the

liquidity ratio. It evaluates whether the organisation has sufficient sources to fulfil the

short-term obligation. The debt equity ratio indicates the relative part of the equity and

debt utilised to finance the asset of entity.

(b) A need of data from the financial statement of PepsiCo in case of potential investor

–

The Investor will require the data such as the net profit of an organisation, proportion of

dividend paid as well as the capital structure.

REPORT 2

(c) The requirement of data from the financial statement of company In case of Labour

negotiator –

The profit and loss statement is very helpful in this matter. The main reason is that they

require data such as the operating profits of corporation. It is evident that the labour

charge paid is compared with the proportion of labour charge to the profits with business.

Additionally, it can say that in case of enhancing profit, they want rise in the wages.

Answer 2:

Following accounting assumptions are violated in the provided situations-

(a) In the provided situation, Melissa bought computer for personal utilisation. However,

Melissa recoded this asset as the asset of Missy’ Teashop instead of personal asset. In

accounting, the economic entity is best assumptions made in generally accepted

accounting principle. It is required by the Economic entity assumption that the activities

of company are to be kept individually from the different functions of owners as well as

other financial organisations. In this situation, the economic entity assumption is

violated (Wisdom, et. al, 2017).

(c) The requirement of data from the financial statement of company In case of Labour

negotiator –

The profit and loss statement is very helpful in this matter. The main reason is that they

require data such as the operating profits of corporation. It is evident that the labour

charge paid is compared with the proportion of labour charge to the profits with business.

Additionally, it can say that in case of enhancing profit, they want rise in the wages.

Answer 2:

Following accounting assumptions are violated in the provided situations-

(a) In the provided situation, Melissa bought computer for personal utilisation. However,

Melissa recoded this asset as the asset of Missy’ Teashop instead of personal asset. In

accounting, the economic entity is best assumptions made in generally accepted

accounting principle. It is required by the Economic entity assumption that the activities

of company are to be kept individually from the different functions of owners as well as

other financial organisations. In this situation, the economic entity assumption is

violated (Wisdom, et. al, 2017).

REPORT 3

(b) It is provided that Houston Electronics bought office building $ 500,000 before some

years. It can be traded presently at $ 850,000. The accountant would present the building

as the asset on the book at $ 850,000. It can see that it is required by the consistency that

the financial statements of organisation adopt the similar accounting principles,

approaches, methodologies, as well as processes from one accounting period to the

upcoming accounting period. This accounting principle permits the reader of the financial

statement of company to create useful comparison between different periods. It also

permits the organisation to initiate the changes to the chosen accounting methods.

However, the changes as well as effects should be presented for the benefits of a reader

of the financial statements. The accounting method or principle should be changed only

when the new method in can improve the reported financial outcomes. In the provided

situation, the consistency assumption is violated.

(a) It is decided by new accountant that he will make financial statement in every 2 years.

The financial statement’s users require current as well as proper data to assess financial

performance as well as condition of organisation to take significant decision as well as

proper action. The time-period assumption enables the organisation to divide the financial

functions in the short-term. In this case, the Time-period assumption is violated. The

time-period assumption is also known as the periodicity assumption.

(b) It is stated that the Candle store has no plan to quit. However, it is decided that it will

utilize market value to report the asset since it takes decision to move on to the smaller

(b) It is provided that Houston Electronics bought office building $ 500,000 before some

years. It can be traded presently at $ 850,000. The accountant would present the building

as the asset on the book at $ 850,000. It can see that it is required by the consistency that

the financial statements of organisation adopt the similar accounting principles,

approaches, methodologies, as well as processes from one accounting period to the

upcoming accounting period. This accounting principle permits the reader of the financial

statement of company to create useful comparison between different periods. It also

permits the organisation to initiate the changes to the chosen accounting methods.

However, the changes as well as effects should be presented for the benefits of a reader

of the financial statements. The accounting method or principle should be changed only

when the new method in can improve the reported financial outcomes. In the provided

situation, the consistency assumption is violated.

(a) It is decided by new accountant that he will make financial statement in every 2 years.

The financial statement’s users require current as well as proper data to assess financial

performance as well as condition of organisation to take significant decision as well as

proper action. The time-period assumption enables the organisation to divide the financial

functions in the short-term. In this case, the Time-period assumption is violated. The

time-period assumption is also known as the periodicity assumption.

(b) It is stated that the Candle store has no plan to quit. However, it is decided that it will

utilize market value to report the asset since it takes decision to move on to the smaller

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REPORT 4

store. It is stated by the Financial Accounting Standard Board that the consistency is a

main quality or feature that develops the accounting information. It is stated by

the consistency principle that once the company adopts the accounting principle or

accounting method, it is continually required to follow this principle on the constant basis

in the upcoming accounting periods. In this situation, the consistency assumption is

violated (Bradbury and Almulla, 2018).

Answer 5:

(a) The General Purpose of the auditor’s report –

The report of auditor is considered as the document containing the opinions of auditor

whether the financial statement of entity comply with generally accepted accounting

principles. The audit report has significant role because the bank, creditor, along with

controllers need the audit the financial statement of organisation. The general purpose of

the report of auditor is to document reasonable declaration that the financial statement of

company is free from errors. In addition of income statements as well as the balance

sheets, the auditor's report also makes up the statutory accounts of entity. It can say that it

is important for the reason that the bank as well as creditor needs the audit of financial

statements of organisation before lending to them. Additionally, the clean audit report

explains the purpose of auditor’s report that the entity adopted the accounting standards

when the unqualified report means there may be error (Yusof and Ismail, 2016).

(b) The going concern –

store. It is stated by the Financial Accounting Standard Board that the consistency is a

main quality or feature that develops the accounting information. It is stated by

the consistency principle that once the company adopts the accounting principle or

accounting method, it is continually required to follow this principle on the constant basis

in the upcoming accounting periods. In this situation, the consistency assumption is

violated (Bradbury and Almulla, 2018).

Answer 5:

(a) The General Purpose of the auditor’s report –

The report of auditor is considered as the document containing the opinions of auditor

whether the financial statement of entity comply with generally accepted accounting

principles. The audit report has significant role because the bank, creditor, along with

controllers need the audit the financial statement of organisation. The general purpose of

the report of auditor is to document reasonable declaration that the financial statement of

company is free from errors. In addition of income statements as well as the balance

sheets, the auditor's report also makes up the statutory accounts of entity. It can say that it

is important for the reason that the bank as well as creditor needs the audit of financial

statements of organisation before lending to them. Additionally, the clean audit report

explains the purpose of auditor’s report that the entity adopted the accounting standards

when the unqualified report means there may be error (Yusof and Ismail, 2016).

(b) The going concern –

REPORT 5

The going concern principle is considered as the assumption that the organisation would

remain in business for upcoming period. On the other hand, it can say that the

organisation would not be forced to stop functions and liquidate the asset in an upcoming

term at what can lessen the fire-selling price. As per the going concern principle, the

accountant can be justified in submitting identification of some expenditures until the

subsequent time, while the organisation would seemingly still be in business and utilising

the assets in the most effectual way. The organisation is assumed the going concern

principle in the absence of relevant as well as important data to contrary. In this way, the

value of the organisation that is supposed to be the going concern is higher than the

breakup value, since the going concern may possibly continue to generate profit (Kolar,

2017).

(c) No, the losses, restructuring, as well as the disposal of segments are not essentially

precursors to demise of an organization. While the organisation sells the fixed asset like

properties as well as equipment, and takes proceed amounting to less than book value of

assets, then the losses on disposal of assets are noted as the non-operating losses (Prasad

and Chand, 2017).

(d) In the particular organizations, the auditor of company made the adverse opinion. As per

his opinion, the company will not remain in the business for the upcoming reason. It will

not run its operations because it has recurred the net loss, which has resulted into the

The going concern principle is considered as the assumption that the organisation would

remain in business for upcoming period. On the other hand, it can say that the

organisation would not be forced to stop functions and liquidate the asset in an upcoming

term at what can lessen the fire-selling price. As per the going concern principle, the

accountant can be justified in submitting identification of some expenditures until the

subsequent time, while the organisation would seemingly still be in business and utilising

the assets in the most effectual way. The organisation is assumed the going concern

principle in the absence of relevant as well as important data to contrary. In this way, the

value of the organisation that is supposed to be the going concern is higher than the

breakup value, since the going concern may possibly continue to generate profit (Kolar,

2017).

(c) No, the losses, restructuring, as well as the disposal of segments are not essentially

precursors to demise of an organization. While the organisation sells the fixed asset like

properties as well as equipment, and takes proceed amounting to less than book value of

assets, then the losses on disposal of assets are noted as the non-operating losses (Prasad

and Chand, 2017).

(d) In the particular organizations, the auditor of company made the adverse opinion. As per

his opinion, the company will not remain in the business for the upcoming reason. It will

not run its operations because it has recurred the net loss, which has resulted into the

REPORT 6

accumulated deficit of 49.7 million dollars as of 31st December, 2012 (Ofori‐Sasu, Abor

and Osei, 2017).

Answer 4:

The dividend is not considered as the expenditure as it is allocation of earning. The dividend is

not regarded as loss of expenditure. It is clear that the dividend declared or dividend paid is not

part of calculation of net income, which is stated on income statement of the entity. The

dividend announced by the entity is reported in the statement of the changes in Equity of

stakeholders and changes in the retained earnings. It can say that the cash dividend means the

sum of money rewarded by the corporation to the shareholders form the reserves as well as

profits of company. It is evident that the dividend is a type of reward to shareholders (Li, Hay

and Lau, 2019). It is a reward decided by the entity to make decision related to essential outlay.

In this way, the dividend is not regarded to be the part of the cash outflows of company that is

essential to run the functions of business. The costs are not involved in the income statement of

organisation. additionally, the outlay is not the expenditure. The dividend policy of entity can be

reversed at the period. It would not show up on the financial statement of company. In addition,

the profits are generated from the money invested by shareholder. The stakeholders are known as

the owners of entity. It can say that the allocation of sharing of profit to owners cannot be

considered as the expenditure. The investments from the owner are never treated as incomes. In

the same way, the profits to the owner are never considered as the expenditures (Gejalaksmi and

Azhagaiah, 2017).

Answer 6 –

accumulated deficit of 49.7 million dollars as of 31st December, 2012 (Ofori‐Sasu, Abor

and Osei, 2017).

Answer 4:

The dividend is not considered as the expenditure as it is allocation of earning. The dividend is

not regarded as loss of expenditure. It is clear that the dividend declared or dividend paid is not

part of calculation of net income, which is stated on income statement of the entity. The

dividend announced by the entity is reported in the statement of the changes in Equity of

stakeholders and changes in the retained earnings. It can say that the cash dividend means the

sum of money rewarded by the corporation to the shareholders form the reserves as well as

profits of company. It is evident that the dividend is a type of reward to shareholders (Li, Hay

and Lau, 2019). It is a reward decided by the entity to make decision related to essential outlay.

In this way, the dividend is not regarded to be the part of the cash outflows of company that is

essential to run the functions of business. The costs are not involved in the income statement of

organisation. additionally, the outlay is not the expenditure. The dividend policy of entity can be

reversed at the period. It would not show up on the financial statement of company. In addition,

the profits are generated from the money invested by shareholder. The stakeholders are known as

the owners of entity. It can say that the allocation of sharing of profit to owners cannot be

considered as the expenditure. The investments from the owner are never treated as incomes. In

the same way, the profits to the owner are never considered as the expenditures (Gejalaksmi and

Azhagaiah, 2017).

Answer 6 –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

The material is considered as the extent of the result of losses will not be huge as to affect the

financial condition of corporation. The material data or occasion are the events as well as aspects

that will put impact upon the judgment of the well-informed investors. The material event is

required to be publicly stated along with corresponding financial statement. In financial term, the

materiality is known as the impact of the omission or misstatement of data in the financial

statement of entity on users of the statement (Solt, 2016). When user will not have changed the

actions, in that case the misstatement (omission) is considered to be the immaterial. The

materiality concept is used frequently in accounting, especially in the following instances:

Implementation of accounting standard - it is not required by the organisation to apply the

requirement of the accounting standards if such inactions are immaterial to company’s

financial statement.

Capitalization limits – the entity may charge expenses to expense, which will be

capitalized as well as depreciated over period. For this reason, the expenses are smaller to

be worth tracking efforts. In this way, the capitalization will have immaterial impacts on

entity’s financial statements.

Minor transaction – the regulator who is closing book for the accounting period may

avoid minor journal entry if conducting so would have immaterial impacts upon financial

statement of company.

In this way, it can say that the materiality permits the organisation to avoid chosen accounting

standards, when also increasing the effectiveness of the accounting functions. It can say that the

material is in a best position to decide the result of the lawsuit (Nieuwenhuis, Munzi and

Gornick, 2017).

The material is considered as the extent of the result of losses will not be huge as to affect the

financial condition of corporation. The material data or occasion are the events as well as aspects

that will put impact upon the judgment of the well-informed investors. The material event is

required to be publicly stated along with corresponding financial statement. In financial term, the

materiality is known as the impact of the omission or misstatement of data in the financial

statement of entity on users of the statement (Solt, 2016). When user will not have changed the

actions, in that case the misstatement (omission) is considered to be the immaterial. The

materiality concept is used frequently in accounting, especially in the following instances:

Implementation of accounting standard - it is not required by the organisation to apply the

requirement of the accounting standards if such inactions are immaterial to company’s

financial statement.

Capitalization limits – the entity may charge expenses to expense, which will be

capitalized as well as depreciated over period. For this reason, the expenses are smaller to

be worth tracking efforts. In this way, the capitalization will have immaterial impacts on

entity’s financial statements.

Minor transaction – the regulator who is closing book for the accounting period may

avoid minor journal entry if conducting so would have immaterial impacts upon financial

statement of company.

In this way, it can say that the materiality permits the organisation to avoid chosen accounting

standards, when also increasing the effectiveness of the accounting functions. It can say that the

material is in a best position to decide the result of the lawsuit (Nieuwenhuis, Munzi and

Gornick, 2017).

REPORT 8

In addition, the remote is considered as the possibility of happening of occasion is lesser such as

less than ten per cent. It is considered as the subset of 'possible', at a lower end of ranges of

probabilities. It states occasions that are not expected to take place, but that may not be ruled out

totally. It is intended to be the typical examination because the contingent liability that

is remote is not stated in financial statement (Patra and Dhar, 2017).

In addition, the remote is considered as the possibility of happening of occasion is lesser such as

less than ten per cent. It is considered as the subset of 'possible', at a lower end of ranges of

probabilities. It states occasions that are not expected to take place, but that may not be ruled out

totally. It is intended to be the typical examination because the contingent liability that

is remote is not stated in financial statement (Patra and Dhar, 2017).

REPORT 9

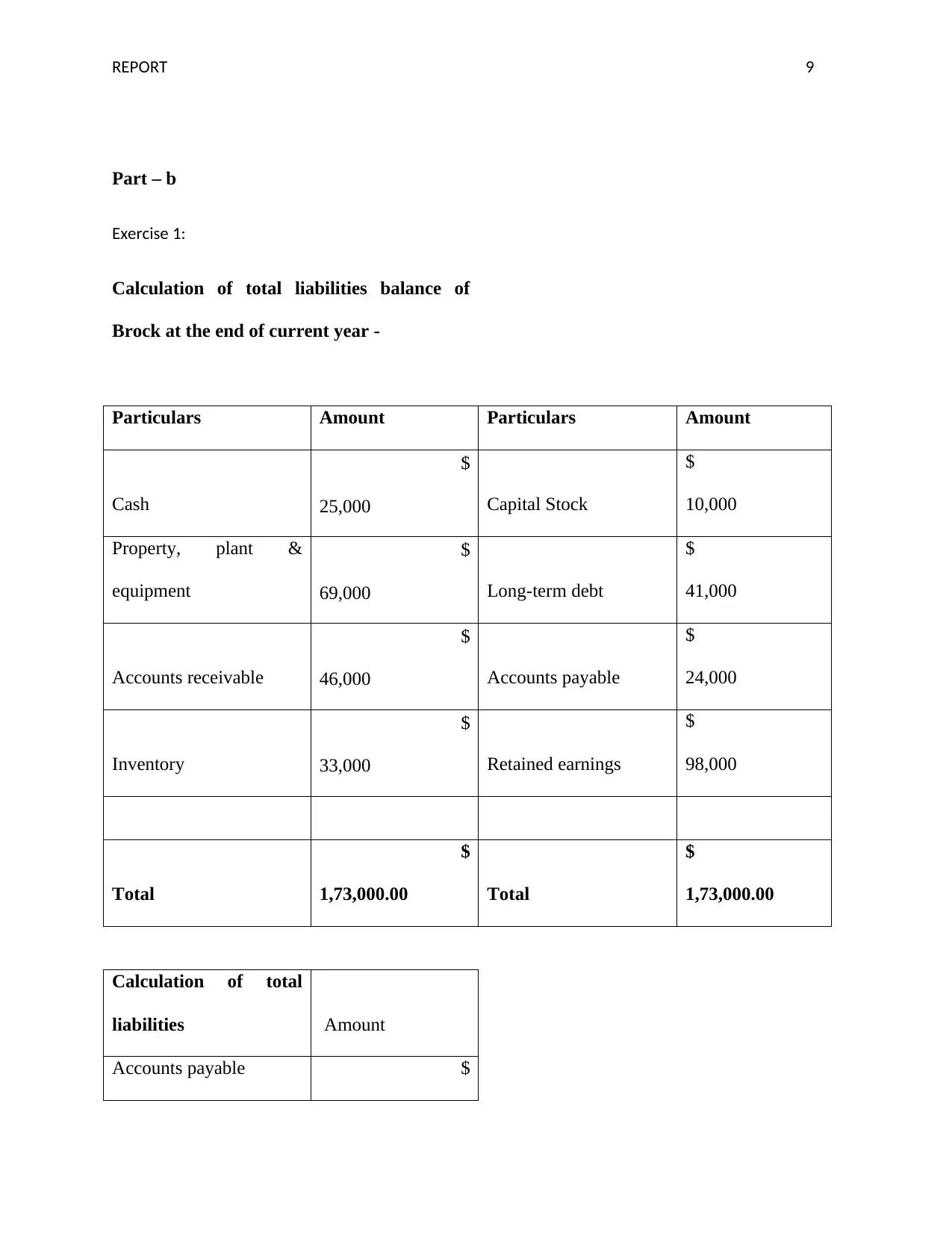

Part – b

Exercise 1:

Calculation of total liabilities balance of

Brock at the end of current year -

Particulars Amount Particulars Amount

Cash

$

25,000 Capital Stock

$

10,000

Property, plant &

equipment

$

69,000 Long-term debt

$

41,000

Accounts receivable

$

46,000 Accounts payable

$

24,000

Inventory

$

33,000 Retained earnings

$

98,000

Total

$

1,73,000.00 Total

$

1,73,000.00

Calculation of total

liabilities Amount

Accounts payable $

Part – b

Exercise 1:

Calculation of total liabilities balance of

Brock at the end of current year -

Particulars Amount Particulars Amount

Cash

$

25,000 Capital Stock

$

10,000

Property, plant &

equipment

$

69,000 Long-term debt

$

41,000

Accounts receivable

$

46,000 Accounts payable

$

24,000

Inventory

$

33,000 Retained earnings

$

98,000

Total

$

1,73,000.00 Total

$

1,73,000.00

Calculation of total

liabilities Amount

Accounts payable $

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

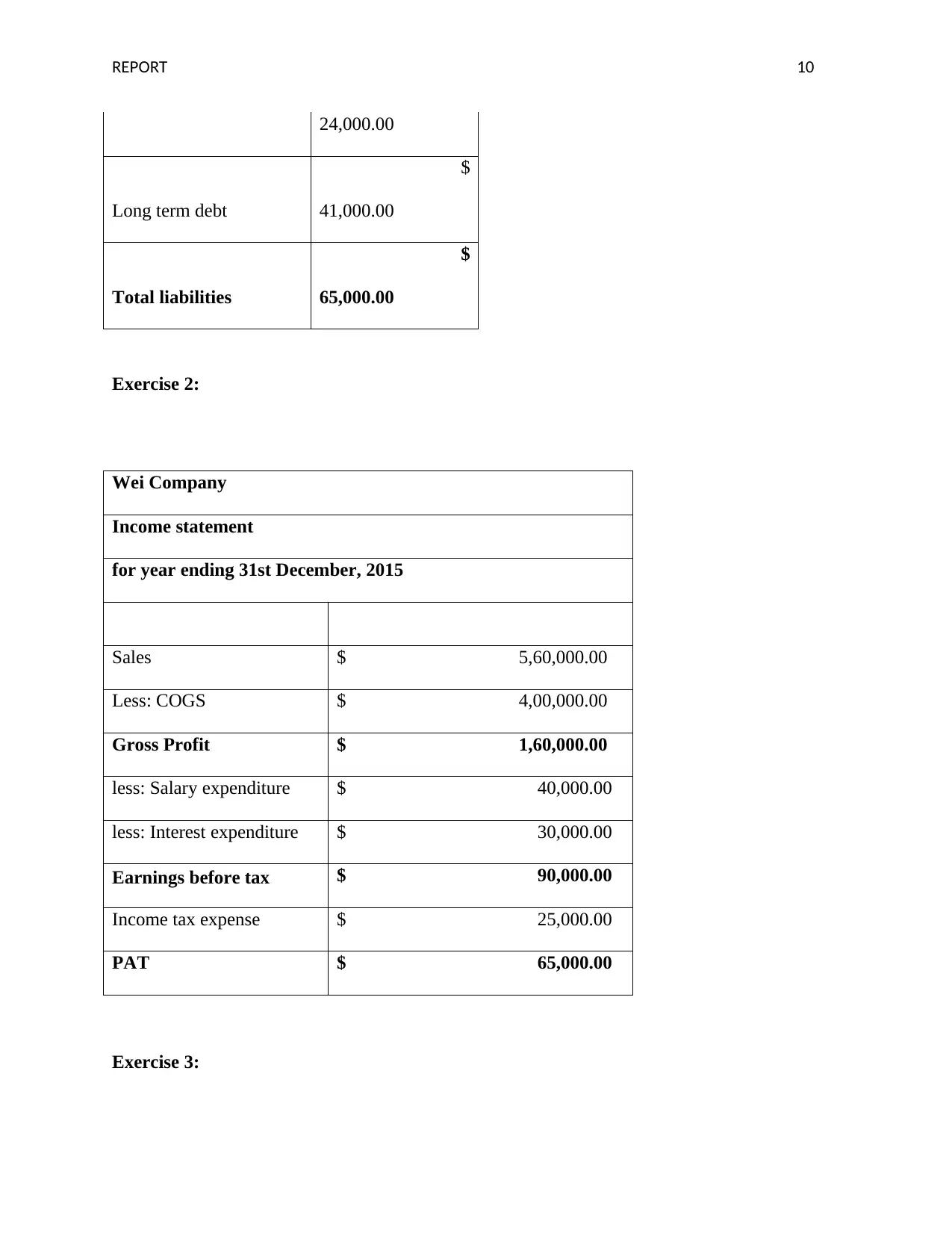

REPORT 10

24,000.00

Long term debt

$

41,000.00

Total liabilities

$

65,000.00

Exercise 2:

Wei Company

Income statement

for year ending 31st December, 2015

Sales $ 5,60,000.00

Less: COGS $ 4,00,000.00

Gross Profit $ 1,60,000.00

less: Salary expenditure $ 40,000.00

less: Interest expenditure $ 30,000.00

Earnings before tax $ 90,000.00

Income tax expense $ 25,000.00

PAT $ 65,000.00

Exercise 3:

24,000.00

Long term debt

$

41,000.00

Total liabilities

$

65,000.00

Exercise 2:

Wei Company

Income statement

for year ending 31st December, 2015

Sales $ 5,60,000.00

Less: COGS $ 4,00,000.00

Gross Profit $ 1,60,000.00

less: Salary expenditure $ 40,000.00

less: Interest expenditure $ 30,000.00

Earnings before tax $ 90,000.00

Income tax expense $ 25,000.00

PAT $ 65,000.00

Exercise 3:

REPORT 11

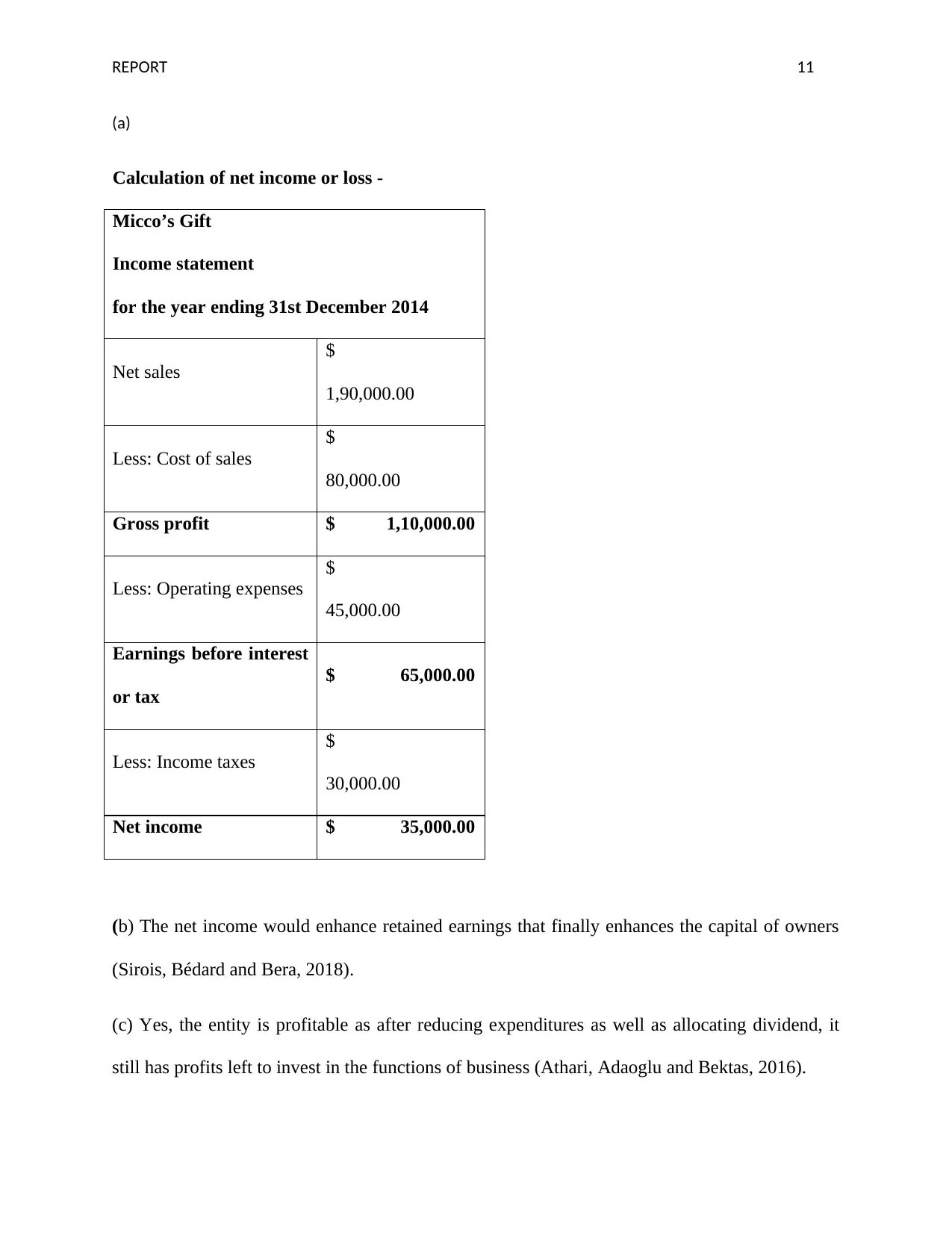

(a)

Calculation of net income or loss -

Micco’s Gift

Income statement

for the year ending 31st December 2014

Net sales

$

1,90,000.00

Less: Cost of sales

$

80,000.00

Gross profit $ 1,10,000.00

Less: Operating expenses

$

45,000.00

Earnings before interest

or tax

$ 65,000.00

Less: Income taxes

$

30,000.00

Net income $ 35,000.00

(b) The net income would enhance retained earnings that finally enhances the capital of owners

(Sirois, Bédard and Bera, 2018).

(c) Yes, the entity is profitable as after reducing expenditures as well as allocating dividend, it

still has profits left to invest in the functions of business (Athari, Adaoglu and Bektas, 2016).

(a)

Calculation of net income or loss -

Micco’s Gift

Income statement

for the year ending 31st December 2014

Net sales

$

1,90,000.00

Less: Cost of sales

$

80,000.00

Gross profit $ 1,10,000.00

Less: Operating expenses

$

45,000.00

Earnings before interest

or tax

$ 65,000.00

Less: Income taxes

$

30,000.00

Net income $ 35,000.00

(b) The net income would enhance retained earnings that finally enhances the capital of owners

(Sirois, Bédard and Bera, 2018).

(c) Yes, the entity is profitable as after reducing expenditures as well as allocating dividend, it

still has profits left to invest in the functions of business (Athari, Adaoglu and Bektas, 2016).

REPORT 12

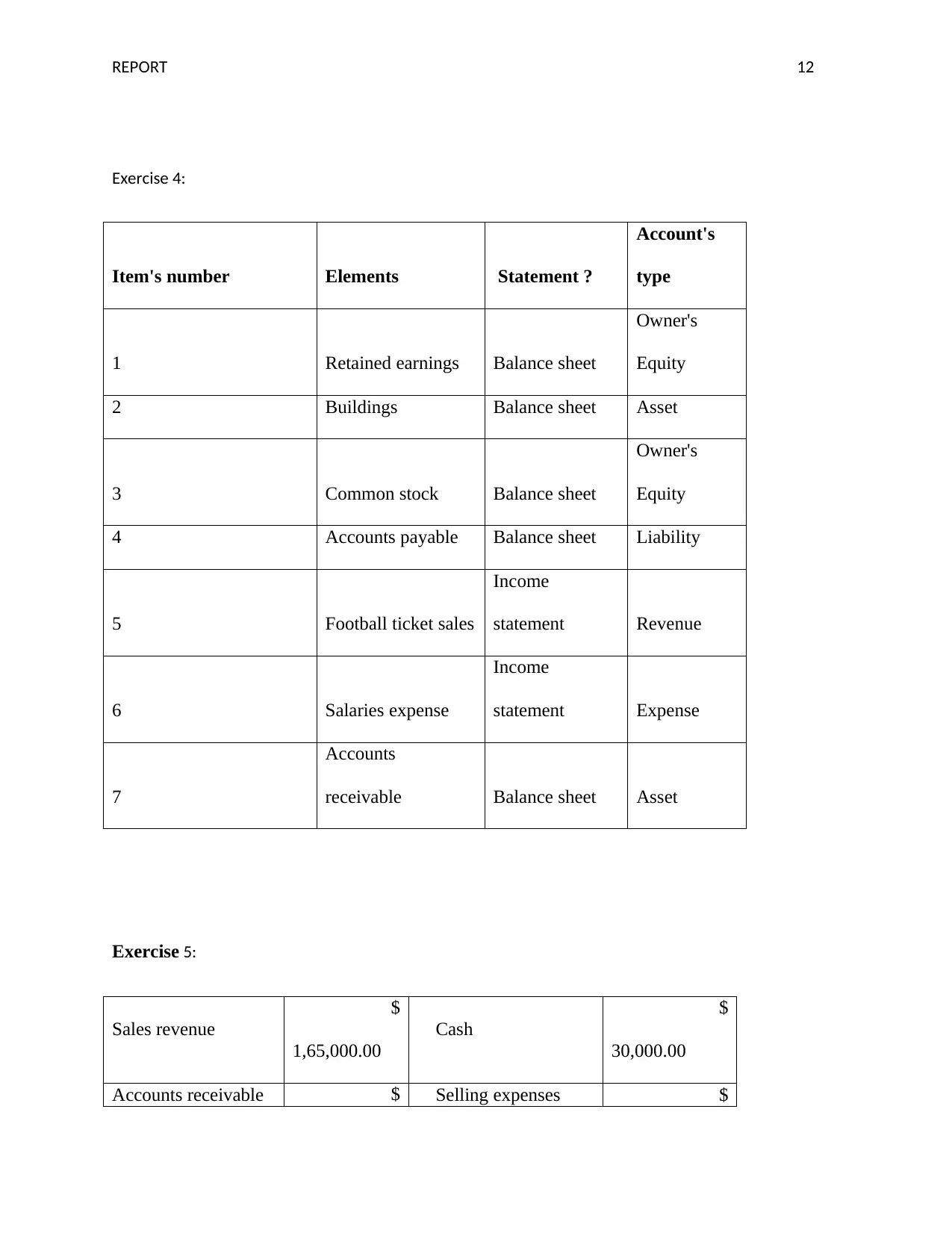

Exercise 4:

Item's number Elements Statement ?

Account's

type

1 Retained earnings Balance sheet

Owner's

Equity

2 Buildings Balance sheet Asset

3 Common stock Balance sheet

Owner's

Equity

4 Accounts payable Balance sheet Liability

5 Football ticket sales

Income

statement Revenue

6 Salaries expense

Income

statement Expense

7

Accounts

receivable Balance sheet Asset

Exercise 5:

Sales revenue

$

1,65,000.00

Cash

$

30,000.00

Accounts receivable $ Selling expenses $

Exercise 4:

Item's number Elements Statement ?

Account's

type

1 Retained earnings Balance sheet

Owner's

Equity

2 Buildings Balance sheet Asset

3 Common stock Balance sheet

Owner's

Equity

4 Accounts payable Balance sheet Liability

5 Football ticket sales

Income

statement Revenue

6 Salaries expense

Income

statement Expense

7

Accounts

receivable Balance sheet Asset

Exercise 5:

Sales revenue

$

1,65,000.00

Cash

$

30,000.00

Accounts receivable $ Selling expenses $

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

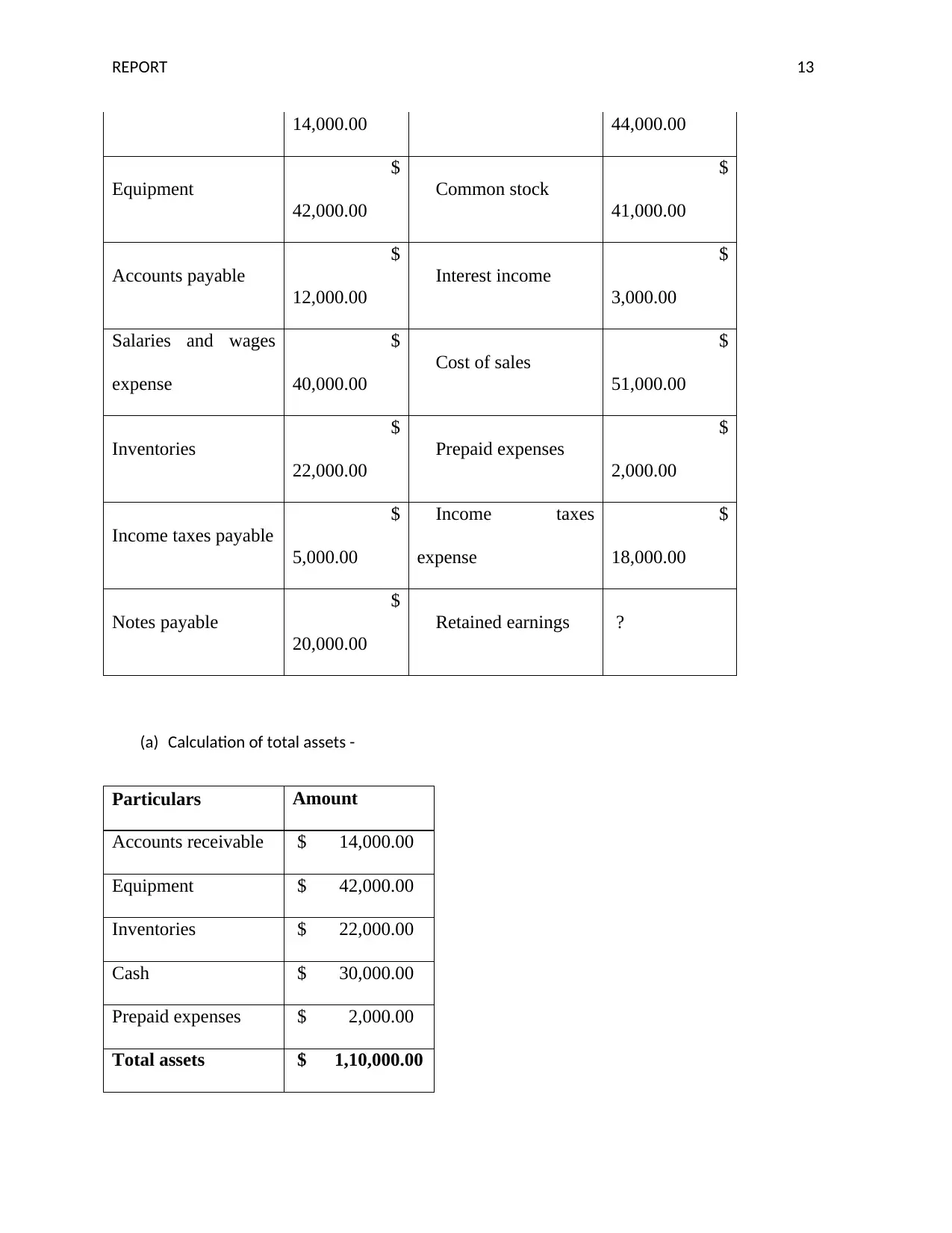

REPORT 13

14,000.00 44,000.00

Equipment

$

42,000.00

Common stock

$

41,000.00

Accounts payable

$

12,000.00

Interest income

$

3,000.00

Salaries and wages

expense

$

40,000.00

Cost of sales

$

51,000.00

Inventories

$

22,000.00

Prepaid expenses

$

2,000.00

Income taxes payable

$

5,000.00

Income taxes

expense

$

18,000.00

Notes payable

$

20,000.00

Retained earnings ?

(a) Calculation of total assets -

Particulars Amount

Accounts receivable $ 14,000.00

Equipment $ 42,000.00

Inventories $ 22,000.00

Cash $ 30,000.00

Prepaid expenses $ 2,000.00

Total assets $ 1,10,000.00

14,000.00 44,000.00

Equipment

$

42,000.00

Common stock

$

41,000.00

Accounts payable

$

12,000.00

Interest income

$

3,000.00

Salaries and wages

expense

$

40,000.00

Cost of sales

$

51,000.00

Inventories

$

22,000.00

Prepaid expenses

$

2,000.00

Income taxes payable

$

5,000.00

Income taxes

expense

$

18,000.00

Notes payable

$

20,000.00

Retained earnings ?

(a) Calculation of total assets -

Particulars Amount

Accounts receivable $ 14,000.00

Equipment $ 42,000.00

Inventories $ 22,000.00

Cash $ 30,000.00

Prepaid expenses $ 2,000.00

Total assets $ 1,10,000.00

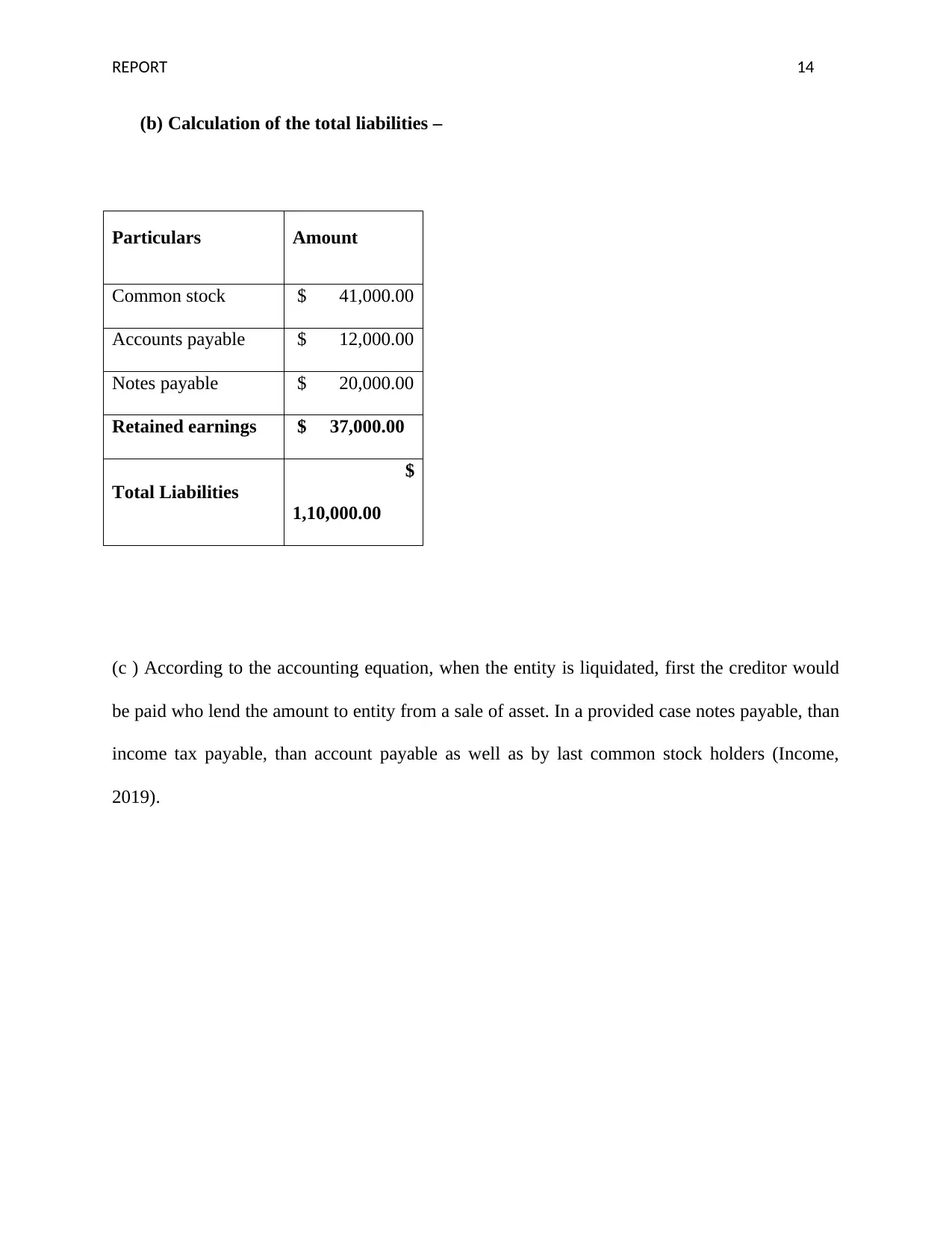

REPORT 14

(b) Calculation of the total liabilities –

Particulars Amount

Common stock $ 41,000.00

Accounts payable $ 12,000.00

Notes payable $ 20,000.00

Retained earnings $ 37,000.00

Total Liabilities

$

1,10,000.00

(c ) According to the accounting equation, when the entity is liquidated, first the creditor would

be paid who lend the amount to entity from a sale of asset. In a provided case notes payable, than

income tax payable, than account payable as well as by last common stock holders (Income,

2019).

(b) Calculation of the total liabilities –

Particulars Amount

Common stock $ 41,000.00

Accounts payable $ 12,000.00

Notes payable $ 20,000.00

Retained earnings $ 37,000.00

Total Liabilities

$

1,10,000.00

(c ) According to the accounting equation, when the entity is liquidated, first the creditor would

be paid who lend the amount to entity from a sale of asset. In a provided case notes payable, than

income tax payable, than account payable as well as by last common stock holders (Income,

2019).

REPORT 15

References

Athari, S.A., Adaoglu, C. and Bektas, E., (2016) Investor protection and dividend policy: The

case of Islamic and conventional banks. Emerging Markets Review, 27, pp.100-117.

Bradbury, M.E. and Almulla, M., (2018) Auditor, Client, and Investor Consequences of the

Enhanced Auditor's Report. Available at SSRN 3165267.

Gejalaksmi, S. and Azhagaiah, R., (2017) The Impact of Dividend Policy on Shareholders'

Wealth: Evidence from Consumer Cyclical Sector in India. Pacific Business Review

International, 9(7), pp.91-103.

Income, N., (2019) Income. Auditing, 1(1,000), pp.1-000

Kolář, M., (2017) Relationship between Stock Returns and Net Income: Evidence from US

Market. USA: Springer

Li, H., Hay, D. and Lau, D., (2019) Assessing the impact of the new auditor’s report. Pacific

Accounting Review, 31(1), pp.110-132.

Nieuwenhuis, R., Munzi, T. and Gornick, J.C., (2017) Comparative research with net and gross

income data: An evaluation of two netting down procedures for the LIS Database. Review of

Income and Wealth, 63(3), pp.564-573.

Ofori‐Sasu, D., Abor, J.Y. and Osei, A.K., (2017) Dividend policy and shareholders’ value:

evidence from listed companies in Ghana. African Development Review, 29(2), pp.293-304.

References

Athari, S.A., Adaoglu, C. and Bektas, E., (2016) Investor protection and dividend policy: The

case of Islamic and conventional banks. Emerging Markets Review, 27, pp.100-117.

Bradbury, M.E. and Almulla, M., (2018) Auditor, Client, and Investor Consequences of the

Enhanced Auditor's Report. Available at SSRN 3165267.

Gejalaksmi, S. and Azhagaiah, R., (2017) The Impact of Dividend Policy on Shareholders'

Wealth: Evidence from Consumer Cyclical Sector in India. Pacific Business Review

International, 9(7), pp.91-103.

Income, N., (2019) Income. Auditing, 1(1,000), pp.1-000

Kolář, M., (2017) Relationship between Stock Returns and Net Income: Evidence from US

Market. USA: Springer

Li, H., Hay, D. and Lau, D., (2019) Assessing the impact of the new auditor’s report. Pacific

Accounting Review, 31(1), pp.110-132.

Nieuwenhuis, R., Munzi, T. and Gornick, J.C., (2017) Comparative research with net and gross

income data: An evaluation of two netting down procedures for the LIS Database. Review of

Income and Wealth, 63(3), pp.564-573.

Ofori‐Sasu, D., Abor, J.Y. and Osei, A.K., (2017) Dividend policy and shareholders’ value:

evidence from listed companies in Ghana. African Development Review, 29(2), pp.293-304.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REPORT 16

Patra, A. and Dhar, P., (2017) Impact of Dividend Policy on Shareholders’ Value: A Study on

Apollo Hospitals Ltd. Bharatiya Vidya Bhavan Institute of Management Science, Kolkata-97,

p.11.

Prasad, P. and Chand, P., (2017) The Changing Face of the Auditor's Report: Implications for

Suppliers and Users of Financial Statements. Australian Accounting Review, 27(4), pp.348-367.

Sirois, L.P., Bédard, J. and Bera, P. (2018) The informational value of key audit matters in the

auditor's report: Evidence from an eye-tracking study. Accounting Horizons, 32(2), pp.141-162.

Solt, F., (2016) The standardized world income inequality database. Social science

quarterly, 97(5), pp.1267-1281.

Wisdom, O., Oyebisi, O., Dorcas, A., David, A. and Oyedeji, L.Q., (2017) Auditor’s report and

investment decisions in Nigeria: The standpoint of accounting academics. Journal of

Management & Administration, 2017(1), pp.181-195.

Yusof, Y. and Ismail, S., (2016) Determinants of dividend policy of public listed companies in

Malaysia. Review of International Business and Strategy, 26(1), pp.88-99.

Patra, A. and Dhar, P., (2017) Impact of Dividend Policy on Shareholders’ Value: A Study on

Apollo Hospitals Ltd. Bharatiya Vidya Bhavan Institute of Management Science, Kolkata-97,

p.11.

Prasad, P. and Chand, P., (2017) The Changing Face of the Auditor's Report: Implications for

Suppliers and Users of Financial Statements. Australian Accounting Review, 27(4), pp.348-367.

Sirois, L.P., Bédard, J. and Bera, P. (2018) The informational value of key audit matters in the

auditor's report: Evidence from an eye-tracking study. Accounting Horizons, 32(2), pp.141-162.

Solt, F., (2016) The standardized world income inequality database. Social science

quarterly, 97(5), pp.1267-1281.

Wisdom, O., Oyebisi, O., Dorcas, A., David, A. and Oyedeji, L.Q., (2017) Auditor’s report and

investment decisions in Nigeria: The standpoint of accounting academics. Journal of

Management & Administration, 2017(1), pp.181-195.

Yusof, Y. and Ismail, S., (2016) Determinants of dividend policy of public listed companies in

Malaysia. Review of International Business and Strategy, 26(1), pp.88-99.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.