Detailed Accounting Systems and Processes Homework Assignment

VerifiedAdded on 2020/04/07

|29

|2058

|36

Homework Assignment

AI Summary

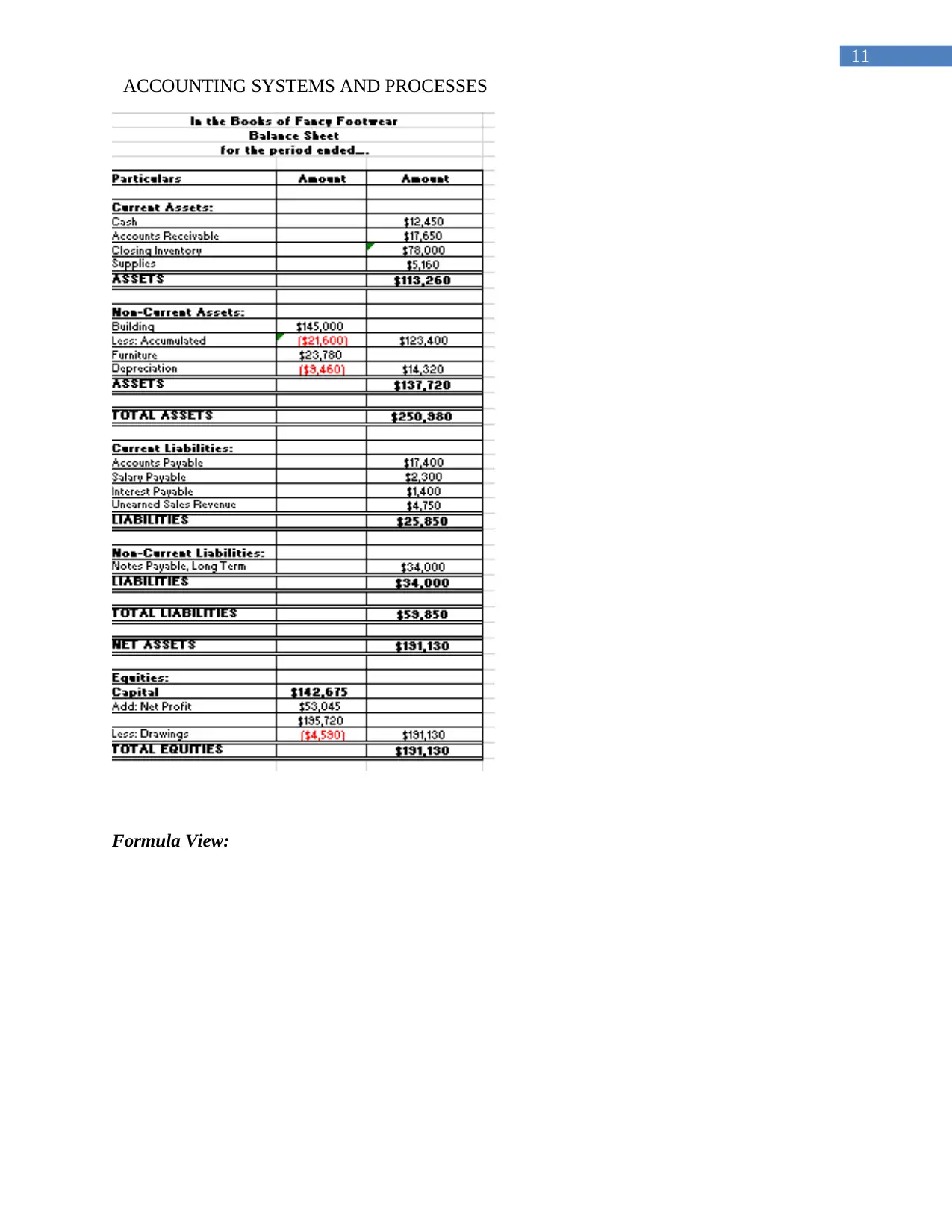

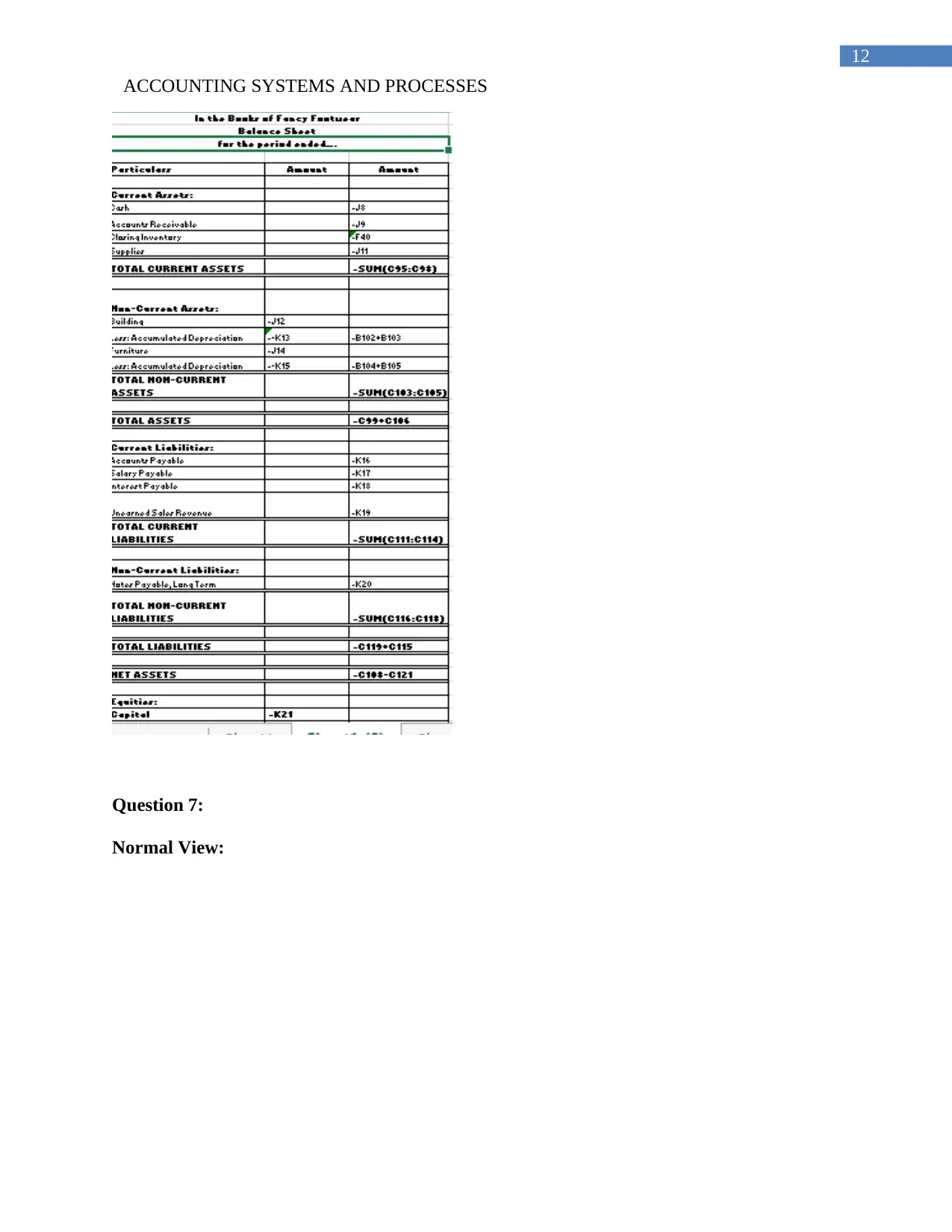

This document presents a comprehensive solution to an accounting systems and processes homework assignment. The solution covers various aspects of accounting, including the use of cell referencing in spreadsheets, displaying negative numbers, and separating spreadsheet areas for data entry and reporting. It delves into specific Excel functions like the IF function and explains the periodic inventory system, including how the cost of goods sold is determined. The assignment also includes practical exercises involving formula view, revised data, and the allowance method. Furthermore, the solution analyzes the Wesfarmers group, providing insights into its statement of comprehensive income, dividend payments, risk management, earnings per share, sustainability, return on equity, corporate governance, income statement, and balance sheet. It concludes with a working capital ratio calculation and investment advice for an individual named Vikram.

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.