Accounting Ratios

VerifiedAdded on 2023/01/11

|8

|1935

|48

AI Summary

Please find attached Assignment Brief and Assignment structure Review Task 2 only

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting Ratios

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

TASK 2............................................................................................................................................1

1. Calculate the following five ratios...........................................................................................1

2. Compare the performance of Alpha Limited...........................................................................2

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

MAIN BODY..................................................................................................................................1

TASK 2............................................................................................................................................1

1. Calculate the following five ratios...........................................................................................1

2. Compare the performance of Alpha Limited...........................................................................2

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Accounting ratios is an essential or major sub-set of financial indicators which categories

into metrics that used to evaluate the company's performance and efficiency based on the

financial results (Haddad, Shibly and Haddad, 2020). These offer a means to explain the

relationship from one accounting set of data to the next and form the basis for interpretation of

the ratios. ALPHA Limited selected for this report, which is UK based manufacturing company.

Company began their operations in 1954 and it plans to expand its operational processes in the

next ten years to other regions of the Country. This assessment covers the several topics such as

ratio analysis and evaluates the performance through comparing two year’s financial

information.

MAIN BODY

TASK 2

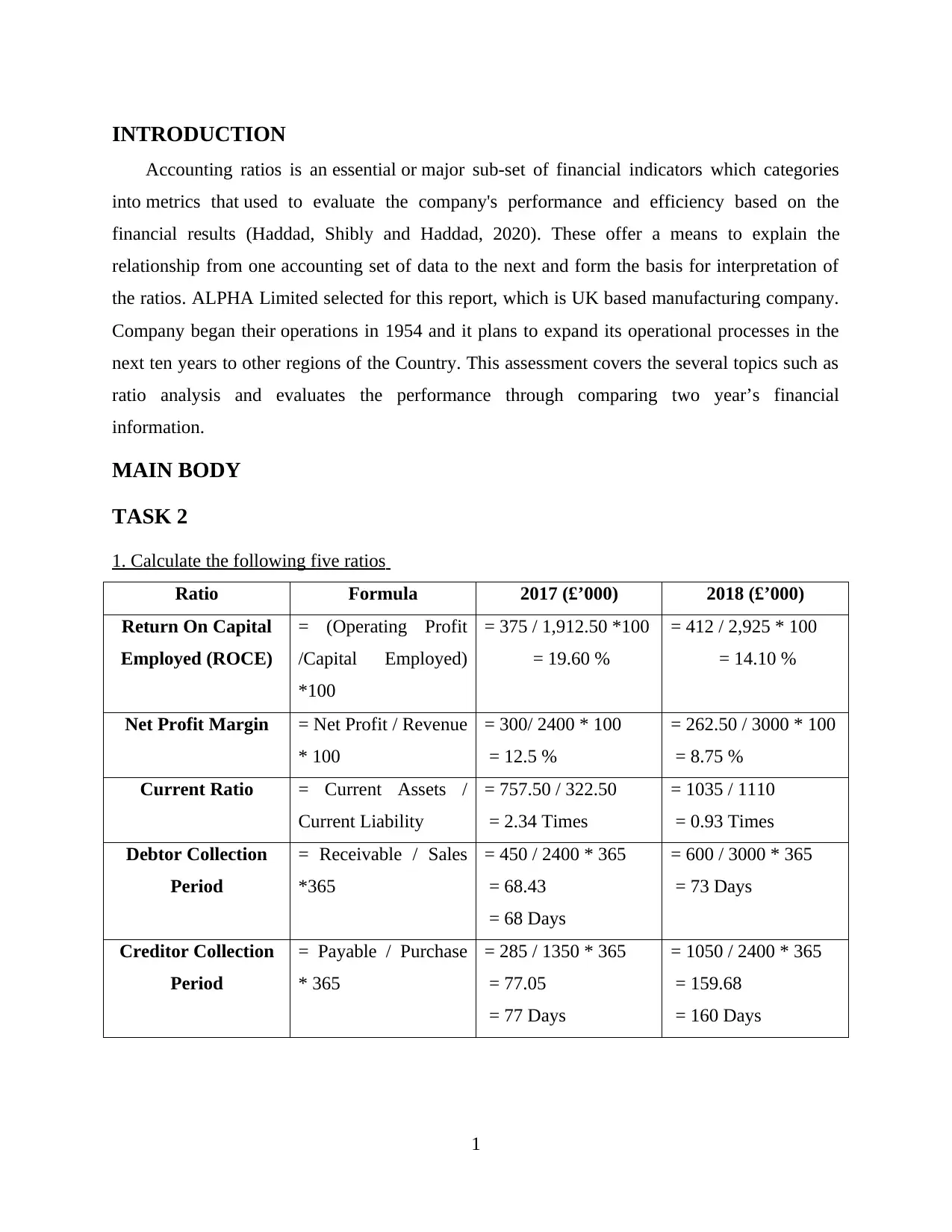

1. Calculate the following five ratios

Ratio Formula 2017 (£’000) 2018 (£’000)

Return On Capital

Employed (ROCE)

= (Operating Profit

/Capital Employed)

*100

= 375 / 1,912.50 *100

= 19.60 %

= 412 / 2,925 * 100

= 14.10 %

Net Profit Margin = Net Profit / Revenue

* 100

= 300/ 2400 * 100

= 12.5 %

= 262.50 / 3000 * 100

= 8.75 %

Current Ratio = Current Assets /

Current Liability

= 757.50 / 322.50

= 2.34 Times

= 1035 / 1110

= 0.93 Times

Debtor Collection

Period

= Receivable / Sales

*365

= 450 / 2400 * 365

= 68.43

= 68 Days

= 600 / 3000 * 365

= 73 Days

Creditor Collection

Period

= Payable / Purchase

* 365

= 285 / 1350 * 365

= 77.05

= 77 Days

= 1050 / 2400 * 365

= 159.68

= 160 Days

1

Accounting ratios is an essential or major sub-set of financial indicators which categories

into metrics that used to evaluate the company's performance and efficiency based on the

financial results (Haddad, Shibly and Haddad, 2020). These offer a means to explain the

relationship from one accounting set of data to the next and form the basis for interpretation of

the ratios. ALPHA Limited selected for this report, which is UK based manufacturing company.

Company began their operations in 1954 and it plans to expand its operational processes in the

next ten years to other regions of the Country. This assessment covers the several topics such as

ratio analysis and evaluates the performance through comparing two year’s financial

information.

MAIN BODY

TASK 2

1. Calculate the following five ratios

Ratio Formula 2017 (£’000) 2018 (£’000)

Return On Capital

Employed (ROCE)

= (Operating Profit

/Capital Employed)

*100

= 375 / 1,912.50 *100

= 19.60 %

= 412 / 2,925 * 100

= 14.10 %

Net Profit Margin = Net Profit / Revenue

* 100

= 300/ 2400 * 100

= 12.5 %

= 262.50 / 3000 * 100

= 8.75 %

Current Ratio = Current Assets /

Current Liability

= 757.50 / 322.50

= 2.34 Times

= 1035 / 1110

= 0.93 Times

Debtor Collection

Period

= Receivable / Sales

*365

= 450 / 2400 * 365

= 68.43

= 68 Days

= 600 / 3000 * 365

= 73 Days

Creditor Collection

Period

= Payable / Purchase

* 365

= 285 / 1350 * 365

= 77.05

= 77 Days

= 1050 / 2400 * 365

= 159.68

= 160 Days

1

2. Compare the performance of Alpha Limited

Return on capital employed: It is a productivity indicator that used to calculates how well

a company uses its resources (Liddle, 2018). They demonstrate how efficiently a organization

uses its properties to earn income, and are widely used by lenders to measure whether or not a

business is appropriate for investment. A higher ROCE means more effective resource use.

ROCE should be higher than the cost of capital; otherwise it would shows that the firm is not

appropriately employing its wealth and is not creating shareholder value. ROCE is especially

useful in comparing firms' results because return on equity helps in analyzing profitability only

in relation to equity of a business, ROCE often includes debt and other liabilities.

Formula:

ROCE = (Operating Profit /Capital Employed) *100

Above calculation shows that net profit of ALPHA limited is £375,000 in 2017 and £

412000 in 2018. This is calculated by the gross profit deduction and description of operating

expenses. The corporation's money spent was £ 2925000 in 2018 and £ 1912500 in 2017. In

2018 and 2017, the returns on the company’s assets were 14.10 per cent and 19.60 per cent

respectively. The decrease in this ratio implies a decrease in the contribution from the

investments made in revenue growth. By improving its net income, the manager can boost

the production performance by reducing its operational expenses and increasing the resources

employed as compared with the customer.

Net profit margin: It is the amount of income left after deduction of all costs from

revenues (Linares-Mustarós, Coenders and Vives-Mestres, 2018). The calculation shows how

much income a corporation can draw from its net revenue. The equation's net revenue is a part

of gross revenue minus any tax deductions, such as projected sales etc. Net profit margin ratio

allows investors to determine that how the management of a business earns adequate income

from its revenue, or whether fixed expenses and labour costs are included. It is among the most

essential determinants of sustainable health for a company in terms of finances.

Formula:

Net Profit Margin = Net Profit / Revenue * 100

At the time of calculating the net profit margin ratio, Alpha Ltd measured as representing

its share, which dropped from 2017 to 2018, that is in favoured of the company.Net profit margin

was 12.5 per cent in 2017 and 8.75 per cent in 2018. Alpha Ltd raise its net profit margin by

2

Return on capital employed: It is a productivity indicator that used to calculates how well

a company uses its resources (Liddle, 2018). They demonstrate how efficiently a organization

uses its properties to earn income, and are widely used by lenders to measure whether or not a

business is appropriate for investment. A higher ROCE means more effective resource use.

ROCE should be higher than the cost of capital; otherwise it would shows that the firm is not

appropriately employing its wealth and is not creating shareholder value. ROCE is especially

useful in comparing firms' results because return on equity helps in analyzing profitability only

in relation to equity of a business, ROCE often includes debt and other liabilities.

Formula:

ROCE = (Operating Profit /Capital Employed) *100

Above calculation shows that net profit of ALPHA limited is £375,000 in 2017 and £

412000 in 2018. This is calculated by the gross profit deduction and description of operating

expenses. The corporation's money spent was £ 2925000 in 2018 and £ 1912500 in 2017. In

2018 and 2017, the returns on the company’s assets were 14.10 per cent and 19.60 per cent

respectively. The decrease in this ratio implies a decrease in the contribution from the

investments made in revenue growth. By improving its net income, the manager can boost

the production performance by reducing its operational expenses and increasing the resources

employed as compared with the customer.

Net profit margin: It is the amount of income left after deduction of all costs from

revenues (Linares-Mustarós, Coenders and Vives-Mestres, 2018). The calculation shows how

much income a corporation can draw from its net revenue. The equation's net revenue is a part

of gross revenue minus any tax deductions, such as projected sales etc. Net profit margin ratio

allows investors to determine that how the management of a business earns adequate income

from its revenue, or whether fixed expenses and labour costs are included. It is among the most

essential determinants of sustainable health for a company in terms of finances.

Formula:

Net Profit Margin = Net Profit / Revenue * 100

At the time of calculating the net profit margin ratio, Alpha Ltd measured as representing

its share, which dropped from 2017 to 2018, that is in favoured of the company.Net profit margin

was 12.5 per cent in 2017 and 8.75 per cent in 2018. Alpha Ltd raise its net profit margin by

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

excluding additional costs which is not in core operations, by minimizing non-deliverable

products and services, by raising sales , customer demand and liquidity and, at times, by raising

premiums that could be challenging but necessary for profitability in industries. Overall

performance of the Alpha limited reduced which negatively impact the operational activities.

Current Ratio: It is the liquidity ratio which helps in measuring the ability of the company

to satisfy short-term obligations, with its current assets. It is a significant step, because in the

next year it will evaluate company debt obligations. It tells the company that its current short

liabilities will be offset by ample liquidity (Morales-Díaz and Zamora-Ramírez, 2018). Current

measures of properties such as currencies, financial reserves, capital and cash equivalents which

depend on their incremental translation into value. Current liabilities can be easily funded by

organizations with strong existing asset base with no need to sell serious long term resources.

This is a simple metric, determined by dividing current assets from current liabilities. The

ideal current ratio is 2:1 and every company will hold this ratio. It will be more favourable for

the company for the current equity ratio. It is mentioned that the proportion of 3:1 that also

means to the current assets which helps in paying company's liability.

Formula:

Current ratio = Current Assets / Current Liability

Compared to Alpha Ltd, calculations show that the current ratio is 2.34 times in 2017 and

0.93 times in 2018, indicating that it's more stable in 2017 and extremely illiquid in 2018.

This ratio can be strengthened by taking the required steps to increase debtors or account

payable, clear existing obligations minimize under-performing loans, boost borrowers' capital to

fulfil their debt obligations and clean up unpaid transactions. Management have to focus on their

resources to pay their obligations and they need to make sure that they balance ideal ratio.

Average Receivable days: This is a system where lenders can make hours or days to pay

organizations. The approach will essentially guarantee the cash is available to meet current

obligations (Norton, Dowd and Maciejewski, 2018). It helps know debtors are facing bankruptcy

in the long future. By identifying possible bankrupt debtors early, company will track the volume

of floor lending and dubious clauses. In a company, managers can conveniently use the debtor

collation ratio to build credit policies. Business needs to analyze this mixture to be able to

function reliably. The cash management division calculates the total amount to be obtained from

3

products and services, by raising sales , customer demand and liquidity and, at times, by raising

premiums that could be challenging but necessary for profitability in industries. Overall

performance of the Alpha limited reduced which negatively impact the operational activities.

Current Ratio: It is the liquidity ratio which helps in measuring the ability of the company

to satisfy short-term obligations, with its current assets. It is a significant step, because in the

next year it will evaluate company debt obligations. It tells the company that its current short

liabilities will be offset by ample liquidity (Morales-Díaz and Zamora-Ramírez, 2018). Current

measures of properties such as currencies, financial reserves, capital and cash equivalents which

depend on their incremental translation into value. Current liabilities can be easily funded by

organizations with strong existing asset base with no need to sell serious long term resources.

This is a simple metric, determined by dividing current assets from current liabilities. The

ideal current ratio is 2:1 and every company will hold this ratio. It will be more favourable for

the company for the current equity ratio. It is mentioned that the proportion of 3:1 that also

means to the current assets which helps in paying company's liability.

Formula:

Current ratio = Current Assets / Current Liability

Compared to Alpha Ltd, calculations show that the current ratio is 2.34 times in 2017 and

0.93 times in 2018, indicating that it's more stable in 2017 and extremely illiquid in 2018.

This ratio can be strengthened by taking the required steps to increase debtors or account

payable, clear existing obligations minimize under-performing loans, boost borrowers' capital to

fulfil their debt obligations and clean up unpaid transactions. Management have to focus on their

resources to pay their obligations and they need to make sure that they balance ideal ratio.

Average Receivable days: This is a system where lenders can make hours or days to pay

organizations. The approach will essentially guarantee the cash is available to meet current

obligations (Norton, Dowd and Maciejewski, 2018). It helps know debtors are facing bankruptcy

in the long future. By identifying possible bankrupt debtors early, company will track the volume

of floor lending and dubious clauses. In a company, managers can conveniently use the debtor

collation ratio to build credit policies. Business needs to analyze this mixture to be able to

function reliably. The cash management division calculates the total amount to be obtained from

3

the receivable company accounts or the debtor's balance. Total volume obtained is multiplied

by number of days to deliver results.

Formula:

Account receivable days = Receivable / Sales *365

From the above calculation Alpha Ltd was classified as having accounts receivables of

£450000 in 2017 and £600000 in 2018. The net sales are 24,00,000 in 2017 and 30,000,000 in

2018; then it reports the total profit figure as credit income. The cumulative reporting period for

Alpha Ltd in 2018 is 73 days, and 2017 is 68 days. A reduction in the average turnaround period

is reported here, pointing out that Alpha Ltd 's productivity needed to recover amounts from its

borrowers has deteriorated and the business may face inadequate liquid cash to conduct its

activities in the immediate future. Through rising credit transactions and maximizing the loan

term offered to its lenders then the business will increase this ratio.

Average Payable days:

The Company decides the total amount of money paid out to the borrowers and accounts

payable. Here lenders include retailers, suppliers as well as other short-term funding outlets. The

margin is measured on a monthly or yearly basis and shows how the company conducts its

money outflows (Restianti and Agustina, 2018). It would take the Company some time to pay its

numerous debts with higher creditors. It shows the company's financial potential, which suggests

that productivity is diminished or shareholders are unable to pay. Investors performing this

process also influenced the term credit.

From the calculation of Alpha Ltd accounts payables in 2017 and 2018 is expected to be

£285000 and £1050000 accordingly. Purchase by the business for the periods 2018 and 2017

were £2400000 and £1350000 separately. It's suspected both sales were on credit here. The

cumulative payable duration for the company is 160 days in 2018, and it was 77 days in 2017.

There is an increase reported over the overall payable duration which demonstrates the ability of

the organization to make purchases to its particular payable customers.

Results from the research of Alpha Ltd’s performances, it is decided that investors will not

interested in this company because the average output falls during 2017 to 2018. ROCE, net

profit or current ratio are all are in losses and because of that, investors not ready to invest and

it reduces its production during the year.

4

by number of days to deliver results.

Formula:

Account receivable days = Receivable / Sales *365

From the above calculation Alpha Ltd was classified as having accounts receivables of

£450000 in 2017 and £600000 in 2018. The net sales are 24,00,000 in 2017 and 30,000,000 in

2018; then it reports the total profit figure as credit income. The cumulative reporting period for

Alpha Ltd in 2018 is 73 days, and 2017 is 68 days. A reduction in the average turnaround period

is reported here, pointing out that Alpha Ltd 's productivity needed to recover amounts from its

borrowers has deteriorated and the business may face inadequate liquid cash to conduct its

activities in the immediate future. Through rising credit transactions and maximizing the loan

term offered to its lenders then the business will increase this ratio.

Average Payable days:

The Company decides the total amount of money paid out to the borrowers and accounts

payable. Here lenders include retailers, suppliers as well as other short-term funding outlets. The

margin is measured on a monthly or yearly basis and shows how the company conducts its

money outflows (Restianti and Agustina, 2018). It would take the Company some time to pay its

numerous debts with higher creditors. It shows the company's financial potential, which suggests

that productivity is diminished or shareholders are unable to pay. Investors performing this

process also influenced the term credit.

From the calculation of Alpha Ltd accounts payables in 2017 and 2018 is expected to be

£285000 and £1050000 accordingly. Purchase by the business for the periods 2018 and 2017

were £2400000 and £1350000 separately. It's suspected both sales were on credit here. The

cumulative payable duration for the company is 160 days in 2018, and it was 77 days in 2017.

There is an increase reported over the overall payable duration which demonstrates the ability of

the organization to make purchases to its particular payable customers.

Results from the research of Alpha Ltd’s performances, it is decided that investors will not

interested in this company because the average output falls during 2017 to 2018. ROCE, net

profit or current ratio are all are in losses and because of that, investors not ready to invest and

it reduces its production during the year.

4

CONCLUSION

From the above discussion it has been observed that accounting ratios help the organizations

to evaluate their overall business performance and operational efficiency. There are several

matrix used to evaluate the outcomes which make the decision making process more easy for

investors.

5

From the above discussion it has been observed that accounting ratios help the organizations

to evaluate their overall business performance and operational efficiency. There are several

matrix used to evaluate the outcomes which make the decision making process more easy for

investors.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals

Haddad, A. E., Shibly, F. B. and Haddad, R., 2020. Voluntary disclosure of accounting ratios and

firm-specific characteristics: the case of GCC. Journal of Financial Reporting and

Accounting.

Liddle, B., 2018. Consumption-based accounting and the trade-carbon emissions nexus. Energy

Economics. 69. pp.71-78.

Linares-Mustarós, S., Coenders, G. and Vives-Mestres, M., 2018. Financial performance and

distress profiles. From classification according to financial ratios to compositional

classification. Advances in Accounting. 40. pp.1-10.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

a new methodological approach. Accounting in Europe. 15(1). pp.105-133.

Norton, E. C., Dowd, B. E. and Maciejewski, M. L., 2018. Odds ratios—current best practice

and use. Jama. 320(1). pp.84-85.

Restianti, T. and Agustina, L., 2018. The effect of financial ratios on financial distress conditions

in sub industrial sector company. Accounting Analysis Journal. 7(1). pp.25-33.

6

Books & Journals

Haddad, A. E., Shibly, F. B. and Haddad, R., 2020. Voluntary disclosure of accounting ratios and

firm-specific characteristics: the case of GCC. Journal of Financial Reporting and

Accounting.

Liddle, B., 2018. Consumption-based accounting and the trade-carbon emissions nexus. Energy

Economics. 69. pp.71-78.

Linares-Mustarós, S., Coenders, G. and Vives-Mestres, M., 2018. Financial performance and

distress profiles. From classification according to financial ratios to compositional

classification. Advances in Accounting. 40. pp.1-10.

Morales-Díaz, J. and Zamora-Ramírez, C., 2018. The impact of IFRS 16 on key financial ratios:

a new methodological approach. Accounting in Europe. 15(1). pp.105-133.

Norton, E. C., Dowd, B. E. and Maciejewski, M. L., 2018. Odds ratios—current best practice

and use. Jama. 320(1). pp.84-85.

Restianti, T. and Agustina, L., 2018. The effect of financial ratios on financial distress conditions

in sub industrial sector company. Accounting Analysis Journal. 7(1). pp.25-33.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.