Comprehensive Accounting Assignment: MUG Ltd. Financial Analysis

VerifiedAdded on 2021/02/20

|10

|1929

|45

Homework Assignment

AI Summary

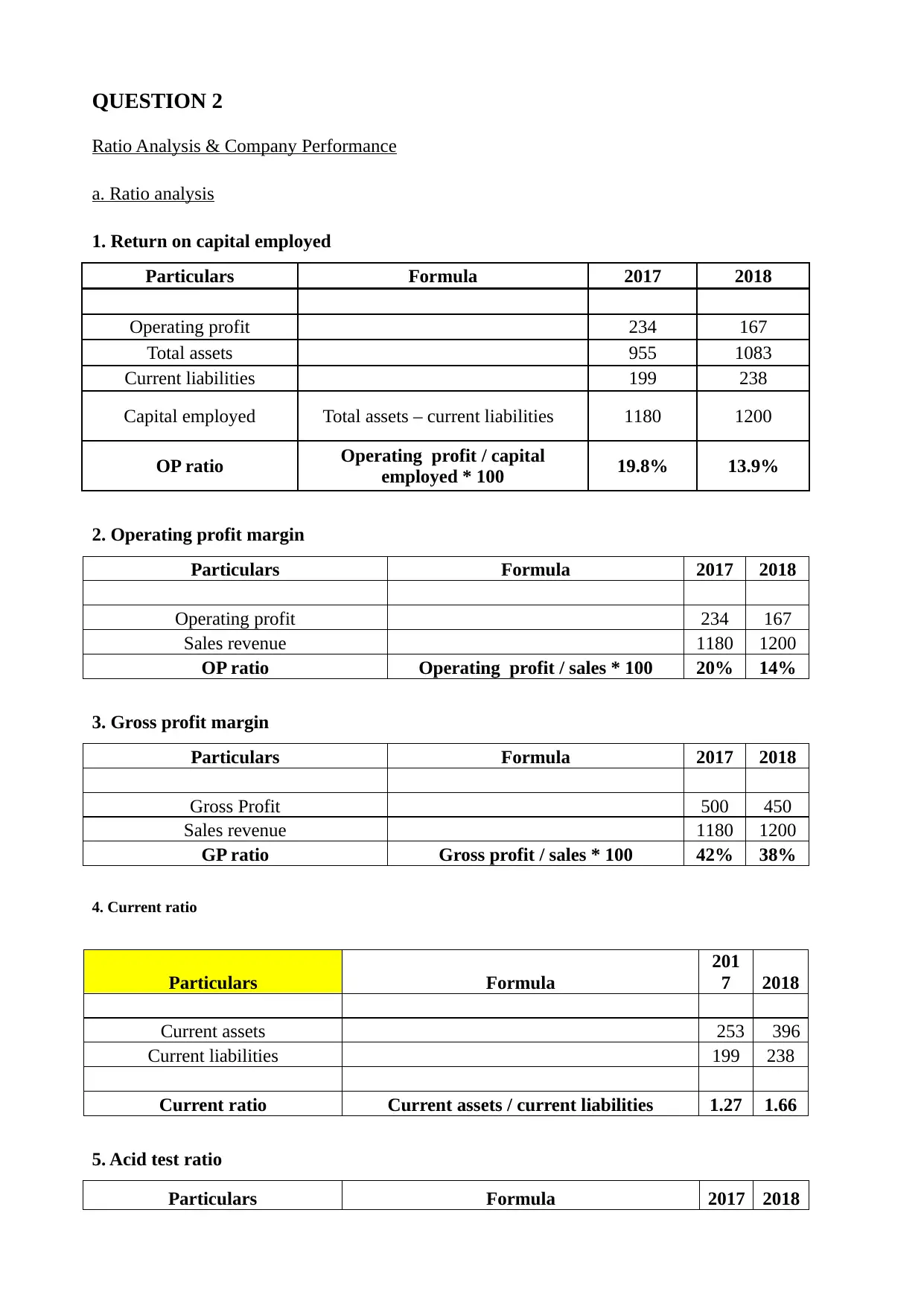

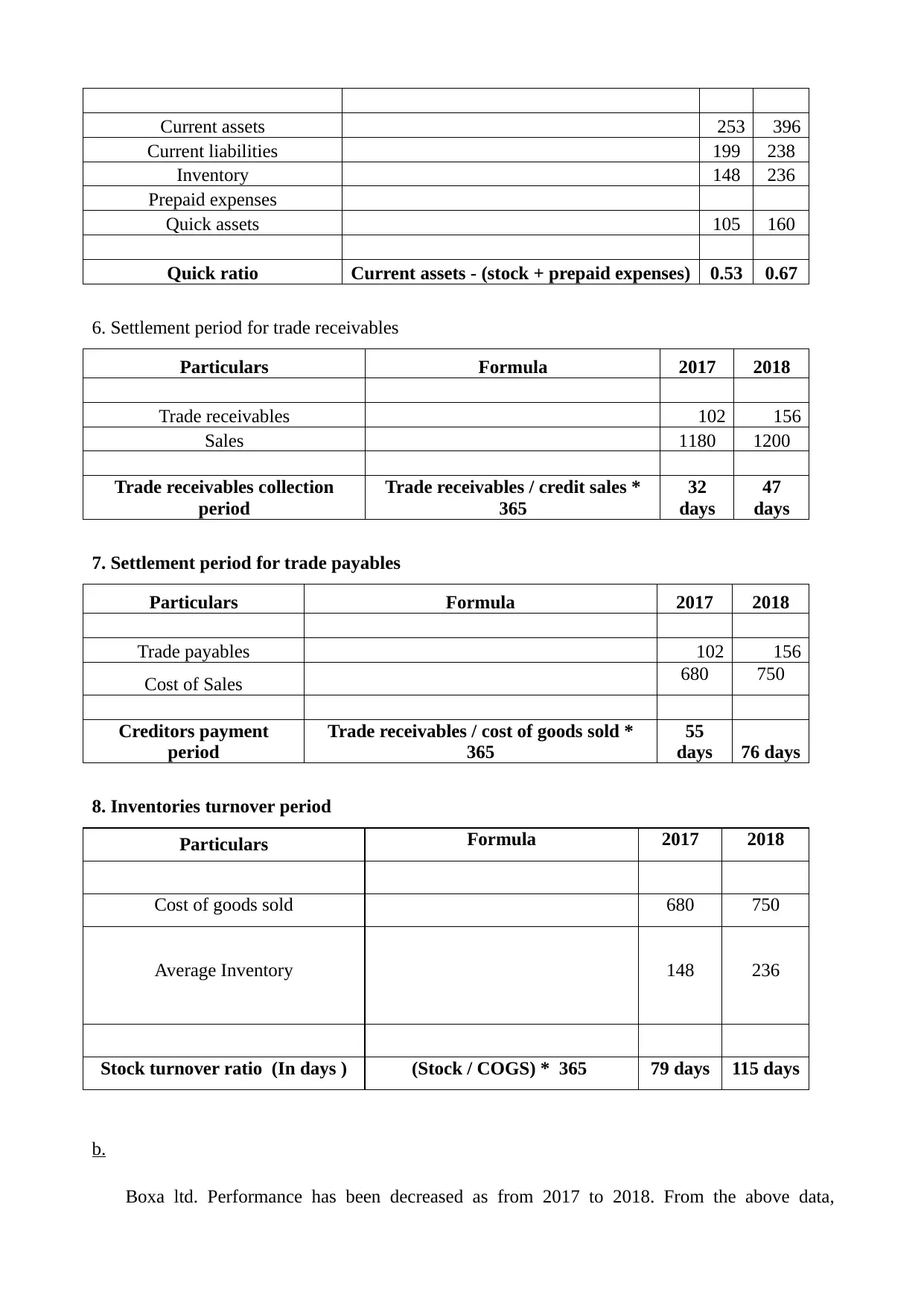

This accounting assignment solution provides a detailed analysis of MUG Ltd.'s financial performance. It includes the preparation of financial statements (Profit & Loss, Balance Sheet, and Cash Flow Statement), followed by a comprehensive ratio analysis covering key metrics such as Return on Capital Employed, Operating Profit Margin, Gross Profit Margin, Current Ratio, Acid Test Ratio, and various turnover ratios. The assignment evaluates the company's performance from 2017 to 2018, highlighting areas of concern like decreasing profitability, increased account receivables, and a longer inventory turnover period. Additionally, the solution explores accountancy theory, specifically budgeting, discussing its advantages, disadvantages, and its application in coordinating and motivating employees. Finally, the assignment addresses crucial accounting concepts and conventions such as prudence, accruals, consistency, going concern, and the dual aspect concept. The conclusion emphasizes the need for Boxa Ltd. to improve its financial ratios and adhere to accounting standards and principles to enhance profitability.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.