Accounting System and Process: Management of Inventory, Bank Reconciliation

Added on 2023-06-04

12 Pages1169 Words140 Views

Running head: ACCOUNTING SYSTEM AND PROCESS

Accounting system and process

Subject code

Subject name

Student Name

Student ID

Assignment task number

Author note

Accounting system and process

Subject code

Subject name

Student Name

Student ID

Assignment task number

Author note

2ACCOUNTING SYSTEM AND PROCESS

Table of Contents

Part B- Management of Inventory...................................................................................................3

Part C – Bank reconciliation............................................................................................................9

Reference list.................................................................................................................................12

Student name

Student ID Page 2

Table of Contents

Part B- Management of Inventory...................................................................................................3

Part C – Bank reconciliation............................................................................................................9

Reference list.................................................................................................................................12

Student name

Student ID Page 2

3ACCOUNTING SYSTEM AND PROCESS

Part B- Management of Inventory

Distinction between the perpetual and periodic inventory

The periodic system refers to the use of the occasional physical count for the

measurement of inventory level along with the cost of goods sold. The Purchases are recorded in

the account for purchase; the cost of goods sold and the inventory account are updates at the end

of set period. The time period can be a month, a quarter and a year (Bragg, 2013). The cost of

goods sold is the accounting metric that if reduced from the revenue represents the gross margin

of the company.

The cost of goods sold under the periodic inventory system is evaluated by the formula

Cost of goods sold = Opening inventory balance + cost of purchase of inventory- Cost of closing

inventory

On the other hand the perpetual system keeps a record of the balances of the stock in a

continuous manner along with automatic updates at the time when the products are transacted.

The returns and the purchase are recorded immediately in the inventory account (O'neil, 2017).

In case of there is no damage or theft; the balance of the inventory account is accurate. There is a

continuous update of the cost of goods sold at the time the sale is made. There is a use of the

digital technology for tracking in the real time electronically in this system.

The major differences of the two inventory measurement systems are as follows:

1. The Perpetual Inventory System is conducted on the basis of records book whereas in

case of the System of Periodic Inventor they considers the base by the physical

verification.

2. In case of Perpetual Inventory System the inventories are recorded and updated in a

continuous manner automatically as and when the inventory transaction occurs. On the

other hand, in case of System of Periodic Inventory the records are made manually after

some duration (Chołodowicz & Orłowski, 2015).

3. The information of real-time of sales of inventory and cost is provided in case system of

perpetual inventory, however in case of the system of periodic inventory gives

knowledge about the cost of goods sold and stock.

4. For the system of perpetual inventory, the loss of commodities is added in closing Stock.

On the other hand, for system of periodic inventory the same is added in cost of goods

sold.

5. In addition to that for system of perpetual inventory, there exists no meddling in the usual

workflow during verification and taking of stock whereas in case of periodic inventory,

the day to day operations of business may be terminated (Brooks et al., 2018).

It can be said that the accounting for periodic inventory is better in case of the small scale

businesses due to the expense of obtaining the technology and staff for supporting the perpetual

system. However, there is a risk in case of periodic system of inaccuracy due to manual

calculation, hence suitable for large scale businesses (Nisha, 2015).

In the present discussion the company of Fashion Haven who deals with the operations of

cloth retailing business can apply the perpetual inventory system. This would help them to make

regular updates in the general ledger. Moreover, as the transactions are automated and systematic

under the perpetual system will be suitable for the business of Fashion Haven for detection of the

errors and get accurate results.

Calculation of COGS and closing inventory for May

Student name

Student ID Page 3

Part B- Management of Inventory

Distinction between the perpetual and periodic inventory

The periodic system refers to the use of the occasional physical count for the

measurement of inventory level along with the cost of goods sold. The Purchases are recorded in

the account for purchase; the cost of goods sold and the inventory account are updates at the end

of set period. The time period can be a month, a quarter and a year (Bragg, 2013). The cost of

goods sold is the accounting metric that if reduced from the revenue represents the gross margin

of the company.

The cost of goods sold under the periodic inventory system is evaluated by the formula

Cost of goods sold = Opening inventory balance + cost of purchase of inventory- Cost of closing

inventory

On the other hand the perpetual system keeps a record of the balances of the stock in a

continuous manner along with automatic updates at the time when the products are transacted.

The returns and the purchase are recorded immediately in the inventory account (O'neil, 2017).

In case of there is no damage or theft; the balance of the inventory account is accurate. There is a

continuous update of the cost of goods sold at the time the sale is made. There is a use of the

digital technology for tracking in the real time electronically in this system.

The major differences of the two inventory measurement systems are as follows:

1. The Perpetual Inventory System is conducted on the basis of records book whereas in

case of the System of Periodic Inventor they considers the base by the physical

verification.

2. In case of Perpetual Inventory System the inventories are recorded and updated in a

continuous manner automatically as and when the inventory transaction occurs. On the

other hand, in case of System of Periodic Inventory the records are made manually after

some duration (Chołodowicz & Orłowski, 2015).

3. The information of real-time of sales of inventory and cost is provided in case system of

perpetual inventory, however in case of the system of periodic inventory gives

knowledge about the cost of goods sold and stock.

4. For the system of perpetual inventory, the loss of commodities is added in closing Stock.

On the other hand, for system of periodic inventory the same is added in cost of goods

sold.

5. In addition to that for system of perpetual inventory, there exists no meddling in the usual

workflow during verification and taking of stock whereas in case of periodic inventory,

the day to day operations of business may be terminated (Brooks et al., 2018).

It can be said that the accounting for periodic inventory is better in case of the small scale

businesses due to the expense of obtaining the technology and staff for supporting the perpetual

system. However, there is a risk in case of periodic system of inaccuracy due to manual

calculation, hence suitable for large scale businesses (Nisha, 2015).

In the present discussion the company of Fashion Haven who deals with the operations of

cloth retailing business can apply the perpetual inventory system. This would help them to make

regular updates in the general ledger. Moreover, as the transactions are automated and systematic

under the perpetual system will be suitable for the business of Fashion Haven for detection of the

errors and get accurate results.

Calculation of COGS and closing inventory for May

Student name

Student ID Page 3

4ACCOUNTING SYSTEM AND PROCESS

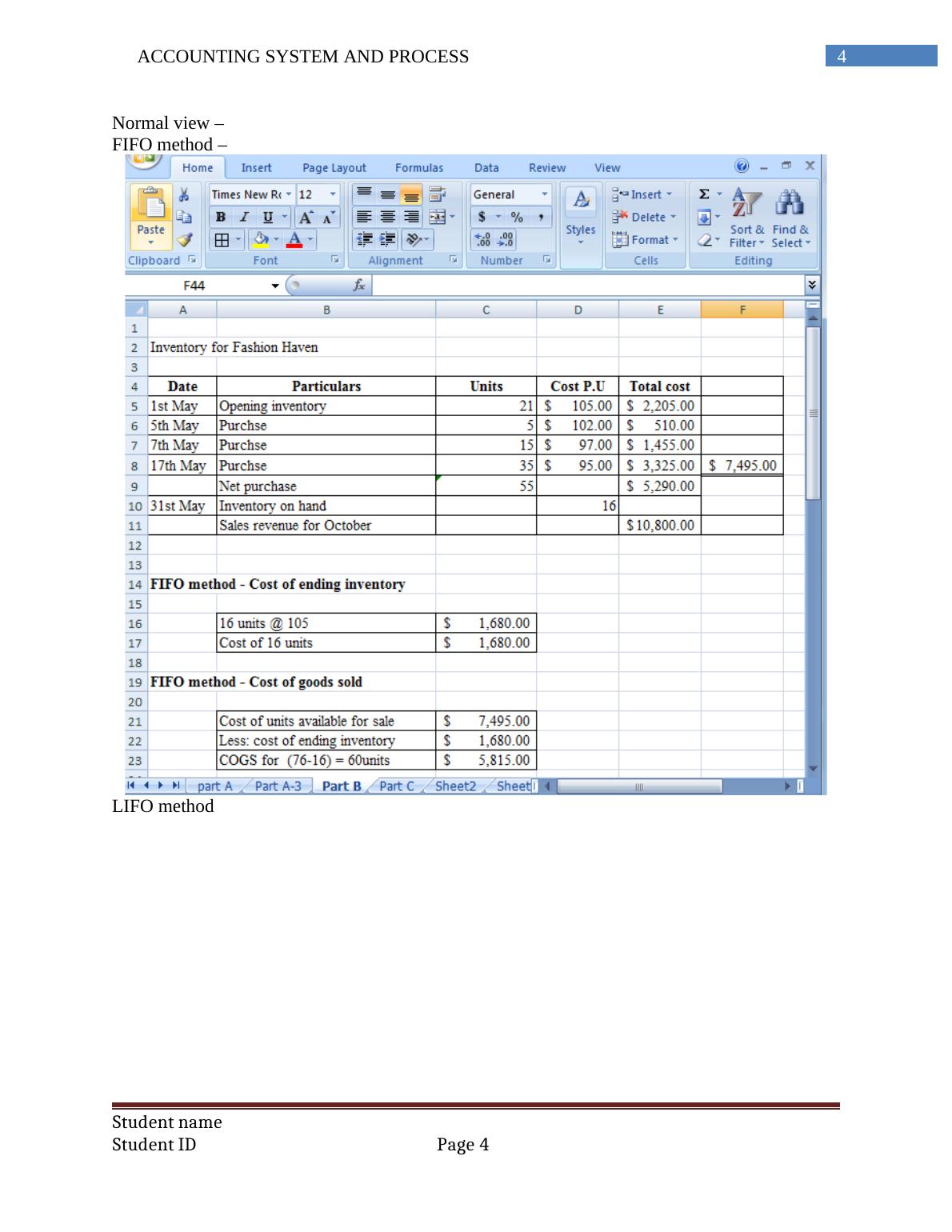

Normal view –

FIFO method –

LIFO method

Student name

Student ID Page 4

Normal view –

FIFO method –

LIFO method

Student name

Student ID Page 4

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Accounting Assignment | Inventory System Assignmentlg...

|4

|650

|129

(Solved) Accounting System and Process- Assignmentlg...

|18

|2992

|39

Basic Accounting Principleslg...

|5

|514

|257

Accounting: Memo on Inventory Methodslg...

|10

|2837

|89

Accounting Systemlg...

|22

|3239

|59

Intermediate Accounting | Question and Answerlg...

|10

|1303

|34