Accounting System and Process

VerifiedAdded on 2023/03/20

|18

|3564

|60

AI Summary

This document provides an in-depth analysis of accounting systems and processes, including inventory systems, perpetual inventory system, periodic inventory system, and Xero cloud based accounting information system. It discusses the advantages and disadvantages of each system and provides recommendations for adoption. The document also includes a memo, report, and letter related to accounting systems and processes.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING SYSTEM AND PROCESS

Accounting System and Process

Name of the Student:

Name of the University:

Author’s Note:

Accounting System and Process

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING SYSTEM AND PROCESS

Table of Contents

Answer to question 1: Memo:..........................................................................................................2

Answer to question 2: Report:.........................................................................................................6

Introduction:................................................................................................................................6

Computerized Accounting Information System:.........................................................................6

Xero Cloud based accounting information system:.....................................................................7

Advantages of Xero Cloud based accounting information system:.............................................7

Disadvantages of Xero Accounting information system:............................................................8

Adoption of the Xero Accounting information system:..............................................................8

Conclusion:..................................................................................................................................9

Answer to question 3: Letter:........................................................................................................10

Answer to question 4: Bank Reconciliation:.................................................................................13

Sub part (i):................................................................................................................................13

Sub part (ii):...............................................................................................................................13

Sub part (iii):..............................................................................................................................15

References and bibliography:........................................................................................................16

Table of Contents

Answer to question 1: Memo:..........................................................................................................2

Answer to question 2: Report:.........................................................................................................6

Introduction:................................................................................................................................6

Computerized Accounting Information System:.........................................................................6

Xero Cloud based accounting information system:.....................................................................7

Advantages of Xero Cloud based accounting information system:.............................................7

Disadvantages of Xero Accounting information system:............................................................8

Adoption of the Xero Accounting information system:..............................................................8

Conclusion:..................................................................................................................................9

Answer to question 3: Letter:........................................................................................................10

Answer to question 4: Bank Reconciliation:.................................................................................13

Sub part (i):................................................................................................................................13

Sub part (ii):...............................................................................................................................13

Sub part (iii):..............................................................................................................................15

References and bibliography:........................................................................................................16

2ACCOUNTING SYSTEM AND PROCESS

Answer to question 1: Memo:

MEMORANDUM

Date: 13 May 2019

To: Directors, Spotty Ltd

From: [Name, Designation]

Subject: Inventory System

Introduction:

This memorandum is prepared to explain various inventory systems and their application

in the business organization. Inventory system means inventory recording and controlling system

in the business practice. There are various concepts in the inventory management system. Such

as perpetual inventory, periodic inventory and Just in time inventory system. In this memo some

of such inventory systems have been explained in details to understand its use and importance in

the business.

Perpetual Inventory System:

Inventory system is recording and maintaining the inventory related transactions in the

books of accounts. There are various concepts in doing such work in business practice. One of

the most important concepts in inventory management and inventory system is the perpetual

inventory system. The main concept of the perpetual inventory system is to record the inventory

and to update the inventory records as and when any purchase of issue of inventory occurs. The

main theme of the perpetual inventory system is to record the purchase and sales of the inventory

as and when such purchase or sale happens. It recognizes the cost of goods sold as and when the

Answer to question 1: Memo:

MEMORANDUM

Date: 13 May 2019

To: Directors, Spotty Ltd

From: [Name, Designation]

Subject: Inventory System

Introduction:

This memorandum is prepared to explain various inventory systems and their application

in the business organization. Inventory system means inventory recording and controlling system

in the business practice. There are various concepts in the inventory management system. Such

as perpetual inventory, periodic inventory and Just in time inventory system. In this memo some

of such inventory systems have been explained in details to understand its use and importance in

the business.

Perpetual Inventory System:

Inventory system is recording and maintaining the inventory related transactions in the

books of accounts. There are various concepts in doing such work in business practice. One of

the most important concepts in inventory management and inventory system is the perpetual

inventory system. The main concept of the perpetual inventory system is to record the inventory

and to update the inventory records as and when any purchase of issue of inventory occurs. The

main theme of the perpetual inventory system is to record the purchase and sales of the inventory

as and when such purchase or sale happens. It recognizes the cost of goods sold as and when the

3ACCOUNTING SYSTEM AND PROCESS

sales transaction is recorded. Now the question may arise about the valuation of cost of goods

sold when recording the cost of goods sold entry in the books of accounts. The same problem

arises at the time of valuation of ending inventory. To solve that problem there are various

methods of inventory records that have been discussed in the following parts in this memo

(Chołodowicz & Orłowski 2016).

First-in-firs-out method:

First-in-first-out (FIFO) is a method of recording the inventory in the perpetual inventory

system. It requires the issue rice to be recorded on the first in first out basis. It implies the

materials, which are purchased earlier, would be issued earlier and the materials, which have

been purchased last, would be issued last. Therefore, in the first in first out method the oldest

materials are issued first then the recent materials are issued. It is only for the recording purpose,

and to consider the cost of materials for valuing the cost of goods sold. In this method the cost of

goods sold is valued at the oldest price and the closing inventory is valued at the latest price. At

the inflationary period, in this method there would be a low amount of cost of goods sold and a

high amount of closing inventory, which will be showing a high amount of profit. This method is

easy to account for but is not as effective and efficient as the weighted average method. In

business organizations, where the prices of inputs fluctuates frequently it is recommended to

adopt the FIFO method of inventory valuation (Kaplan & Atkinson 2015).

Weighted Average method:

Weighted average method of inventory valuation or record keeping is another important

method of inventory management or inventory record keeping. In this system, the issue prices

are valued at the weighted average price based on the last held inventory and their total price. In

sales transaction is recorded. Now the question may arise about the valuation of cost of goods

sold when recording the cost of goods sold entry in the books of accounts. The same problem

arises at the time of valuation of ending inventory. To solve that problem there are various

methods of inventory records that have been discussed in the following parts in this memo

(Chołodowicz & Orłowski 2016).

First-in-firs-out method:

First-in-first-out (FIFO) is a method of recording the inventory in the perpetual inventory

system. It requires the issue rice to be recorded on the first in first out basis. It implies the

materials, which are purchased earlier, would be issued earlier and the materials, which have

been purchased last, would be issued last. Therefore, in the first in first out method the oldest

materials are issued first then the recent materials are issued. It is only for the recording purpose,

and to consider the cost of materials for valuing the cost of goods sold. In this method the cost of

goods sold is valued at the oldest price and the closing inventory is valued at the latest price. At

the inflationary period, in this method there would be a low amount of cost of goods sold and a

high amount of closing inventory, which will be showing a high amount of profit. This method is

easy to account for but is not as effective and efficient as the weighted average method. In

business organizations, where the prices of inputs fluctuates frequently it is recommended to

adopt the FIFO method of inventory valuation (Kaplan & Atkinson 2015).

Weighted Average method:

Weighted average method of inventory valuation or record keeping is another important

method of inventory management or inventory record keeping. In this system, the issue prices

are valued at the weighted average price based on the last held inventory and their total price. In

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING SYSTEM AND PROCESS

this method, the issue price is computed by dividing the total cost of inventory by the total

quantity of the inventory held. It is a more rational and scientific method of inventory record

keeping, it considers the most recent as well as the historical price for valuing the cost of goods

sold and inventory (Kaplan & Atkinson 2015). In the inflationary period, there would not be

much effect on the profitability for this method of inventory valuation. It can be applied in

manufacturing business where the stocks are held for a considerable period of time and the prices

of inputs do not fluctuate frequently (Chołodowicz & Orłowski 2016).

Periodic Inventory System:

Periodic inventory system is another method of inventory management and inventory

control system. In this method only the purchase of inventory is recorded as and when the

purchase transaction takes place, but no cost of goods sold entry is made at that time. In this

method, the cost of goods sold is determined by comparing the opening inventory, sot of

purchase of materials and the closing inventory. To compute the cost of goods sold, the cost of

purchase of materials is added with the opening inventory and then the closing inventory is

deducted from to get the value of cost of goods sold. This is a less effective and less rational

method of inventory management and inventory control system (Kaplan & Atkinson 2015).

Conclusion:

From the above discussion and analysis it can be concluded that, there are various

inventory management system which can be used in business practice to record inventory and to

control and manage the inventory system. The periodic inventory system considers overall

movement in the inventory for inventory valuation and valuation of cost of goods sold. The

perpetual inventory system is more rational, efficient, effective and scientific system. It is

this method, the issue price is computed by dividing the total cost of inventory by the total

quantity of the inventory held. It is a more rational and scientific method of inventory record

keeping, it considers the most recent as well as the historical price for valuing the cost of goods

sold and inventory (Kaplan & Atkinson 2015). In the inflationary period, there would not be

much effect on the profitability for this method of inventory valuation. It can be applied in

manufacturing business where the stocks are held for a considerable period of time and the prices

of inputs do not fluctuate frequently (Chołodowicz & Orłowski 2016).

Periodic Inventory System:

Periodic inventory system is another method of inventory management and inventory

control system. In this method only the purchase of inventory is recorded as and when the

purchase transaction takes place, but no cost of goods sold entry is made at that time. In this

method, the cost of goods sold is determined by comparing the opening inventory, sot of

purchase of materials and the closing inventory. To compute the cost of goods sold, the cost of

purchase of materials is added with the opening inventory and then the closing inventory is

deducted from to get the value of cost of goods sold. This is a less effective and less rational

method of inventory management and inventory control system (Kaplan & Atkinson 2015).

Conclusion:

From the above discussion and analysis it can be concluded that, there are various

inventory management system which can be used in business practice to record inventory and to

control and manage the inventory system. The periodic inventory system considers overall

movement in the inventory for inventory valuation and valuation of cost of goods sold. The

perpetual inventory system is more rational, efficient, effective and scientific system. It is

5ACCOUNTING SYSTEM AND PROCESS

recommended for the company to adopt the weighted average method of perpetual inventory

system, which would be more suitable for them.

recommended for the company to adopt the weighted average method of perpetual inventory

system, which would be more suitable for them.

6ACCOUNTING SYSTEM AND PROCESS

Answer to question 2: Report:

Introduction:

Accounting system is the backbone of any business organization. It is the language for a

business organization to express and explain their financial performance and position. Without

accounting the modern business organization cannot control their financial performances and

financial records. The information generated as an output of the accounting system is used in

managerial decision-making. With the development of the business and advancement of the

technology, various computerized and automated system has been developed to doe the

accounting and reporting job with the help of technology and information system. In this report

such accounting information system have been analyzed and discussed further (Belfo & Trigo

2013).

Computerized Accounting Information System:

With the advancement and innovation in the technology, various computerized software

packages have been developed to make the accounting job easy and accurate. There are various

automated accounting information system and software to record the day-to-day financial

transaction and to process them and to generate meaningful information from there (Collier

2015). There are various desktop accounting software packages available in the market, which

can be used for the accounting and reporting in the computers. In addition, some internet based

accounting packages can be used for the accounting purpose. Such internet based accounting

systems are known as the cloud based accounting systems. Some example of desktop accounting

packages are SAP, Mayob, Recon and so on and some example of cloud based accounting

information system are Xero, cloud based accounting system, Quick books accounting system

Answer to question 2: Report:

Introduction:

Accounting system is the backbone of any business organization. It is the language for a

business organization to express and explain their financial performance and position. Without

accounting the modern business organization cannot control their financial performances and

financial records. The information generated as an output of the accounting system is used in

managerial decision-making. With the development of the business and advancement of the

technology, various computerized and automated system has been developed to doe the

accounting and reporting job with the help of technology and information system. In this report

such accounting information system have been analyzed and discussed further (Belfo & Trigo

2013).

Computerized Accounting Information System:

With the advancement and innovation in the technology, various computerized software

packages have been developed to make the accounting job easy and accurate. There are various

automated accounting information system and software to record the day-to-day financial

transaction and to process them and to generate meaningful information from there (Collier

2015). There are various desktop accounting software packages available in the market, which

can be used for the accounting and reporting in the computers. In addition, some internet based

accounting packages can be used for the accounting purpose. Such internet based accounting

systems are known as the cloud based accounting systems. Some example of desktop accounting

packages are SAP, Mayob, Recon and so on and some example of cloud based accounting

information system are Xero, cloud based accounting system, Quick books accounting system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING SYSTEM AND PROCESS

and so on. In the following paragraphs the features, applications, advantages and disadvantage of

Xero cloud based accounting system has been discussed (Belfo & Trigo 2013).

Xero Cloud based accounting information system:

Xero is a cloud based accounting software package, which can be accessed from

anywhere in the world. It just requires a user id and password to enter into the software and to

work on it. To use the Xero cloud based accounting information system, one need to buy the

annual subscription for the Xero, and to get their company registered with the Xero. Various

roles can be set and defined for various users in the Xero according to their authority and scope

of work in the organization (Hossack 2015). In the initial stage the company and its features and

activities needs to be set after entering into it. All the opening balances of assets and liabilities

are to be given at the very first stage. The Xero is an automated cloud based software, with the

entry of some purchase, sales, receipts and payments transactions, all the effect will be

automatically given to the respective ledgers. It prepares all the reports instantly and can produce

the results in a single click. It is being widely used because of its simplicity and performance. In

the following paragraphs it usefulness, importance, advantages and disadvantages have been

discussed (Hossack 2015).

Advantages of Xero Cloud based accounting information system:

The system processes the financial data and produces the required and meaningful

information and reports based on the given criteria. The main feature of the system is its

accessibility from the anywhere in the world. The software can be accessed from anywhere using

the internet and can be worked into it. Its popularity is because of its simplicity. It is very much

simple and easy to record transactions in the system; the rest part of processing the information is

done by itself automatically. Its user interface is also very simple and easy. Its unique feature is

and so on. In the following paragraphs the features, applications, advantages and disadvantage of

Xero cloud based accounting system has been discussed (Belfo & Trigo 2013).

Xero Cloud based accounting information system:

Xero is a cloud based accounting software package, which can be accessed from

anywhere in the world. It just requires a user id and password to enter into the software and to

work on it. To use the Xero cloud based accounting information system, one need to buy the

annual subscription for the Xero, and to get their company registered with the Xero. Various

roles can be set and defined for various users in the Xero according to their authority and scope

of work in the organization (Hossack 2015). In the initial stage the company and its features and

activities needs to be set after entering into it. All the opening balances of assets and liabilities

are to be given at the very first stage. The Xero is an automated cloud based software, with the

entry of some purchase, sales, receipts and payments transactions, all the effect will be

automatically given to the respective ledgers. It prepares all the reports instantly and can produce

the results in a single click. It is being widely used because of its simplicity and performance. In

the following paragraphs it usefulness, importance, advantages and disadvantages have been

discussed (Hossack 2015).

Advantages of Xero Cloud based accounting information system:

The system processes the financial data and produces the required and meaningful

information and reports based on the given criteria. The main feature of the system is its

accessibility from the anywhere in the world. The software can be accessed from anywhere using

the internet and can be worked into it. Its popularity is because of its simplicity. It is very much

simple and easy to record transactions in the system; the rest part of processing the information is

done by itself automatically. Its user interface is also very simple and easy. Its unique feature is

8ACCOUNTING SYSTEM AND PROCESS

its presentation of information. It shows all the important figures and facts in the dashboard of

the system with a bar chart. It also shows the pending invoices and pending bills to be paid in the

dashboard. One more important feature of the system is the inventory recording and inventory

control system. It tracks the inventory with every inputs and outputs in the inventory. Therefore,

it is very much user friendly easy and efficient in performing all the accounting and reporting

financial transactions (Hossack 2015).

Disadvantages of Xero Accounting information system:

The Xero accounting information system is a completely cloud based accounting system

which is accessed using the internet. All the information are stored in the cloud and updated in

the cloud as and when new information is added to it. Hence, the main disadvantage of the

system is its security (Hossack 2015). As it is a complete internet based system there is a security

issue in the system. Various important information of the business can be stolen by others from

the internet. If the system gets hacked or if he user id and password is lost to anyone else, then

the information of the business would be licked to the outsiders. If that can be assured there

would be no problem in using it for the business organization (Brandas, Megan & Didraga

2015).

Adoption of the Xero Accounting information system:

After observing the importance, advantages and uses of the Xero cloud based accounting

system it can be recommended for the company to adopt the accounting system and to use it for

recording their day-to-day business transaction. It can help them in controlling their financial

transactions as well as to control their inventory system. The company is having various

inventory related transactions, which can be controlled in Xero cloud based accounting system

with a proper tracking of the inventory. It can also help them to generate meaningful information

its presentation of information. It shows all the important figures and facts in the dashboard of

the system with a bar chart. It also shows the pending invoices and pending bills to be paid in the

dashboard. One more important feature of the system is the inventory recording and inventory

control system. It tracks the inventory with every inputs and outputs in the inventory. Therefore,

it is very much user friendly easy and efficient in performing all the accounting and reporting

financial transactions (Hossack 2015).

Disadvantages of Xero Accounting information system:

The Xero accounting information system is a completely cloud based accounting system

which is accessed using the internet. All the information are stored in the cloud and updated in

the cloud as and when new information is added to it. Hence, the main disadvantage of the

system is its security (Hossack 2015). As it is a complete internet based system there is a security

issue in the system. Various important information of the business can be stolen by others from

the internet. If the system gets hacked or if he user id and password is lost to anyone else, then

the information of the business would be licked to the outsiders. If that can be assured there

would be no problem in using it for the business organization (Brandas, Megan & Didraga

2015).

Adoption of the Xero Accounting information system:

After observing the importance, advantages and uses of the Xero cloud based accounting

system it can be recommended for the company to adopt the accounting system and to use it for

recording their day-to-day business transaction. It can help them in controlling their financial

transactions as well as to control their inventory system. The company is having various

inventory related transactions, which can be controlled in Xero cloud based accounting system

with a proper tracking of the inventory. It can also help them to generate meaningful information

9ACCOUNTING SYSTEM AND PROCESS

as and when required and can be used in managerial decision-making process. They need to

adopt the system according to their requirement and setup must be done according to their

information needs (Brandas, Megan & Didraga 2015).

Conclusion:

From the above discussion and analysis, it can be concluded that, Accounting system is

an integral part of the business organization, it is very important for the organization also. If it

can be done effectively and efficiently and meaningful accounting or financial information can

be generated as an output, internal and external stakeholders would be beneficial and various

important decisions can be taken based on such information. Xero, is a fully cloud based

accounting system which is having various advanced and unique features, which can help an

organization in better accounting, management and decision making process.

as and when required and can be used in managerial decision-making process. They need to

adopt the system according to their requirement and setup must be done according to their

information needs (Brandas, Megan & Didraga 2015).

Conclusion:

From the above discussion and analysis, it can be concluded that, Accounting system is

an integral part of the business organization, it is very important for the organization also. If it

can be done effectively and efficiently and meaningful accounting or financial information can

be generated as an output, internal and external stakeholders would be beneficial and various

important decisions can be taken based on such information. Xero, is a fully cloud based

accounting system which is having various advanced and unique features, which can help an

organization in better accounting, management and decision making process.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ACCOUNTING SYSTEM AND PROCESS

Answer to question 3: Letter:

To

The Directors, Mr. and Mrs. Spot

Spotty Ltd

Australia

14 May 2019

Subject: Employee fraud and Importance of internal control

Dear Sir/Madam,

This letter is prepared to inform you the following issues and importance of the internal

control system. Although there is no such events of frauds, mismanagement activities in the

organization, various recent frauds and mismanagements in some Australian companies have

been discussed, and the importance of an internal control system to prevent such activities have

been outlined.

Cash mismanagement is the case, when an employee of an organization steals cash or

mismanages the cash of an organization. It is an unethical behavior of the employee of an

organization. It must not be entertained, and necessary measures must be taken for preventing

such activities in a business organization. Some recent instances of such cash mismanagement

activities in Australia can be outlined as follows.

A recent study has shown that almost $217 million has been stolen by the bank

employees in the last 13 years in Australia, among them a women employee of ING had stolen

$45 million, which wan the biggest cash mismanagement case by employees. In another case a

female employee of an Australian company, stole almost $19 million. She had the cheque

signing authority of the company and was one of the two employees having authority to process

Answer to question 3: Letter:

To

The Directors, Mr. and Mrs. Spot

Spotty Ltd

Australia

14 May 2019

Subject: Employee fraud and Importance of internal control

Dear Sir/Madam,

This letter is prepared to inform you the following issues and importance of the internal

control system. Although there is no such events of frauds, mismanagement activities in the

organization, various recent frauds and mismanagements in some Australian companies have

been discussed, and the importance of an internal control system to prevent such activities have

been outlined.

Cash mismanagement is the case, when an employee of an organization steals cash or

mismanages the cash of an organization. It is an unethical behavior of the employee of an

organization. It must not be entertained, and necessary measures must be taken for preventing

such activities in a business organization. Some recent instances of such cash mismanagement

activities in Australia can be outlined as follows.

A recent study has shown that almost $217 million has been stolen by the bank

employees in the last 13 years in Australia, among them a women employee of ING had stolen

$45 million, which wan the biggest cash mismanagement case by employees. In another case a

female employee of an Australian company, stole almost $19 million. She had the cheque

signing authority of the company and was one of the two employees having authority to process

11ACCOUNTING SYSTEM AND PROCESS

electronic fund transfer activities. She transferred fund from the company’s account to her an

account controlled by her in the name of her own business. She purchased properties by that

amount to channelize the fund and to extract it from the banking cycle. In this case the employee

used to make bills drawn on the name of the company using her own business name, and

transferred fund to pay off those bills which was totally fake. She hided the real case in behind

and shown all those bill as actual payables to the company and duly paid those bills which was a

total fraud.

In another case of employee cash mismanagement, a male employee of 41 years age, who

was employed as the financial controller of the company and the company secretary for a

transport company had stolen a significant amount of cash within a period of only five months.

He was given the authority and role to act as the authorized signatory on behalf of the

organization for banking transactions. Within a five months period, he transferred a total of $11

million to his personal account and bought property and a luxury car using that fund.

Therefore, if all those instances and cases are considered, it can be observed that, there is

a risk of cash mismanagement in every organization. As human beings are working in behalf of

the business organization in various roles and positions, their motives and intentions can never

be completely known by the organization. It depend on their ethical values and beliefs, whether

they would involve in such activities or not.

The risk of such employee frauds can be avoided and reduced applying various internal

control procedures for cash management and cash transactions. In an organization there are

mainly two types of cash transactions, one is cash receipts and the other is cash payments. In

both the ways the cash mismanagement is possible by the employees. Hence, in both the sides of

electronic fund transfer activities. She transferred fund from the company’s account to her an

account controlled by her in the name of her own business. She purchased properties by that

amount to channelize the fund and to extract it from the banking cycle. In this case the employee

used to make bills drawn on the name of the company using her own business name, and

transferred fund to pay off those bills which was totally fake. She hided the real case in behind

and shown all those bill as actual payables to the company and duly paid those bills which was a

total fraud.

In another case of employee cash mismanagement, a male employee of 41 years age, who

was employed as the financial controller of the company and the company secretary for a

transport company had stolen a significant amount of cash within a period of only five months.

He was given the authority and role to act as the authorized signatory on behalf of the

organization for banking transactions. Within a five months period, he transferred a total of $11

million to his personal account and bought property and a luxury car using that fund.

Therefore, if all those instances and cases are considered, it can be observed that, there is

a risk of cash mismanagement in every organization. As human beings are working in behalf of

the business organization in various roles and positions, their motives and intentions can never

be completely known by the organization. It depend on their ethical values and beliefs, whether

they would involve in such activities or not.

The risk of such employee frauds can be avoided and reduced applying various internal

control procedures for cash management and cash transactions. In an organization there are

mainly two types of cash transactions, one is cash receipts and the other is cash payments. In

both the ways the cash mismanagement is possible by the employees. Hence, in both the sides of

12ACCOUNTING SYSTEM AND PROCESS

the cash transaction, implementation of internal control system is required. Some important and

effective internal control techniques have been described as follows.

Access: For applying a control over the cash transactions the access to the cash

transactions should be defined and should be restricted to certain levels, such as a petty cashier

should never make any trading bill payments. Authority of making transaction must be

predefined and must be given based on their duties and responsibilities. If they are given undue

power and authority they would be entering into unethical practices.

Documentation: Proper documentation should be there supporting every cash transaction. It

must be recorded and duly authorized by the respective authority before making any cash

payment and receipts. It ensures the proper authority and the validity of the transaction.

Reconciliation: All the cash transactions must be reconciled at the end of a specified

frequency of period. It must be matched with the documents and bank records. It ensures the

correctness and proper treatment of the cash transactions.

Lastly, it is very important to assign the authority to different employees of an

organization. It must not be the case that, a single employee prepares a bill, authorizes it makes

payment for that. The authority should be so distributed that, the employee making the bill,

authorizing it, paying it and lastly reconciling it would be different persons. In this way the

dishonest employee would not involve in fraud activities as he knows that, this work will be

checked by others.

Therefore it can be recommended for the company to adopt such internal control

measures to avoid any potential risk of employee fraud and cash mismanagement.

Sincerely

[Name]

the cash transaction, implementation of internal control system is required. Some important and

effective internal control techniques have been described as follows.

Access: For applying a control over the cash transactions the access to the cash

transactions should be defined and should be restricted to certain levels, such as a petty cashier

should never make any trading bill payments. Authority of making transaction must be

predefined and must be given based on their duties and responsibilities. If they are given undue

power and authority they would be entering into unethical practices.

Documentation: Proper documentation should be there supporting every cash transaction. It

must be recorded and duly authorized by the respective authority before making any cash

payment and receipts. It ensures the proper authority and the validity of the transaction.

Reconciliation: All the cash transactions must be reconciled at the end of a specified

frequency of period. It must be matched with the documents and bank records. It ensures the

correctness and proper treatment of the cash transactions.

Lastly, it is very important to assign the authority to different employees of an

organization. It must not be the case that, a single employee prepares a bill, authorizes it makes

payment for that. The authority should be so distributed that, the employee making the bill,

authorizing it, paying it and lastly reconciling it would be different persons. In this way the

dishonest employee would not involve in fraud activities as he knows that, this work will be

checked by others.

Therefore it can be recommended for the company to adopt such internal control

measures to avoid any potential risk of employee fraud and cash mismanagement.

Sincerely

[Name]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13ACCOUNTING SYSTEM AND PROCESS

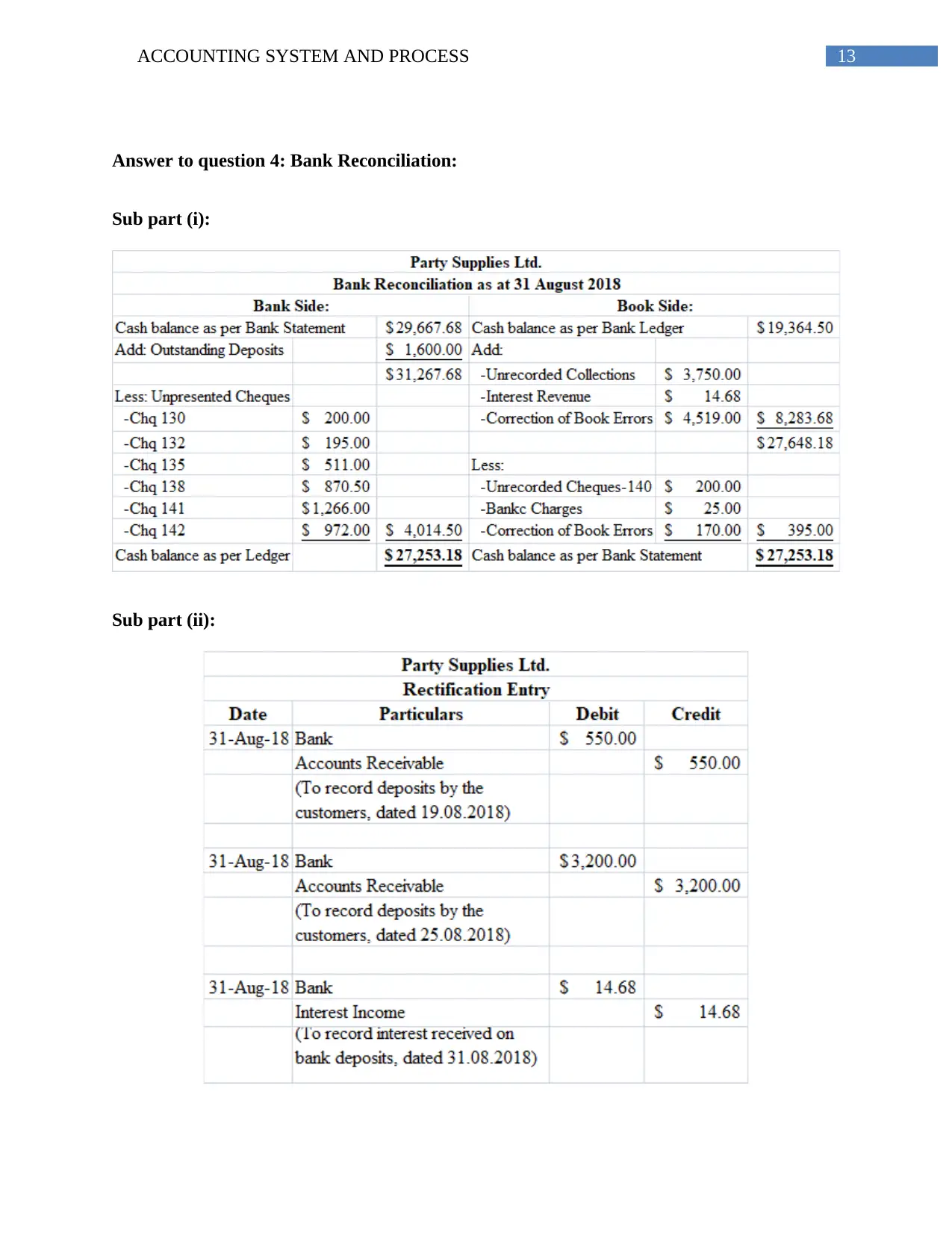

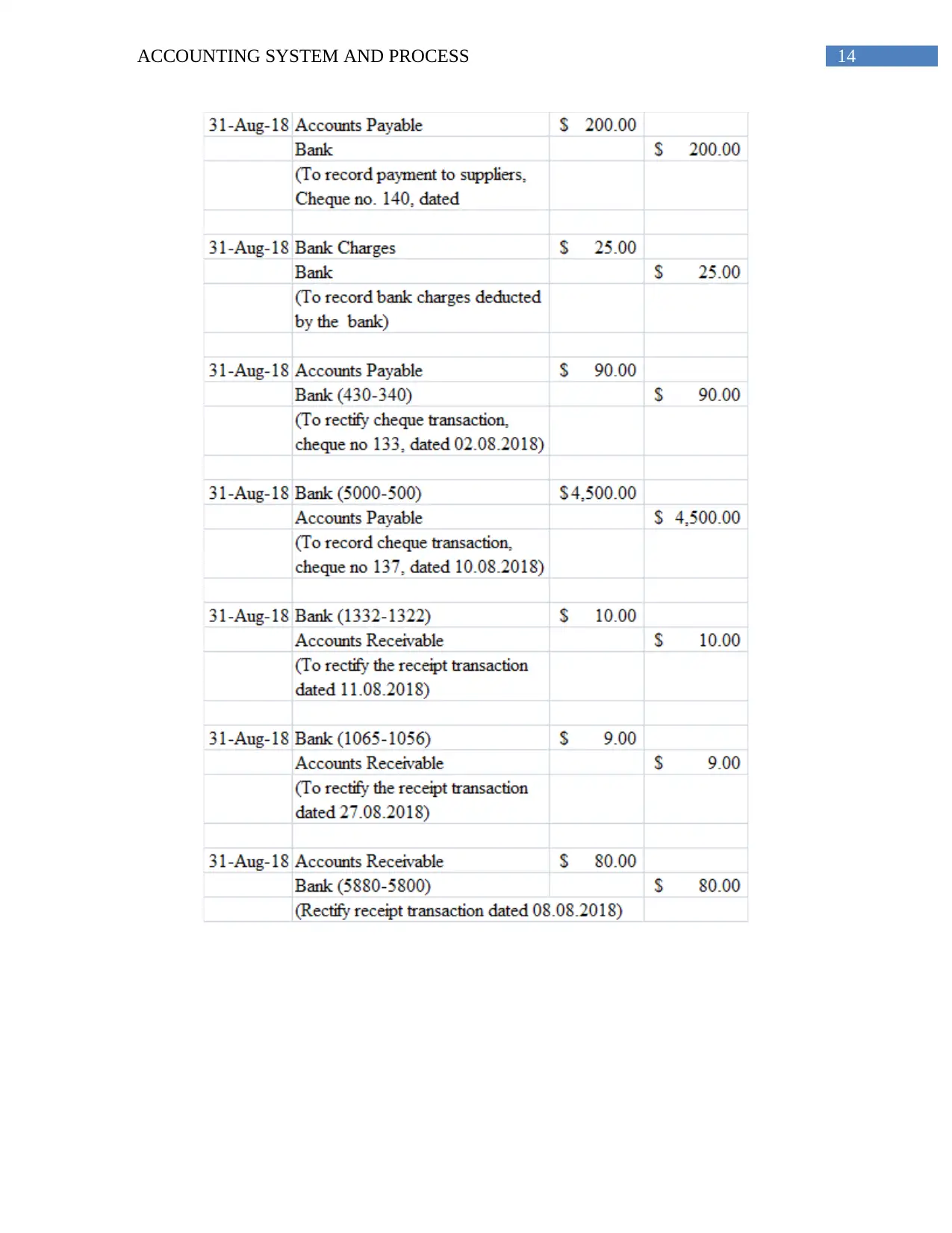

Answer to question 4: Bank Reconciliation:

Sub part (i):

Sub part (ii):

Answer to question 4: Bank Reconciliation:

Sub part (i):

Sub part (ii):

14ACCOUNTING SYSTEM AND PROCESS

15ACCOUNTING SYSTEM AND PROCESS

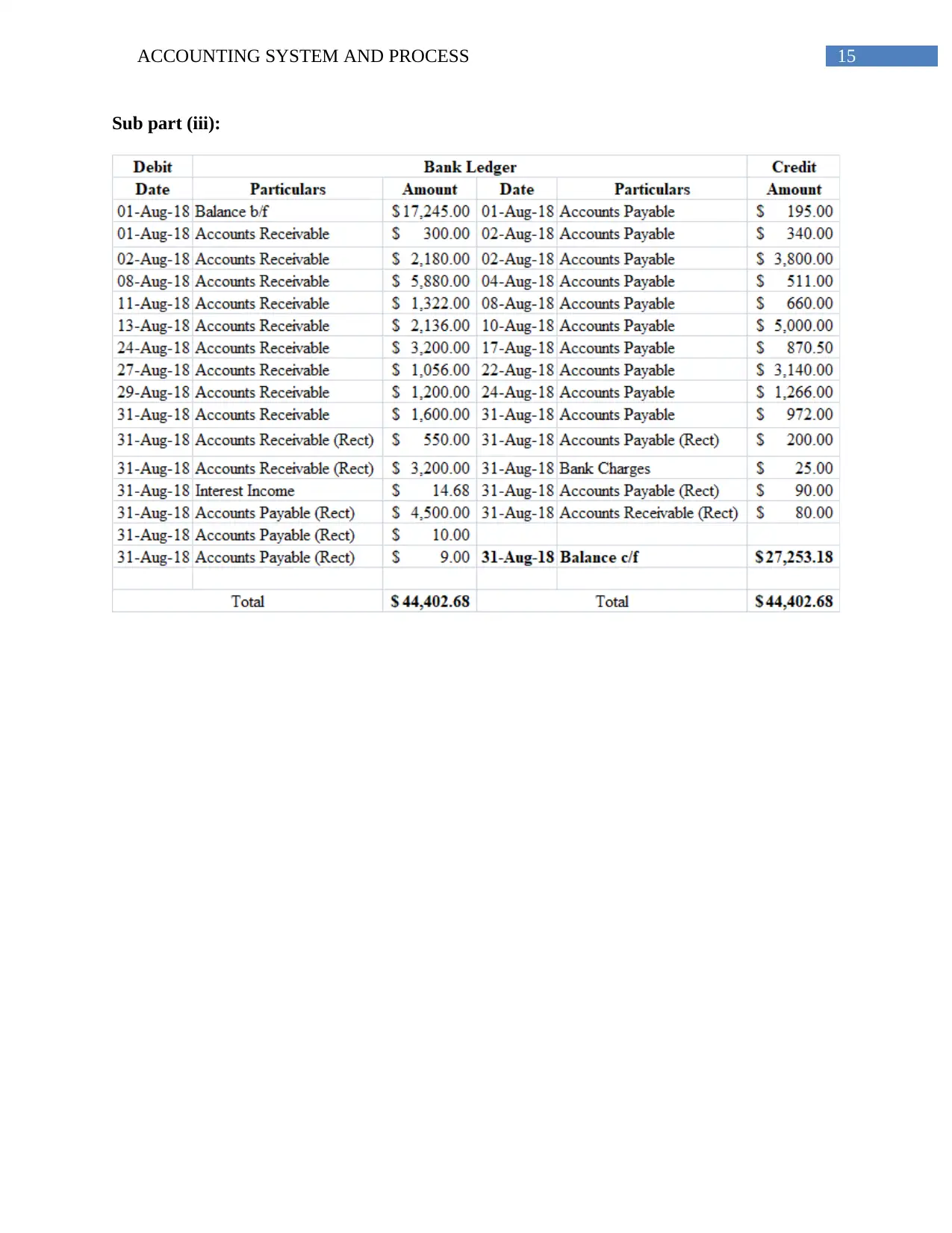

Sub part (iii):

Sub part (iii):

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16ACCOUNTING SYSTEM AND PROCESS

References and bibliography:

Belfo, F., & Trigo, A. (2013). Accounting information systems: Tradition and future

directions. Procedia Technology, 9, 536-546.

Bonny, P., Goode, S., & Lacey, D. (2015). Revisiting employee fraud: gender, investigation

outcomes and offender motivation. Journal of Financial Crime, 22(4), 447-467.

Brandas, C., Megan, O., & Didraga, O. (2015). Global perspectives on accounting information

systems: mobile and cloud approach. Procedia Economics and Finance, 20, 88-93.

Chołodowicz, E., & Orłowski, P. (2016). Comparison of a perpetual and PD inventory control

system with Smith Predictor and different shipping delays using bicriterial optimization

and SPEA2. Pomiary Automatyka Robotyka, 20.

Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Dimitriu, O., & Matei, M. (2014). A new paradigm for accounting through cloud

computing. Procedia economics and finance, 15, 840-846.

Hossack, S. (2015). Cloud-based accounting and productivity tools for practitioners and

taxpayers. Taxation in Australia, 50(5), 265.

Iyer, N., & Samociuk, M. (2016). Fraud and corruption: Prevention and detection. Routledge.

Kaplan, R. S., & Atkinson, A. A. (2015). Advanced management accounting. PHI Learning.

References and bibliography:

Belfo, F., & Trigo, A. (2013). Accounting information systems: Tradition and future

directions. Procedia Technology, 9, 536-546.

Bonny, P., Goode, S., & Lacey, D. (2015). Revisiting employee fraud: gender, investigation

outcomes and offender motivation. Journal of Financial Crime, 22(4), 447-467.

Brandas, C., Megan, O., & Didraga, O. (2015). Global perspectives on accounting information

systems: mobile and cloud approach. Procedia Economics and Finance, 20, 88-93.

Chołodowicz, E., & Orłowski, P. (2016). Comparison of a perpetual and PD inventory control

system with Smith Predictor and different shipping delays using bicriterial optimization

and SPEA2. Pomiary Automatyka Robotyka, 20.

Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons.

Dimitriu, O., & Matei, M. (2014). A new paradigm for accounting through cloud

computing. Procedia economics and finance, 15, 840-846.

Hossack, S. (2015). Cloud-based accounting and productivity tools for practitioners and

taxpayers. Taxation in Australia, 50(5), 265.

Iyer, N., & Samociuk, M. (2016). Fraud and corruption: Prevention and detection. Routledge.

Kaplan, R. S., & Atkinson, A. A. (2015). Advanced management accounting. PHI Learning.

17ACCOUNTING SYSTEM AND PROCESS

Kummer, T. F., Singh, K., & Best, P. (2015). The effectiveness of fraud detection instruments in

not-for-profit organizations. Managerial Auditing Journal, 30(4/5), 435-455.

Kummer, T. F., Singh, K., & Best, P. (2015). The effectiveness of fraud detection instruments in

not-for-profit organizations. Managerial Auditing Journal, 30(4/5), 435-455.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.