Accounting Systems and Processes: Comprehensive Financial Report

VerifiedAdded on 2020/03/28

Accounting systems and Processes

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Table of Contents

Question 1........................................................................................................................................3

Question 2........................................................................................................................................3

Question 3........................................................................................................................................4

Question 4........................................................................................................................................5

Question 5........................................................................................................................................6

Question 6........................................................................................................................................7

Formula View:...............................................................................................................................10

Question 7......................................................................................................................................13

Question 8......................................................................................................................................18

Revised Data:.................................................................................................................................19

Question 9:.....................................................................................................................................19

Question 10....................................................................................................................................20

Question 11....................................................................................................................................21

Question 12....................................................................................................................................21

Question 13....................................................................................................................................22

Reference List................................................................................................................................26

ACCOUNTING SYSTEMS AND PROCESSES

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

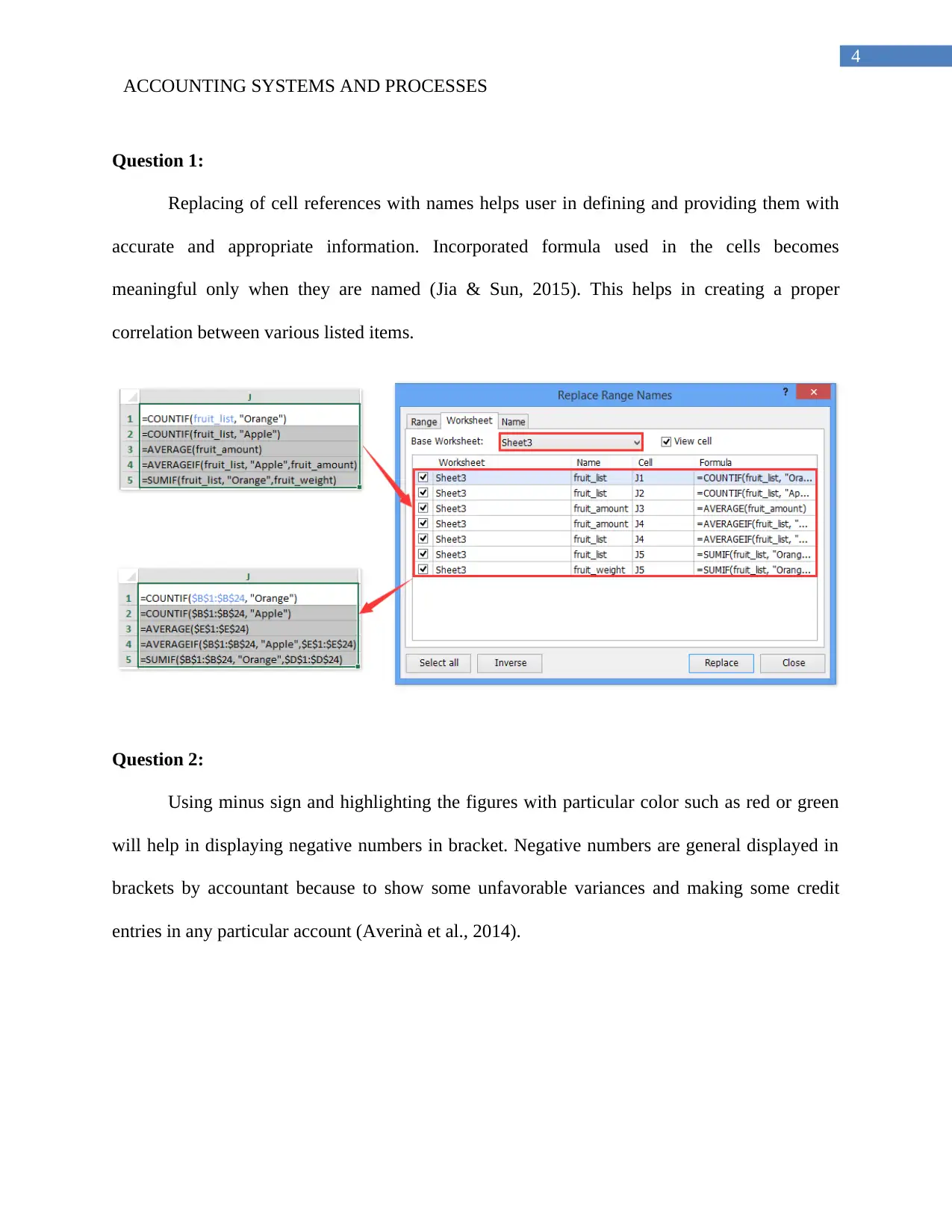

Question 1:

Replacing of cell references with names helps user in defining and providing them with

accurate and appropriate information. Incorporated formula used in the cells becomes

meaningful only when they are named (Jia & Sun, 2015). This helps in creating a proper

correlation between various listed items.

Question 2:

Using minus sign and highlighting the figures with particular color such as red or green

will help in displaying negative numbers in bracket. Negative numbers are general displayed in

brackets by accountant because to show some unfavorable variances and making some credit

entries in any particular account (Averinà et al., 2014).

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Question 3:

It is certainly possible that error can be incurred while performing financial study. Separation of

spreadsheets into report area and data entry areas would ease users and prevent them from

committing any errors. Separation of area would help in systematic entry of data and the

accuracy of information is depicted in the report area.

ACCOUNTING SYSTEMS AND PROCESSES

Question 4:

IF function is one the most popular function that is incorporated in Excel that make use of

logical test and facilitates logical comparison. There are two results obtained by performing IF

function that is the result and false result.

PERIOD Particulars Amount Remarks

September'17

Sales Revenue, less,

Total Expenses 54600

=IF(C7>0,"NET

PROFIT","NET LOSS")

September'17

Sales Revenue, less,

Total Expenses -43700

=IF(C8>0,"NET

PROFIT","NET LOSS")

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

Question 5:

Updating of inventories are done on periodic basis using the periodic system of

inventories. Cost of goods sold under this particular system is calculated by adding purchase mad

by organization to the inventories at beginning periods and then subtracting inventories value at

end of period. An organization employing periodic inventory system has both advantages and

disadvantages. No permanent employees are required to make physical count of incentives and

therefore this method is less expensive.

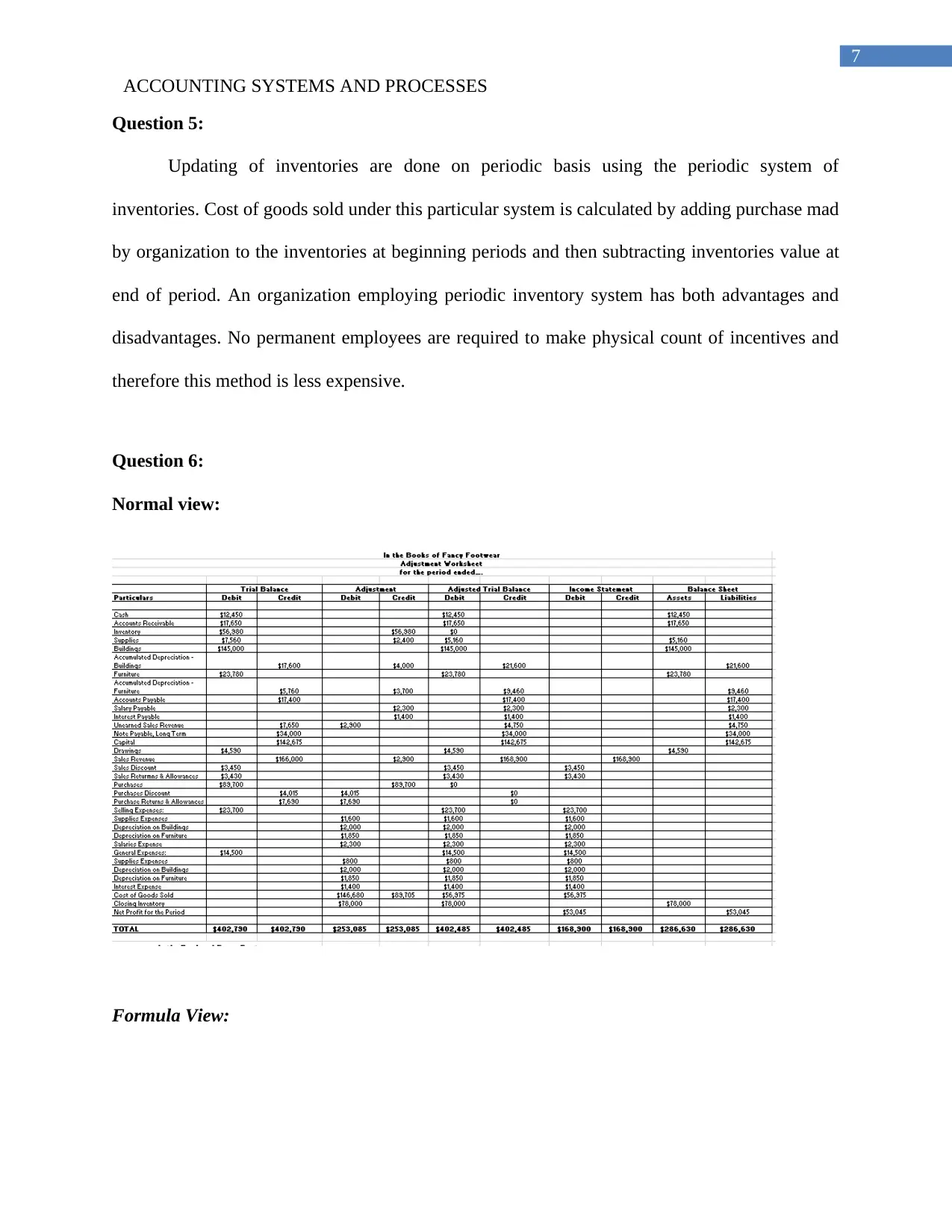

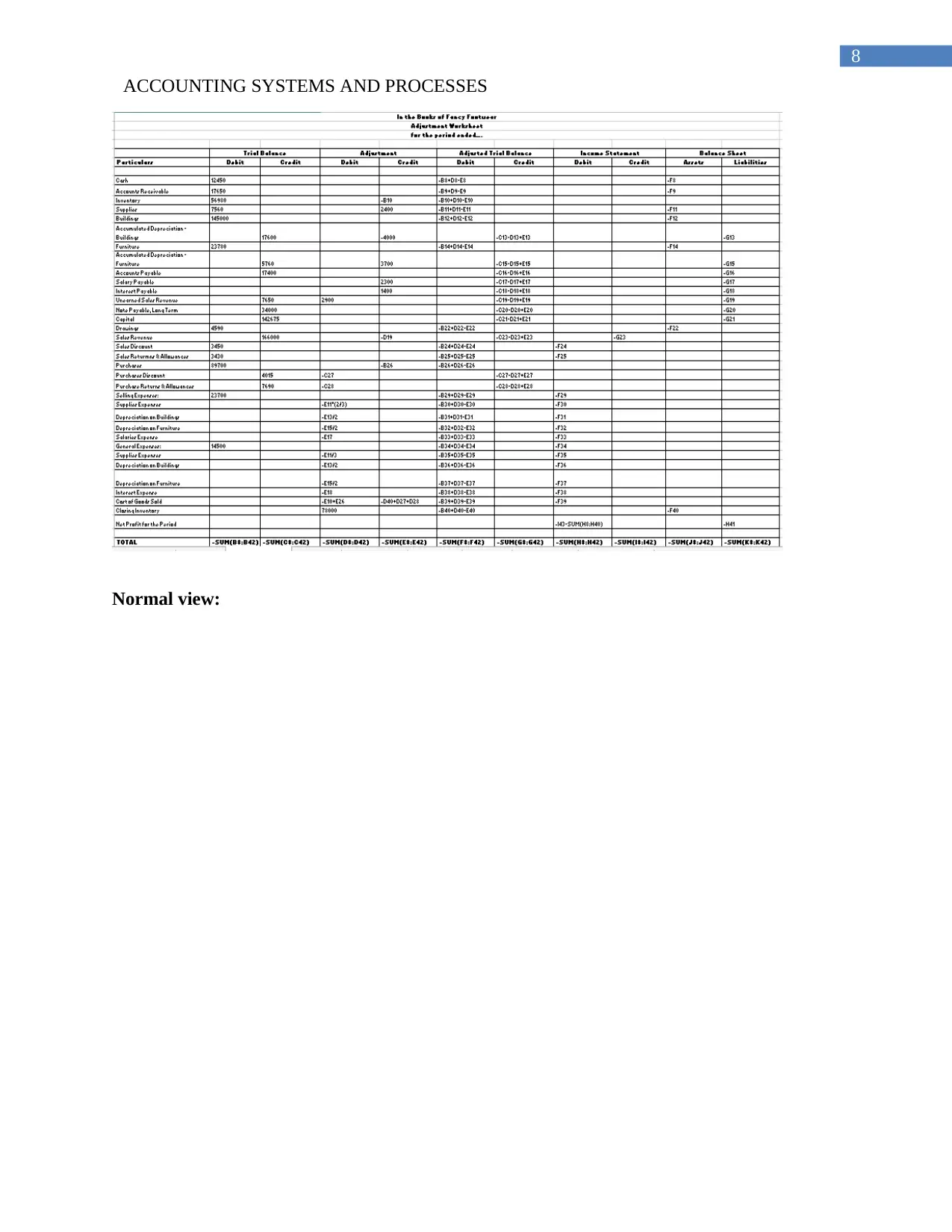

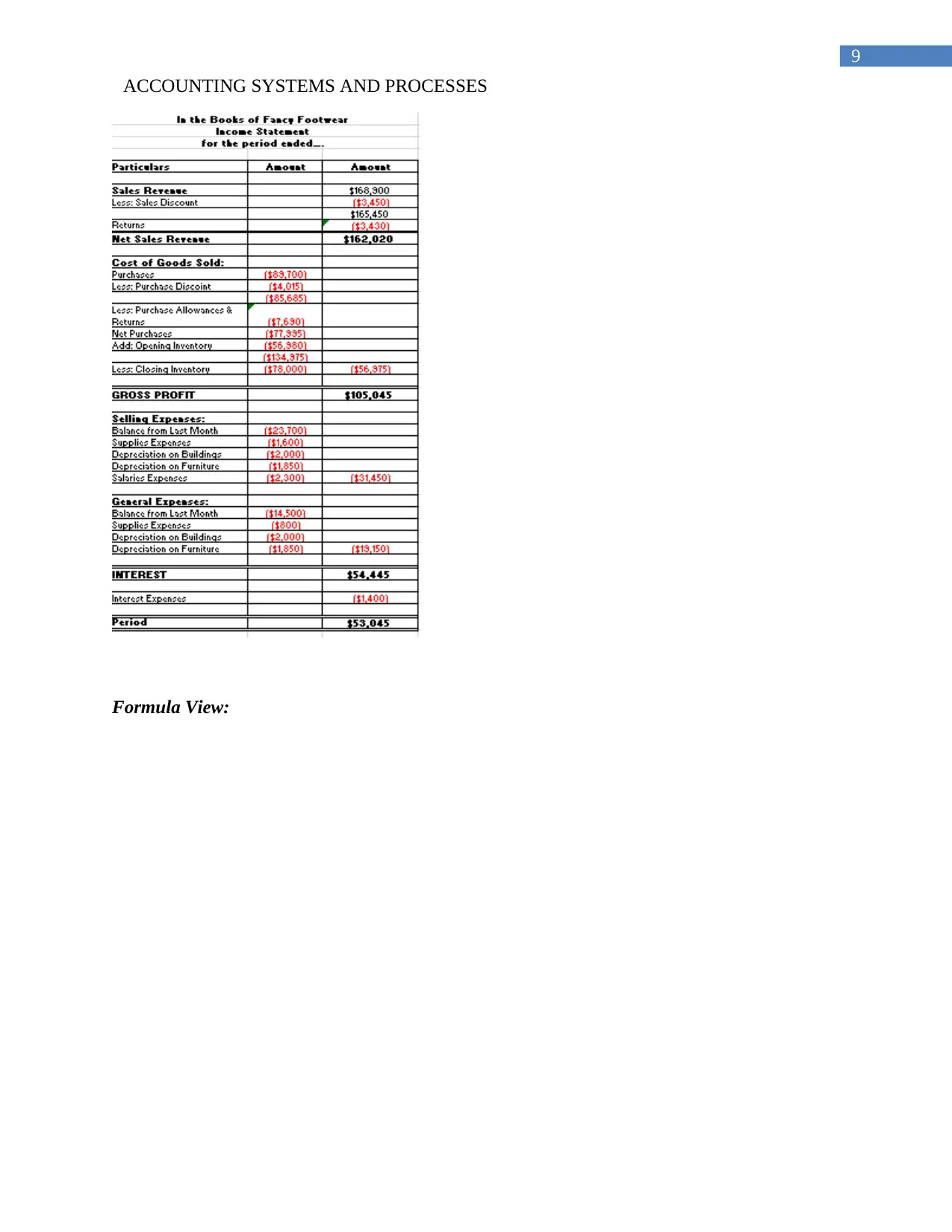

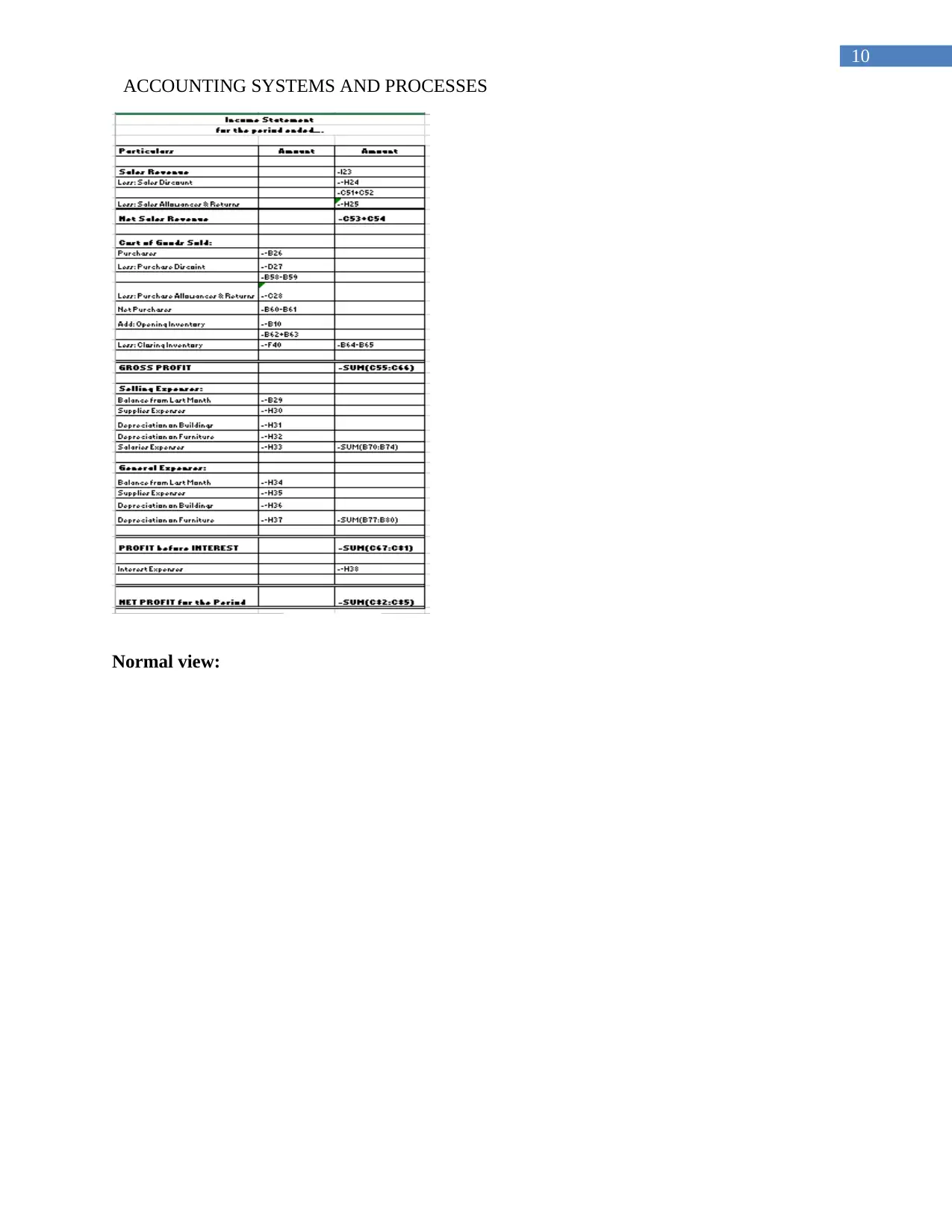

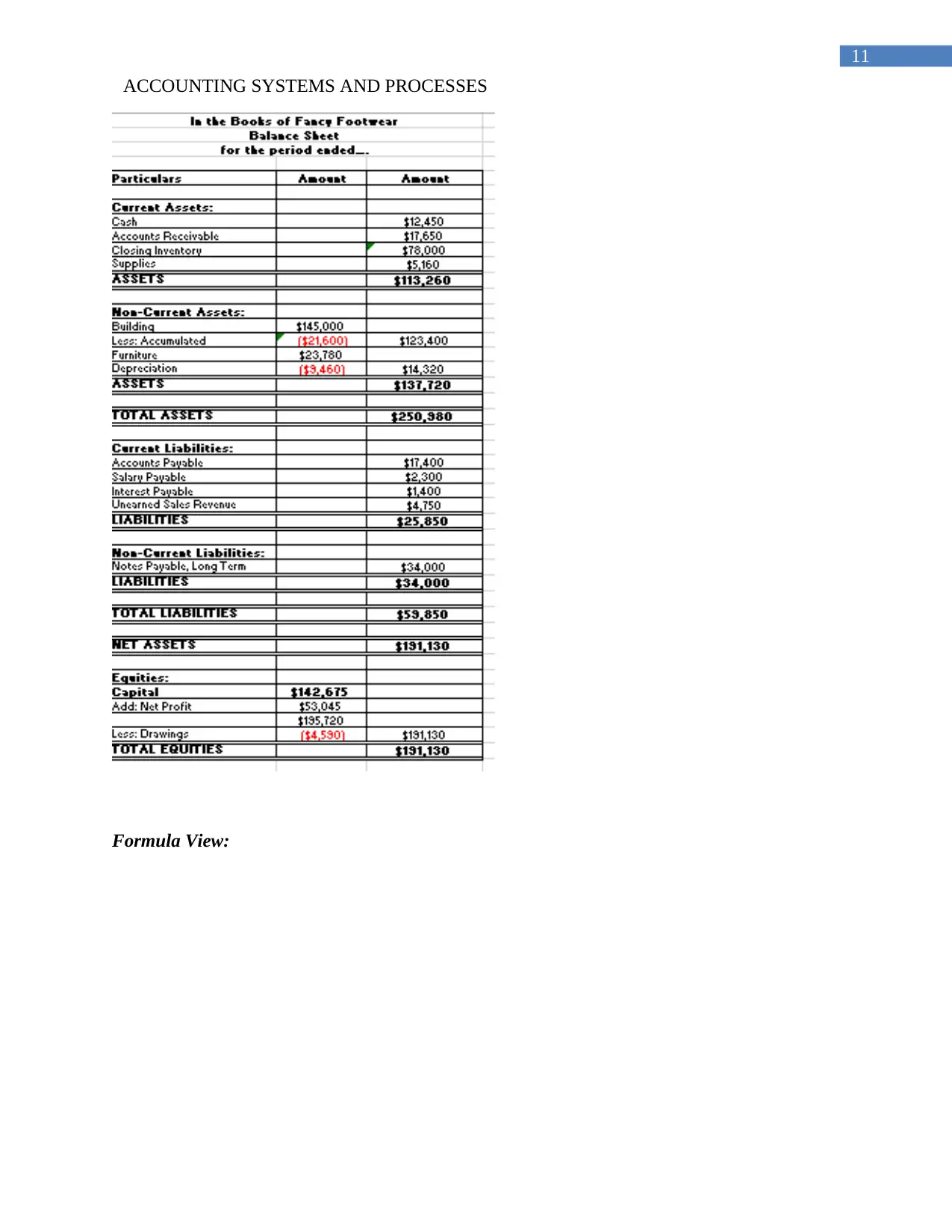

Question 6:

Normal view:

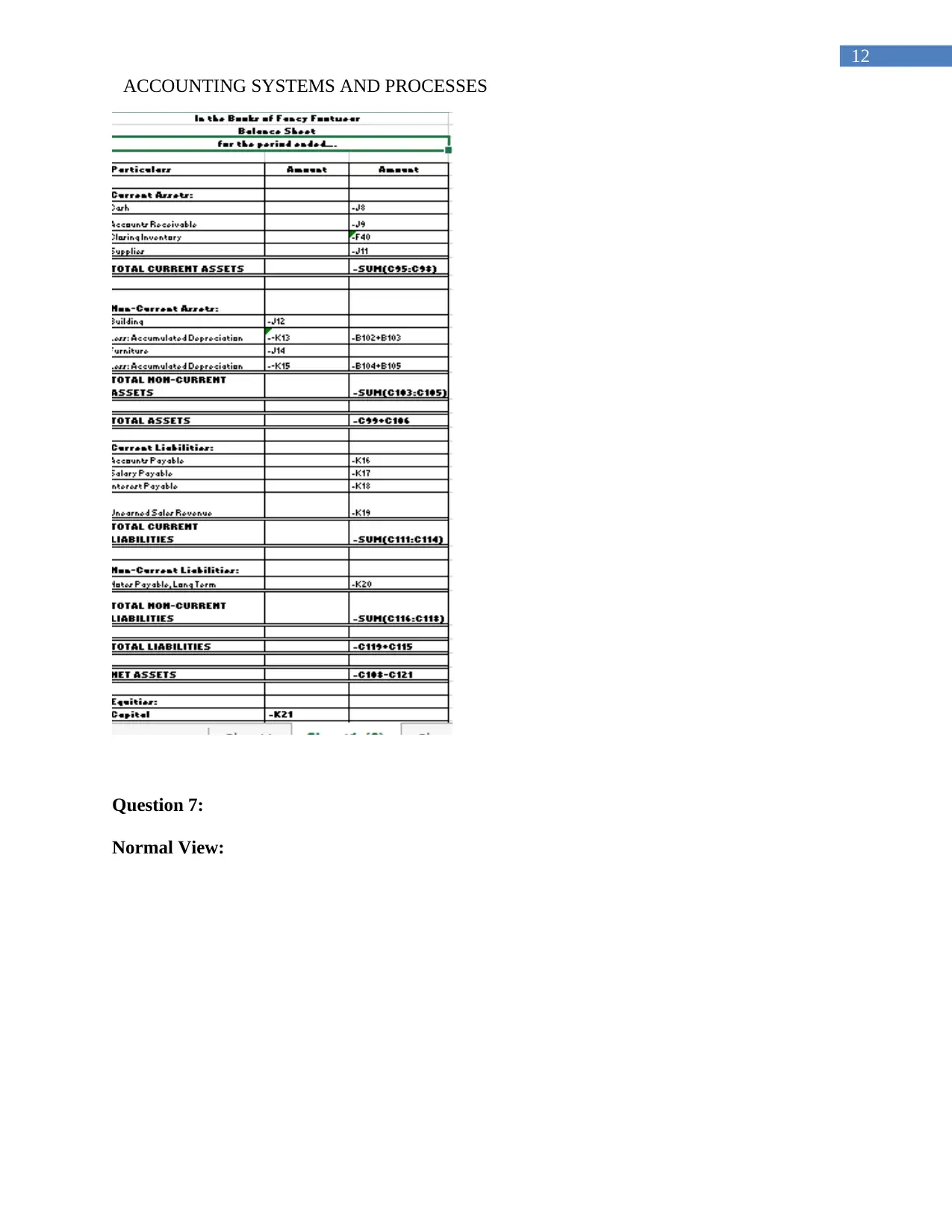

Formula View:

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Normal view:

ACCOUNTING SYSTEMS AND PROCESSES

Formula View:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

Normal view:

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Formula View:

ACCOUNTING SYSTEMS AND PROCESSES

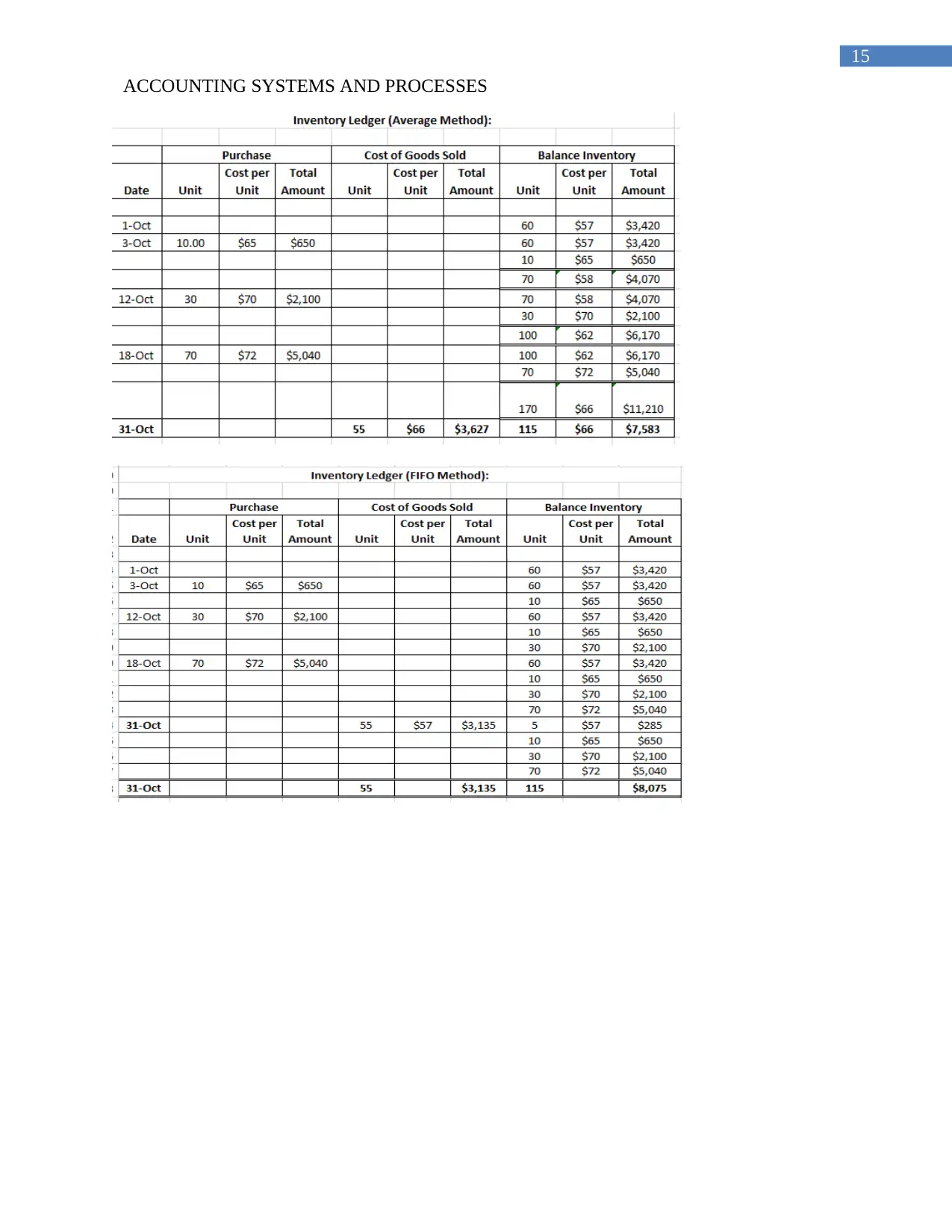

Question 7:

Normal View:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

Particulars

Average

Cost FIFO LIFO

Beginning Inventory $3,420 $3,420 $3,420

Net Purchases $7,790 $7,790 $7,790

Cost of Goods Available $11,210 $11,210 $11,210

Ending Inventory $7,583 $8,075 $7,250

Cost of Goods Sold $3,627 $3,135 $3,960

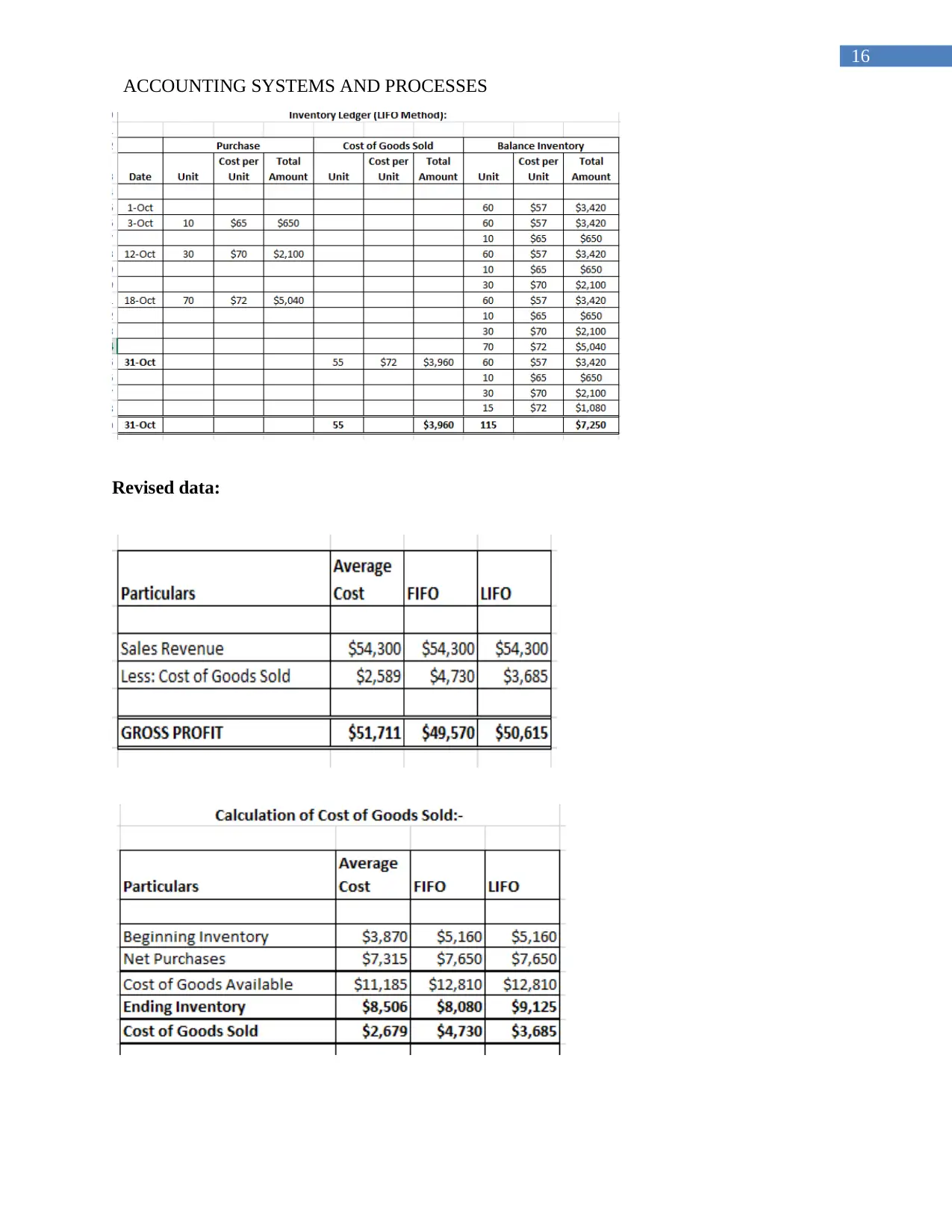

Calculation of Gross Profit:-

Particulars

Average

Cost FIFO LIFO

Sales Revenue $25,000 $25,000 $25,000

Less: Cost of Goods Sold $3,627 $3,135 $3,960

GROSS PROFIT $21,373 $21,865 $21,040

Calculation of Gross Profit:-

Formula View:

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Particulars Average Cost FIFO LIFO

Sales Revenue 25000 =B6 =C6

Less: Cost of Goods Sold 3627 3135 3960

GROSS PROFIT =B6-B7 =C6-C7 =D6-D7

Particulars Average Cost FIFO LIFO

Beginning Inventory 3420 3420 3420

Net Purchases 7790 7790 7790

Cost of Goods Available =B17+B18 =C17+C18 =D17+D18

Ending Inventory 7583 8075 7250

Cost of Goods Sold =B19-B20 =C19-C20 =D19-D20

Calculation of Gross Profit:-

Calculation of Gross Profit:-

Workings:

ACCOUNTING SYSTEMS AND PROCESSES

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

Revised data:

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Workings:

ACCOUNTING SYSTEMS AND PROCESSES

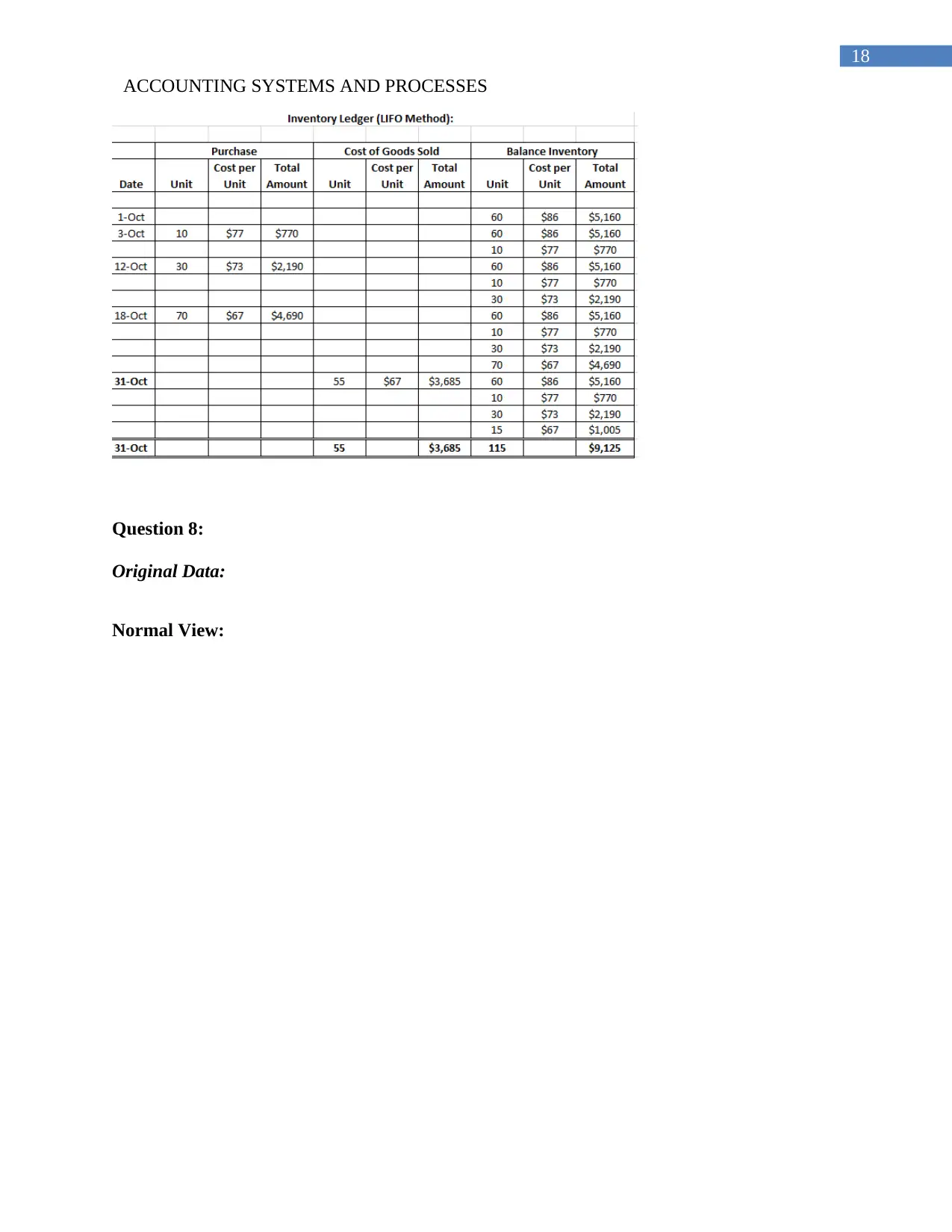

Question 8:

Original Data:

Normal View:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

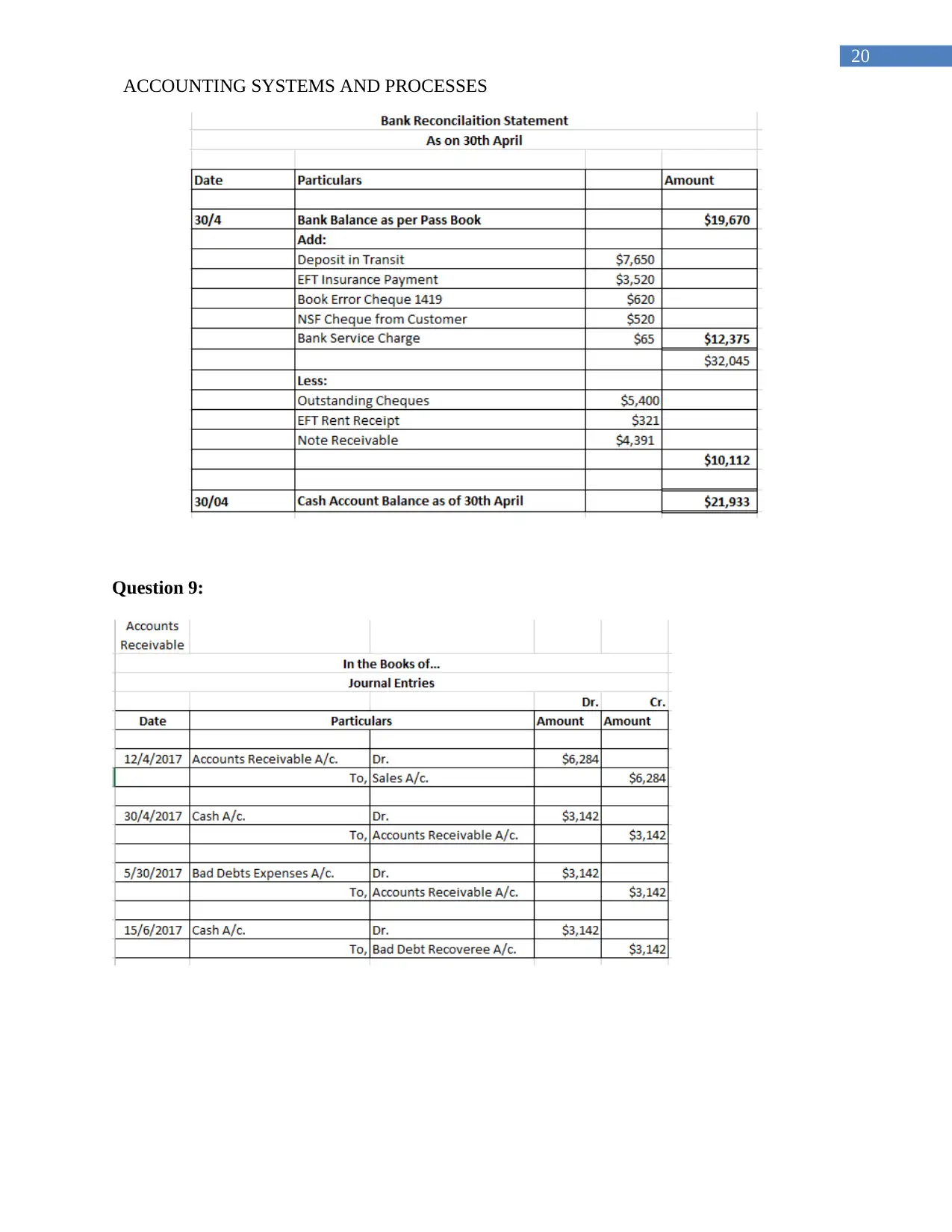

Date Particulars Amount

30/4 Bank Balance as per Pass Book $19,670

Add:

Deposit in Transit $1,543

EFT Insurance Payment $300

Book Error Cheque 1419 $340

NSF Cheque from Customer $1,700

Bank Service Charge $40 $3,923

$23,593

Less:

Outstanding Cheques 2462

EFT Rent Receipt 600

Note Receivable $1,500

$4,562

30/04 Cash Account Balance as of 30th April $19,031

Bank Reconcilaition Statement

As on 30th April

Formula View:

Date Particulars Amount

30/4 Bank Balance as per Pass Book 19670

Add:

Deposit in Transit 1543

EFT Insurance Payment 300

Book Error Cheque 1419 340

NSF Cheque from Customer 1700

Bank Service Charge 40 =SUM(D8:D12)

=E6+E12

Less:

Outstanding Cheques =1532+700+230

EFT Rent Receipt 600

Note Receivable 1500

=SUM(D15:D18)

30/04 =IF(E20>0,"Cash Account Balance as of 30th April","Bank Overdraft Balance as of 30th April") =E13-E18

Bank Reconcilaition Statement

As on 30th April

Revised data:

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Question 9:

ACCOUNTING SYSTEMS AND PROCESSES

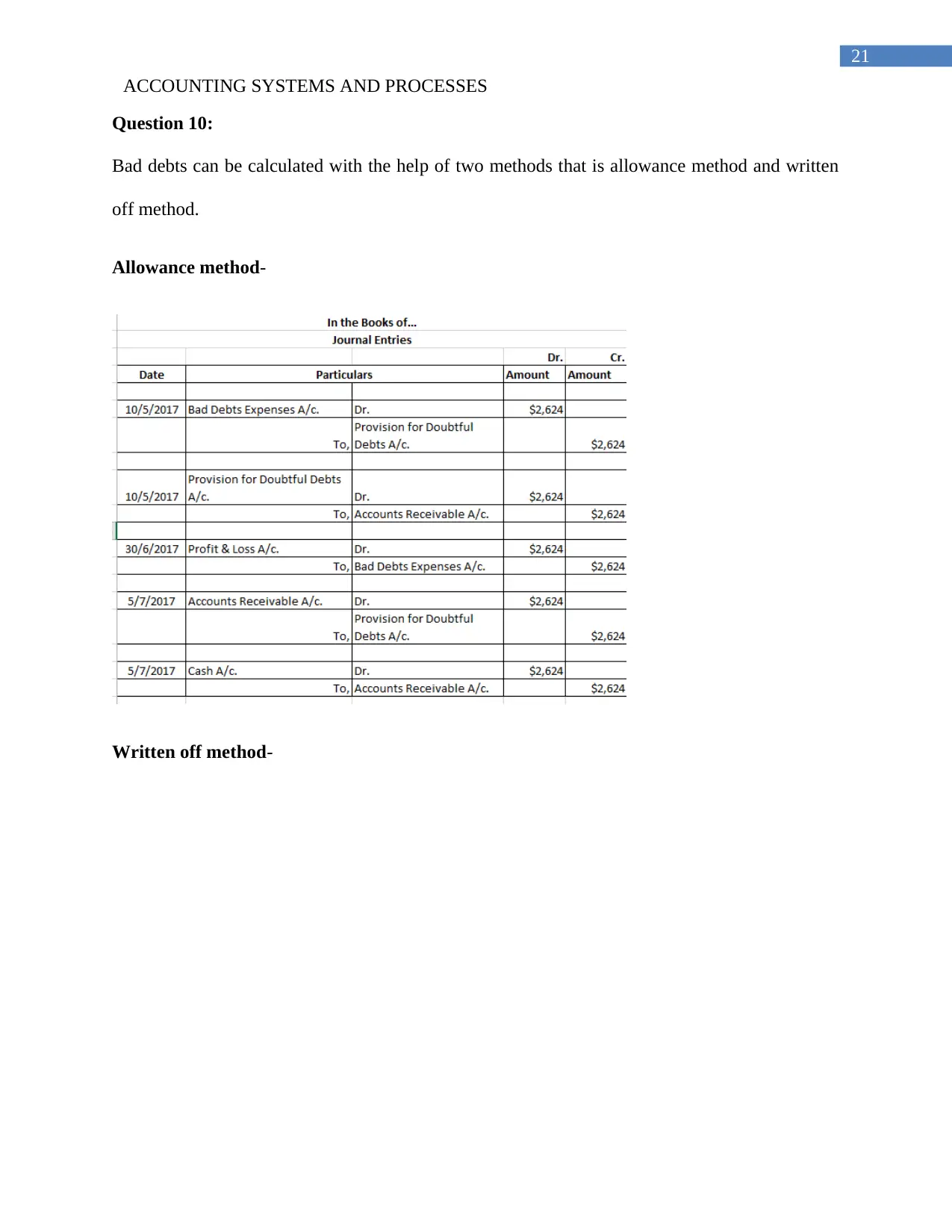

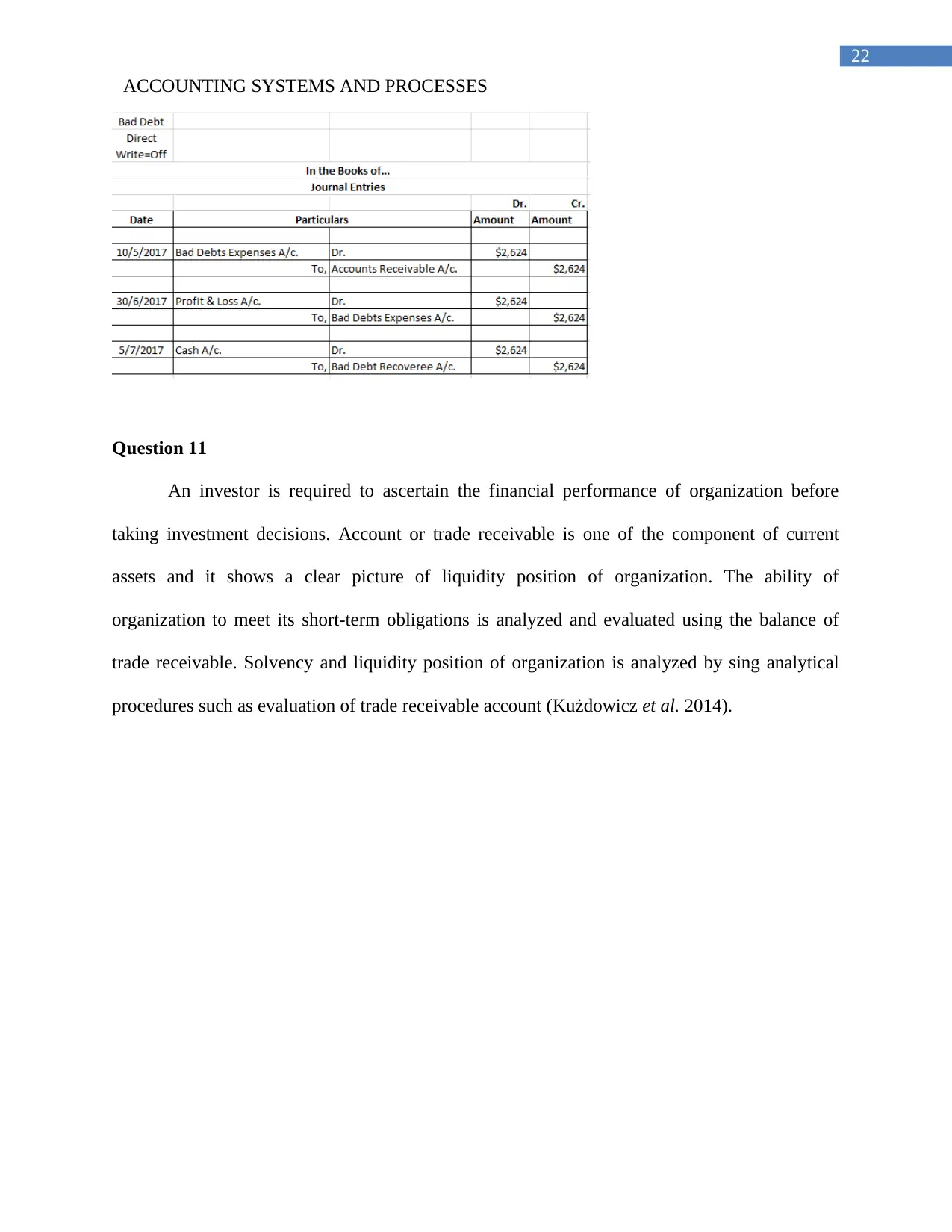

Question 10:

Bad debts can be calculated with the help of two methods that is allowance method and written

off method.

Allowance method-

Written off method-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

Question 11

An investor is required to ascertain the financial performance of organization before

taking investment decisions. Account or trade receivable is one of the component of current

assets and it shows a clear picture of liquidity position of organization. The ability of

organization to meet its short-term obligations is analyzed and evaluated using the balance of

trade receivable. Solvency and liquidity position of organization is analyzed by sing analytical

procedures such as evaluation of trade receivable account (Kużdowicz et al. 2014).

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

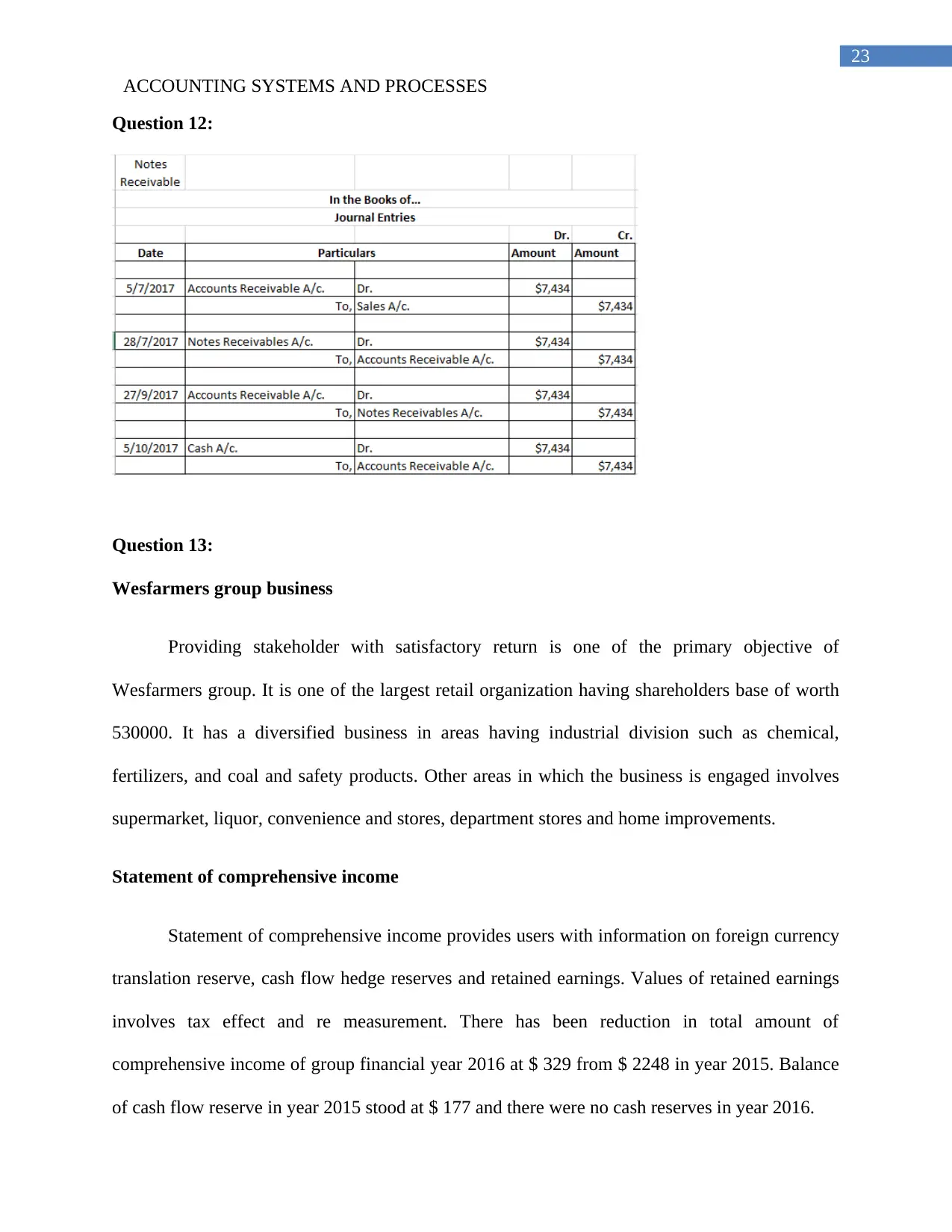

Question 12:

Question 13:

Wesfarmers group business

Providing stakeholder with satisfactory return is one of the primary objective of

Wesfarmers group. It is one of the largest retail organization having shareholders base of worth

530000. It has a diversified business in areas having industrial division such as chemical,

fertilizers, and coal and safety products. Other areas in which the business is engaged involves

supermarket, liquor, convenience and stores, department stores and home improvements.

Statement of comprehensive income

Statement of comprehensive income provides users with information on foreign currency

translation reserve, cash flow hedge reserves and retained earnings. Values of retained earnings

involves tax effect and re measurement. There has been reduction in total amount of

comprehensive income of group financial year 2016 at $ 329 from $ 2248 in year 2015. Balance

of cash flow reserve in year 2015 stood at $ 177 and there were no cash reserves in year 2016.

ACCOUNTING SYSTEMS AND PROCESSES

Commenting on several items of group

Earnings per share- The earning per share of organization as decline significantly in

year 2016 and the value of basic and diluted earning per share remains same. Value of earning

per share relating to both dilute and basic earnings per share is same at 36.2 as against 216.1 in

year 2015. Calculation of diluted and basic EPS involves variances that is attributable to

substance options.

Dividend- Payment of dividend is one of the key component of return to shareholders

and there has been considerable reduction in dividend payment in recent years. The dividend

policy of organization seeks to grow the dividends overtime. For financial year, total value of

dividend paid to shareholders in year 2016 stood at $ 40783 as compared to $ 40402 in year

2015.

Risk and mitigation- One of the focus of organization is to monitor and manage the

risks associated with activities of group. Organization is committed to identify and gain the

needs for minim zing the risks related with business activities. Wesfarmers group has a risk

management framework that intends to manage and monitor the business risks.

Return on equity- an organization obtains return on equity by dividing net income of

organization by total value of shareholder’s equity. Return on average shareholder’s equity as

increased from 9.8 in year 2015 as against 9.6 in year 2016. Decrease in figure is indicative of

fact that organization has not been sufficiently generating return to their shareholders.

Corporate governance- Wesfarmers complies with international standard of corporate

governance. Framework of corporate governance standard is committed towards fulfilling

responsibilities and obligations of corporate governance and providing satisfactory shareholder

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

return. Practice of corporate governance imbibes fostering a compliance culture that

accountability, ethical behaviors and corporate and personal entity.

Sustainability- Organization intends to serve the communities and thereby leading to

long-term value creation. Sustainability of organization is ensured by involvement of long-term

possible management. Several issues that leads to sustainable performance directly impact

financial outcome of organization.

Balance sheet- The balance sheet of organization comprise of items such as total assets,

total liabilities that involves current and non-current assets and liabilities. Total value of current

assets recorded at $ 9684 and total value of current liabilities stood at $ 10424.

Income statement- A detailed picture of revenue, earning before and taxes and revenue

is provided by income statement of organization. There has been increase in revenue generated

by organization to $ 65981 in year 2016 as compared to $ 62447 in year 2015. Profits

attributable to parent company members has declined considerably in recent year.

Working capital ratio calculation:

Working capital ratio indicates the liquidity position of organization that is calculated by

dividing current assets by current liabilities. Delivering satisfactory return to shareholders is

provided by making improvement in working capital efficiency. Vale of current liabilities and

current assets for year 2016 is $ 10424 and $ 9684. Working capital ratio stood at 0.93.

Particular Amount

Current liabilities $ 10424

Current assets $ 9684

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Working capital ratio 0.93

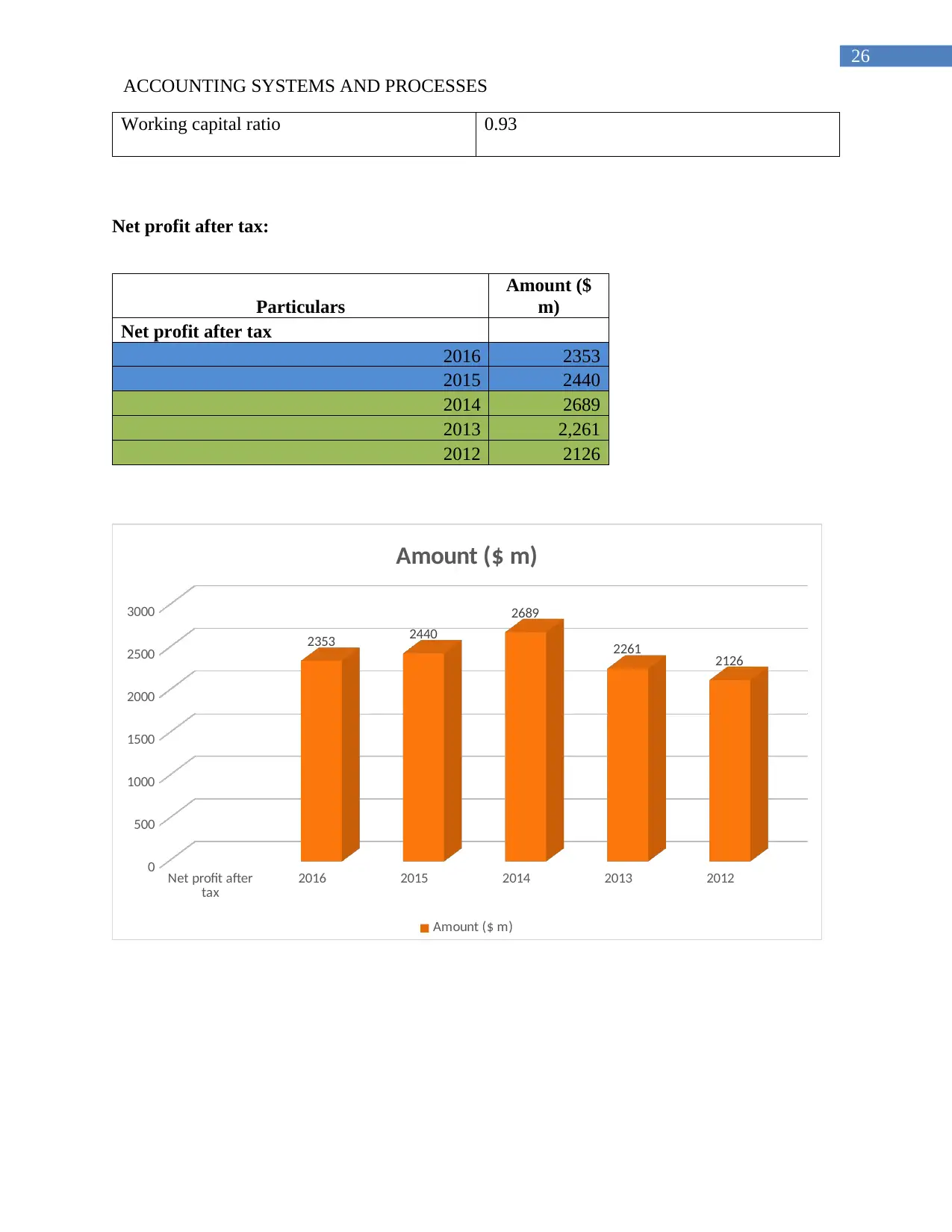

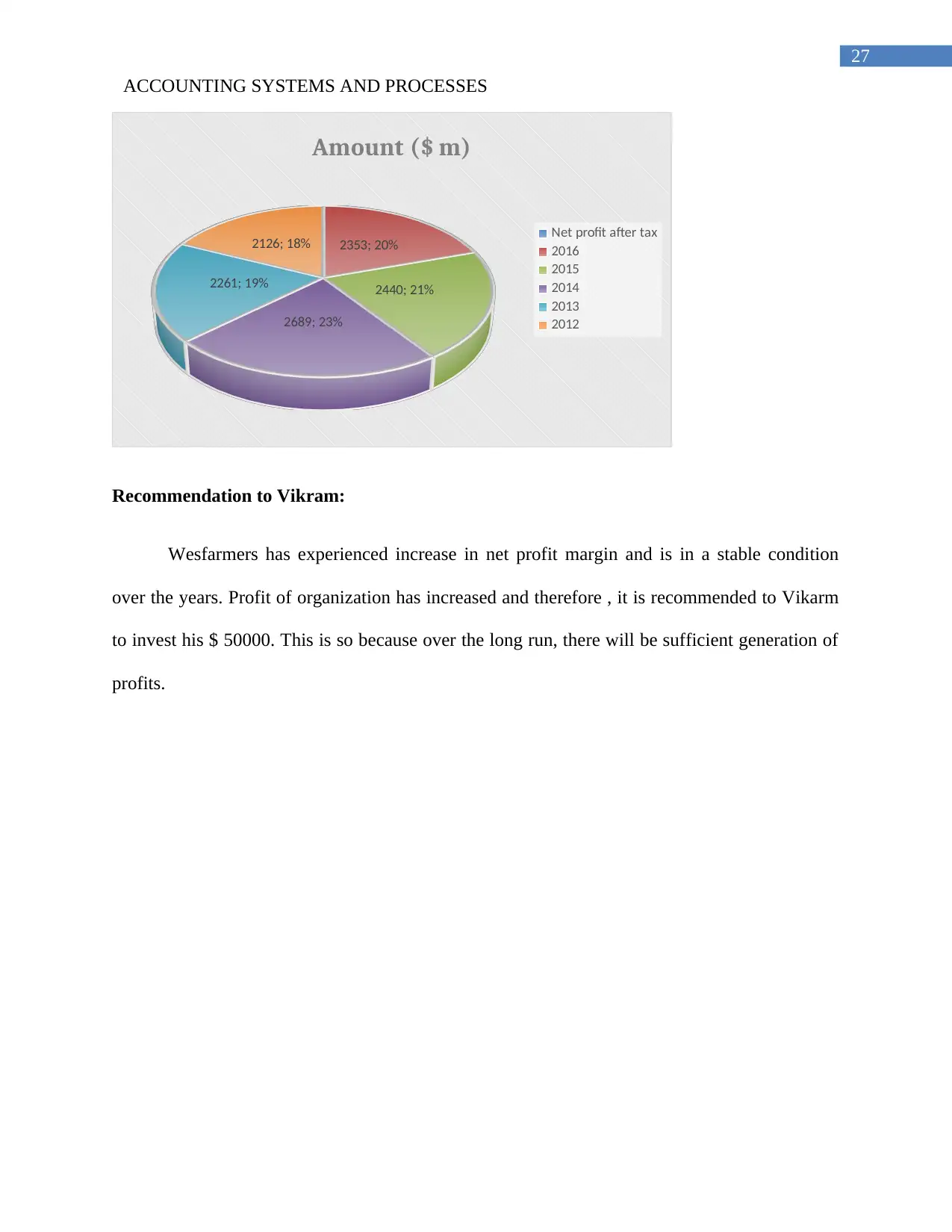

Net profit after tax:

Particulars

Amount ($

m)

Net profit after tax

2016 2353

2015 2440

2014 2689

2013 2,261

2012 2126

Net profit after

tax 2016 2015 2014 2013 2012

0

500

1000

1500

2000

2500

3000

2353 2440

2689

2261 2126

Amount ($ m)

Amount ($ m)

ACCOUNTING SYSTEMS AND PROCESSES

2353; 20%

2440; 21%

2689; 23%

2261; 19%

2126; 18%

Amount ($ m)

Net profit after tax

2016

2015

2014

2013

2012

Recommendation to Vikram:

Wesfarmers has experienced increase in net profit margin and is in a stable condition

over the years. Profit of organization has increased and therefore , it is recommended to Vikarm

to invest his $ 50000. This is so because over the long run, there will be sufficient generation of

profits.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING SYSTEMS AND PROCESSES

References and Bibliography:

Averinà, O. I., Kolesnik, N. F., & Makarova, L. M. (2016). The Integration of the Accounting

System for Implementing World Class Manufacturing (WCM) Principles. European

Research Studies, 19, 53.

Azad, R., Azad, R., Azad, K., & Akbari, F. (2016). The Effect of Cost Accounting System

Inventory on Increasing the Profitability of Products. Journal of Industrial and Intelligent

Information Vol, 4(1).

Greef, A., Healy, J., Reinhold, D., Gall, M., Swaminathan, M., & Schulz, R. (2017). U.S. Patent

No. 9,754,319. Washington, DC: U.S. Patent and Trademark Office.

Jia, S. M., & Sun, Y. (2015). Information quality analysis of computerized accounting system.

Information Management and Management Engineering, 94, 293.

Kużdowicz, P., Kużdowicz, D., & Saniuk, A. (2015). Modeling the accounting system in ERP

software. In Carpathian Logistics Congress-CLC (pp. 1-10).

Lata, P., & Ussahawanitchakit, P. (2015). Management accounting system effectiveness and goal

achievement: evidence from automotive businesses in Thailand. The Business &

Management Review, 7(1), 322.

Swanson, Z. L. (2014). Hyperbolic browser for ERP accounting system pedagogy and

curriculum management. Global Perspectives on Accounting Education, 11, 25.

Paraphrase This Document

ACCOUNTING SYSTEMS AND PROCESSES

Zhang, J., & Xu, L. (2015). Embodied carbon budget accounting system for calculating carbon

footprint of large hydropower project. Journal of Cleaner Production, 96, 444-451.

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.