Importance of Accounting Principles and Concepts

VerifiedAdded on 2023/01/17

|19

|5652

|85

AI Summary

This report discusses the importance of accounting principles and concepts in detail. It is divided into two parts, focusing on financial information, accounting principles, and preparation of financial statements. The report also explores the role of financial statements for bankers, investors, and labor negotiators. It covers topics such as the economic entity assumption principle, historical cost accounting principle, time period principle, and going concern principle. Additionally, it explains the difference between dividends and expenses and the purpose of auditors' reports. The report concludes by discussing the going concern concept and the relationship between losses, restructuring, and the demise of a company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING

SKILLS

SKILLS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

MAIN BODY...................................................................................................................................3

Part A......................................................................................................................................3

Question 1. .............................................................................................................................3

Question 2 ..............................................................................................................................5

Question 4...............................................................................................................................6

Question 5...............................................................................................................................8

Question 7 ..............................................................................................................................9

Part B....................................................................................................................................11

Exercise 1.............................................................................................................................11

Exercise 2.............................................................................................................................12

Exercise 3.............................................................................................................................13

Exercise 4. ...........................................................................................................................14

Exercise 5.............................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

EXECUTIVE SUMMARY.............................................................................................................3

MAIN BODY...................................................................................................................................3

Part A......................................................................................................................................3

Question 1. .............................................................................................................................3

Question 2 ..............................................................................................................................5

Question 4...............................................................................................................................6

Question 5...............................................................................................................................8

Question 7 ..............................................................................................................................9

Part B....................................................................................................................................11

Exercise 1.............................................................................................................................11

Exercise 2.............................................................................................................................12

Exercise 3.............................................................................................................................13

Exercise 4. ...........................................................................................................................14

Exercise 5.............................................................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

EXECUTIVE SUMMARY

The report summarise about importance of accounting principles and concepts in a

detailed manner. The report is categorised into two parts. First part abstracts information regards

to role of financial information, accounting principles and about dividends. While the second

part summarise about preparation of different financial statement in order to get information

about total liabilities, assets etc.

MAIN BODY

Part A

Question 1.

(A) If you were a banker, why would you need information from PepsiCo’s financial

statements?

Bankers need the financial statements for multiple purpose. Basically, bankers ask for financial

statements for companies at the end of a financial year. Generally, banks want to check balance

sheets, profit & loss account statement etc. Herein, below reason for which bankers can see the

financial statement:

Balance sheet- The Balance Sheet shows the assets, debt and net value (equity) of

business at a particular time period (Ahadiat and Martin, 2015). Taking the time to

analyse the balance sheet of business enable bankers to get a clear understanding of

company's plan. The Bank must aim for good net worth and the liabilities-to-equity ratio.

Analysing the balanced sheet lets the bank decide whether its existing and/or potential

debt obligations can be met by the company.

Income statement- The Income Statement or Profit and Loss Statement shows how

much money the corporation received over a number of years and how much was left

after payment of costs (net income). Analysing this argument will enable companies as an

owner to assess whether there are possible areas for controlling costs or areas that seem

out of line. By help of it, bankers can become able to analyse whether they should make

credit transaction with company or not.

The report summarise about importance of accounting principles and concepts in a

detailed manner. The report is categorised into two parts. First part abstracts information regards

to role of financial information, accounting principles and about dividends. While the second

part summarise about preparation of different financial statement in order to get information

about total liabilities, assets etc.

MAIN BODY

Part A

Question 1.

(A) If you were a banker, why would you need information from PepsiCo’s financial

statements?

Bankers need the financial statements for multiple purpose. Basically, bankers ask for financial

statements for companies at the end of a financial year. Generally, banks want to check balance

sheets, profit & loss account statement etc. Herein, below reason for which bankers can see the

financial statement:

Balance sheet- The Balance Sheet shows the assets, debt and net value (equity) of

business at a particular time period (Ahadiat and Martin, 2015). Taking the time to

analyse the balance sheet of business enable bankers to get a clear understanding of

company's plan. The Bank must aim for good net worth and the liabilities-to-equity ratio.

Analysing the balanced sheet lets the bank decide whether its existing and/or potential

debt obligations can be met by the company.

Income statement- The Income Statement or Profit and Loss Statement shows how

much money the corporation received over a number of years and how much was left

after payment of costs (net income). Analysing this argument will enable companies as an

owner to assess whether there are possible areas for controlling costs or areas that seem

out of line. By help of it, bankers can become able to analyse whether they should make

credit transaction with company or not.

So these are the reasons for which bankers will be interested to assess financial information of

PepsiCO's company.

(B) If you were a potential investor in PepsiCo stock, what information would you want from

their financial statements?

Investors are those who make investment in company’s practices and securities. They

need to analyse financial position of companies so that they can take decisions whether they

should make investment or not. Herein, below list information is mentioned which is needed by

investors:

Net profit- Financial reports will show the net income of a corporation, net profit is the

cash left over by a corporation after all costs have been paid. "Does company make

money?" is often the first question asked, but it's just a point of departure (Ragland and

Ramachandran 2014). By analyse the information about net profitability, investors take

decision about making investment.

Sales- It is also a key information which is assessed by investors in order to take suitable

actions for investment. This is so because if PepsiCo's company's sales revenue is higher

then it may leads to higher payment of dividend to shareholders. Hence, investors

evaluate information about sales.

Cash flow Statement- For business entities, cash is the king. Investors interpret the

bank's cash as a symbol of being able to deal with unexpected issues and focus on new

possibilities. Free cash flow is a sign of successful operations and in accordance of the

information of cash flow, investors analyse efficiency of companies.

(C) If you were a labor negotiator for a union that represents a group of PepsiCo’s employees,

which financial statement would provide you with the most useful information?

For labour union, income statement will be suitable. This is so because under it, detailed

information regards to companies operations, revenues, cost of sales etc. is provided (Stone and

Lightbody, 2012). Such as in the aspect of above company, there are income statement for two

years 2013 and 2014. The labour union can analyse key information about how much salary and

wages expenditures is done by company during these years.

PepsiCO's company.

(B) If you were a potential investor in PepsiCo stock, what information would you want from

their financial statements?

Investors are those who make investment in company’s practices and securities. They

need to analyse financial position of companies so that they can take decisions whether they

should make investment or not. Herein, below list information is mentioned which is needed by

investors:

Net profit- Financial reports will show the net income of a corporation, net profit is the

cash left over by a corporation after all costs have been paid. "Does company make

money?" is often the first question asked, but it's just a point of departure (Ragland and

Ramachandran 2014). By analyse the information about net profitability, investors take

decision about making investment.

Sales- It is also a key information which is assessed by investors in order to take suitable

actions for investment. This is so because if PepsiCo's company's sales revenue is higher

then it may leads to higher payment of dividend to shareholders. Hence, investors

evaluate information about sales.

Cash flow Statement- For business entities, cash is the king. Investors interpret the

bank's cash as a symbol of being able to deal with unexpected issues and focus on new

possibilities. Free cash flow is a sign of successful operations and in accordance of the

information of cash flow, investors analyse efficiency of companies.

(C) If you were a labor negotiator for a union that represents a group of PepsiCo’s employees,

which financial statement would provide you with the most useful information?

For labour union, income statement will be suitable. This is so because under it, detailed

information regards to companies operations, revenues, cost of sales etc. is provided (Stone and

Lightbody, 2012). Such as in the aspect of above company, there are income statement for two

years 2013 and 2014. The labour union can analyse key information about how much salary and

wages expenditures is done by company during these years.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 2 .

*Melissa is the owner of Missy’s Tea Shop, a sole proprietorship. She purchases a new

computer for her personal use at home. Melissa records the computer as an asset of Missy’s

Tea Shop.

Overview- In accordance of given case, this is being stated that Melissa who is a sole

proprietor of a tea shop buys a computer for personal use but records it as an assets of tea

shop. The concept which she is applying is wrong. Under this case, below mentioned

accounting principle is needed to be applied:

Economic entity assumption principle- The accountant holds all a sole proprietorship's business

transactions apart from the private transactions of the company owner (Daly, Hoy, Islam and

Mak, 2015). A sole proprietorship and its holder are deemed to be one party for legal purposes,

but they are treated as two different entities for billing purposes. Thus, in the context of above

case, owner of tea shop should keep its personal financial transactions separate from business

transactions.

*Houston Electronics purchased an office building several years ago for $500,000. The office

building could be sold today for $850,000. The accountant will now show the building as an

asset on the books for $850,000.

Overview of case- As per the given information, this can be find out that Houston

electronic company made purchasing of building some years ago whose value was of

$500000. In current time period, the value of assets is of $850000. The accountant is

presenting the value of assets as $850000 in books of accounting. In this context, they

should apply an appropriate accounting principle which is as follows:

Historical cost accounting principle- In accounting, the historical expense of a financial item is

that item's initial estimated economic value. Historical cost accounting includes recording assets

and liabilities at their historical values that are not adjusted for adjustments in the prices of the

products (Pan and Perera, 2012). In the aspect of above case, this is important for their

accountants to record their financial transactions in accordance of historical cost accounting

principle.

*Melissa is the owner of Missy’s Tea Shop, a sole proprietorship. She purchases a new

computer for her personal use at home. Melissa records the computer as an asset of Missy’s

Tea Shop.

Overview- In accordance of given case, this is being stated that Melissa who is a sole

proprietor of a tea shop buys a computer for personal use but records it as an assets of tea

shop. The concept which she is applying is wrong. Under this case, below mentioned

accounting principle is needed to be applied:

Economic entity assumption principle- The accountant holds all a sole proprietorship's business

transactions apart from the private transactions of the company owner (Daly, Hoy, Islam and

Mak, 2015). A sole proprietorship and its holder are deemed to be one party for legal purposes,

but they are treated as two different entities for billing purposes. Thus, in the context of above

case, owner of tea shop should keep its personal financial transactions separate from business

transactions.

*Houston Electronics purchased an office building several years ago for $500,000. The office

building could be sold today for $850,000. The accountant will now show the building as an

asset on the books for $850,000.

Overview of case- As per the given information, this can be find out that Houston

electronic company made purchasing of building some years ago whose value was of

$500000. In current time period, the value of assets is of $850000. The accountant is

presenting the value of assets as $850000 in books of accounting. In this context, they

should apply an appropriate accounting principle which is as follows:

Historical cost accounting principle- In accounting, the historical expense of a financial item is

that item's initial estimated economic value. Historical cost accounting includes recording assets

and liabilities at their historical values that are not adjusted for adjustments in the prices of the

products (Pan and Perera, 2012). In the aspect of above case, this is important for their

accountants to record their financial transactions in accordance of historical cost accounting

principle.

*Henry is a new accountant for Acme Foods. He is extremely busy and has decided that he

can prepare the financial statements every two years.

Overview of case – In accordance of given data, this can be find out that Henry is a new

accountant and busy. That is why he is planning to prepare financial statements in each

two years. This policy is wrong, he should make financial statements at the end of each

year. For this purpose, there is an accounting principle which is needed to be applied:

Time period principle- The concept of time period is a financial accounting principle which

implies that all companies and organizations should divide operations into periods of time. Such

intervals are often referred to as time periods for accounting and reporting and may be weekly,

quarterly, semi-annual, annual, or any other time span. Such as in the above case, it is essential

for accountant to prepare income statements at the end of each year in accordance of this

accounting principle.

*The Candle Store is having financial problems. It has no plans to liquidate, but decides to

use market value to report their assets since they plan on moving to a smaller store.

Overview of case- The given company is facing monetary issue and recording assets as

per the market value though they are planning to move to a smaller store. It shows that

they are using wrong concept to record their assets. In this aspect, it is important to them

to follow below mentioned accounting principle which is as follows:

Going concern principle- This accounting theory implies that a business will continue to remain

long enough to meet its goals and obligations and in the future will not be liquidated. If the

financial position of the business is such that the accountant concludes that the business will not

be able to continue, this determination must be reported to the accountant (McLeod and Harun,

2014). In the above company, they should apply this accounting concept so that financial

statements can be prepared in an effective manner.

Question 4.

Dividends, you have learned, are a distribution of income, not an expense. What is the

difference? Why can’t the corporation list them as an expense, since dividends are just

another amount of money paid out to somebody?

can prepare the financial statements every two years.

Overview of case – In accordance of given data, this can be find out that Henry is a new

accountant and busy. That is why he is planning to prepare financial statements in each

two years. This policy is wrong, he should make financial statements at the end of each

year. For this purpose, there is an accounting principle which is needed to be applied:

Time period principle- The concept of time period is a financial accounting principle which

implies that all companies and organizations should divide operations into periods of time. Such

intervals are often referred to as time periods for accounting and reporting and may be weekly,

quarterly, semi-annual, annual, or any other time span. Such as in the above case, it is essential

for accountant to prepare income statements at the end of each year in accordance of this

accounting principle.

*The Candle Store is having financial problems. It has no plans to liquidate, but decides to

use market value to report their assets since they plan on moving to a smaller store.

Overview of case- The given company is facing monetary issue and recording assets as

per the market value though they are planning to move to a smaller store. It shows that

they are using wrong concept to record their assets. In this aspect, it is important to them

to follow below mentioned accounting principle which is as follows:

Going concern principle- This accounting theory implies that a business will continue to remain

long enough to meet its goals and obligations and in the future will not be liquidated. If the

financial position of the business is such that the accountant concludes that the business will not

be able to continue, this determination must be reported to the accountant (McLeod and Harun,

2014). In the above company, they should apply this accounting concept so that financial

statements can be prepared in an effective manner.

Question 4.

Dividends, you have learned, are a distribution of income, not an expense. What is the

difference? Why can’t the corporation list them as an expense, since dividends are just

another amount of money paid out to somebody?

Dividend- The term dividend can be defined as a reward which company pays to their

shareholders. This can be paid to companies in different forms such as cash payment, stock or

any other way. Basically, the corporation's dividend is determined by board of directors and this

needs approval from shareholders. Though, this is not a liability for companies to pay the

dividend. It is a part of profit which is being shared by business entities with its shareholders.

This dividend is not recorded as an expense. There is difference as the dividend is not an

expenses. It is so because dividends of a business are not an expenditure and therefore will not

show on its statement of profits. Cash dividends are a payment of part of the earnings of a

company paid to its shareholders. When a company has preferred shares, the dividends on

preferred shares are excluded from the net income of a company in order to arrive at common

stock earnings. As well as money or stock dividends paid to stakeholders are not reported in the

income statement of a corporation as an expenditure. This is because securities and even money

dividends do not impact the net income of a business.

Why it is not recorded as an expenses:

Dividends are not an expenditure. Therefore, dividends never show as an expenditure on

the financial statements of an issuing company (Siriwardane, Low and Blietz, 2015).

Alternatively, dividends are viewed as a transfer of a company's equity. As such, dividends are

deducted from the balance sheet equity portion and are also deducted from the balance sheet cash

line item, resulting in an overall decrease in the balance sheet size. When dividends are reported

but not yet paid, they will be listed on the balance sheet as current liability. Dividends paid

during the fiscal quarter are also classified as capital outflows in the funding portion of the cash

flow statement.

Apart from it, the dividend is shared with the shareholders of companies not to other

parties so it can not be considered as an expense (Osmani, Al-Esmail and Weerakkody, 2017).

As well as this is distributed from the net income of companies. For this no addition cost is paid

by companies. So these above mentioned reasons show that dividend is not an expenses. It is just

a sharing of profits among shareholders of companies who make investment in company with an

expectation of gaining higher amount of return. By comparison to costs, dividends are not

shareholders. This can be paid to companies in different forms such as cash payment, stock or

any other way. Basically, the corporation's dividend is determined by board of directors and this

needs approval from shareholders. Though, this is not a liability for companies to pay the

dividend. It is a part of profit which is being shared by business entities with its shareholders.

This dividend is not recorded as an expense. There is difference as the dividend is not an

expenses. It is so because dividends of a business are not an expenditure and therefore will not

show on its statement of profits. Cash dividends are a payment of part of the earnings of a

company paid to its shareholders. When a company has preferred shares, the dividends on

preferred shares are excluded from the net income of a company in order to arrive at common

stock earnings. As well as money or stock dividends paid to stakeholders are not reported in the

income statement of a corporation as an expenditure. This is because securities and even money

dividends do not impact the net income of a business.

Why it is not recorded as an expenses:

Dividends are not an expenditure. Therefore, dividends never show as an expenditure on

the financial statements of an issuing company (Siriwardane, Low and Blietz, 2015).

Alternatively, dividends are viewed as a transfer of a company's equity. As such, dividends are

deducted from the balance sheet equity portion and are also deducted from the balance sheet cash

line item, resulting in an overall decrease in the balance sheet size. When dividends are reported

but not yet paid, they will be listed on the balance sheet as current liability. Dividends paid

during the fiscal quarter are also classified as capital outflows in the funding portion of the cash

flow statement.

Apart from it, the dividend is shared with the shareholders of companies not to other

parties so it can not be considered as an expense (Osmani, Al-Esmail and Weerakkody, 2017).

As well as this is distributed from the net income of companies. For this no addition cost is paid

by companies. So these above mentioned reasons show that dividend is not an expenses. It is just

a sharing of profits among shareholders of companies who make investment in company with an

expectation of gaining higher amount of return. By comparison to costs, dividends are not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

component of a business profit measurement: they are not a cost of business. They are essentially

a process through which businesses allocate to their investors the profits they have made.

So in accordance of above mentioned discussion, this can be stated that payment of dividend is

not an expenses. The main reason of it is that payment of dividend does not impact to balance

sheet and profit & loss account of companies (Mitrić, Stanković and Lakićević, 2012).

Question 5.

(a) Purpose of auditors' report.

Auditors' report- Basically, an auditor's report is designed to provide assurance that the financial

reports of an entity do not contain material errors (Liu, 2012). It is assumed that the auditor will

provide the organization and its financial statements with a complete picture. They also have to

state their relation to the financial statements in the report, and whether they operate externally or

directly for the business. Herein, below purpose of auditors' report are mentioned which are as

follows:

The report allows financial statement clients to ensure the financial information is

accurate or not.

The most crucial thing is that the government wants the company to comply with the

rules and regulations, so the audit report says it follows the rules and laws (Jones, 2014).

Audit report benefits the investor as the investor can think the business is booming and

there is no concern.

(b) What is going concern concept?

Going concern- The current accounting principle means that the corporation will continue its

activities in the potential and will not be forced to sell or suspend operations for any reason

whatsoever (Elijido-Ten and Kloot, 2015). A business is an ongoing concern if there is no

evidence to say that in the near future it will or will have to interrupt its activities. In other

words, the going concern is a basic accounting concept. This assumes that a corporation can

execute its current plans, use its existing assets and continue to meet its obligations during and

after the next fiscal year. Basically, it is an expectation that the company will remain profitable

and also that the value of its assets will last. The fundamental theory is also referred to as the

idea of continuing concern.

a process through which businesses allocate to their investors the profits they have made.

So in accordance of above mentioned discussion, this can be stated that payment of dividend is

not an expenses. The main reason of it is that payment of dividend does not impact to balance

sheet and profit & loss account of companies (Mitrić, Stanković and Lakićević, 2012).

Question 5.

(a) Purpose of auditors' report.

Auditors' report- Basically, an auditor's report is designed to provide assurance that the financial

reports of an entity do not contain material errors (Liu, 2012). It is assumed that the auditor will

provide the organization and its financial statements with a complete picture. They also have to

state their relation to the financial statements in the report, and whether they operate externally or

directly for the business. Herein, below purpose of auditors' report are mentioned which are as

follows:

The report allows financial statement clients to ensure the financial information is

accurate or not.

The most crucial thing is that the government wants the company to comply with the

rules and regulations, so the audit report says it follows the rules and laws (Jones, 2014).

Audit report benefits the investor as the investor can think the business is booming and

there is no concern.

(b) What is going concern concept?

Going concern- The current accounting principle means that the corporation will continue its

activities in the potential and will not be forced to sell or suspend operations for any reason

whatsoever (Elijido-Ten and Kloot, 2015). A business is an ongoing concern if there is no

evidence to say that in the near future it will or will have to interrupt its activities. In other

words, the going concern is a basic accounting concept. This assumes that a corporation can

execute its current plans, use its existing assets and continue to meet its obligations during and

after the next fiscal year. Basically, it is an expectation that the company will remain profitable

and also that the value of its assets will last. The fundamental theory is also referred to as the

idea of continuing concern.

(c) Are losses, restructuring, and the disposal of segments necessarily precursors to the demise

of the company?

No, the losses, restructuring, and the disposal of segments are necessarily precursors to

the demise of the company (Anis, 2017). This is so because in business, loss can be occurred in

any time which does not mean that business will close. Companies can make effective policies

and plans to overcome from losses. As well as restructuring of business is also a necessary

process of companies in order tom grow in competitive market. Thus, above mentioned

statement is not accurate.

(d) What is auditors saying about above company?

The auditors are stating that company has limited amount of cash and working capital to

fund its upcoming operations. As well as in accordance of consolidated financial statement of

company, this can be find out that they had net loss which resulted as accumulated deficit of

$49.7 million. Along with this financial statement does not not consists any modifications which

may result from outcome of the uncertainties.

Question 7 .

Is Unique factory considered a business or non business company?

In accordance of given data, this can be find out there are two financial statements which

are balance sheet and income statement. The information included in both of statements states

that above company is to be considered as a business entity. It is so because of following

reasons:

Net sales- In the income statement , it is stated that there is sale of $174206 and $209203

for year 2014 and 2015. This is indicating that they are making sales transaction with

customers and it is being done in a business entity. A non business entity does not make

any sales transactions or if they make transaction then does not record in their accounting

books.

of the company?

No, the losses, restructuring, and the disposal of segments are necessarily precursors to

the demise of the company (Anis, 2017). This is so because in business, loss can be occurred in

any time which does not mean that business will close. Companies can make effective policies

and plans to overcome from losses. As well as restructuring of business is also a necessary

process of companies in order tom grow in competitive market. Thus, above mentioned

statement is not accurate.

(d) What is auditors saying about above company?

The auditors are stating that company has limited amount of cash and working capital to

fund its upcoming operations. As well as in accordance of consolidated financial statement of

company, this can be find out that they had net loss which resulted as accumulated deficit of

$49.7 million. Along with this financial statement does not not consists any modifications which

may result from outcome of the uncertainties.

Question 7 .

Is Unique factory considered a business or non business company?

In accordance of given data, this can be find out there are two financial statements which

are balance sheet and income statement. The information included in both of statements states

that above company is to be considered as a business entity. It is so because of following

reasons:

Net sales- In the income statement , it is stated that there is sale of $174206 and $209203

for year 2014 and 2015. This is indicating that they are making sales transaction with

customers and it is being done in a business entity. A non business entity does not make

any sales transactions or if they make transaction then does not record in their accounting

books.

Selling, general and administrative expenses- Under the financial statement of company,

this is being stated that they are making expense on selling and administration in both of

years. The company which is involved in process of business makes these expenses and

records in their accounting books. This shows that company is considered as business

entity.

Income tax expenses- This can be defined as a type of expenditure which is paid by

companies to government on the occurred amount of income during a particular time

period (Pernsteiner, 2015). It is essential to business entities who conduct specific

operations and activities. Such as in the income statement of above company, this can be

find out that they are making payment of income tax expenses which are $2388 and

$3534 for year 2014 & 2015. It shows that company is considered to be a business entity.

Stock holder equity- In the above company, there are different number of stockholders

who are making investment. Basically, the stakeholders make investment in business

entities not in the non business entities. Such as the total value of stakeholder equity is of

$86919 and $90908 for year 2014 and 2015. This is indicating that above company is a

business entity.

Long term debts- The company is taking huge amount of debts from different sources and

recording it in their balance sheet. As well as they are recording this amount, in their

balance sheet. The amount is of $25676 and $20491 for year 2014- 2015. This huge

amount of debts shows that company is operating their business activities in large

number.

Investment- In the aspect of current liabilities of this company, it can be find out that

there is investment amount in both of years 2014 and 2015. It is showing that company is

involved in the context of business operations. Such as in year 2014, the amount of

investment was of $1061 which reduced in next year 2015 and became of $303.

So in accordance of above discussion, this can be find out that company is considered to be a

business entity because they are conducting all those activities which are performed by

businesses.

this is being stated that they are making expense on selling and administration in both of

years. The company which is involved in process of business makes these expenses and

records in their accounting books. This shows that company is considered as business

entity.

Income tax expenses- This can be defined as a type of expenditure which is paid by

companies to government on the occurred amount of income during a particular time

period (Pernsteiner, 2015). It is essential to business entities who conduct specific

operations and activities. Such as in the income statement of above company, this can be

find out that they are making payment of income tax expenses which are $2388 and

$3534 for year 2014 & 2015. It shows that company is considered to be a business entity.

Stock holder equity- In the above company, there are different number of stockholders

who are making investment. Basically, the stakeholders make investment in business

entities not in the non business entities. Such as the total value of stakeholder equity is of

$86919 and $90908 for year 2014 and 2015. This is indicating that above company is a

business entity.

Long term debts- The company is taking huge amount of debts from different sources and

recording it in their balance sheet. As well as they are recording this amount, in their

balance sheet. The amount is of $25676 and $20491 for year 2014- 2015. This huge

amount of debts shows that company is operating their business activities in large

number.

Investment- In the aspect of current liabilities of this company, it can be find out that

there is investment amount in both of years 2014 and 2015. It is showing that company is

involved in the context of business operations. Such as in year 2014, the amount of

investment was of $1061 which reduced in next year 2015 and became of $303.

So in accordance of above discussion, this can be find out that company is considered to be a

business entity because they are conducting all those activities which are performed by

businesses.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Part B

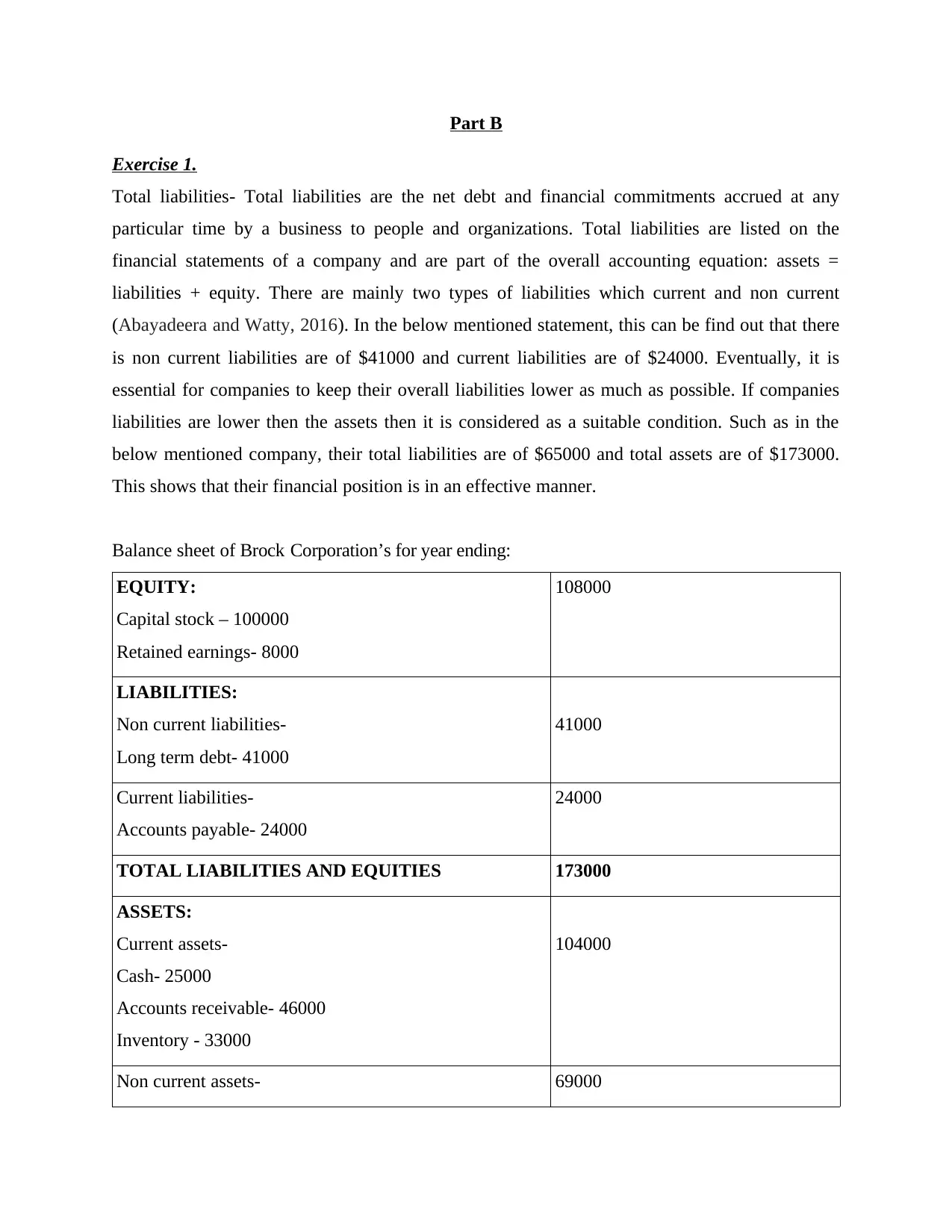

Exercise 1.

Total liabilities- Total liabilities are the net debt and financial commitments accrued at any

particular time by a business to people and organizations. Total liabilities are listed on the

financial statements of a company and are part of the overall accounting equation: assets =

liabilities + equity. There are mainly two types of liabilities which current and non current

(Abayadeera and Watty, 2016). In the below mentioned statement, this can be find out that there

is non current liabilities are of $41000 and current liabilities are of $24000. Eventually, it is

essential for companies to keep their overall liabilities lower as much as possible. If companies

liabilities are lower then the assets then it is considered as a suitable condition. Such as in the

below mentioned company, their total liabilities are of $65000 and total assets are of $173000.

This shows that their financial position is in an effective manner.

Balance sheet of Brock Corporation’s for year ending:

EQUITY:

Capital stock – 100000

Retained earnings- 8000

108000

LIABILITIES:

Non current liabilities-

Long term debt- 41000

41000

Current liabilities-

Accounts payable- 24000

24000

TOTAL LIABILITIES AND EQUITIES 173000

ASSETS:

Current assets-

Cash- 25000

Accounts receivable- 46000

Inventory - 33000

104000

Non current assets- 69000

Exercise 1.

Total liabilities- Total liabilities are the net debt and financial commitments accrued at any

particular time by a business to people and organizations. Total liabilities are listed on the

financial statements of a company and are part of the overall accounting equation: assets =

liabilities + equity. There are mainly two types of liabilities which current and non current

(Abayadeera and Watty, 2016). In the below mentioned statement, this can be find out that there

is non current liabilities are of $41000 and current liabilities are of $24000. Eventually, it is

essential for companies to keep their overall liabilities lower as much as possible. If companies

liabilities are lower then the assets then it is considered as a suitable condition. Such as in the

below mentioned company, their total liabilities are of $65000 and total assets are of $173000.

This shows that their financial position is in an effective manner.

Balance sheet of Brock Corporation’s for year ending:

EQUITY:

Capital stock – 100000

Retained earnings- 8000

108000

LIABILITIES:

Non current liabilities-

Long term debt- 41000

41000

Current liabilities-

Accounts payable- 24000

24000

TOTAL LIABILITIES AND EQUITIES 173000

ASSETS:

Current assets-

Cash- 25000

Accounts receivable- 46000

Inventory - 33000

104000

Non current assets- 69000

Property, plant & equipment- 69000

TOTAL ASSETS 173000

Analysis- The total liabilities of above company are of $65000. As well as the value of equities is

of $108000.

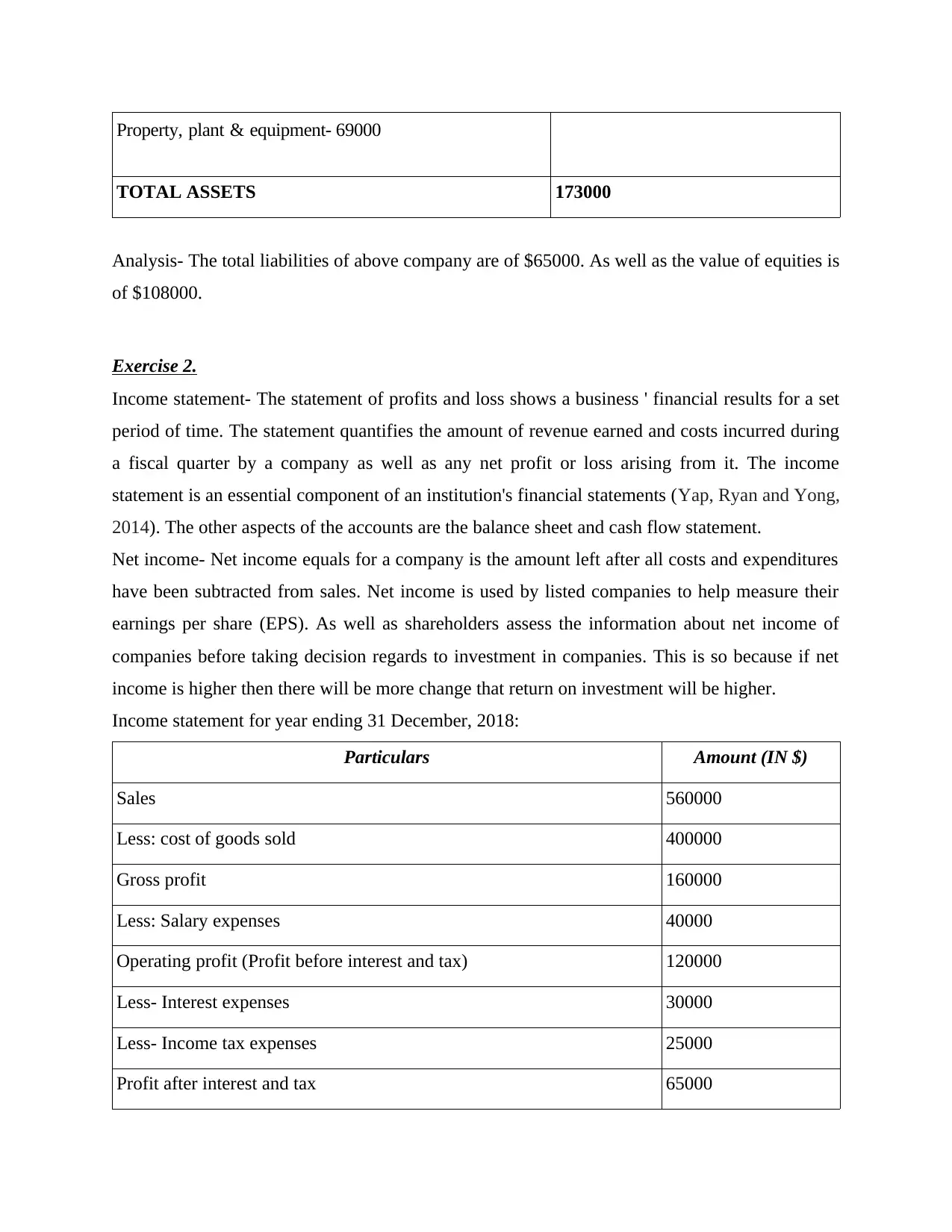

Exercise 2.

Income statement- The statement of profits and loss shows a business ' financial results for a set

period of time. The statement quantifies the amount of revenue earned and costs incurred during

a fiscal quarter by a company as well as any net profit or loss arising from it. The income

statement is an essential component of an institution's financial statements (Yap, Ryan and Yong,

2014). The other aspects of the accounts are the balance sheet and cash flow statement.

Net income- Net income equals for a company is the amount left after all costs and expenditures

have been subtracted from sales. Net income is used by listed companies to help measure their

earnings per share (EPS). As well as shareholders assess the information about net income of

companies before taking decision regards to investment in companies. This is so because if net

income is higher then there will be more change that return on investment will be higher.

Income statement for year ending 31 December, 2018:

Particulars Amount (IN $)

Sales 560000

Less: cost of goods sold 400000

Gross profit 160000

Less: Salary expenses 40000

Operating profit (Profit before interest and tax) 120000

Less- Interest expenses 30000

Less- Income tax expenses 25000

Profit after interest and tax 65000

TOTAL ASSETS 173000

Analysis- The total liabilities of above company are of $65000. As well as the value of equities is

of $108000.

Exercise 2.

Income statement- The statement of profits and loss shows a business ' financial results for a set

period of time. The statement quantifies the amount of revenue earned and costs incurred during

a fiscal quarter by a company as well as any net profit or loss arising from it. The income

statement is an essential component of an institution's financial statements (Yap, Ryan and Yong,

2014). The other aspects of the accounts are the balance sheet and cash flow statement.

Net income- Net income equals for a company is the amount left after all costs and expenditures

have been subtracted from sales. Net income is used by listed companies to help measure their

earnings per share (EPS). As well as shareholders assess the information about net income of

companies before taking decision regards to investment in companies. This is so because if net

income is higher then there will be more change that return on investment will be higher.

Income statement for year ending 31 December, 2018:

Particulars Amount (IN $)

Sales 560000

Less: cost of goods sold 400000

Gross profit 160000

Less: Salary expenses 40000

Operating profit (Profit before interest and tax) 120000

Less- Interest expenses 30000

Less- Income tax expenses 25000

Profit after interest and tax 65000

Less- Dividend 20000

Net income 45000

Analysis- On the basis of above presented income statement of this company, it can be find out

that net income is of $45000. As well as sales revenue is of $560000 and gross profit is of

$160000. The operating profit is of $120000 for company. The value of interest and tax expenses

is of $55000. This is showing that company's financial position is in an effective manner.

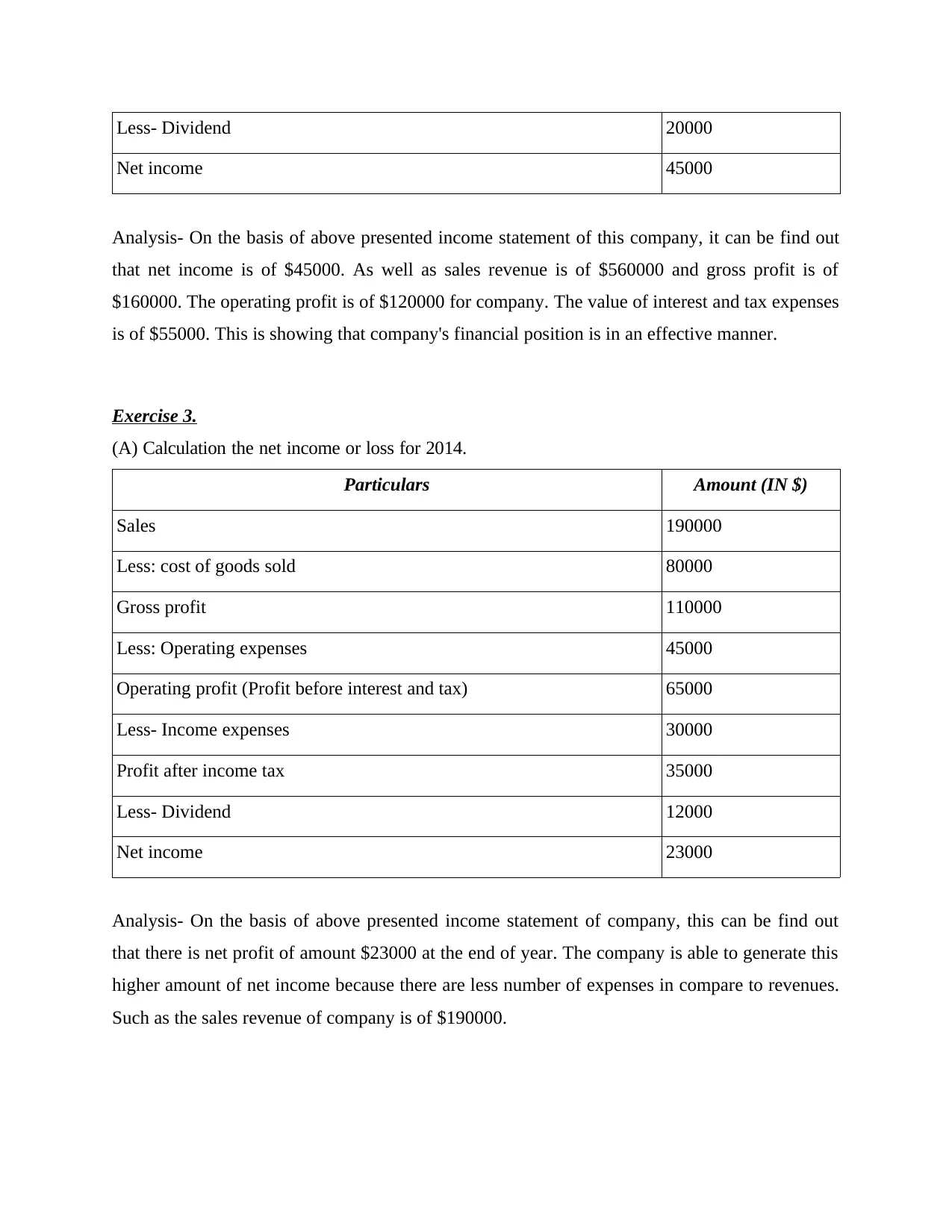

Exercise 3.

(A) Calculation the net income or loss for 2014.

Particulars Amount (IN $)

Sales 190000

Less: cost of goods sold 80000

Gross profit 110000

Less: Operating expenses 45000

Operating profit (Profit before interest and tax) 65000

Less- Income expenses 30000

Profit after income tax 35000

Less- Dividend 12000

Net income 23000

Analysis- On the basis of above presented income statement of company, this can be find out

that there is net profit of amount $23000 at the end of year. The company is able to generate this

higher amount of net income because there are less number of expenses in compare to revenues.

Such as the sales revenue of company is of $190000.

Net income 45000

Analysis- On the basis of above presented income statement of this company, it can be find out

that net income is of $45000. As well as sales revenue is of $560000 and gross profit is of

$160000. The operating profit is of $120000 for company. The value of interest and tax expenses

is of $55000. This is showing that company's financial position is in an effective manner.

Exercise 3.

(A) Calculation the net income or loss for 2014.

Particulars Amount (IN $)

Sales 190000

Less: cost of goods sold 80000

Gross profit 110000

Less: Operating expenses 45000

Operating profit (Profit before interest and tax) 65000

Less- Income expenses 30000

Profit after income tax 35000

Less- Dividend 12000

Net income 23000

Analysis- On the basis of above presented income statement of company, this can be find out

that there is net profit of amount $23000 at the end of year. The company is able to generate this

higher amount of net income because there are less number of expenses in compare to revenues.

Such as the sales revenue of company is of $190000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(B) Explanation of how the amount from part “A” will affect the financial position of Micco’s

Gift Store.

In accordance of above measured net profit of this company, it can be find out that there is

net profit of $23000. This is showing that company is in good condition and their financial position

will be effected in a positive manner. Along with the company's expenses are also lower in compare

to overall amount of profitability.

(C) Is the company profitable? Explain your answer.

As per the calculated amount of net profit of this company, it can be find out that their

financial position is in profitable manner. This is so because their amount of expense is lower and

generated revenues are higher. It shows that company's financial position is better and profitable at

which they can attract more number of stakeholders to make investment in their company.

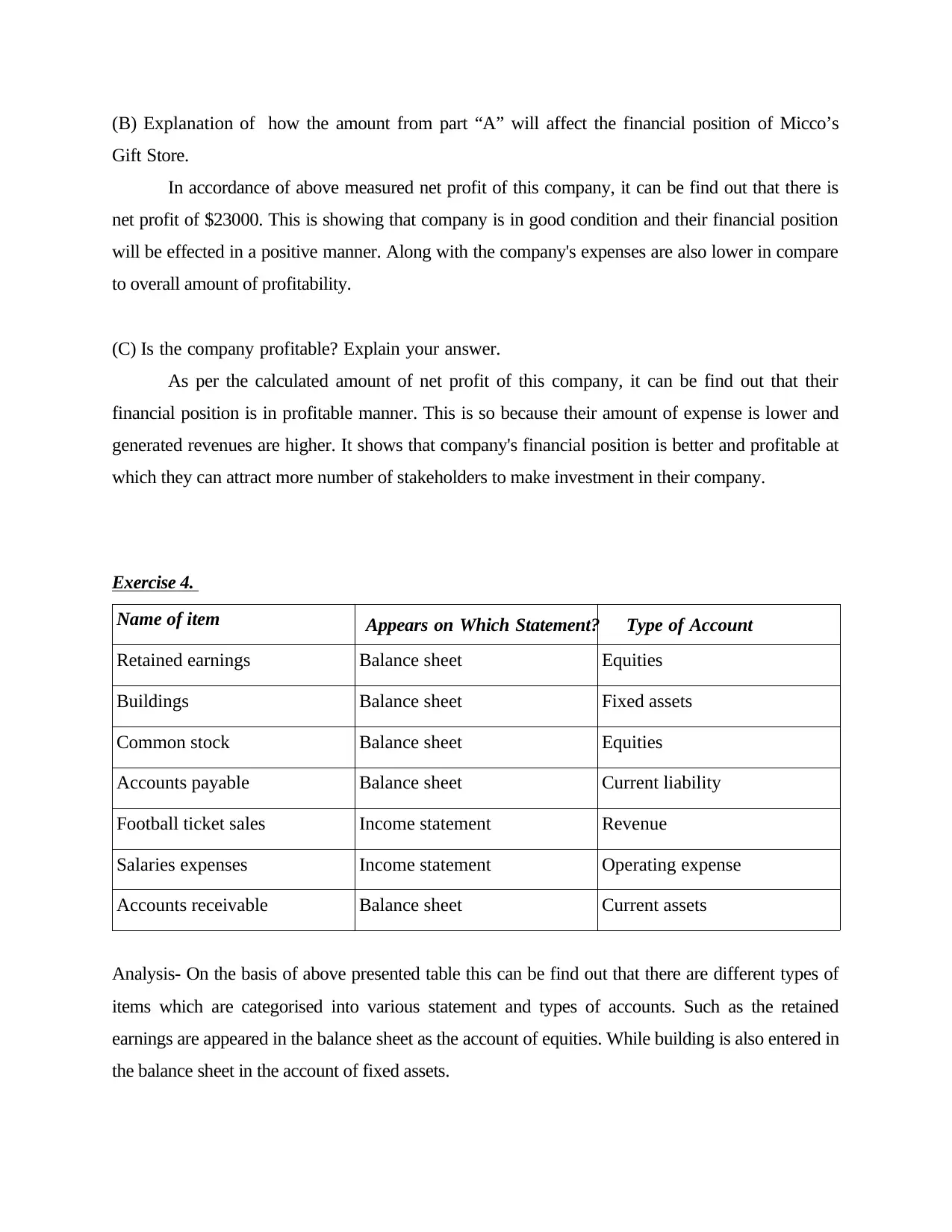

Exercise 4.

Name of item Appears on Which Statement? Type of Account

Retained earnings Balance sheet Equities

Buildings Balance sheet Fixed assets

Common stock Balance sheet Equities

Accounts payable Balance sheet Current liability

Football ticket sales Income statement Revenue

Salaries expenses Income statement Operating expense

Accounts receivable Balance sheet Current assets

Analysis- On the basis of above presented table this can be find out that there are different types of

items which are categorised into various statement and types of accounts. Such as the retained

earnings are appeared in the balance sheet as the account of equities. While building is also entered in

the balance sheet in the account of fixed assets.

Gift Store.

In accordance of above measured net profit of this company, it can be find out that there is

net profit of $23000. This is showing that company is in good condition and their financial position

will be effected in a positive manner. Along with the company's expenses are also lower in compare

to overall amount of profitability.

(C) Is the company profitable? Explain your answer.

As per the calculated amount of net profit of this company, it can be find out that their

financial position is in profitable manner. This is so because their amount of expense is lower and

generated revenues are higher. It shows that company's financial position is better and profitable at

which they can attract more number of stakeholders to make investment in their company.

Exercise 4.

Name of item Appears on Which Statement? Type of Account

Retained earnings Balance sheet Equities

Buildings Balance sheet Fixed assets

Common stock Balance sheet Equities

Accounts payable Balance sheet Current liability

Football ticket sales Income statement Revenue

Salaries expenses Income statement Operating expense

Accounts receivable Balance sheet Current assets

Analysis- On the basis of above presented table this can be find out that there are different types of

items which are categorised into various statement and types of accounts. Such as the retained

earnings are appeared in the balance sheet as the account of equities. While building is also entered in

the balance sheet in the account of fixed assets.

The common stock is appeared in the balance sheet in the account of equities. In addition,

accounts payable and receivables also entered in the statement of balance in account of current

liabilities and assets. There are only two items which are included in the income statements which are

football ticket sales and salaries expenses. The ticket sales is considered in the revenue account and

salary expenses in the operating expenses.

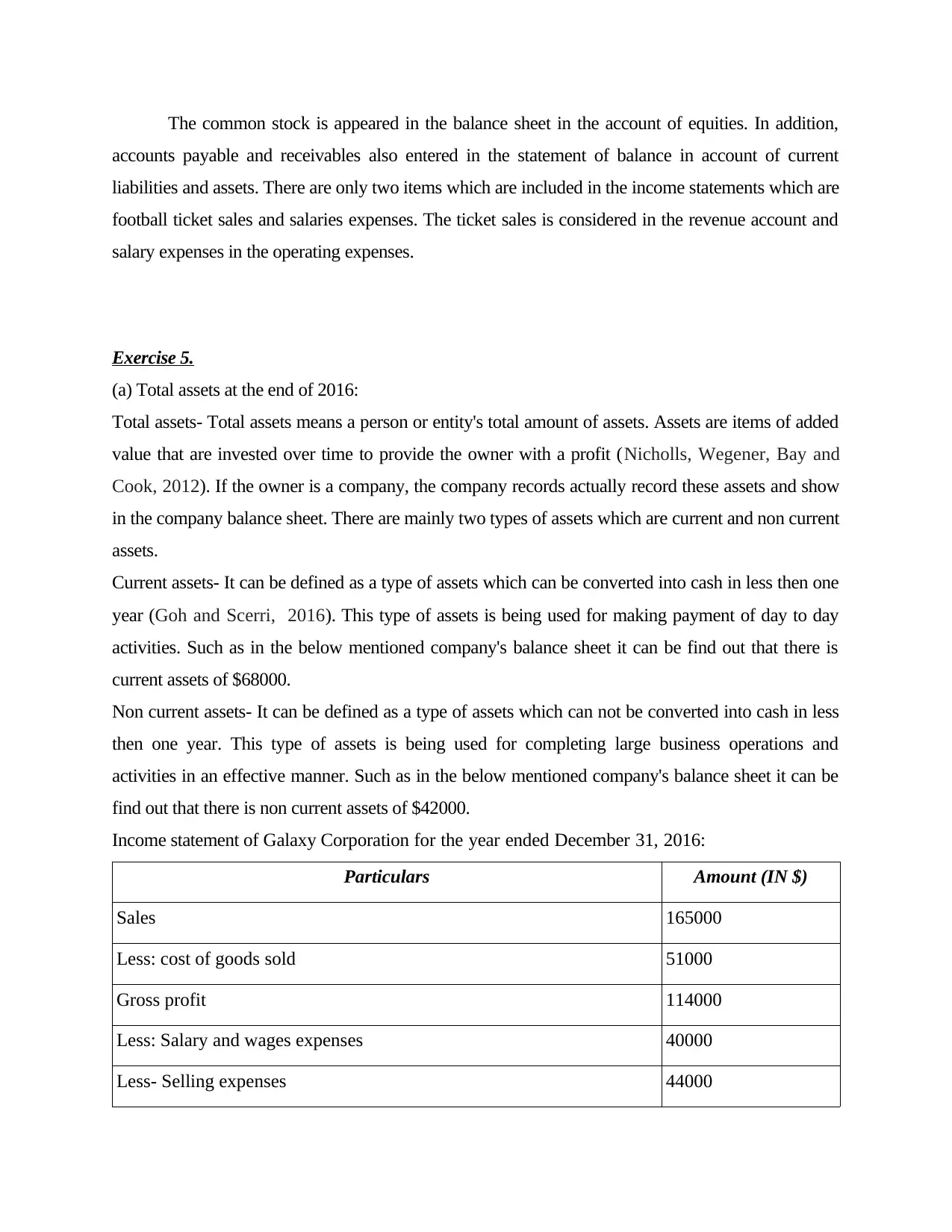

Exercise 5.

(a) Total assets at the end of 2016:

Total assets- Total assets means a person or entity's total amount of assets. Assets are items of added

value that are invested over time to provide the owner with a profit (Nicholls, Wegener, Bay and

Cook, 2012). If the owner is a company, the company records actually record these assets and show

in the company balance sheet. There are mainly two types of assets which are current and non current

assets.

Current assets- It can be defined as a type of assets which can be converted into cash in less then one

year (Goh and Scerri, 2016). This type of assets is being used for making payment of day to day

activities. Such as in the below mentioned company's balance sheet it can be find out that there is

current assets of $68000.

Non current assets- It can be defined as a type of assets which can not be converted into cash in less

then one year. This type of assets is being used for completing large business operations and

activities in an effective manner. Such as in the below mentioned company's balance sheet it can be

find out that there is non current assets of $42000.

Income statement of Galaxy Corporation for the year ended December 31, 2016:

Particulars Amount (IN $)

Sales 165000

Less: cost of goods sold 51000

Gross profit 114000

Less: Salary and wages expenses 40000

Less- Selling expenses 44000

accounts payable and receivables also entered in the statement of balance in account of current

liabilities and assets. There are only two items which are included in the income statements which are

football ticket sales and salaries expenses. The ticket sales is considered in the revenue account and

salary expenses in the operating expenses.

Exercise 5.

(a) Total assets at the end of 2016:

Total assets- Total assets means a person or entity's total amount of assets. Assets are items of added

value that are invested over time to provide the owner with a profit (Nicholls, Wegener, Bay and

Cook, 2012). If the owner is a company, the company records actually record these assets and show

in the company balance sheet. There are mainly two types of assets which are current and non current

assets.

Current assets- It can be defined as a type of assets which can be converted into cash in less then one

year (Goh and Scerri, 2016). This type of assets is being used for making payment of day to day

activities. Such as in the below mentioned company's balance sheet it can be find out that there is

current assets of $68000.

Non current assets- It can be defined as a type of assets which can not be converted into cash in less

then one year. This type of assets is being used for completing large business operations and

activities in an effective manner. Such as in the below mentioned company's balance sheet it can be

find out that there is non current assets of $42000.

Income statement of Galaxy Corporation for the year ended December 31, 2016:

Particulars Amount (IN $)

Sales 165000

Less: cost of goods sold 51000

Gross profit 114000

Less: Salary and wages expenses 40000

Less- Selling expenses 44000

Less- Income tax expenses 18000

Add- Interest income 3000

Net income 15000

Balance sheet of Galaxy Corporation for the year ended December 31, 2016:

EQUITY:

Capital stock (41000+15000) = 56000

Retained earnings- 17000

73000

LIABILITIES:

Non current liabilities-

Current liabilities-

Accounts payable- 12000

Notes payable- 20000

Income tax payable- 5000

37000

TOTAL LIABILITIES AND EQUITIES 110000

ASSETS:

Current assets-

Cash- 30000

Accounts receivable- 14000

Inventory – 22000

Prepaid expenses- 2000

68000

Non current assets-

Equipment- 42000

42000

TOTAL ASSETS 110000

Analysis- The above presented balance sheet shows that they have total assets of $110000 at the

end of year 2016.

Add- Interest income 3000

Net income 15000

Balance sheet of Galaxy Corporation for the year ended December 31, 2016:

EQUITY:

Capital stock (41000+15000) = 56000

Retained earnings- 17000

73000

LIABILITIES:

Non current liabilities-

Current liabilities-

Accounts payable- 12000

Notes payable- 20000

Income tax payable- 5000

37000

TOTAL LIABILITIES AND EQUITIES 110000

ASSETS:

Current assets-

Cash- 30000

Accounts receivable- 14000

Inventory – 22000

Prepaid expenses- 2000

68000

Non current assets-

Equipment- 42000

42000

TOTAL ASSETS 110000

Analysis- The above presented balance sheet shows that they have total assets of $110000 at the

end of year 2016.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(b) Total liabilities at the end of year 2016

As per the prepared balance sheet of company, this can be find out that there is total

liabilities is of $37000. This is a current liability. There is no any specific information about non

current liabilities.

(c) What parties have a claim on Galaxy Corporation’ assets? Explain you answer in the terms of

the accounting equation.

Accounting equation- The double-entry accounting system is likely to be based on the accounting

equation. The accounting equation indicates on the balance sheet of a business in which the average

of all the company's assets is the amount of the liabilities of the company and the equity of the

investors. The parties have to claim on company's current assets because its value is too higher in

compare to current liabilities.

CONCLUSION

On the basis of above project report, it has been concluded that accounting skills are essential

for companies in order to manager entire business transactions. The report concludes about role of

financial information for bankers and investors as well as in next part of report some accounting

concepts are concluded such as going concern principle, time period principle etc. In addition further

part of report concludes about, role of auditors report and about dividends. In the end part of report

some practical questions are solved in accordance of given data in brief.

As per the prepared balance sheet of company, this can be find out that there is total

liabilities is of $37000. This is a current liability. There is no any specific information about non

current liabilities.

(c) What parties have a claim on Galaxy Corporation’ assets? Explain you answer in the terms of

the accounting equation.

Accounting equation- The double-entry accounting system is likely to be based on the accounting

equation. The accounting equation indicates on the balance sheet of a business in which the average

of all the company's assets is the amount of the liabilities of the company and the equity of the

investors. The parties have to claim on company's current assets because its value is too higher in

compare to current liabilities.

CONCLUSION

On the basis of above project report, it has been concluded that accounting skills are essential

for companies in order to manager entire business transactions. The report concludes about role of

financial information for bankers and investors as well as in next part of report some accounting

concepts are concluded such as going concern principle, time period principle etc. In addition further

part of report concludes about, role of auditors report and about dividends. In the end part of report

some practical questions are solved in accordance of given data in brief.

REFERENCES

Books and journals:

Ahadiat, N. and Martin, R .M., 2015. Attributes, preparations, and skills accounting

professionals seek in college graduates for entry-level positions vs. promotion. Journal

of Business and Accounting. 8(1). p.179.

Ragland, L. and Ramachandran, U., 2014. Towards an understanding of excel functional skills

needed for a career in public accounting: Perceptions from public accountants and

accounting students. Journal of Accounting Education. 32(2). pp.113-129.

Stone, G. and Lightbody, M., 2012. The nature and significance of listening skills in accounting

practice. Accounting Education. 21(4). pp.363-384.

Daly, A., Hoy, S., Hughes, M., Islam, J. and Mak, A.S., 2015. Using group work to develop

intercultural skills in the accounting curriculum in Australia. Accounting Education.

24(1). pp.27-40.

Pan, P. and Perera, H., 2012, June. Market relevance of university accounting programs:

Evidence from Australia. In Accounting Forum (Vol. 36, No. 2, pp. 91-108). Taylor &

Francis.

McLeod, R .H. and Harun, H., 2014. Public sector accounting reform at local government level

in Indonesia. Financial Accountability & Management. 30(2). pp.238-258.

Abayadeera, N. and Watty, K., 2016. Generic skills in accounting education in a developing

country: exploratory evidence from Sri Lanka. Asian Review of Accounting. 24(2).

pp.149-170.

Yap, C., Ryan, S. and Yong, J., 2014. Challenges facing professional accounting education in a

commercialised education sector. Accounting Education. 23(6). pp.562-581.

Goh, E. and Scerri, M., 2016. “I study accounting because I have to”: An exploratory study of

hospitality students’ attitudes toward accounting education. Journal of Hospitality &

Tourism Education. 28(2). pp.85-94.

Nicholls, S., Wegener, M., Bay, D. and Cook, G .L., 2012. Emotional intelligence tests: Potential

impacts on the hiring process for accounting students. Accounting Education. 21(1).

pp.75-95.

Anis, A., 2017. Auditors’ and accounting educators’ perceptions of accounting education gaps

and audit quality in Egypt. Journal of Accounting in Emerging Economies. 7(3).

pp.337-351.

Elijido-Ten, E. and Kloot, L., 2015. Experiential learning in accounting work-integrated

learning: a three-way partnership. Education+ Training. 57(2). pp.204-218.

Liu, G., 2012. A survey on student satisfaction with cooperative accounting education based on

CPA firm internships. Asian Review of Accounting. 20(3). pp.259-277.

Jones, R., 2014. Bridging the gap: Engaging in scholarship with accountancy employers to

enhance understanding of skills development and employability. Accounting Education.

23(6). pp.527-541.

Siriwardane, H. P., Low, K. Y. and Blietz, D., 2015. Making entry-level accountants better

communicators: A Singapore-based study of communication tasks, skills, and

attributes. Journal of Accounting Education. 33(4). pp.332-347.

Osmani, M., Hindi, N., Al-Esmail, R. and Weerakkody, V., 2017. Examining graduate skills in

accounting and finance: The perception of Middle Eastern students. Industry and

Higher Education. 31(5). pp.318-327.

Books and journals:

Ahadiat, N. and Martin, R .M., 2015. Attributes, preparations, and skills accounting

professionals seek in college graduates for entry-level positions vs. promotion. Journal

of Business and Accounting. 8(1). p.179.

Ragland, L. and Ramachandran, U., 2014. Towards an understanding of excel functional skills

needed for a career in public accounting: Perceptions from public accountants and

accounting students. Journal of Accounting Education. 32(2). pp.113-129.

Stone, G. and Lightbody, M., 2012. The nature and significance of listening skills in accounting

practice. Accounting Education. 21(4). pp.363-384.

Daly, A., Hoy, S., Hughes, M., Islam, J. and Mak, A.S., 2015. Using group work to develop

intercultural skills in the accounting curriculum in Australia. Accounting Education.

24(1). pp.27-40.

Pan, P. and Perera, H., 2012, June. Market relevance of university accounting programs:

Evidence from Australia. In Accounting Forum (Vol. 36, No. 2, pp. 91-108). Taylor &

Francis.

McLeod, R .H. and Harun, H., 2014. Public sector accounting reform at local government level

in Indonesia. Financial Accountability & Management. 30(2). pp.238-258.

Abayadeera, N. and Watty, K., 2016. Generic skills in accounting education in a developing

country: exploratory evidence from Sri Lanka. Asian Review of Accounting. 24(2).

pp.149-170.

Yap, C., Ryan, S. and Yong, J., 2014. Challenges facing professional accounting education in a

commercialised education sector. Accounting Education. 23(6). pp.562-581.

Goh, E. and Scerri, M., 2016. “I study accounting because I have to”: An exploratory study of

hospitality students’ attitudes toward accounting education. Journal of Hospitality &

Tourism Education. 28(2). pp.85-94.

Nicholls, S., Wegener, M., Bay, D. and Cook, G .L., 2012. Emotional intelligence tests: Potential

impacts on the hiring process for accounting students. Accounting Education. 21(1).

pp.75-95.

Anis, A., 2017. Auditors’ and accounting educators’ perceptions of accounting education gaps

and audit quality in Egypt. Journal of Accounting in Emerging Economies. 7(3).

pp.337-351.

Elijido-Ten, E. and Kloot, L., 2015. Experiential learning in accounting work-integrated

learning: a three-way partnership. Education+ Training. 57(2). pp.204-218.

Liu, G., 2012. A survey on student satisfaction with cooperative accounting education based on

CPA firm internships. Asian Review of Accounting. 20(3). pp.259-277.

Jones, R., 2014. Bridging the gap: Engaging in scholarship with accountancy employers to

enhance understanding of skills development and employability. Accounting Education.

23(6). pp.527-541.

Siriwardane, H. P., Low, K. Y. and Blietz, D., 2015. Making entry-level accountants better

communicators: A Singapore-based study of communication tasks, skills, and

attributes. Journal of Accounting Education. 33(4). pp.332-347.

Osmani, M., Hindi, N., Al-Esmail, R. and Weerakkody, V., 2017. Examining graduate skills in

accounting and finance: The perception of Middle Eastern students. Industry and

Higher Education. 31(5). pp.318-327.

Mitrić, M., Stanković, A. and Lakićević, A., 2012. Forensic Accounting—the Missing Link in

Education and Practice. Management (1820-0222). (65).

Pernsteiner, A. J., 2015. The Value of an Accounting Internship: What Do Accounting Students

Really Gain?. Academy of Educational Leadership Journal. 19(3). p.223.

Education and Practice. Management (1820-0222). (65).

Pernsteiner, A. J., 2015. The Value of an Accounting Internship: What Do Accounting Students

Really Gain?. Academy of Educational Leadership Journal. 19(3). p.223.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.