Accounting Systems and Processes - Desklib

VerifiedAdded on 2022/10/04

|19

|3894

|311

AI Summary

This document covers the journal entries, T-account, adjusted trial balance, income statement, balance sheet, and statement of equity changes for Pete's Handyman Services. It also analyses the history of accounting and ethical principles in the code of ethics.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING SYSTEMS AND PROCESSES

Accounting Systems and Processes

Name of the Student:

Name of the University:

Authors Note:

Accounting Systems and Processes

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEMS AND PROCESSES

1

Table of Contents

Question 1:.................................................................................................................................2

i) Preparing journal entries for July 2019 transactions:.............................................................2

ii) Preparing the T-account for the transactions:........................................................................4

iii) Preparing the Adjusted Trial Balance:.................................................................................7

iv) Preparing the income statement, Balance sheet and statement of equity changes:..............8

v) Calculating and evaluating the business current ratio and debt ratio:.................................10

Question 2:...............................................................................................................................10

Analysing the history of accounting:.......................................................................................10

Question 3:...............................................................................................................................15

i) Listing and explaining each of the ethical principles in the code of ethics:.........................15

ii) Indicating the measures that need to be taken by the accountant in ethical dilemma:........16

References and Bibliography:..................................................................................................17

1

Table of Contents

Question 1:.................................................................................................................................2

i) Preparing journal entries for July 2019 transactions:.............................................................2

ii) Preparing the T-account for the transactions:........................................................................4

iii) Preparing the Adjusted Trial Balance:.................................................................................7

iv) Preparing the income statement, Balance sheet and statement of equity changes:..............8

v) Calculating and evaluating the business current ratio and debt ratio:.................................10

Question 2:...............................................................................................................................10

Analysing the history of accounting:.......................................................................................10

Question 3:...............................................................................................................................15

i) Listing and explaining each of the ethical principles in the code of ethics:.........................15

ii) Indicating the measures that need to be taken by the accountant in ethical dilemma:........16

References and Bibliography:..................................................................................................17

ACCOUNTING SYSTEMS AND PROCESSES

2

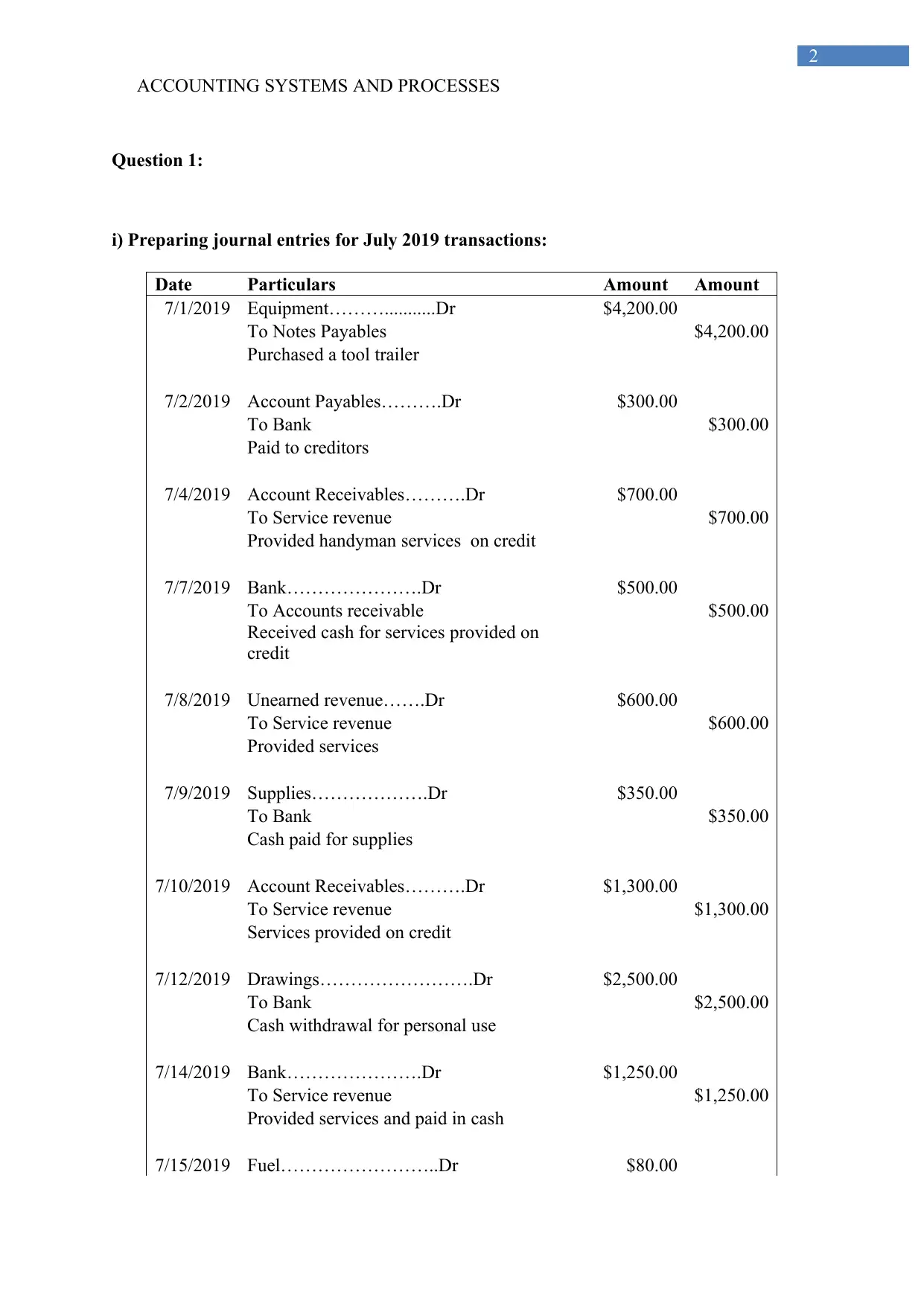

Question 1:

i) Preparing journal entries for July 2019 transactions:

Date Particulars Amount Amount

7/1/2019 Equipment………...........Dr $4,200.00

To Notes Payables $4,200.00

Purchased a tool trailer

7/2/2019 Account Payables……….Dr $300.00

To Bank $300.00

Paid to creditors

7/4/2019 Account Receivables……….Dr $700.00

To Service revenue $700.00

Provided handyman services on credit

7/7/2019 Bank………………….Dr $500.00

To Accounts receivable $500.00

Received cash for services provided on

credit

7/8/2019 Unearned revenue…….Dr $600.00

To Service revenue $600.00

Provided services

7/9/2019 Supplies……………….Dr $350.00

To Bank $350.00

Cash paid for supplies

7/10/2019 Account Receivables……….Dr $1,300.00

To Service revenue $1,300.00

Services provided on credit

7/12/2019 Drawings…………………….Dr $2,500.00

To Bank $2,500.00

Cash withdrawal for personal use

7/14/2019 Bank………………….Dr $1,250.00

To Service revenue $1,250.00

Provided services and paid in cash

7/15/2019 Fuel……………………..Dr $80.00

2

Question 1:

i) Preparing journal entries for July 2019 transactions:

Date Particulars Amount Amount

7/1/2019 Equipment………...........Dr $4,200.00

To Notes Payables $4,200.00

Purchased a tool trailer

7/2/2019 Account Payables……….Dr $300.00

To Bank $300.00

Paid to creditors

7/4/2019 Account Receivables……….Dr $700.00

To Service revenue $700.00

Provided handyman services on credit

7/7/2019 Bank………………….Dr $500.00

To Accounts receivable $500.00

Received cash for services provided on

credit

7/8/2019 Unearned revenue…….Dr $600.00

To Service revenue $600.00

Provided services

7/9/2019 Supplies……………….Dr $350.00

To Bank $350.00

Cash paid for supplies

7/10/2019 Account Receivables……….Dr $1,300.00

To Service revenue $1,300.00

Services provided on credit

7/12/2019 Drawings…………………….Dr $2,500.00

To Bank $2,500.00

Cash withdrawal for personal use

7/14/2019 Bank………………….Dr $1,250.00

To Service revenue $1,250.00

Provided services and paid in cash

7/15/2019 Fuel……………………..Dr $80.00

ACCOUNTING SYSTEMS AND PROCESSES

3

To Bank $80.00

Paid cash for fuel

7/16/2019 Bank………………….Dr $1,300.00

To Accounts receivable $1,300.00

Received cash for services provided on

credit

7/22/2019 Account Receivables……….Dr $500.00

To Service revenue $500.00

Services provided on credit

7/23/2019 Unearned revenue…….Dr $2,600.00

To Bank $2,600.00

Received cash for services provided on

credit

7/23/2019 Prepaid advertisement………………….Dr $1,200.00

To Bank $1,200.00

Paid in advance for advertisement

7/23/2019 Bank………………….Dr $700.00

To Accounts receivable $700.00

Received cash for services provided on

credit

7/26/2019 Drawings…………………….Dr $2,500.00

To Bank $2,500.00

Cash withdrawal for personal use

7/26/2019 Bank………………….Dr $280.00

To Service revenue $280.00

Received cash for services provided

7/30/2019 Prepaid Insurance………………….Dr $320.00

To Bank $320.00

Paid in advance for Insurance

7/31/2019 Notes Payable…..................Dr $350.00

Interest expense….............Dr $50.00

To Bank $400.00

Payment for loan instalment

7/31/2019 Repairs…............................Dr $320.00

To Accounts payable $320.00

Expenses accrued on repairs

3

To Bank $80.00

Paid cash for fuel

7/16/2019 Bank………………….Dr $1,300.00

To Accounts receivable $1,300.00

Received cash for services provided on

credit

7/22/2019 Account Receivables……….Dr $500.00

To Service revenue $500.00

Services provided on credit

7/23/2019 Unearned revenue…….Dr $2,600.00

To Bank $2,600.00

Received cash for services provided on

credit

7/23/2019 Prepaid advertisement………………….Dr $1,200.00

To Bank $1,200.00

Paid in advance for advertisement

7/23/2019 Bank………………….Dr $700.00

To Accounts receivable $700.00

Received cash for services provided on

credit

7/26/2019 Drawings…………………….Dr $2,500.00

To Bank $2,500.00

Cash withdrawal for personal use

7/26/2019 Bank………………….Dr $280.00

To Service revenue $280.00

Received cash for services provided

7/30/2019 Prepaid Insurance………………….Dr $320.00

To Bank $320.00

Paid in advance for Insurance

7/31/2019 Notes Payable…..................Dr $350.00

Interest expense….............Dr $50.00

To Bank $400.00

Payment for loan instalment

7/31/2019 Repairs…............................Dr $320.00

To Accounts payable $320.00

Expenses accrued on repairs

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEMS AND PROCESSES

4

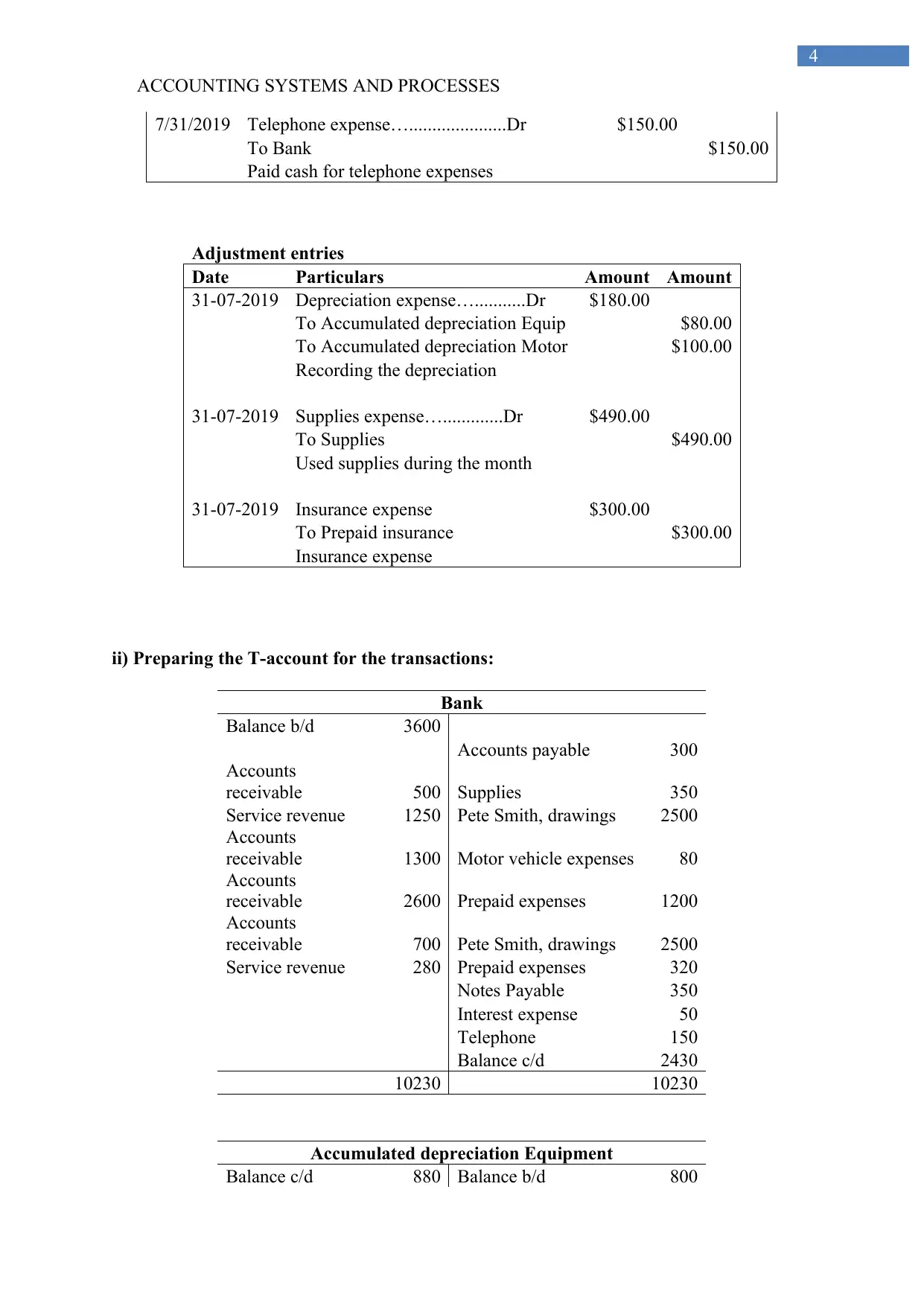

7/31/2019 Telephone expense….....................Dr $150.00

To Bank $150.00

Paid cash for telephone expenses

Adjustment entries

Date Particulars Amount Amount

31-07-2019 Depreciation expense…...........Dr $180.00

To Accumulated depreciation Equip $80.00

To Accumulated depreciation Motor $100.00

Recording the depreciation

31-07-2019 Supplies expense….............Dr $490.00

To Supplies $490.00

Used supplies during the month

31-07-2019 Insurance expense $300.00

To Prepaid insurance $300.00

Insurance expense

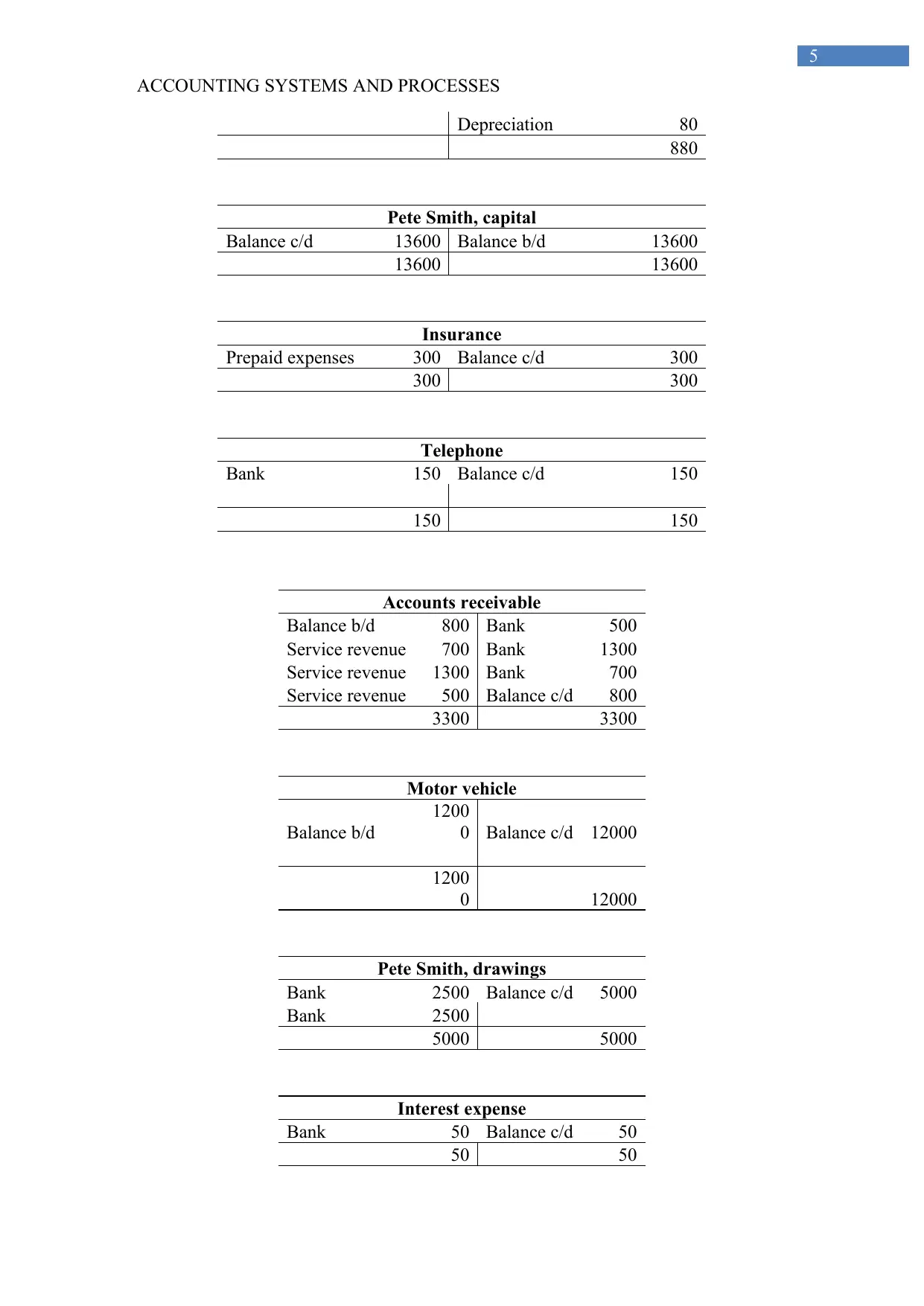

ii) Preparing the T-account for the transactions:

Bank

Balance b/d 3600

Accounts payable 300

Accounts

receivable 500 Supplies 350

Service revenue 1250 Pete Smith, drawings 2500

Accounts

receivable 1300 Motor vehicle expenses 80

Accounts

receivable 2600 Prepaid expenses 1200

Accounts

receivable 700 Pete Smith, drawings 2500

Service revenue 280 Prepaid expenses 320

Notes Payable 350

Interest expense 50

Telephone 150

Balance c/d 2430

10230 10230

Accumulated depreciation Equipment

Balance c/d 880 Balance b/d 800

4

7/31/2019 Telephone expense….....................Dr $150.00

To Bank $150.00

Paid cash for telephone expenses

Adjustment entries

Date Particulars Amount Amount

31-07-2019 Depreciation expense…...........Dr $180.00

To Accumulated depreciation Equip $80.00

To Accumulated depreciation Motor $100.00

Recording the depreciation

31-07-2019 Supplies expense….............Dr $490.00

To Supplies $490.00

Used supplies during the month

31-07-2019 Insurance expense $300.00

To Prepaid insurance $300.00

Insurance expense

ii) Preparing the T-account for the transactions:

Bank

Balance b/d 3600

Accounts payable 300

Accounts

receivable 500 Supplies 350

Service revenue 1250 Pete Smith, drawings 2500

Accounts

receivable 1300 Motor vehicle expenses 80

Accounts

receivable 2600 Prepaid expenses 1200

Accounts

receivable 700 Pete Smith, drawings 2500

Service revenue 280 Prepaid expenses 320

Notes Payable 350

Interest expense 50

Telephone 150

Balance c/d 2430

10230 10230

Accumulated depreciation Equipment

Balance c/d 880 Balance b/d 800

ACCOUNTING SYSTEMS AND PROCESSES

5

Depreciation 80

880

Pete Smith, capital

Balance c/d 13600 Balance b/d 13600

13600 13600

Insurance

Prepaid expenses 300 Balance c/d 300

300 300

Telephone

Bank 150 Balance c/d 150

150 150

Accounts receivable

Balance b/d 800 Bank 500

Service revenue 700 Bank 1300

Service revenue 1300 Bank 700

Service revenue 500 Balance c/d 800

3300 3300

Motor vehicle

Balance b/d

1200

0 Balance c/d 12000

1200

0 12000

Pete Smith, drawings

Bank 2500 Balance c/d 5000

Bank 2500

5000 5000

Interest expense

Bank 50 Balance c/d 50

50 50

5

Depreciation 80

880

Pete Smith, capital

Balance c/d 13600 Balance b/d 13600

13600 13600

Insurance

Prepaid expenses 300 Balance c/d 300

300 300

Telephone

Bank 150 Balance c/d 150

150 150

Accounts receivable

Balance b/d 800 Bank 500

Service revenue 700 Bank 1300

Service revenue 1300 Bank 700

Service revenue 500 Balance c/d 800

3300 3300

Motor vehicle

Balance b/d

1200

0 Balance c/d 12000

1200

0 12000

Pete Smith, drawings

Bank 2500 Balance c/d 5000

Bank 2500

5000 5000

Interest expense

Bank 50 Balance c/d 50

50 50

ACCOUNTING SYSTEMS AND PROCESSES

6

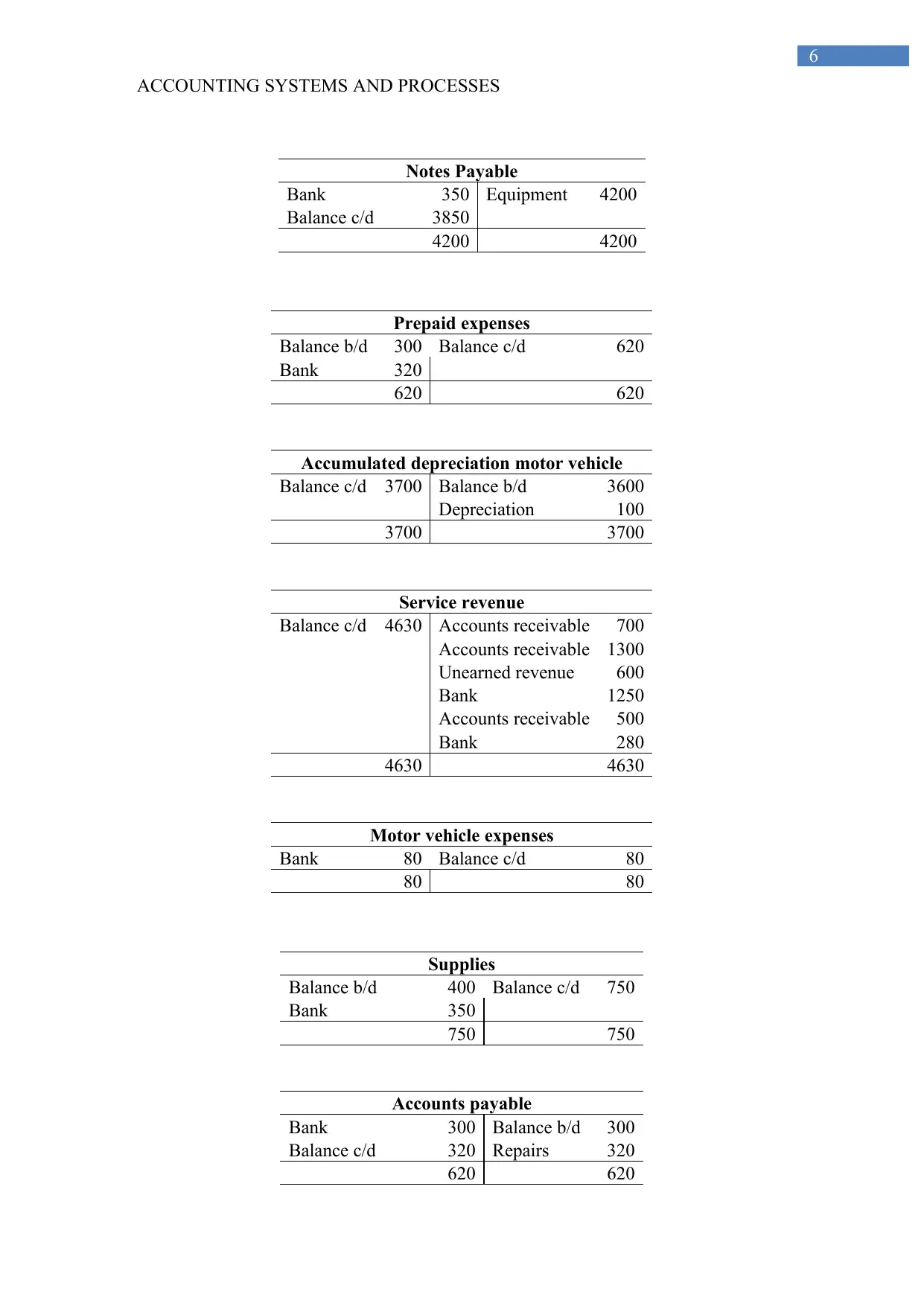

Notes Payable

Bank 350 Equipment 4200

Balance c/d 3850

4200 4200

Prepaid expenses

Balance b/d 300 Balance c/d 620

Bank 320

620 620

Accumulated depreciation motor vehicle

Balance c/d 3700 Balance b/d 3600

Depreciation 100

3700 3700

Service revenue

Balance c/d 4630 Accounts receivable 700

Accounts receivable 1300

Unearned revenue 600

Bank 1250

Accounts receivable 500

Bank 280

4630 4630

Motor vehicle expenses

Bank 80 Balance c/d 80

80 80

Supplies

Balance b/d 400 Balance c/d 750

Bank 350

750 750

Accounts payable

Bank 300 Balance b/d 300

Balance c/d 320 Repairs 320

620 620

6

Notes Payable

Bank 350 Equipment 4200

Balance c/d 3850

4200 4200

Prepaid expenses

Balance b/d 300 Balance c/d 620

Bank 320

620 620

Accumulated depreciation motor vehicle

Balance c/d 3700 Balance b/d 3600

Depreciation 100

3700 3700

Service revenue

Balance c/d 4630 Accounts receivable 700

Accounts receivable 1300

Unearned revenue 600

Bank 1250

Accounts receivable 500

Bank 280

4630 4630

Motor vehicle expenses

Bank 80 Balance c/d 80

80 80

Supplies

Balance b/d 400 Balance c/d 750

Bank 350

750 750

Accounts payable

Bank 300 Balance b/d 300

Balance c/d 320 Repairs 320

620 620

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEMS AND PROCESSES

7

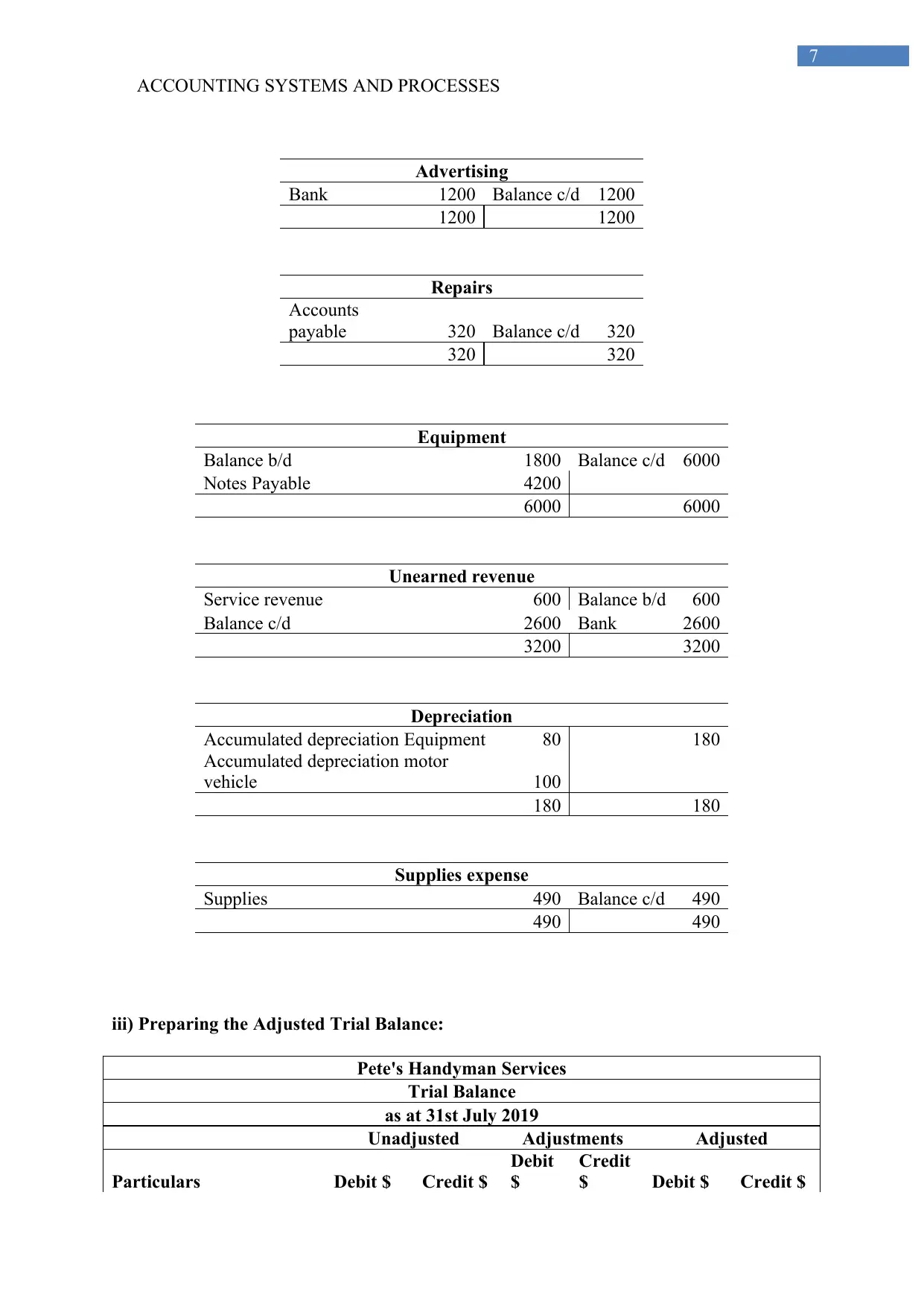

Advertising

Bank 1200 Balance c/d 1200

1200 1200

Repairs

Accounts

payable 320 Balance c/d 320

320 320

Equipment

Balance b/d 1800 Balance c/d 6000

Notes Payable 4200

6000 6000

Unearned revenue

Service revenue 600 Balance b/d 600

Balance c/d 2600 Bank 2600

3200 3200

Depreciation

Accumulated depreciation Equipment 80 180

Accumulated depreciation motor

vehicle 100

180 180

Supplies expense

Supplies 490 Balance c/d 490

490 490

iii) Preparing the Adjusted Trial Balance:

Pete's Handyman Services

Trial Balance

as at 31st July 2019

Unadjusted Adjustments Adjusted

Particulars Debit $ Credit $

Debit

$

Credit

$ Debit $ Credit $

7

Advertising

Bank 1200 Balance c/d 1200

1200 1200

Repairs

Accounts

payable 320 Balance c/d 320

320 320

Equipment

Balance b/d 1800 Balance c/d 6000

Notes Payable 4200

6000 6000

Unearned revenue

Service revenue 600 Balance b/d 600

Balance c/d 2600 Bank 2600

3200 3200

Depreciation

Accumulated depreciation Equipment 80 180

Accumulated depreciation motor

vehicle 100

180 180

Supplies expense

Supplies 490 Balance c/d 490

490 490

iii) Preparing the Adjusted Trial Balance:

Pete's Handyman Services

Trial Balance

as at 31st July 2019

Unadjusted Adjustments Adjusted

Particulars Debit $ Credit $

Debit

$

Credit

$ Debit $ Credit $

ACCOUNTING SYSTEMS AND PROCESSES

8

Bank

$2,430.0

0

$2,430.0

0

Accounts receivable $800.00 $800.00

Prepaid expenses $620.00

$300.0

0 $320.00

Supplies $750.00

$490.0

0 $260.00

Equipment

$6,000.0

0

$6,000.0

0

Less: Accumulated

depreciation $800.00 $80.00 $880.00

Motor vehicle

$12,000.

00

$12,000.

00

Less: Accumulated

depreciation

$3,600.0

0

$100.0

0

$3,700.0

0

Accounts payable $320.00 $320.00

Unearned revenue

$2,600.0

0

$2,600.0

0

Notes Payable

$3,850.0

0

$3,850.0

0

Pete Smith, capital

$13,600.

00

$13,600.

00

Pete Smith, drawings

$5,000.0

0

$5,000.0

0

Service revenue

$4,630.0

0

$4,630.0

0

Advertising

$1,200.0

0

$1,200.0

0

Depreciation

$180.0

0 $180.00

Insurance

$300.0

0 $300.00

Interest expense $50.00 $50.00

Motor vehicle expenses $80.00 $80.00

Repairs $320.00 $320.00

Supplies expense

$490.0

0 $490.00

Telephone $150.00 $150.00

Total

$29,400.

00

$29,400.

00

$970.0

0

$970.0

0

$29,580.

00

$29,580.

00

iv) Preparing the income statement, Balance sheet and statement of equity changes:

Pete's Handyman Services

Statement of Income

as at 31st July 2019

8

Bank

$2,430.0

0

$2,430.0

0

Accounts receivable $800.00 $800.00

Prepaid expenses $620.00

$300.0

0 $320.00

Supplies $750.00

$490.0

0 $260.00

Equipment

$6,000.0

0

$6,000.0

0

Less: Accumulated

depreciation $800.00 $80.00 $880.00

Motor vehicle

$12,000.

00

$12,000.

00

Less: Accumulated

depreciation

$3,600.0

0

$100.0

0

$3,700.0

0

Accounts payable $320.00 $320.00

Unearned revenue

$2,600.0

0

$2,600.0

0

Notes Payable

$3,850.0

0

$3,850.0

0

Pete Smith, capital

$13,600.

00

$13,600.

00

Pete Smith, drawings

$5,000.0

0

$5,000.0

0

Service revenue

$4,630.0

0

$4,630.0

0

Advertising

$1,200.0

0

$1,200.0

0

Depreciation

$180.0

0 $180.00

Insurance

$300.0

0 $300.00

Interest expense $50.00 $50.00

Motor vehicle expenses $80.00 $80.00

Repairs $320.00 $320.00

Supplies expense

$490.0

0 $490.00

Telephone $150.00 $150.00

Total

$29,400.

00

$29,400.

00

$970.0

0

$970.0

0

$29,580.

00

$29,580.

00

iv) Preparing the income statement, Balance sheet and statement of equity changes:

Pete's Handyman Services

Statement of Income

as at 31st July 2019

ACCOUNTING SYSTEMS AND PROCESSES

9

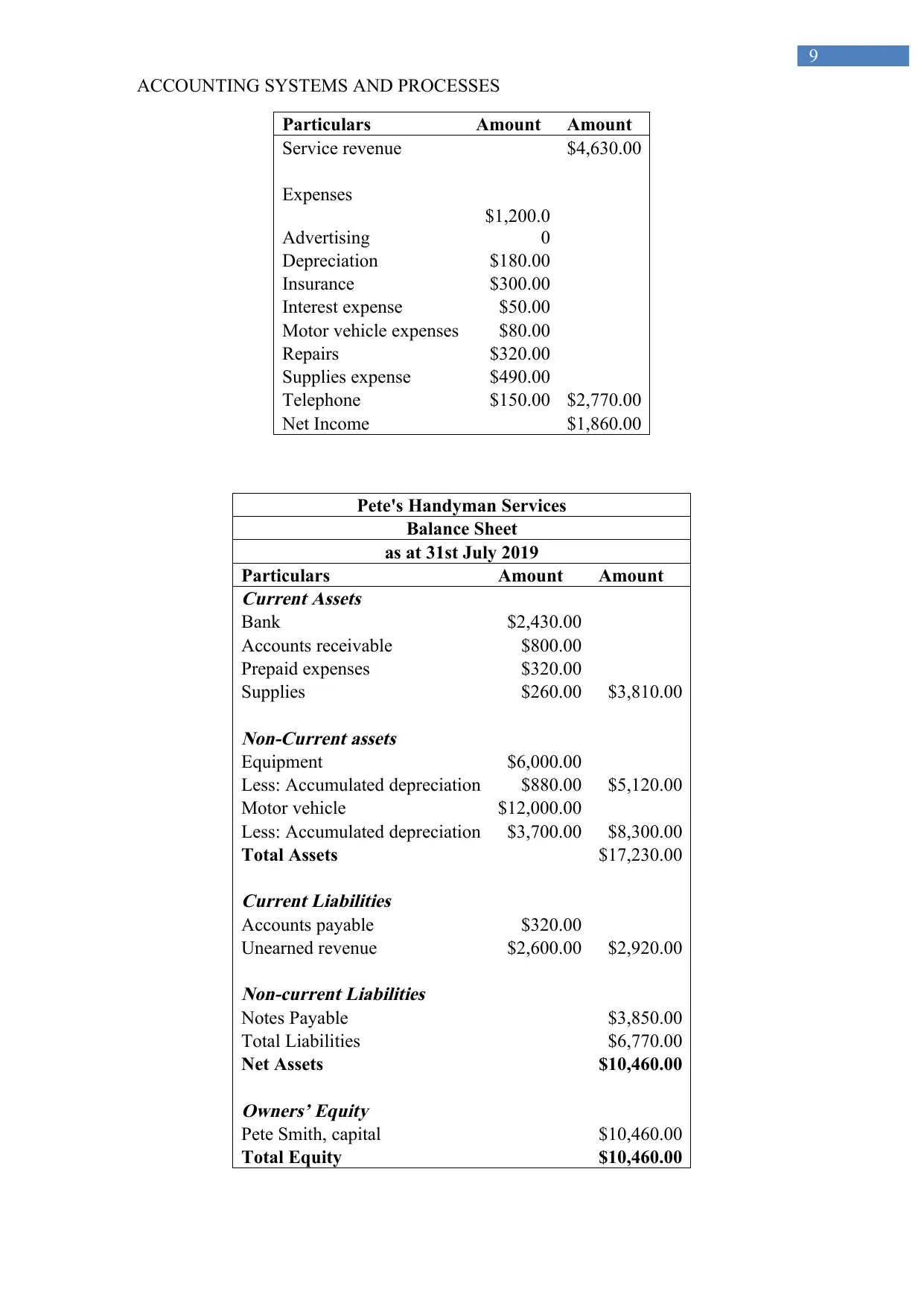

Particulars Amount Amount

Service revenue $4,630.00

Expenses

Advertising

$1,200.0

0

Depreciation $180.00

Insurance $300.00

Interest expense $50.00

Motor vehicle expenses $80.00

Repairs $320.00

Supplies expense $490.00

Telephone $150.00 $2,770.00

Net Income $1,860.00

Pete's Handyman Services

Balance Sheet

as at 31st July 2019

Particulars Amount Amount

Current Assets

Bank $2,430.00

Accounts receivable $800.00

Prepaid expenses $320.00

Supplies $260.00 $3,810.00

Non-Current assets

Equipment $6,000.00

Less: Accumulated depreciation $880.00 $5,120.00

Motor vehicle $12,000.00

Less: Accumulated depreciation $3,700.00 $8,300.00

Total Assets $17,230.00

Current Liabilities

Accounts payable $320.00

Unearned revenue $2,600.00 $2,920.00

Non-current Liabilities

Notes Payable $3,850.00

Total Liabilities $6,770.00

Net Assets $10,460.00

Owners’ Equity

Pete Smith, capital $10,460.00

Total Equity $10,460.00

9

Particulars Amount Amount

Service revenue $4,630.00

Expenses

Advertising

$1,200.0

0

Depreciation $180.00

Insurance $300.00

Interest expense $50.00

Motor vehicle expenses $80.00

Repairs $320.00

Supplies expense $490.00

Telephone $150.00 $2,770.00

Net Income $1,860.00

Pete's Handyman Services

Balance Sheet

as at 31st July 2019

Particulars Amount Amount

Current Assets

Bank $2,430.00

Accounts receivable $800.00

Prepaid expenses $320.00

Supplies $260.00 $3,810.00

Non-Current assets

Equipment $6,000.00

Less: Accumulated depreciation $880.00 $5,120.00

Motor vehicle $12,000.00

Less: Accumulated depreciation $3,700.00 $8,300.00

Total Assets $17,230.00

Current Liabilities

Accounts payable $320.00

Unearned revenue $2,600.00 $2,920.00

Non-current Liabilities

Notes Payable $3,850.00

Total Liabilities $6,770.00

Net Assets $10,460.00

Owners’ Equity

Pete Smith, capital $10,460.00

Total Equity $10,460.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEMS AND PROCESSES

10

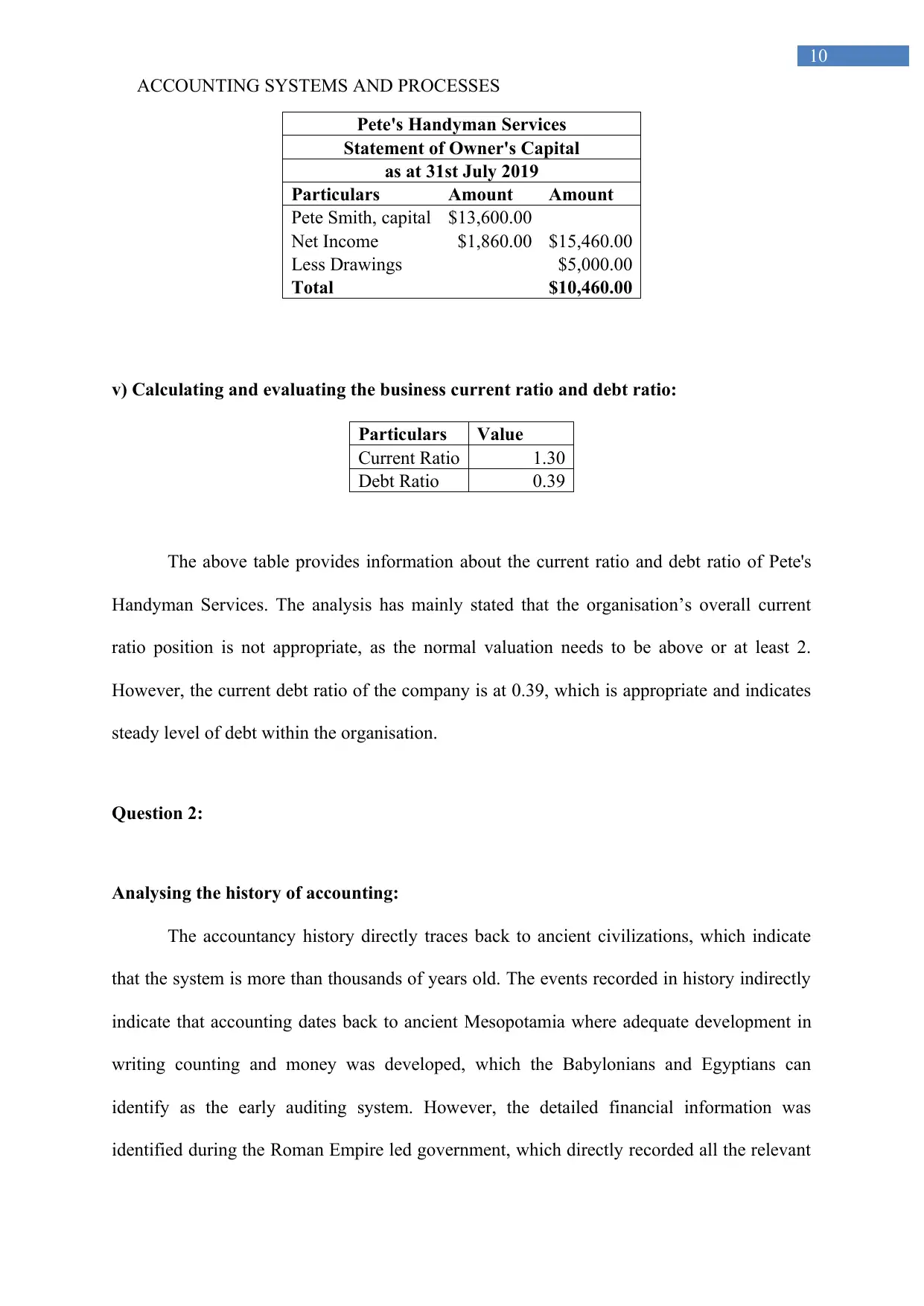

Pete's Handyman Services

Statement of Owner's Capital

as at 31st July 2019

Particulars Amount Amount

Pete Smith, capital $13,600.00

Net Income $1,860.00 $15,460.00

Less Drawings $5,000.00

Total $10,460.00

v) Calculating and evaluating the business current ratio and debt ratio:

Particulars Value

Current Ratio 1.30

Debt Ratio 0.39

The above table provides information about the current ratio and debt ratio of Pete's

Handyman Services. The analysis has mainly stated that the organisation’s overall current

ratio position is not appropriate, as the normal valuation needs to be above or at least 2.

However, the current debt ratio of the company is at 0.39, which is appropriate and indicates

steady level of debt within the organisation.

Question 2:

Analysing the history of accounting:

The accountancy history directly traces back to ancient civilizations, which indicate

that the system is more than thousands of years old. The events recorded in history indirectly

indicate that accounting dates back to ancient Mesopotamia where adequate development in

writing counting and money was developed, which the Babylonians and Egyptians can

identify as the early auditing system. However, the detailed financial information was

identified during the Roman Empire led government, which directly recorded all the relevant

10

Pete's Handyman Services

Statement of Owner's Capital

as at 31st July 2019

Particulars Amount Amount

Pete Smith, capital $13,600.00

Net Income $1,860.00 $15,460.00

Less Drawings $5,000.00

Total $10,460.00

v) Calculating and evaluating the business current ratio and debt ratio:

Particulars Value

Current Ratio 1.30

Debt Ratio 0.39

The above table provides information about the current ratio and debt ratio of Pete's

Handyman Services. The analysis has mainly stated that the organisation’s overall current

ratio position is not appropriate, as the normal valuation needs to be above or at least 2.

However, the current debt ratio of the company is at 0.39, which is appropriate and indicates

steady level of debt within the organisation.

Question 2:

Analysing the history of accounting:

The accountancy history directly traces back to ancient civilizations, which indicate

that the system is more than thousands of years old. The events recorded in history indirectly

indicate that accounting dates back to ancient Mesopotamia where adequate development in

writing counting and money was developed, which the Babylonians and Egyptians can

identify as the early auditing system. However, the detailed financial information was

identified during the Roman Empire led government, which directly recorded all the relevant

ACCOUNTING SYSTEMS AND PROCESSES

11

events and financial transactions to depict the financial conditions of a town. The manuscripts

that was similar to the financial management book was written by Chanakya during the

Mauryan empire where the book name Arthashasthra containing the detailed aspects of

maintaining the financial books of accounts for a Sovereign state. The detailed information

that was provided in the book during the Mauryan Empire directly related the progress that

has been made throughout history in accounting. Therefore, it has been detected that the

maintenance of financial accounts or accountancy has been present in human history for a

longer duration where it allowed Sovereign Nations to detect the level of their financial

capability and treasury amount. Thus, detailed financial accounting was an essential part of

maintaining and creating an empire since ancient times (Brown, 2014).

The progress of accounting is directly e sub divided in four different aspects, which

contains Ancient History, Roman Empire, Mediaeval or Renaissance period, and Modern

Professional Accounting. The different segments of the accounting history directly indicate

about the progress and the improvements that were conducted in the field of accountancy to

improve the financial management and accounting conditions of both servant missions and

companies in later years. There were adequate early developments of accounting and

expansion of the role of an accountant, which was laid during the ancient times. The timeline

or the time period of the accounting development are depicted as follows.

Ancient History: One of the accounting records that is dated back for more than 7000 years

ago was found in Mesopotamia where are all the relevant documents from the ancient

civilization directly identifies the list of expenditures and goods received during trade. The

development of accounting directly indicates about the add element money and numbers that

work directly indicating the trading activities that were conducted in the civilization during

the era (D. Carnegie, 2014). The development of accounting is closely related to the

improvements that were conducted with money, writing and counting that have been

11

events and financial transactions to depict the financial conditions of a town. The manuscripts

that was similar to the financial management book was written by Chanakya during the

Mauryan empire where the book name Arthashasthra containing the detailed aspects of

maintaining the financial books of accounts for a Sovereign state. The detailed information

that was provided in the book during the Mauryan Empire directly related the progress that

has been made throughout history in accounting. Therefore, it has been detected that the

maintenance of financial accounts or accountancy has been present in human history for a

longer duration where it allowed Sovereign Nations to detect the level of their financial

capability and treasury amount. Thus, detailed financial accounting was an essential part of

maintaining and creating an empire since ancient times (Brown, 2014).

The progress of accounting is directly e sub divided in four different aspects, which

contains Ancient History, Roman Empire, Mediaeval or Renaissance period, and Modern

Professional Accounting. The different segments of the accounting history directly indicate

about the progress and the improvements that were conducted in the field of accountancy to

improve the financial management and accounting conditions of both servant missions and

companies in later years. There were adequate early developments of accounting and

expansion of the role of an accountant, which was laid during the ancient times. The timeline

or the time period of the accounting development are depicted as follows.

Ancient History: One of the accounting records that is dated back for more than 7000 years

ago was found in Mesopotamia where are all the relevant documents from the ancient

civilization directly identifies the list of expenditures and goods received during trade. The

development of accounting directly indicates about the add element money and numbers that

work directly indicating the trading activities that were conducted in the civilization during

the era (D. Carnegie, 2014). The development of accounting is closely related to the

improvements that were conducted with money, writing and counting that have been

ACCOUNTING SYSTEMS AND PROCESSES

12

conducted over the period of human history. Historical analysis of accounting also indicate

that there were adequate developments in the field of counting where the transition from

concrete to abstract counting methods was conducted which allowed the development of

accounting and money during the Mesopotamian Civilization.

One of the early accounting records that have been identified by the stories dates back

more than 7000 years, which was related to the ancient ruins of Babylon, Sumeria and

Assyria. The accounting methods developed during the ancient times was directly related to

the primitive accounting calculations, which was related to the recording of crop and hard

growth. This method of counting positively conducted at a naturally seasons where the

surplus and deficit of the crops gained during the season can be identified by the individuals

in this civilization (Zeff, 2016). Thus, it could be understood that a primitive accounting

method was developed during the ancient period to identify the level of food that was

available for consumption and detect any kind of surplus or deficit.

The historical events also indicate that during the fourth millennium BC and the third

millennium BC different civilizations started to utilize tables and figures to represent their

current accounting statistics. This led to the expansion or invention of a form of bookkeeping,

which can be considered a used cognitive leap for the human civilization. During the period

of Egyptians, the probable bookkeeping purposes expanded its horizon, which relatively

included adequate scripts three form of accounting that is present as a proof in the Old

Testament, and the book of exodus. The concept of the accountant or the role of accountant

was adequately developed in ancient Egyptian civilization where adequate depiction of

materials and other wealth calculations were conducted to identify the level of progress made

during the period (Lee, Bishop & Parker, 2014).

Roman Empire: During the Roman Empire, the record of cash commodity and transactions

was led to be conducted by military personnel for identifying the wealth and the overall cash

12

conducted over the period of human history. Historical analysis of accounting also indicate

that there were adequate developments in the field of counting where the transition from

concrete to abstract counting methods was conducted which allowed the development of

accounting and money during the Mesopotamian Civilization.

One of the early accounting records that have been identified by the stories dates back

more than 7000 years, which was related to the ancient ruins of Babylon, Sumeria and

Assyria. The accounting methods developed during the ancient times was directly related to

the primitive accounting calculations, which was related to the recording of crop and hard

growth. This method of counting positively conducted at a naturally seasons where the

surplus and deficit of the crops gained during the season can be identified by the individuals

in this civilization (Zeff, 2016). Thus, it could be understood that a primitive accounting

method was developed during the ancient period to identify the level of food that was

available for consumption and detect any kind of surplus or deficit.

The historical events also indicate that during the fourth millennium BC and the third

millennium BC different civilizations started to utilize tables and figures to represent their

current accounting statistics. This led to the expansion or invention of a form of bookkeeping,

which can be considered a used cognitive leap for the human civilization. During the period

of Egyptians, the probable bookkeeping purposes expanded its horizon, which relatively

included adequate scripts three form of accounting that is present as a proof in the Old

Testament, and the book of exodus. The concept of the accountant or the role of accountant

was adequately developed in ancient Egyptian civilization where adequate depiction of

materials and other wealth calculations were conducted to identify the level of progress made

during the period (Lee, Bishop & Parker, 2014).

Roman Empire: During the Roman Empire, the record of cash commodity and transactions

was led to be conducted by military personnel for identifying the wealth and the overall cash

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING SYSTEMS AND PROCESSES

13

sums that was held military unit. These calculations also conducted by the governor of

relevant districts to identify the level of wealth that needs to be taxed to the citizens of the

regions. The vast Empire that was maintained by the Roman civilization was due to the

adequate use of accountancy, which allowed the accountants to record all the relevant

transactions and affect the adequate coffers of the region. This method of accounting has

been developed and accommodated by many businesses and small organizations that were

developed during the period of the Roman Empire. The Roman Empire directly introduced

the standardized system of accounting, which allowed the local farm managers to identify and

subdivide all the relevant transactions and conduct the day to day accounts of the estate.

One of the major accounting management system that was used by the Romans was

the heroine archive that had a huge collection of paperless documents mostly letters that

provided the same number of accounts, which was used to detect the wealth conditions of the

Empire. The division so that was made by the accountants on the basis of archived details

directly help in detecting the cash expenses in each parts to obtain the relevant gain from the

transaction. The accounting in the Roman Era directly allowed the owners with better

opportunity to take economic decisions that allowed them to purposely select and arrange

their actions (Fleischman, Tyson & Oldroyd, 2017).

Mediaeval or Renaissance period: The mediaeval and Renaissance period directly increase

the progress of the accounting conditions that was being used by individuals. The concept of

double entry bookkeeping was introduced which directly help in overseeing the multiple and

simultaneous transactions that was conducted by banks and other organizations. Period is

considered to be the foothold of accounting system which relatively accommodated the debit

and credit measures to help track accounts and determine what is owed or can be collected by

the organization. During the period the accounting world made rabbit progress where II

introduction of memorandum, journals and ledger was conducted to identify all the relevant

13

sums that was held military unit. These calculations also conducted by the governor of

relevant districts to identify the level of wealth that needs to be taxed to the citizens of the

regions. The vast Empire that was maintained by the Roman civilization was due to the

adequate use of accountancy, which allowed the accountants to record all the relevant

transactions and affect the adequate coffers of the region. This method of accounting has

been developed and accommodated by many businesses and small organizations that were

developed during the period of the Roman Empire. The Roman Empire directly introduced

the standardized system of accounting, which allowed the local farm managers to identify and

subdivide all the relevant transactions and conduct the day to day accounts of the estate.

One of the major accounting management system that was used by the Romans was

the heroine archive that had a huge collection of paperless documents mostly letters that

provided the same number of accounts, which was used to detect the wealth conditions of the

Empire. The division so that was made by the accountants on the basis of archived details

directly help in detecting the cash expenses in each parts to obtain the relevant gain from the

transaction. The accounting in the Roman Era directly allowed the owners with better

opportunity to take economic decisions that allowed them to purposely select and arrange

their actions (Fleischman, Tyson & Oldroyd, 2017).

Mediaeval or Renaissance period: The mediaeval and Renaissance period directly increase

the progress of the accounting conditions that was being used by individuals. The concept of

double entry bookkeeping was introduced which directly help in overseeing the multiple and

simultaneous transactions that was conducted by banks and other organizations. Period is

considered to be the foothold of accounting system which relatively accommodated the debit

and credit measures to help track accounts and determine what is owed or can be collected by

the organization. During the period the accounting world made rabbit progress where II

introduction of memorandum, journals and ledger was conducted to identify all the relevant

ACCOUNTING SYSTEMS AND PROCESSES

14

transactions conducted by the organization or an individual. The accounting system that was

developed during the Renaissance period is still common today as the financial books of an

organization keep both journal and ledger to identify the financial position, while preparing

their profit & loss and balance sheet. The analysis has directly indicated that both financial

and management accounting was developed during the period where the joint stock

companies specially from 1600 was built to support higher accounting information’s, which

can handle and send knowledge of operations that directly relied on accounts and other

requisite information’s (Antonelli & D'Alessio, 2014).

Modern Professional Accounting: The current modern accounting concept of the century

directly helps in identifying the actions and conventions that allow the overall business

conditions of an organization. The double entry bookkeeping system developed in the 14th

and 15th century is still used as adequate accounting principles, which allow the professional

accountants to identify and offered 11th services to the clients. Currently the accounting

forensic system has been developed in the modern era to identify and detect all the relevant

transactions that is conducted by organizations during the financial period. The industrial

revolution that was strong in London during the 19th century directly boosted the relevant

growth of limited liability companies and last in manufacturing and logistics.

This development in the manufacturing sector increase complexity for the profession

accounting conditions, as they were not able to handle all the relevant increment in the

figures and calculations (Bryer, 2016). The speed of global transactions that were conducted

during the period added depreciation and inventory valuation was needed it irrelevant change

in the legislation that would support the accounting conditions and financial system of the

organization. The current accounting system directly involves two major accounting

conditions fair generally accepted accounting profession and International Financial

Reporting Standards is used by companies to prepare their financial report and conduct

14

transactions conducted by the organization or an individual. The accounting system that was

developed during the Renaissance period is still common today as the financial books of an

organization keep both journal and ledger to identify the financial position, while preparing

their profit & loss and balance sheet. The analysis has directly indicated that both financial

and management accounting was developed during the period where the joint stock

companies specially from 1600 was built to support higher accounting information’s, which

can handle and send knowledge of operations that directly relied on accounts and other

requisite information’s (Antonelli & D'Alessio, 2014).

Modern Professional Accounting: The current modern accounting concept of the century

directly helps in identifying the actions and conventions that allow the overall business

conditions of an organization. The double entry bookkeeping system developed in the 14th

and 15th century is still used as adequate accounting principles, which allow the professional

accountants to identify and offered 11th services to the clients. Currently the accounting

forensic system has been developed in the modern era to identify and detect all the relevant

transactions that is conducted by organizations during the financial period. The industrial

revolution that was strong in London during the 19th century directly boosted the relevant

growth of limited liability companies and last in manufacturing and logistics.

This development in the manufacturing sector increase complexity for the profession

accounting conditions, as they were not able to handle all the relevant increment in the

figures and calculations (Bryer, 2016). The speed of global transactions that were conducted

during the period added depreciation and inventory valuation was needed it irrelevant change

in the legislation that would support the accounting conditions and financial system of the

organization. The current accounting system directly involves two major accounting

conditions fair generally accepted accounting profession and International Financial

Reporting Standards is used by companies to prepare their financial report and conduct

ACCOUNTING SYSTEMS AND PROCESSES

15

complex calculations to detect the accurate financial conditions in their annual report. The

current accounting progress is appropriate for the period, where certain amendments need to

be conducted for minimizing the manipulations and loopholes that provides leverage for

unethical activities.

Question 3:

i) Listing and explaining each of the ethical principles in the code of ethics:

The ethical principles in the code of ethical that needs to be followed by the

accountants are mainly depicted as follows.

Integrity is one of the major ethical attributes, where a professional accountant needs to

be straightforward and honest with all professional and business relationships

(Apesb.org.au, 2019).

One of the ethical attributes is objectivity, where professional accountant should not

allow biasness, as conflicts of interest or undue of others business judgements. Thus, it is

can indicated that the accounts cannot be biased in a form while disclosing the relevant

information to the companies.

Professional Competence and Due Care is another major ethical code of problems is the

need to be followed by the accountants. The professional accountants need to continue the

duty, while maintaining the professional knowledge and skill. Thus, the accounting needs

to provide client with competent professional service based on current developments in

practice. Hence, professional services need to be provided by applying the entire relevant

technical and professional standard by the accountants (Apesb.org.au, 2019).

Confidentiality is a major component of ethics principles, which needs to be followed by

the accountants, while providing the relevant services to their clients. Thus, it is the

15

complex calculations to detect the accurate financial conditions in their annual report. The

current accounting progress is appropriate for the period, where certain amendments need to

be conducted for minimizing the manipulations and loopholes that provides leverage for

unethical activities.

Question 3:

i) Listing and explaining each of the ethical principles in the code of ethics:

The ethical principles in the code of ethical that needs to be followed by the

accountants are mainly depicted as follows.

Integrity is one of the major ethical attributes, where a professional accountant needs to

be straightforward and honest with all professional and business relationships

(Apesb.org.au, 2019).

One of the ethical attributes is objectivity, where professional accountant should not

allow biasness, as conflicts of interest or undue of others business judgements. Thus, it is

can indicated that the accounts cannot be biased in a form while disclosing the relevant

information to the companies.

Professional Competence and Due Care is another major ethical code of problems is the

need to be followed by the accountants. The professional accountants need to continue the

duty, while maintaining the professional knowledge and skill. Thus, the accounting needs

to provide client with competent professional service based on current developments in

practice. Hence, professional services need to be provided by applying the entire relevant

technical and professional standard by the accountants (Apesb.org.au, 2019).

Confidentiality is a major component of ethics principles, which needs to be followed by

the accountants, while providing the relevant services to their clients. Thus, it is the

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ACCOUNTING SYSTEMS AND PROCESSES

16

responsibility of the accountants for not sharing any kind of confidential details regarding

the company’s secrets to another organisation. The confidentiality clause allows the

company to trust the accountant and provide all the relevant information that is conducted

to complete its financial cycle. This would eventually help in clearing the adequate

financial report for the organisation which witnessed all the relevant transactions

conducted during the financial year.

The accountant needs to comply with all the relevant laws and a regulation that is

addressed in the professional behaviour clauses. This would eventually help in avoiding

any actions that described the profession and integrity of the accountant’s altogether.

ii) Indicating the measures that need to be taken by the accountant in ethical dilemma:

There are certain situations under which organization can persuade the accountants to

conduct unethical activities, which would lead to ethical dilemma. One of the major ethical

dilemmas that are faced by accountants is during the manipulations that are demanded by the

organization to be conducted on their financial report. The current financial report format has

certain loopholes, which are utilized by organizations to raise their financial position and

progress. Before the financial crisis, the accountants were faced with the ethical dilemma of

manipulating the company's financial accounts for hiding the toxic assets, which were

depleting the progress of the organization. The accountants complied with the request of the

organizations due to the persuasion that was provided through monetary benefits and long

term contracts (Apesb.org.au, 2019).

However, the accountants should have not taken into consideration the lucrative offers

provided by the organization and must have reported the incident to appropriate authorities.

This would have insured the continuation of ethical consideration within the profession of

accountants. The different whistleblowers had highlighted the manipulations that were

16

responsibility of the accountants for not sharing any kind of confidential details regarding

the company’s secrets to another organisation. The confidentiality clause allows the

company to trust the accountant and provide all the relevant information that is conducted

to complete its financial cycle. This would eventually help in clearing the adequate

financial report for the organisation which witnessed all the relevant transactions

conducted during the financial year.

The accountant needs to comply with all the relevant laws and a regulation that is

addressed in the professional behaviour clauses. This would eventually help in avoiding

any actions that described the profession and integrity of the accountant’s altogether.

ii) Indicating the measures that need to be taken by the accountant in ethical dilemma:

There are certain situations under which organization can persuade the accountants to

conduct unethical activities, which would lead to ethical dilemma. One of the major ethical

dilemmas that are faced by accountants is during the manipulations that are demanded by the

organization to be conducted on their financial report. The current financial report format has

certain loopholes, which are utilized by organizations to raise their financial position and

progress. Before the financial crisis, the accountants were faced with the ethical dilemma of

manipulating the company's financial accounts for hiding the toxic assets, which were

depleting the progress of the organization. The accountants complied with the request of the

organizations due to the persuasion that was provided through monetary benefits and long

term contracts (Apesb.org.au, 2019).

However, the accountants should have not taken into consideration the lucrative offers

provided by the organization and must have reported the incident to appropriate authorities.

This would have insured the continuation of ethical consideration within the profession of

accountants. The different whistleblowers had highlighted the manipulations that were

ACCOUNTING SYSTEMS AND PROCESSES

17

conducted by organization on large basis, which led to the reduction in corruption within a

company. Therefore, the accountant needs to comply with the ethical principles lay down in

the fundamental section to avoid any kind of discrepancy in their work and maintain the

integrity of the profession.

References and Bibliography:

Antonelli, V., & D'Alessio, R. (2014). Accounting history as a local discipline: The case of

the Italian-speaking literature (1869–2008). Accounting Historians Journal, 41(1), 79-

111.

Antonelli, V., & Sargiacomo, M. (2015). Alberto Ceccherelli (1885–1958): Pioneer in the

history of accounting practice and leader in international dissemination. Accounting

History Review, 25(2), 121-144.

Apesb.org.au. (2019). Apesb.org.au. Retrieved 13 August 2019, from

https://www.apesb.org.au/uploads/standards/apesb_standards/23072019055710_APE

S_110_Code_of_Ethics_for_Professional_Accountants_December_2010_-_Final.pdf

Brown, R. (2014). A history of accounting and accountants. Routledge.

Bryer, R. (2016). Linking Pacioli's double-entry bookkeeping, algebra, and art: accounting

history or idle speculation?. Accounting History Review, 26(1), 33-40.

D. Carnegie, G. (2014). The present and future of accounting history. Accounting, Auditing &

Accountability Journal, 27(8), 1241-1249.

Fleischman, R. K., & Parker, L. D. (2017). What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

17

conducted by organization on large basis, which led to the reduction in corruption within a

company. Therefore, the accountant needs to comply with the ethical principles lay down in

the fundamental section to avoid any kind of discrepancy in their work and maintain the

integrity of the profession.

References and Bibliography:

Antonelli, V., & D'Alessio, R. (2014). Accounting history as a local discipline: The case of

the Italian-speaking literature (1869–2008). Accounting Historians Journal, 41(1), 79-

111.

Antonelli, V., & Sargiacomo, M. (2015). Alberto Ceccherelli (1885–1958): Pioneer in the

history of accounting practice and leader in international dissemination. Accounting

History Review, 25(2), 121-144.

Apesb.org.au. (2019). Apesb.org.au. Retrieved 13 August 2019, from

https://www.apesb.org.au/uploads/standards/apesb_standards/23072019055710_APE

S_110_Code_of_Ethics_for_Professional_Accountants_December_2010_-_Final.pdf

Brown, R. (2014). A history of accounting and accountants. Routledge.

Bryer, R. (2016). Linking Pacioli's double-entry bookkeeping, algebra, and art: accounting

history or idle speculation?. Accounting History Review, 26(1), 33-40.

D. Carnegie, G. (2014). The present and future of accounting history. Accounting, Auditing &

Accountability Journal, 27(8), 1241-1249.

Fleischman, R. K., & Parker, L. D. (2017). What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

ACCOUNTING SYSTEMS AND PROCESSES

18

Fleischman, R. K., Tyson, T. N., & Oldroyd, D. (2017). Accounting history. The Routledge

Companion to Critical Accounting.

Lee, T. A., Bishop, A., & Parker, R. H. (2014). Accounting history from the Renaissance to

the present: A remembrance of Luca Pacioli. Routledge.

Macve, R. H. (2015). Fair value vs conservatism? Aspects of the history of accounting,

auditing, business and finance from ancient Mesopotamia to modern China. The

British Accounting Review, 47(2), 124-141.

Walker, S. P. (2016). Revisiting the roles of accounting in society. Accounting, Organizations

and Society, 49, 41-50.

Zeff, S. A. (2016). Forging accounting principles in five countries: A history and an analysis

of trends. Routledge.

18

Fleischman, R. K., Tyson, T. N., & Oldroyd, D. (2017). Accounting history. The Routledge

Companion to Critical Accounting.

Lee, T. A., Bishop, A., & Parker, R. H. (2014). Accounting history from the Renaissance to

the present: A remembrance of Luca Pacioli. Routledge.

Macve, R. H. (2015). Fair value vs conservatism? Aspects of the history of accounting,

auditing, business and finance from ancient Mesopotamia to modern China. The

British Accounting Review, 47(2), 124-141.

Walker, S. P. (2016). Revisiting the roles of accounting in society. Accounting, Organizations

and Society, 49, 41-50.

Zeff, S. A. (2016). Forging accounting principles in five countries: A history and an analysis

of trends. Routledge.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.