BIZ201 Case Study: Crystal Hotel Financial Performance Analysis

VerifiedAdded on 2023/01/16

|15

|2988

|23

Case Study

AI Summary

This case study analyzes the financial statements of Crystal Hotel Pty Ltd for the period ending June 30, 2015. It includes a vertical analysis of the profit and loss account and the statement of financial position, calculating percentages for various revenue and expense items. Key financial ratios, including profitability, efficiency, liquidity, and solvency ratios, are calculated and compared to industry benchmarks. The analysis also includes a comparative analysis of the income statement, highlighting revenue sources, cost of sales, personnel costs, and operating costs. The study evaluates Crystal Hotel's financial performance, identifying strengths and weaknesses, and provides recommendations for improvement, focusing on cost management and revenue optimization. The case study assesses the company's profitability, efficiency in managing assets and liabilities, and overall financial stability, providing a comprehensive overview of Crystal Hotel's financial health.

Running head: ACCOUNTING STATEMENT ANALYSIS

Accounting Statement Analysis

Name of the Student

Name of the University

Authors Note

Course ID

Accounting Statement Analysis

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING STATEMENT ANALYSIS

Table of Contents

Part 1..........................................................................................................................................2

Vertical Analysis of Profit and Loss Account........................................................................2

Vertical Analysis of Statement of Financial Position:...........................................................4

Calculation of Key Financial Ratios:.....................................................................................6

Part 2:.........................................................................................................................................6

Analysis of information included in the general purpose financial statements:....................6

Comparative Analysis of Income Statement:.........................................................................7

Ratio Analysis:...........................................................................................................................9

Profitability Ratios:................................................................................................................9

Efficiency Ratios:...................................................................................................................9

Liquidity ratios:....................................................................................................................10

Solvency Ratios:...................................................................................................................10

Additional industry specific benchmarks:............................................................................11

References................................................................................................................................12

Table of Contents

Part 1..........................................................................................................................................2

Vertical Analysis of Profit and Loss Account........................................................................2

Vertical Analysis of Statement of Financial Position:...........................................................4

Calculation of Key Financial Ratios:.....................................................................................6

Part 2:.........................................................................................................................................6

Analysis of information included in the general purpose financial statements:....................6

Comparative Analysis of Income Statement:.........................................................................7

Ratio Analysis:...........................................................................................................................9

Profitability Ratios:................................................................................................................9

Efficiency Ratios:...................................................................................................................9

Liquidity ratios:....................................................................................................................10

Solvency Ratios:...................................................................................................................10

Additional industry specific benchmarks:............................................................................11

References................................................................................................................................12

2ACCOUNTING STATEMENT ANALYSIS

Part 1

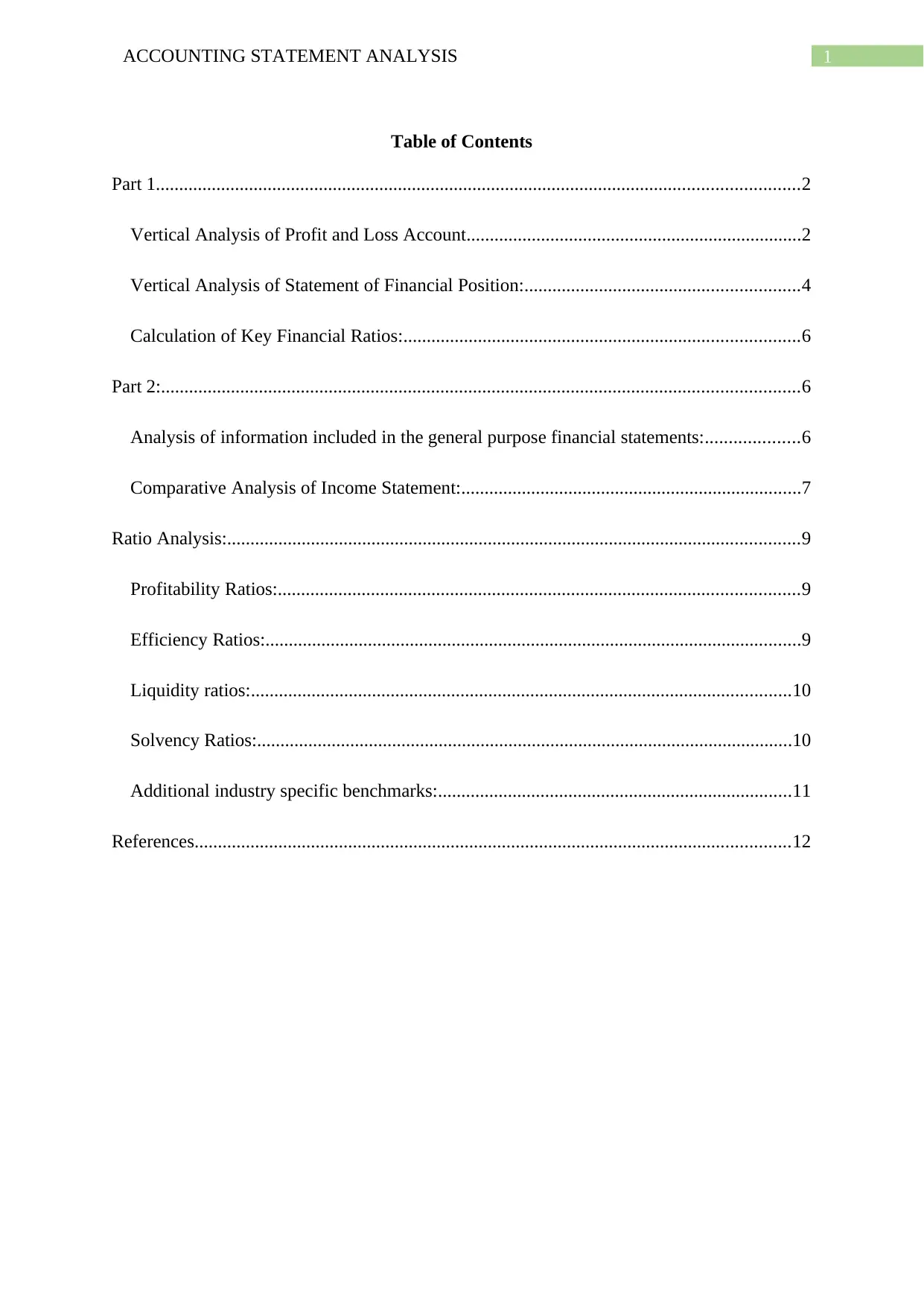

Vertical Analysis of Profit and Loss Account

Revenue

Rooms Revenue $40,06,920 61.88%

Food and Beverage Revenue $9,36,497 14.46%

Functions $9,60,326 14.83%

Other Revenue $5,71,906 8.83%

Total Revenue $64,75,650 100%

Cost of Sales

Rooms Cost of Sales $8,44,634 13.04%

Food and Beverage Cost of Sales $8,07,461 12.47%

Other Cost of Sales $1,34,636 2.08%

Total Cost of Sales ( excluding personnel cost) $17,86,731 27.59%

Gross Profit $46,88,919 72.41%

Personnel Costs

Rooms $4,92,078 7.60%

Food and Beverage $4,58,716 7.08%

Administrative and General $2,97,868 4.60%

Sales and Marketing $2,22,209 3.43%

Property Management and Maintenance $1,72,763 2.67%

Total Personnel Costs $16,43,634 25.38%

Crystal Hotel Pty Ltd

Statement of Profit or Loss

For the period ended 30/ 06/ 2015

Vertical

Analysis

Part 1

Vertical Analysis of Profit and Loss Account

Revenue

Rooms Revenue $40,06,920 61.88%

Food and Beverage Revenue $9,36,497 14.46%

Functions $9,60,326 14.83%

Other Revenue $5,71,906 8.83%

Total Revenue $64,75,650 100%

Cost of Sales

Rooms Cost of Sales $8,44,634 13.04%

Food and Beverage Cost of Sales $8,07,461 12.47%

Other Cost of Sales $1,34,636 2.08%

Total Cost of Sales ( excluding personnel cost) $17,86,731 27.59%

Gross Profit $46,88,919 72.41%

Personnel Costs

Rooms $4,92,078 7.60%

Food and Beverage $4,58,716 7.08%

Administrative and General $2,97,868 4.60%

Sales and Marketing $2,22,209 3.43%

Property Management and Maintenance $1,72,763 2.67%

Total Personnel Costs $16,43,634 25.38%

Crystal Hotel Pty Ltd

Statement of Profit or Loss

For the period ended 30/ 06/ 2015

Vertical

Analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING STATEMENT ANALYSIS

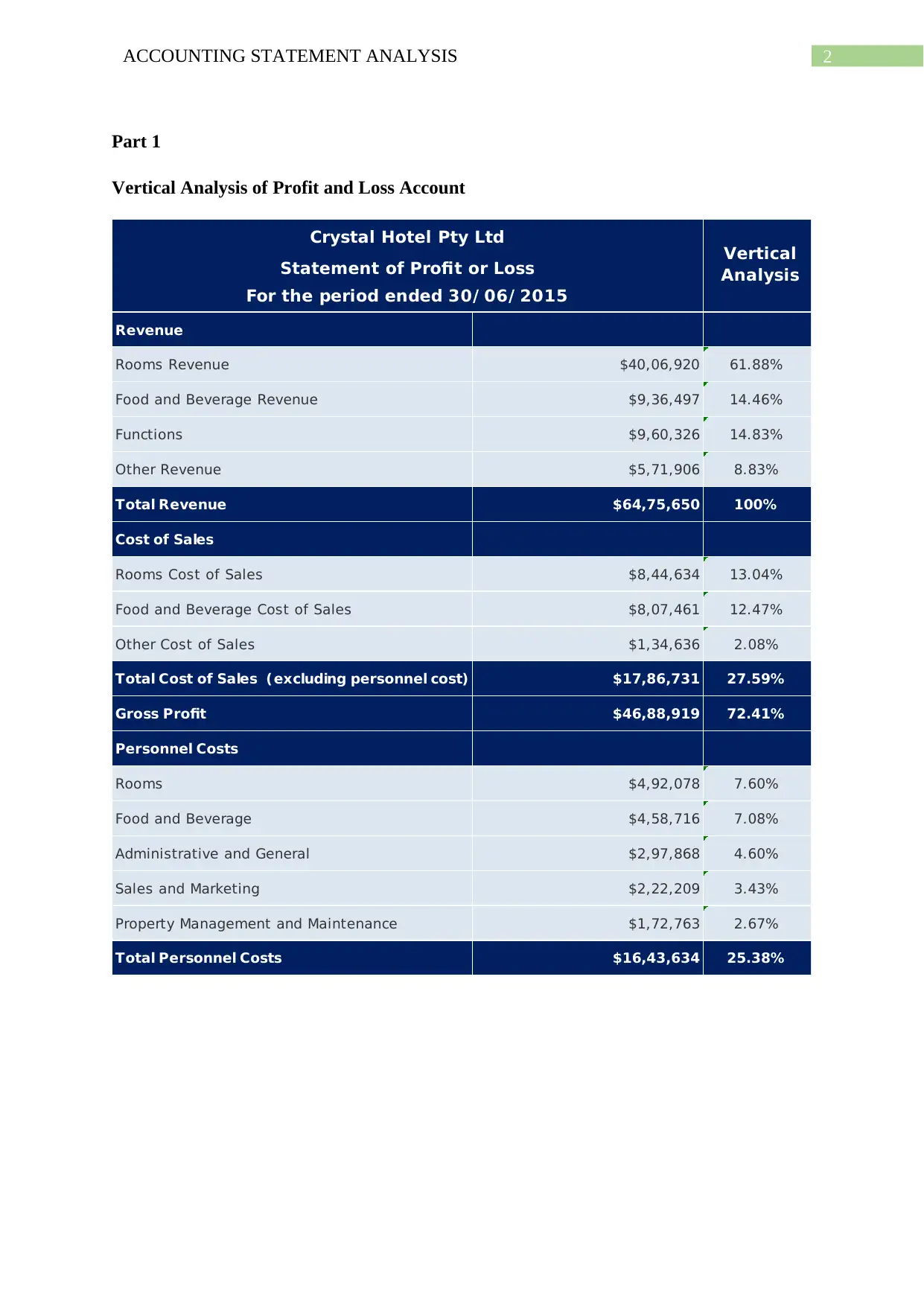

Unallocated Operating Costs

Administrative and General $4,38,461 6.77%

I nformation Systems $3,574 0.06%

Sales and Marketing $2,00,167 3.09%

Security $53,616 0.83%

Transportation $81,020 1.25%

Property Operations and Maintenance $2,91,911 4.51%

Utilities $1,16,764 1.80%

Total Undistributed Operating Costs $11,85,514 18.31%

Operating Profit $18,59,770 28.72%

I nsurance Expense $27,404 0.42%

Depreciation and Amortisation $45,276 0.70%

I ncome Before I nterest and Tax $17,87,090 27.60%

I nterest Expense $29,787 0.46%

I ncome Before I ncome Taxes $17,57,304 27.14%

I ncome Taxes $4,92,554 7.61%

Net Profit $12,64,750 19.53%

Unallocated Operating Costs

Administrative and General $4,38,461 6.77%

I nformation Systems $3,574 0.06%

Sales and Marketing $2,00,167 3.09%

Security $53,616 0.83%

Transportation $81,020 1.25%

Property Operations and Maintenance $2,91,911 4.51%

Utilities $1,16,764 1.80%

Total Undistributed Operating Costs $11,85,514 18.31%

Operating Profit $18,59,770 28.72%

I nsurance Expense $27,404 0.42%

Depreciation and Amortisation $45,276 0.70%

I ncome Before I nterest and Tax $17,87,090 27.60%

I nterest Expense $29,787 0.46%

I ncome Before I ncome Taxes $17,57,304 27.14%

I ncome Taxes $4,92,554 7.61%

Net Profit $12,64,750 19.53%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING STATEMENT ANALYSIS

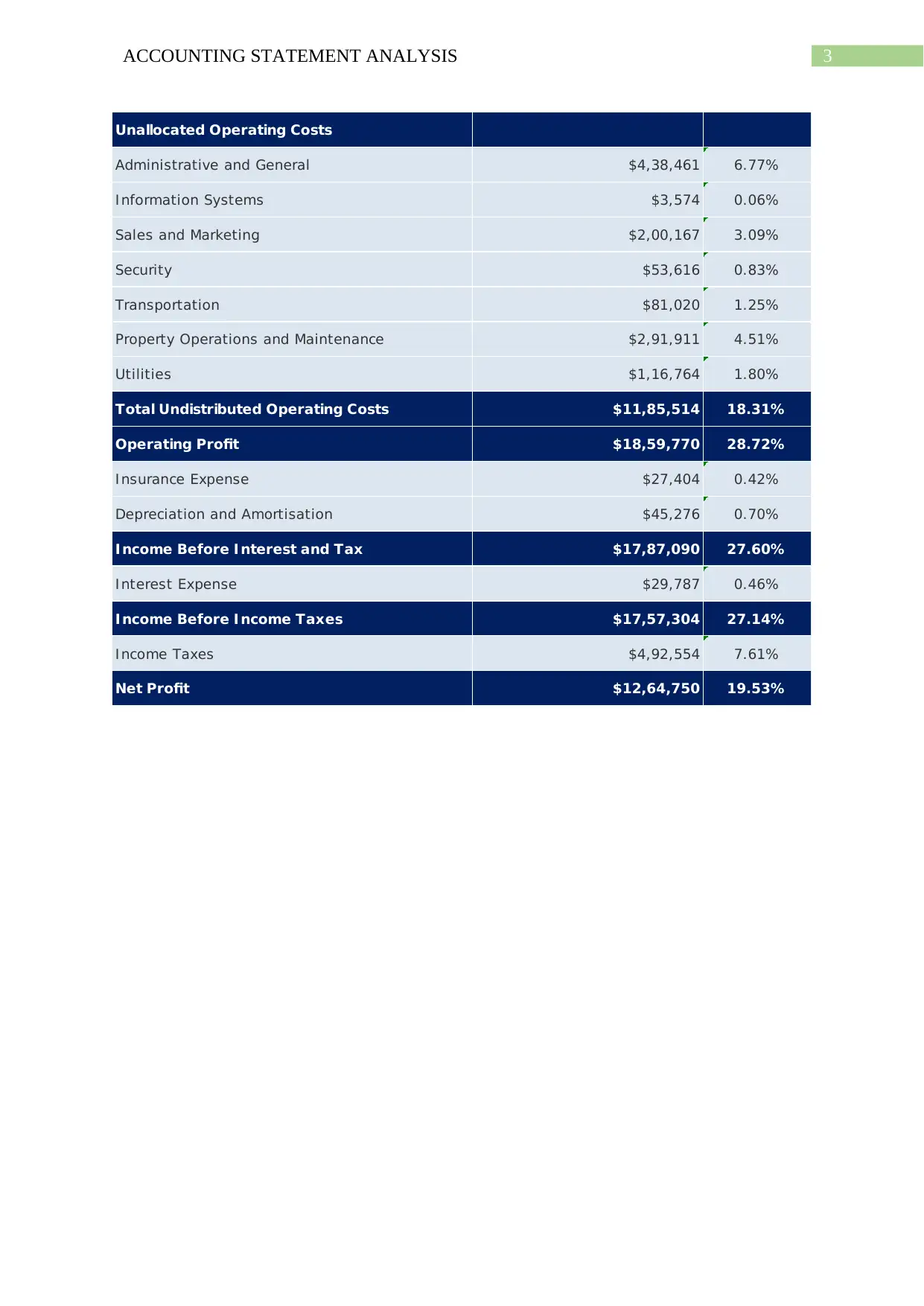

Vertical Analysis of Statement of Financial Position:

Current Assets

Cash and Cash Equivalents $7,10,535 12.76%

Accounts Receivable $6,99,930 12.57%

I nventory $2,43,915 4.38%

Pre-paid Expenses $1,31,715 2.37%

Total Current Assets $17,86,095 32.09%

Non Current Assets

Property, Plant & Equipment $27,83,810 50.01%

I ntangible Assets $7,30,621 13.13%

Vehicles $1,27,260 2.29%

Other Non-current Assets $1,38,634 2.49%

Total Non-Current Assets $37,80,325 67.91%

Total Assets $55,66,420 100%

Crystal Hotel Pty Ltd

Statement of Financial Position

at at 30/ 06/ 2015

Vertical

Analysis

Current Liabilities

Bank Overdraft $13,786 0.25%

Accounts Payable $2,79,935 5.03%

Provisions $1,59,075 2.86%

Other Current Liabilities $5,09,994 9.16%

Total Current Liabilities $9,62,790 17.30%

Non Current Liabilities

Loans $5,05,000 9.07%

Total Non Current Liabilities $5,05,000 9.07%

Total Liabilities $14,67,790 26.37%

Vertical Analysis of Statement of Financial Position:

Current Assets

Cash and Cash Equivalents $7,10,535 12.76%

Accounts Receivable $6,99,930 12.57%

I nventory $2,43,915 4.38%

Pre-paid Expenses $1,31,715 2.37%

Total Current Assets $17,86,095 32.09%

Non Current Assets

Property, Plant & Equipment $27,83,810 50.01%

I ntangible Assets $7,30,621 13.13%

Vehicles $1,27,260 2.29%

Other Non-current Assets $1,38,634 2.49%

Total Non-Current Assets $37,80,325 67.91%

Total Assets $55,66,420 100%

Crystal Hotel Pty Ltd

Statement of Financial Position

at at 30/ 06/ 2015

Vertical

Analysis

Current Liabilities

Bank Overdraft $13,786 0.25%

Accounts Payable $2,79,935 5.03%

Provisions $1,59,075 2.86%

Other Current Liabilities $5,09,994 9.16%

Total Current Liabilities $9,62,790 17.30%

Non Current Liabilities

Loans $5,05,000 9.07%

Total Non Current Liabilities $5,05,000 9.07%

Total Liabilities $14,67,790 26.37%

5ACCOUNTING STATEMENT ANALYSIS

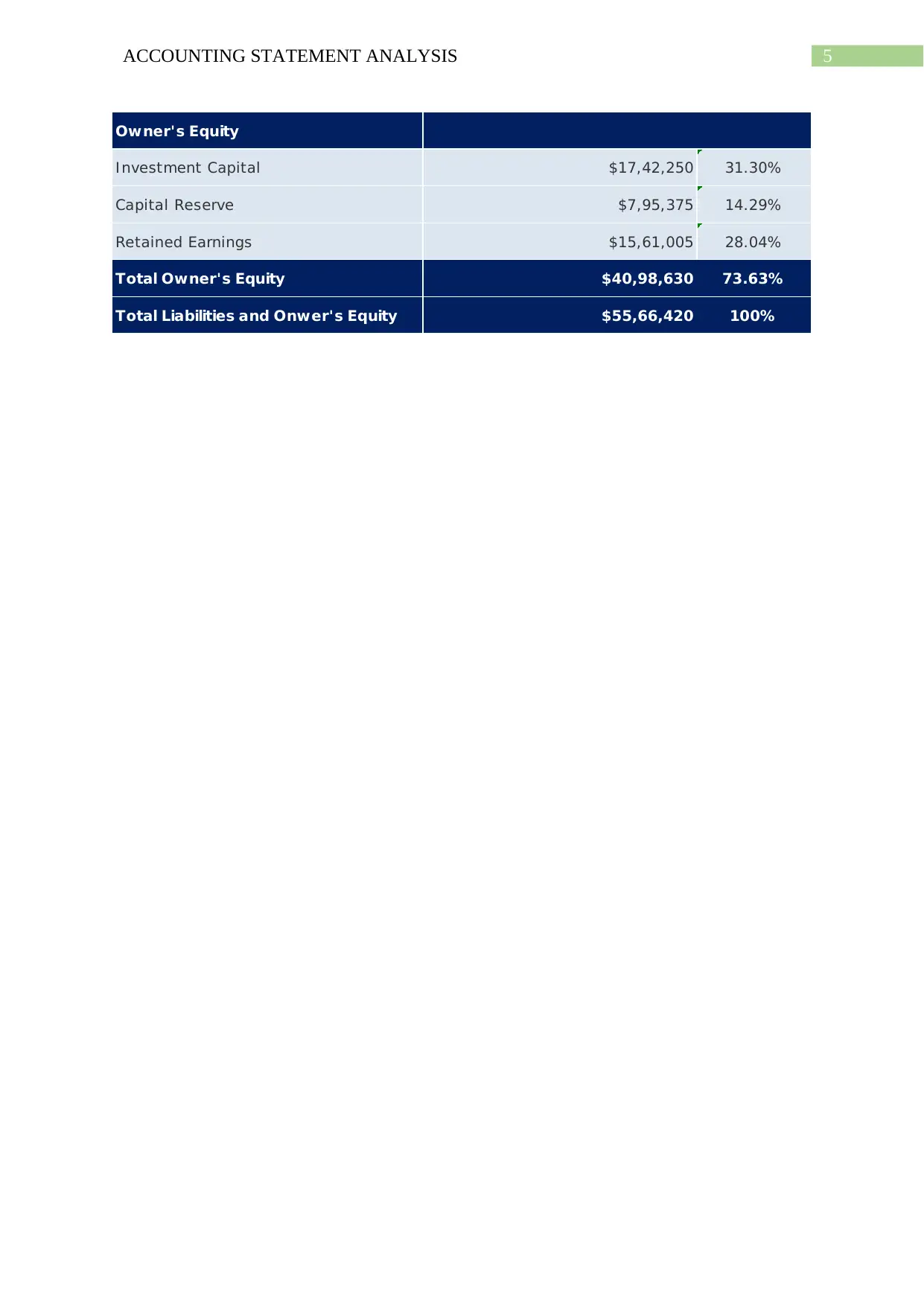

Owner's Equity

I nvestment Capital $17,42,250 31.30%

Capital Reserve $7,95,375 14.29%

Retained Earnings $15,61,005 28.04%

Total Owner's Equity $40,98,630 73.63%

Total Liabilities and Onwer's Equity $55,66,420 100%

Owner's Equity

I nvestment Capital $17,42,250 31.30%

Capital Reserve $7,95,375 14.29%

Retained Earnings $15,61,005 28.04%

Total Owner's Equity $40,98,630 73.63%

Total Liabilities and Onwer's Equity $55,66,420 100%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING STATEMENT ANALYSIS

Calculation of Key Financial Ratios:

Profitability Ratios 2015 I ndustry

Gross Profit Margin 72.41% 81%

Net Profit Margin 19.53% 11%

Return on Assets 22.72% 8%

Return on Equity 30.86% 9%

Efficiency Ratios

I nventory Turnover 1.65 8.60

Number of days I nventory Held 221.08

Accounts Receivable Turnover 0.95

Accounts Receivable Collection Period 382.68 35.00

Liquidity Ratios

Current ratio 1.86 3.20

Quick Ratio 1.46 2.12

Solvency Ratios

Debt to Equity Ratio 35.81%

Debt Ratio 26.37%

Equity Ratio 73.63%

I nterest Coverage 1.67%

Part 2:

Analysis of information included in the general purpose financial statements:

The financial information that are included into the statement of financial position and

profit & loss account is known as general purpose financial statement because it comprises of

Calculation of Key Financial Ratios:

Profitability Ratios 2015 I ndustry

Gross Profit Margin 72.41% 81%

Net Profit Margin 19.53% 11%

Return on Assets 22.72% 8%

Return on Equity 30.86% 9%

Efficiency Ratios

I nventory Turnover 1.65 8.60

Number of days I nventory Held 221.08

Accounts Receivable Turnover 0.95

Accounts Receivable Collection Period 382.68 35.00

Liquidity Ratios

Current ratio 1.86 3.20

Quick Ratio 1.46 2.12

Solvency Ratios

Debt to Equity Ratio 35.81%

Debt Ratio 26.37%

Equity Ratio 73.63%

I nterest Coverage 1.67%

Part 2:

Analysis of information included in the general purpose financial statements:

The financial information that are included into the statement of financial position and

profit & loss account is known as general purpose financial statement because it comprises of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING STATEMENT ANALYSIS

fundamental information which can be used by numerous users such as lenders, stakeholders,

creditors and investors (Hoyle et al., 2015). Vertical analysis gives the business with the

opportunity of calculating the percentage of different items that are based on the particular

base that are pre-determined. This method is treated as useful for assessing the growth and

development of business. For Crystal Hotel, a vertical analysis of income statement and

statement of financial position is performed. The base that are considered in profit and loss

account is the Total revenue reported by the company, while for the statement of financial

position the total assets and total liabilities are considered as base figure. A comparative

analysis of the percentage obtained is performed with the industry average standard.

Comparative Analysis of Income Statement:

Income statement is regarded as one of the three vital financial statements which is

used for reporting the financial performance of the company over the particular accounting

period (Nobes, 2014). The comparative Profit and Loss analysis explains the way through

which Crystal Hotel produces revenues and incurs expenses. The Profit and Loss account of

Crystal Hotel states that a major portion of 61.88% is occupied by the total revenues

produced through room revenues while the industry benchmark stands 51%. Crystal Hotel

has been successful in producing greater revenue through room charges as compared to the

industry benchmark. While the average revenue per rooms for the year 2015 stands 47%. The

industry standards for F&B average price stood 41 and Halls accounted for 8% in 2015 as

compared to the 61.88% of the total revenues reported by Crystal Hotel.

Similarly, the cost of sales for Crystal Hotel accounted for 27.59% leading to profit of

72.41%. In contrast the industry benchmark for cost of sales stands 20% resulting in the gross

profit of 80%. While the industrial benchmark for the vertical analysis of Profit and Loss

accounts states that the total cost of sales per room stands at an average of 20. Comparatively,

the cost of sales for Crystal Hotel is greater than the industry standard. This signifies that the

fundamental information which can be used by numerous users such as lenders, stakeholders,

creditors and investors (Hoyle et al., 2015). Vertical analysis gives the business with the

opportunity of calculating the percentage of different items that are based on the particular

base that are pre-determined. This method is treated as useful for assessing the growth and

development of business. For Crystal Hotel, a vertical analysis of income statement and

statement of financial position is performed. The base that are considered in profit and loss

account is the Total revenue reported by the company, while for the statement of financial

position the total assets and total liabilities are considered as base figure. A comparative

analysis of the percentage obtained is performed with the industry average standard.

Comparative Analysis of Income Statement:

Income statement is regarded as one of the three vital financial statements which is

used for reporting the financial performance of the company over the particular accounting

period (Nobes, 2014). The comparative Profit and Loss analysis explains the way through

which Crystal Hotel produces revenues and incurs expenses. The Profit and Loss account of

Crystal Hotel states that a major portion of 61.88% is occupied by the total revenues

produced through room revenues while the industry benchmark stands 51%. Crystal Hotel

has been successful in producing greater revenue through room charges as compared to the

industry benchmark. While the average revenue per rooms for the year 2015 stands 47%. The

industry standards for F&B average price stood 41 and Halls accounted for 8% in 2015 as

compared to the 61.88% of the total revenues reported by Crystal Hotel.

Similarly, the cost of sales for Crystal Hotel accounted for 27.59% leading to profit of

72.41%. In contrast the industry benchmark for cost of sales stands 20% resulting in the gross

profit of 80%. While the industrial benchmark for the vertical analysis of Profit and Loss

accounts states that the total cost of sales per room stands at an average of 20. Comparatively,

the cost of sales for Crystal Hotel is greater than the industry standard. This signifies that the

8ACCOUNTING STATEMENT ANALYSIS

Crystal Hotel has not been successful in negotiating on terms with the suppliers. Furthermore,

it is also assumed that the company has been holding back its inventories instead of quickly

turning its inventories all through the year.

Taking into account the total personal costs for Crystal Hotel it stands 25.38% of total

revenues while the industry benchmark stands 35% of total revenues. The average total

personal costs in terms of the industry standard for each room stands 43%. Therefore, the

total personnel costs for Crystal Hotel is superior in contrast to the industry standard. The

total undistributed operation cost for Crystal Hotel for 2015 stands 18.31% of the total

revenues in contrast the industry standard of 15%. Furthermore, the average total unallocated

costs for the year 2015 accounted for 18%. Therefore, the total amount of undistributed

operational cost for Crystal Hotel is marginally superior than the present industry standard

(Warren & Jones, 2018).

Finally, on considering the total cost of the Crystal Hotel the company reported the

total costs prior to fixed charges of 71.28% of the revenues that amounted to 28.72%

operational profit or profit before the fixed charges. In contrast to this, the industry standard

for the total costs amounts to 74% leading to 26% of the total revenues as the income prior to

the fixed costs. Simultaneously, the average total costs for the rooms during the year 2015

stands 81% with income before fixed charges for the year 2015 standing 19%. The analysis

suggests that the fixed charges for Crystal in terms of both industry standard and average cost

per room is superior which suggest that it is producing adequate profits to support its

operations.

Taking into the account the sales proceeds and expenditure of Crystal Hotels for the

financial year ended 2015 it is understood that the profitability position of the Crystal Hotel

stands superior in contrast to the industry standard. Furthermore, to further enhance the

Crystal Hotel has not been successful in negotiating on terms with the suppliers. Furthermore,

it is also assumed that the company has been holding back its inventories instead of quickly

turning its inventories all through the year.

Taking into account the total personal costs for Crystal Hotel it stands 25.38% of total

revenues while the industry benchmark stands 35% of total revenues. The average total

personal costs in terms of the industry standard for each room stands 43%. Therefore, the

total personnel costs for Crystal Hotel is superior in contrast to the industry standard. The

total undistributed operation cost for Crystal Hotel for 2015 stands 18.31% of the total

revenues in contrast the industry standard of 15%. Furthermore, the average total unallocated

costs for the year 2015 accounted for 18%. Therefore, the total amount of undistributed

operational cost for Crystal Hotel is marginally superior than the present industry standard

(Warren & Jones, 2018).

Finally, on considering the total cost of the Crystal Hotel the company reported the

total costs prior to fixed charges of 71.28% of the revenues that amounted to 28.72%

operational profit or profit before the fixed charges. In contrast to this, the industry standard

for the total costs amounts to 74% leading to 26% of the total revenues as the income prior to

the fixed costs. Simultaneously, the average total costs for the rooms during the year 2015

stands 81% with income before fixed charges for the year 2015 standing 19%. The analysis

suggests that the fixed charges for Crystal in terms of both industry standard and average cost

per room is superior which suggest that it is producing adequate profits to support its

operations.

Taking into the account the sales proceeds and expenditure of Crystal Hotels for the

financial year ended 2015 it is understood that the profitability position of the Crystal Hotel

stands superior in contrast to the industry standard. Furthermore, to further enhance the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING STATEMENT ANALYSIS

profitability position of the company a recommendation can be made where Crystal Hotel

should make an attempt to minimize the cost of sales in comparison to the industry

benchmark (Kimmel et al., 2016). The cost of sales for the room, foods and beverage can be

reduced as it presently stands 13.04% and 12.47% of the total revenues. To further improve

the business structure of Crystal Hotel below stated are the following recommendations;

a. The services related to food and beverage operating in the current industry appears to

be higher than the industry average (Barth, 2015). The management should undertake

the necessary amendments in the food and beverage services as this would help in

deriving maximum amount of revenues and contributing towards business’s total

revenue.

b. The vertical analysis represents that the cost of sales for Crystal Hotel is higher and

requires significant improvement in the operational structure.

c. The company incurs significant amount of undistributed costs and security

expenditure. These costs needs to be minimized where the overall business of

revenues would be improved simultaneously.

Ratio Analysis:

Ratio analysis can be defined as the quantitative method of obtaining an insight into

the organization’s liquidity position, operational effectiveness and profitability by performing

a comparative analysis of the information in the financial statement (Nilsson &

Stockenstrand, 2015).

Profitability Ratios:

Profitability ratios is regarded as the useful procedure of measuring the organization’s

performance (Macve, 2015). The gross profit margin for Crystal Hotel in 2015 stood 72.41%

while the industry standard stood 81%. While the net profit margin stood 19.53% for the

profitability position of the company a recommendation can be made where Crystal Hotel

should make an attempt to minimize the cost of sales in comparison to the industry

benchmark (Kimmel et al., 2016). The cost of sales for the room, foods and beverage can be

reduced as it presently stands 13.04% and 12.47% of the total revenues. To further improve

the business structure of Crystal Hotel below stated are the following recommendations;

a. The services related to food and beverage operating in the current industry appears to

be higher than the industry average (Barth, 2015). The management should undertake

the necessary amendments in the food and beverage services as this would help in

deriving maximum amount of revenues and contributing towards business’s total

revenue.

b. The vertical analysis represents that the cost of sales for Crystal Hotel is higher and

requires significant improvement in the operational structure.

c. The company incurs significant amount of undistributed costs and security

expenditure. These costs needs to be minimized where the overall business of

revenues would be improved simultaneously.

Ratio Analysis:

Ratio analysis can be defined as the quantitative method of obtaining an insight into

the organization’s liquidity position, operational effectiveness and profitability by performing

a comparative analysis of the information in the financial statement (Nilsson &

Stockenstrand, 2015).

Profitability Ratios:

Profitability ratios is regarded as the useful procedure of measuring the organization’s

performance (Macve, 2015). The gross profit margin for Crystal Hotel in 2015 stood 72.41%

while the industry standard stood 81%. While the net profit margin stood 19.53% for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING STATEMENT ANALYSIS

company with the industry standard being 11%. The ratio signifies that Crystal hotel is

successful in selling its inventory at greater profit.

The return on assets for Crystal hotel in 2015 stood 23.37% while the return on equity

stood 32.85%. The industry standard stood 8% and 9% respectively. The higher ROA of

Crystal hotel can be considered more favourable to the investors as it displays that the

company is highly effective in managing its assets for producing higher net profit (Henderson

et al., 2015). The ROE of crystal hotel shows that the company uses the money of

shareholders effectively to produce profits.

Efficiency Ratios:

Efficiency ratio is useful in assessing whether the company is effectively using is

assets and liabilities internally (Robinson et al., 2015). The inventory turnover for Crystal

hotel in 2015 was 6.60 while industry standard was 8.60 times. The number of days’

inventory held stood 55.27 days which signifies that Crystal hotel is holding too much of the

inventory in comparison to its sales. The accounts receivable turnover in 2015 stood 3.82

while the accounts receivable collection period stood 95.67 days with industry standard being

35.00. The ratio stands greater than the industry standard which makes sense that the

company is not effectively and frequently collecting its receivables. Crystal collection of

accounts receivables is not efficient which indicates that higher proportion of quality

customers are not paying their debts quickly.

Liquidity ratios:

The liquidity ratio is regarded as the class of financial metrics that is used to ascertain

the ability of the debtors to pay its current obligation of debt without raising any kind of

external debt (Dicle & Meyer, 2018). The current ratio here for crystal hotel is computed to

determine the ability of the organization in paying off its short term debt obligations. For the

company with the industry standard being 11%. The ratio signifies that Crystal hotel is

successful in selling its inventory at greater profit.

The return on assets for Crystal hotel in 2015 stood 23.37% while the return on equity

stood 32.85%. The industry standard stood 8% and 9% respectively. The higher ROA of

Crystal hotel can be considered more favourable to the investors as it displays that the

company is highly effective in managing its assets for producing higher net profit (Henderson

et al., 2015). The ROE of crystal hotel shows that the company uses the money of

shareholders effectively to produce profits.

Efficiency Ratios:

Efficiency ratio is useful in assessing whether the company is effectively using is

assets and liabilities internally (Robinson et al., 2015). The inventory turnover for Crystal

hotel in 2015 was 6.60 while industry standard was 8.60 times. The number of days’

inventory held stood 55.27 days which signifies that Crystal hotel is holding too much of the

inventory in comparison to its sales. The accounts receivable turnover in 2015 stood 3.82

while the accounts receivable collection period stood 95.67 days with industry standard being

35.00. The ratio stands greater than the industry standard which makes sense that the

company is not effectively and frequently collecting its receivables. Crystal collection of

accounts receivables is not efficient which indicates that higher proportion of quality

customers are not paying their debts quickly.

Liquidity ratios:

The liquidity ratio is regarded as the class of financial metrics that is used to ascertain

the ability of the debtors to pay its current obligation of debt without raising any kind of

external debt (Dicle & Meyer, 2018). The current ratio here for crystal hotel is computed to

determine the ability of the organization in paying off its short term debt obligations. For the

11ACCOUNTING STATEMENT ANALYSIS

financial year ended 2015 the current ratio for Crystal Hotel stood 1.86 while the industry

standard stood 3.20. This signifies that the company may struggle to pay its current liabilities.

The quick ratio for Crystal Hotel in 2015 stood 1.46 however the industry standard

stood as high as 2.12. Similar to current ratio the quick ratio too appears feeble and Crystal

hotel may have to sell off its fixed assets to pay its debt obligations and it is not making

sufficient operations to support their activities. This can be attributed due to poor accounts

receivables collection period.

Solvency Ratios:

The solvency ratio is regarded as the key metric which is used to assess the ability of

the company in satisfying its debt obligations and it is used regularly by the prospective

business lenders (Hermason et al., 2016). The debt to equity ratio for Crystal Hotel in 2015

stood 35.81%. The lower ratio is good indicator that Crystal hotel is financially more stable

business and less risky. Similarly, the debt ratio for Crystal hotel stands 26.37% in 2015. The

lower debt ratio signifies the longevity of the business with overall lower burden of debt. The

equity ratio for Crystal hotel in 2015 stood at 73.63%. The higher ratio signifies that the

company demonstrates potential to credits with greater sustainability and less risky towards

future loans. The interest coverage ratio in 2015 was 59 times which signifies that it can

afford to make the principle payments. The ratio appears less risky to the creditors and the

banks may be more comfortable with the number.

Additional industry specific benchmarks:

There are numerous ways by which the company can perform the comparative

analysis through the industry benchmarks which are as follows;

Horizontal Analysis: The horizontal analysis is regarded as the financial statement analysis

techniques that can be used by Crystal Hotel. It is the useful tool that would help in

financial year ended 2015 the current ratio for Crystal Hotel stood 1.86 while the industry

standard stood 3.20. This signifies that the company may struggle to pay its current liabilities.

The quick ratio for Crystal Hotel in 2015 stood 1.46 however the industry standard

stood as high as 2.12. Similar to current ratio the quick ratio too appears feeble and Crystal

hotel may have to sell off its fixed assets to pay its debt obligations and it is not making

sufficient operations to support their activities. This can be attributed due to poor accounts

receivables collection period.

Solvency Ratios:

The solvency ratio is regarded as the key metric which is used to assess the ability of

the company in satisfying its debt obligations and it is used regularly by the prospective

business lenders (Hermason et al., 2016). The debt to equity ratio for Crystal Hotel in 2015

stood 35.81%. The lower ratio is good indicator that Crystal hotel is financially more stable

business and less risky. Similarly, the debt ratio for Crystal hotel stands 26.37% in 2015. The

lower debt ratio signifies the longevity of the business with overall lower burden of debt. The

equity ratio for Crystal hotel in 2015 stood at 73.63%. The higher ratio signifies that the

company demonstrates potential to credits with greater sustainability and less risky towards

future loans. The interest coverage ratio in 2015 was 59 times which signifies that it can

afford to make the principle payments. The ratio appears less risky to the creditors and the

banks may be more comfortable with the number.

Additional industry specific benchmarks:

There are numerous ways by which the company can perform the comparative

analysis through the industry benchmarks which are as follows;

Horizontal Analysis: The horizontal analysis is regarded as the financial statement analysis

techniques that can be used by Crystal Hotel. It is the useful tool that would help in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.