Accounting Statement Analysis, Budgeting, and Decision Making

VerifiedAdded on 2023/06/05

|9

|2966

|473

Homework Assignment

AI Summary

This assignment delves into financial statement analysis, covering key concepts like profitability, cost relationships, and budgeting. The student reflects on the importance of financial statement analysis, exploring techniques such as ratio analysis and economic profit. The assignment includes restati...

Accounting Statement Analysis

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Step-1: Ideas, Reflections and Reactions to Analyzing Financial Statements

Reading the material given in chapter-4, I got the knowledge and importance of financial

statement analysis. Initially, the author wrote about the working pattern of capital market and

linked it to analysis of financial health of a business. This made it interesting for me to go further

and dig out what is that which affects the decisions to choose a particular type of business for

investment. I found out that this is all about past, present and future of financial performance of a

business. An investor needs to analyze what business has delivered in past for its investors, how

is it doing presently and how well it can do in future years. If it is expected that the business will

provide good returns in future, the investor jumps into investing in the business. The financial

results of past give a strong basis to predict future, however, I found it difficult to strike out the

items which will be used in analysis. After going through the entire chapter, I got those items. I

think those items should be operating profits and free cash flows. Analyzing the operating profits

through profit and loss statement and free cash flows through cash flow statement is essential to

predict future value of business. There are a number of techniques such as ratio analysis,

economic profit analysis, free cash flow valuation etc. which are useful in financial analysis and

investment decision making (Kim, Li, Lu, & Yu, 2016).

The reading of this chapter was quite interesting with a good learning; however, few questions

arose in mind, which are as under:

To analyze the profitability, one can apply economic profit approach or one can compute

simply profitability ratios such as net margin and return on equity, so which one is

better?

Why can not I use financial statements for ratio analysis without restating them?

Step-2: Ideas, Reflections and Reactions to Understanding Key Cost Relationships

The reading of this chapter began with overview of the cost and what is that which drives the

cost to incur. I had an understanding of cost but it was interesting for me to go deep in finding

out its drivers. I further read and came to know that proper allocation of cost to the products is

essential for optimal decision making and the knowledge of drivers of cost is important for

proper allocation of cost. In the traditional costing system, there were used to be only two main

cost drivers such as machine hours and units produced. However, I was surprised after going

through the concept of activity based costing. I came to know that there may be various cost

drivers apart from machine hours and units produced. The activity based costing introduced the

use of different cost drivers for different types of costs. However, it was difficult for me to

understand and figure out the cost drivers for each and every item of cost incurred for a large

organization which is involved in multiple manufacturing activities. I also found the crucial

relation of variable and fixed cost with the level of output. However, it was difficult to

understand relationship with output of few costs which were categorized as mixed cost (Hill,

2017). There were few questions that came to my mind as shown below:

Why is it necessary to write down all period costs and charge to profit and loss account?

How difficult, time consuming, cumbersome will it be for a business to apply activities

based costing?

2

Reading the material given in chapter-4, I got the knowledge and importance of financial

statement analysis. Initially, the author wrote about the working pattern of capital market and

linked it to analysis of financial health of a business. This made it interesting for me to go further

and dig out what is that which affects the decisions to choose a particular type of business for

investment. I found out that this is all about past, present and future of financial performance of a

business. An investor needs to analyze what business has delivered in past for its investors, how

is it doing presently and how well it can do in future years. If it is expected that the business will

provide good returns in future, the investor jumps into investing in the business. The financial

results of past give a strong basis to predict future, however, I found it difficult to strike out the

items which will be used in analysis. After going through the entire chapter, I got those items. I

think those items should be operating profits and free cash flows. Analyzing the operating profits

through profit and loss statement and free cash flows through cash flow statement is essential to

predict future value of business. There are a number of techniques such as ratio analysis,

economic profit analysis, free cash flow valuation etc. which are useful in financial analysis and

investment decision making (Kim, Li, Lu, & Yu, 2016).

The reading of this chapter was quite interesting with a good learning; however, few questions

arose in mind, which are as under:

To analyze the profitability, one can apply economic profit approach or one can compute

simply profitability ratios such as net margin and return on equity, so which one is

better?

Why can not I use financial statements for ratio analysis without restating them?

Step-2: Ideas, Reflections and Reactions to Understanding Key Cost Relationships

The reading of this chapter began with overview of the cost and what is that which drives the

cost to incur. I had an understanding of cost but it was interesting for me to go deep in finding

out its drivers. I further read and came to know that proper allocation of cost to the products is

essential for optimal decision making and the knowledge of drivers of cost is important for

proper allocation of cost. In the traditional costing system, there were used to be only two main

cost drivers such as machine hours and units produced. However, I was surprised after going

through the concept of activity based costing. I came to know that there may be various cost

drivers apart from machine hours and units produced. The activity based costing introduced the

use of different cost drivers for different types of costs. However, it was difficult for me to

understand and figure out the cost drivers for each and every item of cost incurred for a large

organization which is involved in multiple manufacturing activities. I also found the crucial

relation of variable and fixed cost with the level of output. However, it was difficult to

understand relationship with output of few costs which were categorized as mixed cost (Hill,

2017). There were few questions that came to my mind as shown below:

Why is it necessary to write down all period costs and charge to profit and loss account?

How difficult, time consuming, cumbersome will it be for a business to apply activities

based costing?

2

Step-3:

The restatement of AssetCo Plc financial statements has been done (refer attached excel).

The statement of changes in equity was restated by dividing the items into more headings so that

figures could be made more relevant for analysis. For instance, income was divided into

operating comprehensive income and financial comprehensive income. Similarly, the balance

sheet was restated adding new headings such as operating assets, operating liabilities, and net

operating assets. Restating the balance sheet was a quite tedious task. While restating the balance

one has to ensure that balance tallies after transferring various items of assets and liabilities from

one head to another. The income statement was also restated on same lines. There was made a

clear distinction between the operating and financial income and expenses in the restated income

statement (Hoyle, Schaefer, & Doupnik, 2015).

Step-4: Feedback

My Comments

Step 3

My feedback:

Your restatements to changes in equity were quite simple.

You could have shown details of individual items being

restated in the statement of changes in equity.

However, I found that your restatements to balance sheet

were good. You manipulated the figures and turned and

twisted them quite wisely. At the end, the balances tallied

which shows correctness of your work.

The restatements of figures in the statement of income

were also good; however, I observed that you clubbed

certain items which could have been avoided.

Other student’s feedback:

I showed my work to the students and many of them

praised me. Some of them were quite surprised seeing my

restated balance sheet matching conveniently. Some

students advised me on formatting which helped me in

further refining my work.

Restated Statement of Changes

in Equity

Balance Sheet

Income Statement

Commentary and discussion

with others

(Note: You may wish to give

some comments

on their Excel spreadsheet)

3

The restatement of AssetCo Plc financial statements has been done (refer attached excel).

The statement of changes in equity was restated by dividing the items into more headings so that

figures could be made more relevant for analysis. For instance, income was divided into

operating comprehensive income and financial comprehensive income. Similarly, the balance

sheet was restated adding new headings such as operating assets, operating liabilities, and net

operating assets. Restating the balance sheet was a quite tedious task. While restating the balance

one has to ensure that balance tallies after transferring various items of assets and liabilities from

one head to another. The income statement was also restated on same lines. There was made a

clear distinction between the operating and financial income and expenses in the restated income

statement (Hoyle, Schaefer, & Doupnik, 2015).

Step-4: Feedback

My Comments

Step 3

My feedback:

Your restatements to changes in equity were quite simple.

You could have shown details of individual items being

restated in the statement of changes in equity.

However, I found that your restatements to balance sheet

were good. You manipulated the figures and turned and

twisted them quite wisely. At the end, the balances tallied

which shows correctness of your work.

The restatements of figures in the statement of income

were also good; however, I observed that you clubbed

certain items which could have been avoided.

Other student’s feedback:

I showed my work to the students and many of them

praised me. Some of them were quite surprised seeing my

restated balance sheet matching conveniently. Some

students advised me on formatting which helped me in

further refining my work.

Restated Statement of Changes

in Equity

Balance Sheet

Income Statement

Commentary and discussion

with others

(Note: You may wish to give

some comments

on their Excel spreadsheet)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Step 4

Individual feedback with other

students

Restatement of the financial statement is essential to know

the concept of balancing. This task opened up my mind

regarding accounting and preparation of the financial

statements. Now, I can think from a broader perspective

when talking about preparation of the financial statements.

Overall ASS#2 (Steps 3 & 4) I found the feedback sharing process is quite healthy. It

promotes brainstorming which is necessary to understand

the things conceptually. I realized the importance of

feedback sharing the most when we were discussing the

restated financial statements.

Step-5: Ideas, Reflections and Reactions to Budget for the Short Term

The budgets are needed to be prepaid in the normal day to day life as well so I was well aware

that to run a business, we need to prepare budgets but to know how and what to include in

budgets was interesting for me. I was surprised to know that it is not as simple as it looks. After

reading this chapter, I got to know that a business manager needs to estimate and prepare budget

for all revenue, expenditures, and cash needed. Further, it was also interesting to figure out that

the work is not over only on prepare the budget and putting it forward for implementation, the

crucial aspect is its monitoring throughout the budget period. A business manager needs to

closely monitor the progress, ensure that everything is going as planned and take necessary

actions in case deviations found (Ittner & Michels, 2017).

Further, I got to know that it is necessary to set benchmarks and performance measurement

criteria and appraise the performance of employees. However, it was difficult for me understand

the design of a suitable performance evaluation basis in certain cases. There were few questions

which came to my mind as shown below:

How difficult would it be for a manager to ensure proper co-operation and co-ordination

between different departments?

Should budgets to be rigid or flexible and set on the basis of achievable targets?

4

Individual feedback with other

students

Restatement of the financial statement is essential to know

the concept of balancing. This task opened up my mind

regarding accounting and preparation of the financial

statements. Now, I can think from a broader perspective

when talking about preparation of the financial statements.

Overall ASS#2 (Steps 3 & 4) I found the feedback sharing process is quite healthy. It

promotes brainstorming which is necessary to understand

the things conceptually. I realized the importance of

feedback sharing the most when we were discussing the

restated financial statements.

Step-5: Ideas, Reflections and Reactions to Budget for the Short Term

The budgets are needed to be prepaid in the normal day to day life as well so I was well aware

that to run a business, we need to prepare budgets but to know how and what to include in

budgets was interesting for me. I was surprised to know that it is not as simple as it looks. After

reading this chapter, I got to know that a business manager needs to estimate and prepare budget

for all revenue, expenditures, and cash needed. Further, it was also interesting to figure out that

the work is not over only on prepare the budget and putting it forward for implementation, the

crucial aspect is its monitoring throughout the budget period. A business manager needs to

closely monitor the progress, ensure that everything is going as planned and take necessary

actions in case deviations found (Ittner & Michels, 2017).

Further, I got to know that it is necessary to set benchmarks and performance measurement

criteria and appraise the performance of employees. However, it was difficult for me understand

the design of a suitable performance evaluation basis in certain cases. There were few questions

which came to my mind as shown below:

How difficult would it be for a manager to ensure proper co-operation and co-ordination

between different departments?

Should budgets to be rigid or flexible and set on the basis of achievable targets?

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Step-6: Ideas, Reflections and Reactions to We Have Got to Make Some Decisions

The reading of this chapter took me to the concepts of decision making. Relevant cost, capacity

constraints, and time value of money were the three most crucial concepts of decision making

which I learned after reading this chapter. It was very interesting to read the concept of relevant

cost because before going through this concept I was of the view that each and every dollar

incurred on a particular product is a cost but the same is not the case. One has to access the

situation and decide which costs are being incurred solely due to the decision at hand. In short

term decision making, the manager also has to take into consideration the capacity constraints of

the firm. Further, the time value of money gave me the understanding that dollar received today

is not equal to the dollar received after one year.

Apart from this, I also learned few long term decision making techniques such as accounting rate

of return, net present value, payback period, and internal rate of return. Overall reading this

chapter was a good experience but it left many questions in mind few of them are as under:

Which decision making technique out of ARR, NPV, IRR, and Payback period is the

best?

Do we need to consider contribution lost on one product due to new product being

produced as relevant cost and if yes then why?

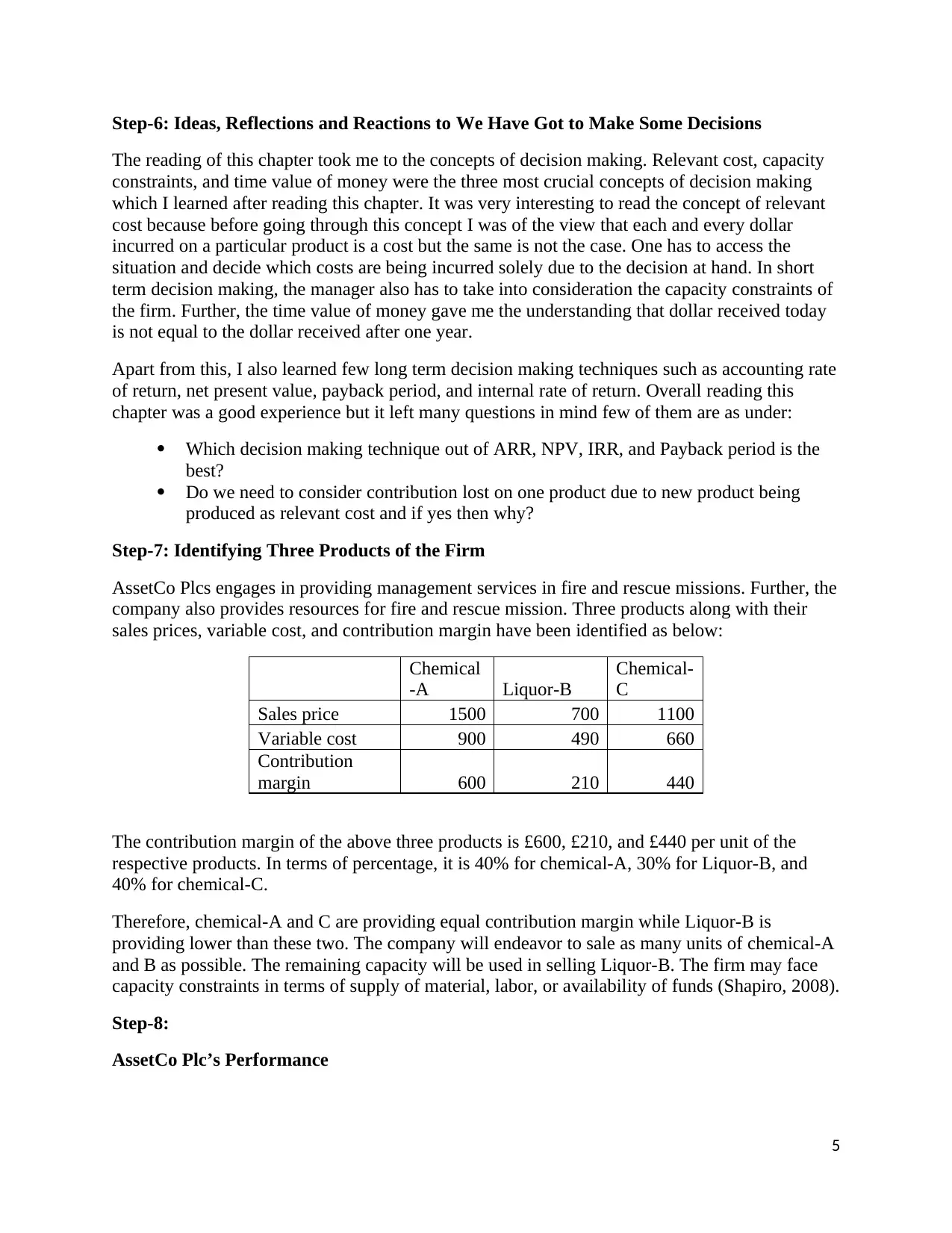

Step-7: Identifying Three Products of the Firm

AssetCo Plcs engages in providing management services in fire and rescue missions. Further, the

company also provides resources for fire and rescue mission. Three products along with their

sales prices, variable cost, and contribution margin have been identified as below:

Chemical

-A Liquor-B

Chemical-

C

Sales price 1500 700 1100

Variable cost 900 490 660

Contribution

margin 600 210 440

The contribution margin of the above three products is £600, £210, and £440 per unit of the

respective products. In terms of percentage, it is 40% for chemical-A, 30% for Liquor-B, and

40% for chemical-C.

Therefore, chemical-A and C are providing equal contribution margin while Liquor-B is

providing lower than these two. The company will endeavor to sale as many units of chemical-A

and B as possible. The remaining capacity will be used in selling Liquor-B. The firm may face

capacity constraints in terms of supply of material, labor, or availability of funds (Shapiro, 2008).

Step-8:

AssetCo Plc’s Performance

5

The reading of this chapter took me to the concepts of decision making. Relevant cost, capacity

constraints, and time value of money were the three most crucial concepts of decision making

which I learned after reading this chapter. It was very interesting to read the concept of relevant

cost because before going through this concept I was of the view that each and every dollar

incurred on a particular product is a cost but the same is not the case. One has to access the

situation and decide which costs are being incurred solely due to the decision at hand. In short

term decision making, the manager also has to take into consideration the capacity constraints of

the firm. Further, the time value of money gave me the understanding that dollar received today

is not equal to the dollar received after one year.

Apart from this, I also learned few long term decision making techniques such as accounting rate

of return, net present value, payback period, and internal rate of return. Overall reading this

chapter was a good experience but it left many questions in mind few of them are as under:

Which decision making technique out of ARR, NPV, IRR, and Payback period is the

best?

Do we need to consider contribution lost on one product due to new product being

produced as relevant cost and if yes then why?

Step-7: Identifying Three Products of the Firm

AssetCo Plcs engages in providing management services in fire and rescue missions. Further, the

company also provides resources for fire and rescue mission. Three products along with their

sales prices, variable cost, and contribution margin have been identified as below:

Chemical

-A Liquor-B

Chemical-

C

Sales price 1500 700 1100

Variable cost 900 490 660

Contribution

margin 600 210 440

The contribution margin of the above three products is £600, £210, and £440 per unit of the

respective products. In terms of percentage, it is 40% for chemical-A, 30% for Liquor-B, and

40% for chemical-C.

Therefore, chemical-A and C are providing equal contribution margin while Liquor-B is

providing lower than these two. The company will endeavor to sale as many units of chemical-A

and B as possible. The remaining capacity will be used in selling Liquor-B. The firm may face

capacity constraints in terms of supply of material, labor, or availability of funds (Shapiro, 2008).

Step-8:

AssetCo Plc’s Performance

5

The profitability of the firm in the year 2017 went down as depicted from the decline in net profit

margin and return on assets ratio. The net profit margin went down from 15.4% in 2014 to 8.70%

in 2017. Similarly, return on assets also declined from 13% in 2014 to 6.70% in 2017. However,

the financial results of 2016 shows that the firm was making good returns. The net profit margin

reached to 19.70% and return on assets also showed improvement reaching at 14.70% (Excel

attached).

The Days inventory ratio could not be calculated except for the year 2014 because the company

does not maintain inventories as such. Increase in days inventory ratio shows inefficiency of

management in regards to inventory handling decisions (Tracy, 2012). Further, assets turnover

ratio was observed to be decreasing from 0.84 times to 0.76 times showing a decline in revenues

over the period effectively.

The debt to equity ratio has been found to be stable except for the year 2016. In the year 2016,

the ratio went up to 19.90% from 17.90% showing increase in debt. Further, the debt ratio was

15.50% in 2014 which decreased to 14.62% in 2017 (Excel attached). The decrease in debt ratio

shows that the firm is less dependent on debt than equity for financing its assets which is a

favorable position.

Comparison with other Students

When I compared financial ratios of my company i.e. AssetCo Plcs with other the

company allotted to other student’s, I found difference in many areas. I found that profitability

ratio of my company was higher than the average of other companies which implies that my

company was earning better profits. However, there were few companies which were better than

AssetCo Plcs. I found many other companies having better current ratio and debt equity ratio

which indicates that other companies were in better liquidity and solvency position.

Economic profits

The economic profits of AssetCo Plcs for the year 2014 were £2,087.47 million. In the year 2015

and 2016, the firm experienced hike in economic profits of reaching to £3,901.94 and £4,040.20

respectively (Excel attached). The return on operating assets was very high as compared to the

cost of capital in the 2015 and 2016 which caused the economic profits to be on the higher side

in these years. In the year 2017, the economic profits again turned positive with the positive

movement in the net operating income.

Step-9: Developing a Capital Investment Decision

The NPV, IRR, and Payback period for alternative-1 and 2 have been computed as shown in the

Excel worksheet. The NPV of Bunning alternative is £6,553.43 and that of Cole alternative it is

£34,358.30. So, clearly alternative of Coles wins based on NPC comparisons. The IRR of

Bunning is 14.37% while that of Cole it is 28.37%. Further, the payback period of the former is

5.23 years while that of later it is 3.16 years. It could be observed that IRR and Payback period

also suggest that alternative Coles is preferable over the alternative of Bunning.

There are certain limitations of this analysis. The assumptions made in regards to cash inflows

and outflows might not be as accurate as expected. So, there are the chances the actual results

might be different from the expected ones.

6

margin and return on assets ratio. The net profit margin went down from 15.4% in 2014 to 8.70%

in 2017. Similarly, return on assets also declined from 13% in 2014 to 6.70% in 2017. However,

the financial results of 2016 shows that the firm was making good returns. The net profit margin

reached to 19.70% and return on assets also showed improvement reaching at 14.70% (Excel

attached).

The Days inventory ratio could not be calculated except for the year 2014 because the company

does not maintain inventories as such. Increase in days inventory ratio shows inefficiency of

management in regards to inventory handling decisions (Tracy, 2012). Further, assets turnover

ratio was observed to be decreasing from 0.84 times to 0.76 times showing a decline in revenues

over the period effectively.

The debt to equity ratio has been found to be stable except for the year 2016. In the year 2016,

the ratio went up to 19.90% from 17.90% showing increase in debt. Further, the debt ratio was

15.50% in 2014 which decreased to 14.62% in 2017 (Excel attached). The decrease in debt ratio

shows that the firm is less dependent on debt than equity for financing its assets which is a

favorable position.

Comparison with other Students

When I compared financial ratios of my company i.e. AssetCo Plcs with other the

company allotted to other student’s, I found difference in many areas. I found that profitability

ratio of my company was higher than the average of other companies which implies that my

company was earning better profits. However, there were few companies which were better than

AssetCo Plcs. I found many other companies having better current ratio and debt equity ratio

which indicates that other companies were in better liquidity and solvency position.

Economic profits

The economic profits of AssetCo Plcs for the year 2014 were £2,087.47 million. In the year 2015

and 2016, the firm experienced hike in economic profits of reaching to £3,901.94 and £4,040.20

respectively (Excel attached). The return on operating assets was very high as compared to the

cost of capital in the 2015 and 2016 which caused the economic profits to be on the higher side

in these years. In the year 2017, the economic profits again turned positive with the positive

movement in the net operating income.

Step-9: Developing a Capital Investment Decision

The NPV, IRR, and Payback period for alternative-1 and 2 have been computed as shown in the

Excel worksheet. The NPV of Bunning alternative is £6,553.43 and that of Cole alternative it is

£34,358.30. So, clearly alternative of Coles wins based on NPC comparisons. The IRR of

Bunning is 14.37% while that of Cole it is 28.37%. Further, the payback period of the former is

5.23 years while that of later it is 3.16 years. It could be observed that IRR and Payback period

also suggest that alternative Coles is preferable over the alternative of Bunning.

There are certain limitations of this analysis. The assumptions made in regards to cash inflows

and outflows might not be as accurate as expected. So, there are the chances the actual results

might be different from the expected ones.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Step-10: Feedback

My Comments

Step 7

Identify three products or services of

your firm

Estimate selling price, variable cost &

CM

Commentary – contribution margins

Constraints – identify & commentary

The step 7 was little easy as compared to others so the

feedback sharing on this was for shorter time period.

Almost all the students were able to identify products/

services and estimate prices, costs, and margins.

However, the communication with the students helped

in reorganizing and formatting the content better.

Step 8

In calculating the ratios, few students were confused

about linking the data cells in excel. However, it was

sorted out with discussion. Further, interpreting the

ratios was also tedious task. There different

interpretations of different students on the same

results. With the logical discussion among the

members, it was also sorted out and we reached to the

common consensus. However, the most difficult part

was interpretation of economic profits. Everybody was

confused while interpreting the economic profits.

Calculation of ratios

Ratios – commentary (blog)

Calculate economic profit

Commentary – drivers of economic

profit (blog)

Step 9

This task was quite interesting as it helped in learning

not only financial concepts but also the excel

functions. I observed that few student put in wrong

function of calculating NPV resulting in wrong

solution. IRR and Payback period was correctly

computed by many students. I also learned good points

regarding presentation by reviewing the work of

others.

Develop capital investment decision

for your firm

Calculation of payback period, NPV &

IRR

Recommendation & discussion

Step 10

I had one on one conversation with the students which

helped in passing individual feedbacks. It was a good

learning curve for all of us.

Individual feedback with other

students

Overall ASS#3 Overall, this assessment proved to be a pioneer in

terms of learning the concepts of financial reporting,

7

My Comments

Step 7

Identify three products or services of

your firm

Estimate selling price, variable cost &

CM

Commentary – contribution margins

Constraints – identify & commentary

The step 7 was little easy as compared to others so the

feedback sharing on this was for shorter time period.

Almost all the students were able to identify products/

services and estimate prices, costs, and margins.

However, the communication with the students helped

in reorganizing and formatting the content better.

Step 8

In calculating the ratios, few students were confused

about linking the data cells in excel. However, it was

sorted out with discussion. Further, interpreting the

ratios was also tedious task. There different

interpretations of different students on the same

results. With the logical discussion among the

members, it was also sorted out and we reached to the

common consensus. However, the most difficult part

was interpretation of economic profits. Everybody was

confused while interpreting the economic profits.

Calculation of ratios

Ratios – commentary (blog)

Calculate economic profit

Commentary – drivers of economic

profit (blog)

Step 9

This task was quite interesting as it helped in learning

not only financial concepts but also the excel

functions. I observed that few student put in wrong

function of calculating NPV resulting in wrong

solution. IRR and Payback period was correctly

computed by many students. I also learned good points

regarding presentation by reviewing the work of

others.

Develop capital investment decision

for your firm

Calculation of payback period, NPV &

IRR

Recommendation & discussion

Step 10

I had one on one conversation with the students which

helped in passing individual feedbacks. It was a good

learning curve for all of us.

Individual feedback with other

students

Overall ASS#3 Overall, this assessment proved to be a pioneer in

terms of learning the concepts of financial reporting,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial analysis, and capital budgeting.

8

8

References

Hill, T. (2017). Manufacturing strategy: the strategic management of the manufacturing

function. Macmillan International Higher Education.

Hoyle, J. B., Schaefer, T., & Doupnik, T. (2015). Advanced accounting. McGraw Hill.

Ittner, C. D., & Michels, J. (2017). Risk-based forecasting and planning and management

earnings forecasts. Review of Accounting Studies, 22(3), 1005-1047.

Kim, J. B., Li, L., Lu, L. Y., & Yu, Y. (2016). Financial statement comparability and expected

crash risk. Journal of Accounting and Economics, 61(2-3), 294-312.

Shapiro. 2008. Capital Budgeting and Investment Analysis. Pearson Education India.

Tracy, E. 2012. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to

Analyse Any Business on the Planet. RatioAnalysis.net.

9

Hill, T. (2017). Manufacturing strategy: the strategic management of the manufacturing

function. Macmillan International Higher Education.

Hoyle, J. B., Schaefer, T., & Doupnik, T. (2015). Advanced accounting. McGraw Hill.

Ittner, C. D., & Michels, J. (2017). Risk-based forecasting and planning and management

earnings forecasts. Review of Accounting Studies, 22(3), 1005-1047.

Kim, J. B., Li, L., Lu, L. Y., & Yu, Y. (2016). Financial statement comparability and expected

crash risk. Journal of Accounting and Economics, 61(2-3), 294-312.

Shapiro. 2008. Capital Budgeting and Investment Analysis. Pearson Education India.

Tracy, E. 2012. Ratio Analysis Fundamentals: How 17 Financial Ratios Can Allow You to

Analyse Any Business on the Planet. RatioAnalysis.net.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

![Financial Statement Analysis Homework - [University Name] - Semester 1](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fpl%2F94032add73c5467f81c103edfc1a6f31.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.