Financial Statement Analysis and Reporting

VerifiedAdded on 2021/04/21

|30

|2825

|142

AI Summary

This assignment delves into the world of financial accounting, focusing on the significance of financial statement analysis, and the preparation of various financial reports such as trial balance, income statements, balance sheets, and changes in equity. It also touches upon current ratio calculations and highlights the importance of these reports for decision-making and accountability. The document includes references to relevant studies and publications in the field of accounting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING SYSTEM AND PROCESSES

Accounting system and processes

Name of the student

Student ID number

Assignment task number

Author note

DECLARATION: THE WORK IN THIS ASSIGNMENT IS MY OWN WORK, AND HAS NOT BEEN

PLAGIARISED.

Accounting system and processes

Name of the student

Student ID number

Assignment task number

Author note

DECLARATION: THE WORK IN THIS ASSIGNMENT IS MY OWN WORK, AND HAS NOT BEEN

PLAGIARISED.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEM AND PROCESSES

Table of Contents

1. Plagiarism:..................................................................................................................................................2

2. Pasting spreadsheets in the doc files:..........................................................................................................2

3. Accounting resources on the internet:........................................................................................................4

4. Professional accounting bodies:..................................................................................................................4

5. Work integrated assessment:......................................................................................................................4

6. Business report:...........................................................................................................................................5

7. P A L E R:...................................................................................................................................................5

8. Balance sheet equation................................................................................................................................6

9. Debit and credit balance:............................................................................................................................7

10. Trial balance............................................................................................................................................7

11. Crossword.............................................................................................................................................12

12. Adjusting entries...................................................................................................................................13

13. Current and non-current liabilities........................................................................................................14

14. Ratios.....................................................................................................................................................14

15. Worksheets and financial reports..........................................................................................................14

References:.......................................................................................................................................................24

1

Student Name

Student ID number

Table of Contents

1. Plagiarism:..................................................................................................................................................2

2. Pasting spreadsheets in the doc files:..........................................................................................................2

3. Accounting resources on the internet:........................................................................................................4

4. Professional accounting bodies:..................................................................................................................4

5. Work integrated assessment:......................................................................................................................4

6. Business report:...........................................................................................................................................5

7. P A L E R:...................................................................................................................................................5

8. Balance sheet equation................................................................................................................................6

9. Debit and credit balance:............................................................................................................................7

10. Trial balance............................................................................................................................................7

11. Crossword.............................................................................................................................................12

12. Adjusting entries...................................................................................................................................13

13. Current and non-current liabilities........................................................................................................14

14. Ratios.....................................................................................................................................................14

15. Worksheets and financial reports..........................................................................................................14

References:.......................................................................................................................................................24

1

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

1. Plagiarism:

Plagiarism takes place when the writer duplicates the ideas or language of another student and

presents the work as his own. All unpublished and published material; whether in electronic or printed form

is covered under the definition. Collusion takes place when more than 1 student has taken part in completing

the assignment and is submitted as individual’s work subsequently (Ferro & Martins, 2016). Therefore,

collusion will also be considered as plagiarism. This is unfair to the honest students as the honest student

who has submitted his task on his own may get lower marks as compared to the student who has copied

someone else’s work.

2. Pasting spreadsheets in the doc files:

Normal view:

2

Student Name

Student ID number

1. Plagiarism:

Plagiarism takes place when the writer duplicates the ideas or language of another student and

presents the work as his own. All unpublished and published material; whether in electronic or printed form

is covered under the definition. Collusion takes place when more than 1 student has taken part in completing

the assignment and is submitted as individual’s work subsequently (Ferro & Martins, 2016). Therefore,

collusion will also be considered as plagiarism. This is unfair to the honest students as the honest student

who has submitted his task on his own may get lower marks as compared to the student who has copied

someone else’s work.

2. Pasting spreadsheets in the doc files:

Normal view:

2

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

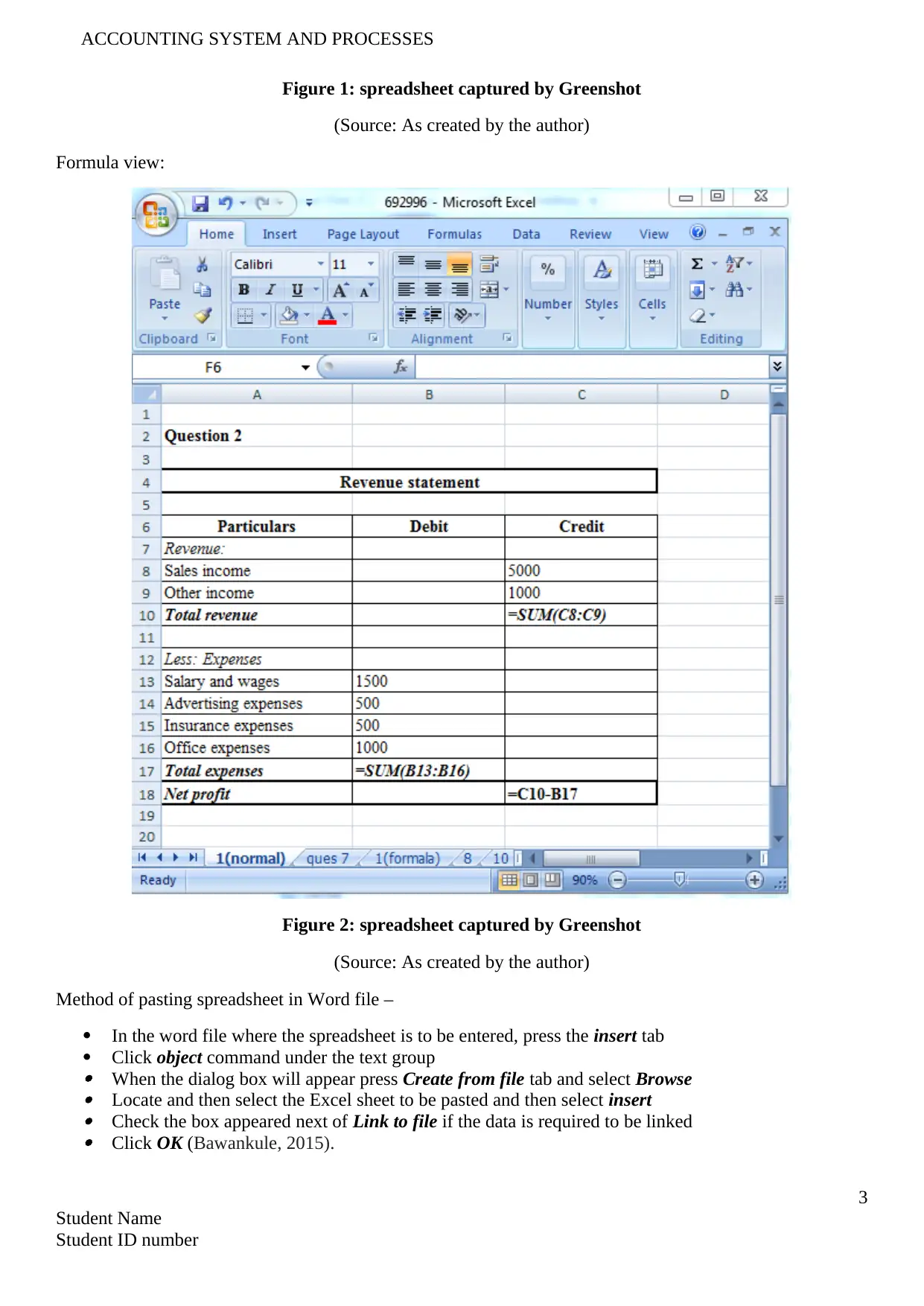

Figure 1: spreadsheet captured by Greenshot

(Source: As created by the author)

Formula view:

Figure 2: spreadsheet captured by Greenshot

(Source: As created by the author)

Method of pasting spreadsheet in Word file –

In the word file where the spreadsheet is to be entered, press the insert tab

Click object command under the text group When the dialog box will appear press Create from file tab and select Browse Locate and then select the Excel sheet to be pasted and then select insert Check the box appeared next of Link to file if the data is required to be linked Click OK (Bawankule, 2015).

3

Student Name

Student ID number

Figure 1: spreadsheet captured by Greenshot

(Source: As created by the author)

Formula view:

Figure 2: spreadsheet captured by Greenshot

(Source: As created by the author)

Method of pasting spreadsheet in Word file –

In the word file where the spreadsheet is to be entered, press the insert tab

Click object command under the text group When the dialog box will appear press Create from file tab and select Browse Locate and then select the Excel sheet to be pasted and then select insert Check the box appeared next of Link to file if the data is required to be linked Click OK (Bawankule, 2015).

3

Student Name

Student ID number

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEM AND PROCESSES

3. Accounting resources on the internet:

International Federation of accountants – It develops international standard on accounting standards,

ethics, education, auditing and assurance. The website is - http://www.ifac.org/

Institute of public accountants – IPA is the professional organization for the accountants and

recognized for hands on skill, practical and wide understanding of total environment of the business.

The website is - http://www.publicaccountants.org.au/

Bruce Edmunds & Associates – the site offers resources and tools that can be used for business

finance and accounting. the website is - https://edmunds.com.au/resources/internet_links/

Accounting coach – it assists the user in learning the advanced accounting tools and enhancing the

levels of knowledge in accounting. The website is - http://www.accountingcoach.com/

The Sleeter Group – the users can find accounts related educational resources under this site. The

website is - https://www.sleeter.com/

Above the line accounting – they are the proactive tax and chartered accounting firm that serves the

Australian entertainment and media industry with financing, tax and accounting advices. The website

is - http://abovethelineaccounting.com.au/

4. Professional accounting bodies:

The Association of Accounting Technicians (AAT) Australia is the largest professional body of

Australia. Their website is - aat.org.au/about-aat-australia.html. This resource has been chosen as they

provides services for bookkeeping, finance and accounting sector and is the support for 3 professional

bodies – Institute of Chartered Accountants in Australia, Institute of Public Accountants and CPA Australia.

5. Work integrated assessment:

Computing environment is the collection of the computers that are used for processing and

exchanging information for solving various computing problems. Various computing software, equipment

that are used in the workplace are as follows –

Personal computers – PCs are used for individual use by the person at office for applications like

financial analysis, data management and MS Office. It is utilised for various functions like

performing research, using internet, calculating numbers and creating letters are few to be named. It

is also used for the purpose of business applications (Brigham & Ehrhardt, 2013).

Laptops – it is used for almost all duties as it is more powerful as compared to the desktops and they

come with the options of tablet mode, touch screen and longer life for battery. Mobility is the main

advantage of laptop and it can be used more efficiently as compared to PCs.

Printers – Printers are used for printing various documents required normal business operations.

Fax machines – fax machines are used for receiving and sending documents as quick alternative

against postal mail or any other delivery services (Kim, Batchu & Sirota, 2016).

Routers for internet – it is used to forward the data packets among the computer networks. It

performs traffic directing activities on internet.

Further, the internet of the company can be accessed only with proper authorization. If anyone is

found misusing the office internet it will be considered as punishable offence. The above mentioned

software and equipments are used for carrying out the work smoothly (Walker et al., 2016).

4

Student Name

Student ID number

3. Accounting resources on the internet:

International Federation of accountants – It develops international standard on accounting standards,

ethics, education, auditing and assurance. The website is - http://www.ifac.org/

Institute of public accountants – IPA is the professional organization for the accountants and

recognized for hands on skill, practical and wide understanding of total environment of the business.

The website is - http://www.publicaccountants.org.au/

Bruce Edmunds & Associates – the site offers resources and tools that can be used for business

finance and accounting. the website is - https://edmunds.com.au/resources/internet_links/

Accounting coach – it assists the user in learning the advanced accounting tools and enhancing the

levels of knowledge in accounting. The website is - http://www.accountingcoach.com/

The Sleeter Group – the users can find accounts related educational resources under this site. The

website is - https://www.sleeter.com/

Above the line accounting – they are the proactive tax and chartered accounting firm that serves the

Australian entertainment and media industry with financing, tax and accounting advices. The website

is - http://abovethelineaccounting.com.au/

4. Professional accounting bodies:

The Association of Accounting Technicians (AAT) Australia is the largest professional body of

Australia. Their website is - aat.org.au/about-aat-australia.html. This resource has been chosen as they

provides services for bookkeeping, finance and accounting sector and is the support for 3 professional

bodies – Institute of Chartered Accountants in Australia, Institute of Public Accountants and CPA Australia.

5. Work integrated assessment:

Computing environment is the collection of the computers that are used for processing and

exchanging information for solving various computing problems. Various computing software, equipment

that are used in the workplace are as follows –

Personal computers – PCs are used for individual use by the person at office for applications like

financial analysis, data management and MS Office. It is utilised for various functions like

performing research, using internet, calculating numbers and creating letters are few to be named. It

is also used for the purpose of business applications (Brigham & Ehrhardt, 2013).

Laptops – it is used for almost all duties as it is more powerful as compared to the desktops and they

come with the options of tablet mode, touch screen and longer life for battery. Mobility is the main

advantage of laptop and it can be used more efficiently as compared to PCs.

Printers – Printers are used for printing various documents required normal business operations.

Fax machines – fax machines are used for receiving and sending documents as quick alternative

against postal mail or any other delivery services (Kim, Batchu & Sirota, 2016).

Routers for internet – it is used to forward the data packets among the computer networks. It

performs traffic directing activities on internet.

Further, the internet of the company can be accessed only with proper authorization. If anyone is

found misusing the office internet it will be considered as punishable offence. The above mentioned

software and equipments are used for carrying out the work smoothly (Walker et al., 2016).

4

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

6. Business report:

Introduction – the main objective of the report is to state the lesson learned from ABC learning case study.

Further, the report will discuss 3 ethical issues associated with ABC Learning Case. It will also mention the

main financial reports used in the business and their uses.

Discussion –

1. Learning from video – ABC Learning Child-care has become the nightmare for the parents whose

children were used to attend the centre. Further, the government held responsible policy blenders

who allowed the organization for the big fail. The last published annual report of the company that

was published for the half year ending 31 December 2007. The statement of the company before it

collapsed in November indicated the loss for the year ended 30th June and wiped out the profit that

was ever made by the company. Eventually the company’s shares were reduced to 54 cents that were

dealing at $ 8.60 per share (ABC Learning collapse case study, 2018).

2. Major financial reports and their purposes – four major financial statements are –

Statement of the financial position – it states the company’s financial position at specific date. It

includes three sections. These are – assets that is owned or controlled by the business, liabilities that

the business owes to third party and the equity that is the business owes to the owners.

Income statement – it is also known as profit and loss statement and it reports the financial

performance of the company in terms of profit or loss over the particular period. Income states the

earning of the business over specific period and expenses states the cost that is incurred by the

company over the specific period (Dalnial et al., 2014).

Statement for changes in equity – this also known as statement of retained earnings and id shows the

details for movement in the owner’s equity over the period. it takes into account the reported net loss

or profit, payment of dividends, share capital repaid or issued and losses or gains recognized under

equity.

Cash flow statement – it reveals the movement of cash in bank and cash balances over the specific

period. The movement is classified under operating activities, financing activities and investing

activities (Lin et al., 2015).

3. Ethical issues from ABC case study –

The associated inherent risk with assets valuation was enormous and should have been the red flag.

The profit of the company rapidly increased through acquisition that shall have raised questions

regarding the underlying asset valuation for the assets it acquired as 70% of the assets were

intangible.

The accounting procedures and ethical duties were not followed properly and the company’s major

focus was on profits only. Therefore, it neglected the customer’s welfare.

Conclusion – it is concluded from the above discussion that the ABC learning was major failure owing to

their unethical accounting practices. It should have been followed the corporation law properly to protect the

customer’s and investor’s interest.

7. P A L E R:

P A L E R is acronym of understanding credit and debit. Here, P states Proprietorship, A states assets,

L states liability, E states expenses and R states Revenues. Increase in expenses, decrease in revenues and

decrease in owner’s equity is debit account. On the other hand, decrease in expenses, increase in revenues

and increase in owner’s equity is credit account

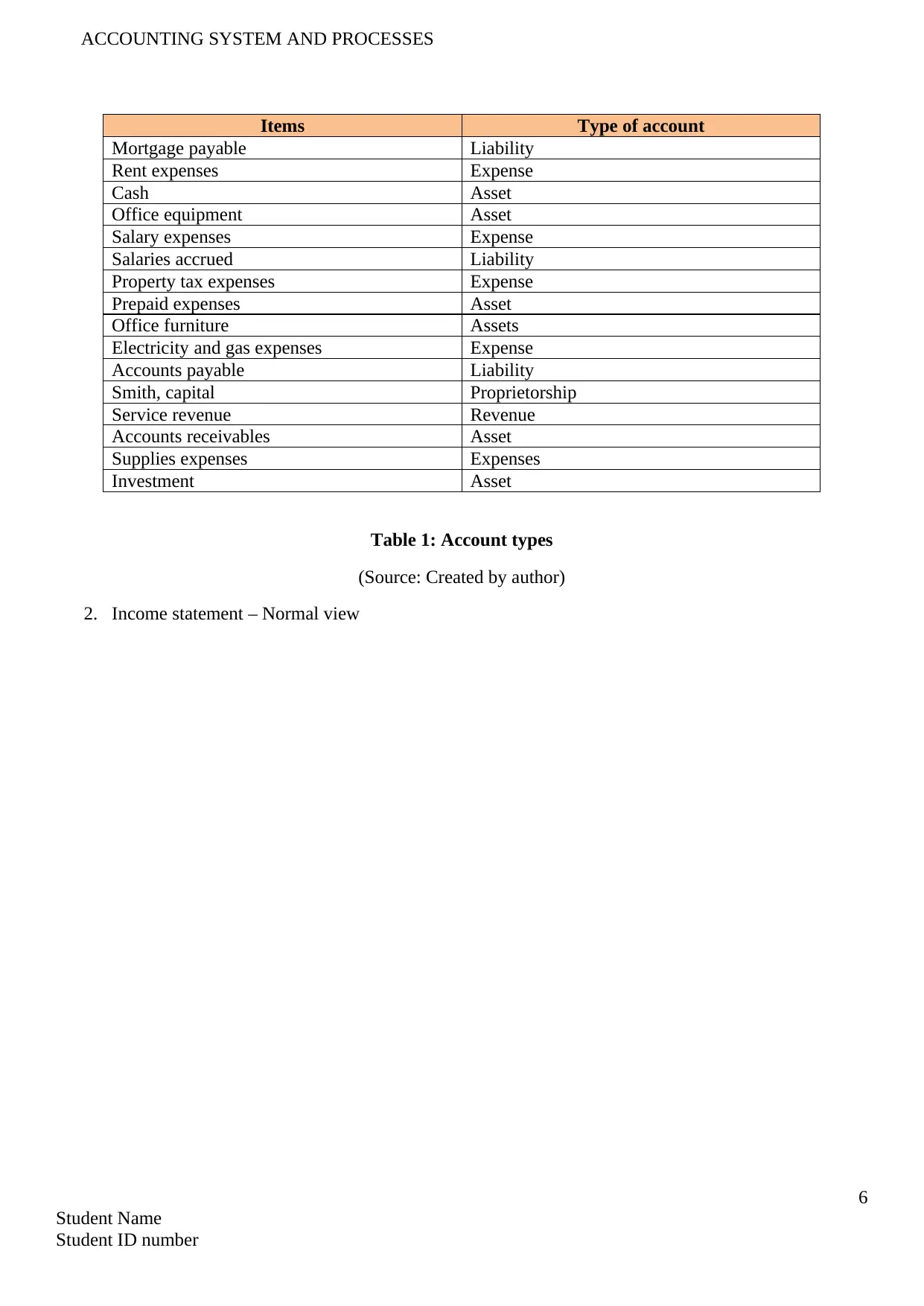

1. Account types

5

Student Name

Student ID number

6. Business report:

Introduction – the main objective of the report is to state the lesson learned from ABC learning case study.

Further, the report will discuss 3 ethical issues associated with ABC Learning Case. It will also mention the

main financial reports used in the business and their uses.

Discussion –

1. Learning from video – ABC Learning Child-care has become the nightmare for the parents whose

children were used to attend the centre. Further, the government held responsible policy blenders

who allowed the organization for the big fail. The last published annual report of the company that

was published for the half year ending 31 December 2007. The statement of the company before it

collapsed in November indicated the loss for the year ended 30th June and wiped out the profit that

was ever made by the company. Eventually the company’s shares were reduced to 54 cents that were

dealing at $ 8.60 per share (ABC Learning collapse case study, 2018).

2. Major financial reports and their purposes – four major financial statements are –

Statement of the financial position – it states the company’s financial position at specific date. It

includes three sections. These are – assets that is owned or controlled by the business, liabilities that

the business owes to third party and the equity that is the business owes to the owners.

Income statement – it is also known as profit and loss statement and it reports the financial

performance of the company in terms of profit or loss over the particular period. Income states the

earning of the business over specific period and expenses states the cost that is incurred by the

company over the specific period (Dalnial et al., 2014).

Statement for changes in equity – this also known as statement of retained earnings and id shows the

details for movement in the owner’s equity over the period. it takes into account the reported net loss

or profit, payment of dividends, share capital repaid or issued and losses or gains recognized under

equity.

Cash flow statement – it reveals the movement of cash in bank and cash balances over the specific

period. The movement is classified under operating activities, financing activities and investing

activities (Lin et al., 2015).

3. Ethical issues from ABC case study –

The associated inherent risk with assets valuation was enormous and should have been the red flag.

The profit of the company rapidly increased through acquisition that shall have raised questions

regarding the underlying asset valuation for the assets it acquired as 70% of the assets were

intangible.

The accounting procedures and ethical duties were not followed properly and the company’s major

focus was on profits only. Therefore, it neglected the customer’s welfare.

Conclusion – it is concluded from the above discussion that the ABC learning was major failure owing to

their unethical accounting practices. It should have been followed the corporation law properly to protect the

customer’s and investor’s interest.

7. P A L E R:

P A L E R is acronym of understanding credit and debit. Here, P states Proprietorship, A states assets,

L states liability, E states expenses and R states Revenues. Increase in expenses, decrease in revenues and

decrease in owner’s equity is debit account. On the other hand, decrease in expenses, increase in revenues

and increase in owner’s equity is credit account

1. Account types

5

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

Items Type of account

Mortgage payable Liability

Rent expenses Expense

Cash Asset

Office equipment Asset

Salary expenses Expense

Salaries accrued Liability

Property tax expenses Expense

Prepaid expenses Asset

Office furniture Assets

Electricity and gas expenses Expense

Accounts payable Liability

Smith, capital Proprietorship

Service revenue Revenue

Accounts receivables Asset

Supplies expenses Expenses

Investment Asset

Table 1: Account types

(Source: Created by author)

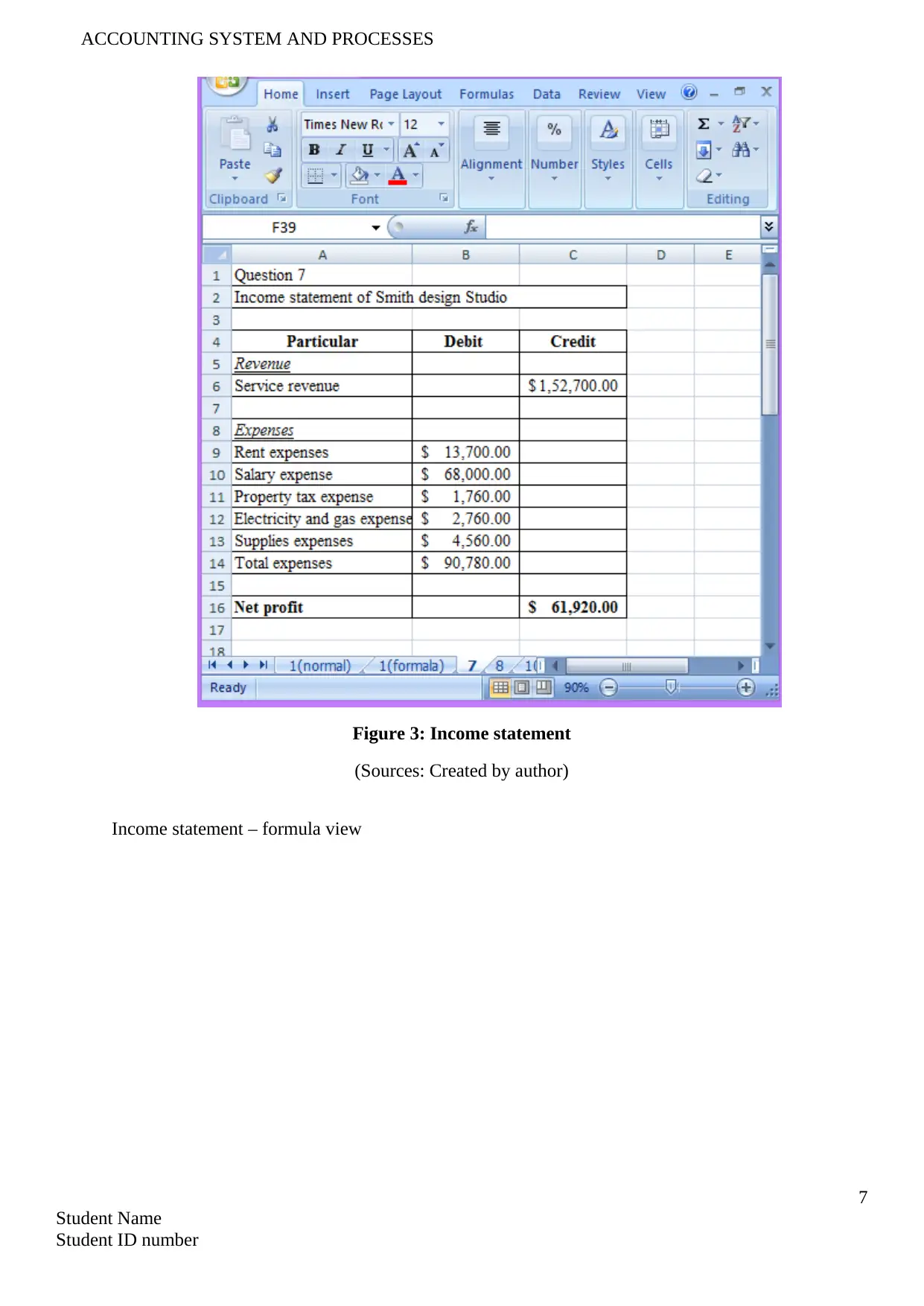

2. Income statement – Normal view

6

Student Name

Student ID number

Items Type of account

Mortgage payable Liability

Rent expenses Expense

Cash Asset

Office equipment Asset

Salary expenses Expense

Salaries accrued Liability

Property tax expenses Expense

Prepaid expenses Asset

Office furniture Assets

Electricity and gas expenses Expense

Accounts payable Liability

Smith, capital Proprietorship

Service revenue Revenue

Accounts receivables Asset

Supplies expenses Expenses

Investment Asset

Table 1: Account types

(Source: Created by author)

2. Income statement – Normal view

6

Student Name

Student ID number

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEM AND PROCESSES

Figure 3: Income statement

(Sources: Created by author)

Income statement – formula view

7

Student Name

Student ID number

Figure 3: Income statement

(Sources: Created by author)

Income statement – formula view

7

Student Name

Student ID number

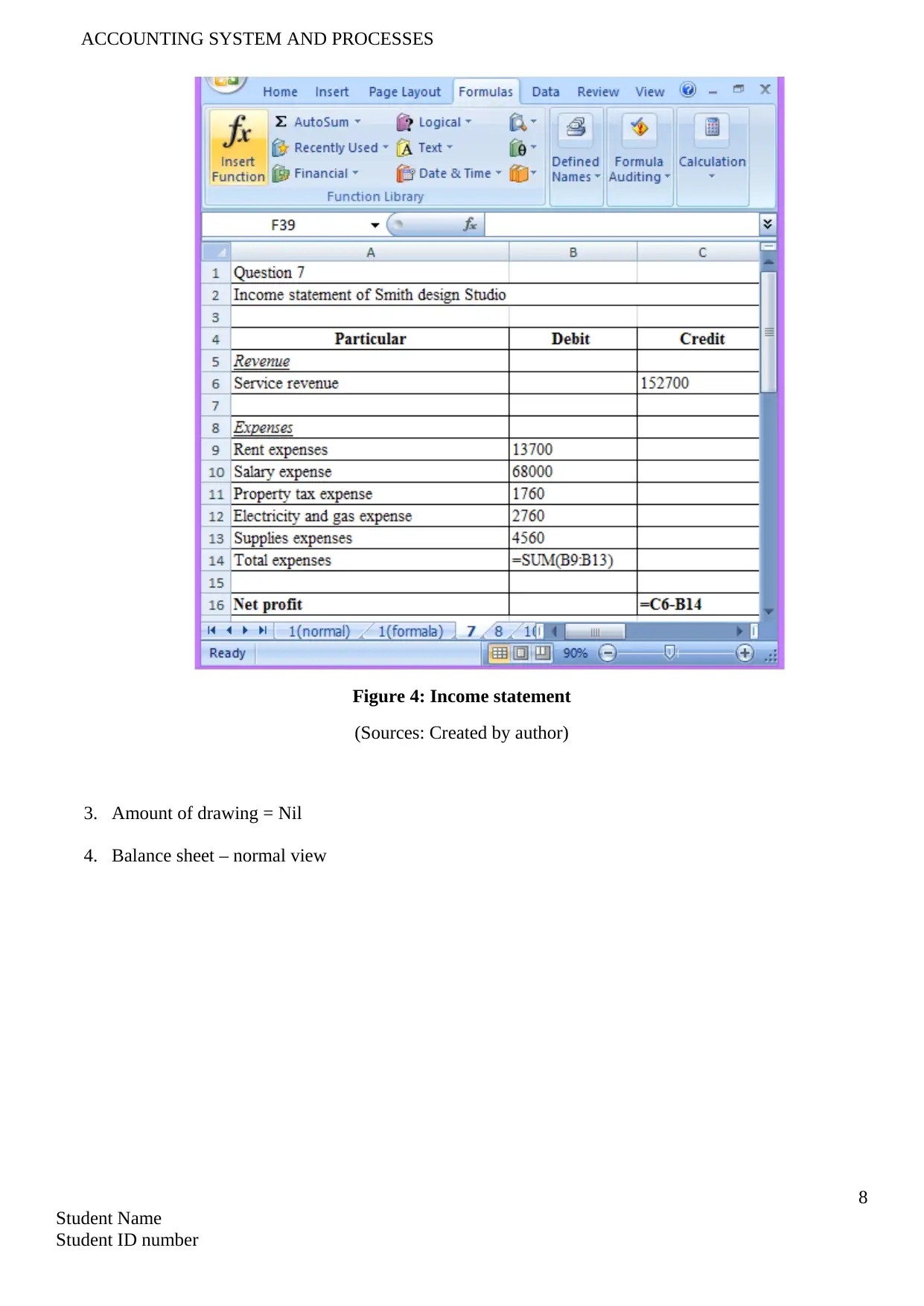

ACCOUNTING SYSTEM AND PROCESSES

Figure 4: Income statement

(Sources: Created by author)

3. Amount of drawing = Nil

4. Balance sheet – normal view

8

Student Name

Student ID number

Figure 4: Income statement

(Sources: Created by author)

3. Amount of drawing = Nil

4. Balance sheet – normal view

8

Student Name

Student ID number

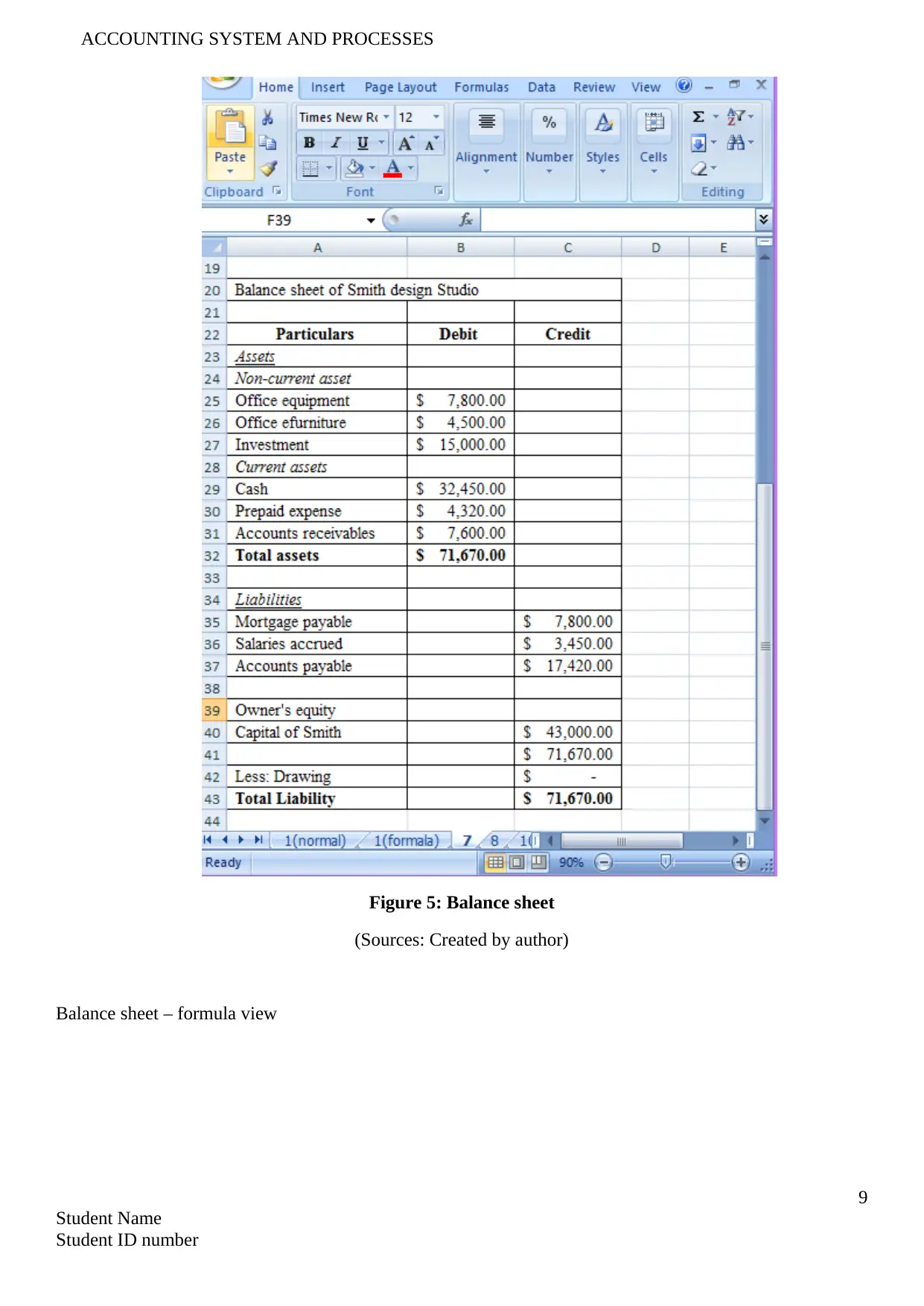

ACCOUNTING SYSTEM AND PROCESSES

Figure 5: Balance sheet

(Sources: Created by author)

Balance sheet – formula view

9

Student Name

Student ID number

Figure 5: Balance sheet

(Sources: Created by author)

Balance sheet – formula view

9

Student Name

Student ID number

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEM AND PROCESSES

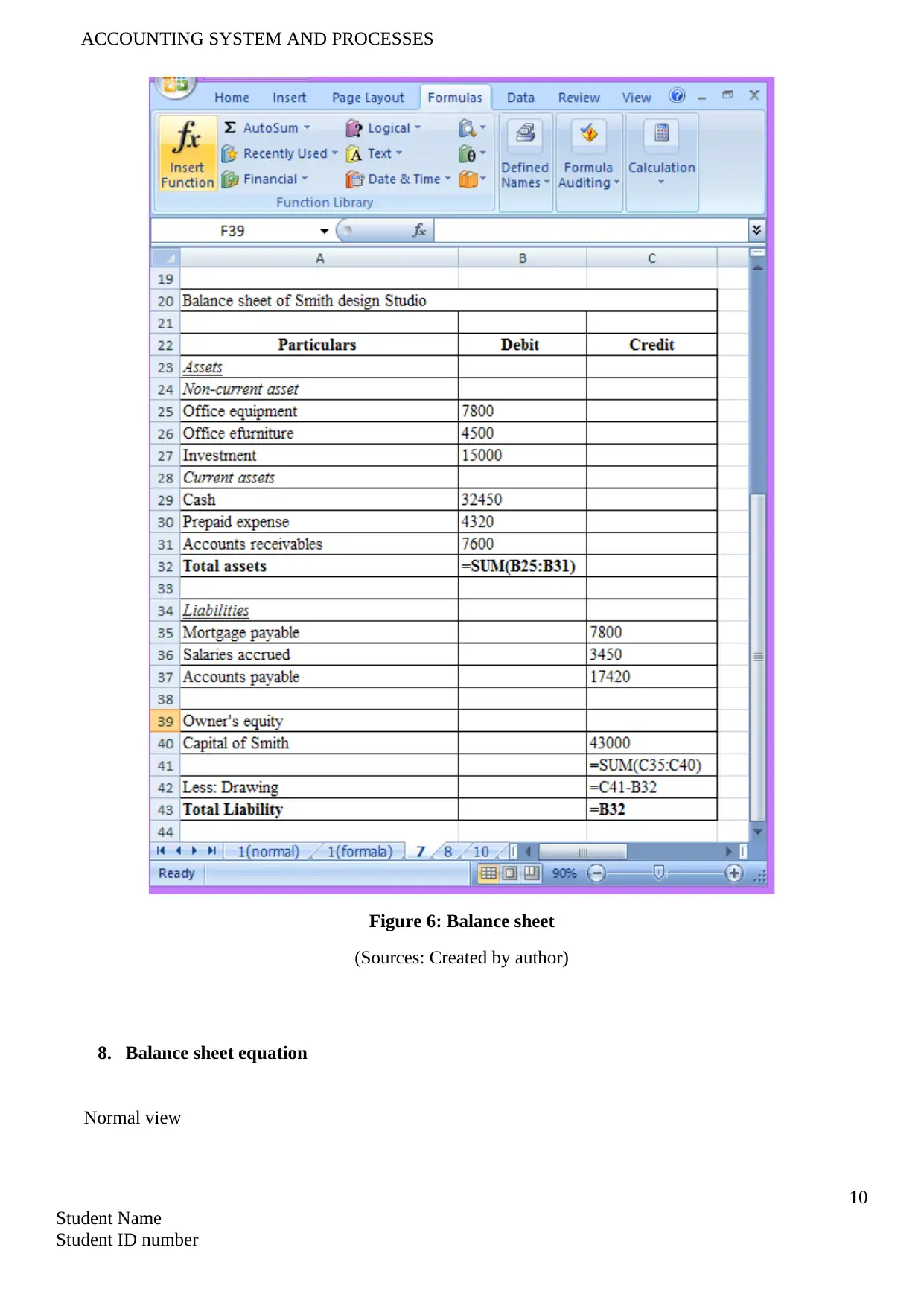

Figure 6: Balance sheet

(Sources: Created by author)

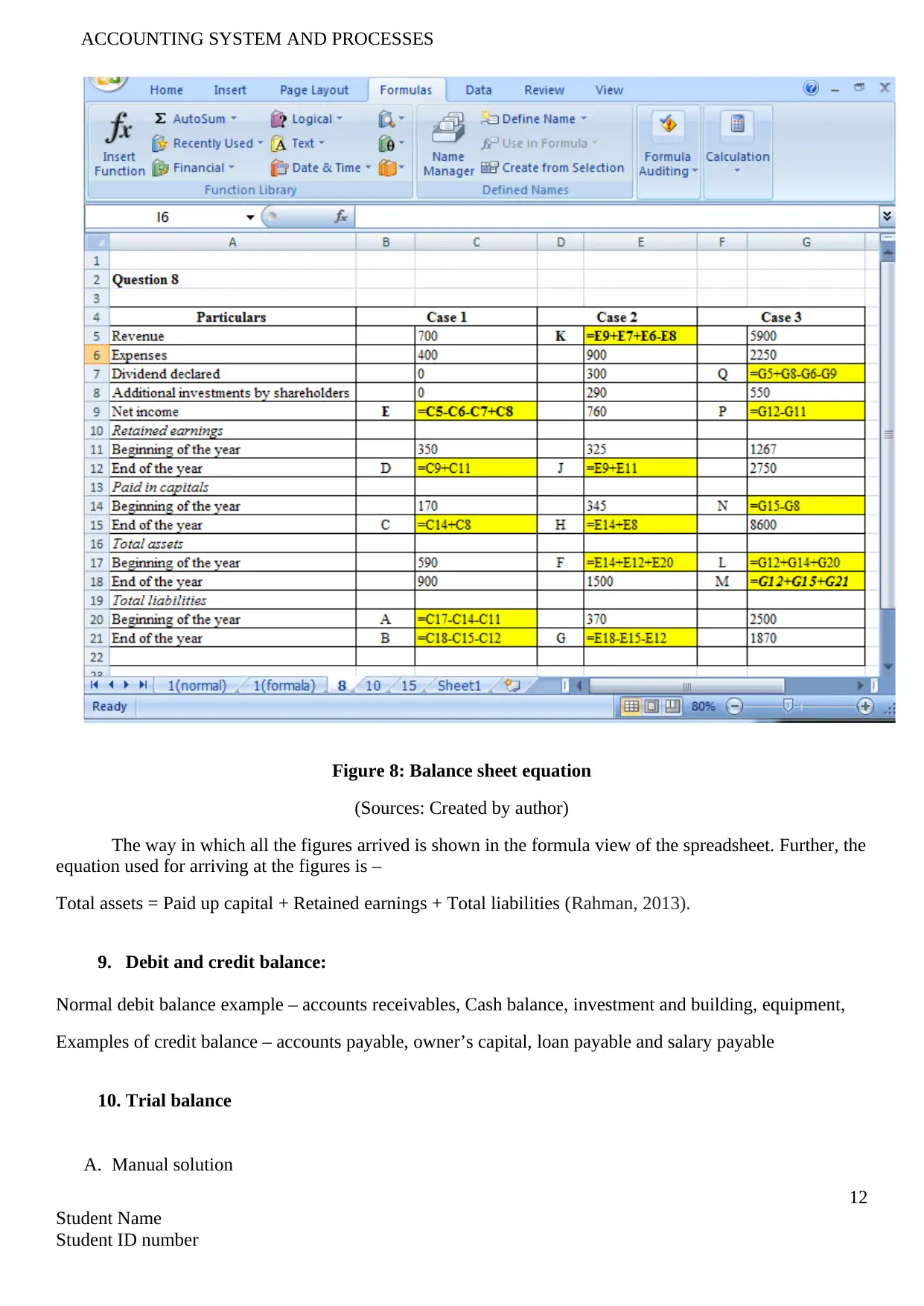

8. Balance sheet equation

Normal view

10

Student Name

Student ID number

Figure 6: Balance sheet

(Sources: Created by author)

8. Balance sheet equation

Normal view

10

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

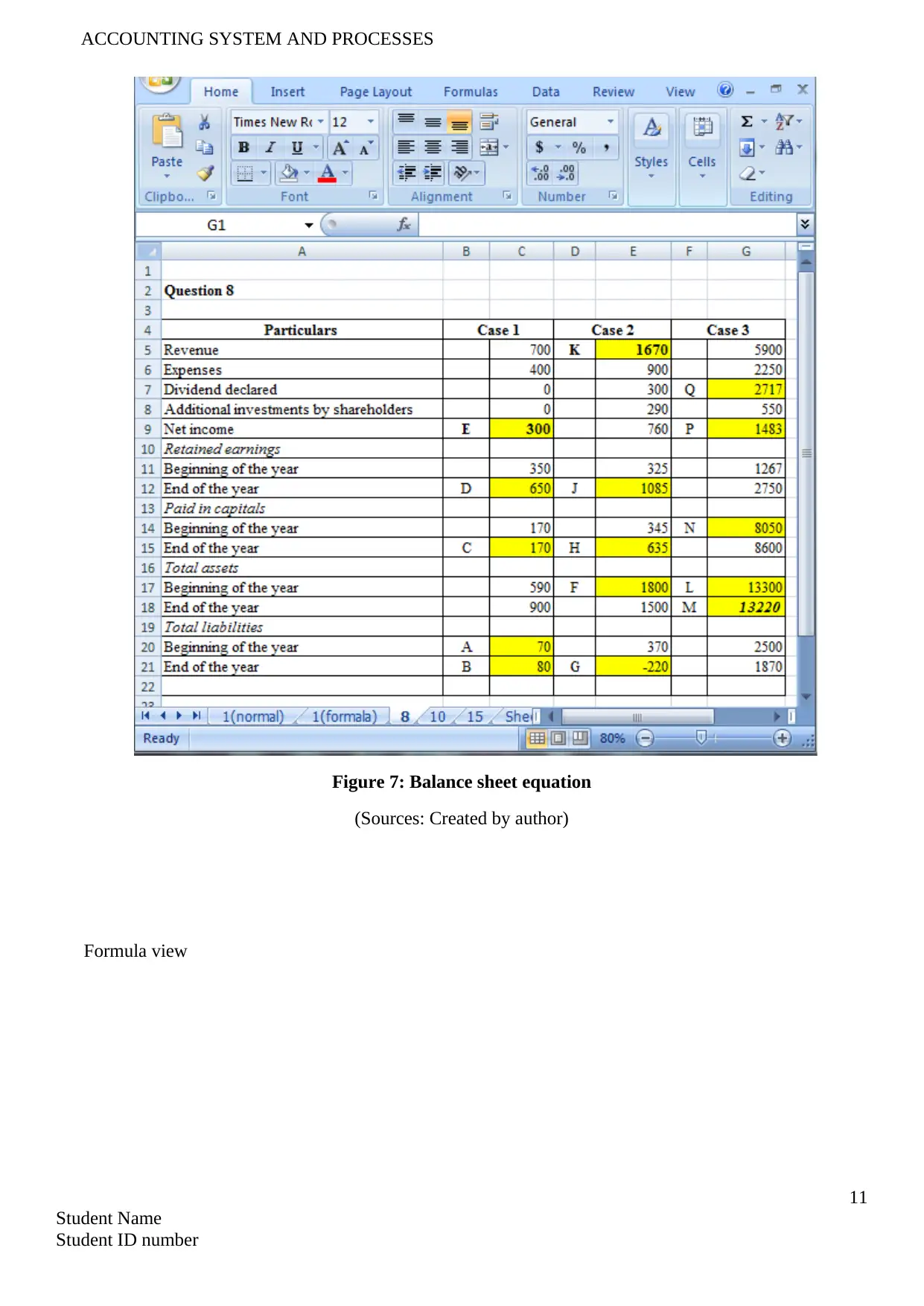

Figure 7: Balance sheet equation

(Sources: Created by author)

Formula view

11

Student Name

Student ID number

Figure 7: Balance sheet equation

(Sources: Created by author)

Formula view

11

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

Figure 8: Balance sheet equation

(Sources: Created by author)

The way in which all the figures arrived is shown in the formula view of the spreadsheet. Further, the

equation used for arriving at the figures is –

Total assets = Paid up capital + Retained earnings + Total liabilities (Rahman, 2013).

9. Debit and credit balance:

Normal debit balance example – accounts receivables, Cash balance, investment and building, equipment,

Examples of credit balance – accounts payable, owner’s capital, loan payable and salary payable

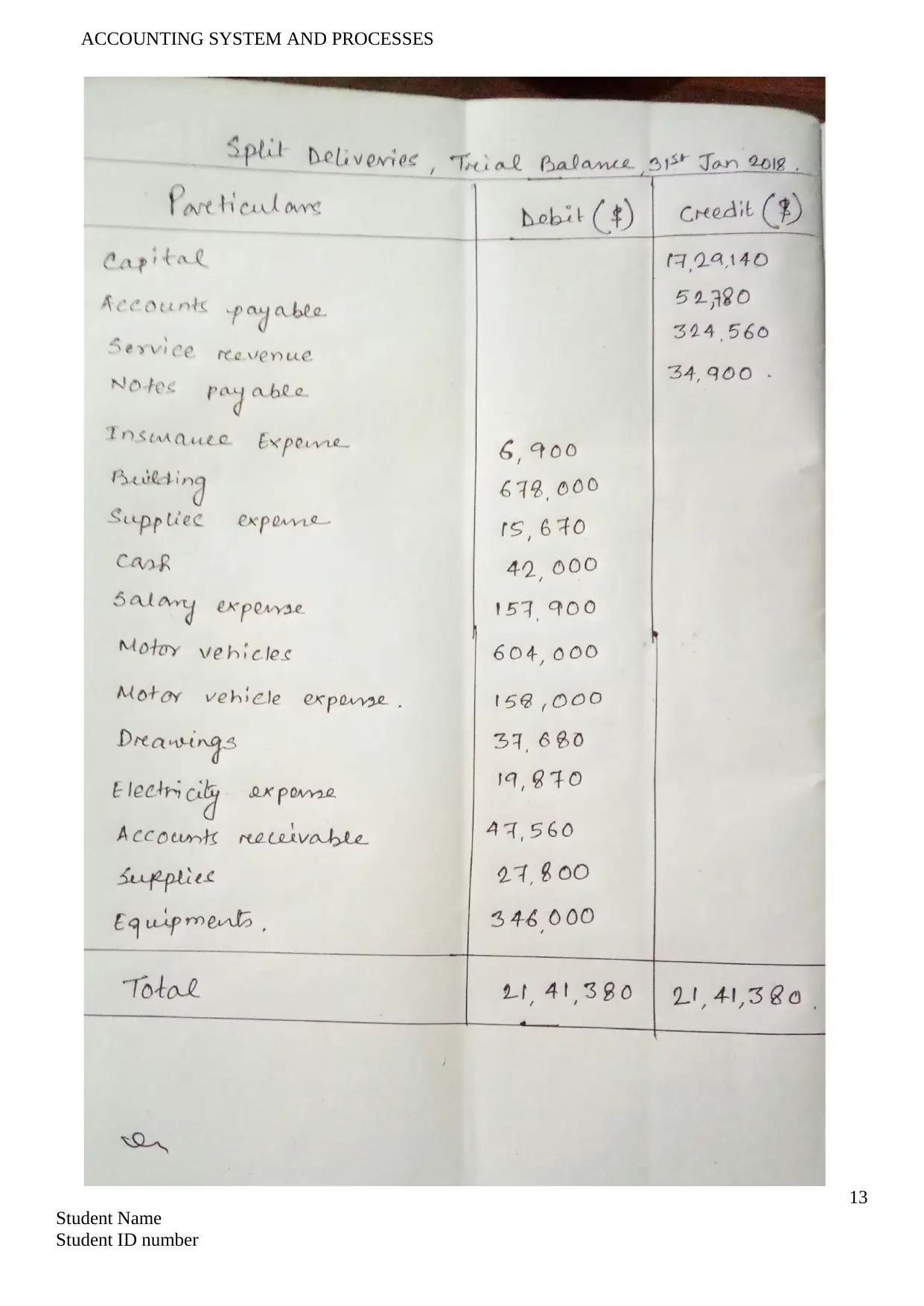

10. Trial balance

A. Manual solution

12

Student Name

Student ID number

Figure 8: Balance sheet equation

(Sources: Created by author)

The way in which all the figures arrived is shown in the formula view of the spreadsheet. Further, the

equation used for arriving at the figures is –

Total assets = Paid up capital + Retained earnings + Total liabilities (Rahman, 2013).

9. Debit and credit balance:

Normal debit balance example – accounts receivables, Cash balance, investment and building, equipment,

Examples of credit balance – accounts payable, owner’s capital, loan payable and salary payable

10. Trial balance

A. Manual solution

12

Student Name

Student ID number

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEM AND PROCESSES

13

Student Name

Student ID number

13

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

Figure 9: Manual solution

(Sources: Created by author)

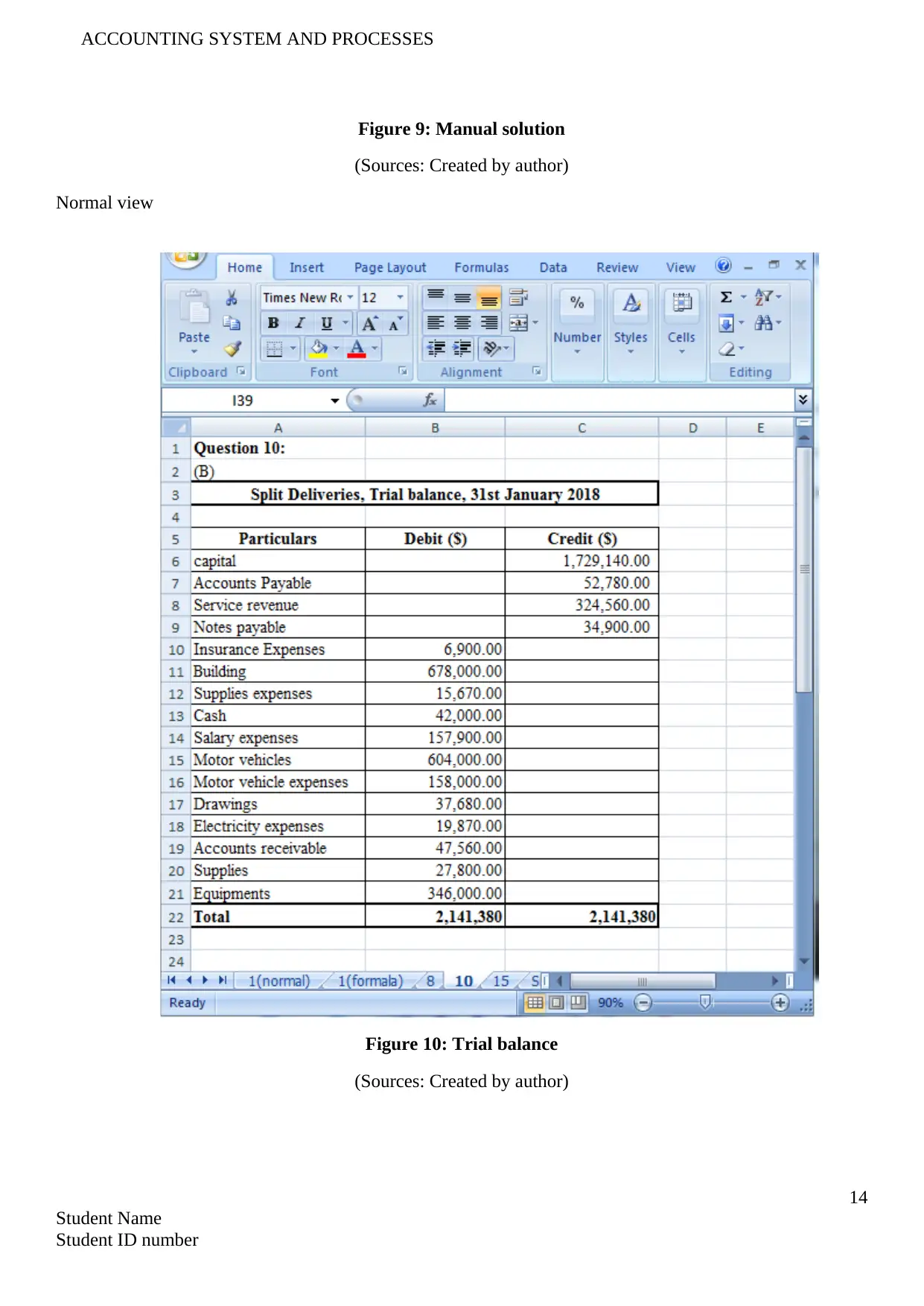

Normal view

Figure 10: Trial balance

(Sources: Created by author)

14

Student Name

Student ID number

Figure 9: Manual solution

(Sources: Created by author)

Normal view

Figure 10: Trial balance

(Sources: Created by author)

14

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

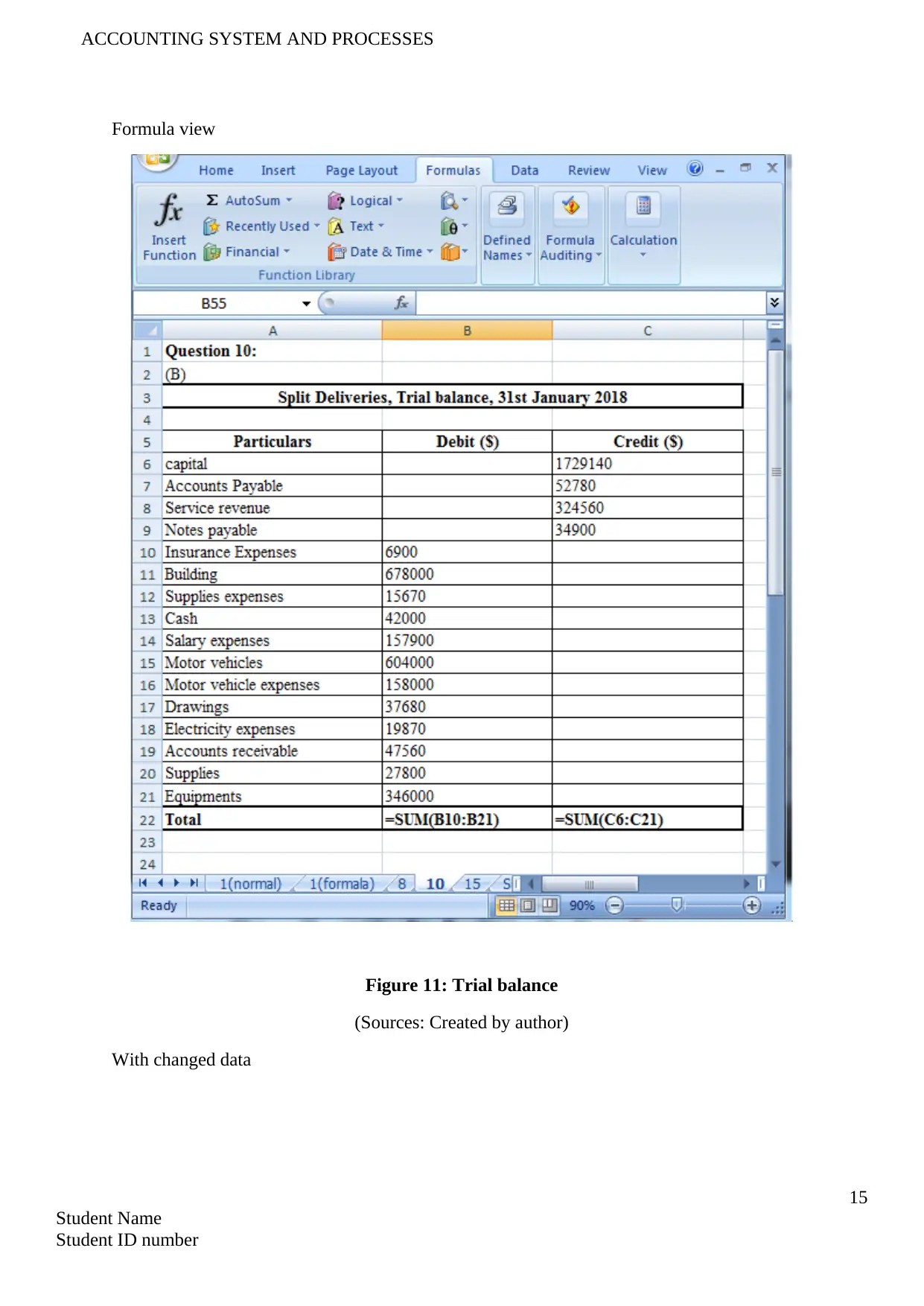

Formula view

Figure 11: Trial balance

(Sources: Created by author)

With changed data

15

Student Name

Student ID number

Formula view

Figure 11: Trial balance

(Sources: Created by author)

With changed data

15

Student Name

Student ID number

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

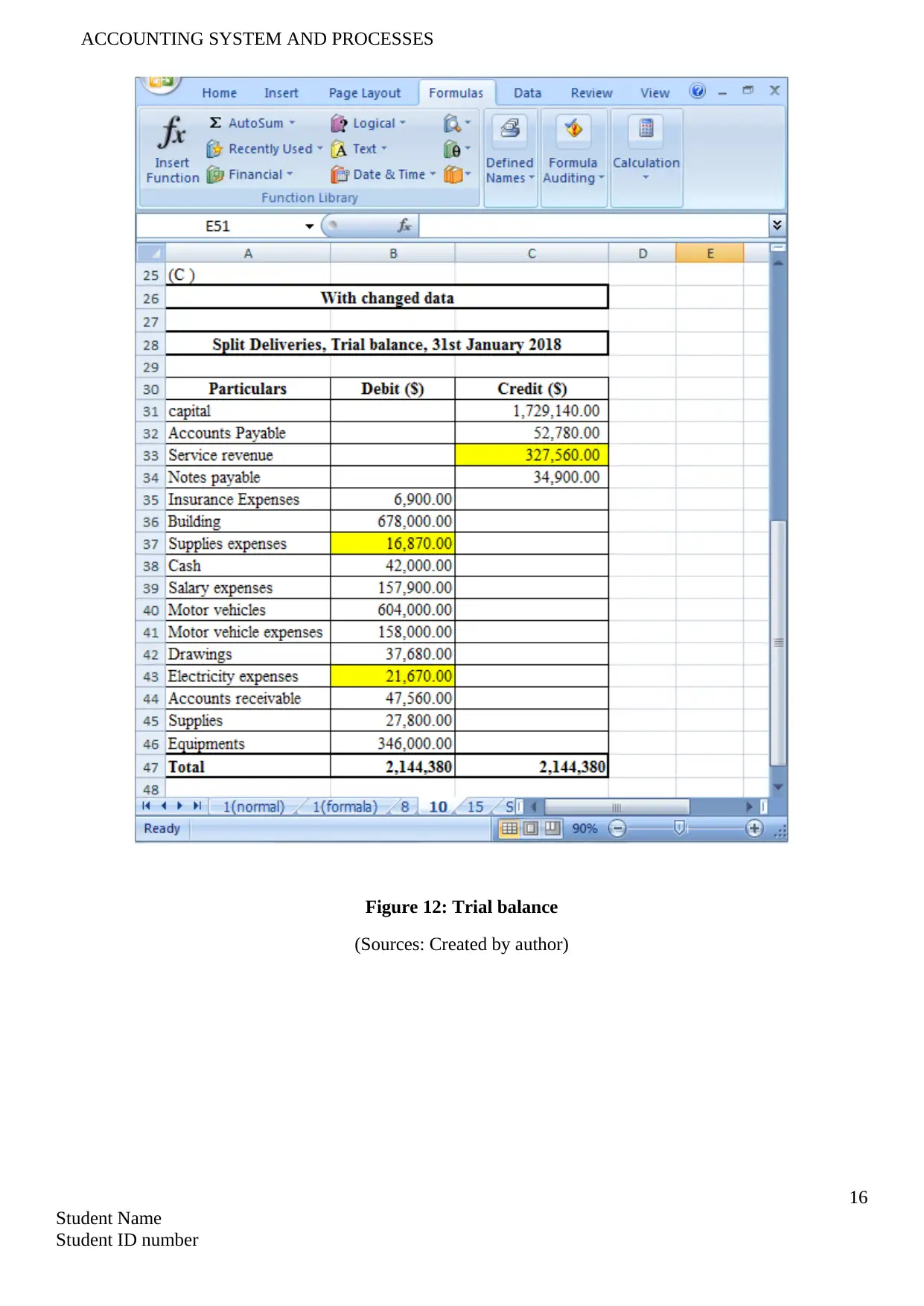

ACCOUNTING SYSTEM AND PROCESSES

Figure 12: Trial balance

(Sources: Created by author)

16

Student Name

Student ID number

Figure 12: Trial balance

(Sources: Created by author)

16

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

11. Crossword

Blank copy for crossword

Figure 13: Crossword

(Sources: Created by author)

17

Student Name

Student ID number

11. Crossword

Blank copy for crossword

Figure 13: Crossword

(Sources: Created by author)

17

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

Filled up copy

Figure 14: Crossword

(Sources: Created by author)

12. Adjusting entries

Deferred revenue – here the services is to provided later for which the revenue already raised

Example – service charges amounting to $ 10,000 for entire year charged at the beginning of the year.

Journal entry –

Service charges receivable a/c $ 10,000

To deferred revenue a/c $ 10,000

Deferred expenses – here the cast is already incurred but the service has not yet been consumed.

Example – insurance premium for $ 2,000 of April 2017 is paid in March 2017

Journal entry –

Prepaid insurance a/c $ 2,000

18

Student Name

Student ID number

Filled up copy

Figure 14: Crossword

(Sources: Created by author)

12. Adjusting entries

Deferred revenue – here the services is to provided later for which the revenue already raised

Example – service charges amounting to $ 10,000 for entire year charged at the beginning of the year.

Journal entry –

Service charges receivable a/c $ 10,000

To deferred revenue a/c $ 10,000

Deferred expenses – here the cast is already incurred but the service has not yet been consumed.

Example – insurance premium for $ 2,000 of April 2017 is paid in March 2017

Journal entry –

Prepaid insurance a/c $ 2,000

18

Student Name

Student ID number

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEM AND PROCESSES

To cash $ 2,000

Accrued revenue – the revenue here will be received later for which the amount is earned already

Example – rent amounting $ 20,000 for January 2017 will be received in March 2017.

Journal entry –

Accrued rent a/c debited $ 20,000

To rent a/c $ 20,000

Accrued expenses – here the payment will be made later for the expenses that is already incurred.

Example – interest for the month of January 2017 will be paid in March 2017

Journal entry –

Interest expenses a/c $ 5,000

To interest payable $ 5,000

13. Current and non-current liabilities

Current liabilities of the company are the short-term obligation for debt that is expected to get

liquidated in 12 months period. Examples of current liabilities are – short-term borrowings and accounts

payable. On the contrary, non-current liabilities of the company are the long-term obligation for debt that is

not expected to get liquidated in 12 months period. Examples of non-current liabilities are – long-term

borrowings and bonds payable (Brochet, Jagolinzer & Riedl, 2013).

14. Ratios

Current ratio – it measures the current assets of the company as against its current liabilities. It is calculated

through dividing the current assets by current liabilities of the company (Babalola & Abiola, 2013).

Example – current assets of the company $ 200,000 and current liabilities is $ 100,000

Therefore, Current ratio = $ 200,000/$ 100,000 = 2

15. Worksheets and financial reports

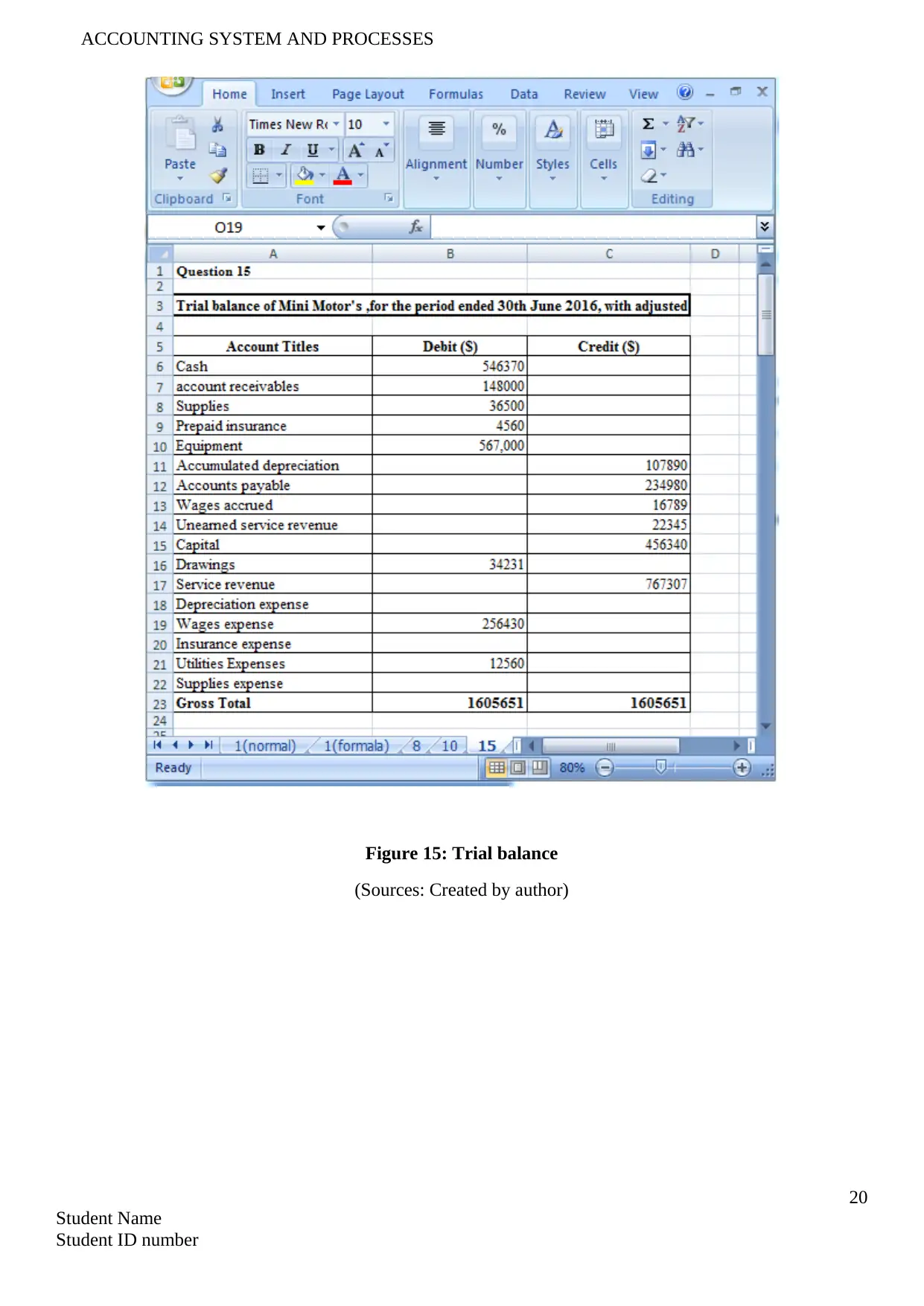

(A) Trial balance

19

Student Name

Student ID number

To cash $ 2,000

Accrued revenue – the revenue here will be received later for which the amount is earned already

Example – rent amounting $ 20,000 for January 2017 will be received in March 2017.

Journal entry –

Accrued rent a/c debited $ 20,000

To rent a/c $ 20,000

Accrued expenses – here the payment will be made later for the expenses that is already incurred.

Example – interest for the month of January 2017 will be paid in March 2017

Journal entry –

Interest expenses a/c $ 5,000

To interest payable $ 5,000

13. Current and non-current liabilities

Current liabilities of the company are the short-term obligation for debt that is expected to get

liquidated in 12 months period. Examples of current liabilities are – short-term borrowings and accounts

payable. On the contrary, non-current liabilities of the company are the long-term obligation for debt that is

not expected to get liquidated in 12 months period. Examples of non-current liabilities are – long-term

borrowings and bonds payable (Brochet, Jagolinzer & Riedl, 2013).

14. Ratios

Current ratio – it measures the current assets of the company as against its current liabilities. It is calculated

through dividing the current assets by current liabilities of the company (Babalola & Abiola, 2013).

Example – current assets of the company $ 200,000 and current liabilities is $ 100,000

Therefore, Current ratio = $ 200,000/$ 100,000 = 2

15. Worksheets and financial reports

(A) Trial balance

19

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

Figure 15: Trial balance

(Sources: Created by author)

20

Student Name

Student ID number

Figure 15: Trial balance

(Sources: Created by author)

20

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

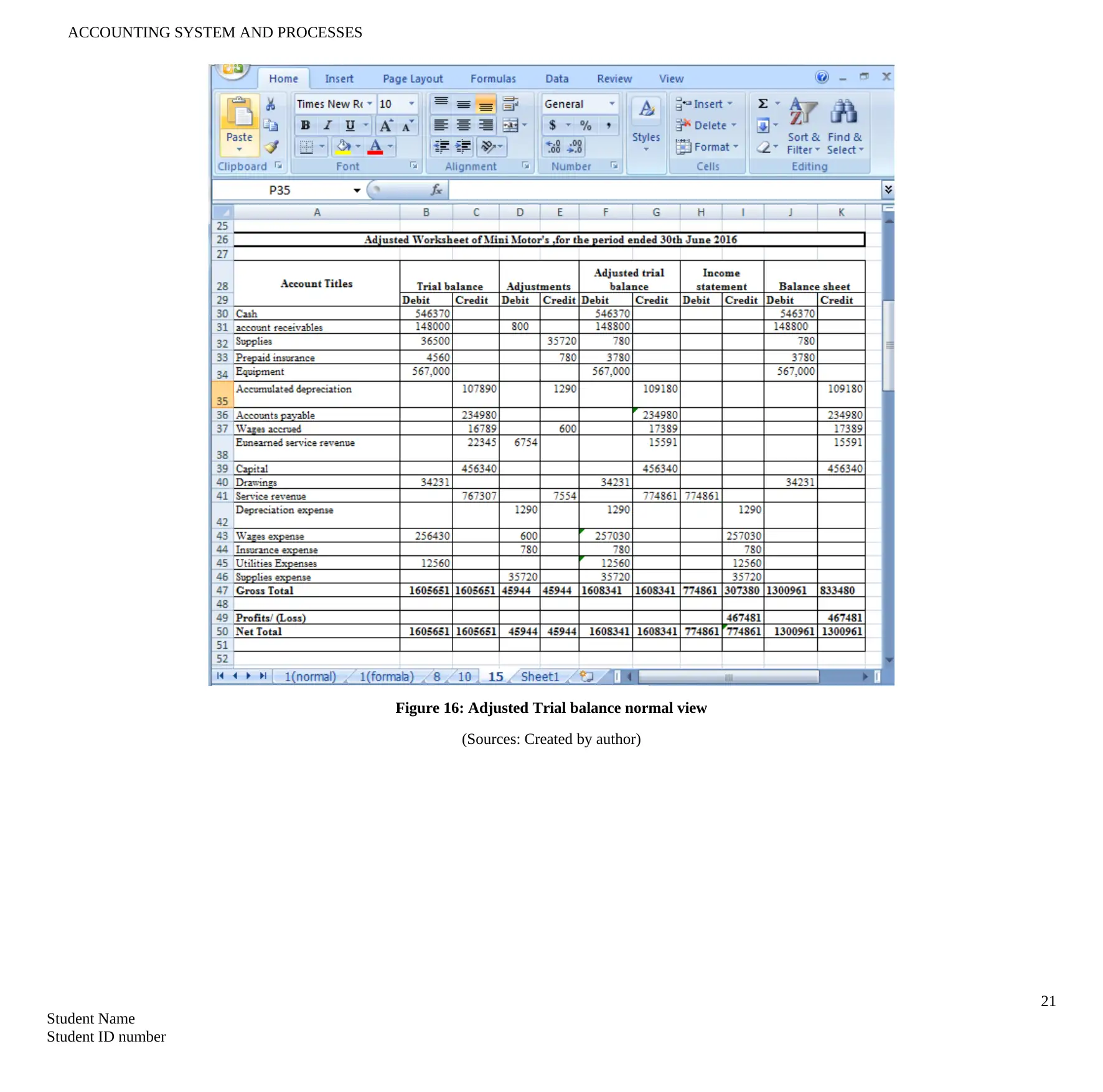

Figure 16: Adjusted Trial balance normal view

(Sources: Created by author)

21

Student Name

Student ID number

Figure 16: Adjusted Trial balance normal view

(Sources: Created by author)

21

Student Name

Student ID number

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEM AND PROCESSES

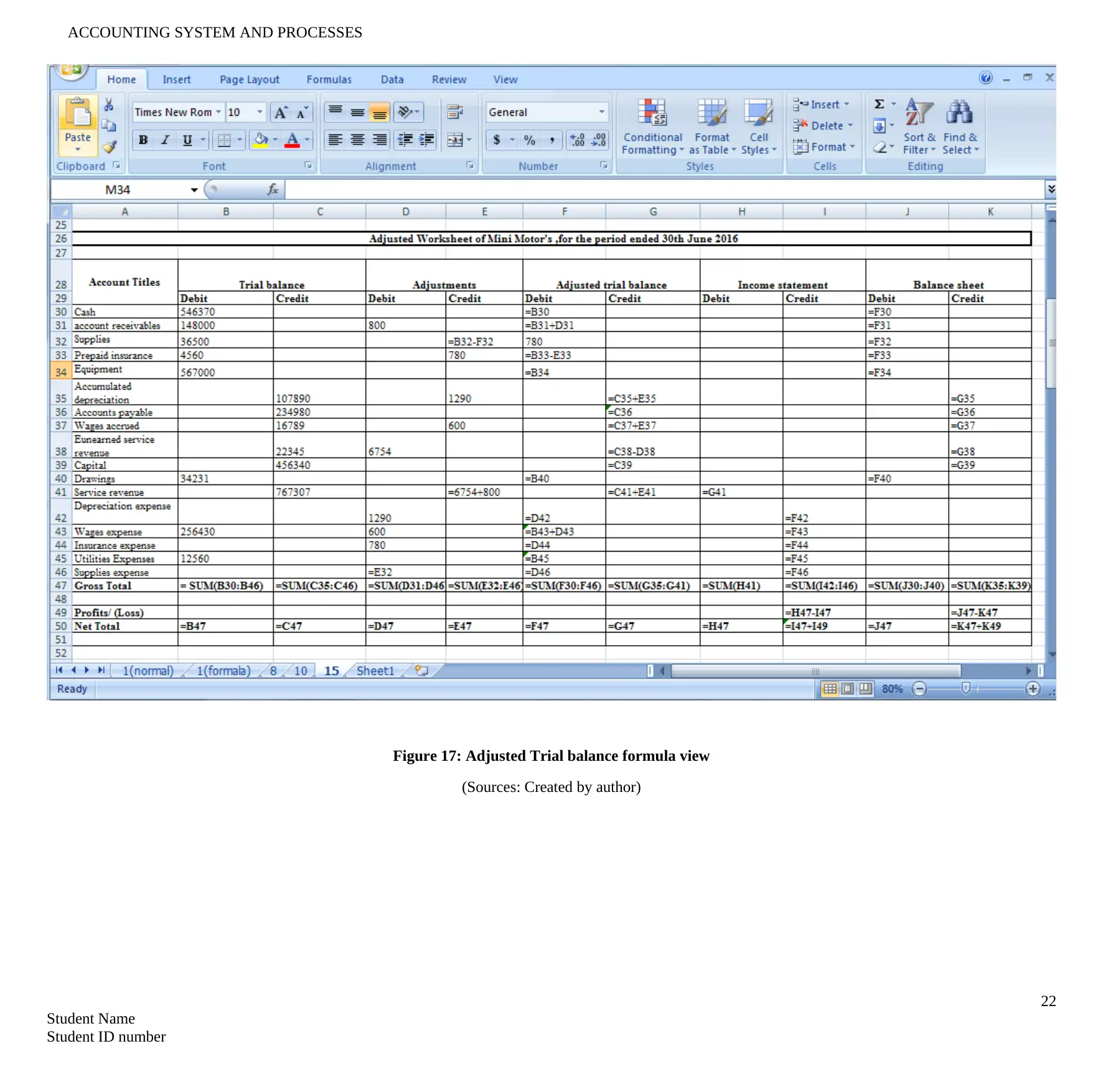

Figure 17: Adjusted Trial balance formula view

(Sources: Created by author)

22

Student Name

Student ID number

Figure 17: Adjusted Trial balance formula view

(Sources: Created by author)

22

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

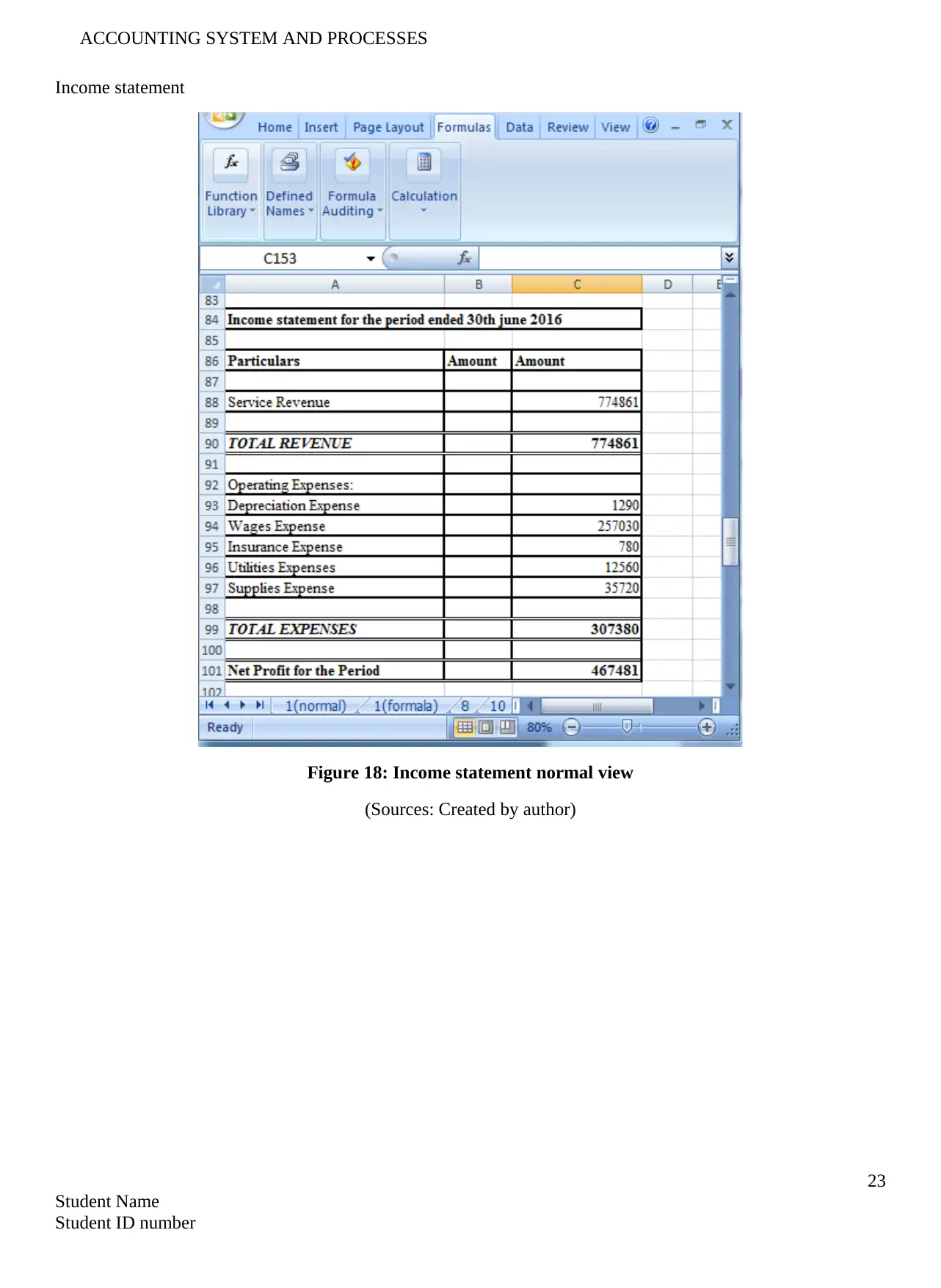

Income statement

Figure 18: Income statement normal view

(Sources: Created by author)

23

Student Name

Student ID number

Income statement

Figure 18: Income statement normal view

(Sources: Created by author)

23

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

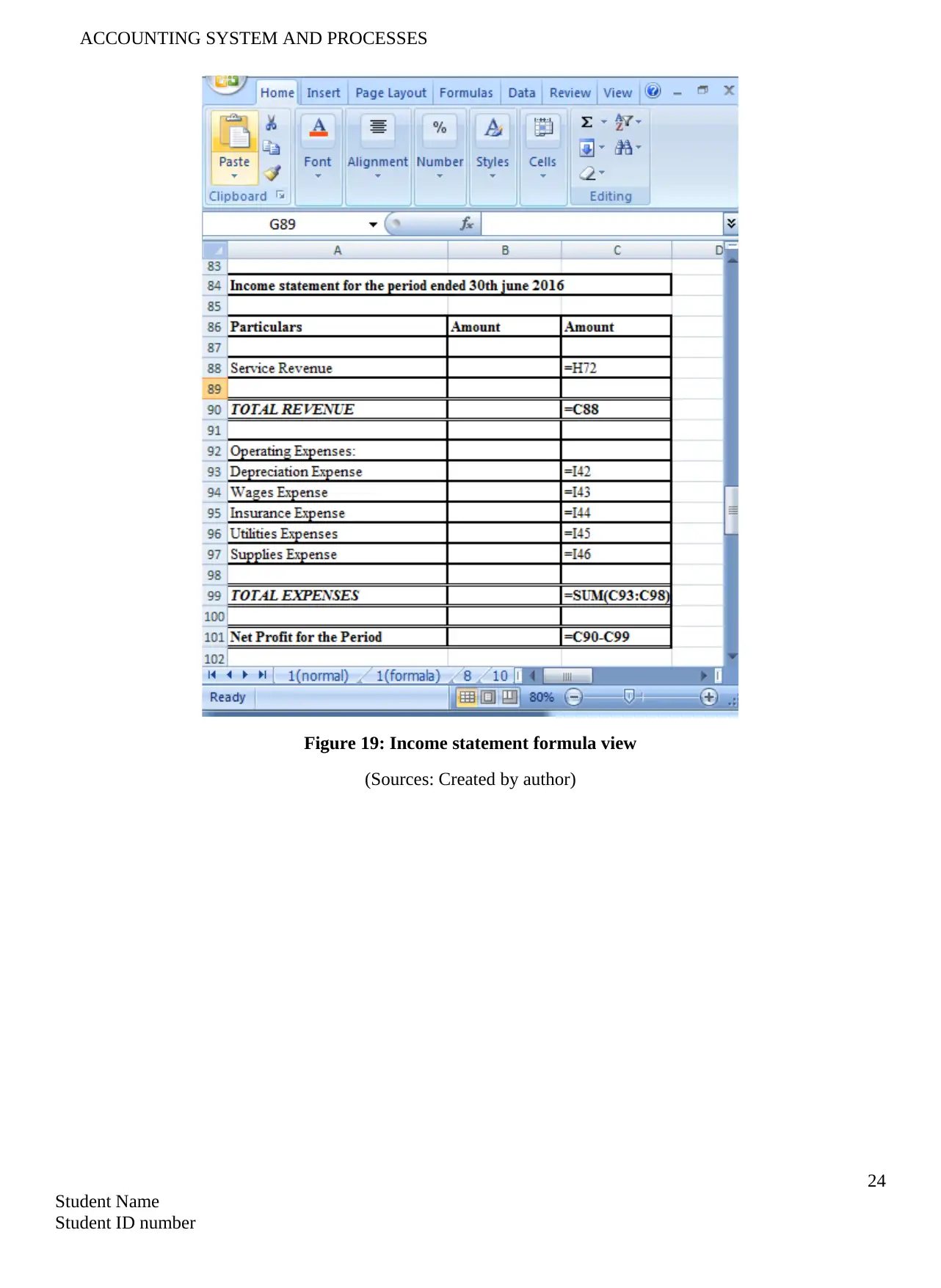

Figure 19: Income statement formula view

(Sources: Created by author)

24

Student Name

Student ID number

Figure 19: Income statement formula view

(Sources: Created by author)

24

Student Name

Student ID number

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEM AND PROCESSES

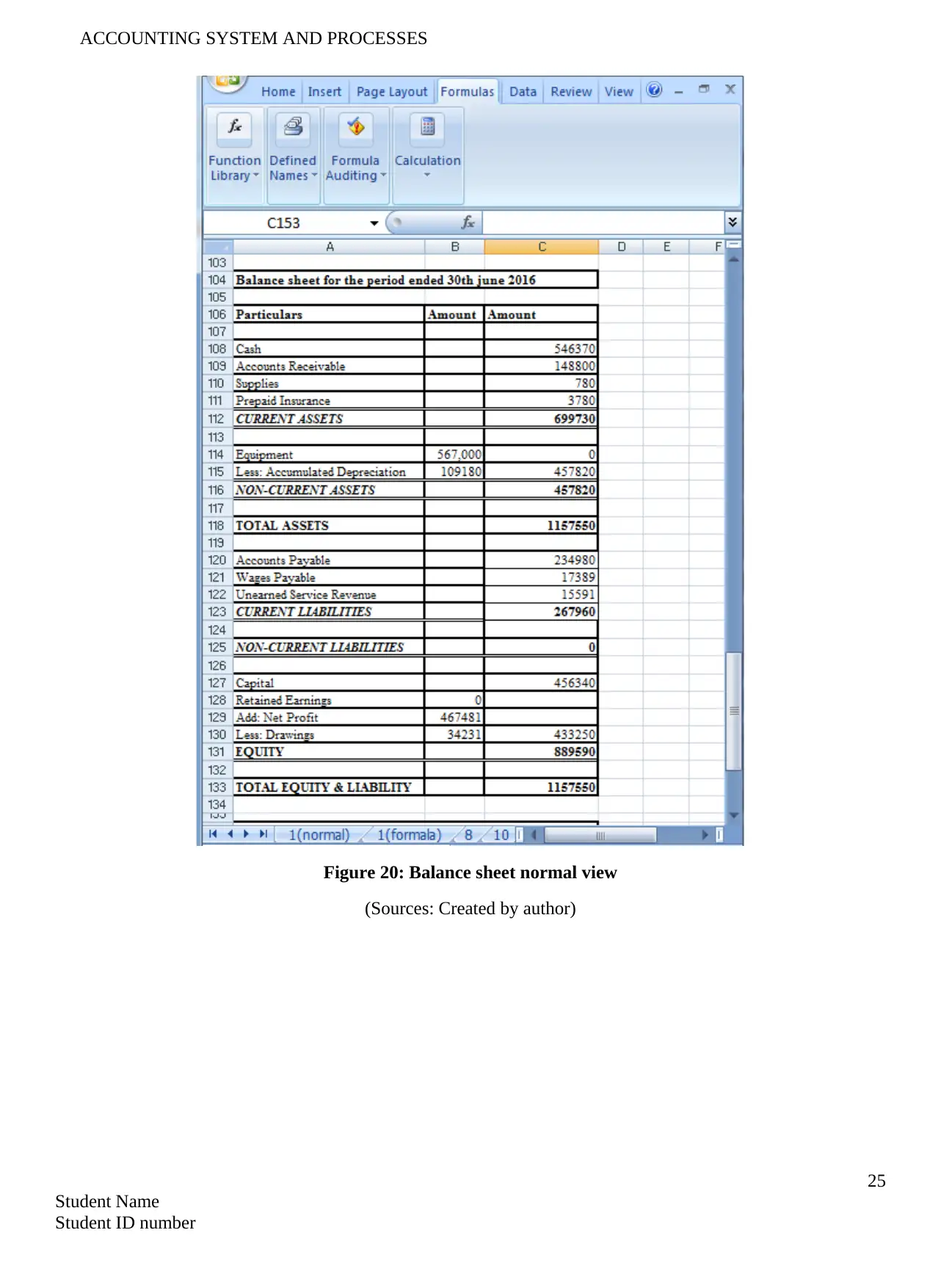

Figure 20: Balance sheet normal view

(Sources: Created by author)

25

Student Name

Student ID number

Figure 20: Balance sheet normal view

(Sources: Created by author)

25

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

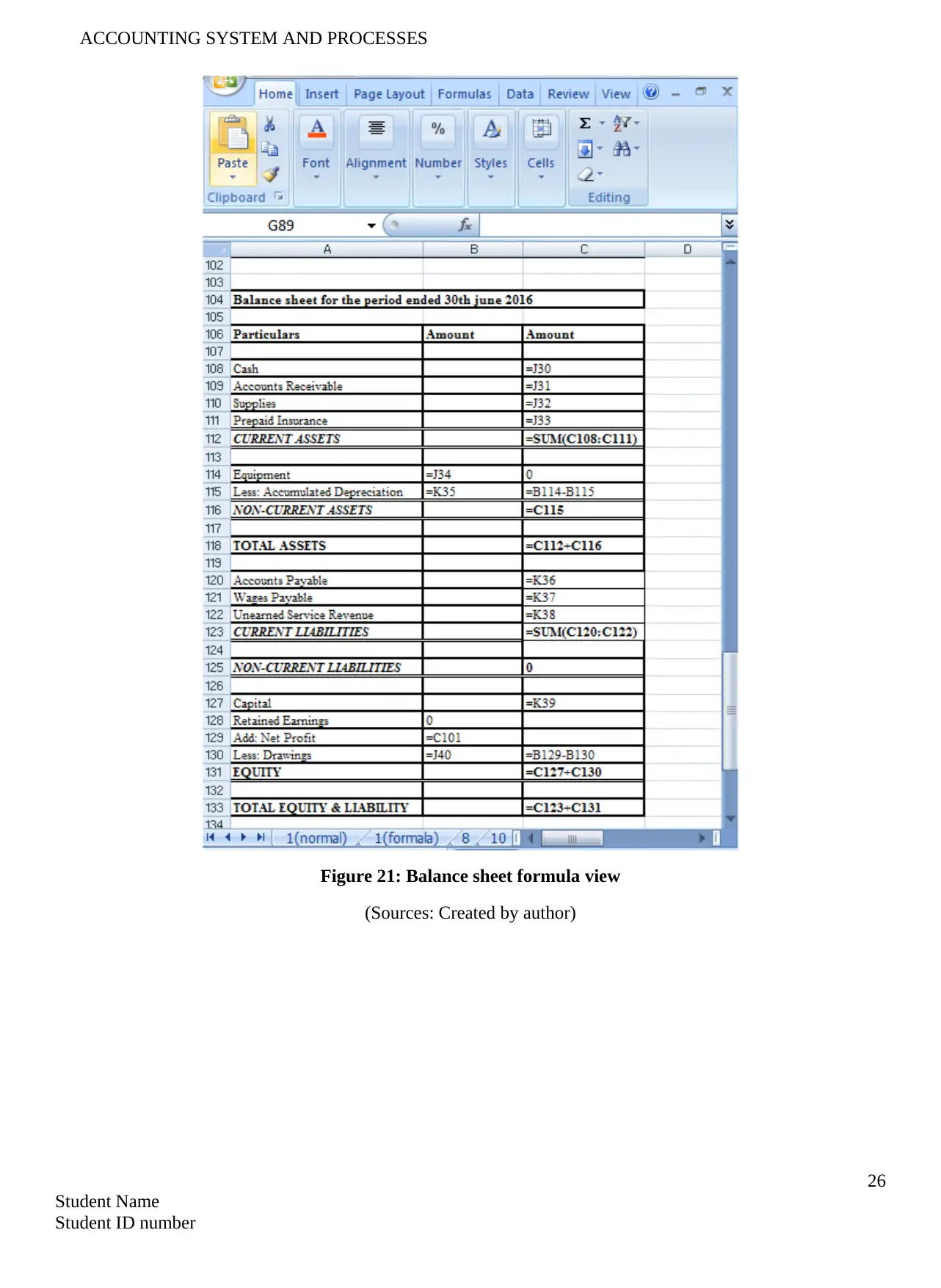

Figure 21: Balance sheet formula view

(Sources: Created by author)

26

Student Name

Student ID number

Figure 21: Balance sheet formula view

(Sources: Created by author)

26

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

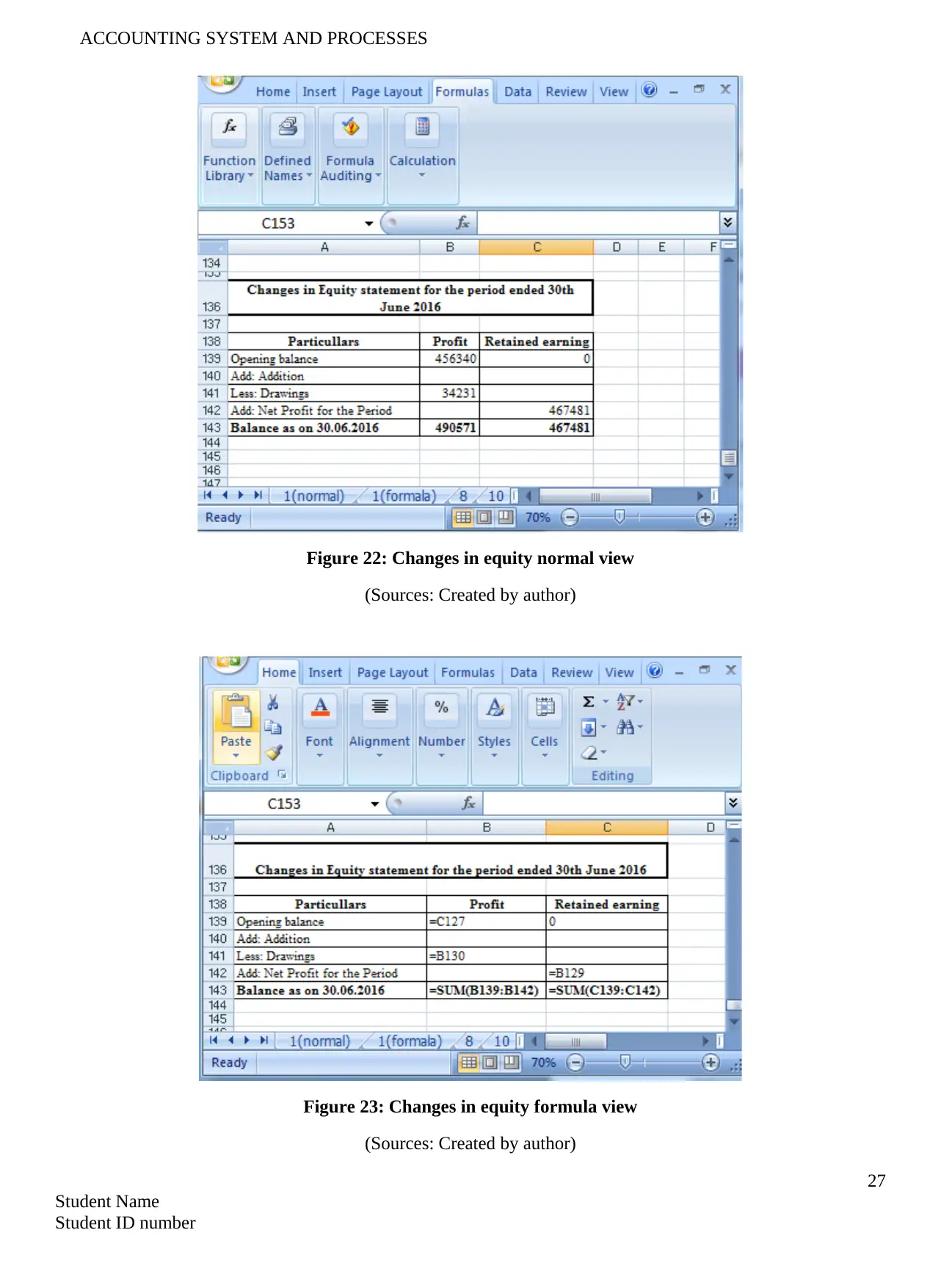

Figure 22: Changes in equity normal view

(Sources: Created by author)

Figure 23: Changes in equity formula view

(Sources: Created by author)

27

Student Name

Student ID number

Figure 22: Changes in equity normal view

(Sources: Created by author)

Figure 23: Changes in equity formula view

(Sources: Created by author)

27

Student Name

Student ID number

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEM AND PROCESSES

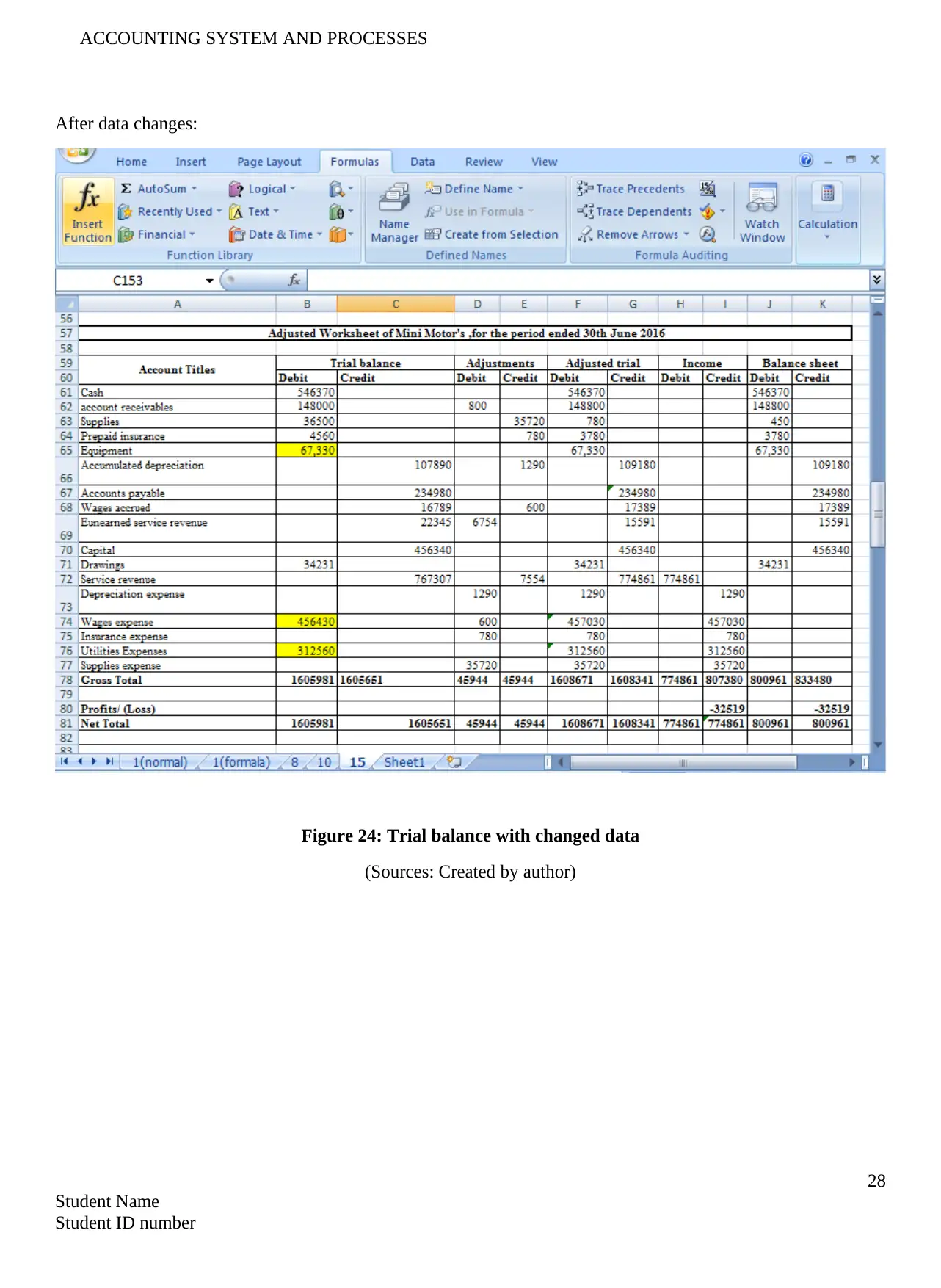

After data changes:

Figure 24: Trial balance with changed data

(Sources: Created by author)

28

Student Name

Student ID number

After data changes:

Figure 24: Trial balance with changed data

(Sources: Created by author)

28

Student Name

Student ID number

ACCOUNTING SYSTEM AND PROCESSES

References:

ABC Learning collapse case study. (2018). Cpaaustralia.com.au. Retrieved 20 March 2018, from

https://www.cpaaustralia.com.au/professional-resources/education/abc-learning-collapse-case-study

Babalola, Y. A., & Abiola, F. R. (2013). Financial ratio analysis of firms: A tool for decision

making. International journal of management sciences, 1(4), 132-137.

Bawankule, K. L. (2015). Design and implementation of massive MYSQL data intelligent export system to

excel by using Apache-POI libraries. International Journal of Computer Science and Network Security

(IJCSNS), 15(9), 85.

Brigham, E. F., & Ehrhardt, M. C. (2013). Financial management: Theory & practice. Cengage Learning.

Brochet, F., Jagolinzer, A. D., & Riedl, E. J. (2013). Mandatory IFRS adoption and financial statement

comparability. Contemporary Accounting Research, 30(4), 1373-1400.

Dalnial, H., Kamaluddin, A., Sanusi, Z. M., & Khairuddin, K. S. (2014). Detecting fraudulent financial reporting

through financial statement analysis. Journal of Advanced Management Science, 2(1).

Ferro, M. J., & Martins, H. F. (2016). Academic plagiarism: yielding to temptation. British Journal of

Education, Society & Behavioural Science, 13(1), 1-11.

Kim, M., Batchu, S. K., & Sirota, J. (2016). U.S. Patent No. 9,235,717. Washington, DC: U.S. Patent and

Trademark Office.

Lin, C. C., Chiu, A. A., Huang, S. Y., & Yen, D. C. (2015). Detecting the financial statement fraud: The analysis

of the differences between data mining techniques and experts’ judgments. Knowledge-Based

Systems, 89, 459-470.

Rahman, A. R. (2013). The Australian Accounting Standards Review Board (RLE Accounting): The

Establishment of Its Participative Review Process. Routledge.

Walker, J. S., Tulley, S. C., Jorasch, J. A., Sammon, R. P., & Gelman, G. M. (2016). U.S. Patent Application

No. 14/992,770.

29

Student Name

Student ID number

References:

ABC Learning collapse case study. (2018). Cpaaustralia.com.au. Retrieved 20 March 2018, from

https://www.cpaaustralia.com.au/professional-resources/education/abc-learning-collapse-case-study

Babalola, Y. A., & Abiola, F. R. (2013). Financial ratio analysis of firms: A tool for decision

making. International journal of management sciences, 1(4), 132-137.

Bawankule, K. L. (2015). Design and implementation of massive MYSQL data intelligent export system to

excel by using Apache-POI libraries. International Journal of Computer Science and Network Security

(IJCSNS), 15(9), 85.

Brigham, E. F., & Ehrhardt, M. C. (2013). Financial management: Theory & practice. Cengage Learning.

Brochet, F., Jagolinzer, A. D., & Riedl, E. J. (2013). Mandatory IFRS adoption and financial statement

comparability. Contemporary Accounting Research, 30(4), 1373-1400.

Dalnial, H., Kamaluddin, A., Sanusi, Z. M., & Khairuddin, K. S. (2014). Detecting fraudulent financial reporting

through financial statement analysis. Journal of Advanced Management Science, 2(1).

Ferro, M. J., & Martins, H. F. (2016). Academic plagiarism: yielding to temptation. British Journal of

Education, Society & Behavioural Science, 13(1), 1-11.

Kim, M., Batchu, S. K., & Sirota, J. (2016). U.S. Patent No. 9,235,717. Washington, DC: U.S. Patent and

Trademark Office.

Lin, C. C., Chiu, A. A., Huang, S. Y., & Yen, D. C. (2015). Detecting the financial statement fraud: The analysis

of the differences between data mining techniques and experts’ judgments. Knowledge-Based

Systems, 89, 459-470.

Rahman, A. R. (2013). The Australian Accounting Standards Review Board (RLE Accounting): The

Establishment of Its Participative Review Process. Routledge.

Walker, J. S., Tulley, S. C., Jorasch, J. A., Sammon, R. P., & Gelman, G. M. (2016). U.S. Patent Application

No. 14/992,770.

29

Student Name

Student ID number

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.