AASB 16 Leases: Financial Statement Impact on Rio Tinto & BHP Billiton

VerifiedAdded on 2023/04/21

|14

|2860

|157

Report

AI Summary

This report provides a comprehensive analysis of the potential impact of AASB 16 Leases on Rio Tinto Ltd and BHP Billiton Ltd, comparing their 2017 annual reports. It examines the implementation of AASB 16, its effect on financial statements (income statement, balance sheet, and cash flow statement), and includes a ratio analysis (current ratio, quick ratio, net profit margin, and operating profit margin) to assess the companies' liquidity and profitability. The report also evaluates the environmental and social reporting practices of both companies based on their sustainability reports, focusing on social investments, emission reductions, and employee safety. The overall impact of AASB 16 is discussed, emphasizing increased transparency and improved financial reporting for both companies.

Running head: ACCOUNTING STANDARD AND GOVERNANCE

Accounting Standard and Governance

Name of the Student:

Name of the University:

Author’s Note

Accounting Standard and Governance

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING STANDARD AND GOVERNANCE

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Implementation of AASB 16.......................................................................................................3

Effect on the Financial Statements..............................................................................................5

Ratio Analysis..............................................................................................................................6

Reporting of Environmental and Social Aspects.........................................................................9

Overall Impact of AASB 16......................................................................................................11

Summary for Investment Company...........................................................................................11

Conclusion.....................................................................................................................................12

Reference.......................................................................................................................................12

ACCOUNTING STANDARD AND GOVERNANCE

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Implementation of AASB 16.......................................................................................................3

Effect on the Financial Statements..............................................................................................5

Ratio Analysis..............................................................................................................................6

Reporting of Environmental and Social Aspects.........................................................................9

Overall Impact of AASB 16......................................................................................................11

Summary for Investment Company...........................................................................................11

Conclusion.....................................................................................................................................12

Reference.......................................................................................................................................12

2

ACCOUNTING STANDARD AND GOVERNANCE

Introduction

The main purpose of this assessment is to analyze the annual reports of two companies

which are engaged in the same industry. The companies which are selected are Rio Tinto Ltd and

BHP Billiton ltd and for these companies, the annual report for 2017 is considered for the

purpose of analysis. The assessment aims to analyze the reporting standards which are followed

by the business for leases and whether the new standard on leases AASB 16 can impact the

reporting framework which is applied by both the companies. The assessment also involves

evaluating the environmental and social reporting which is undertaken by the management of the

company and whether the same is appropriate or not. The assessment would also be included

computation and analysis of key financial ratios which are useful in determining the financial

performance of the business. The computation of key financial ratios of the business would on

the basis of the annual reports of both the companies for the year 2017.

Discussion

Implementation of AASB 16

The changes which have been brought about in the reporting of leases which are shown

in the financial statements of the business. The changes have been brought in the accounting

standards for leases so as to improve the reporting process for operating leases and ensure that

proper disclosures are provided in the financial statements of the business. In earlier standard,

operating leases was not recognized in the financial statements and therefore there was a scope

for manipulations in the transactions which are included in the annual reports (Barone, Birt and

Moya 2014). The new standards require mandatory disclosure of operating leases in the balance

ACCOUNTING STANDARD AND GOVERNANCE

Introduction

The main purpose of this assessment is to analyze the annual reports of two companies

which are engaged in the same industry. The companies which are selected are Rio Tinto Ltd and

BHP Billiton ltd and for these companies, the annual report for 2017 is considered for the

purpose of analysis. The assessment aims to analyze the reporting standards which are followed

by the business for leases and whether the new standard on leases AASB 16 can impact the

reporting framework which is applied by both the companies. The assessment also involves

evaluating the environmental and social reporting which is undertaken by the management of the

company and whether the same is appropriate or not. The assessment would also be included

computation and analysis of key financial ratios which are useful in determining the financial

performance of the business. The computation of key financial ratios of the business would on

the basis of the annual reports of both the companies for the year 2017.

Discussion

Implementation of AASB 16

The changes which have been brought about in the reporting of leases which are shown

in the financial statements of the business. The changes have been brought in the accounting

standards for leases so as to improve the reporting process for operating leases and ensure that

proper disclosures are provided in the financial statements of the business. In earlier standard,

operating leases was not recognized in the financial statements and therefore there was a scope

for manipulations in the transactions which are included in the annual reports (Barone, Birt and

Moya 2014). The new standards require mandatory disclosure of operating leases in the balance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING STANDARD AND GOVERNANCE

sheet of the business, In addition to this, the identification of leases can be appropriately done

with the help of AASB 16 and also lease payments can be done in an more efficient manner.

The changes in the leasing standard is expected to bring about more transparency in the

reporting framework and thereby also ensure that the financial aspects of the business are

appropriately reported. The changes would restrict any manipulations which was done when the

operating leases were not recognized in the financial statements of the company (Fitó, Moya and

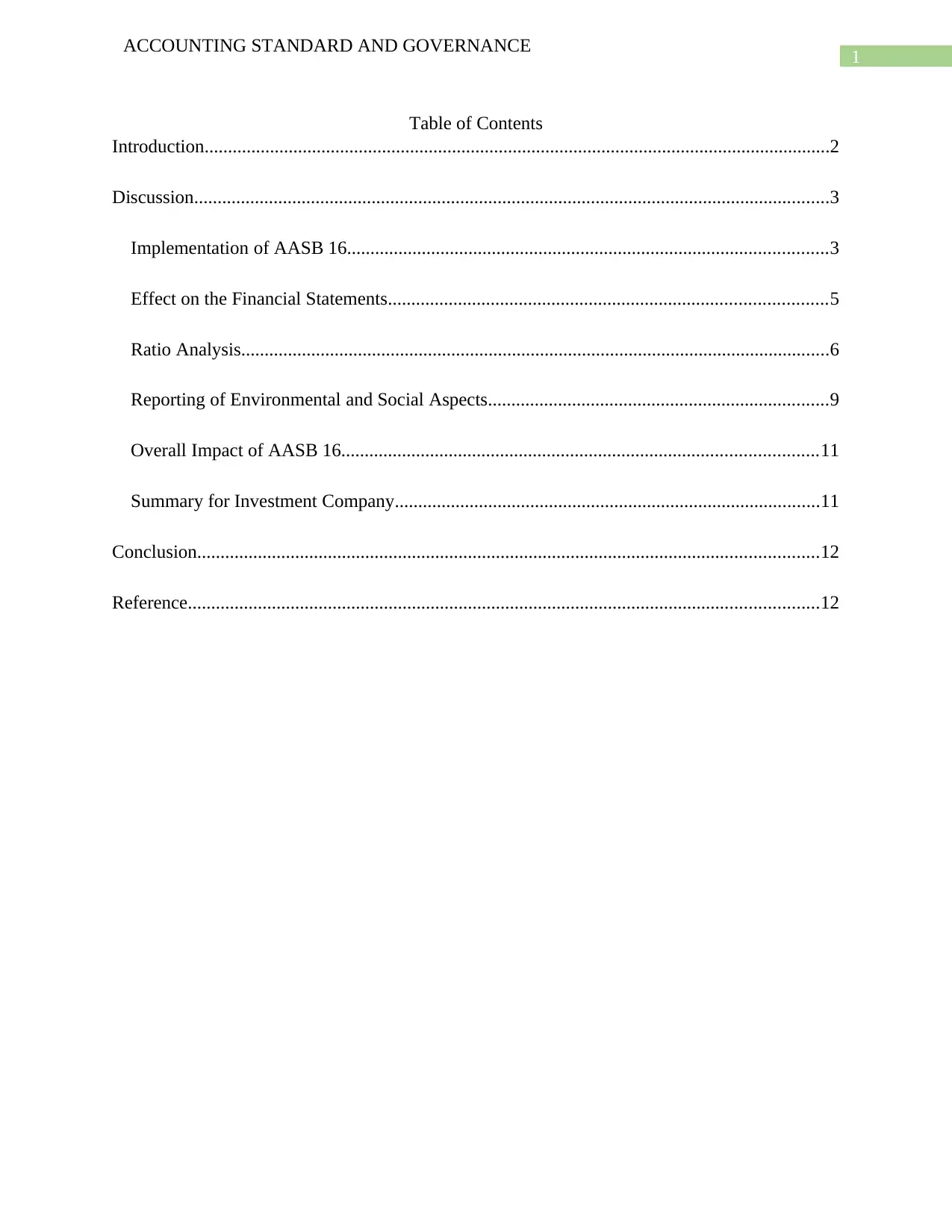

Orgaz 2013). In the case of BHP Billiton, the annual report of the company shows that the

business does not have any operating lease but has financial lease which is on equipment. The

operating leases is on rental payments for which adjustment are showing in the income statement

of the business.

Figure 1: (Extract showing leases of the BHP Billiton ltd).

Source: (Bhp.com. 2018)

In the case of Rio Tinto Ltd, the annual report shows that there are certain financial leases

which is taken by the business for which appropriate disclosures are provided in the annual

report of the business (Dakis 2016). The management of the company has mining properties on

ACCOUNTING STANDARD AND GOVERNANCE

sheet of the business, In addition to this, the identification of leases can be appropriately done

with the help of AASB 16 and also lease payments can be done in an more efficient manner.

The changes in the leasing standard is expected to bring about more transparency in the

reporting framework and thereby also ensure that the financial aspects of the business are

appropriately reported. The changes would restrict any manipulations which was done when the

operating leases were not recognized in the financial statements of the company (Fitó, Moya and

Orgaz 2013). In the case of BHP Billiton, the annual report of the company shows that the

business does not have any operating lease but has financial lease which is on equipment. The

operating leases is on rental payments for which adjustment are showing in the income statement

of the business.

Figure 1: (Extract showing leases of the BHP Billiton ltd).

Source: (Bhp.com. 2018)

In the case of Rio Tinto Ltd, the annual report shows that there are certain financial leases

which is taken by the business for which appropriate disclosures are provided in the annual

report of the business (Dakis 2016). The management of the company has mining properties on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING STANDARD AND GOVERNANCE

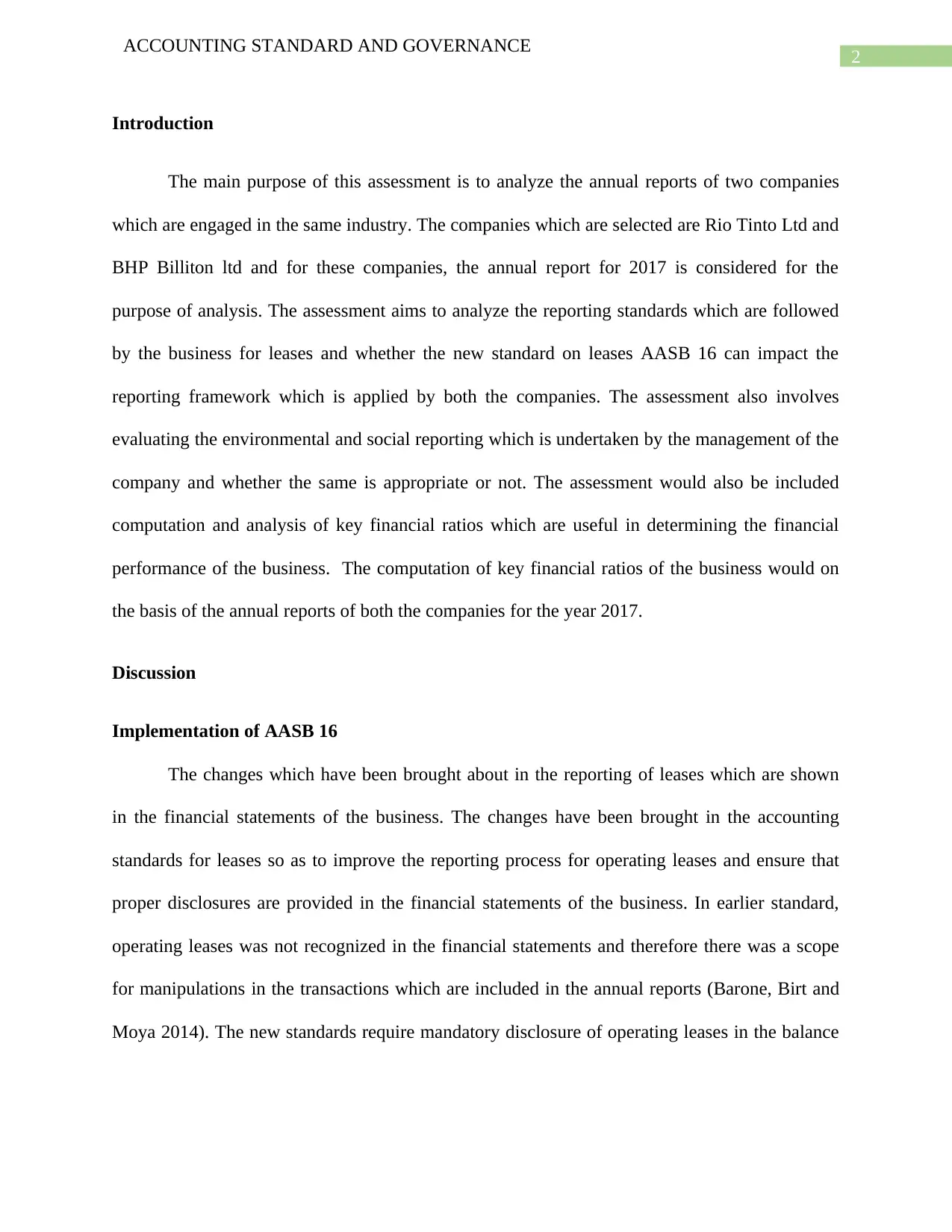

leases and there are also certain operating leases which is shown in the annual report of the

business which is shown in the notes to account section of the business.

Figure 1: (Extract showing leases of the Rio Tinto Ltd).

Source: (Riotinto.com. 2018)

The above extract shows the operating leases of the business of Rio Tinto ltd and the

payment period for the same. In case of both the companies the introduction of the new standard

would mean that the reporting framework of both the companies would significantly improve

and proper disclosures can be provided for both the companies. The implementation of the new

AASB 16 would also mean that the business would be reporting more efficiently on the reporting

of leases of the business (Joubert, Garvie and Parle 2017). The new standard would effectively

help the management of both companies to effectively identify the nature of the lease whether

the same is operating or financial lease and thereby also help in the disclosure process of the

business. Therefore, in an overall estimate, it can be said that the changes which has taken place

in the reporting of leases due to the new standard would be beneficial for both the companies.

ACCOUNTING STANDARD AND GOVERNANCE

leases and there are also certain operating leases which is shown in the annual report of the

business which is shown in the notes to account section of the business.

Figure 1: (Extract showing leases of the Rio Tinto Ltd).

Source: (Riotinto.com. 2018)

The above extract shows the operating leases of the business of Rio Tinto ltd and the

payment period for the same. In case of both the companies the introduction of the new standard

would mean that the reporting framework of both the companies would significantly improve

and proper disclosures can be provided for both the companies. The implementation of the new

AASB 16 would also mean that the business would be reporting more efficiently on the reporting

of leases of the business (Joubert, Garvie and Parle 2017). The new standard would effectively

help the management of both companies to effectively identify the nature of the lease whether

the same is operating or financial lease and thereby also help in the disclosure process of the

business. Therefore, in an overall estimate, it can be said that the changes which has taken place

in the reporting of leases due to the new standard would be beneficial for both the companies.

5

ACCOUNTING STANDARD AND GOVERNANCE

Effect on the Financial Statements

The new standard on leases AASB 16 would become enforceable from 2019 on all

companies. The new standards have made tremendous improvements in terms of reporting for

leases in a business. The annual report of Rio Tinto and BHP Billiton both shows that the

companies have taken both financial leases and operating leases during the year. The new

standard effectively covers the gap which was present in the previous standard relating to

reporting for operating leases and thereby also allows the business to effectively recognize the

type of risk which is taken by the management of both the companies and assist them to classify

the leases as whether the same is operating lease or financial lease.

Under the new lease standards, the income statement would be showing the lease

payments which are undertaken by the business during the period and also the interest which the

business needs to pay for the assets which are taken on leases. In case of the balance sheet,

operating leases would be disclosed which was not the case in case of previous accounting

standards and thereby this ensures that there is full transparency in the annual reports of the

business and the users are able to effectively analyze the same for taking decisions (Stice and

Stice 2013). The cash flow statement would also be affected as lease payments would involve

cash outflows which would be shown in the annual report of the business. The major changes

which has taken place in comparison to previous standards is that no off-balance sheet treatment

would be allowed in the financial statements. The new standard is very useful for the users of the

financial statement as the same provide full disclosures regarding the treatment relating to leases

of a business. The new standard would enable the users to have full information relating to the

company and according to the same take important decisions which is related to the company.

Therefore, it can be said appropriately that the introduction of the new lease would only enhance

ACCOUNTING STANDARD AND GOVERNANCE

Effect on the Financial Statements

The new standard on leases AASB 16 would become enforceable from 2019 on all

companies. The new standards have made tremendous improvements in terms of reporting for

leases in a business. The annual report of Rio Tinto and BHP Billiton both shows that the

companies have taken both financial leases and operating leases during the year. The new

standard effectively covers the gap which was present in the previous standard relating to

reporting for operating leases and thereby also allows the business to effectively recognize the

type of risk which is taken by the management of both the companies and assist them to classify

the leases as whether the same is operating lease or financial lease.

Under the new lease standards, the income statement would be showing the lease

payments which are undertaken by the business during the period and also the interest which the

business needs to pay for the assets which are taken on leases. In case of the balance sheet,

operating leases would be disclosed which was not the case in case of previous accounting

standards and thereby this ensures that there is full transparency in the annual reports of the

business and the users are able to effectively analyze the same for taking decisions (Stice and

Stice 2013). The cash flow statement would also be affected as lease payments would involve

cash outflows which would be shown in the annual report of the business. The major changes

which has taken place in comparison to previous standards is that no off-balance sheet treatment

would be allowed in the financial statements. The new standard is very useful for the users of the

financial statement as the same provide full disclosures regarding the treatment relating to leases

of a business. The new standard would enable the users to have full information relating to the

company and according to the same take important decisions which is related to the company.

Therefore, it can be said appropriately that the introduction of the new lease would only enhance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING STANDARD AND GOVERNANCE

the quality of reporting of both companies and would also be beneficial for the users of the

financial statements of the business.

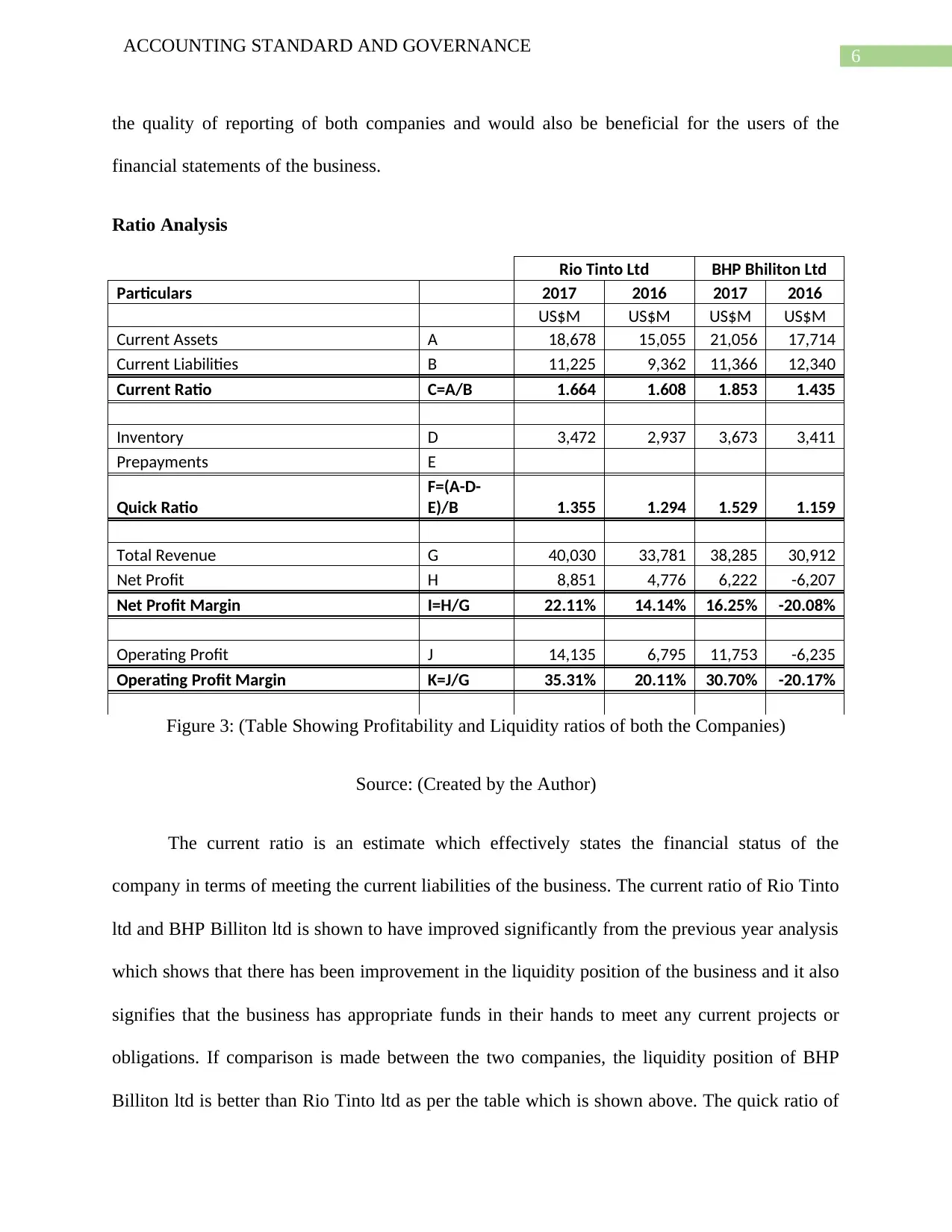

Ratio Analysis

Rio Tinto Ltd BHP Bhiliton Ltd

Particulars 2017 2016 2017 2016

US$M US$M US$M US$M

Current Assets A 18,678 15,055 21,056 17,714

Current Liabilities B 11,225 9,362 11,366 12,340

Current Ratio C=A/B 1.664 1.608 1.853 1.435

Inventory D 3,472 2,937 3,673 3,411

Prepayments E

Quick Ratio

F=(A-D-

E)/B 1.355 1.294 1.529 1.159

Total Revenue G 40,030 33,781 38,285 30,912

Net Profit H 8,851 4,776 6,222 -6,207

Net Profit Margin I=H/G 22.11% 14.14% 16.25% -20.08%

Operating Profit J 14,135 6,795 11,753 -6,235

Operating Profit Margin K=J/G 35.31% 20.11% 30.70% -20.17%

Figure 3: (Table Showing Profitability and Liquidity ratios of both the Companies)

Source: (Created by the Author)

The current ratio is an estimate which effectively states the financial status of the

company in terms of meeting the current liabilities of the business. The current ratio of Rio Tinto

ltd and BHP Billiton ltd is shown to have improved significantly from the previous year analysis

which shows that there has been improvement in the liquidity position of the business and it also

signifies that the business has appropriate funds in their hands to meet any current projects or

obligations. If comparison is made between the two companies, the liquidity position of BHP

Billiton ltd is better than Rio Tinto ltd as per the table which is shown above. The quick ratio of

ACCOUNTING STANDARD AND GOVERNANCE

the quality of reporting of both companies and would also be beneficial for the users of the

financial statements of the business.

Ratio Analysis

Rio Tinto Ltd BHP Bhiliton Ltd

Particulars 2017 2016 2017 2016

US$M US$M US$M US$M

Current Assets A 18,678 15,055 21,056 17,714

Current Liabilities B 11,225 9,362 11,366 12,340

Current Ratio C=A/B 1.664 1.608 1.853 1.435

Inventory D 3,472 2,937 3,673 3,411

Prepayments E

Quick Ratio

F=(A-D-

E)/B 1.355 1.294 1.529 1.159

Total Revenue G 40,030 33,781 38,285 30,912

Net Profit H 8,851 4,776 6,222 -6,207

Net Profit Margin I=H/G 22.11% 14.14% 16.25% -20.08%

Operating Profit J 14,135 6,795 11,753 -6,235

Operating Profit Margin K=J/G 35.31% 20.11% 30.70% -20.17%

Figure 3: (Table Showing Profitability and Liquidity ratios of both the Companies)

Source: (Created by the Author)

The current ratio is an estimate which effectively states the financial status of the

company in terms of meeting the current liabilities of the business. The current ratio of Rio Tinto

ltd and BHP Billiton ltd is shown to have improved significantly from the previous year analysis

which shows that there has been improvement in the liquidity position of the business and it also

signifies that the business has appropriate funds in their hands to meet any current projects or

obligations. If comparison is made between the two companies, the liquidity position of BHP

Billiton ltd is better than Rio Tinto ltd as per the table which is shown above. The quick ratio of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING STANDARD AND GOVERNANCE

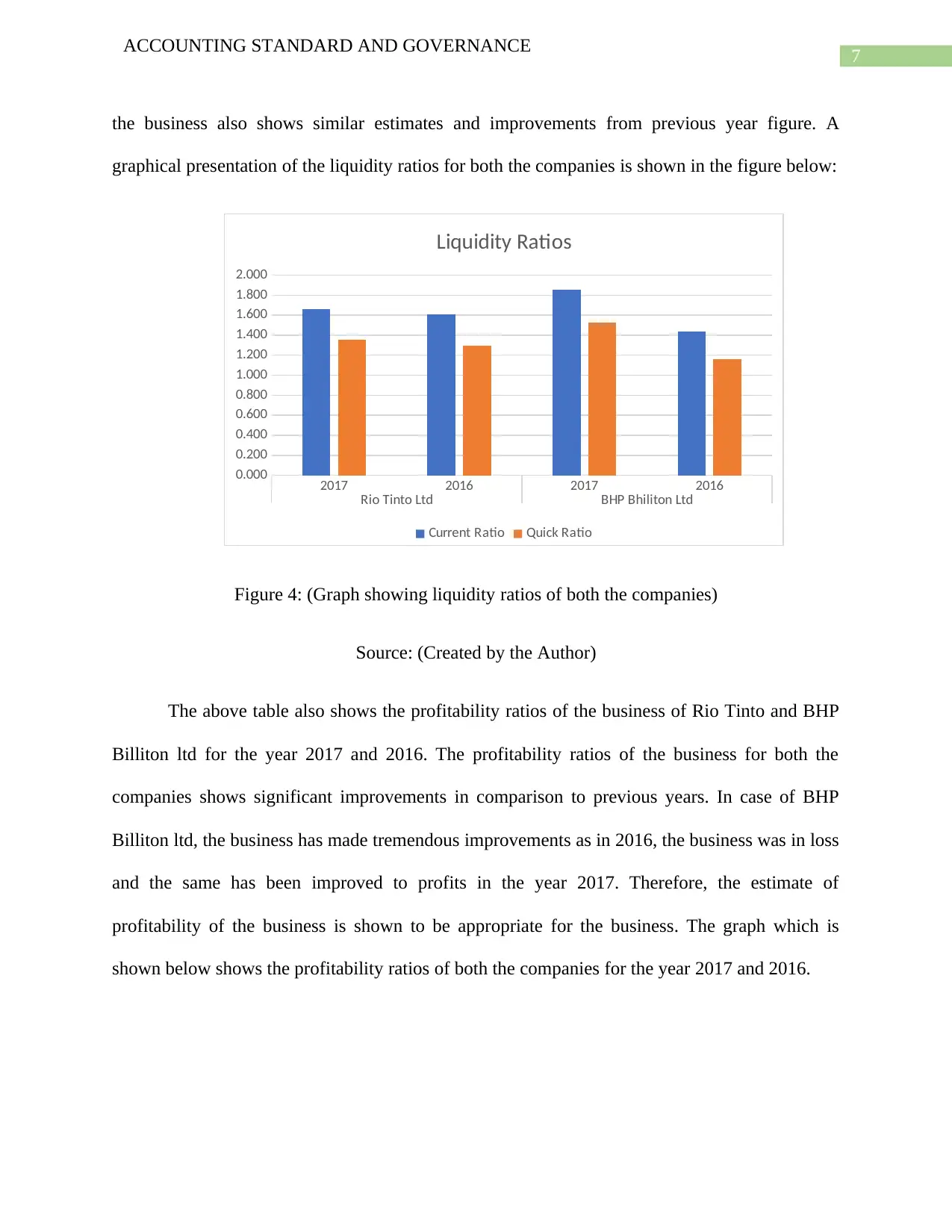

the business also shows similar estimates and improvements from previous year figure. A

graphical presentation of the liquidity ratios for both the companies is shown in the figure below:

2017 2016 2017 2016

Rio Tinto Ltd BHP Bhiliton Ltd

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

1.800

2.000

Liquidity Ratios

Current Ratio Quick Ratio

Figure 4: (Graph showing liquidity ratios of both the companies)

Source: (Created by the Author)

The above table also shows the profitability ratios of the business of Rio Tinto and BHP

Billiton ltd for the year 2017 and 2016. The profitability ratios of the business for both the

companies shows significant improvements in comparison to previous years. In case of BHP

Billiton ltd, the business has made tremendous improvements as in 2016, the business was in loss

and the same has been improved to profits in the year 2017. Therefore, the estimate of

profitability of the business is shown to be appropriate for the business. The graph which is

shown below shows the profitability ratios of both the companies for the year 2017 and 2016.

ACCOUNTING STANDARD AND GOVERNANCE

the business also shows similar estimates and improvements from previous year figure. A

graphical presentation of the liquidity ratios for both the companies is shown in the figure below:

2017 2016 2017 2016

Rio Tinto Ltd BHP Bhiliton Ltd

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

1.800

2.000

Liquidity Ratios

Current Ratio Quick Ratio

Figure 4: (Graph showing liquidity ratios of both the companies)

Source: (Created by the Author)

The above table also shows the profitability ratios of the business of Rio Tinto and BHP

Billiton ltd for the year 2017 and 2016. The profitability ratios of the business for both the

companies shows significant improvements in comparison to previous years. In case of BHP

Billiton ltd, the business has made tremendous improvements as in 2016, the business was in loss

and the same has been improved to profits in the year 2017. Therefore, the estimate of

profitability of the business is shown to be appropriate for the business. The graph which is

shown below shows the profitability ratios of both the companies for the year 2017 and 2016.

8

ACCOUNTING STANDARD AND GOVERNANCE

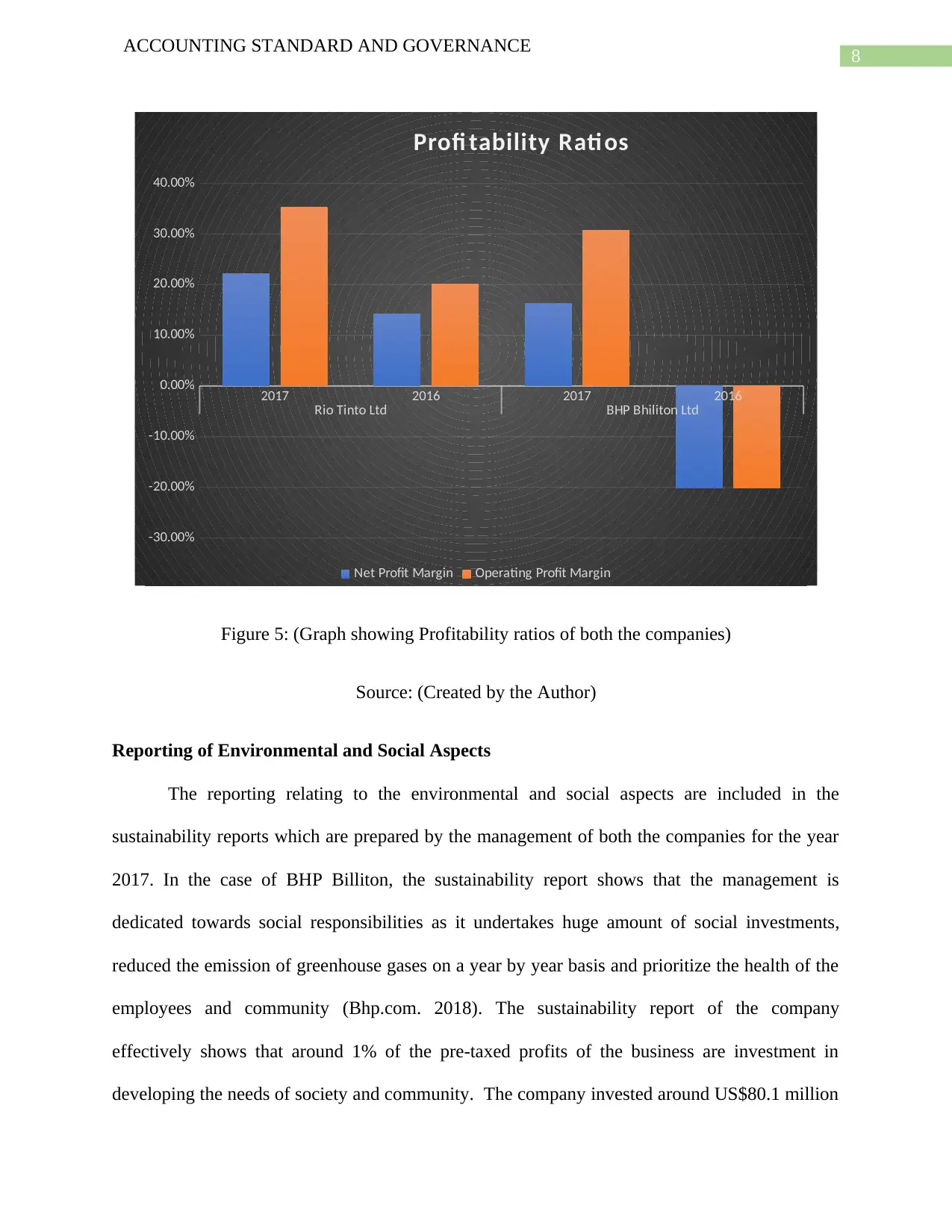

2017 2016 2017 2016

Rio Tinto Ltd BHP Bhiliton Ltd

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

Profi tability Rati os

Net Profit Margin Operating Profit Margin

Figure 5: (Graph showing Profitability ratios of both the companies)

Source: (Created by the Author)

Reporting of Environmental and Social Aspects

The reporting relating to the environmental and social aspects are included in the

sustainability reports which are prepared by the management of both the companies for the year

2017. In the case of BHP Billiton, the sustainability report shows that the management is

dedicated towards social responsibilities as it undertakes huge amount of social investments,

reduced the emission of greenhouse gases on a year by year basis and prioritize the health of the

employees and community (Bhp.com. 2018). The sustainability report of the company

effectively shows that around 1% of the pre-taxed profits of the business are investment in

developing the needs of society and community. The company invested around US$80.1 million

ACCOUNTING STANDARD AND GOVERNANCE

2017 2016 2017 2016

Rio Tinto Ltd BHP Bhiliton Ltd

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

Profi tability Rati os

Net Profit Margin Operating Profit Margin

Figure 5: (Graph showing Profitability ratios of both the companies)

Source: (Created by the Author)

Reporting of Environmental and Social Aspects

The reporting relating to the environmental and social aspects are included in the

sustainability reports which are prepared by the management of both the companies for the year

2017. In the case of BHP Billiton, the sustainability report shows that the management is

dedicated towards social responsibilities as it undertakes huge amount of social investments,

reduced the emission of greenhouse gases on a year by year basis and prioritize the health of the

employees and community (Bhp.com. 2018). The sustainability report of the company

effectively shows that around 1% of the pre-taxed profits of the business are investment in

developing the needs of society and community. The company invested around US$80.1 million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING STANDARD AND GOVERNANCE

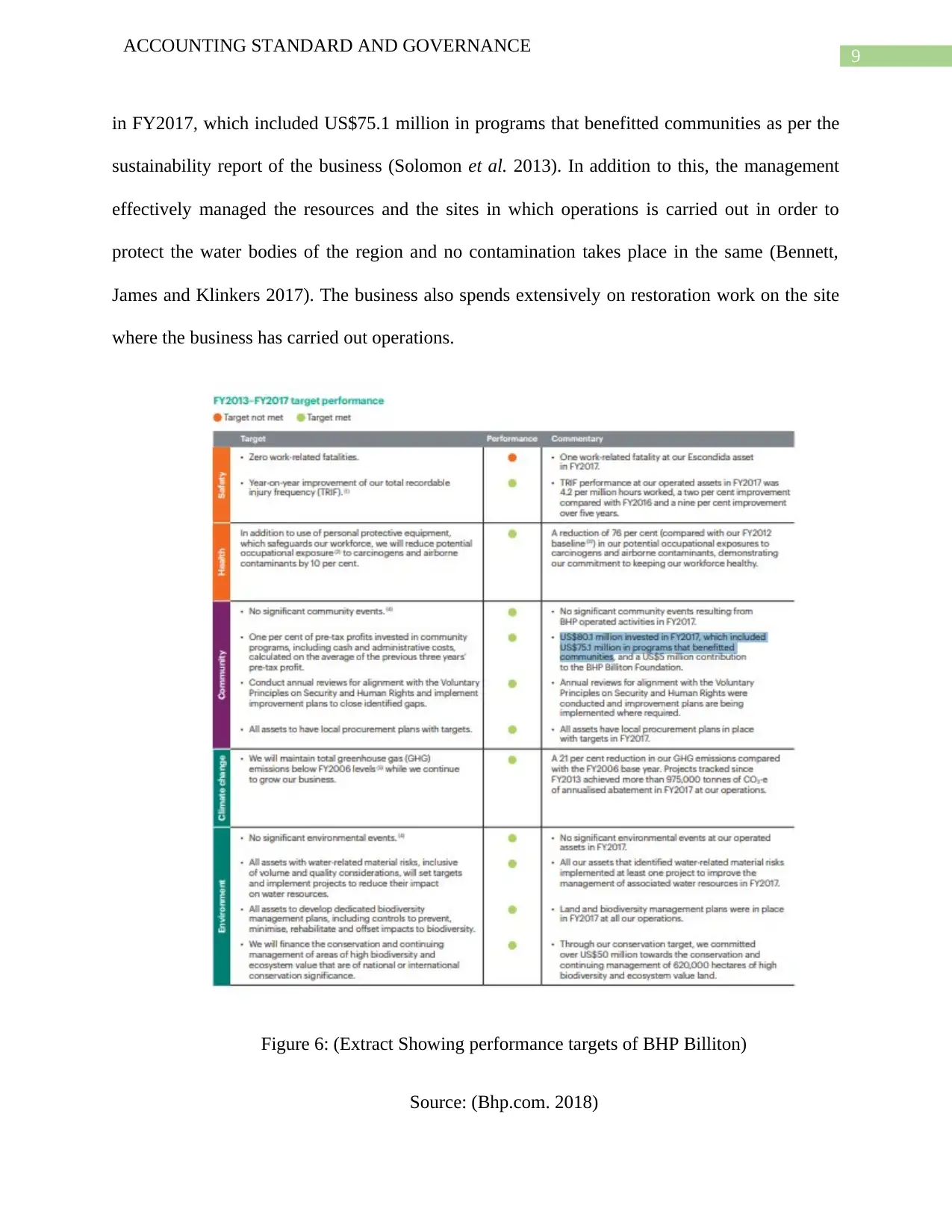

in FY2017, which included US$75.1 million in programs that benefitted communities as per the

sustainability report of the business (Solomon et al. 2013). In addition to this, the management

effectively managed the resources and the sites in which operations is carried out in order to

protect the water bodies of the region and no contamination takes place in the same (Bennett,

James and Klinkers 2017). The business also spends extensively on restoration work on the site

where the business has carried out operations.

Figure 6: (Extract Showing performance targets of BHP Billiton)

Source: (Bhp.com. 2018)

ACCOUNTING STANDARD AND GOVERNANCE

in FY2017, which included US$75.1 million in programs that benefitted communities as per the

sustainability report of the business (Solomon et al. 2013). In addition to this, the management

effectively managed the resources and the sites in which operations is carried out in order to

protect the water bodies of the region and no contamination takes place in the same (Bennett,

James and Klinkers 2017). The business also spends extensively on restoration work on the site

where the business has carried out operations.

Figure 6: (Extract Showing performance targets of BHP Billiton)

Source: (Bhp.com. 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING STANDARD AND GOVERNANCE

In the case of Rio Tinto Ltd, the management of the company has great emphasis on the

safety of the employees of the business and also the protection of the workers who are working

for the business (Qiu, Shaukat and Tharyan 2016). In terms of protection of the environment, the

business has effectively reduced the emission of green houses gases by 29%. The business has

also reduced the use of renewable resources of the business and has also introduced practices

which are sustainable and environmental friendly (Riotinto.com. 2018). Therefore, it can be said

that both the companies has effectively made disclosures relating to social and environment

activities which are undertaken by the business and the same is shown in the sustainability

reports of the business and the same is also as per the requirements of the loan.

Overall Impact of AASB 16

The introduction of AASB 16 would bring about significant changes in the reporting

framework which is followed by the business of both the companies. The new standard would

bring about transparency in the reporting framework and also ensure that the financial statements

are appropriately presented and showing true view. The new standard is beneficial for the users

of the financial statement as complete information would be available for the purpose of taking

appropriate decisions relating to investment in the business. Operating and financial leases form

part of the liabilities section and therefore with the new standard appropriate estimation of the

financial position of the business can be derived. Therefore, in overall it can be said that the new

standard would be the reporting framework better for both the companies.

Summary for Investment Company

The analysis of both the companies shows that the management of both the company has

appropriately prepared the financial statements following all rules and regulations. The adoption

of new accounting standards on leases would further improve the reporting framework of the

ACCOUNTING STANDARD AND GOVERNANCE

In the case of Rio Tinto Ltd, the management of the company has great emphasis on the

safety of the employees of the business and also the protection of the workers who are working

for the business (Qiu, Shaukat and Tharyan 2016). In terms of protection of the environment, the

business has effectively reduced the emission of green houses gases by 29%. The business has

also reduced the use of renewable resources of the business and has also introduced practices

which are sustainable and environmental friendly (Riotinto.com. 2018). Therefore, it can be said

that both the companies has effectively made disclosures relating to social and environment

activities which are undertaken by the business and the same is shown in the sustainability

reports of the business and the same is also as per the requirements of the loan.

Overall Impact of AASB 16

The introduction of AASB 16 would bring about significant changes in the reporting

framework which is followed by the business of both the companies. The new standard would

bring about transparency in the reporting framework and also ensure that the financial statements

are appropriately presented and showing true view. The new standard is beneficial for the users

of the financial statement as complete information would be available for the purpose of taking

appropriate decisions relating to investment in the business. Operating and financial leases form

part of the liabilities section and therefore with the new standard appropriate estimation of the

financial position of the business can be derived. Therefore, in overall it can be said that the new

standard would be the reporting framework better for both the companies.

Summary for Investment Company

The analysis of both the companies shows that the management of both the company has

appropriately prepared the financial statements following all rules and regulations. The adoption

of new accounting standards on leases would further improve the reporting framework of the

11

ACCOUNTING STANDARD AND GOVERNANCE

business. The ratio analysis also show that the financial performance of the business has

improved significantly for both the companies in the year 2017. Therefore, investment can be

undertaken in both the companies but the financial position is better for BHP Billiton ltd.

Conclusion

The above discussion effectively shows that the performance of Rio Tinto Ltd and BHP

Billiton ltd and makes comparison for the same. The above assessment shows the ratio analysis

of both the companies which represent the financial performance of the business. The above

discussion also shows the environmental and social reporting which is included in the

sustainability reports of the business. The investment decisions are also to be taken on the basis

of the results of ratios and reporting framework which is adopted by the business.

ACCOUNTING STANDARD AND GOVERNANCE

business. The ratio analysis also show that the financial performance of the business has

improved significantly for both the companies in the year 2017. Therefore, investment can be

undertaken in both the companies but the financial position is better for BHP Billiton ltd.

Conclusion

The above discussion effectively shows that the performance of Rio Tinto Ltd and BHP

Billiton ltd and makes comparison for the same. The above assessment shows the ratio analysis

of both the companies which represent the financial performance of the business. The above

discussion also shows the environmental and social reporting which is included in the

sustainability reports of the business. The investment decisions are also to be taken on the basis

of the results of ratios and reporting framework which is adopted by the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.