HI6025 Accounting Theory: IFRS, CSR, Fair Value & Lease Accounting

VerifiedAdded on 2023/04/25

|17

|3807

|435

Report

AI Summary

This report provides a detailed analysis of accounting standards and principles, focusing on current issues such as IFRS adoption in the U.S., nonspecific CSR regulation in Australia, a comparison of fair value and cost models, impairment testing and fair value accounting applied to Wesfarmers Company, and the new accounting for leases as proposed by the IASB. The report explores the qualitative characteristics of financial reporting, the impact of IFRS on financial disclosure, and the theoretical underpinnings of CSR regulation. It also examines the motivations behind directors' decisions regarding asset revaluation and the effects of these decisions on financial statements and shareholder wealth. Furthermore, the report analyzes Wesfarmers' impairment testing procedures, key estimates, and assumptions. Finally, it discusses the IASB chairperson's views on the new accounting for leases and its implications for financial reporting and investment decisions. Desklib provides this document and many more resources for students.

Accounting 1

ACCOUNTING THEORY AND PRACTICE

Student’s Name:

Institution Affiliation:

ACCOUNTING THEORY AND PRACTICE

Student’s Name:

Institution Affiliation:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 2

Executive Summary

The report examines the accounting standards and principles which guide firms in addressing the

current Issues. Some of the accounting issues under consideration are impairment testing, asset,

and liability revaluation, and the adoption of IFRS standards in the U.S. The report is divided

into five parts. Part A addresses the IFRS Adoption in the U.S. Part B examines the application

of nonspecific regulation on CSR in Australia. Part C is divided into three subsections which

compare Fair Value and Cost model accounting standards. Part D analyze the application of

impairment testing and fair value accounting by Wesfarmers Company, an ASX listed company.

Part E addresses the adoption and acceptance of the New Accounting for Lease as proposed by

the IASB.

Table of Contents

Executive Summary

The report examines the accounting standards and principles which guide firms in addressing the

current Issues. Some of the accounting issues under consideration are impairment testing, asset,

and liability revaluation, and the adoption of IFRS standards in the U.S. The report is divided

into five parts. Part A addresses the IFRS Adoption in the U.S. Part B examines the application

of nonspecific regulation on CSR in Australia. Part C is divided into three subsections which

compare Fair Value and Cost model accounting standards. Part D analyze the application of

impairment testing and fair value accounting by Wesfarmers Company, an ASX listed company.

Part E addresses the adoption and acceptance of the New Accounting for Lease as proposed by

the IASB.

Table of Contents

Accounting 3

Introduction.................................................................................................................................................4

Part A: IFRS Adoption in the U.S...............................................................................................................4

Qualitative characteristics of financial reporting.....................................................................................4

IFRS on financial disclosure....................................................................................................................5

Task Part B: Nonspecific regulation on CSR...............................................................................................5

(a) Public Interest Theory..................................................................................................................6

(b) Capture Theory............................................................................................................................6

(c) Economic Interest Group Theory of regulation............................................................................6

Part C: Fair Value vs Cost model................................................................................................................7

(a) The motivating factor for directors not to revalue the property, plant, and equipment.................7

(b) The effects the decision not to revalue PPE on the firm’s financial statements...........................7

(c) The impact of the decision not to revalue PPE on shareholders’ wealth......................................8

PART D: Wesfarmers Company.................................................................................................................8

(i) Asset/s that were tested for impairment...........................................................................................8

(ii) Procedure to conduct impairment testing.....................................................................................9

(iii) Impairment expenditures during the period.................................................................................9

(iv) The key estimates and assumptions used to conduct the impairment testing.............................10

(v) Presence of subjectivity that would influence the outcome of the impairment testing...............10

(vi) Difficulties to understand about the impairment testing.............................................................10

(vii) Insightful gained about conduct impairment testing......................................................................11

(viii) Based on your assignment, comment on the “fair value measurement”........................................11

PART E: New Accounting for Leases.......................................................................................................11

i. IASB chairperson’s comment on new accounting for lease...........................................................11

ii. Higher balance sheet lease liabilities compared to the debt under the former accounting for lease

accounting.............................................................................................................................................12

iii. Former accounting standard for leases offered ‘no level playing field’ between some airlines

companies..............................................................................................................................................12

iv. Chairperson’s view on the unpopularity of the new accounting for leases.................................12

v. Reasons why the chairperson believes the new visibility of all leases will lead to better-informed

investment decisions by investors and the management........................................................................13

Conclusion.................................................................................................................................................13

References List..........................................................................................................................................14

Introduction.................................................................................................................................................4

Part A: IFRS Adoption in the U.S...............................................................................................................4

Qualitative characteristics of financial reporting.....................................................................................4

IFRS on financial disclosure....................................................................................................................5

Task Part B: Nonspecific regulation on CSR...............................................................................................5

(a) Public Interest Theory..................................................................................................................6

(b) Capture Theory............................................................................................................................6

(c) Economic Interest Group Theory of regulation............................................................................6

Part C: Fair Value vs Cost model................................................................................................................7

(a) The motivating factor for directors not to revalue the property, plant, and equipment.................7

(b) The effects the decision not to revalue PPE on the firm’s financial statements...........................7

(c) The impact of the decision not to revalue PPE on shareholders’ wealth......................................8

PART D: Wesfarmers Company.................................................................................................................8

(i) Asset/s that were tested for impairment...........................................................................................8

(ii) Procedure to conduct impairment testing.....................................................................................9

(iii) Impairment expenditures during the period.................................................................................9

(iv) The key estimates and assumptions used to conduct the impairment testing.............................10

(v) Presence of subjectivity that would influence the outcome of the impairment testing...............10

(vi) Difficulties to understand about the impairment testing.............................................................10

(vii) Insightful gained about conduct impairment testing......................................................................11

(viii) Based on your assignment, comment on the “fair value measurement”........................................11

PART E: New Accounting for Leases.......................................................................................................11

i. IASB chairperson’s comment on new accounting for lease...........................................................11

ii. Higher balance sheet lease liabilities compared to the debt under the former accounting for lease

accounting.............................................................................................................................................12

iii. Former accounting standard for leases offered ‘no level playing field’ between some airlines

companies..............................................................................................................................................12

iv. Chairperson’s view on the unpopularity of the new accounting for leases.................................12

v. Reasons why the chairperson believes the new visibility of all leases will lead to better-informed

investment decisions by investors and the management........................................................................13

Conclusion.................................................................................................................................................13

References List..........................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 4

Introduction

This report provides conclusive analysis of some inherent changes in the accounting frameworks

as a function of recent changes brought about by the IFRS standards. The research also

demonstrates the response of the various industry stakeholders to the changes in accounting

standards including the government. More specifically the analysis covers the effect of such

changes on the account standards such as revaluation, impairment, and leases for various assets

within companies and the subsequent treatment of these changes in financial statements.

Part A: IFRS Adoption in the U.S.

Qualitative characteristics of financial reporting

Confidentiality has been a guiding principle in financial reporting however the adoption of IFRS

would go against this principle. IFRS states that companies must publically publish their

financial statements for the stakeholders to scrutinize. According to a statement published by Lin

(2017), “Millions of dollars have been spent adopting international financial reporting standards

to help investors make like-for-like comparisons between companies in global capital markets.

But CFOs say they are useless and have driven financial disclosures to unmanageable levels”.

According to this statement, although IFRS has been updated to cater for the current reporting

practices, the standard disregards confidentiality of company audited reports. The adoption of

IFRS by the U.S entities would prohibit them from enjoying professionalism and confidentiality

principles under the U.S. GAAP (Brown, 2012, p. 63).

Introduction

This report provides conclusive analysis of some inherent changes in the accounting frameworks

as a function of recent changes brought about by the IFRS standards. The research also

demonstrates the response of the various industry stakeholders to the changes in accounting

standards including the government. More specifically the analysis covers the effect of such

changes on the account standards such as revaluation, impairment, and leases for various assets

within companies and the subsequent treatment of these changes in financial statements.

Part A: IFRS Adoption in the U.S.

Qualitative characteristics of financial reporting

Confidentiality has been a guiding principle in financial reporting however the adoption of IFRS

would go against this principle. IFRS states that companies must publically publish their

financial statements for the stakeholders to scrutinize. According to a statement published by Lin

(2017), “Millions of dollars have been spent adopting international financial reporting standards

to help investors make like-for-like comparisons between companies in global capital markets.

But CFOs say they are useless and have driven financial disclosures to unmanageable levels”.

According to this statement, although IFRS has been updated to cater for the current reporting

practices, the standard disregards confidentiality of company audited reports. The adoption of

IFRS by the U.S entities would prohibit them from enjoying professionalism and confidentiality

principles under the U.S. GAAP (Brown, 2012, p. 63).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 5

IFRS on financial disclosure

The IFRS principle on financial disclosure has been adopted globally. The principle requires

companies to disclose specific financial information to achieve financial uniformity in company

reporting (Nobes, 2011, p. 112) (Azmi, 2016, p. 51). A good example is the IFRS 7 which

requires the provision of the important financial instruments and the risks attached to the specific

financial instruments including the nature of such risks (Deloitte, 2019, p. 43) (Beerbaum, 2016).

Likewise, the IFRS 9 provides for the measurement at fair value of financial assets and liabilities

held by a firm for trade or their original value (Beerbaum, 2016, p. 32).

The statement by the former AXA head of finance Geoff Roberts contradicts the importance of

the IFRS adjustments. This statement elaborates on the importance of the financial adjustments

required by IFRS. Investment analysts and fund managers only assume the adjustments because

they are either not aware or not really affected by the adjustments or are completely ignorant.

The IFRS adjustments should be adopted and applied not only by companies but by stakeholders

as well.

The statement by the Wes farmers’ manager indicates that analysts may experience problems

when interpreting the IFRS given the technical nature. Such analysts require subsequent training

which would support acceptance of IFRS. The two statements are inconsistent with the intended

adoption of the IFRS by companies in terms of the technicalities presented.

Task Part B: Nonspecific regulation on CSR

The decision by the Australian government not to introduce specific regulation on CRS can be

explained from the perspective of:

IFRS on financial disclosure

The IFRS principle on financial disclosure has been adopted globally. The principle requires

companies to disclose specific financial information to achieve financial uniformity in company

reporting (Nobes, 2011, p. 112) (Azmi, 2016, p. 51). A good example is the IFRS 7 which

requires the provision of the important financial instruments and the risks attached to the specific

financial instruments including the nature of such risks (Deloitte, 2019, p. 43) (Beerbaum, 2016).

Likewise, the IFRS 9 provides for the measurement at fair value of financial assets and liabilities

held by a firm for trade or their original value (Beerbaum, 2016, p. 32).

The statement by the former AXA head of finance Geoff Roberts contradicts the importance of

the IFRS adjustments. This statement elaborates on the importance of the financial adjustments

required by IFRS. Investment analysts and fund managers only assume the adjustments because

they are either not aware or not really affected by the adjustments or are completely ignorant.

The IFRS adjustments should be adopted and applied not only by companies but by stakeholders

as well.

The statement by the Wes farmers’ manager indicates that analysts may experience problems

when interpreting the IFRS given the technical nature. Such analysts require subsequent training

which would support acceptance of IFRS. The two statements are inconsistent with the intended

adoption of the IFRS by companies in terms of the technicalities presented.

Task Part B: Nonspecific regulation on CSR

The decision by the Australian government not to introduce specific regulation on CRS can be

explained from the perspective of:

Accounting 6

(a) Public Interest Theory

The public interest theory states that decisions should be to the best interests for the general

public. The public interests theory is inclined toward the preservation of general welfare rather

than the interest that is expressed by well-organized stakeholders (Deegan, 2013, p. 98). Based

on this theory, the government chose not to introduce specific regulations on CSR. The

government decided that the market forces would provide a win-win situation for public

companies and society. The onus is on companies to streamline their operations in line with the

main objectives of social and environmental concerns. Therefore, companies should maintain the

best interests and policies that relate to social and environmental aspects (Lama, 2015, p. 41).

(b) Capture Theory

The capture theory states that the agency relationship that exists between the regulators and the

industry has more benefit for the industry rather than the public interest. The theory holds that

government regulators tend to promote regulations that give more advantage to companies at the

expense of the public. Companies tend to influence the decisions made by government regulators

through financial favors. The effect of such observation is the opposite of intended outcomes

which is to promote the social and environmental responsibilities by companies. Therefore, there

was no need for specific regulations which would not be implemented by the regulatory agencies

(Shimeld, 2017, p. 71).

(c) Economic Interest Group Theory of regulation

The economic interest group theory states that the industry develops its own regulations and

these regulations are aimed at creating equal benefits for the parties concerned. The theory puts

the government on the supply side and the interest groups on the demand side. The government

(a) Public Interest Theory

The public interest theory states that decisions should be to the best interests for the general

public. The public interests theory is inclined toward the preservation of general welfare rather

than the interest that is expressed by well-organized stakeholders (Deegan, 2013, p. 98). Based

on this theory, the government chose not to introduce specific regulations on CSR. The

government decided that the market forces would provide a win-win situation for public

companies and society. The onus is on companies to streamline their operations in line with the

main objectives of social and environmental concerns. Therefore, companies should maintain the

best interests and policies that relate to social and environmental aspects (Lama, 2015, p. 41).

(b) Capture Theory

The capture theory states that the agency relationship that exists between the regulators and the

industry has more benefit for the industry rather than the public interest. The theory holds that

government regulators tend to promote regulations that give more advantage to companies at the

expense of the public. Companies tend to influence the decisions made by government regulators

through financial favors. The effect of such observation is the opposite of intended outcomes

which is to promote the social and environmental responsibilities by companies. Therefore, there

was no need for specific regulations which would not be implemented by the regulatory agencies

(Shimeld, 2017, p. 71).

(c) Economic Interest Group Theory of regulation

The economic interest group theory states that the industry develops its own regulations and

these regulations are aimed at creating equal benefits for the parties concerned. The theory puts

the government on the supply side and the interest groups on the demand side. The government

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 7

supplies the regulation and the interest groups apply them. However, the government uses its

leverage to attain more leverage compared to the interest groups. The advantage of the economic

interest group theory is that the national gains more by regulating the industry while the

disadvantage is that some groups gain more. At the end of the day, the government and the

industry gain more than other specific interest groups. In this case, the Australian government

does not make any social or environmental changes to the Corporations Act because it would

lose the benefits by doing so (Safari, 2017, p. 127).

Part C: Fair Value vs Cost model

(a) The motivating factor for directors not to revalue the property, plant, and equipment

Revaluation of property plant and equipment (PPE) is consistent with the international

accounting standard 16 (IAS 16) (Islam, 2016, p. 201). PPE depreciates over time thus the need

to revalue them in the balance sheet. Revaluation normally reduces the value of PPE because of

the element of depreciation which is treated as an expense in the company financials. Therefore,

the revaluation of PPE attracts a depreciation cost and more taxation when there is a revaluation

surplus recognized in the statement of other comprehensive income. Another factor that

motivates directors to oppose revaluation of PPE is the decrease in the company value or the

market capitalization based on the total net assets (Park, 2016, p. 88).

(b) The effects the decision not to revalue PPE on the firm’s financial statements

Failure to reevaluate PPE has a direct effect on a company’s financial statements. First, the

financial statements shall not represent a true and fair financial position of a company’s value

leading to probable misstatement (Chong, 2009, p. 66). The information would misguide the

supplies the regulation and the interest groups apply them. However, the government uses its

leverage to attain more leverage compared to the interest groups. The advantage of the economic

interest group theory is that the national gains more by regulating the industry while the

disadvantage is that some groups gain more. At the end of the day, the government and the

industry gain more than other specific interest groups. In this case, the Australian government

does not make any social or environmental changes to the Corporations Act because it would

lose the benefits by doing so (Safari, 2017, p. 127).

Part C: Fair Value vs Cost model

(a) The motivating factor for directors not to revalue the property, plant, and equipment

Revaluation of property plant and equipment (PPE) is consistent with the international

accounting standard 16 (IAS 16) (Islam, 2016, p. 201). PPE depreciates over time thus the need

to revalue them in the balance sheet. Revaluation normally reduces the value of PPE because of

the element of depreciation which is treated as an expense in the company financials. Therefore,

the revaluation of PPE attracts a depreciation cost and more taxation when there is a revaluation

surplus recognized in the statement of other comprehensive income. Another factor that

motivates directors to oppose revaluation of PPE is the decrease in the company value or the

market capitalization based on the total net assets (Park, 2016, p. 88).

(b) The effects the decision not to revalue PPE on the firm’s financial statements

Failure to reevaluate PPE has a direct effect on a company’s financial statements. First, the

financial statements shall not represent a true and fair financial position of a company’s value

leading to probable misstatement (Chong, 2009, p. 66). The information would misguide the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 8

stakeholders and the decision makers who rely on the company’s financials. A company’s failure

to reevaluate PPE can be established during auditing by either forensic analysts or forensic

auditors (Ngwakwe, 2017, p. 59). The findings can be a disappointment to the company’s

shareholders and bring about the subsequent adverse impact on future operations of the

company.

(c) The impact of the decision not to revalue PPE on shareholders’ wealth

The decision to keep the company assets as they are without revaluation shall affect both the

total valuation of the company and its total value of shares. In light of this statement then it

becomes quite likely that shareholders’ wealth can be adversely affected where assets depreciate.

In the case of appreciation of the value of assets such as land, the total value of shareholders’

wealth shall be undervalued (Wolk, et al., 2017, p. 87).

PART D: Wesfarmers Company

The analysis has been prepared based on Wes Farmers’ 2018 financial report.

Within your firm’s latest annual report

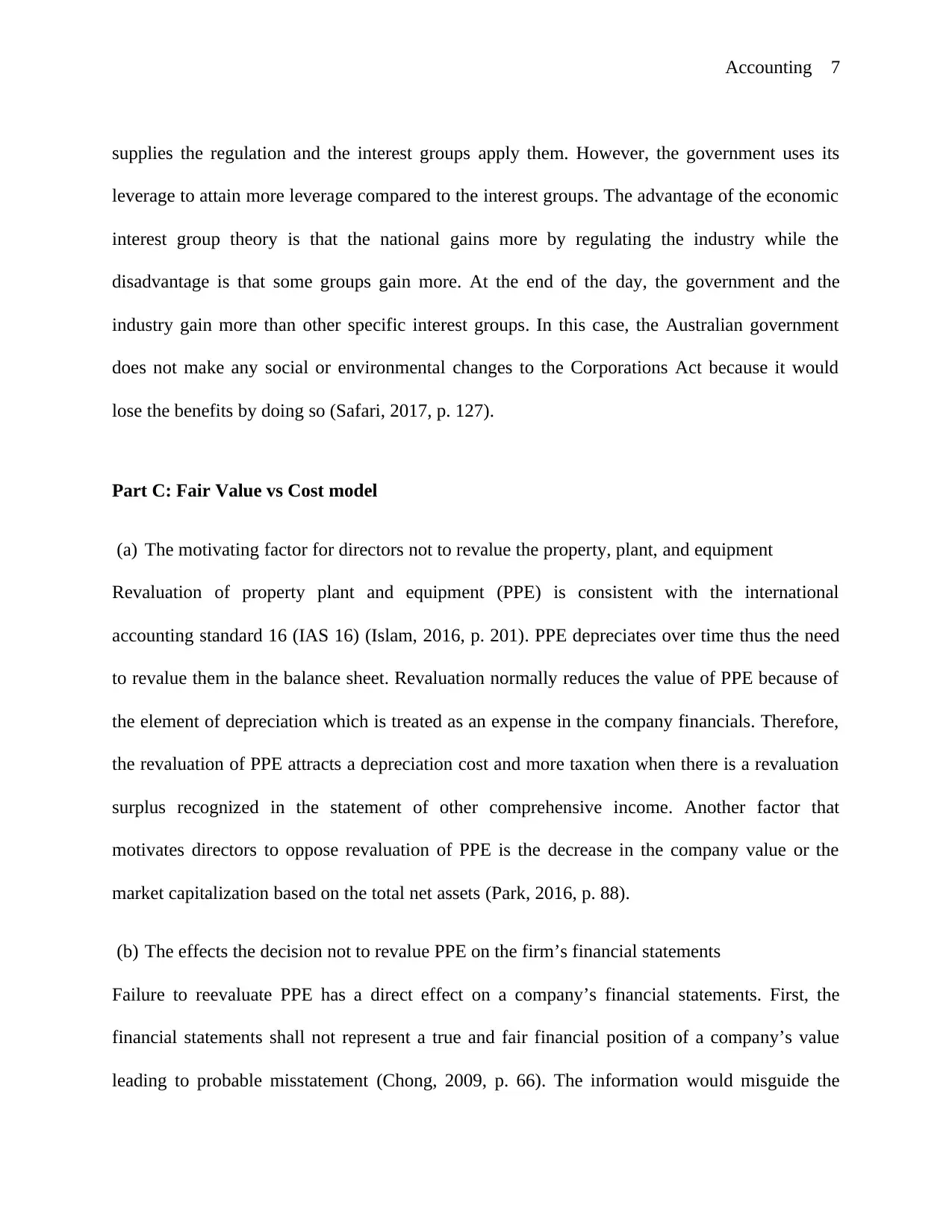

(i) Asset/s that were tested for impairment

Testing for impairment for Wesfarmers Group has been addressed under note 17 of the 2018

annual report. The company tested its property, plant and equipment, intangibles and goodwill as

shown in the Impairment of non-financial assets picture below.

stakeholders and the decision makers who rely on the company’s financials. A company’s failure

to reevaluate PPE can be established during auditing by either forensic analysts or forensic

auditors (Ngwakwe, 2017, p. 59). The findings can be a disappointment to the company’s

shareholders and bring about the subsequent adverse impact on future operations of the

company.

(c) The impact of the decision not to revalue PPE on shareholders’ wealth

The decision to keep the company assets as they are without revaluation shall affect both the

total valuation of the company and its total value of shares. In light of this statement then it

becomes quite likely that shareholders’ wealth can be adversely affected where assets depreciate.

In the case of appreciation of the value of assets such as land, the total value of shareholders’

wealth shall be undervalued (Wolk, et al., 2017, p. 87).

PART D: Wesfarmers Company

The analysis has been prepared based on Wes Farmers’ 2018 financial report.

Within your firm’s latest annual report

(i) Asset/s that were tested for impairment

Testing for impairment for Wesfarmers Group has been addressed under note 17 of the 2018

annual report. The company tested its property, plant and equipment, intangibles and goodwill as

shown in the Impairment of non-financial assets picture below.

Accounting 9

Picture 1: Impairment of non-financial assets

Source: (WesFarmers, 2018, p. 129)

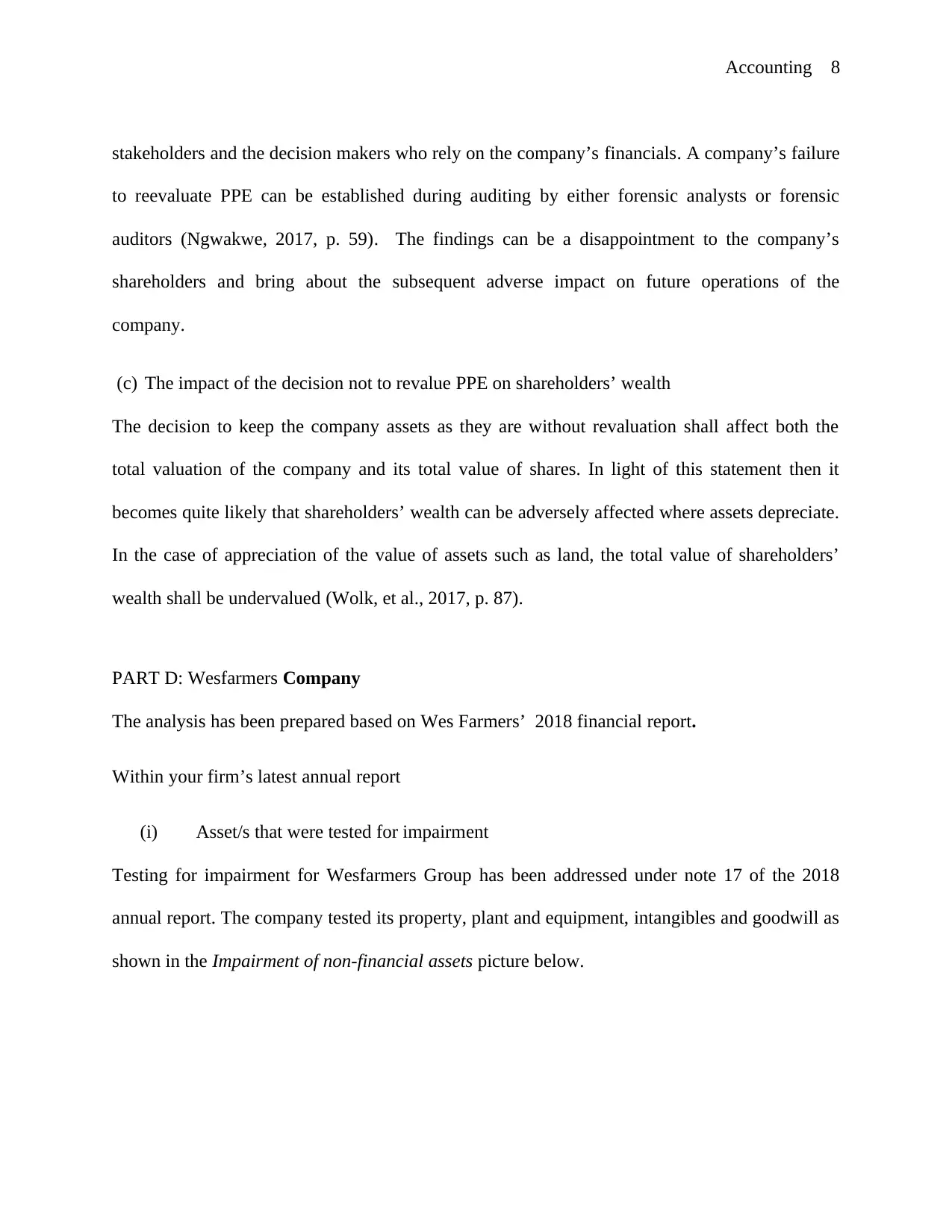

(ii) Procedure to conduct impairment testing

Wesfarmers Inc. calculated the impairment based on an annual percentage test on the specific

PPE assets of the firm and the subsequent recognition of a provision within the financial

statements (WesFarmers, 2018, p. 129). The impairment was also established as a function of

revaluation of the company assets and the figures compared to the initial company figures,

therefore, enabling the determination of the actual impairment costs (Ji, 2013, p. 76). Impairment

was tested and calculated as shown in picture 2 below.

Picture 2: Impairment Calculations procedure

Source: (WesFarmers, 2018, p. 129)

Picture 1: Impairment of non-financial assets

Source: (WesFarmers, 2018, p. 129)

(ii) Procedure to conduct impairment testing

Wesfarmers Inc. calculated the impairment based on an annual percentage test on the specific

PPE assets of the firm and the subsequent recognition of a provision within the financial

statements (WesFarmers, 2018, p. 129). The impairment was also established as a function of

revaluation of the company assets and the figures compared to the initial company figures,

therefore, enabling the determination of the actual impairment costs (Ji, 2013, p. 76). Impairment

was tested and calculated as shown in picture 2 below.

Picture 2: Impairment Calculations procedure

Source: (WesFarmers, 2018, p. 129)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting 10

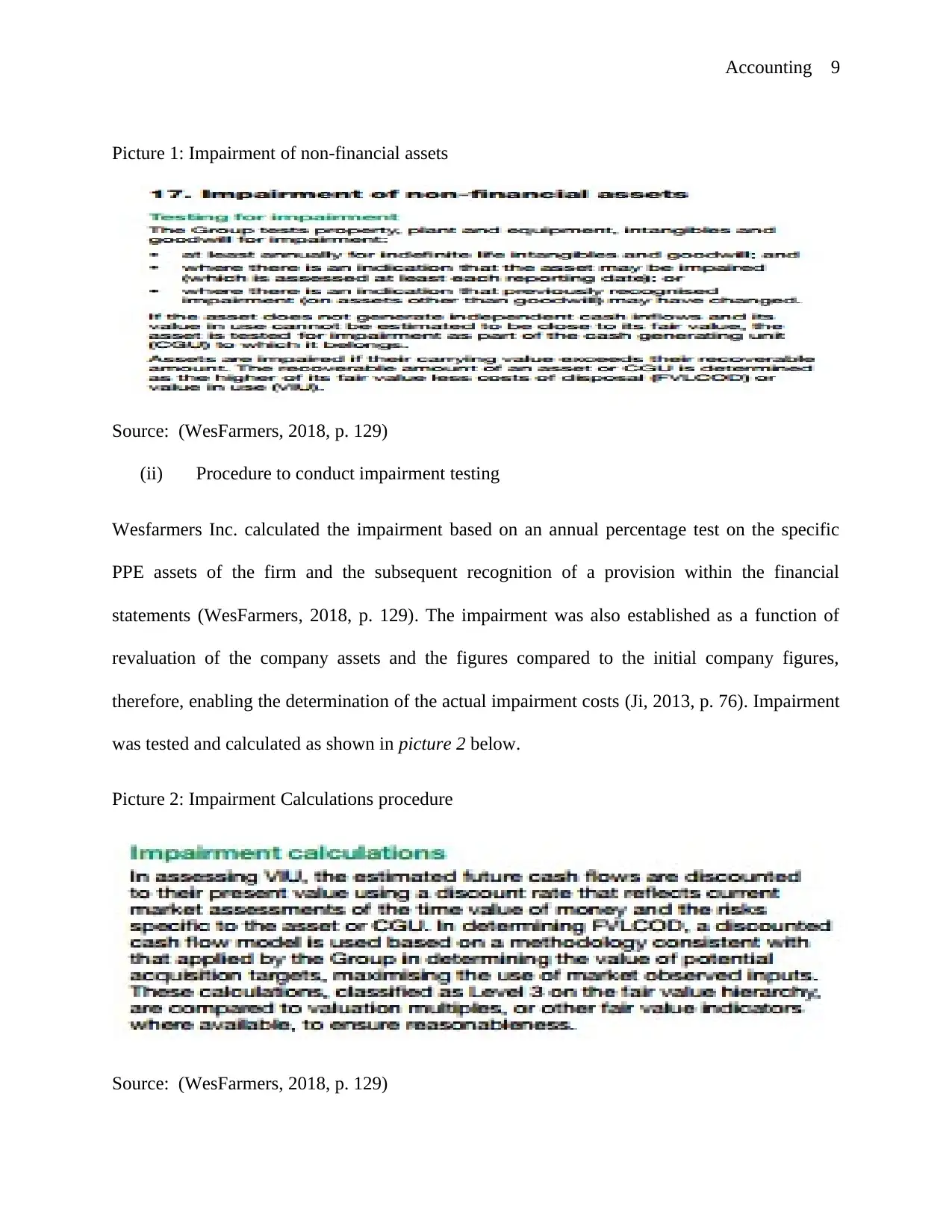

(iii) Impairment expenditures during the period

Yes, Wesfarmers Inc. has determined that the firm has had impairment expenditures reduce the

net profit after tax significantly which include $92 M impairments relating to write-offs and store

closure provisions as well as 66M relating to the write-down of stock as shown in picture 3

below.

Picture 3: Impairment recognised during the 2018 financial year

Source: (WesFarmers, 2018, p. 129)

(iv) The key estimates and assumptions used to conduct the impairment testing.

The impairments are assumed to relate to the annual depreciation of the PEE held by the firm

and therefore there has been a provision for the impairment charges. The key estimates include

the fair value determination of one of the lines of operations that have been disposed of, which is

Buki. The impairments also include the fair value determination of the value of the firm and the

related goodwill amortization as impairment charges (Nobe, 2015).

(v) Presence of subjectivity that would influence the outcome of the impairment testing.

(iii) Impairment expenditures during the period

Yes, Wesfarmers Inc. has determined that the firm has had impairment expenditures reduce the

net profit after tax significantly which include $92 M impairments relating to write-offs and store

closure provisions as well as 66M relating to the write-down of stock as shown in picture 3

below.

Picture 3: Impairment recognised during the 2018 financial year

Source: (WesFarmers, 2018, p. 129)

(iv) The key estimates and assumptions used to conduct the impairment testing.

The impairments are assumed to relate to the annual depreciation of the PEE held by the firm

and therefore there has been a provision for the impairment charges. The key estimates include

the fair value determination of one of the lines of operations that have been disposed of, which is

Buki. The impairments also include the fair value determination of the value of the firm and the

related goodwill amortization as impairment charges (Nobe, 2015).

(v) Presence of subjectivity that would influence the outcome of the impairment testing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting 11

No subjectivity was found in the impairment testing process for Wesfarmers Inc. thus no

material influence on the firm.

(vi) Difficulties to understand about the impairment testing

Impairment testing for Wesfarmers Inc. has been combined with the write-offs as well as store

closure provisions as one figure of $99 M. The target impairments for 2018 has been provided as

$300M which has been deducted from the 2018 EBIT amounts pretax. The confusing aspect

however about the impairment realized is that the impairment has not been specified for the

exact asset it relates to rather than the PPE generalization (Wang, 2018, p. 139).

(vii) Insightful gained about conduct impairment testing

First, impairment testing is based on estimates and assumptions that are not necessarily accurate

in terms of the amounts recorded within the financial statements. Second, impairment testing can

be done for the cash and non-cash impairments and combined cash Generating Unit (CGU). And

third, impairment testing is based on the measurement of assets at fair value of assets (Roozen,

2018, p. 119).

(viii) Based on your assignment, comment on the “fair value measurement”.

Fair value measurement is the best approximation or determination of the best possible value for

an asset at the fair market value. The international accounting standards provide the

measurement of assets at the best possible fair value as per the IFRS. IFRS 9 provides for the

measurement of fair value through the profit and loss for the assets held at original costs and

those financial assets that are held for sale. The differences in the valuation of assets at fair value

No subjectivity was found in the impairment testing process for Wesfarmers Inc. thus no

material influence on the firm.

(vi) Difficulties to understand about the impairment testing

Impairment testing for Wesfarmers Inc. has been combined with the write-offs as well as store

closure provisions as one figure of $99 M. The target impairments for 2018 has been provided as

$300M which has been deducted from the 2018 EBIT amounts pretax. The confusing aspect

however about the impairment realized is that the impairment has not been specified for the

exact asset it relates to rather than the PPE generalization (Wang, 2018, p. 139).

(vii) Insightful gained about conduct impairment testing

First, impairment testing is based on estimates and assumptions that are not necessarily accurate

in terms of the amounts recorded within the financial statements. Second, impairment testing can

be done for the cash and non-cash impairments and combined cash Generating Unit (CGU). And

third, impairment testing is based on the measurement of assets at fair value of assets (Roozen,

2018, p. 119).

(viii) Based on your assignment, comment on the “fair value measurement”.

Fair value measurement is the best approximation or determination of the best possible value for

an asset at the fair market value. The international accounting standards provide the

measurement of assets at the best possible fair value as per the IFRS. IFRS 9 provides for the

measurement of fair value through the profit and loss for the assets held at original costs and

those financial assets that are held for sale. The differences in the valuation of assets at fair value

Accounting 12

over time amount to impairment except for the assets whose value increases with time (Carlin,

2008, p. 42).

PART E: New Accounting for Leases

i. IASB chairperson’s comment on new accounting for lease

The chairperson of the IASB was of the view that the former accounting standard of leases did

not reflect the actual economic reality as it was majorly based on finance leases recognition

rather than all leases thus concealing material liabilities in company financials (Lin, 2017, p. 21).

ii. Higher balance sheet lease liabilities compared to the debt under the former accounting for

lease accounting

This observation was because of the long term debt obligation represented by the operating

leases and the widespread number of leases that were taken up by firms due to the ability of non-

disclosure in the balance sheet thus the accumulation of debt obligations by firms (Nobe, 2015,

p. 90).

iii. Former accounting standard for leases offered ‘no level playing field’ between some airlines

companies

Some airline companies lease all their fleet thus accumulating long term debt obligations which

are intentionally left out from being reported in the balance sheet. Other airlines acquire all their

fleet by purchase thus incurring actual costs and actual ownership of fleets. The performance of

such companies could not be compared on similar scope given the treatment of leases under the

old accounting standard (Ram, 2013, p. 37).

over time amount to impairment except for the assets whose value increases with time (Carlin,

2008, p. 42).

PART E: New Accounting for Leases

i. IASB chairperson’s comment on new accounting for lease

The chairperson of the IASB was of the view that the former accounting standard of leases did

not reflect the actual economic reality as it was majorly based on finance leases recognition

rather than all leases thus concealing material liabilities in company financials (Lin, 2017, p. 21).

ii. Higher balance sheet lease liabilities compared to the debt under the former accounting for

lease accounting

This observation was because of the long term debt obligation represented by the operating

leases and the widespread number of leases that were taken up by firms due to the ability of non-

disclosure in the balance sheet thus the accumulation of debt obligations by firms (Nobe, 2015,

p. 90).

iii. Former accounting standard for leases offered ‘no level playing field’ between some airlines

companies

Some airline companies lease all their fleet thus accumulating long term debt obligations which

are intentionally left out from being reported in the balance sheet. Other airlines acquire all their

fleet by purchase thus incurring actual costs and actual ownership of fleets. The performance of

such companies could not be compared on similar scope given the treatment of leases under the

old accounting standard (Ram, 2013, p. 37).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.