Accounting Skills Report: Financial Analysis and Budgeting Techniques

VerifiedAdded on 2021/01/01

|15

|3508

|337

Report

AI Summary

This report provides a detailed analysis of various accounting concepts and techniques. It begins with the preparation of financial statements, including an income statement and balance sheet for Fort Road Foxtrot, followed by a discussion of the differences between financial and management acco...

Accounting Skills

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A) Preparation of Income Statement and Balance sheet for Fort Road Foxtrot.....................1

B) Differences between financial and management accounting............................................2

QUESTION 2 (A)............................................................................................................................3

A) Calculations of CVP Analysis...........................................................................................3

QUESTION 2 (B) ...........................................................................................................................4

A) Decision-making and commenting on manager's argument for Sparks Ltd ....................4

B) Make or buy decision for Thunder company....................................................................4

QUESTION 3...................................................................................................................................5

A) Calculation of financial ratios and interpretation for J. P. Robard Mfg. Company..........5

B) Producing report to Gulf Banks PLC regarding recommendation for loan sanction. ......6

C) Ratio interpretation regarding the investment in the company and recommendation to

investors..................................................................................................................................7

QUESTION 4...................................................................................................................................8

A) Preparing the cash budget of ABACUS Inc......................................................................8

B) Explaining benefits and limitations of budgeting..............................................................8

QUESTION 5...................................................................................................................................9

1. A) Calculation of various variances...................................................................................9

B) Calculation of variable overhead spending variance.......................................................11

C) Computation of variable overhead efficiency variance...................................................11

2. Describing variance analysis............................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A) Preparation of Income Statement and Balance sheet for Fort Road Foxtrot.....................1

B) Differences between financial and management accounting............................................2

QUESTION 2 (A)............................................................................................................................3

A) Calculations of CVP Analysis...........................................................................................3

QUESTION 2 (B) ...........................................................................................................................4

A) Decision-making and commenting on manager's argument for Sparks Ltd ....................4

B) Make or buy decision for Thunder company....................................................................4

QUESTION 3...................................................................................................................................5

A) Calculation of financial ratios and interpretation for J. P. Robard Mfg. Company..........5

B) Producing report to Gulf Banks PLC regarding recommendation for loan sanction. ......6

C) Ratio interpretation regarding the investment in the company and recommendation to

investors..................................................................................................................................7

QUESTION 4...................................................................................................................................8

A) Preparing the cash budget of ABACUS Inc......................................................................8

B) Explaining benefits and limitations of budgeting..............................................................8

QUESTION 5...................................................................................................................................9

1. A) Calculation of various variances...................................................................................9

B) Calculation of variable overhead spending variance.......................................................11

C) Computation of variable overhead efficiency variance...................................................11

2. Describing variance analysis............................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Accounting is an integral part of the company directing towards assessing business

operations in financial terms so that proper records could be kept and financial statements may

be prepared. Present report deals with various scenarios where financials are produced from

adjusted trial balance. CVP analysis is conducted, financial ratios have been calculated.

Moreover, cash budget is prepared and advantages and limitations of budgeting is done.

Furthermore, variance analysis is devised and accounting is done.

QUESTION 1

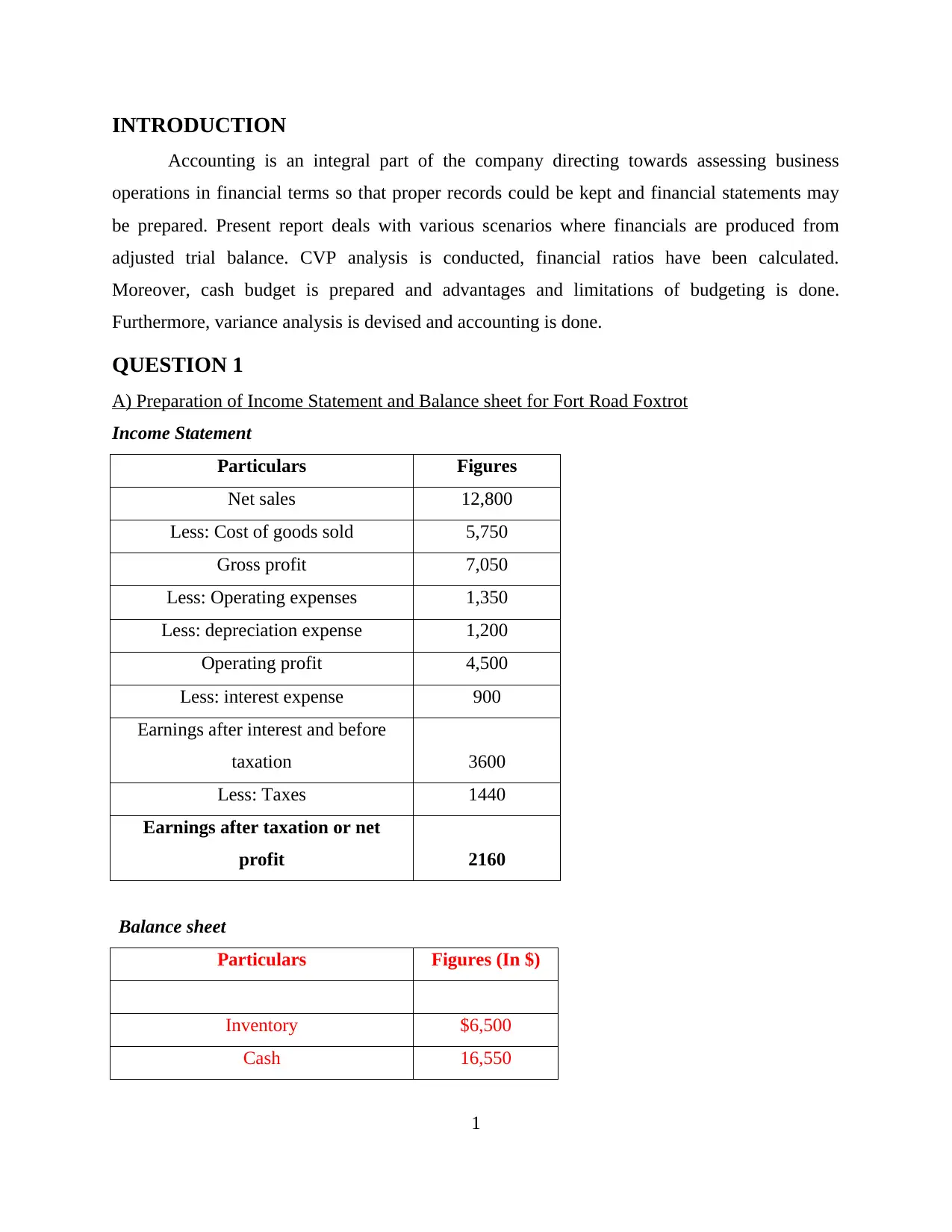

A) Preparation of Income Statement and Balance sheet for Fort Road Foxtrot

Income Statement

Particulars Figures

Net sales 12,800

Less: Cost of goods sold 5,750

Gross profit 7,050

Less: Operating expenses 1,350

Less: depreciation expense 1,200

Operating profit 4,500

Less: interest expense 900

Earnings after interest and before

taxation 3600

Less: Taxes 1440

Earnings after taxation or net

profit 2160

Balance sheet

Particulars Figures (In $)

Inventory $6,500

Cash 16,550

1

Accounting is an integral part of the company directing towards assessing business

operations in financial terms so that proper records could be kept and financial statements may

be prepared. Present report deals with various scenarios where financials are produced from

adjusted trial balance. CVP analysis is conducted, financial ratios have been calculated.

Moreover, cash budget is prepared and advantages and limitations of budgeting is done.

Furthermore, variance analysis is devised and accounting is done.

QUESTION 1

A) Preparation of Income Statement and Balance sheet for Fort Road Foxtrot

Income Statement

Particulars Figures

Net sales 12,800

Less: Cost of goods sold 5,750

Gross profit 7,050

Less: Operating expenses 1,350

Less: depreciation expense 1,200

Operating profit 4,500

Less: interest expense 900

Earnings after interest and before

taxation 3600

Less: Taxes 1440

Earnings after taxation or net

profit 2160

Balance sheet

Particulars Figures (In $)

Inventory $6,500

Cash 16,550

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounts receivable 9,600

Total current assets $32,650

Buildings and equipment 122,000

Less: Accumulated depreciation 34,000

Net fixed assets 88,000

Total assets $120,650

Liabilities

Current Liabilities

Notes payable 600

Accounts payable 4,800

Total current liabilities 5,400

Long-term debt 55,000

Capital 45000

Retained earnings 15,250

Add: net profit 2160

Total shareholders equity 62,410

Total liabilities 122,810

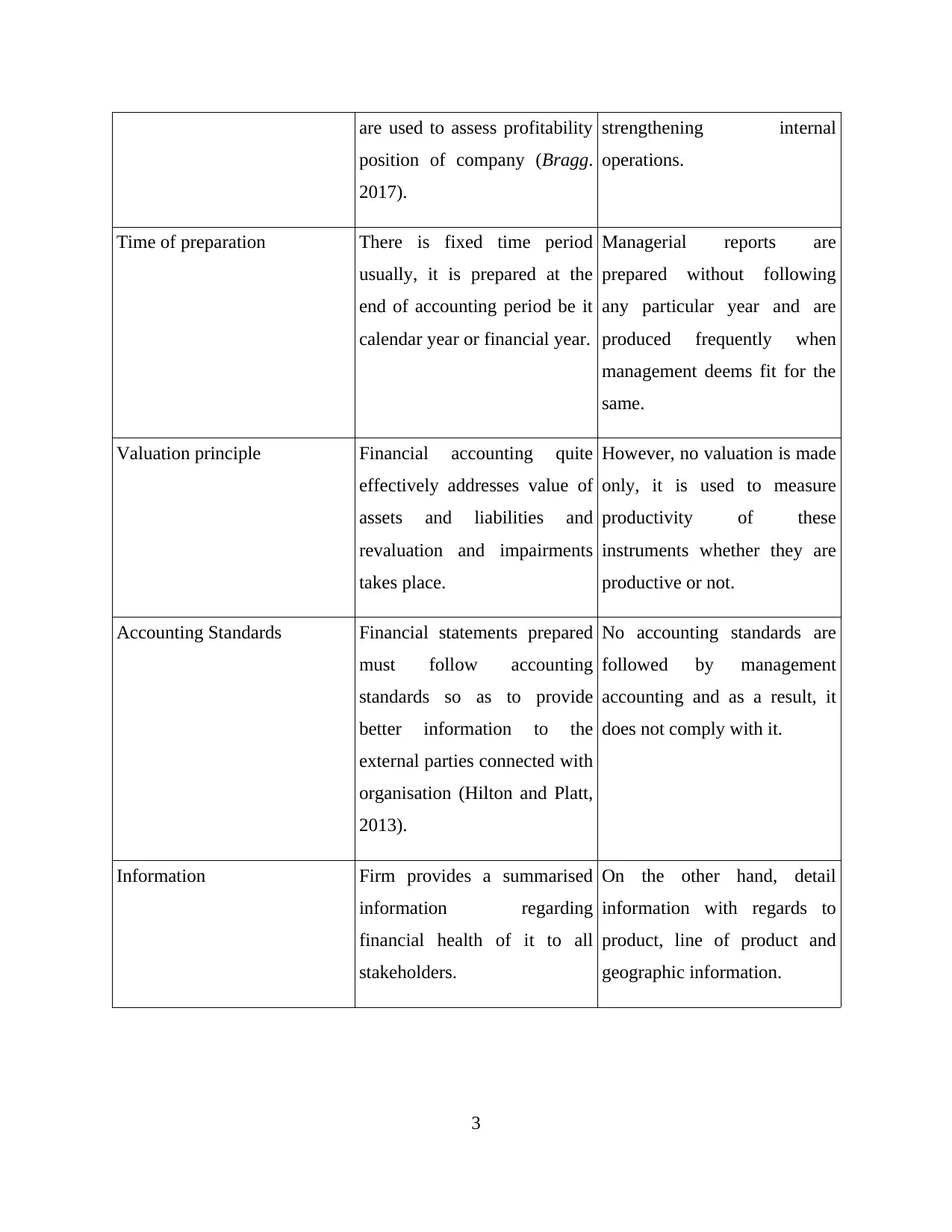

B) Differences between financial and management accounting

Basis of differentiation Financial Accounting Management Accounting

Users of accounting

information

External and internal users are

benefited as from financial

accounting, various financial

statements are prepared which

Only internal users such as top

management are provided with

information which helps to

make decisions for

2

Total current assets $32,650

Buildings and equipment 122,000

Less: Accumulated depreciation 34,000

Net fixed assets 88,000

Total assets $120,650

Liabilities

Current Liabilities

Notes payable 600

Accounts payable 4,800

Total current liabilities 5,400

Long-term debt 55,000

Capital 45000

Retained earnings 15,250

Add: net profit 2160

Total shareholders equity 62,410

Total liabilities 122,810

B) Differences between financial and management accounting

Basis of differentiation Financial Accounting Management Accounting

Users of accounting

information

External and internal users are

benefited as from financial

accounting, various financial

statements are prepared which

Only internal users such as top

management are provided with

information which helps to

make decisions for

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

are used to assess profitability

position of company (Bragg.

2017).

strengthening internal

operations.

Time of preparation There is fixed time period

usually, it is prepared at the

end of accounting period be it

calendar year or financial year.

Managerial reports are

prepared without following

any particular year and are

produced frequently when

management deems fit for the

same.

Valuation principle Financial accounting quite

effectively addresses value of

assets and liabilities and

revaluation and impairments

takes place.

However, no valuation is made

only, it is used to measure

productivity of these

instruments whether they are

productive or not.

Accounting Standards Financial statements prepared

must follow accounting

standards so as to provide

better information to the

external parties connected with

organisation (Hilton and Platt,

2013).

No accounting standards are

followed by management

accounting and as a result, it

does not comply with it.

Information Firm provides a summarised

information regarding

financial health of it to all

stakeholders.

On the other hand, detail

information with regards to

product, line of product and

geographic information.

3

position of company (Bragg.

2017).

strengthening internal

operations.

Time of preparation There is fixed time period

usually, it is prepared at the

end of accounting period be it

calendar year or financial year.

Managerial reports are

prepared without following

any particular year and are

produced frequently when

management deems fit for the

same.

Valuation principle Financial accounting quite

effectively addresses value of

assets and liabilities and

revaluation and impairments

takes place.

However, no valuation is made

only, it is used to measure

productivity of these

instruments whether they are

productive or not.

Accounting Standards Financial statements prepared

must follow accounting

standards so as to provide

better information to the

external parties connected with

organisation (Hilton and Platt,

2013).

No accounting standards are

followed by management

accounting and as a result, it

does not comply with it.

Information Firm provides a summarised

information regarding

financial health of it to all

stakeholders.

On the other hand, detail

information with regards to

product, line of product and

geographic information.

3

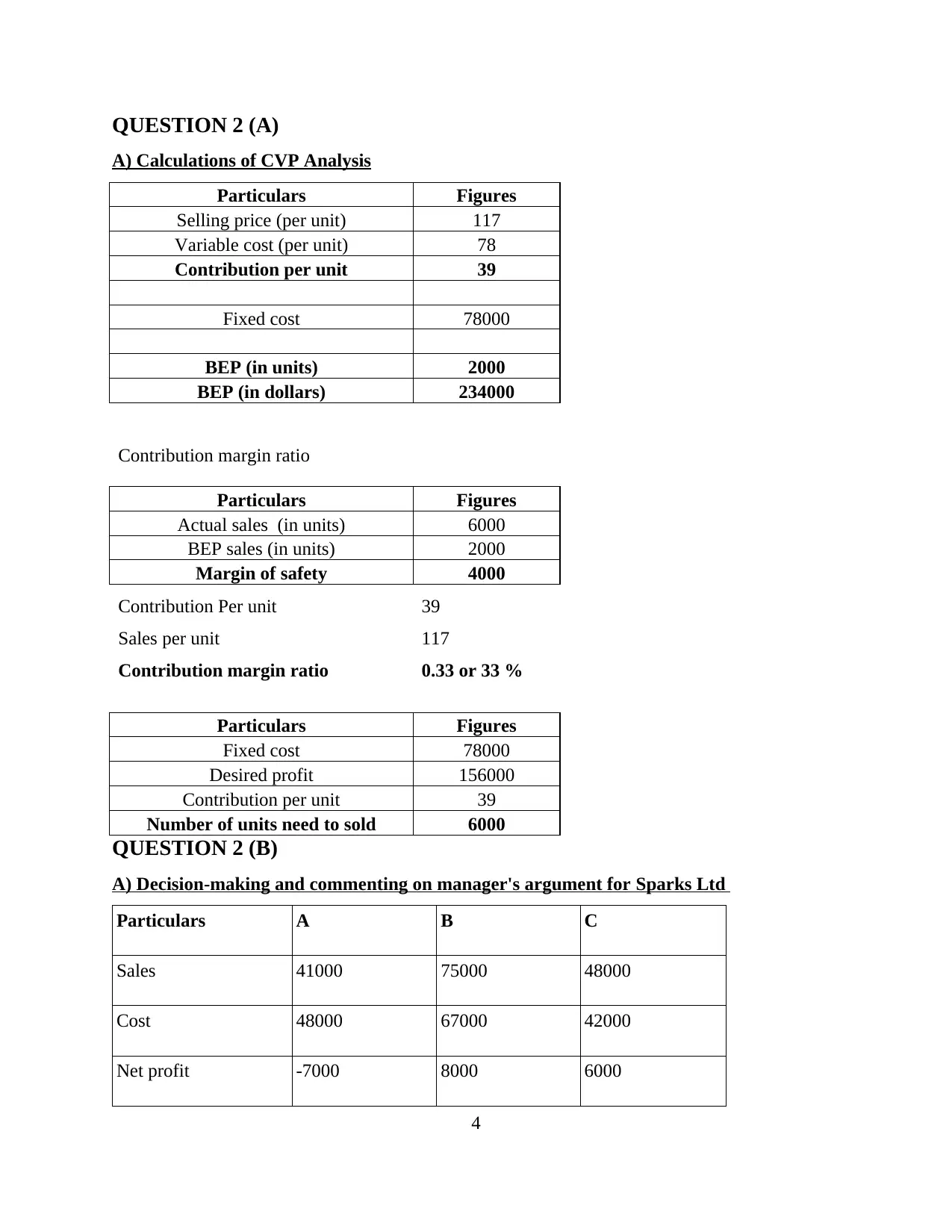

QUESTION 2 (A)

A) Calculations of CVP Analysis

Particulars Figures

Selling price (per unit) 117

Variable cost (per unit) 78

Contribution per unit 39

Fixed cost 78000

BEP (in units) 2000

BEP (in dollars) 234000

Contribution margin ratio

Particulars Figures

Actual sales (in units) 6000

BEP sales (in units) 2000

Margin of safety 4000

Contribution Per unit 39

Sales per unit 117

Contribution margin ratio 0.33 or 33 %

Particulars Figures

Fixed cost 78000

Desired profit 156000

Contribution per unit 39

Number of units need to sold 6000

QUESTION 2 (B)

A) Decision-making and commenting on manager's argument for Sparks Ltd

Particulars A B C

Sales 41000 75000 48000

Cost 48000 67000 42000

Net profit -7000 8000 6000

4

A) Calculations of CVP Analysis

Particulars Figures

Selling price (per unit) 117

Variable cost (per unit) 78

Contribution per unit 39

Fixed cost 78000

BEP (in units) 2000

BEP (in dollars) 234000

Contribution margin ratio

Particulars Figures

Actual sales (in units) 6000

BEP sales (in units) 2000

Margin of safety 4000

Contribution Per unit 39

Sales per unit 117

Contribution margin ratio 0.33 or 33 %

Particulars Figures

Fixed cost 78000

Desired profit 156000

Contribution per unit 39

Number of units need to sold 6000

QUESTION 2 (B)

A) Decision-making and commenting on manager's argument for Sparks Ltd

Particulars A B C

Sales 41000 75000 48000

Cost 48000 67000 42000

Net profit -7000 8000 6000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above estimation of costs and revenue is provided which clarifies about three

products for the forthcoming year in effective manner. It can be analysed that manager said that

product A should be discontinued as it will make loss because of less profit. However, sales

estimated are 41000 and costs associated with it is 48000. This clearly shows that cost is required

to be reduced up to a high extent so that profits could be attained in the best possible manner.

This would be beneficial for company in accomplishing profits. If costs are not minimised, then

firm will lend into loss and as a result, revenue will be unfavourable as expenses would exceed.

Hence, it is recommended not to discontinue product A and minimise expenditures on it.

B) Make or buy decision for Thunder company

Costs Amount

Purchasing units (15000 * 34) 510000

Cost of Materials 17.95%

Cost of labour 33.33%

Cost of variable manufacturing overhead 23.08%

Cost of fixed manufacturing overhead 25.64%

Total costs 100.00%

The scenario provides clarity regarding the unit cost of production. It can be analysed that

firm can purchase the product. The firm can produce 15000 units of 3741 product. Furthermore,

it will be able to generate 15000 of contribution margin by making another commodity in the

best possible manner. Moreover, by purchasing part, 75 % of fixed manufacturing overhead will

have to be incurred. This means that firm can reduce upon direct material, direct labour and

variable manufacturing overheads in effective way. It implies that nearly 74.36 % of cost can be

incurred by doubling production units. Hence, fixed expenses could be set off easily as more of

5

products for the forthcoming year in effective manner. It can be analysed that manager said that

product A should be discontinued as it will make loss because of less profit. However, sales

estimated are 41000 and costs associated with it is 48000. This clearly shows that cost is required

to be reduced up to a high extent so that profits could be attained in the best possible manner.

This would be beneficial for company in accomplishing profits. If costs are not minimised, then

firm will lend into loss and as a result, revenue will be unfavourable as expenses would exceed.

Hence, it is recommended not to discontinue product A and minimise expenditures on it.

B) Make or buy decision for Thunder company

Costs Amount

Purchasing units (15000 * 34) 510000

Cost of Materials 17.95%

Cost of labour 33.33%

Cost of variable manufacturing overhead 23.08%

Cost of fixed manufacturing overhead 25.64%

Total costs 100.00%

The scenario provides clarity regarding the unit cost of production. It can be analysed that

firm can purchase the product. The firm can produce 15000 units of 3741 product. Furthermore,

it will be able to generate 15000 of contribution margin by making another commodity in the

best possible manner. Moreover, by purchasing part, 75 % of fixed manufacturing overhead will

have to be incurred. This means that firm can reduce upon direct material, direct labour and

variable manufacturing overheads in effective way. It implies that nearly 74.36 % of cost can be

incurred by doubling production units. Hence, fixed expenses could be set off easily as more of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the manufacturing can be done. It will be fruitful for Thunder company to buy the part and make

higher level of production (DRURY, 2013).

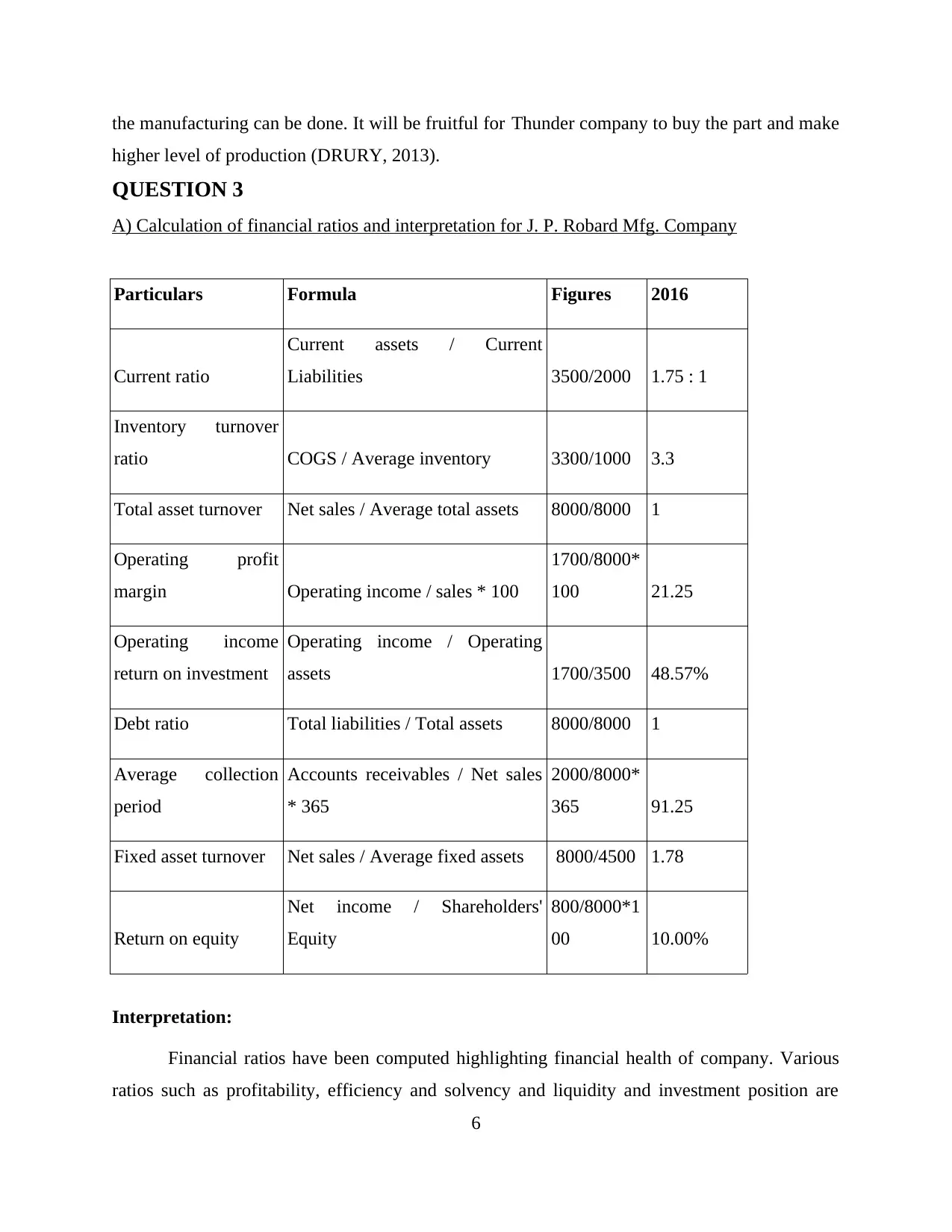

QUESTION 3

A) Calculation of financial ratios and interpretation for J. P. Robard Mfg. Company

Particulars Formula Figures 2016

Current ratio

Current assets / Current

Liabilities 3500/2000 1.75 : 1

Inventory turnover

ratio COGS / Average inventory 3300/1000 3.3

Total asset turnover Net sales / Average total assets 8000/8000 1

Operating profit

margin Operating income / sales * 100

1700/8000*

100 21.25

Operating income

return on investment

Operating income / Operating

assets 1700/3500 48.57%

Debt ratio Total liabilities / Total assets 8000/8000 1

Average collection

period

Accounts receivables / Net sales

* 365

2000/8000*

365 91.25

Fixed asset turnover Net sales / Average fixed assets 8000/4500 1.78

Return on equity

Net income / Shareholders'

Equity

800/8000*1

00 10.00%

Interpretation:

Financial ratios have been computed highlighting financial health of company. Various

ratios such as profitability, efficiency and solvency and liquidity and investment position are

6

higher level of production (DRURY, 2013).

QUESTION 3

A) Calculation of financial ratios and interpretation for J. P. Robard Mfg. Company

Particulars Formula Figures 2016

Current ratio

Current assets / Current

Liabilities 3500/2000 1.75 : 1

Inventory turnover

ratio COGS / Average inventory 3300/1000 3.3

Total asset turnover Net sales / Average total assets 8000/8000 1

Operating profit

margin Operating income / sales * 100

1700/8000*

100 21.25

Operating income

return on investment

Operating income / Operating

assets 1700/3500 48.57%

Debt ratio Total liabilities / Total assets 8000/8000 1

Average collection

period

Accounts receivables / Net sales

* 365

2000/8000*

365 91.25

Fixed asset turnover Net sales / Average fixed assets 8000/4500 1.78

Return on equity

Net income / Shareholders'

Equity

800/8000*1

00 10.00%

Interpretation:

Financial ratios have been computed highlighting financial health of company. Various

ratios such as profitability, efficiency and solvency and liquidity and investment position are

6

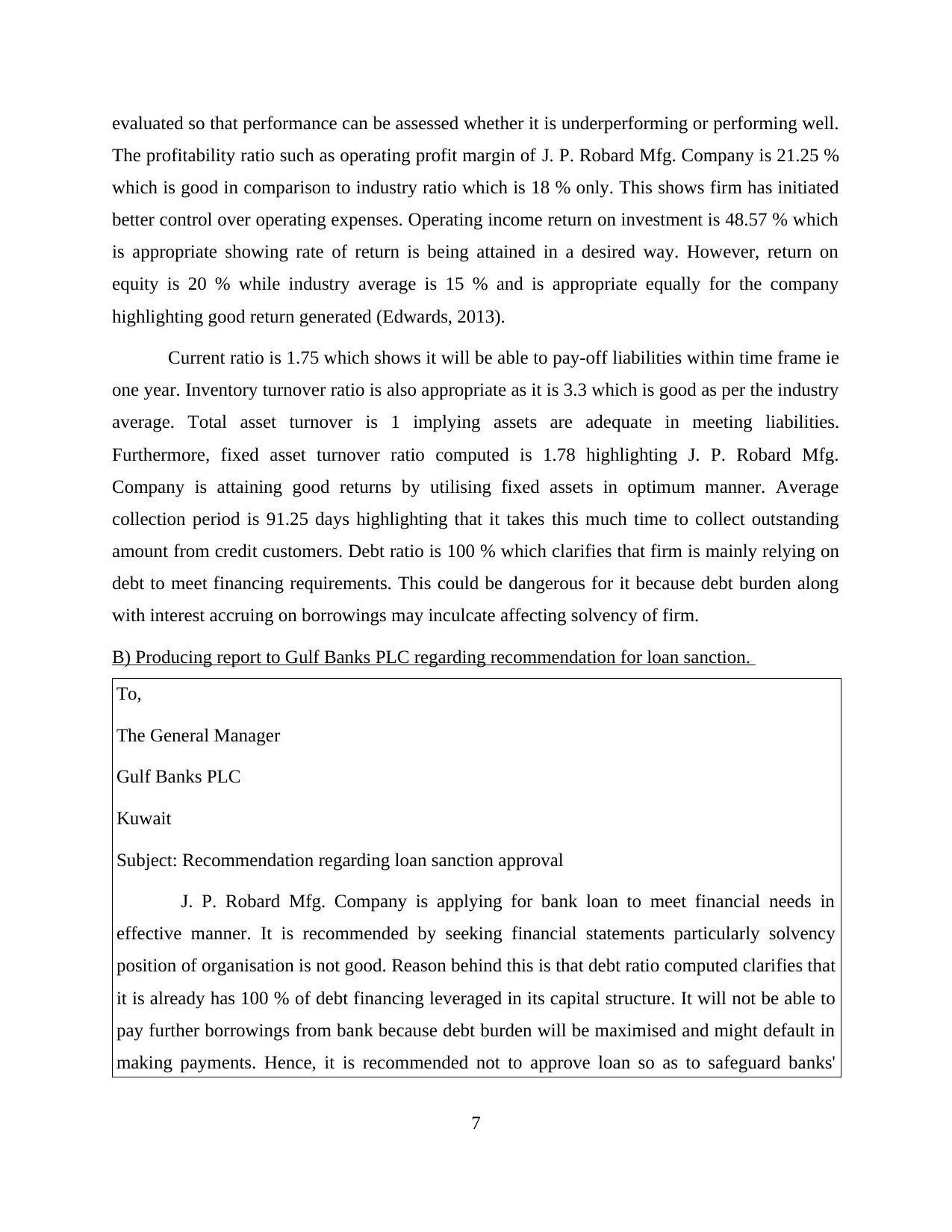

evaluated so that performance can be assessed whether it is underperforming or performing well.

The profitability ratio such as operating profit margin of J. P. Robard Mfg. Company is 21.25 %

which is good in comparison to industry ratio which is 18 % only. This shows firm has initiated

better control over operating expenses. Operating income return on investment is 48.57 % which

is appropriate showing rate of return is being attained in a desired way. However, return on

equity is 20 % while industry average is 15 % and is appropriate equally for the company

highlighting good return generated (Edwards, 2013).

Current ratio is 1.75 which shows it will be able to pay-off liabilities within time frame ie

one year. Inventory turnover ratio is also appropriate as it is 3.3 which is good as per the industry

average. Total asset turnover is 1 implying assets are adequate in meeting liabilities.

Furthermore, fixed asset turnover ratio computed is 1.78 highlighting J. P. Robard Mfg.

Company is attaining good returns by utilising fixed assets in optimum manner. Average

collection period is 91.25 days highlighting that it takes this much time to collect outstanding

amount from credit customers. Debt ratio is 100 % which clarifies that firm is mainly relying on

debt to meet financing requirements. This could be dangerous for it because debt burden along

with interest accruing on borrowings may inculcate affecting solvency of firm.

B) Producing report to Gulf Banks PLC regarding recommendation for loan sanction.

To,

The General Manager

Gulf Banks PLC

Kuwait

Subject: Recommendation regarding loan sanction approval

J. P. Robard Mfg. Company is applying for bank loan to meet financial needs in

effective manner. It is recommended by seeking financial statements particularly solvency

position of organisation is not good. Reason behind this is that debt ratio computed clarifies that

it is already has 100 % of debt financing leveraged in its capital structure. It will not be able to

pay further borrowings from bank because debt burden will be maximised and might default in

making payments. Hence, it is recommended not to approve loan so as to safeguard banks'

7

The profitability ratio such as operating profit margin of J. P. Robard Mfg. Company is 21.25 %

which is good in comparison to industry ratio which is 18 % only. This shows firm has initiated

better control over operating expenses. Operating income return on investment is 48.57 % which

is appropriate showing rate of return is being attained in a desired way. However, return on

equity is 20 % while industry average is 15 % and is appropriate equally for the company

highlighting good return generated (Edwards, 2013).

Current ratio is 1.75 which shows it will be able to pay-off liabilities within time frame ie

one year. Inventory turnover ratio is also appropriate as it is 3.3 which is good as per the industry

average. Total asset turnover is 1 implying assets are adequate in meeting liabilities.

Furthermore, fixed asset turnover ratio computed is 1.78 highlighting J. P. Robard Mfg.

Company is attaining good returns by utilising fixed assets in optimum manner. Average

collection period is 91.25 days highlighting that it takes this much time to collect outstanding

amount from credit customers. Debt ratio is 100 % which clarifies that firm is mainly relying on

debt to meet financing requirements. This could be dangerous for it because debt burden along

with interest accruing on borrowings may inculcate affecting solvency of firm.

B) Producing report to Gulf Banks PLC regarding recommendation for loan sanction.

To,

The General Manager

Gulf Banks PLC

Kuwait

Subject: Recommendation regarding loan sanction approval

J. P. Robard Mfg. Company is applying for bank loan to meet financial needs in

effective manner. It is recommended by seeking financial statements particularly solvency

position of organisation is not good. Reason behind this is that debt ratio computed clarifies that

it is already has 100 % of debt financing leveraged in its capital structure. It will not be able to

pay further borrowings from bank because debt burden will be maximised and might default in

making payments. Hence, it is recommended not to approve loan so as to safeguard banks'

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

interest.

C) Ratio interpretation regarding the investment in the company and recommendation to

investors

To,

The Investors

J. P. Robard Mfg. Company

Subject: Recommendation regarding investment

Financial position of J. P. Robard Mfg. Company is good as it is earning good amount

of profits and returns are higher in comparison to industrial average, in fact, position is good.

Investment should be made by investors by seeking profitability and investment ratios which

are calculated above. Particularly, Return in equity turns out to be 20 % implying organisation

is attaining higher returns i.e. income. In other words, J. P. Robard Mfg. Company is wisely

using investment done by shareholders up to a high extent better than industrial figures. Hence,

it is recommended to investors that they can invest their money in company for seeking better

returns and achieving higher dividends.

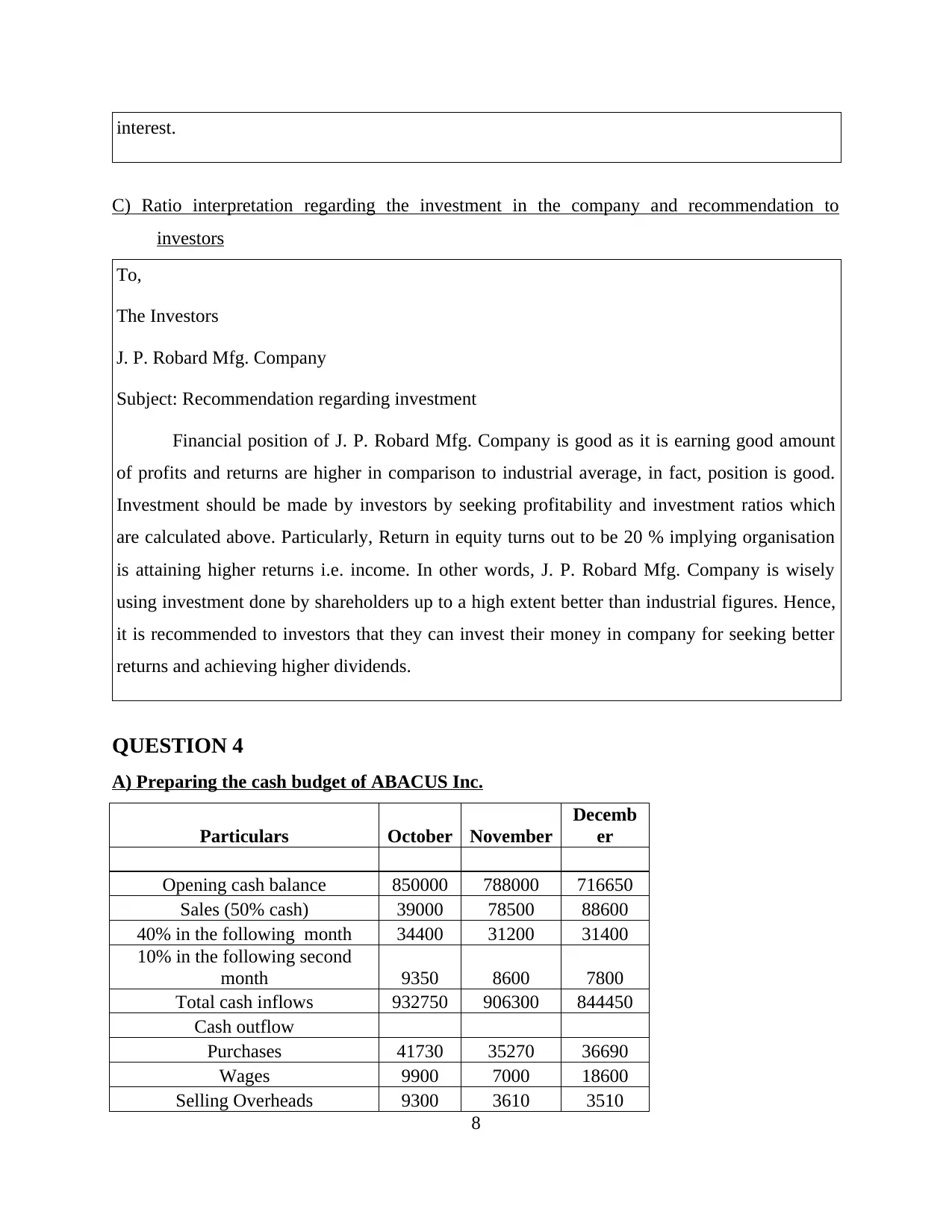

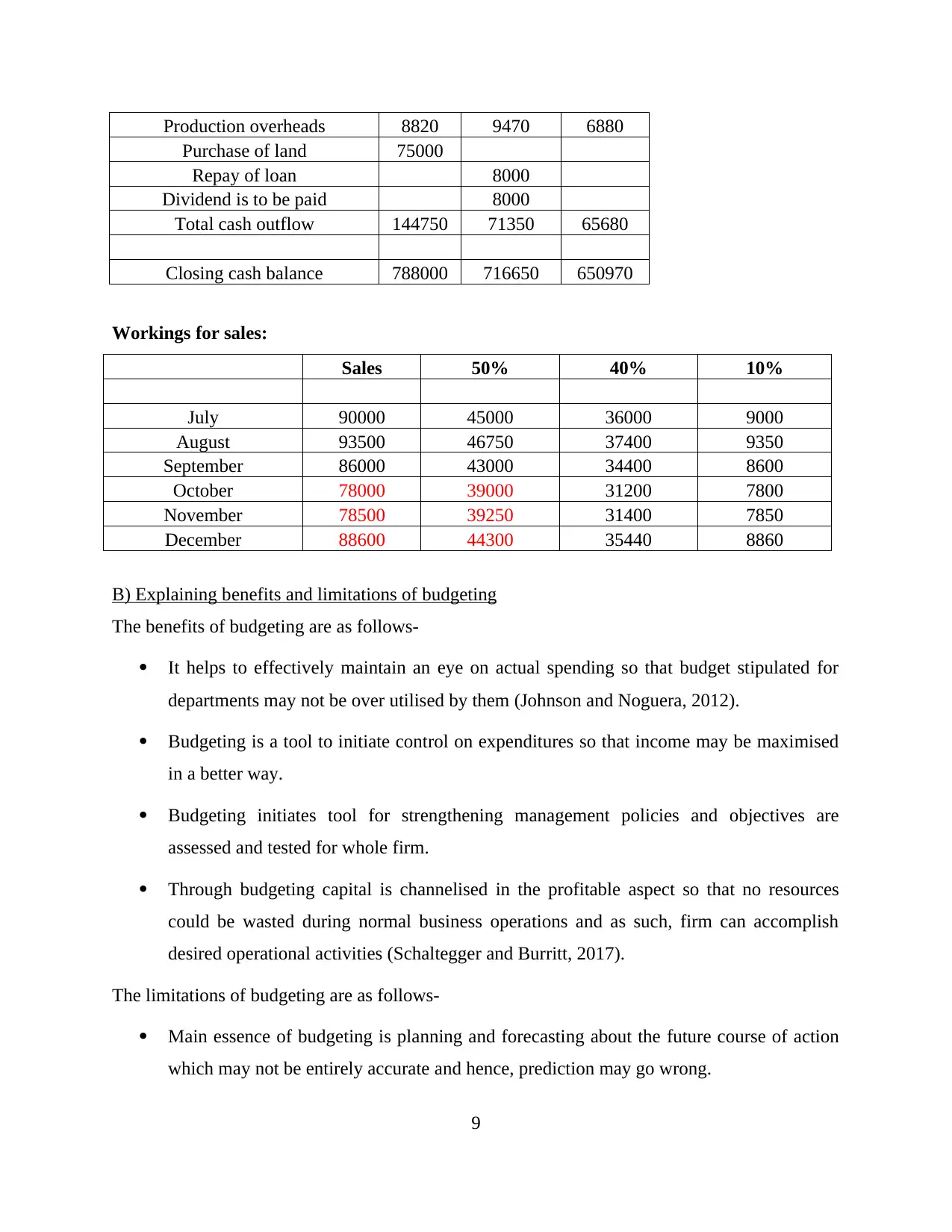

QUESTION 4

A) Preparing the cash budget of ABACUS Inc.

Particulars October November

Decemb

er

Opening cash balance 850000 788000 716650

Sales (50% cash) 39000 78500 88600

40% in the following month 34400 31200 31400

10% in the following second

month 9350 8600 7800

Total cash inflows 932750 906300 844450

Cash outflow

Purchases 41730 35270 36690

Wages 9900 7000 18600

Selling Overheads 9300 3610 3510

8

C) Ratio interpretation regarding the investment in the company and recommendation to

investors

To,

The Investors

J. P. Robard Mfg. Company

Subject: Recommendation regarding investment

Financial position of J. P. Robard Mfg. Company is good as it is earning good amount

of profits and returns are higher in comparison to industrial average, in fact, position is good.

Investment should be made by investors by seeking profitability and investment ratios which

are calculated above. Particularly, Return in equity turns out to be 20 % implying organisation

is attaining higher returns i.e. income. In other words, J. P. Robard Mfg. Company is wisely

using investment done by shareholders up to a high extent better than industrial figures. Hence,

it is recommended to investors that they can invest their money in company for seeking better

returns and achieving higher dividends.

QUESTION 4

A) Preparing the cash budget of ABACUS Inc.

Particulars October November

Decemb

er

Opening cash balance 850000 788000 716650

Sales (50% cash) 39000 78500 88600

40% in the following month 34400 31200 31400

10% in the following second

month 9350 8600 7800

Total cash inflows 932750 906300 844450

Cash outflow

Purchases 41730 35270 36690

Wages 9900 7000 18600

Selling Overheads 9300 3610 3510

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production overheads 8820 9470 6880

Purchase of land 75000

Repay of loan 8000

Dividend is to be paid 8000

Total cash outflow 144750 71350 65680

Closing cash balance 788000 716650 650970

Workings for sales:

Sales 50% 40% 10%

July 90000 45000 36000 9000

August 93500 46750 37400 9350

September 86000 43000 34400 8600

October 78000 39000 31200 7800

November 78500 39250 31400 7850

December 88600 44300 35440 8860

B) Explaining benefits and limitations of budgeting

The benefits of budgeting are as follows-

It helps to effectively maintain an eye on actual spending so that budget stipulated for

departments may not be over utilised by them (Johnson and Noguera, 2012).

Budgeting is a tool to initiate control on expenditures so that income may be maximised

in a better way.

Budgeting initiates tool for strengthening management policies and objectives are

assessed and tested for whole firm.

Through budgeting capital is channelised in the profitable aspect so that no resources

could be wasted during normal business operations and as such, firm can accomplish

desired operational activities (Schaltegger and Burritt, 2017).

The limitations of budgeting are as follows-

Main essence of budgeting is planning and forecasting about the future course of action

which may not be entirely accurate and hence, prediction may go wrong.

9

Purchase of land 75000

Repay of loan 8000

Dividend is to be paid 8000

Total cash outflow 144750 71350 65680

Closing cash balance 788000 716650 650970

Workings for sales:

Sales 50% 40% 10%

July 90000 45000 36000 9000

August 93500 46750 37400 9350

September 86000 43000 34400 8600

October 78000 39000 31200 7800

November 78500 39250 31400 7850

December 88600 44300 35440 8860

B) Explaining benefits and limitations of budgeting

The benefits of budgeting are as follows-

It helps to effectively maintain an eye on actual spending so that budget stipulated for

departments may not be over utilised by them (Johnson and Noguera, 2012).

Budgeting is a tool to initiate control on expenditures so that income may be maximised

in a better way.

Budgeting initiates tool for strengthening management policies and objectives are

assessed and tested for whole firm.

Through budgeting capital is channelised in the profitable aspect so that no resources

could be wasted during normal business operations and as such, firm can accomplish

desired operational activities (Schaltegger and Burritt, 2017).

The limitations of budgeting are as follows-

Main essence of budgeting is planning and forecasting about the future course of action

which may not be entirely accurate and hence, prediction may go wrong.

9

Since, business operates in a uncertain environment, nothing remains stable and

ABACUS Inc. may not be able to prepare budget with certainty of events.

Budgeting is a whole procedure which is directly linked to entire departments of

organisation. Top management should consult and make participation with other units so

that with better coordination, operations can be injected. However, coordination does not

prevail.

QUESTION 5

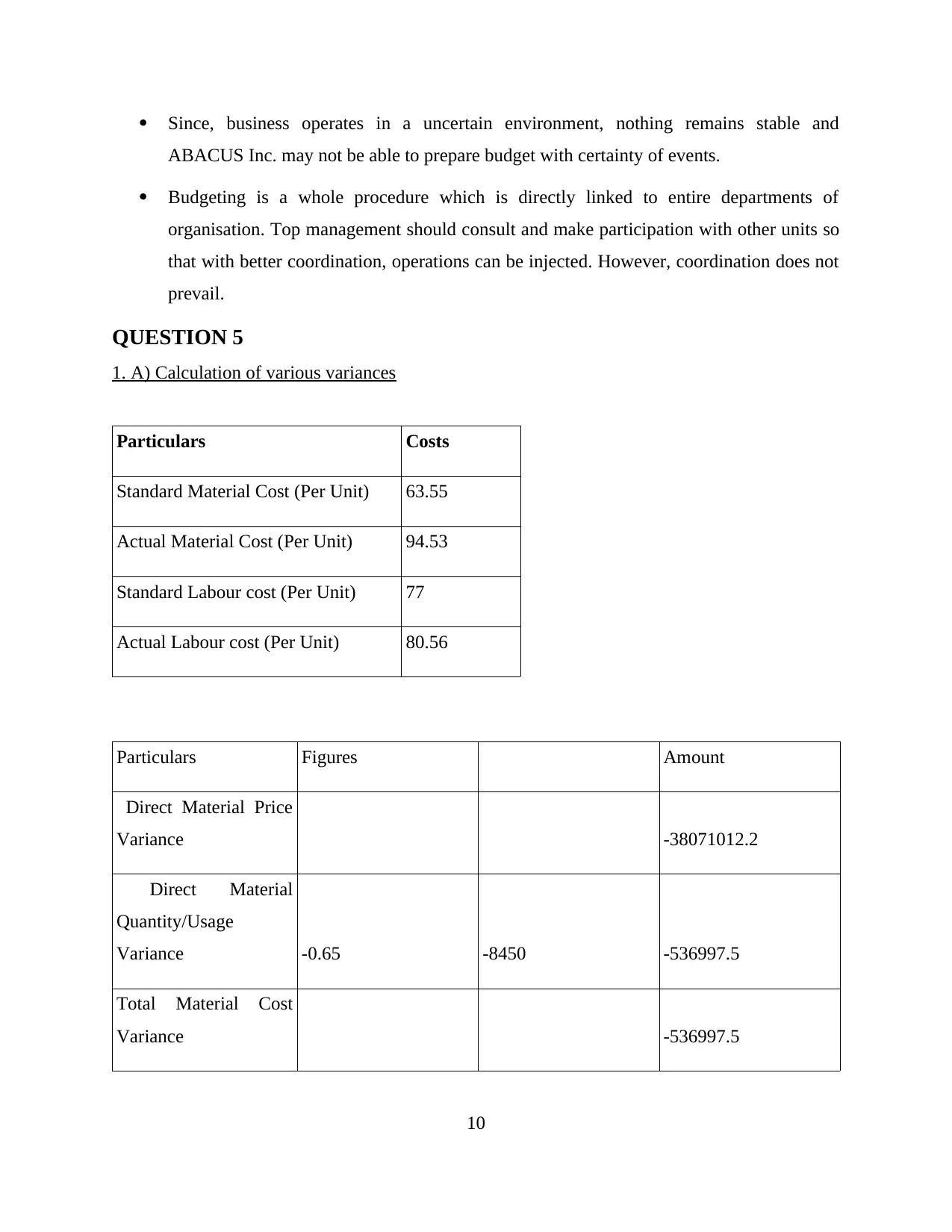

1. A) Calculation of various variances

Particulars Costs

Standard Material Cost (Per Unit) 63.55

Actual Material Cost (Per Unit) 94.53

Standard Labour cost (Per Unit) 77

Actual Labour cost (Per Unit) 80.56

Particulars Figures Amount

Direct Material Price

Variance -38071012.2

Direct Material

Quantity/Usage

Variance -0.65 -8450 -536997.5

Total Material Cost

Variance -536997.5

10

ABACUS Inc. may not be able to prepare budget with certainty of events.

Budgeting is a whole procedure which is directly linked to entire departments of

organisation. Top management should consult and make participation with other units so

that with better coordination, operations can be injected. However, coordination does not

prevail.

QUESTION 5

1. A) Calculation of various variances

Particulars Costs

Standard Material Cost (Per Unit) 63.55

Actual Material Cost (Per Unit) 94.53

Standard Labour cost (Per Unit) 77

Actual Labour cost (Per Unit) 80.56

Particulars Figures Amount

Direct Material Price

Variance -38071012.2

Direct Material

Quantity/Usage

Variance -0.65 -8450 -536997.5

Total Material Cost

Variance -536997.5

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

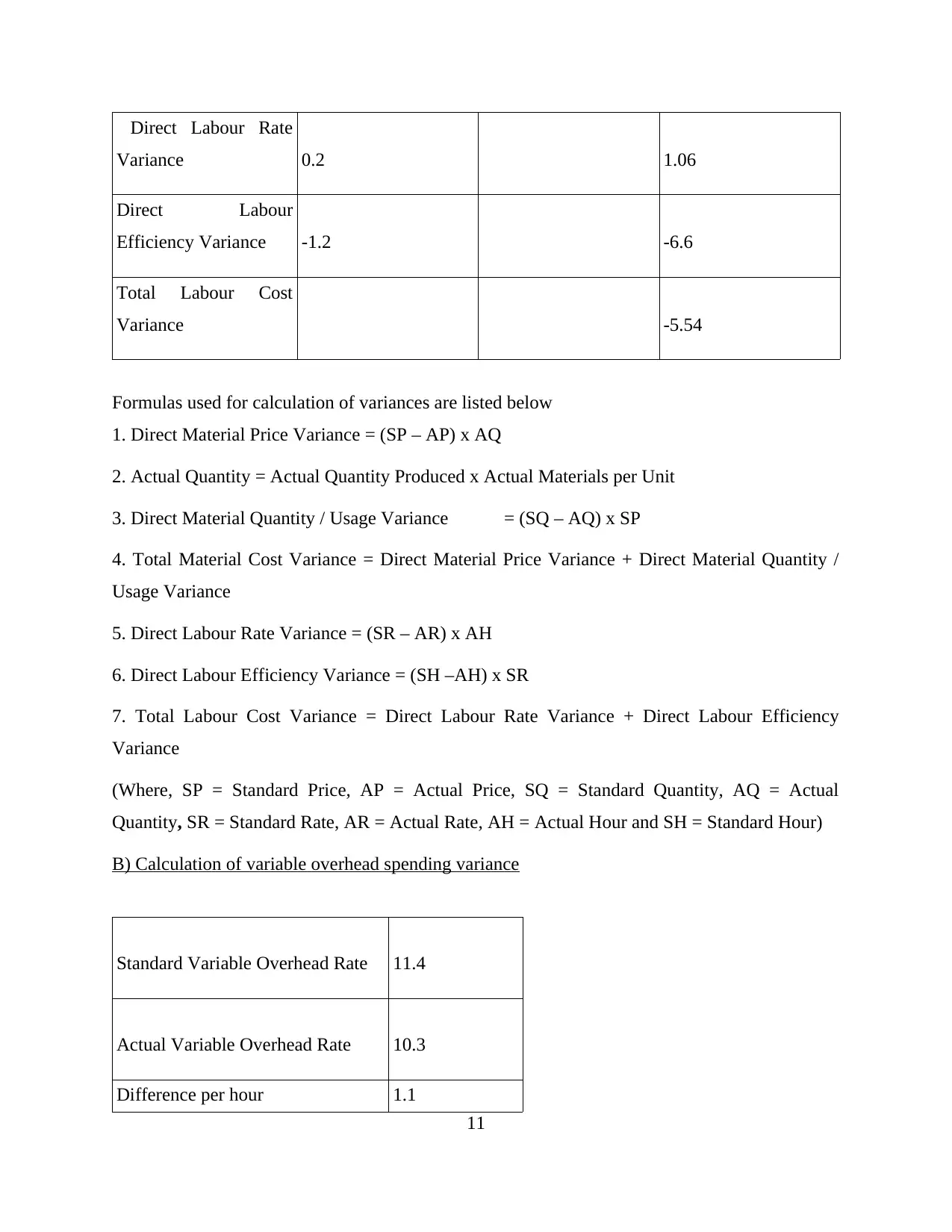

Direct Labour Rate

Variance 0.2 1.06

Direct Labour

Efficiency Variance -1.2 -6.6

Total Labour Cost

Variance -5.54

Formulas used for calculation of variances are listed below

1. Direct Material Price Variance = (SP – AP) x AQ

2. Actual Quantity = Actual Quantity Produced x Actual Materials per Unit

3. Direct Material Quantity / Usage Variance = (SQ – AQ) x SP

4. Total Material Cost Variance = Direct Material Price Variance + Direct Material Quantity /

Usage Variance

5. Direct Labour Rate Variance = (SR – AR) x AH

6. Direct Labour Efficiency Variance = (SH –AH) x SR

7. Total Labour Cost Variance = Direct Labour Rate Variance + Direct Labour Efficiency

Variance

(Where, SP = Standard Price, AP = Actual Price, SQ = Standard Quantity, AQ = Actual

Quantity, SR = Standard Rate, AR = Actual Rate, AH = Actual Hour and SH = Standard Hour)

B) Calculation of variable overhead spending variance

Standard Variable Overhead Rate 11.4

Actual Variable Overhead Rate 10.3

Difference per hour 1.1

11

Variance 0.2 1.06

Direct Labour

Efficiency Variance -1.2 -6.6

Total Labour Cost

Variance -5.54

Formulas used for calculation of variances are listed below

1. Direct Material Price Variance = (SP – AP) x AQ

2. Actual Quantity = Actual Quantity Produced x Actual Materials per Unit

3. Direct Material Quantity / Usage Variance = (SQ – AQ) x SP

4. Total Material Cost Variance = Direct Material Price Variance + Direct Material Quantity /

Usage Variance

5. Direct Labour Rate Variance = (SR – AR) x AH

6. Direct Labour Efficiency Variance = (SH –AH) x SR

7. Total Labour Cost Variance = Direct Labour Rate Variance + Direct Labour Efficiency

Variance

(Where, SP = Standard Price, AP = Actual Price, SQ = Standard Quantity, AQ = Actual

Quantity, SR = Standard Rate, AR = Actual Rate, AH = Actual Hour and SH = Standard Hour)

B) Calculation of variable overhead spending variance

Standard Variable Overhead Rate 11.4

Actual Variable Overhead Rate 10.3

Difference per hour 1.1

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

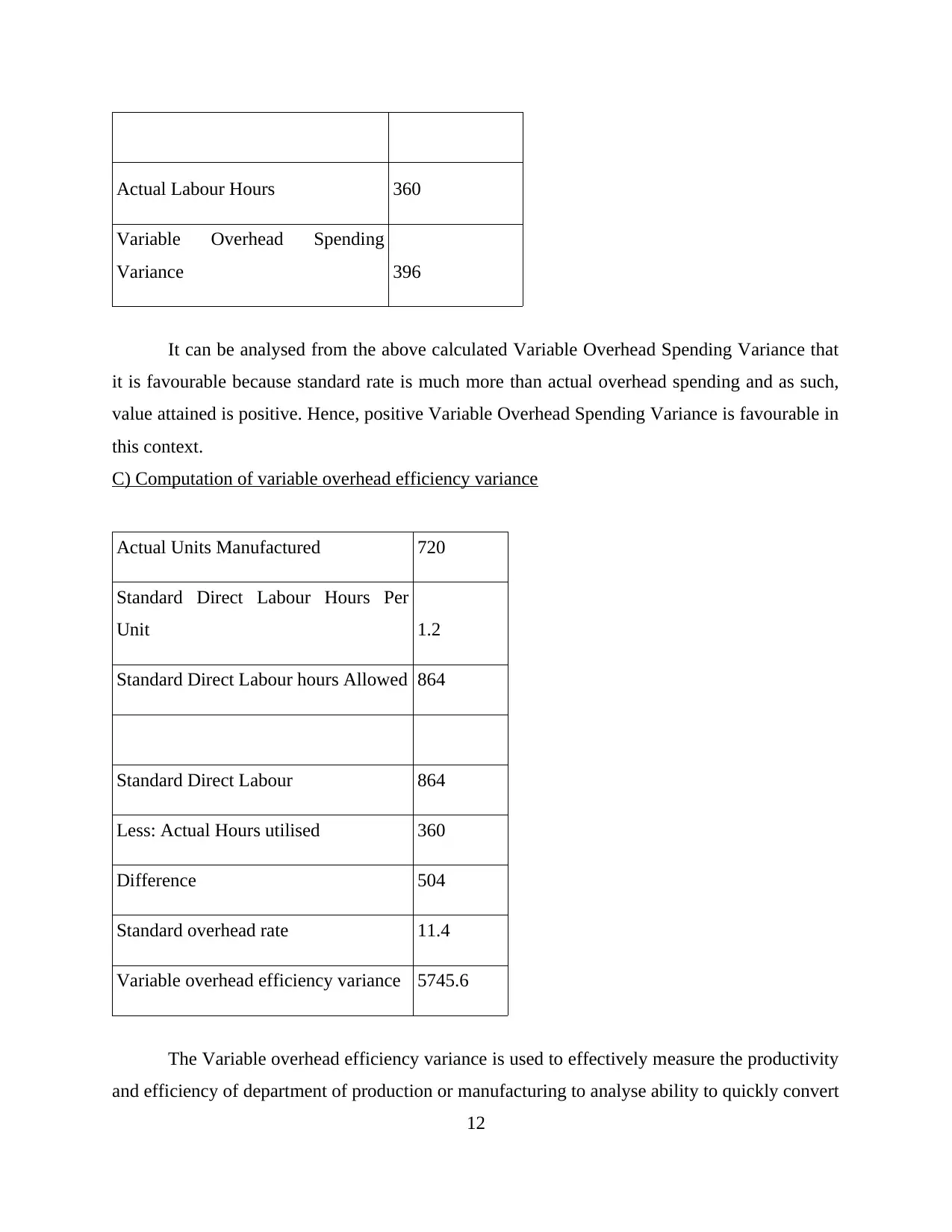

Actual Labour Hours 360

Variable Overhead Spending

Variance 396

It can be analysed from the above calculated Variable Overhead Spending Variance that

it is favourable because standard rate is much more than actual overhead spending and as such,

value attained is positive. Hence, positive Variable Overhead Spending Variance is favourable in

this context.

C) Computation of variable overhead efficiency variance

Actual Units Manufactured 720

Standard Direct Labour Hours Per

Unit 1.2

Standard Direct Labour hours Allowed 864

Standard Direct Labour 864

Less: Actual Hours utilised 360

Difference 504

Standard overhead rate 11.4

Variable overhead efficiency variance 5745.6

The Variable overhead efficiency variance is used to effectively measure the productivity

and efficiency of department of production or manufacturing to analyse ability to quickly convert

12

Variable Overhead Spending

Variance 396

It can be analysed from the above calculated Variable Overhead Spending Variance that

it is favourable because standard rate is much more than actual overhead spending and as such,

value attained is positive. Hence, positive Variable Overhead Spending Variance is favourable in

this context.

C) Computation of variable overhead efficiency variance

Actual Units Manufactured 720

Standard Direct Labour Hours Per

Unit 1.2

Standard Direct Labour hours Allowed 864

Standard Direct Labour 864

Less: Actual Hours utilised 360

Difference 504

Standard overhead rate 11.4

Variable overhead efficiency variance 5745.6

The Variable overhead efficiency variance is used to effectively measure the productivity

and efficiency of department of production or manufacturing to analyse ability to quickly convert

12

inputs into favourable outputs and that too at shortest possible time. It should be positive which

means that actual hours allowed are less than standard allowed. This shows that firm is able to

carry out production in timely manner and also at minimum resources or perfectly utilising it for

gaining production with much ease (Libby, 2017).

2. Describing variance analysis

Variance analysis is an effective technique frequently used in the budgeting so as to

analyse actual performance with that of budgeted performance in effectual manner. This is quite

useful method because it helps to identify whether actual performance is in accordance to

planned performance or not. It is helpful in company whether it is using budget in optimum

manner or not (Hall, 2012). Moreover, when difference is observed between budgeted and actual

performance, variance exists between them. In order to correct the same and make improvement,

corrective action is taken and implemented in the best possible manner. Hence, it can be said that

it is quite vital in initiating control upon costs and thus, actual costs can be controlled in a better

way and performance can be enhanced quite effectually. Thus, variance analysis is useful

technique to carry out deviations if any being assessed and then taking corrective action for

improving with ease.

CONCLUSION

Hereby it can be concluded that accounting plays vital role in the company in taking out

perfect records of diversified business operations which are crucial to handle. The techniques and

methods involved in financial accounting paves the way for preparation of true financial

statements. Moreover, CVP analysis is another way by which maximum volume of sales could

be analysed and costs may be reduced to enhance overall profits. Apart from this, cash budget

plays important role in displaying cash balance for future months highlighting whether it would

be favourable or unfavourable for business.

REFERENCES

Books and Journals

DRURY, C. M., 2013. Management and cost accounting. Springer.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

13

means that actual hours allowed are less than standard allowed. This shows that firm is able to

carry out production in timely manner and also at minimum resources or perfectly utilising it for

gaining production with much ease (Libby, 2017).

2. Describing variance analysis

Variance analysis is an effective technique frequently used in the budgeting so as to

analyse actual performance with that of budgeted performance in effectual manner. This is quite

useful method because it helps to identify whether actual performance is in accordance to

planned performance or not. It is helpful in company whether it is using budget in optimum

manner or not (Hall, 2012). Moreover, when difference is observed between budgeted and actual

performance, variance exists between them. In order to correct the same and make improvement,

corrective action is taken and implemented in the best possible manner. Hence, it can be said that

it is quite vital in initiating control upon costs and thus, actual costs can be controlled in a better

way and performance can be enhanced quite effectually. Thus, variance analysis is useful

technique to carry out deviations if any being assessed and then taking corrective action for

improving with ease.

CONCLUSION

Hereby it can be concluded that accounting plays vital role in the company in taking out

perfect records of diversified business operations which are crucial to handle. The techniques and

methods involved in financial accounting paves the way for preparation of true financial

statements. Moreover, CVP analysis is another way by which maximum volume of sales could

be analysed and costs may be reduced to enhance overall profits. Apart from this, cash budget

plays important role in displaying cash balance for future months highlighting whether it would

be favourable or unfavourable for business.

REFERENCES

Books and Journals

DRURY, C. M., 2013. Management and cost accounting. Springer.

Edwards, J. R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.