Financial Accounting Report: Analyzing AASB 110, Deferred Tax Assets

VerifiedAdded on 2023/06/10

|11

|2563

|62

Report

AI Summary

This financial accounting report addresses several key areas including the application of AASB 110 regarding events occurring after the reporting period, covering both adjusting and non-adjusting events with specific examples and required disclosures. It delves into the treatment of depreciation, development costs, annual leave entitlements, impairment of goodwill, and advance rent received, providing journal entries and schedules of temporary differences to calculate deferred tax assets and liabilities. Furthermore, the report examines lease accounting, classifying a lease as a capital lease based on specific criteria and presenting the relevant journal entries for recording the lease and associated expenses. The analysis incorporates Australian accounting standards and taxation office guidelines, offering a comprehensive overview of the financial implications and accounting treatments for each scenario.

Assessment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART A...........................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................4

4...................................................................................................................................................5

5...................................................................................................................................................5

Part B...............................................................................................................................................6

6. Provision of Journal entries, preparation of Schedule of temporary differences and

calculation of Deferred tax assets and Deferred tax liabilities....................................................6

7. Lease accounting.....................................................................................................................9

REFERENCES..............................................................................................................................11

Books and Journals....................................................................................................................11

PART A...........................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................4

4...................................................................................................................................................5

5...................................................................................................................................................5

Part B...............................................................................................................................................6

6. Provision of Journal entries, preparation of Schedule of temporary differences and

calculation of Deferred tax assets and Deferred tax liabilities....................................................6

7. Lease accounting.....................................................................................................................9

REFERENCES..............................................................................................................................11

Books and Journals....................................................................................................................11

PART A

1.

As per Australian Standard AASB 110, the events whether favourable or unfavourable that

occur between the end of the reporting period and the date when financial statement are

authorized. The transaction of fire on 7th July is occurred between the annual report date and

issue date. Hence, on this basis this are events occurring after the balance sheet date. The nature

of this event is non-adjusting event after the reporting period because there is no indicative of

conditions that arose after the balance sheet date. The applicable accounting standard this event

relates is AASB 102 Inventories. This standard prescribes the accounting treatment of

inventories such as closing stock is recorded at cost or NPV whichever is lower (Czerney, and

et.al., 2020). Yes, there is a requirement to disclose the stock loss or financial loss of $2 million

on the notes to accounts. It is because first this is a non-adjusting event and the loss of stock is

40% of total value of stock.

1.

As per Australian Standard AASB 110, the events whether favourable or unfavourable that

occur between the end of the reporting period and the date when financial statement are

authorized. The transaction of fire on 7th July is occurred between the annual report date and

issue date. Hence, on this basis this are events occurring after the balance sheet date. The nature

of this event is non-adjusting event after the reporting period because there is no indicative of

conditions that arose after the balance sheet date. The applicable accounting standard this event

relates is AASB 102 Inventories. This standard prescribes the accounting treatment of

inventories such as closing stock is recorded at cost or NPV whichever is lower (Czerney, and

et.al., 2020). Yes, there is a requirement to disclose the stock loss or financial loss of $2 million

on the notes to accounts. It is because first this is a non-adjusting event and the loss of stock is

40% of total value of stock.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.

As per AASB 110, the particular transaction of bad debt recovering is considered as

adjusting transaction or events after the reporting period. It is because this transaction provides

the evidence of condition that existed at the reporting period in the form of provision made

against bad debts. The applicable accounting standard relates to the present transaction is AASB

137 provision, contingent liabilities and contingent assets. This standard indicates that the

possible assets that arises from the past events and whose existence is in the balance sheet are

recorded or recognised in the financial statement at the time when the income occurrence. This

transaction will not disclose in the books of account because it is an adjusting transaction.

However, the particular transaction need to be adjusted in the financial statement of the end

reporting period (Dobson, 2020). The adjustment of this transaction is as follows:

Debtor a/c $550000

To Bad debt recovered a/c $550000

Bad debt recovered a/c $550000

To P&L a/c $550000

On this basis, the adjustment in the financial statement of MQE ltd is that their debtors i.e.,

accounts receivable value will be increased by $550000 that result into the total value of trade

receivable after adjustment is 4.037 million. Further, the income of the company will increase by

0.55 million due to this transaction adjustment. This should be done by the company as it affects

the decision-making of the financial statement of business.

3.

As per AASB 110, the nature of transaction of job seeker payment received from

government is adjusting event occurring after the balance sheet date. It is because the condition

regarding the profit of business should not fall by greater than 20%. Thus, this is an adjusting

event after reporting period. The applicable accounting standards relates to this particular

transaction is AASB 118 Revenue recognition. This standard state that the company should

recognise its business revenue on the accrual basis. Further, the principle of conservatism

indicate that the company should recognise its uncertain income at the time when it earned but

for uncertain loss the company should create provision at the time when it actually arises. This

particular transaction is a non-adjusting event thus it is not required to be disclose in the notes to

As per AASB 110, the particular transaction of bad debt recovering is considered as

adjusting transaction or events after the reporting period. It is because this transaction provides

the evidence of condition that existed at the reporting period in the form of provision made

against bad debts. The applicable accounting standard relates to the present transaction is AASB

137 provision, contingent liabilities and contingent assets. This standard indicates that the

possible assets that arises from the past events and whose existence is in the balance sheet are

recorded or recognised in the financial statement at the time when the income occurrence. This

transaction will not disclose in the books of account because it is an adjusting transaction.

However, the particular transaction need to be adjusted in the financial statement of the end

reporting period (Dobson, 2020). The adjustment of this transaction is as follows:

Debtor a/c $550000

To Bad debt recovered a/c $550000

Bad debt recovered a/c $550000

To P&L a/c $550000

On this basis, the adjustment in the financial statement of MQE ltd is that their debtors i.e.,

accounts receivable value will be increased by $550000 that result into the total value of trade

receivable after adjustment is 4.037 million. Further, the income of the company will increase by

0.55 million due to this transaction adjustment. This should be done by the company as it affects

the decision-making of the financial statement of business.

3.

As per AASB 110, the nature of transaction of job seeker payment received from

government is adjusting event occurring after the balance sheet date. It is because the condition

regarding the profit of business should not fall by greater than 20%. Thus, this is an adjusting

event after reporting period. The applicable accounting standards relates to this particular

transaction is AASB 118 Revenue recognition. This standard state that the company should

recognise its business revenue on the accrual basis. Further, the principle of conservatism

indicate that the company should recognise its uncertain income at the time when it earned but

for uncertain loss the company should create provision at the time when it actually arises. This

particular transaction is a non-adjusting event thus it is not required to be disclose in the notes to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

account (Lessambo, 2018). However, this particular transaction of job seeker payment is

adjusted in the financial statement account. Here, in order to adjust this account, the following

entry need to be passed by MQE Ltd

Accrued liability a/c debit $500000

To Jobseeker account $500000

This indicate that the payment of job seeker the company have received from government are

now need to be paid by company again. This leads to increase in the liability of MQE Ltd by

$500000.

4.

As per AASB 110, the events occurring after the reporting period is of two types adjusting

and non-adjusting event. The nature of particular event of renegotiating some of the supplier in

the upcoming year of 2022 has been arises after the losses suffered by company from fire is non-

adjusting event. It is because there was no indicative of conditions that arose after the reporting

period which further means the company need not to adjust this event in the financial statement.

The applicable accounting standards relates to this particular event is AASB 124 Related party

transaction (Szulc and Zieniuk, 2020). This standard indicate that entity financial statement

should contain the necessary or materialistic disclosure about the related party’s transaction and

outstanding balance. It is because the this affect the financial position and decision-making of the

users of financial statement. As the event in this question is non-adjusting event, it is important

for the MQE ltd that they should disclose this event as it influence the financial statement user’s

decision. It is because the company have accepted the quota of that supplier in which one of the

director of MQE Ltd is holding share of 50%.

5.

As per AASB 110, the nature of this event is also adjusting event because the condition of

designing the new type of golf club is present in the balance sheet date as they have received

order for new club in May and June is $250000. The applicable accounting standard relate to this

transaction is AASB 110, events occurring after the balance sheet date. This standard indicate

that company should discourse all the material events that occur after the balance sheet and

adjust the event if condition is present in at the balance sheet date (Heazlewood and Andrew,

adjusted in the financial statement account. Here, in order to adjust this account, the following

entry need to be passed by MQE Ltd

Accrued liability a/c debit $500000

To Jobseeker account $500000

This indicate that the payment of job seeker the company have received from government are

now need to be paid by company again. This leads to increase in the liability of MQE Ltd by

$500000.

4.

As per AASB 110, the events occurring after the reporting period is of two types adjusting

and non-adjusting event. The nature of particular event of renegotiating some of the supplier in

the upcoming year of 2022 has been arises after the losses suffered by company from fire is non-

adjusting event. It is because there was no indicative of conditions that arose after the reporting

period which further means the company need not to adjust this event in the financial statement.

The applicable accounting standards relates to this particular event is AASB 124 Related party

transaction (Szulc and Zieniuk, 2020). This standard indicate that entity financial statement

should contain the necessary or materialistic disclosure about the related party’s transaction and

outstanding balance. It is because the this affect the financial position and decision-making of the

users of financial statement. As the event in this question is non-adjusting event, it is important

for the MQE ltd that they should disclose this event as it influence the financial statement user’s

decision. It is because the company have accepted the quota of that supplier in which one of the

director of MQE Ltd is holding share of 50%.

5.

As per AASB 110, the nature of this event is also adjusting event because the condition of

designing the new type of golf club is present in the balance sheet date as they have received

order for new club in May and June is $250000. The applicable accounting standard relate to this

transaction is AASB 110, events occurring after the balance sheet date. This standard indicate

that company should discourse all the material events that occur after the balance sheet and

adjust the event if condition is present in at the balance sheet date (Heazlewood and Andrew,

2021). As per this standard, the MQE ltd need to adjust the expenses associated with the

designing of new type of golf club in their financial statement as this affect the decision-making

of the users of the financial statement of MQE Ltd. The company should record the expenses in

their financial statement which involve the total cost they will incur in the designing of new golf

type is $135000. This will reduce the net income of company by amount $135000.

Part B

6. Provision of Journal entries, preparation of Schedule of temporary differences and calculation

of Deferred tax assets and Deferred tax liabilities

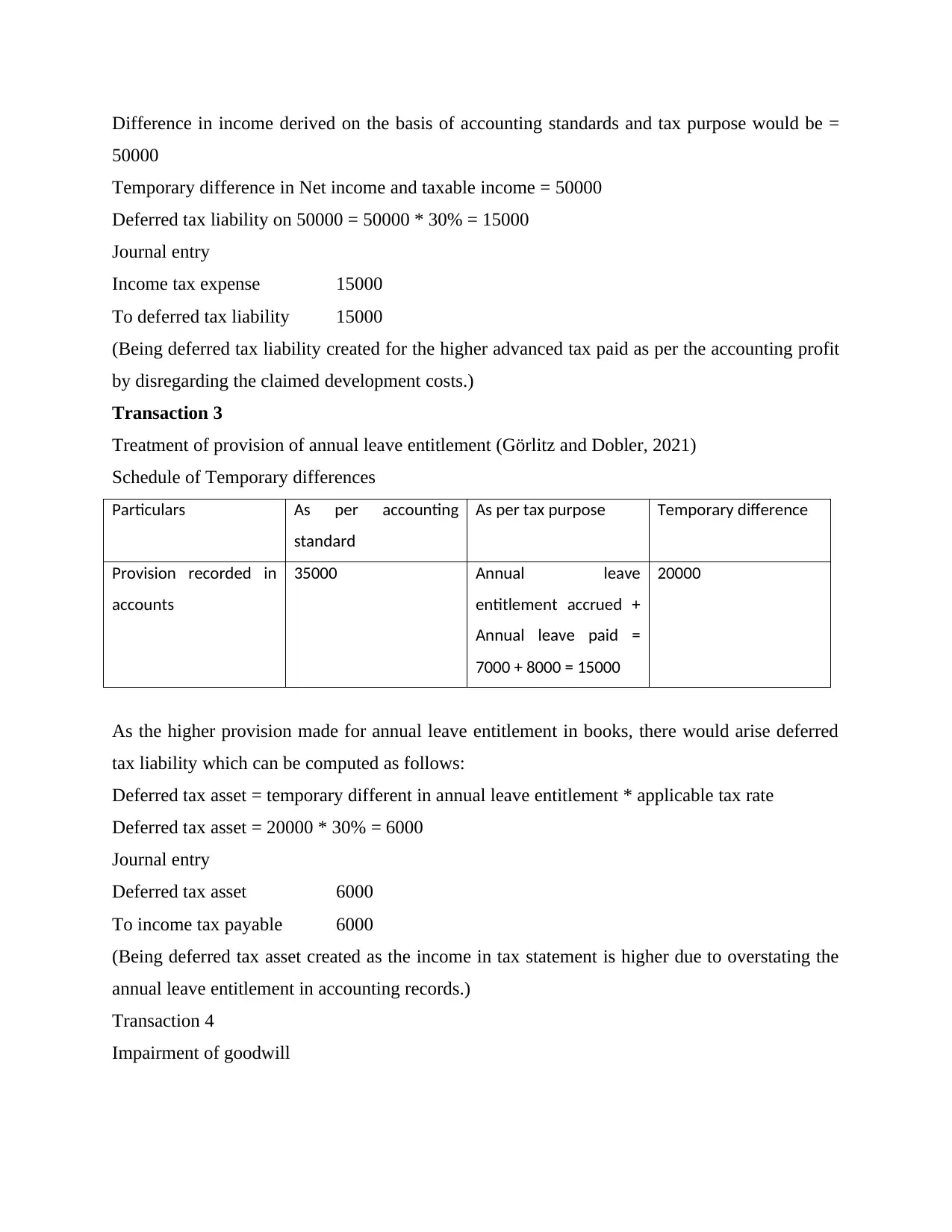

Transaction 1

Treatment of Depreciation

Useful life as per the books of accounts = 6 years

Useful life as per the tax purpose = 5 years

Particulars As per accounting

standard

As per tax purpose Temporary difference

Depreciation to be

charged

240000 / 6 = 40000 240000 / 5 = 48000 8000

Income tax

applicable

40000 * 30% = 12000 48000 * 30% = 14400 2400

Deferred tax liabilities = 8000 * 30% = 2400

Journal entries:

Income tax expense 2400

To deferred tax liability 2400

(Being deferred tax liability created as the depreciation charged as per the tax laws is higher.)

Transaction 2

Treatment of development costs

Balance sheet shows development cost = 50000

Cost claimed as deduction in prior financial year = 50000

designing of new type of golf club in their financial statement as this affect the decision-making

of the users of the financial statement of MQE Ltd. The company should record the expenses in

their financial statement which involve the total cost they will incur in the designing of new golf

type is $135000. This will reduce the net income of company by amount $135000.

Part B

6. Provision of Journal entries, preparation of Schedule of temporary differences and calculation

of Deferred tax assets and Deferred tax liabilities

Transaction 1

Treatment of Depreciation

Useful life as per the books of accounts = 6 years

Useful life as per the tax purpose = 5 years

Particulars As per accounting

standard

As per tax purpose Temporary difference

Depreciation to be

charged

240000 / 6 = 40000 240000 / 5 = 48000 8000

Income tax

applicable

40000 * 30% = 12000 48000 * 30% = 14400 2400

Deferred tax liabilities = 8000 * 30% = 2400

Journal entries:

Income tax expense 2400

To deferred tax liability 2400

(Being deferred tax liability created as the depreciation charged as per the tax laws is higher.)

Transaction 2

Treatment of development costs

Balance sheet shows development cost = 50000

Cost claimed as deduction in prior financial year = 50000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

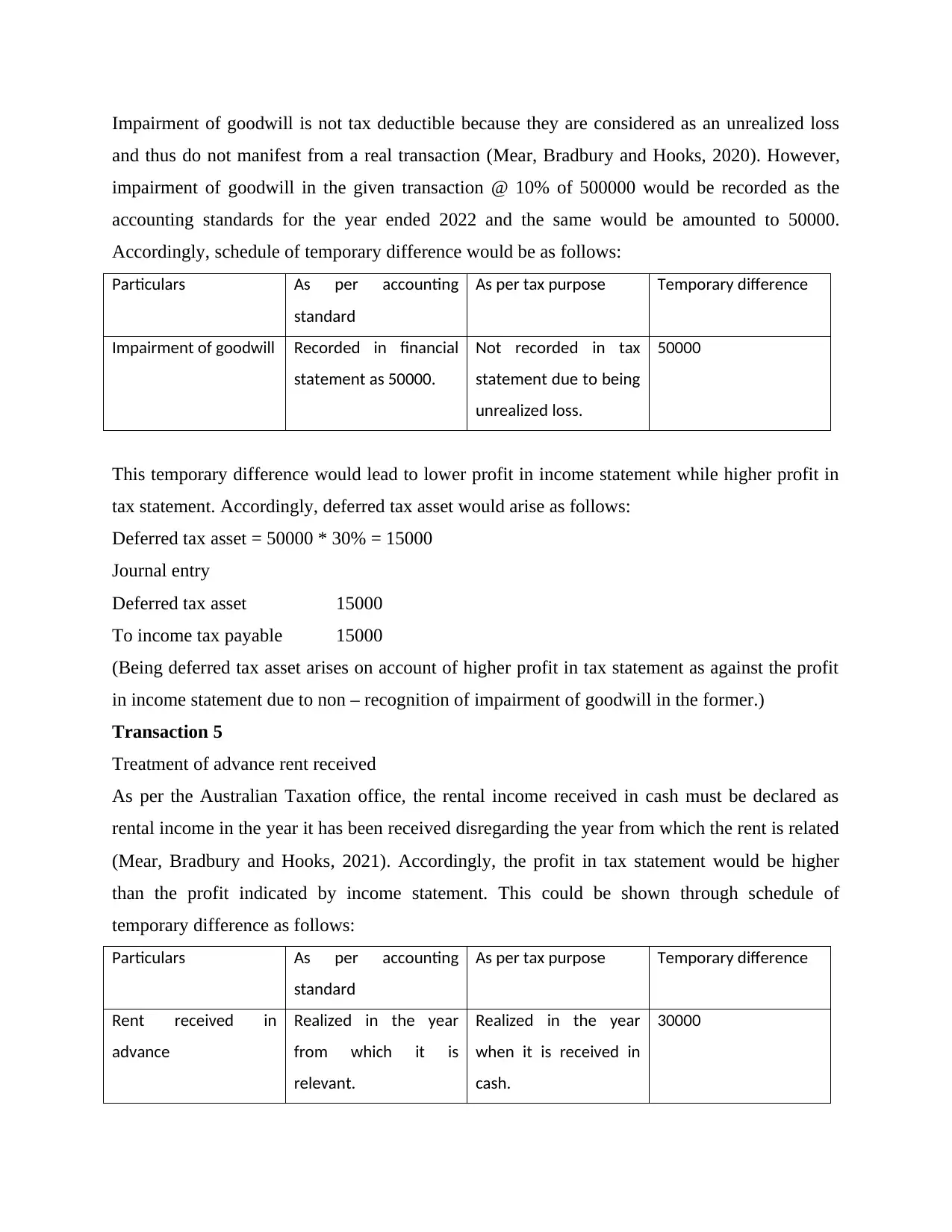

Difference in income derived on the basis of accounting standards and tax purpose would be =

50000

Temporary difference in Net income and taxable income = 50000

Deferred tax liability on 50000 = 50000 * 30% = 15000

Journal entry

Income tax expense 15000

To deferred tax liability 15000

(Being deferred tax liability created for the higher advanced tax paid as per the accounting profit

by disregarding the claimed development costs.)

Transaction 3

Treatment of provision of annual leave entitlement (Görlitz and Dobler, 2021)

Schedule of Temporary differences

Particulars As per accounting

standard

As per tax purpose Temporary difference

Provision recorded in

accounts

35000 Annual leave

entitlement accrued +

Annual leave paid =

7000 + 8000 = 15000

20000

As the higher provision made for annual leave entitlement in books, there would arise deferred

tax liability which can be computed as follows:

Deferred tax asset = temporary different in annual leave entitlement * applicable tax rate

Deferred tax asset = 20000 * 30% = 6000

Journal entry

Deferred tax asset 6000

To income tax payable 6000

(Being deferred tax asset created as the income in tax statement is higher due to overstating the

annual leave entitlement in accounting records.)

Transaction 4

Impairment of goodwill

50000

Temporary difference in Net income and taxable income = 50000

Deferred tax liability on 50000 = 50000 * 30% = 15000

Journal entry

Income tax expense 15000

To deferred tax liability 15000

(Being deferred tax liability created for the higher advanced tax paid as per the accounting profit

by disregarding the claimed development costs.)

Transaction 3

Treatment of provision of annual leave entitlement (Görlitz and Dobler, 2021)

Schedule of Temporary differences

Particulars As per accounting

standard

As per tax purpose Temporary difference

Provision recorded in

accounts

35000 Annual leave

entitlement accrued +

Annual leave paid =

7000 + 8000 = 15000

20000

As the higher provision made for annual leave entitlement in books, there would arise deferred

tax liability which can be computed as follows:

Deferred tax asset = temporary different in annual leave entitlement * applicable tax rate

Deferred tax asset = 20000 * 30% = 6000

Journal entry

Deferred tax asset 6000

To income tax payable 6000

(Being deferred tax asset created as the income in tax statement is higher due to overstating the

annual leave entitlement in accounting records.)

Transaction 4

Impairment of goodwill

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Impairment of goodwill is not tax deductible because they are considered as an unrealized loss

and thus do not manifest from a real transaction (Mear, Bradbury and Hooks, 2020). However,

impairment of goodwill in the given transaction @ 10% of 500000 would be recorded as the

accounting standards for the year ended 2022 and the same would be amounted to 50000.

Accordingly, schedule of temporary difference would be as follows:

Particulars As per accounting

standard

As per tax purpose Temporary difference

Impairment of goodwill Recorded in financial

statement as 50000.

Not recorded in tax

statement due to being

unrealized loss.

50000

This temporary difference would lead to lower profit in income statement while higher profit in

tax statement. Accordingly, deferred tax asset would arise as follows:

Deferred tax asset = 50000 * 30% = 15000

Journal entry

Deferred tax asset 15000

To income tax payable 15000

(Being deferred tax asset arises on account of higher profit in tax statement as against the profit

in income statement due to non – recognition of impairment of goodwill in the former.)

Transaction 5

Treatment of advance rent received

As per the Australian Taxation office, the rental income received in cash must be declared as

rental income in the year it has been received disregarding the year from which the rent is related

(Mear, Bradbury and Hooks, 2021). Accordingly, the profit in tax statement would be higher

than the profit indicated by income statement. This could be shown through schedule of

temporary difference as follows:

Particulars As per accounting

standard

As per tax purpose Temporary difference

Rent received in

advance

Realized in the year

from which it is

relevant.

Realized in the year

when it is received in

cash.

30000

and thus do not manifest from a real transaction (Mear, Bradbury and Hooks, 2020). However,

impairment of goodwill in the given transaction @ 10% of 500000 would be recorded as the

accounting standards for the year ended 2022 and the same would be amounted to 50000.

Accordingly, schedule of temporary difference would be as follows:

Particulars As per accounting

standard

As per tax purpose Temporary difference

Impairment of goodwill Recorded in financial

statement as 50000.

Not recorded in tax

statement due to being

unrealized loss.

50000

This temporary difference would lead to lower profit in income statement while higher profit in

tax statement. Accordingly, deferred tax asset would arise as follows:

Deferred tax asset = 50000 * 30% = 15000

Journal entry

Deferred tax asset 15000

To income tax payable 15000

(Being deferred tax asset arises on account of higher profit in tax statement as against the profit

in income statement due to non – recognition of impairment of goodwill in the former.)

Transaction 5

Treatment of advance rent received

As per the Australian Taxation office, the rental income received in cash must be declared as

rental income in the year it has been received disregarding the year from which the rent is related

(Mear, Bradbury and Hooks, 2021). Accordingly, the profit in tax statement would be higher

than the profit indicated by income statement. This could be shown through schedule of

temporary difference as follows:

Particulars As per accounting

standard

As per tax purpose Temporary difference

Rent received in

advance

Realized in the year

from which it is

relevant.

Realized in the year

when it is received in

cash.

30000

Rental income = 0 Rental income = 30000

As a result of this temporary difference, the profit in tax statement would be higher than the

profit in income statement, therefore, deferred tax asset would arise as follows:

Deferred tax asset = 30000 * 30% = 9000

Journal entry

Deferred tax asset 9000

To income tax payable 9000

(Being deferred tax asset created as profit in tax statement was higher than profit in income

statement due to recognition of rent received in advance in the former.)

7. Lease accounting

The current lease would be treated as capital lease it is satisfying the following conditions:

Lease term is greater than 75% of economic life of the asset, that is 5 years > 4.5 years

(75% of 6 years) (Sorrentino, Smarra and Briamonte, 2020).

Present value of lease payments is greater than 90% of the fair value of asset in the

beginning.

Initial value of asset = 65000 + 2500 (additional costs) = 67500

92550 > 60750 (90% of 67500).

Journal entries for recording capital lease

Yearly lease payments = 22500

Lease term = 5 years

Present value of lease payments = (1 / r) – 1 / r (1 + r)t

r = 7%

t = 5 years

= (1 / 7%) – 1 / 7% (1 + 7%)5

= (14.29) – 1 / 7% (1.40)

= (14.29) – 1 / 0.098

= (14.29) – (10.19) = 4.1

Present value annuity factor = 4.1

Present value of lease payments = 4.1 * 22500 = 92250

Interest payment at the end of first year (included in lease rent) = 92250 * 7% = 6458

Depreciation of leased van = 92250 / 5 = 18450

As a result of this temporary difference, the profit in tax statement would be higher than the

profit in income statement, therefore, deferred tax asset would arise as follows:

Deferred tax asset = 30000 * 30% = 9000

Journal entry

Deferred tax asset 9000

To income tax payable 9000

(Being deferred tax asset created as profit in tax statement was higher than profit in income

statement due to recognition of rent received in advance in the former.)

7. Lease accounting

The current lease would be treated as capital lease it is satisfying the following conditions:

Lease term is greater than 75% of economic life of the asset, that is 5 years > 4.5 years

(75% of 6 years) (Sorrentino, Smarra and Briamonte, 2020).

Present value of lease payments is greater than 90% of the fair value of asset in the

beginning.

Initial value of asset = 65000 + 2500 (additional costs) = 67500

92550 > 60750 (90% of 67500).

Journal entries for recording capital lease

Yearly lease payments = 22500

Lease term = 5 years

Present value of lease payments = (1 / r) – 1 / r (1 + r)t

r = 7%

t = 5 years

= (1 / 7%) – 1 / 7% (1 + 7%)5

= (14.29) – 1 / 7% (1.40)

= (14.29) – 1 / 0.098

= (14.29) – (10.19) = 4.1

Present value annuity factor = 4.1

Present value of lease payments = 4.1 * 22500 = 92250

Interest payment at the end of first year (included in lease rent) = 92250 * 7% = 6458

Depreciation of leased van = 92250 / 5 = 18450

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

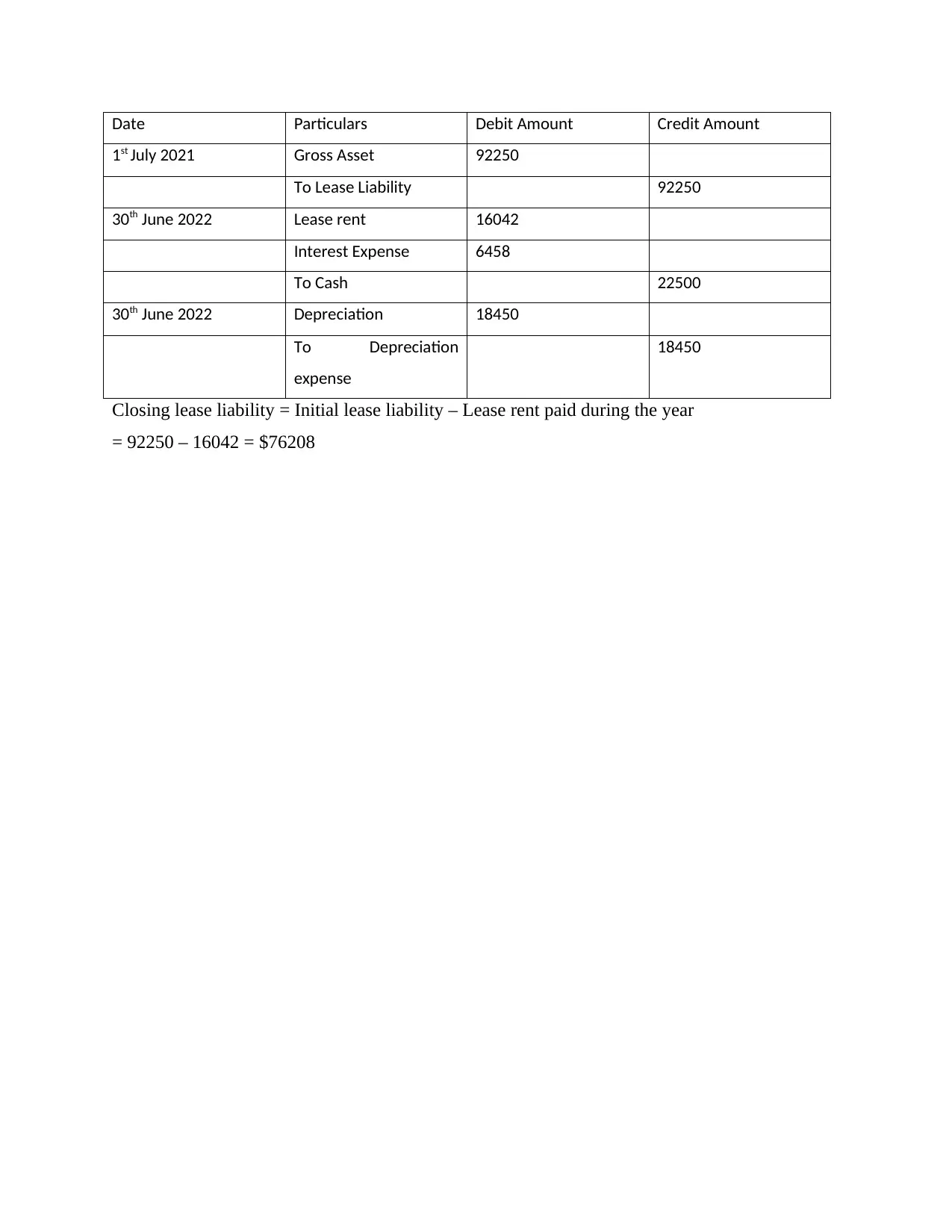

Date Particulars Debit Amount Credit Amount

1st July 2021 Gross Asset 92250

To Lease Liability 92250

30th June 2022 Lease rent 16042

Interest Expense 6458

To Cash 22500

30th June 2022 Depreciation 18450

To Depreciation

expense

18450

Closing lease liability = Initial lease liability – Lease rent paid during the year

= 92250 – 16042 = $76208

1st July 2021 Gross Asset 92250

To Lease Liability 92250

30th June 2022 Lease rent 16042

Interest Expense 6458

To Cash 22500

30th June 2022 Depreciation 18450

To Depreciation

expense

18450

Closing lease liability = Initial lease liability – Lease rent paid during the year

= 92250 – 16042 = $76208

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Sorrentino, M., Smarra, M. and Briamonte, M. F., 2020. Lease accounting: Back into the past—a

general review of different theoretical approaches. International journal of business and

management, 15(2).

Mear, K., Bradbury, M. and Hooks, J., 2021. The ability of deferred tax to predict future

tax. Accounting & Finance, 61(1), pp.241-264.

Mear, K., Bradbury, M. and Hooks, J., 2020. Is the balance sheet method of deferred tax

informative?. Pacific Accounting Review.

Görlitz, A. and Dobler, M., 2021. Financial accounting for deferred taxes: a systematic review of

empirical evidence. Management Review Quarterly, pp.1-53.

Heazlewood, C. and Andrew, B., 2021. Company law administrators in Victoria and the

Australian Capital Territory object to tax-effect accountinq whilst the NSW Corporate

Affairs Commission endorses the method required in Standard DS4. Aus tralian Journal

of M anagement'f'.

Szulc, M. and Zieniuk, P., 2020. The disclosure of events after the reporting period. The example

of listed companies from selected European countries. Zeszyty Teoretyczne

Rachunkowości, (109 (165)), pp.139-155.

Lessambo, F. I., 2018. Subsequent Events; and Going Concern. In Auditing, Assurance Services,

and Forensics (pp. 247-259). Palgrave Macmillan, Cham.

Dobson, C., 2020. Assessing the effects of housing policy measures on new lending in

Australia. BIS Paper, (110c).

Czerney, K. and et.al., 2020. Do type II subsequent events impair financial reporting

quality?. The Accounting Review, 95(6), pp.97-123.

Books and Journals

Sorrentino, M., Smarra, M. and Briamonte, M. F., 2020. Lease accounting: Back into the past—a

general review of different theoretical approaches. International journal of business and

management, 15(2).

Mear, K., Bradbury, M. and Hooks, J., 2021. The ability of deferred tax to predict future

tax. Accounting & Finance, 61(1), pp.241-264.

Mear, K., Bradbury, M. and Hooks, J., 2020. Is the balance sheet method of deferred tax

informative?. Pacific Accounting Review.

Görlitz, A. and Dobler, M., 2021. Financial accounting for deferred taxes: a systematic review of

empirical evidence. Management Review Quarterly, pp.1-53.

Heazlewood, C. and Andrew, B., 2021. Company law administrators in Victoria and the

Australian Capital Territory object to tax-effect accountinq whilst the NSW Corporate

Affairs Commission endorses the method required in Standard DS4. Aus tralian Journal

of M anagement'f'.

Szulc, M. and Zieniuk, P., 2020. The disclosure of events after the reporting period. The example

of listed companies from selected European countries. Zeszyty Teoretyczne

Rachunkowości, (109 (165)), pp.139-155.

Lessambo, F. I., 2018. Subsequent Events; and Going Concern. In Auditing, Assurance Services,

and Forensics (pp. 247-259). Palgrave Macmillan, Cham.

Dobson, C., 2020. Assessing the effects of housing policy measures on new lending in

Australia. BIS Paper, (110c).

Czerney, K. and et.al., 2020. Do type II subsequent events impair financial reporting

quality?. The Accounting Review, 95(6), pp.97-123.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.