Comparison of Accounting Standards of Coal India Ltd in India and Ceylon Steel Corporation in Sri Lanka

VerifiedAdded on 2023/06/12

|31

|7672

|326

AI Summary

This research project is conducted to learn accounting standards and norms typically followed in India and Sri Lanka. The purpose of the research is to evaluate the accounting standards of Sri Lanka and India. Thus, identify the standards and their impact on the organizations, the research considers two different organizations such Coal India Limited in India and Ceylon Steel Corporation in Sri Lanka.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: RESEARCH REPORT

Research Report

Name of the Student

Name of the University

Author Note

Research Report

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1RESEARCH REPORT

Abstract

This research project is conducted to learn accounting standards and norms typically followed

in India and Sri Lanka. The purpose of the research is to evaluate the accounting standards of

Sri Lanka and India. Thus, identify the standards and their impact on the organizations, the

research considers two differentorganizations such Coal India Limited in India and Ceylon

Steel Corporation in Sri Lanka. The review of literature indicates that both the nations

conduct accounting operation on the basis of Global Accounting Standards. The review of

literature also indicates that the major features of “Sri Lanka Accounting Standards” consists

of the accounting procedures which is prefixed with SLFRS and LKAS and LKAS is the

main accounting standards in Sri Lanka. The review of literature has been observed with the

Ind AS being named and number conforming to International Financial Reporting Standards

(IFRS). The research includes a secondary analysis which is conducted by collecting

secondary data from peer reviewed journals, blogs and annual report of the selected

organizations. To derive the outcome from the data findings, thematic data analysis has been

performed. The findings indicate that there are several differences in accounting standards in

India and Sri Lanka. However, the despite the differences in the accounting standa4rds,

organizations follow global accounting standards to make understandable accounting

standards format, which is further represented to investors for taking investment decisions.

Abstract

This research project is conducted to learn accounting standards and norms typically followed

in India and Sri Lanka. The purpose of the research is to evaluate the accounting standards of

Sri Lanka and India. Thus, identify the standards and their impact on the organizations, the

research considers two differentorganizations such Coal India Limited in India and Ceylon

Steel Corporation in Sri Lanka. The review of literature indicates that both the nations

conduct accounting operation on the basis of Global Accounting Standards. The review of

literature also indicates that the major features of “Sri Lanka Accounting Standards” consists

of the accounting procedures which is prefixed with SLFRS and LKAS and LKAS is the

main accounting standards in Sri Lanka. The review of literature has been observed with the

Ind AS being named and number conforming to International Financial Reporting Standards

(IFRS). The research includes a secondary analysis which is conducted by collecting

secondary data from peer reviewed journals, blogs and annual report of the selected

organizations. To derive the outcome from the data findings, thematic data analysis has been

performed. The findings indicate that there are several differences in accounting standards in

India and Sri Lanka. However, the despite the differences in the accounting standa4rds,

organizations follow global accounting standards to make understandable accounting

standards format, which is further represented to investors for taking investment decisions.

2RESEARCH REPORT

Table of Contents

1.0 Introduction..........................................................................................................................3

1.1 Background to the research..............................................................................................4

1.2 Research Questions and Explanation...............................................................................4

2.0 Literature Review.................................................................................................................5

2.1 Accounting standards followed both in India and Sri Lanka...........................................6

2.2 Dissimilarities between the accounting standards both India and Sri Lanka...................7

3.0 Research Methodology.........................................................................................................8

3.1 Research philosophy........................................................................................................8

3.2 Research approach...........................................................................................................8

3.3 Data collection.................................................................................................................9

3.4 Qualitative data collection method...................................................................................9

3.5 Ethical consideration......................................................................................................10

3.6 Research limitation.........................................................................................................10

4.0 Investigation and Research Findings.................................................................................10

Theme 1: Comparison of Accounting Standards Followed in Sri Lanka and India............10

Theme 2: Similarity in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation..........................................................................................................................14

Theme 3: Differences in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation..........................................................................................................................17

5. Ratio Analysis of Coal India Ltd in India and Ceylon Steel Corporation...........................20

Table of Contents

1.0 Introduction..........................................................................................................................3

1.1 Background to the research..............................................................................................4

1.2 Research Questions and Explanation...............................................................................4

2.0 Literature Review.................................................................................................................5

2.1 Accounting standards followed both in India and Sri Lanka...........................................6

2.2 Dissimilarities between the accounting standards both India and Sri Lanka...................7

3.0 Research Methodology.........................................................................................................8

3.1 Research philosophy........................................................................................................8

3.2 Research approach...........................................................................................................8

3.3 Data collection.................................................................................................................9

3.4 Qualitative data collection method...................................................................................9

3.5 Ethical consideration......................................................................................................10

3.6 Research limitation.........................................................................................................10

4.0 Investigation and Research Findings.................................................................................10

Theme 1: Comparison of Accounting Standards Followed in Sri Lanka and India............10

Theme 2: Similarity in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation..........................................................................................................................14

Theme 3: Differences in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation..........................................................................................................................17

5. Ratio Analysis of Coal India Ltd in India and Ceylon Steel Corporation...........................20

3RESEARCH REPORT

5.1. Profitability Ratios........................................................................................................20

5.2. Efficiency Ratios...........................................................................................................21

5.3. Liquidity Ratios.............................................................................................................21

5.4. Solvency Ratios.............................................................................................................22

6.0 Conclusion..........................................................................................................................23

References and Bibliography...................................................................................................25

5.1. Profitability Ratios........................................................................................................20

5.2. Efficiency Ratios...........................................................................................................21

5.3. Liquidity Ratios.............................................................................................................21

5.4. Solvency Ratios.............................................................................................................22

6.0 Conclusion..........................................................................................................................23

References and Bibliography...................................................................................................25

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4RESEARCH REPORT

Topic: Comparison of accounting standards of Coal India Ltd in India and Ceylon Steel

Corporation in Sri Lanka

1.0 Introduction

This research report is based on financial accounting procedures standards of India

and Sri Lanka. It has been identified that the recent paradigm in the economic environment in

India in the last few years led to extending attention being put forward to account standards

as the base towardsensuring potent as well as transparent financial reporting by corporates.As

mentionedby Brown, PreiatoandTarca (2014), accounting standards are the documented or

written statementsconsistingof rules and instructions which is further issued by the

accounting institutions, for the preparation of uniform as well as consistent financial

statements. This may further havefurther impact on different users of accounting information.

Wang (2014) mentioned that the fact that “International Financial Reporting Standards”

(IFRSs), issued by International Accounting Standards Board, as the uniform language of

business to protect the interest of international investor brought into the focus of IAS/IFRS. A

two decades ago, “The Institute of Chartered Accountants” in India become a premier

accounting body in the nation, took upon itself the leadership role by developing Accounting

Standards Board in the year 1997. Nonetheless, Today in India, the accounting standards

have come a long way (Pacter, 2014). However, the effectiveness of developed accounting

standards in India have not been assessed as required.

On the other side, the accounting standards in Sri Lanka observed some significant

changes based on the objectives set by nation itself. Sri Lanka is determined to makes

changes in the accounting standards with objective of developing understandable, enforceable

accounting standards that needs high quality transparent as well as comparable information in

the financial statement. The government of the nation is making effort to promote theuse as

Topic: Comparison of accounting standards of Coal India Ltd in India and Ceylon Steel

Corporation in Sri Lanka

1.0 Introduction

This research report is based on financial accounting procedures standards of India

and Sri Lanka. It has been identified that the recent paradigm in the economic environment in

India in the last few years led to extending attention being put forward to account standards

as the base towardsensuring potent as well as transparent financial reporting by corporates.As

mentionedby Brown, PreiatoandTarca (2014), accounting standards are the documented or

written statementsconsistingof rules and instructions which is further issued by the

accounting institutions, for the preparation of uniform as well as consistent financial

statements. This may further havefurther impact on different users of accounting information.

Wang (2014) mentioned that the fact that “International Financial Reporting Standards”

(IFRSs), issued by International Accounting Standards Board, as the uniform language of

business to protect the interest of international investor brought into the focus of IAS/IFRS. A

two decades ago, “The Institute of Chartered Accountants” in India become a premier

accounting body in the nation, took upon itself the leadership role by developing Accounting

Standards Board in the year 1997. Nonetheless, Today in India, the accounting standards

have come a long way (Pacter, 2014). However, the effectiveness of developed accounting

standards in India have not been assessed as required.

On the other side, the accounting standards in Sri Lanka observed some significant

changes based on the objectives set by nation itself. Sri Lanka is determined to makes

changes in the accounting standards with objective of developing understandable, enforceable

accounting standards that needs high quality transparent as well as comparable information in

the financial statement. The government of the nation is making effort to promote theuse as

5RESEARCH REPORT

well as rigorous applications those standards. Thus, to identify the effectiveness of

accounting standards of both the nations, this research report performs a comparative analysis

involving two different organizations namely Coal India Limited and Ceylon Steel

Corporation in Sri Lanka.

1.1 Background to the research

As put forward by Preiato, Brown and Tarca (2015) Accounting Standards are

formed with the focus to harmonize different accounting policies as well as practices in the

use in a nation. Therefore, the major goal of Accounting Standard is, to minimize the

accounting alternatives in the making of financial statements within the grounds of

rationality. Thus, ensuring comparability of financial statements of differentorganizationsas

with the focus to deliver meaningful information to different users of financial statements to

allow to make informed economic decisions. As put forward by Mora and Walker (2015) The

Companies Act and several other statutes in Indian mentions that the financial statement of an

organizations should deliver a true as well as fair view of its financial stateas well as working

outcome. Theprinciple of this act also reveals that thisnecessity is implicit even in the absent

of a particular statutory provisions to this effect. According to Crawford et al., (2014),

financialreporting framework Sri Lanka indicates that Institute of CharteredAccount of Sri

Lanka made a significant decisions to converge with all pronouncements imposed by IASB.

1.2 Research Questions and Explanation

1. What are aspects based on which the differences in the accounting standards between

India and Sri Lanka can be compared?

This research question is appropriate because as the topic revolves around the differences and

similarities of accounting standards of two difference nations. This research question helps to

know all differences in accounting standards followed by India and Sri Lanka.

well as rigorous applications those standards. Thus, to identify the effectiveness of

accounting standards of both the nations, this research report performs a comparative analysis

involving two different organizations namely Coal India Limited and Ceylon Steel

Corporation in Sri Lanka.

1.1 Background to the research

As put forward by Preiato, Brown and Tarca (2015) Accounting Standards are

formed with the focus to harmonize different accounting policies as well as practices in the

use in a nation. Therefore, the major goal of Accounting Standard is, to minimize the

accounting alternatives in the making of financial statements within the grounds of

rationality. Thus, ensuring comparability of financial statements of differentorganizationsas

with the focus to deliver meaningful information to different users of financial statements to

allow to make informed economic decisions. As put forward by Mora and Walker (2015) The

Companies Act and several other statutes in Indian mentions that the financial statement of an

organizations should deliver a true as well as fair view of its financial stateas well as working

outcome. Theprinciple of this act also reveals that thisnecessity is implicit even in the absent

of a particular statutory provisions to this effect. According to Crawford et al., (2014),

financialreporting framework Sri Lanka indicates that Institute of CharteredAccount of Sri

Lanka made a significant decisions to converge with all pronouncements imposed by IASB.

1.2 Research Questions and Explanation

1. What are aspects based on which the differences in the accounting standards between

India and Sri Lanka can be compared?

This research question is appropriate because as the topic revolves around the differences and

similarities of accounting standards of two difference nations. This research question helps to

know all differences in accounting standards followed by India and Sri Lanka.

6RESEARCH REPORT

2. What are the similarities in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation?

There are many differences existing in the accounting standards of India and Sri

Lanka but the exact differences are not yet reviewed. So, identifying the accounting standards

of Coal India and Ceylon Steel Corporation will help to know how the similarities and norms

create impact on the organizational operation.

3. What are the differences in the accounting standards Coal India Ltd and Ceylon Steel

Corporation?

This research question is designed to identify how the differences create the barriers

and breakthrough for the organizations. The research question will help to learn how the

organizations in India and Sri Lanka are dealing with the accounting barriers.

2.0 Literature Review

This section of the report provides a comparative analysis of the accounting standards

of two nations namely India and Sri Lanka. To conduct the analysis, twenty different peer-

review journals performed on accounting standards of India and Sri Lanka. Likewise, in order

to make the analysis and critical, booth advantages and disadvantage of accounting standard

produced developed by the nation. As mentioned by Nurunnabi (2015) “Indian Accounting

Standard” is considered as the primary “Accounting Standards Board (ASB). It is identified

that ASB is observed to be a group under the “Institute of Chartered Accountants of India”

which further contains different representatives from governmental stake and academicians

from some relevant professional bodies like ICAI. Likewise, the compare the accounting

standards of both the nations in the review, this section of the research includes facts and

findings of scholarly researched papers.

2. What are the similarities in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation?

There are many differences existing in the accounting standards of India and Sri

Lanka but the exact differences are not yet reviewed. So, identifying the accounting standards

of Coal India and Ceylon Steel Corporation will help to know how the similarities and norms

create impact on the organizational operation.

3. What are the differences in the accounting standards Coal India Ltd and Ceylon Steel

Corporation?

This research question is designed to identify how the differences create the barriers

and breakthrough for the organizations. The research question will help to learn how the

organizations in India and Sri Lanka are dealing with the accounting barriers.

2.0 Literature Review

This section of the report provides a comparative analysis of the accounting standards

of two nations namely India and Sri Lanka. To conduct the analysis, twenty different peer-

review journals performed on accounting standards of India and Sri Lanka. Likewise, in order

to make the analysis and critical, booth advantages and disadvantage of accounting standard

produced developed by the nation. As mentioned by Nurunnabi (2015) “Indian Accounting

Standard” is considered as the primary “Accounting Standards Board (ASB). It is identified

that ASB is observed to be a group under the “Institute of Chartered Accountants of India”

which further contains different representatives from governmental stake and academicians

from some relevant professional bodies like ICAI. Likewise, the compare the accounting

standards of both the nations in the review, this section of the research includes facts and

findings of scholarly researched papers.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7RESEARCH REPORT

2.1 Accounting standards followed both in India and Sri Lanka

As mentioned by Vijitha and Nimalathasan (2014) a reliable and uniform financial

reporting is a significant aspect of a good corporate governance around the world. The author

has mentioned that different nations have different sets of accounting standards to operate

and control the financial reporting by their corporate sector. Nonetheless, with the advent of

globalization, the investment beyond limits as well as trading has enhanced. Therefore, the

author has suggested that the investors require a uniform globally accepted set of Accounting

Standards followed by the organizations; thereby, the comparison across the organization

internationally is facilitated. Therefore, initiative, many nations with the inclusion of India

have positively responded to such requirements. The International Accounting Standards

(IASB) is identified as an international “Accounting Standard” setter. Similarly, Sri Lanka

also follow the global accounting standards to modernize the accounting programs

(Abayadeera&Watty, 2014). In this context, Nagendrakumar, Fonseka and Dissanayake

(2015) commented that modern economic usually rely on the cross border transactions and

the free flow of International Capital. It is identified that a large percentage of all financial

transactions take place across the boarders and this number is expected to increase.

In addition, in Sri Lanka, the major governing body for the accounting standards have

been observed to be separated in the form of convergence of “Sri Lanka Accounting

Standards” as well as “International Financial Reporting Standards” (IFRSs) for generating

high quality solutions. Furthermore, it has also been identified that the fundamental feature of

“Sri Lanka AccountingStandards’” may include some accounting procedures which is

prefixed with SLFRS. As put forward by Albu, Albu and Alexander (2014), SLFRS is

referred as the major accounting standards in Sri Lanka which could correspond to IFRS as

well as LKAS. So, as both the nations are identified to prepare their financial reports

according to “International Financial Reporting Standards” the accounting procedures are

2.1 Accounting standards followed both in India and Sri Lanka

As mentioned by Vijitha and Nimalathasan (2014) a reliable and uniform financial

reporting is a significant aspect of a good corporate governance around the world. The author

has mentioned that different nations have different sets of accounting standards to operate

and control the financial reporting by their corporate sector. Nonetheless, with the advent of

globalization, the investment beyond limits as well as trading has enhanced. Therefore, the

author has suggested that the investors require a uniform globally accepted set of Accounting

Standards followed by the organizations; thereby, the comparison across the organization

internationally is facilitated. Therefore, initiative, many nations with the inclusion of India

have positively responded to such requirements. The International Accounting Standards

(IASB) is identified as an international “Accounting Standard” setter. Similarly, Sri Lanka

also follow the global accounting standards to modernize the accounting programs

(Abayadeera&Watty, 2014). In this context, Nagendrakumar, Fonseka and Dissanayake

(2015) commented that modern economic usually rely on the cross border transactions and

the free flow of International Capital. It is identified that a large percentage of all financial

transactions take place across the boarders and this number is expected to increase.

In addition, in Sri Lanka, the major governing body for the accounting standards have

been observed to be separated in the form of convergence of “Sri Lanka Accounting

Standards” as well as “International Financial Reporting Standards” (IFRSs) for generating

high quality solutions. Furthermore, it has also been identified that the fundamental feature of

“Sri Lanka AccountingStandards’” may include some accounting procedures which is

prefixed with SLFRS. As put forward by Albu, Albu and Alexander (2014), SLFRS is

referred as the major accounting standards in Sri Lanka which could correspond to IFRS as

well as LKAS. So, as both the nations are identified to prepare their financial reports

according to “International Financial Reporting Standards” the accounting procedures are

8RESEARCH REPORT

observed to be based on multiple types of he consideration which are further identified to be

considered as per the prescribed by the regulations of the board. For example, Indian

accounting standards SLFRS 3 is observed to be as the major accounting standards for the

business combination. On the basis of different sorts of similarities under this standards.

Hence, SLFRS focuses on recognizing and measuring different types of financial statements,

as per the identifiable assets needed for the liabilities considered.

2.2 Dissimilarities between the accounting standards both India and Sri Lanka

According to Vijitha and Nimalathasan (2014) the most significant difference in the

accounting procedures followed in Sri Lanka and India is observed with the “Accounting

Policies”, “Changes in Accounting Estimates” as well as “Errors”. Furthermore, it has also

been identified that the implementation of LKAS 8 corresponds to theapplication of

“accounting policies and changes pertaining to the tax effect of the correction prior to the

retrospectiveadjustment which are further considered to be applied to the changes in the

accounting policies (Abayadeera&Watty, 2014). Furthermore, it is also identified that prior

errors are observed with the “exclusion from and mis-statements” that are considered to be

available as derived and taken onto account while preparing the financial statements. Such

errors are observed to be considered with the mistake in using the accounting policies. Some

major differences are explained here with AS 24 Related Party Disclosure and “LKAS 24

Related Party Disclosure”. Some of the disclosure under AS24 Related Party Disclosure has

been mentioned with the disclosure made by the parent organization for the joint venture,

associated and subsidiaries that are known as the related parties (Vijitha&Nimalathasan,

2014). The application of such standards is observedwith the major objectives of improving

the reliability as well as relevance of entity’s financial statements.

observed to be based on multiple types of he consideration which are further identified to be

considered as per the prescribed by the regulations of the board. For example, Indian

accounting standards SLFRS 3 is observed to be as the major accounting standards for the

business combination. On the basis of different sorts of similarities under this standards.

Hence, SLFRS focuses on recognizing and measuring different types of financial statements,

as per the identifiable assets needed for the liabilities considered.

2.2 Dissimilarities between the accounting standards both India and Sri Lanka

According to Vijitha and Nimalathasan (2014) the most significant difference in the

accounting procedures followed in Sri Lanka and India is observed with the “Accounting

Policies”, “Changes in Accounting Estimates” as well as “Errors”. Furthermore, it has also

been identified that the implementation of LKAS 8 corresponds to theapplication of

“accounting policies and changes pertaining to the tax effect of the correction prior to the

retrospectiveadjustment which are further considered to be applied to the changes in the

accounting policies (Abayadeera&Watty, 2014). Furthermore, it is also identified that prior

errors are observed with the “exclusion from and mis-statements” that are considered to be

available as derived and taken onto account while preparing the financial statements. Such

errors are observed to be considered with the mistake in using the accounting policies. Some

major differences are explained here with AS 24 Related Party Disclosure and “LKAS 24

Related Party Disclosure”. Some of the disclosure under AS24 Related Party Disclosure has

been mentioned with the disclosure made by the parent organization for the joint venture,

associated and subsidiaries that are known as the related parties (Vijitha&Nimalathasan,

2014). The application of such standards is observedwith the major objectives of improving

the reliability as well as relevance of entity’s financial statements.

9RESEARCH REPORT

3.0 Research Methodology

To conduct research, the detailed analysis has been conducted by considering the

secondary data. The secondary data has been collected from the reliable secondary sources

such as books, peer reviewed journal articles, newspaper articles, blogs and annual report of

the organization. The following section and paragraph provides the detailed description of the

research methodologies used in the research.

3.1 Research philosophy

According to Mkansi and Acheampong (2012), there are three different types of

research philosophies such as positivism, interpretivism, and pragmatism. According to the

principle of positivism, the knowledge can be driven through the generation of hypothesis

and this further lead to the creation of generalisation of validated patterns of evidences with

the core belief of deduction. On the other side, in interpretivism, the knowledge can be gained

through meaning-rich context sensitive as well as subjectively constructed accounts of the

study considering the principle of induction.

Unlike positivism and interpretivism, pragmatism focuses on developing knowledge that will

have practical bearing and frame relevant action. However, in the present research,

interpretivism research philosophy will be used because in interpretivism research

philosophy, the research findings are usually judged against the criteria of meaning and

casual adequacy and transferability.

3.2 Research approach

There are two different types of research approaches namely deductive and inductive

research approaches. The major difference between this inductive and deductive research

approach functionally aims new theory and test theory while the inductive theory is

concerned with the development of new theory which emerges from the data. As put forward

3.0 Research Methodology

To conduct research, the detailed analysis has been conducted by considering the

secondary data. The secondary data has been collected from the reliable secondary sources

such as books, peer reviewed journal articles, newspaper articles, blogs and annual report of

the organization. The following section and paragraph provides the detailed description of the

research methodologies used in the research.

3.1 Research philosophy

According to Mkansi and Acheampong (2012), there are three different types of

research philosophies such as positivism, interpretivism, and pragmatism. According to the

principle of positivism, the knowledge can be driven through the generation of hypothesis

and this further lead to the creation of generalisation of validated patterns of evidences with

the core belief of deduction. On the other side, in interpretivism, the knowledge can be gained

through meaning-rich context sensitive as well as subjectively constructed accounts of the

study considering the principle of induction.

Unlike positivism and interpretivism, pragmatism focuses on developing knowledge that will

have practical bearing and frame relevant action. However, in the present research,

interpretivism research philosophy will be used because in interpretivism research

philosophy, the research findings are usually judged against the criteria of meaning and

casual adequacy and transferability.

3.2 Research approach

There are two different types of research approaches namely deductive and inductive

research approaches. The major difference between this inductive and deductive research

approach functionally aims new theory and test theory while the inductive theory is

concerned with the development of new theory which emerges from the data. As put forward

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10RESEARCH REPORT

by Maxwell (2012), a deductive research approach typically begins with the hypothesis but

the inductive research approach use the research questions to decrees the scope of the study.

However, for the current study, inductive research has been applied.

Justifying the research approaches

Even though, the study does not form new theories, the study is based on the inductive

research approach because with the help of exiting theories, the research questions have been

answered. On the basis of the theoretical underpinning with research to corporate social

responsibility and its impact on the organizational performance.

3.3 Data collection

There are two different types of data such as primary data and secondary data. The

primary data are usually a fresh and they are collected for the first time and thus, they are

original in content (Neuman 2013). Unlike primary data, the secondary data are those which

have been collected by a parties and which already been used, analysed and passed through

the statistical process. However, for the present research, the secondary data has been

collected from the reliable secondary sources such as peer reviewed journals conducted on

CSR and its impact, books on CSR management. In addition, the newspaper articles have

also been used to collect the statistical information. The annual reports of Coal India Ltd

and Ceylon Steel Corporation have been used as the real-world evidences in the analysis.

3.4 Qualitative data collection method

Qualitative data collection techniques are usually explanatory in type and they are

majorly concerned with deriving insights and understanding on the underlying factors and

motivations. Therefore, the qualitative research method has been used in the research because

it is often considered to be providing rich data regarding the existence of real life people to

by Maxwell (2012), a deductive research approach typically begins with the hypothesis but

the inductive research approach use the research questions to decrees the scope of the study.

However, for the current study, inductive research has been applied.

Justifying the research approaches

Even though, the study does not form new theories, the study is based on the inductive

research approach because with the help of exiting theories, the research questions have been

answered. On the basis of the theoretical underpinning with research to corporate social

responsibility and its impact on the organizational performance.

3.3 Data collection

There are two different types of data such as primary data and secondary data. The

primary data are usually a fresh and they are collected for the first time and thus, they are

original in content (Neuman 2013). Unlike primary data, the secondary data are those which

have been collected by a parties and which already been used, analysed and passed through

the statistical process. However, for the present research, the secondary data has been

collected from the reliable secondary sources such as peer reviewed journals conducted on

CSR and its impact, books on CSR management. In addition, the newspaper articles have

also been used to collect the statistical information. The annual reports of Coal India Ltd

and Ceylon Steel Corporation have been used as the real-world evidences in the analysis.

3.4 Qualitative data collection method

Qualitative data collection techniques are usually explanatory in type and they are

majorly concerned with deriving insights and understanding on the underlying factors and

motivations. Therefore, the qualitative research method has been used in the research because

it is often considered to be providing rich data regarding the existence of real life people to

11RESEARCH REPORT

understand the behaviour within its broader context. However, in the present study, thematic

analysis has been conducted.

3.5 Ethical consideration

Ethical consideration is another significant challenge that researcher often faces

during the making of the project. The principle of Data Collection Act 1998, the data has

been kept confidential and the identity of the respondents has not been disclosed or

mentioned anywhere in the research work. When it comes to primary secondary data

collection, there is no such major challenge that researches faces but as the secondary data

has been collected, data provided by other researchers have clearly been acknowledge to

avoid the copyright issue. To avoid any challenges from the external parties, all

organizational data have been taken from organization’s corporate websites and annual

report.

3.6 Research limitation

The present research is limited to secondary analysis only, the study lacks a primary

analysis. In addition to this, time and budget is another significant limitation that the research

faces because due to lack of time, the entire research work process have been narrowed

down. More rich content would has been collected if some more time was given to the

research. Thereby, the research lacks consistency and the scope for future research is limited.

4.0 Investigation and Research Findings

Theme 1: Comparison of Accounting Standards Followed in Sri Lanka and India

From analyzing the gathered data from Institute of Charter Accountants in India and Sri

Lankan Accounting Standards Committee it has been gathered that both the countries follow

accounting standards that has both similar and different attributes. From analyzing the Indian

understand the behaviour within its broader context. However, in the present study, thematic

analysis has been conducted.

3.5 Ethical consideration

Ethical consideration is another significant challenge that researcher often faces

during the making of the project. The principle of Data Collection Act 1998, the data has

been kept confidential and the identity of the respondents has not been disclosed or

mentioned anywhere in the research work. When it comes to primary secondary data

collection, there is no such major challenge that researches faces but as the secondary data

has been collected, data provided by other researchers have clearly been acknowledge to

avoid the copyright issue. To avoid any challenges from the external parties, all

organizational data have been taken from organization’s corporate websites and annual

report.

3.6 Research limitation

The present research is limited to secondary analysis only, the study lacks a primary

analysis. In addition to this, time and budget is another significant limitation that the research

faces because due to lack of time, the entire research work process have been narrowed

down. More rich content would has been collected if some more time was given to the

research. Thereby, the research lacks consistency and the scope for future research is limited.

4.0 Investigation and Research Findings

Theme 1: Comparison of Accounting Standards Followed in Sri Lanka and India

From analyzing the gathered data from Institute of Charter Accountants in India and Sri

Lankan Accounting Standards Committee it has been gathered that both the countries follow

accounting standards that has both similar and different attributes. From analyzing the Indian

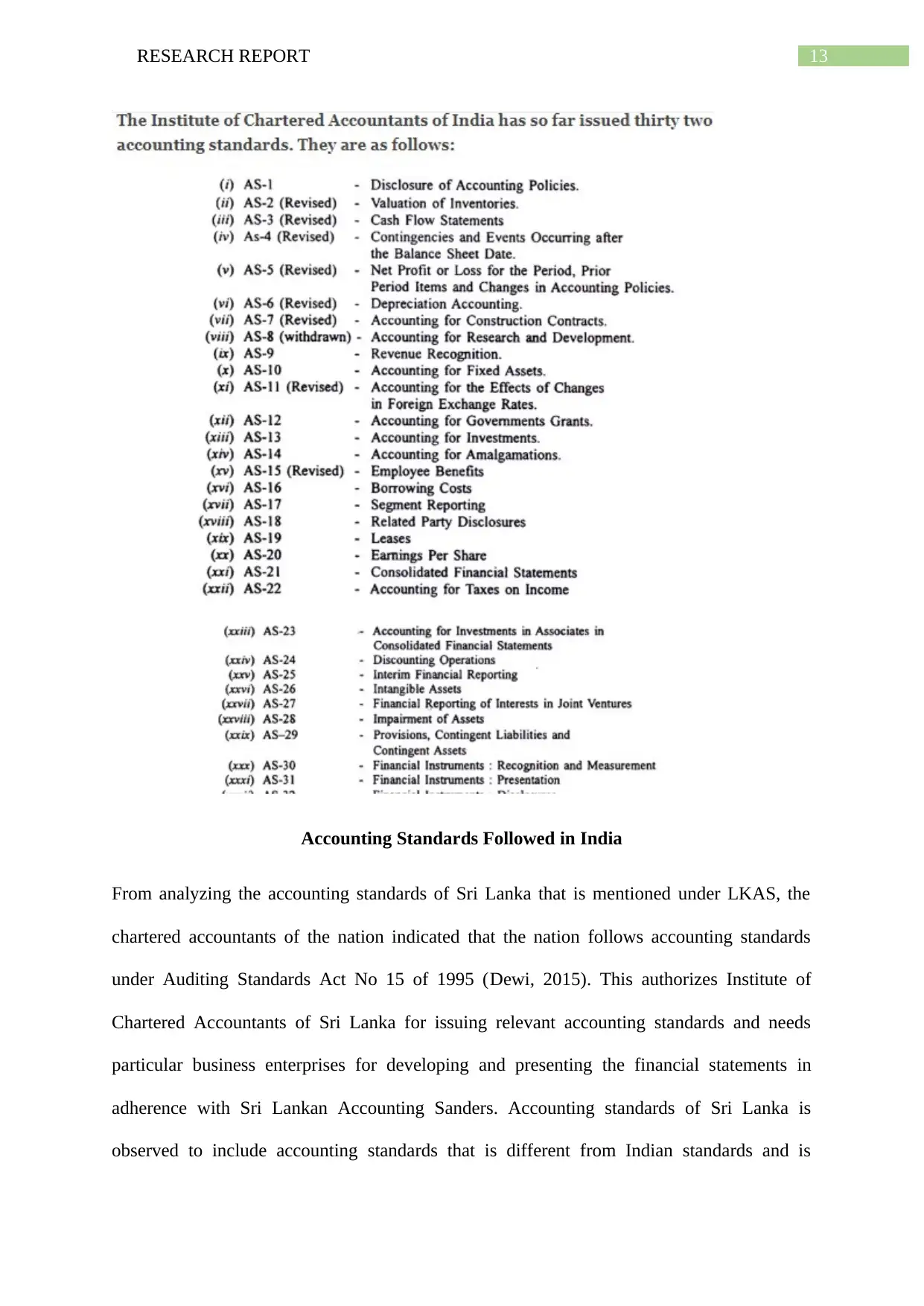

12RESEARCH REPORT

accounting standards described in the figure below it can be observed that the accounting

standards board carries out the function of following the accounting standards

(Abayadeera&Watty, 2014). The Indian accounting standards described below also takes into

consideration the applicable laws, customs, usages as well as business environment. IFRS

accounting standards are followed in India that ensures suitable representation of companies

financial statements to all the parties interested. The accounting standards board of India is

observed to include industry representatives, Central board of direct taxes and Controller and

Auditor General of India (Abayadeera&Watty, 2014). Moreover, certain accounting

standards such as IASC and ICAI consider accuracy and consistency to be the vital aspects of

financial statements. In addition, it has also been assumed that the financial statements are

drawn on accrual basis without any changes within the accounting policies. Moreover, these

Indian accounting standards also make sure that there is a necessity of liquidating or winding

up the substantial aspects of the company. The accounting standards ranging from AS-1 to

AS-22 provides vita considerations that support the selection and application of suitable

accounting policies (Das, 2015).

accounting standards described in the figure below it can be observed that the accounting

standards board carries out the function of following the accounting standards

(Abayadeera&Watty, 2014). The Indian accounting standards described below also takes into

consideration the applicable laws, customs, usages as well as business environment. IFRS

accounting standards are followed in India that ensures suitable representation of companies

financial statements to all the parties interested. The accounting standards board of India is

observed to include industry representatives, Central board of direct taxes and Controller and

Auditor General of India (Abayadeera&Watty, 2014). Moreover, certain accounting

standards such as IASC and ICAI consider accuracy and consistency to be the vital aspects of

financial statements. In addition, it has also been assumed that the financial statements are

drawn on accrual basis without any changes within the accounting policies. Moreover, these

Indian accounting standards also make sure that there is a necessity of liquidating or winding

up the substantial aspects of the company. The accounting standards ranging from AS-1 to

AS-22 provides vita considerations that support the selection and application of suitable

accounting policies (Das, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13RESEARCH REPORT

Accounting Standards Followed in India

From analyzing the accounting standards of Sri Lanka that is mentioned under LKAS, the

chartered accountants of the nation indicated that the nation follows accounting standards

under Auditing Standards Act No 15 of 1995 (Dewi, 2015). This authorizes Institute of

Chartered Accountants of Sri Lanka for issuing relevant accounting standards and needs

particular business enterprises for developing and presenting the financial statements in

adherence with Sri Lankan Accounting Sanders. Accounting standards of Sri Lanka is

observed to include accounting standards that is different from Indian standards and is

Accounting Standards Followed in India

From analyzing the accounting standards of Sri Lanka that is mentioned under LKAS, the

chartered accountants of the nation indicated that the nation follows accounting standards

under Auditing Standards Act No 15 of 1995 (Dewi, 2015). This authorizes Institute of

Chartered Accountants of Sri Lanka for issuing relevant accounting standards and needs

particular business enterprises for developing and presenting the financial statements in

adherence with Sri Lankan Accounting Sanders. Accounting standards of Sri Lanka is

observed to include accounting standards that is different from Indian standards and is

14RESEARCH REPORT

explained as SLFRS and LKAS. In addition, the nation has also implemented IFRIC and

SICS pronouncements that are issued by the IASB. Accounting standards of Sri Lanka further

considers the fact that all the companies operating within this nation must follow “Statements

of Recommended Practices”, “financial Reporting Guidelines” and “Statement of Alternate

Treatment” those are issued by the accounting institute (Dissanayake, 2017).

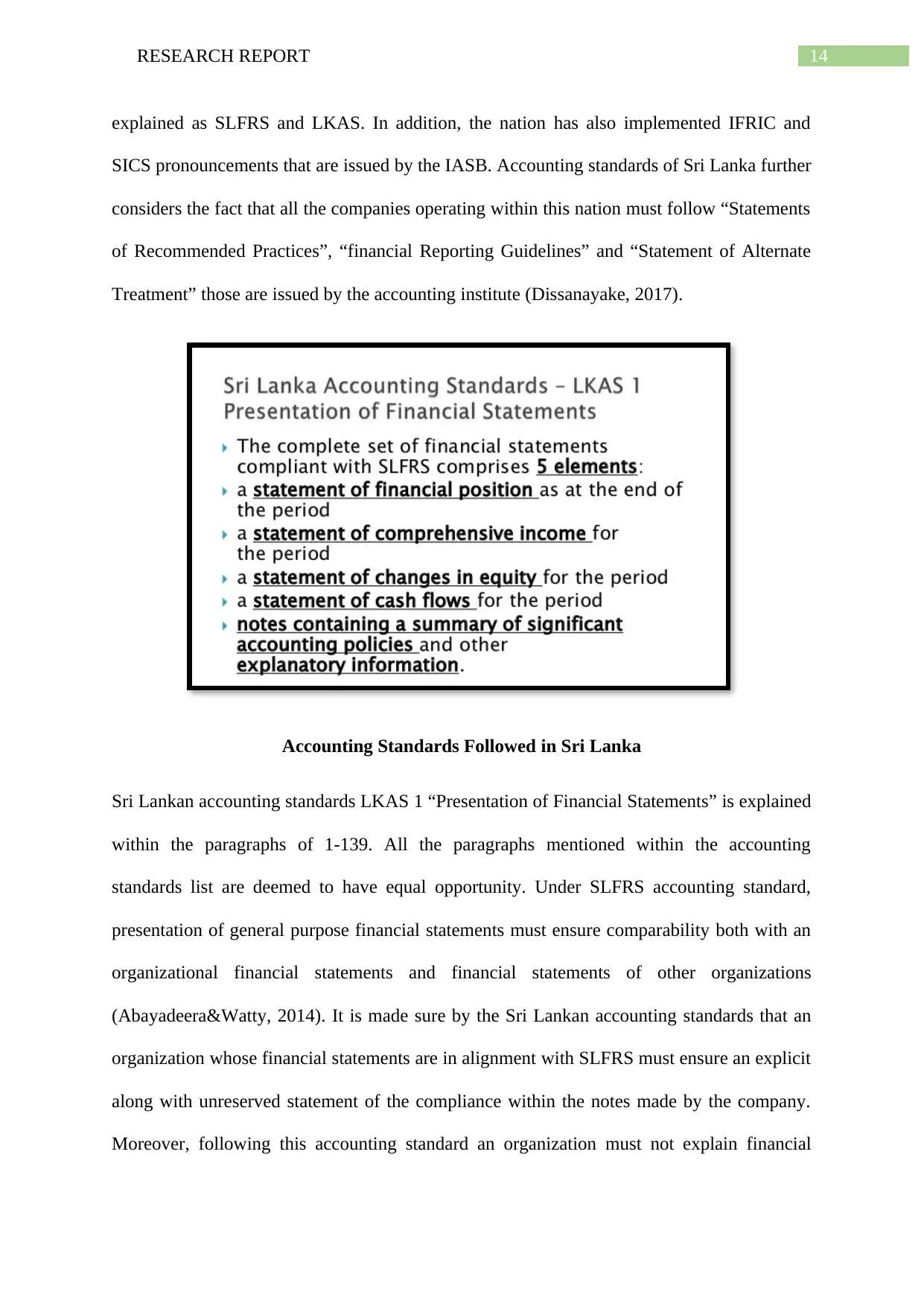

Accounting Standards Followed in Sri Lanka

Sri Lankan accounting standards LKAS 1 “Presentation of Financial Statements” is explained

within the paragraphs of 1-139. All the paragraphs mentioned within the accounting

standards list are deemed to have equal opportunity. Under SLFRS accounting standard,

presentation of general purpose financial statements must ensure comparability both with an

organizational financial statements and financial statements of other organizations

(Abayadeera&Watty, 2014). It is made sure by the Sri Lankan accounting standards that an

organization whose financial statements are in alignment with SLFRS must ensure an explicit

along with unreserved statement of the compliance within the notes made by the company.

Moreover, following this accounting standard an organization must not explain financial

explained as SLFRS and LKAS. In addition, the nation has also implemented IFRIC and

SICS pronouncements that are issued by the IASB. Accounting standards of Sri Lanka further

considers the fact that all the companies operating within this nation must follow “Statements

of Recommended Practices”, “financial Reporting Guidelines” and “Statement of Alternate

Treatment” those are issued by the accounting institute (Dissanayake, 2017).

Accounting Standards Followed in Sri Lanka

Sri Lankan accounting standards LKAS 1 “Presentation of Financial Statements” is explained

within the paragraphs of 1-139. All the paragraphs mentioned within the accounting

standards list are deemed to have equal opportunity. Under SLFRS accounting standard,

presentation of general purpose financial statements must ensure comparability both with an

organizational financial statements and financial statements of other organizations

(Abayadeera&Watty, 2014). It is made sure by the Sri Lankan accounting standards that an

organization whose financial statements are in alignment with SLFRS must ensure an explicit

along with unreserved statement of the compliance within the notes made by the company.

Moreover, following this accounting standard an organization must not explain financial

15RESEARCH REPORT

statements as complying with SLFRS standards unless they are aligned with all the

requirements of the accounting standards. Opposing to the Indian accounting standards, the

SLFRS ensures that an organization cannot rectify the accounting policies either through

disclosure of the accounting policies or by means of exploratory materials or notes

(Abayadeera&Watty, 2014). On the other hand, IFRS followed by India ensures that an

organization must follow accounting disclosure policies mentioned under AS-1. This

facilitates in dealing with disclosure of considerable accounting policies followed by Indian

organizations in development of their financial statements.

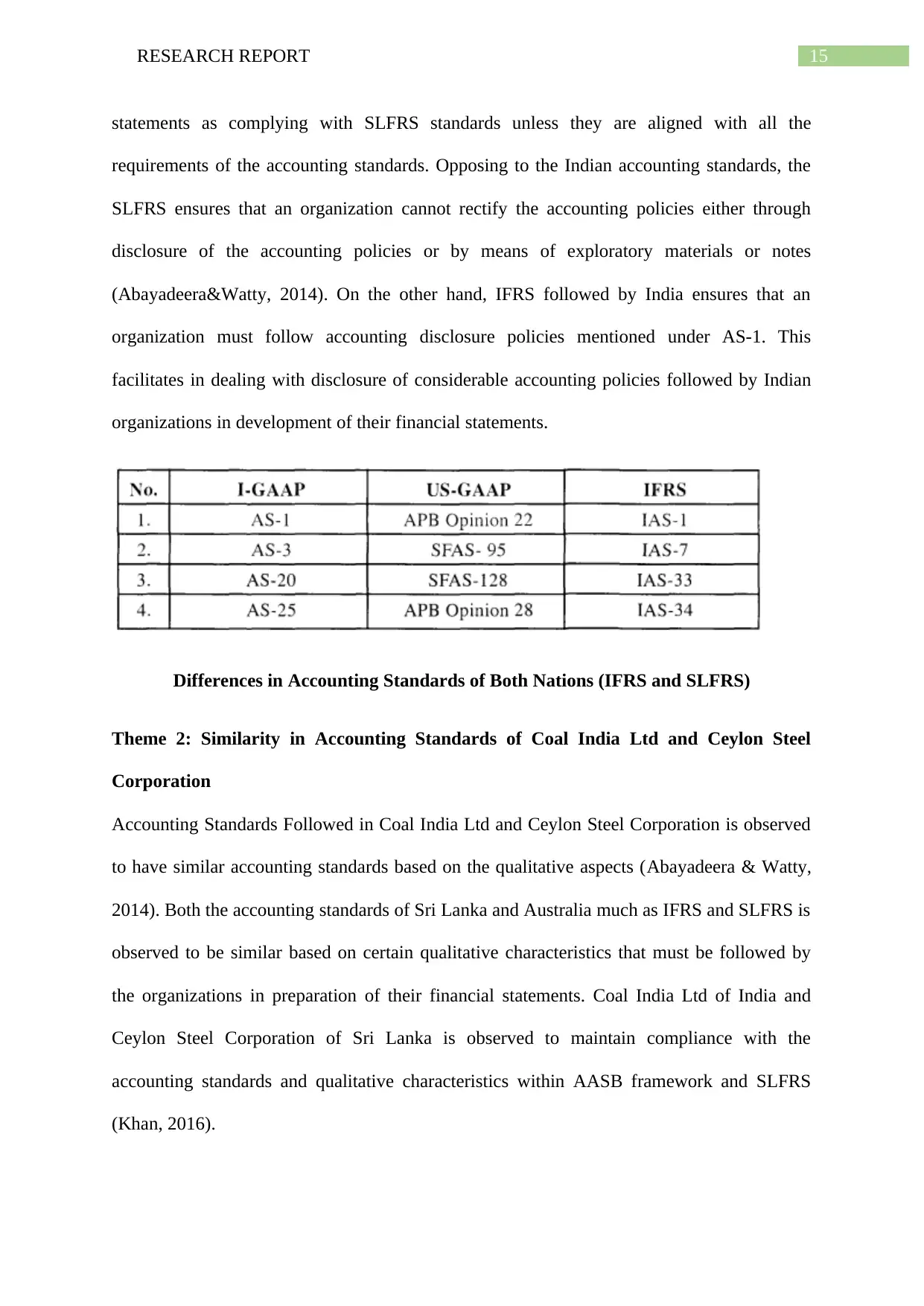

Differences in Accounting Standards of Both Nations (IFRS and SLFRS)

Theme 2: Similarity in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation

Accounting Standards Followed in Coal India Ltd and Ceylon Steel Corporation is observed

to have similar accounting standards based on the qualitative aspects (Abayadeera & Watty,

2014). Both the accounting standards of Sri Lanka and Australia much as IFRS and SLFRS is

observed to be similar based on certain qualitative characteristics that must be followed by

the organizations in preparation of their financial statements. Coal India Ltd of India and

Ceylon Steel Corporation of Sri Lanka is observed to maintain compliance with the

accounting standards and qualitative characteristics within AASB framework and SLFRS

(Khan, 2016).

statements as complying with SLFRS standards unless they are aligned with all the

requirements of the accounting standards. Opposing to the Indian accounting standards, the

SLFRS ensures that an organization cannot rectify the accounting policies either through

disclosure of the accounting policies or by means of exploratory materials or notes

(Abayadeera&Watty, 2014). On the other hand, IFRS followed by India ensures that an

organization must follow accounting disclosure policies mentioned under AS-1. This

facilitates in dealing with disclosure of considerable accounting policies followed by Indian

organizations in development of their financial statements.

Differences in Accounting Standards of Both Nations (IFRS and SLFRS)

Theme 2: Similarity in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation

Accounting Standards Followed in Coal India Ltd and Ceylon Steel Corporation is observed

to have similar accounting standards based on the qualitative aspects (Abayadeera & Watty,

2014). Both the accounting standards of Sri Lanka and Australia much as IFRS and SLFRS is

observed to be similar based on certain qualitative characteristics that must be followed by

the organizations in preparation of their financial statements. Coal India Ltd of India and

Ceylon Steel Corporation of Sri Lanka is observed to maintain compliance with the

accounting standards and qualitative characteristics within AASB framework and SLFRS

(Khan, 2016).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16RESEARCH REPORT

Faithful Representation- Coal India Ltd of India and Ceylon Steel Corporation of

Sri Lanka are observed to prepare transparent and fair financial statements

representation within the annual report prepared by these companies. For making sure

that faithful representation of financial statements, both these companies ensure that

shareholder confidence has a significant role focused on the perception of the

organization (Abayadeera&Watty, 2014). Audit report prepared by KMPG for these

companies also takes into account the faithful representation of financial report is

maintained by Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka.

This is for the reason that these companies follow important accounting standards

faithfully and considerably (Doliya& Singh, 2016).

Relevance- Based on such accounting standards set by SLFRS and AASB, it can be

observed that Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka

provide relevant information in supporting the better decision making process of the

organization. Considering the case of these companies, it is gathered that they follow

the relevancy standards set by AASB, IFRS and SLFRS. These companies also take

into consideration the current depreciation rates and tax along with other aspects. This

is the reason for which the financial decisions taken by Coal India Ltd of India and

Ceylon Steel Corporation of Sri Lanka are deemed to maintain valuable aspect that is

also reflected in their financial statements (Kamath, 2017).

Verifiability- Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka is

observed to maintain the qualitative aspect of verifiability within their financial

statements in consideration to the accounting standards followed within their

respective countries such as IFRS, AASB and SLFRS. Complying by these standards,

the companies are observed to maintain their financial data in a manner that the

investors remain able to verify the same in an effective manner (Abayadeera&Watty,

Faithful Representation- Coal India Ltd of India and Ceylon Steel Corporation of

Sri Lanka are observed to prepare transparent and fair financial statements

representation within the annual report prepared by these companies. For making sure

that faithful representation of financial statements, both these companies ensure that

shareholder confidence has a significant role focused on the perception of the

organization (Abayadeera&Watty, 2014). Audit report prepared by KMPG for these

companies also takes into account the faithful representation of financial report is

maintained by Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka.

This is for the reason that these companies follow important accounting standards

faithfully and considerably (Doliya& Singh, 2016).

Relevance- Based on such accounting standards set by SLFRS and AASB, it can be

observed that Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka

provide relevant information in supporting the better decision making process of the

organization. Considering the case of these companies, it is gathered that they follow

the relevancy standards set by AASB, IFRS and SLFRS. These companies also take

into consideration the current depreciation rates and tax along with other aspects. This

is the reason for which the financial decisions taken by Coal India Ltd of India and

Ceylon Steel Corporation of Sri Lanka are deemed to maintain valuable aspect that is

also reflected in their financial statements (Kamath, 2017).

Verifiability- Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka is

observed to maintain the qualitative aspect of verifiability within their financial

statements in consideration to the accounting standards followed within their

respective countries such as IFRS, AASB and SLFRS. Complying by these standards,

the companies are observed to maintain their financial data in a manner that the

investors remain able to verify the same in an effective manner (Abayadeera&Watty,

17RESEARCH REPORT

2014). In order to make sure that financial statements verifiability is maintained Coal

India Ltd of India and Ceylon Steel Corporation of Sri Lanka considers preparing a

section where notes will be explained in the organization’s annual report along with

all their financial statements.

Comparability- Based on the accounting standards followed in India and Sri Lanka

such as IFRS, AASB and SLFRS, it is mentioned that these companies provides

increased opportunities to all its stakeholders that can facilitate them in understanding

the differences as well as similarities and deviations in the financial information

explained within their financial reports (Ratnatunga&Tse, 2017). Certain vital

information is provided to the users by Coal India Ltd of India and Ceylon Steel

Corporation of Sri Lanka Coal India Ltd of India and Ceylon Steel Corporation of Sri

Lanka through charts as well as tables. This enhances understanding of the financial

statements represented by companies which can further facilitate them in better

decision making. Financial position of Coal India Ltd of India and Ceylon Steel

Corporation of Sri Lanka can also be compared with its competitors within the market

that facilitates representing real financial position of these organizations

(Abayadeera&Watty, 2014).

Understandability- AASB, IFRS and SLFRS ensures that the Coal India Ltd of India

and Ceylon Steel Corporation of Sri Lanka complies with understandability

qualitative aspects of these standards in order to prepare financial information in a

manner that makes it simple for the investors to understand financial statements in an

effective manner. Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka

reports their financial statements in a format that is aligned with financial reporting

conceptual framework mentioned under AASB, IASB and SLFRS accounting

2014). In order to make sure that financial statements verifiability is maintained Coal

India Ltd of India and Ceylon Steel Corporation of Sri Lanka considers preparing a

section where notes will be explained in the organization’s annual report along with

all their financial statements.

Comparability- Based on the accounting standards followed in India and Sri Lanka

such as IFRS, AASB and SLFRS, it is mentioned that these companies provides

increased opportunities to all its stakeholders that can facilitate them in understanding

the differences as well as similarities and deviations in the financial information

explained within their financial reports (Ratnatunga&Tse, 2017). Certain vital

information is provided to the users by Coal India Ltd of India and Ceylon Steel

Corporation of Sri Lanka Coal India Ltd of India and Ceylon Steel Corporation of Sri

Lanka through charts as well as tables. This enhances understanding of the financial

statements represented by companies which can further facilitate them in better

decision making. Financial position of Coal India Ltd of India and Ceylon Steel

Corporation of Sri Lanka can also be compared with its competitors within the market

that facilitates representing real financial position of these organizations

(Abayadeera&Watty, 2014).

Understandability- AASB, IFRS and SLFRS ensures that the Coal India Ltd of India

and Ceylon Steel Corporation of Sri Lanka complies with understandability

qualitative aspects of these standards in order to prepare financial information in a

manner that makes it simple for the investors to understand financial statements in an

effective manner. Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka

reports their financial statements in a format that is aligned with financial reporting

conceptual framework mentioned under AASB, IASB and SLFRS accounting

18RESEARCH REPORT

conceptual framework which supports its investors in understanding them in an

efficient way (Abayadeera&Watty, 2014).

Timeliness- Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka

follows the accounting standards of AASB, IASB and SLFRS in making their

financial statements highly reliable and of better quality based on which investors can

take better decision making regarding their further investment within these

organizations. Quarterly along with the annual reports of Coal India Ltd of India and

Ceylon Steel Corporation of Sri Lanka are prepared in a manner so that it offers to its

investors a proper view regarding the situation of the companies (Saggar& Singh,

2017). Considering the same, accounting standards followed by both of these

companies belonging to different companies are similar. This is because they comply

by the accounting standards of timely information disclosure that can facilitate them

in obtaining a fair perception concerning the performance and position of companies

in the market.

Theme 3: Differences in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation

Based on several amendments made in the accounting standards followed in India and Sri

Lanka it has been gathered that there are certain differences within the accounting standards

followed by Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka. It has been

evidenced that Ceylon Steel Corporation of Sri Lanka puts an increased focus on the balance

sheet in comparison to historical focus on profit and loss account. These new standards are

prefixed to be SLFRS in accordance with LKAS and corresponding to IAS (Bhatt & Olive,

2016).

On the other hand, Coal India Ltd of India follows IFRS and AASB that has certain different

accounting standards complaisance in comparison to the Sri Lankan ones. For instance, Coal

conceptual framework which supports its investors in understanding them in an

efficient way (Abayadeera&Watty, 2014).

Timeliness- Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka

follows the accounting standards of AASB, IASB and SLFRS in making their

financial statements highly reliable and of better quality based on which investors can

take better decision making regarding their further investment within these

organizations. Quarterly along with the annual reports of Coal India Ltd of India and

Ceylon Steel Corporation of Sri Lanka are prepared in a manner so that it offers to its

investors a proper view regarding the situation of the companies (Saggar& Singh,

2017). Considering the same, accounting standards followed by both of these

companies belonging to different companies are similar. This is because they comply

by the accounting standards of timely information disclosure that can facilitate them

in obtaining a fair perception concerning the performance and position of companies

in the market.

Theme 3: Differences in Accounting Standards of Coal India Ltd and Ceylon Steel

Corporation

Based on several amendments made in the accounting standards followed in India and Sri

Lanka it has been gathered that there are certain differences within the accounting standards

followed by Coal India Ltd of India and Ceylon Steel Corporation of Sri Lanka. It has been

evidenced that Ceylon Steel Corporation of Sri Lanka puts an increased focus on the balance

sheet in comparison to historical focus on profit and loss account. These new standards are

prefixed to be SLFRS in accordance with LKAS and corresponding to IAS (Bhatt & Olive,

2016).

On the other hand, Coal India Ltd of India follows IFRS and AASB that has certain different

accounting standards complaisance in comparison to the Sri Lankan ones. For instance, Coal

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

19RESEARCH REPORT

India Ltd of India follows “AS 22- Accounting for Taxes on Income”, based on which the

debt and securities of this company is deemed to be listed within recognized stock exchange

of India. Considering the same accounting standard, Coal India Ltd of India considers that

takes on income is acquired within a definite financial period as the expenses and revenue are

related and the company also considers that taxable income might significantly be different

from accounting income (Kraal, Yapa& Joshi, 2015).

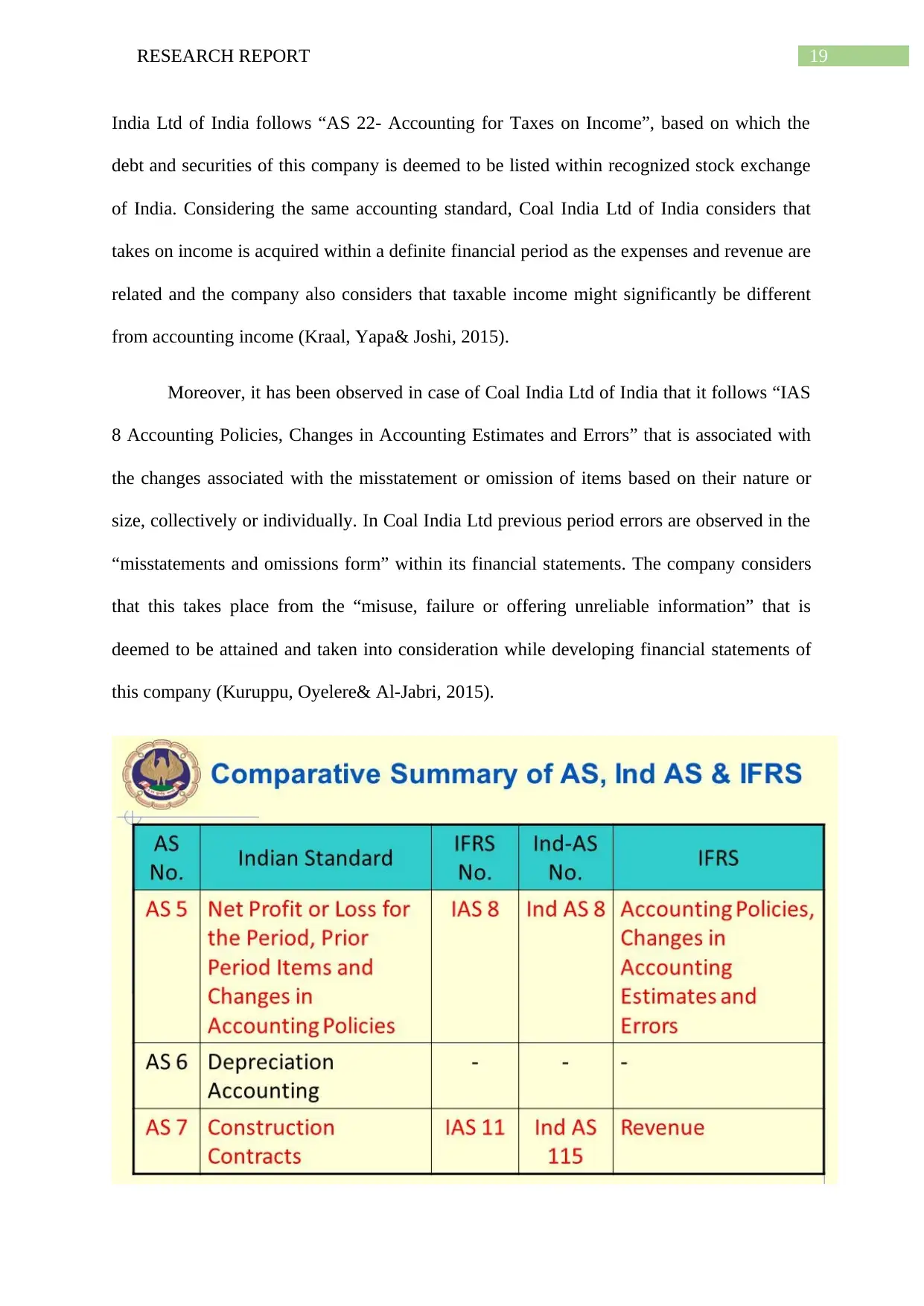

Moreover, it has been observed in case of Coal India Ltd of India that it follows “IAS

8 Accounting Policies, Changes in Accounting Estimates and Errors” that is associated with

the changes associated with the misstatement or omission of items based on their nature or

size, collectively or individually. In Coal India Ltd previous period errors are observed in the

“misstatements and omissions form” within its financial statements. The company considers

that this takes place from the “misuse, failure or offering unreliable information” that is

deemed to be attained and taken into consideration while developing financial statements of

this company (Kuruppu, Oyelere& Al-Jabri, 2015).

India Ltd of India follows “AS 22- Accounting for Taxes on Income”, based on which the

debt and securities of this company is deemed to be listed within recognized stock exchange

of India. Considering the same accounting standard, Coal India Ltd of India considers that

takes on income is acquired within a definite financial period as the expenses and revenue are

related and the company also considers that taxable income might significantly be different

from accounting income (Kraal, Yapa& Joshi, 2015).

Moreover, it has been observed in case of Coal India Ltd of India that it follows “IAS

8 Accounting Policies, Changes in Accounting Estimates and Errors” that is associated with

the changes associated with the misstatement or omission of items based on their nature or

size, collectively or individually. In Coal India Ltd previous period errors are observed in the

“misstatements and omissions form” within its financial statements. The company considers

that this takes place from the “misuse, failure or offering unreliable information” that is

deemed to be attained and taken into consideration while developing financial statements of

this company (Kuruppu, Oyelere& Al-Jabri, 2015).

20RESEARCH REPORT

In contrast, Ceylon Steel Corporation of Sri Lanka is observed to follow “LKAS 8 -

Accounting Policies, Changes in Accounting Estimates and Errors” that is different from the

Indian accounting standards. The implementation of LKAS 8 in the company corresponds to

the implementation of the accounting policies. Moreover, Ceylon Steel Corporation considers

conducting changes focused on tax impacts of the corrections before the retrospective

adjustments (Perera& Chand, 2015). This is observed to be applied within the accounting

policy changes that are observed to be accounted based on the disclosers prepared in

compliance with LKAS 12 Income Taxes.

Certain differences in the implementation of accounting standards by Ceylon Steel

Corporation and Coal India Ltd are observed through measuring differences in its standards.

Coal India Ltd follows “Ind AS 24 Related Party Disclosures” and Ceylon Steel Corporation

follows “LKAS 24-Related Party Disclosures”. Different disclosures that are made by Coal

India Ltd based on “Ind AS 24 Related Party Disclosures” that considers disclosure can be

made by the organization for joint venture, subsidiaries and associated referred as related

parties (Ratnatunga, Balachandran&Tse, 2017). Differing the same, Ceylon Steel Corporation

follows “LKAS 24-Related Party Disclosures” that ensures prescribed criteria for choosing

In contrast, Ceylon Steel Corporation of Sri Lanka is observed to follow “LKAS 8 -

Accounting Policies, Changes in Accounting Estimates and Errors” that is different from the

Indian accounting standards. The implementation of LKAS 8 in the company corresponds to

the implementation of the accounting policies. Moreover, Ceylon Steel Corporation considers

conducting changes focused on tax impacts of the corrections before the retrospective

adjustments (Perera& Chand, 2015). This is observed to be applied within the accounting

policy changes that are observed to be accounted based on the disclosers prepared in

compliance with LKAS 12 Income Taxes.

Certain differences in the implementation of accounting standards by Ceylon Steel

Corporation and Coal India Ltd are observed through measuring differences in its standards.

Coal India Ltd follows “Ind AS 24 Related Party Disclosures” and Ceylon Steel Corporation

follows “LKAS 24-Related Party Disclosures”. Different disclosures that are made by Coal

India Ltd based on “Ind AS 24 Related Party Disclosures” that considers disclosure can be

made by the organization for joint venture, subsidiaries and associated referred as related

parties (Ratnatunga, Balachandran&Tse, 2017). Differing the same, Ceylon Steel Corporation

follows “LKAS 24-Related Party Disclosures” that ensures prescribed criteria for choosing

21RESEARCH REPORT

and changing accounting policies along with ensuring changes within accounting

anticipations focused on error corrections.

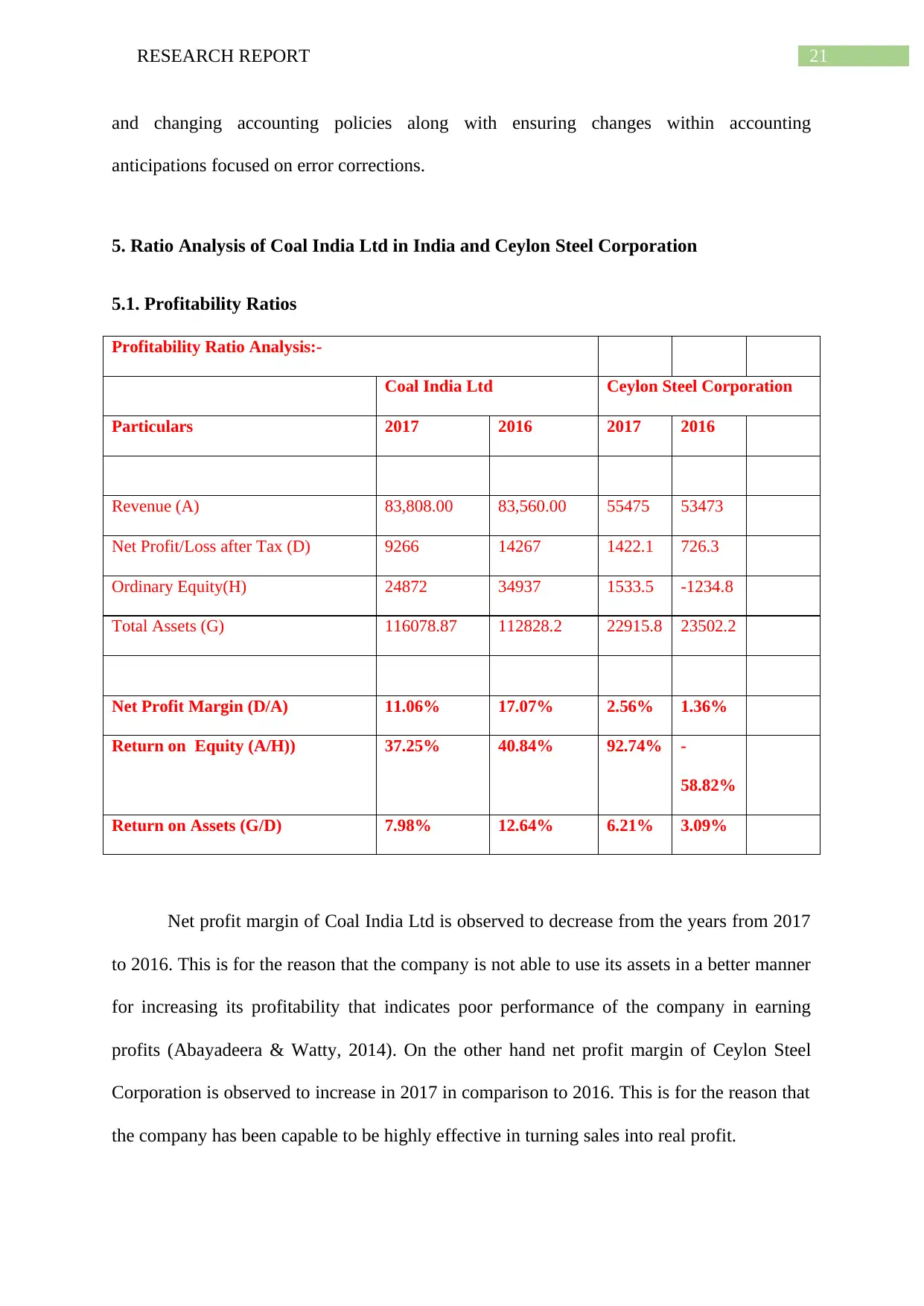

5. Ratio Analysis of Coal India Ltd in India and Ceylon Steel Corporation

5.1. Profitability Ratios

Profitability Ratio Analysis:-

Coal India Ltd Ceylon Steel Corporation

Particulars 2017 2016 2017 2016

Revenue (A) 83,808.00 83,560.00 55475 53473

Net Profit/Loss after Tax (D) 9266 14267 1422.1 726.3

Ordinary Equity(H) 24872 34937 1533.5 -1234.8

Total Assets (G) 116078.87 112828.2 22915.8 23502.2

Net Profit Margin (D/A) 11.06% 17.07% 2.56% 1.36%

Return on Equity (A/H)) 37.25% 40.84% 92.74% -

58.82%

Return on Assets (G/D) 7.98% 12.64% 6.21% 3.09%

Net profit margin of Coal India Ltd is observed to decrease from the years from 2017

to 2016. This is for the reason that the company is not able to use its assets in a better manner

for increasing its profitability that indicates poor performance of the company in earning

profits (Abayadeera & Watty, 2014). On the other hand net profit margin of Ceylon Steel

Corporation is observed to increase in 2017 in comparison to 2016. This is for the reason that

the company has been capable to be highly effective in turning sales into real profit.

and changing accounting policies along with ensuring changes within accounting

anticipations focused on error corrections.

5. Ratio Analysis of Coal India Ltd in India and Ceylon Steel Corporation

5.1. Profitability Ratios

Profitability Ratio Analysis:-

Coal India Ltd Ceylon Steel Corporation

Particulars 2017 2016 2017 2016

Revenue (A) 83,808.00 83,560.00 55475 53473

Net Profit/Loss after Tax (D) 9266 14267 1422.1 726.3

Ordinary Equity(H) 24872 34937 1533.5 -1234.8

Total Assets (G) 116078.87 112828.2 22915.8 23502.2

Net Profit Margin (D/A) 11.06% 17.07% 2.56% 1.36%

Return on Equity (A/H)) 37.25% 40.84% 92.74% -

58.82%

Return on Assets (G/D) 7.98% 12.64% 6.21% 3.09%

Net profit margin of Coal India Ltd is observed to decrease from the years from 2017

to 2016. This is for the reason that the company is not able to use its assets in a better manner

for increasing its profitability that indicates poor performance of the company in earning

profits (Abayadeera & Watty, 2014). On the other hand net profit margin of Ceylon Steel

Corporation is observed to increase in 2017 in comparison to 2016. This is for the reason that

the company has been capable to be highly effective in turning sales into real profit.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

22RESEARCH REPORT

Return on assets of Coal India Ltd is observed to decrease from the years from 2017

to 2016. This is for the reason that it is not being able to attain enough profit in comparison to

its overall resources. On the other hand return on assets of Ceylon Steel Corporation is

observed to increase in 2017 in comparison to 2016. This is for the reason that it is highly

capable to increase its profit margin through employing its assets and increasing sales (Bhatt

& Olive, 2016).

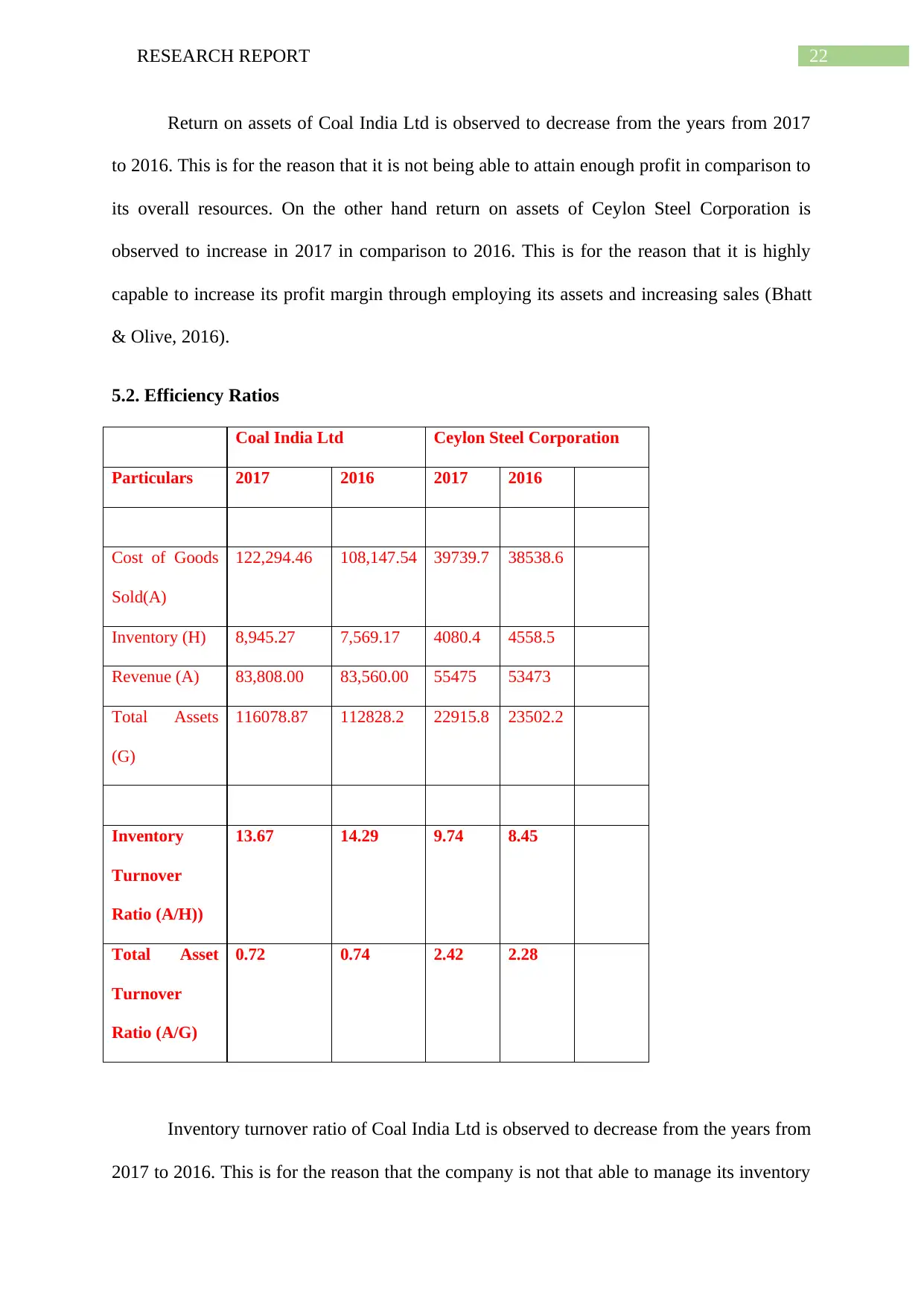

5.2. Efficiency Ratios

Coal India Ltd Ceylon Steel Corporation

Particulars 2017 2016 2017 2016

Cost of Goods

Sold(A)

122,294.46 108,147.54 39739.7 38538.6

Inventory (H) 8,945.27 7,569.17 4080.4 4558.5

Revenue (A) 83,808.00 83,560.00 55475 53473

Total Assets

(G)

116078.87 112828.2 22915.8 23502.2

Inventory

Turnover

Ratio (A/H))

13.67 14.29 9.74 8.45

Total Asset

Turnover

Ratio (A/G)

0.72 0.74 2.42 2.28

Inventory turnover ratio of Coal India Ltd is observed to decrease from the years from

2017 to 2016. This is for the reason that the company is not that able to manage its inventory

Return on assets of Coal India Ltd is observed to decrease from the years from 2017

to 2016. This is for the reason that it is not being able to attain enough profit in comparison to

its overall resources. On the other hand return on assets of Ceylon Steel Corporation is

observed to increase in 2017 in comparison to 2016. This is for the reason that it is highly

capable to increase its profit margin through employing its assets and increasing sales (Bhatt

& Olive, 2016).

5.2. Efficiency Ratios

Coal India Ltd Ceylon Steel Corporation

Particulars 2017 2016 2017 2016

Cost of Goods

Sold(A)

122,294.46 108,147.54 39739.7 38538.6

Inventory (H) 8,945.27 7,569.17 4080.4 4558.5

Revenue (A) 83,808.00 83,560.00 55475 53473

Total Assets

(G)

116078.87 112828.2 22915.8 23502.2

Inventory

Turnover

Ratio (A/H))

13.67 14.29 9.74 8.45

Total Asset

Turnover

Ratio (A/G)

0.72 0.74 2.42 2.28

Inventory turnover ratio of Coal India Ltd is observed to decrease from the years from

2017 to 2016. This is for the reason that the company is not that able to manage its inventory

23RESEARCH REPORT

through considering the cost of goods sold (Abayadeera & Watty, 2014). On the other hand

inventory turnover ratio of Ceylon Steel Corporation is observed to increase in 2017 in

comparison to 2016. This is for the reason that the company is efficient in selling its

inventory through increase sales or by offering huge discounts.

Total asset turnover of Coal India Ltd is observed to decrease from the years from

2017 to 2016. On the other hand total assets turnover of Ceylon Steel Corporation is observed

to increase in 2017 in comparison to 2016. This is for the reason that both the companies

indicate increased sales and less accumulation of inventory (Bhatt & Olive, 2016). This also

serves as an effective measure of business performance as this signifies that these companies

are making high profit on each sale.

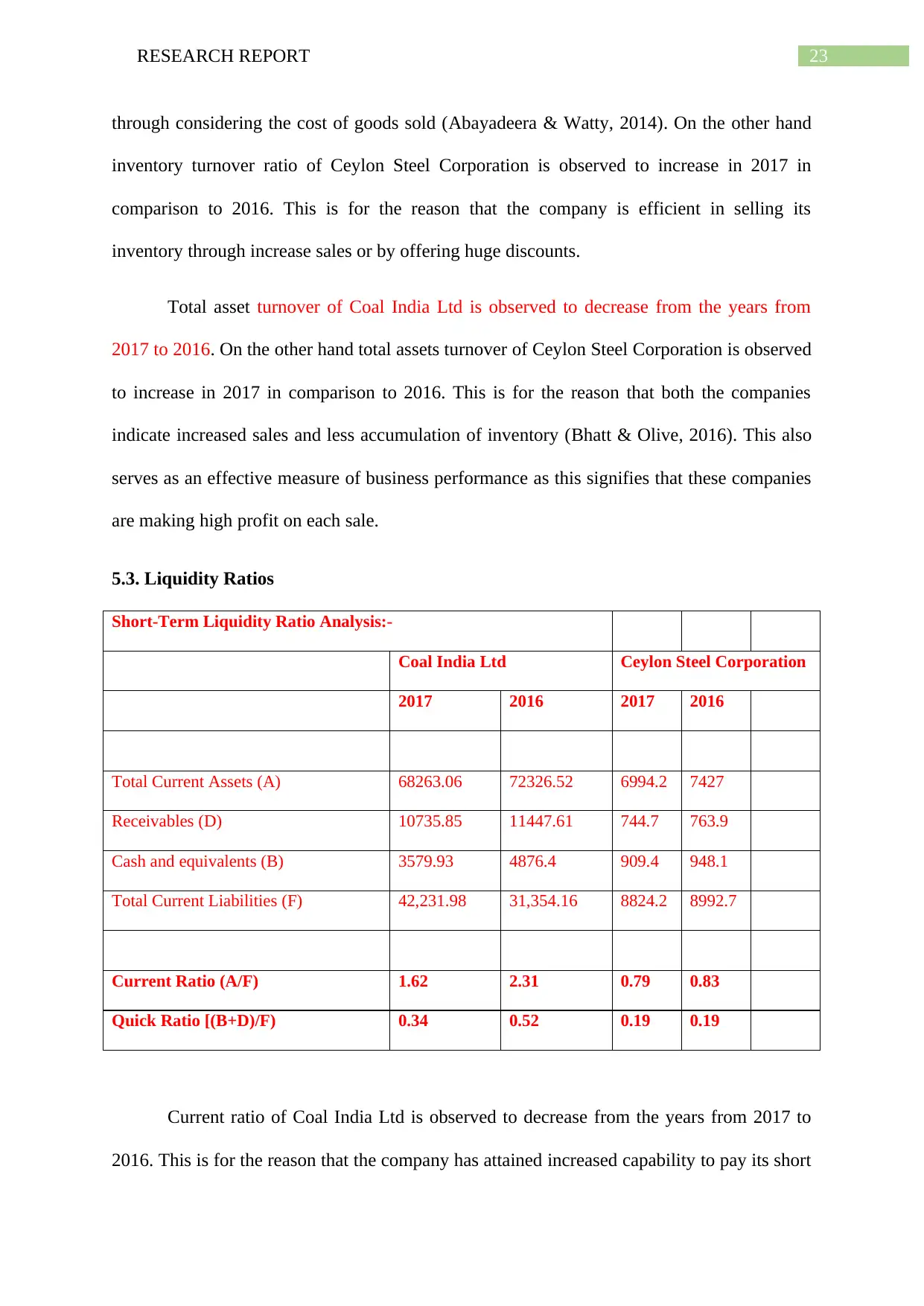

5.3. Liquidity Ratios

Short-Term Liquidity Ratio Analysis:-

Coal India Ltd Ceylon Steel Corporation

2017 2016 2017 2016

Total Current Assets (A) 68263.06 72326.52 6994.2 7427

Receivables (D) 10735.85 11447.61 744.7 763.9

Cash and equivalents (B) 3579.93 4876.4 909.4 948.1

Total Current Liabilities (F) 42,231.98 31,354.16 8824.2 8992.7

Current Ratio (A/F) 1.62 2.31 0.79 0.83

Quick Ratio [(B+D)/F) 0.34 0.52 0.19 0.19

Current ratio of Coal India Ltd is observed to decrease from the years from 2017 to

2016. This is for the reason that the company has attained increased capability to pay its short

through considering the cost of goods sold (Abayadeera & Watty, 2014). On the other hand

inventory turnover ratio of Ceylon Steel Corporation is observed to increase in 2017 in

comparison to 2016. This is for the reason that the company is efficient in selling its

inventory through increase sales or by offering huge discounts.