HI6025 Accounting Theory: AASB 16 and Lease Accounting Review

VerifiedAdded on 2022/12/26

|13

|4055

|80

Report

AI Summary

This report critically examines AASB 16, the Australian accounting standard for lease financing, replacing the previous AASB 117. It delves into the drawbacks of AASB 117, the necessity for change, and the changes incorporated in AASB 16, inspired by IFRS 16. The report analyzes the impact of AASB 16 on companies with lease financing, highlighting the shift from operating to finance leases. It includes a comparative analysis of AASB 117 and AASB 16, with a practical presentation of financial reporting, using Telstra (ASX: TLS) as a case study to demonstrate required disclosures in their annual financial report. The report also explores the implications for financial statements, key accounting ratios, and banking contracts. Overall, the report aims to provide a comprehensive understanding of the new lease accounting standard and its implications for businesses and stakeholders.

Accounting Theory and Contemporary

Issue

1 | P a g e

Issue

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

This article emphasized on the ensuing issue of AASB 16 to be effective from 1st

January, 2019 in perspective of its old version AASB 117- Leases. The article critically

analyzed the aspects of old AASB standard 117 and the drawbacks of this standard to

replace it with the new version AASB 16. As this standard is related to leases, which is

essential ingredient for any business, accounting standard is required to regulate the

operation of it with its proper presentation in financial reporting. The role of financial

reporting standard through IFRS 16 is prescribed by IASB for generalized presentation

of financial information related to AASB 16. This discussion includes a comparative

analysis of both the standards AASB 117 and AASB 16 with a practical presentation of

financial reporting of any ASX- listed company in respect of required disclosures in their

annual financial report.

Key Words: AASB 117, AASB 16, IFRS 16, Transition, Finance Lease, Operating Lease

2 | P a g e

This article emphasized on the ensuing issue of AASB 16 to be effective from 1st

January, 2019 in perspective of its old version AASB 117- Leases. The article critically

analyzed the aspects of old AASB standard 117 and the drawbacks of this standard to

replace it with the new version AASB 16. As this standard is related to leases, which is

essential ingredient for any business, accounting standard is required to regulate the

operation of it with its proper presentation in financial reporting. The role of financial

reporting standard through IFRS 16 is prescribed by IASB for generalized presentation

of financial information related to AASB 16. This discussion includes a comparative

analysis of both the standards AASB 117 and AASB 16 with a practical presentation of

financial reporting of any ASX- listed company in respect of required disclosures in their

annual financial report.

Key Words: AASB 117, AASB 16, IFRS 16, Transition, Finance Lease, Operating Lease

2 | P a g e

Table of Contents

Introduction................................................................................................................................................4

Discussion.................................................................................................................................................4

AASB 117- Critical analysis and drawback.......................................................................................4

Necessity for change............................................................................................................................5

Changes incorporated in AASB 16.....................................................................................................5

Impact of AASB 16 on the companies with lease financing............................................................6

Inclination to operating lease by companies- AASB 117.................................................................8

Comparison of lessee and lessor as per IFRS 16............................................................................9

Explanation of procurement of new assets-post AASB 16..............................................................9

Disclosure of Lease accounting in Annual report 2018- Telstra(ASX Code TLS)........................9

Conclusion...............................................................................................................................................10

References:................................................................................................................................................12

3 | P a g e

Introduction................................................................................................................................................4

Discussion.................................................................................................................................................4

AASB 117- Critical analysis and drawback.......................................................................................4

Necessity for change............................................................................................................................5

Changes incorporated in AASB 16.....................................................................................................5

Impact of AASB 16 on the companies with lease financing............................................................6

Inclination to operating lease by companies- AASB 117.................................................................8

Comparison of lessee and lessor as per IFRS 16............................................................................9

Explanation of procurement of new assets-post AASB 16..............................................................9

Disclosure of Lease accounting in Annual report 2018- Telstra(ASX Code TLS)........................9

Conclusion...............................................................................................................................................10

References:................................................................................................................................................12

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

AASB 117 was effective since 1st July 2007 by AASB for leases accounting and its

financial presentation in the annual accounting report. This standard was initiated with

the objective of accounting treatment for Leases. Due to its drawbacks regarding

treatment of different types of leases and subsequent loopholes related to its application

of finance and operating leases, the need of new standard was evolved. This situation

led to requirement of amended standard with the assurance of standardized system for

accounting of Leases with more prudent and professional approach. The main objective

of setting accounting standard by regulator is to provide proper treatment of financial

instruments to project financial report more transparent for the stakeholders. The

objective of this article is to provide the discussion about both the standards- the

erstwhile standard AASB 117 and upcoming AASB 16. Main focal points of this

discussion are the features of AASB 117 and its drawbacks, the need for change of this

standard, the application of AASB 16, comparison between the features of both these

standards and exemplification of the application of both these standards in corporate

accounting with the case study of one ASX listed company- Telstra, which has the

business operation with the feature of leases by comparison of exercised standard and

the would-be exercised standard for this accounting issues. Main objective of the

amendment is to ensure proper application of accounting system for the financial

instrument- Leases, to be followed by the corporate. This article will conclude with the

future impact of upcoming standard AASB 16 with its positive features to ensure

prudence and professional presentation of financial accounting for the stakeholders to

make them comfortable and satisfied with the annual financial report for their

subsequent justified decision.

Discussion

AASB 117- Critical analysis and drawback

AASB 117 is inspired by IAS 17 and is insisting on financial treatment and reporting

about the financial instrument-Leases. This standard was effective from 1st July, 2007

for incorporation in accounting reports of business entities involved in leases

transactions. Main interpretation of this standard is to distinguish between operating and

finance leases. The basis of this comparison is on the view point of operating and

finance lease and its subsequent impact on risks faced and rewards achieved, which

are incidental to the proprietorship of any leased assets owned by lessee or lessor. The

identification of finance leases are done when the leases transfer the rewards and risks

to the ownership flowed from lessor to lessee. The identification of operating lease is

made when the rewards or risks of the lease is not transferred from lessor to lessee with

substantial effect. This standard demands that in case of an operating lease, the

payment of lease is to be recognized as the nature of expense on the basis of straight-

line calculation; if any other suitable basis found more authentic as per the time frame of

the user’s gain. Normal business practice endorses the lease concept for one or more

4 | P a g e

AASB 117 was effective since 1st July 2007 by AASB for leases accounting and its

financial presentation in the annual accounting report. This standard was initiated with

the objective of accounting treatment for Leases. Due to its drawbacks regarding

treatment of different types of leases and subsequent loopholes related to its application

of finance and operating leases, the need of new standard was evolved. This situation

led to requirement of amended standard with the assurance of standardized system for

accounting of Leases with more prudent and professional approach. The main objective

of setting accounting standard by regulator is to provide proper treatment of financial

instruments to project financial report more transparent for the stakeholders. The

objective of this article is to provide the discussion about both the standards- the

erstwhile standard AASB 117 and upcoming AASB 16. Main focal points of this

discussion are the features of AASB 117 and its drawbacks, the need for change of this

standard, the application of AASB 16, comparison between the features of both these

standards and exemplification of the application of both these standards in corporate

accounting with the case study of one ASX listed company- Telstra, which has the

business operation with the feature of leases by comparison of exercised standard and

the would-be exercised standard for this accounting issues. Main objective of the

amendment is to ensure proper application of accounting system for the financial

instrument- Leases, to be followed by the corporate. This article will conclude with the

future impact of upcoming standard AASB 16 with its positive features to ensure

prudence and professional presentation of financial accounting for the stakeholders to

make them comfortable and satisfied with the annual financial report for their

subsequent justified decision.

Discussion

AASB 117- Critical analysis and drawback

AASB 117 is inspired by IAS 17 and is insisting on financial treatment and reporting

about the financial instrument-Leases. This standard was effective from 1st July, 2007

for incorporation in accounting reports of business entities involved in leases

transactions. Main interpretation of this standard is to distinguish between operating and

finance leases. The basis of this comparison is on the view point of operating and

finance lease and its subsequent impact on risks faced and rewards achieved, which

are incidental to the proprietorship of any leased assets owned by lessee or lessor. The

identification of finance leases are done when the leases transfer the rewards and risks

to the ownership flowed from lessor to lessee. The identification of operating lease is

made when the rewards or risks of the lease is not transferred from lessor to lessee with

substantial effect. This standard demands that in case of an operating lease, the

payment of lease is to be recognized as the nature of expense on the basis of straight-

line calculation; if any other suitable basis found more authentic as per the time frame of

the user’s gain. Normal business practice endorses the lease concept for one or more

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

resources to be used in the respective business. The most prolific instances of this

lease are the lease of equipments, office premises and vehicles. The objective of

operating leases is to enjoy access to the specific assets with obtaining finance and

ensuring the reduction to the profile of the lessee in regard to risk of the ownership of

such assets.

Main drawback of AASB 117 was in its financial treatment and subsequent reporting

about the lease accounting. This standard endorses the concept of classifying and

adopting financial leases at same situations occur to the procured assets with

subsequent reporting them in the balance sheet. Any other situations of leases were

classified in the form of operating lease with subsequent impact of not following the

measurement method to report them in the financial statements. (McKinney et al., 2018)

Necessity for change

AASB 117 was framed with the concept of two different leases- finance and operating.

With this concept, the regulators thought that some loopholes were there, through which

the reporting is not matching with the practical demand of the financial reporting to

satisfy the needs of the stakeholders. To remove this shortcoming of AASB 117, the

regulators made amendment to the standard with specification AASB 16. The new

standard will amend the definition of the lease with dual classification and make all the

leases come under one umbrella of Lease. The resultant treatment will be featured in

the balance sheet as per the standing practice of finance lease under AASB 117. This

new accounting standard AASB 16 ensures featuring of any type of Leases in the

Balance Sheet. IFRS 16 will ensure substantial impact on the financial reporting of the

business entities with no option for operating lease through income statement. The

accounting treatment of all leases in the financial report will feature in balance sheet

through assets with right of use and liabilities. Erstwhile accounting treatment under

AASB 117 confused the stakeholders to assess the accuracy of the financial statement

of the respective company to project true picture of financial position of the entity. AASB

16 ensures the abolition of such ambiguity with insertion of all the leases irrespective of

their nomenclature to include in the financial report of the entity with same treatment of

finance lease. AASB 16 will also feature with the liability related to lease accounts and

the respective right to use the specified asset with allied benefits in the financial

statement of the company. (Ohm, 2018)

Changes incorporated in AASB 16

This standard is featured with some basic consideration in the form of date of

application and provisions for transition period. (Azih, 2018) The date of application is

on or after 1st July, 2019. The entities can apply early adoption of this standard if they

are complaint to new standard AASB 15- Revenue recognition on the date of AASB 16

application or prior to that. (Koo & KordaMentha, 2016)

This standard is with two main transitional provisions options- Full Retrospective and

Cumulative Retrospective.

5 | P a g e

lease are the lease of equipments, office premises and vehicles. The objective of

operating leases is to enjoy access to the specific assets with obtaining finance and

ensuring the reduction to the profile of the lessee in regard to risk of the ownership of

such assets.

Main drawback of AASB 117 was in its financial treatment and subsequent reporting

about the lease accounting. This standard endorses the concept of classifying and

adopting financial leases at same situations occur to the procured assets with

subsequent reporting them in the balance sheet. Any other situations of leases were

classified in the form of operating lease with subsequent impact of not following the

measurement method to report them in the financial statements. (McKinney et al., 2018)

Necessity for change

AASB 117 was framed with the concept of two different leases- finance and operating.

With this concept, the regulators thought that some loopholes were there, through which

the reporting is not matching with the practical demand of the financial reporting to

satisfy the needs of the stakeholders. To remove this shortcoming of AASB 117, the

regulators made amendment to the standard with specification AASB 16. The new

standard will amend the definition of the lease with dual classification and make all the

leases come under one umbrella of Lease. The resultant treatment will be featured in

the balance sheet as per the standing practice of finance lease under AASB 117. This

new accounting standard AASB 16 ensures featuring of any type of Leases in the

Balance Sheet. IFRS 16 will ensure substantial impact on the financial reporting of the

business entities with no option for operating lease through income statement. The

accounting treatment of all leases in the financial report will feature in balance sheet

through assets with right of use and liabilities. Erstwhile accounting treatment under

AASB 117 confused the stakeholders to assess the accuracy of the financial statement

of the respective company to project true picture of financial position of the entity. AASB

16 ensures the abolition of such ambiguity with insertion of all the leases irrespective of

their nomenclature to include in the financial report of the entity with same treatment of

finance lease. AASB 16 will also feature with the liability related to lease accounts and

the respective right to use the specified asset with allied benefits in the financial

statement of the company. (Ohm, 2018)

Changes incorporated in AASB 16

This standard is featured with some basic consideration in the form of date of

application and provisions for transition period. (Azih, 2018) The date of application is

on or after 1st July, 2019. The entities can apply early adoption of this standard if they

are complaint to new standard AASB 15- Revenue recognition on the date of AASB 16

application or prior to that. (Koo & KordaMentha, 2016)

This standard is with two main transitional provisions options- Full Retrospective and

Cumulative Retrospective.

5 | P a g e

Full Retrospective endorses the concept of retrospective application of this standard to

periods of earlier reporting with the consideration of AASB 16, effective from the starting

of every lease. In that case the impact of comparatives and opening retained earnings

would be amended as per the standard.

Cumulative Retrospective will feature with the recognition of the initial date of

application as per AASB 16. This option does not demand the comparative information

to be refurnished. Only the opening retained earnings are to be amended as of the initial

date of application.

These needs of transitional impacts are endorsing the allowance for some applicable

practical measures.

As per AASB 16, identification of lease is to be done with the feature of any contract

containing a Lease. This practice can be ensured through the consideration of right to

control of use of any specific asset for any specified tenure of time in exchange for the

purpose of consideration. The need for reassessing of contracts will be required at the

initial stage of application unless the entity selects the adoption of the practical

measurement exemption. (BDOAustralia, nd)

Lease Accounting under AASB 16 demands two aspects- liability of Lease and right of

use of the specific asset. The standard demands recognition of asset by lessees to

determine the right of use of that asset along with its respective liability. To derive the

right of use of any asset, first factor to determine is to measure the lease liability; and

after that the calculation of preliminary cost of the right of use of specific asset can be

determined through initial barrier of lease liability. (Fonteyn, 2017)

Implication in financial statements is expected in the accounting of lessee. In the

balance sheet, the recognition of leases will be done to clarify the right of use of any

asset and the allied liability related to that asset. This treatment will obviously increase

the total value assets with corresponding liabilities in comparison with the provision to

recognizing the assets under operating lease as per previous standard AASB 117.

Implication in income statement will feature refreshed treatment of recognized operating

lease expense. The amended standard made provision with the replacement by

amortization and expense of related interest methodology as per AASB 16. The impact

may feature inflated EBITDA and diversion from the earlier recognition of operating

lease done though straight-line system. Apart from these effects in the financial reports,

the entities have to consider other impacts on the domains of key accounting ratios,

banking contracts, etc. (Gummery, 2019)

Impact of AASB 16 on the companies with lease financing

To cope up with the requirement of AASB 16 compliance, the companies with

substantial lease financing have to fasten their seat belts to be ready to meet the

requirements of the ensuing standard. There are different areas in which the

companies have to make them ready for the upcoming changes with real

6 | P a g e

periods of earlier reporting with the consideration of AASB 16, effective from the starting

of every lease. In that case the impact of comparatives and opening retained earnings

would be amended as per the standard.

Cumulative Retrospective will feature with the recognition of the initial date of

application as per AASB 16. This option does not demand the comparative information

to be refurnished. Only the opening retained earnings are to be amended as of the initial

date of application.

These needs of transitional impacts are endorsing the allowance for some applicable

practical measures.

As per AASB 16, identification of lease is to be done with the feature of any contract

containing a Lease. This practice can be ensured through the consideration of right to

control of use of any specific asset for any specified tenure of time in exchange for the

purpose of consideration. The need for reassessing of contracts will be required at the

initial stage of application unless the entity selects the adoption of the practical

measurement exemption. (BDOAustralia, nd)

Lease Accounting under AASB 16 demands two aspects- liability of Lease and right of

use of the specific asset. The standard demands recognition of asset by lessees to

determine the right of use of that asset along with its respective liability. To derive the

right of use of any asset, first factor to determine is to measure the lease liability; and

after that the calculation of preliminary cost of the right of use of specific asset can be

determined through initial barrier of lease liability. (Fonteyn, 2017)

Implication in financial statements is expected in the accounting of lessee. In the

balance sheet, the recognition of leases will be done to clarify the right of use of any

asset and the allied liability related to that asset. This treatment will obviously increase

the total value assets with corresponding liabilities in comparison with the provision to

recognizing the assets under operating lease as per previous standard AASB 117.

Implication in income statement will feature refreshed treatment of recognized operating

lease expense. The amended standard made provision with the replacement by

amortization and expense of related interest methodology as per AASB 16. The impact

may feature inflated EBITDA and diversion from the earlier recognition of operating

lease done though straight-line system. Apart from these effects in the financial reports,

the entities have to consider other impacts on the domains of key accounting ratios,

banking contracts, etc. (Gummery, 2019)

Impact of AASB 16 on the companies with lease financing

To cope up with the requirement of AASB 16 compliance, the companies with

substantial lease financing have to fasten their seat belts to be ready to meet the

requirements of the ensuing standard. There are different areas in which the

companies have to make them ready for the upcoming changes with real

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

understanding and respective preparation for this standard to be applied. AASB 16 is

the new standard and IFRS 16 is the instrument through which the compliance of this

standard will be ensured by the companies in their financial reporting. For proper

compliance of this standard, different level of stakeholders of the company have to be

well aware of the changes coming to the accounting system of the company and

then, through proper knowledge-sharing and discussion, those changes are to be

implemented by the company with transitional impact in lease accounting of the

company. There are different challenges in this aspect for the company. Basic

challenge will be considered as accumulation of required data with its proven

authenticity and the readiness of the systems of the company. (Deloitte, 2018)

For proper accumulation of authentic data, the representatives of the departments to

be involved through efficient project governance for discussion, knowledge-sharing

and planning are:

Finance and accounting;

Property and real estate;

Department of operations;

Department of purchase;

Information Technology;

Treasury;

Tax;

Investor’s relation.

After the identification of different stakeholders, communication should start between

them regarding responsibilities and timeline for execution. If necessary, support from

external contributor may also be welcome at different stages during the project of

transition. (LLP, 2018)

For successful implementation of AASB 16, the assessment for readiness of the

company is to be done. For this purpose a questionnaire consisting of 10 key

questions are to be considered, as furnished below:

1. Identification of the contracts with context of lease;

2. Ability to capture all necessary information by the process and system;

3. Ability of process and system to monitor lease and to keep track of the needed

continuous assessments;

4. Ability to consider the use of IFRS 16 as per exemptions related to recognition

with practical measurements;

5. Identification of available relief regarding transition, and if the company will

apply for them;

6. Identification of discount rates for different types of leases;

7. Consideration of the effects in financial reporting with its results and respective

position;

8. Communication of the effects of AASB 16 application to the respective

stakeholders;

7 | P a g e

the new standard and IFRS 16 is the instrument through which the compliance of this

standard will be ensured by the companies in their financial reporting. For proper

compliance of this standard, different level of stakeholders of the company have to be

well aware of the changes coming to the accounting system of the company and

then, through proper knowledge-sharing and discussion, those changes are to be

implemented by the company with transitional impact in lease accounting of the

company. There are different challenges in this aspect for the company. Basic

challenge will be considered as accumulation of required data with its proven

authenticity and the readiness of the systems of the company. (Deloitte, 2018)

For proper accumulation of authentic data, the representatives of the departments to

be involved through efficient project governance for discussion, knowledge-sharing

and planning are:

Finance and accounting;

Property and real estate;

Department of operations;

Department of purchase;

Information Technology;

Treasury;

Tax;

Investor’s relation.

After the identification of different stakeholders, communication should start between

them regarding responsibilities and timeline for execution. If necessary, support from

external contributor may also be welcome at different stages during the project of

transition. (LLP, 2018)

For successful implementation of AASB 16, the assessment for readiness of the

company is to be done. For this purpose a questionnaire consisting of 10 key

questions are to be considered, as furnished below:

1. Identification of the contracts with context of lease;

2. Ability to capture all necessary information by the process and system;

3. Ability of process and system to monitor lease and to keep track of the needed

continuous assessments;

4. Ability to consider the use of IFRS 16 as per exemptions related to recognition

with practical measurements;

5. Identification of available relief regarding transition, and if the company will

apply for them;

6. Identification of discount rates for different types of leases;

7. Consideration of the effects in financial reporting with its results and respective

position;

8. Communication of the effects of AASB 16 application to the respective

stakeholders;

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9. Planning of tax impact consideration;

10. Assessment of existing leasing strategy with further need of change

identification.

The companies with significant level of lease financing will be affected as per the

nature of leases. They have to be reviewed with conversion method of different

leases to be covered under one lease to avoid complexity of understanding and

respective treatment. (PwC, 2016)

Inclination to operating lease by companies- AASB 117

As per AASB 117, there are provisions of two types of leases- financial lease and

operating lease. The definitions of these two types of leases are differentiated by the

feature of transfer of allied risks and rewards to the ownership of the assets and

liabilities. When financial lease is confirming the transfer of substantial risk and

reward factor to the ownership, operating lease is not acknowledging the same in

respect of risk and reward factor fully to the ownership. (AASB, 2015)

To understand the fascination of the companies to consider the assets or liabilities in

respect of lease treatment, we have to find the benefits provided by operating lease

for the companies, which are absent from finance lease concept. The advantages

are: (Advantage, 2013)

Absence of residual risk featuring uncertainty of the asset value at the

termination of lease period;

Fixed ongoing payments inclusive of payment towards lease of referred asset

and allied payments related to maintenance and operation of that asset.

Off-Balance sheet treatment in financial presentation with projection of

expenses in income statement for expenses related to liability or asset

considered for this purpose;

Tax benefit arising out of the operating lease of asset by full amount from tax

perspective. (Finder, 2019)

Positive Accounting theory highlighted its role with prediction of such activities as the

selection of accounting process by entities with subsequent reciprocation by the

entities to new standard of accounting. Three hypotheses of this theory are:

Maximization of compensation for managers- Bonus Plan Hypothesis;

Mitigation of problems by the creditors- Debt Covenant Hypothesis;

Minimization of political effect- Political Cost Hypothesis. (Demski, 1988)

The managers tend to adopt operating lease to maximize their compensation with

less problem with creditors and minimized intervention by politics. (REPeC, 2017)

8 | P a g e

10. Assessment of existing leasing strategy with further need of change

identification.

The companies with significant level of lease financing will be affected as per the

nature of leases. They have to be reviewed with conversion method of different

leases to be covered under one lease to avoid complexity of understanding and

respective treatment. (PwC, 2016)

Inclination to operating lease by companies- AASB 117

As per AASB 117, there are provisions of two types of leases- financial lease and

operating lease. The definitions of these two types of leases are differentiated by the

feature of transfer of allied risks and rewards to the ownership of the assets and

liabilities. When financial lease is confirming the transfer of substantial risk and

reward factor to the ownership, operating lease is not acknowledging the same in

respect of risk and reward factor fully to the ownership. (AASB, 2015)

To understand the fascination of the companies to consider the assets or liabilities in

respect of lease treatment, we have to find the benefits provided by operating lease

for the companies, which are absent from finance lease concept. The advantages

are: (Advantage, 2013)

Absence of residual risk featuring uncertainty of the asset value at the

termination of lease period;

Fixed ongoing payments inclusive of payment towards lease of referred asset

and allied payments related to maintenance and operation of that asset.

Off-Balance sheet treatment in financial presentation with projection of

expenses in income statement for expenses related to liability or asset

considered for this purpose;

Tax benefit arising out of the operating lease of asset by full amount from tax

perspective. (Finder, 2019)

Positive Accounting theory highlighted its role with prediction of such activities as the

selection of accounting process by entities with subsequent reciprocation by the

entities to new standard of accounting. Three hypotheses of this theory are:

Maximization of compensation for managers- Bonus Plan Hypothesis;

Mitigation of problems by the creditors- Debt Covenant Hypothesis;

Minimization of political effect- Political Cost Hypothesis. (Demski, 1988)

The managers tend to adopt operating lease to maximize their compensation with

less problem with creditors and minimized intervention by politics. (REPeC, 2017)

8 | P a g e

Comparison of lessee and lessor as per IFRS 16

The comparison between lessee and lessor regarding implementation of IFRS 16 has

accounting impact between them.

Lessor accounting will not feature any significant changes compared to erstwhile

practice. The recognition of finance lease is not required by the lessor as the related

risk and award of the lease is not owned by the lessor. (BDO, 2018)

For Lessee accounting, due to conversion of leases to finance lease, main feature to

consider is ‘right of use approach’ for the lessee as per IFRS 16. There is limited scope

of application of operating lease when the lease is of short-term period(less than 12

months) or the referred asset is of low value. IFRS 16 proposes the recognition of

liability of lease of both liability and asset including the right of use of asset in the

balance sheet. The liability is to be calculated on the basis of present value of lease

payment with basic term of lease. In addition of recognition of ‘initial direct costs’ made

for the right to use of the asset with depreciation in straight-line method with elimination

of ‘leasing incentives’, lessee has to recognize all leases in the balance sheet. (Vistra,

2019)

Explanation of procurement of new assets-post AASB 16

The main benefit of lease accounting as per AASB 117 was with lessee to treat most

of the leases as operating types, with easier accounting implications and benefit of

incentives. When these benefits are not prevalent for lessee with effect of AASB 16,

the companies may tend to buy more assets without taken them on lease for the

reason of complexity of financial treatment and subsequent accounting disclosures

under AASB 16. In totality, the lessee has to provide financial disclosure under IFRS

16from 16.51 to 16.60 (10); the lessor has to provide disclosure from 16.89 to 16.92

(4), the finance lease attracts disclosure from 16.93 to 16.94 (92) and operating lease

demands disclosure 16.95 to 16.97 (3). (CPAAustralia, 2019)

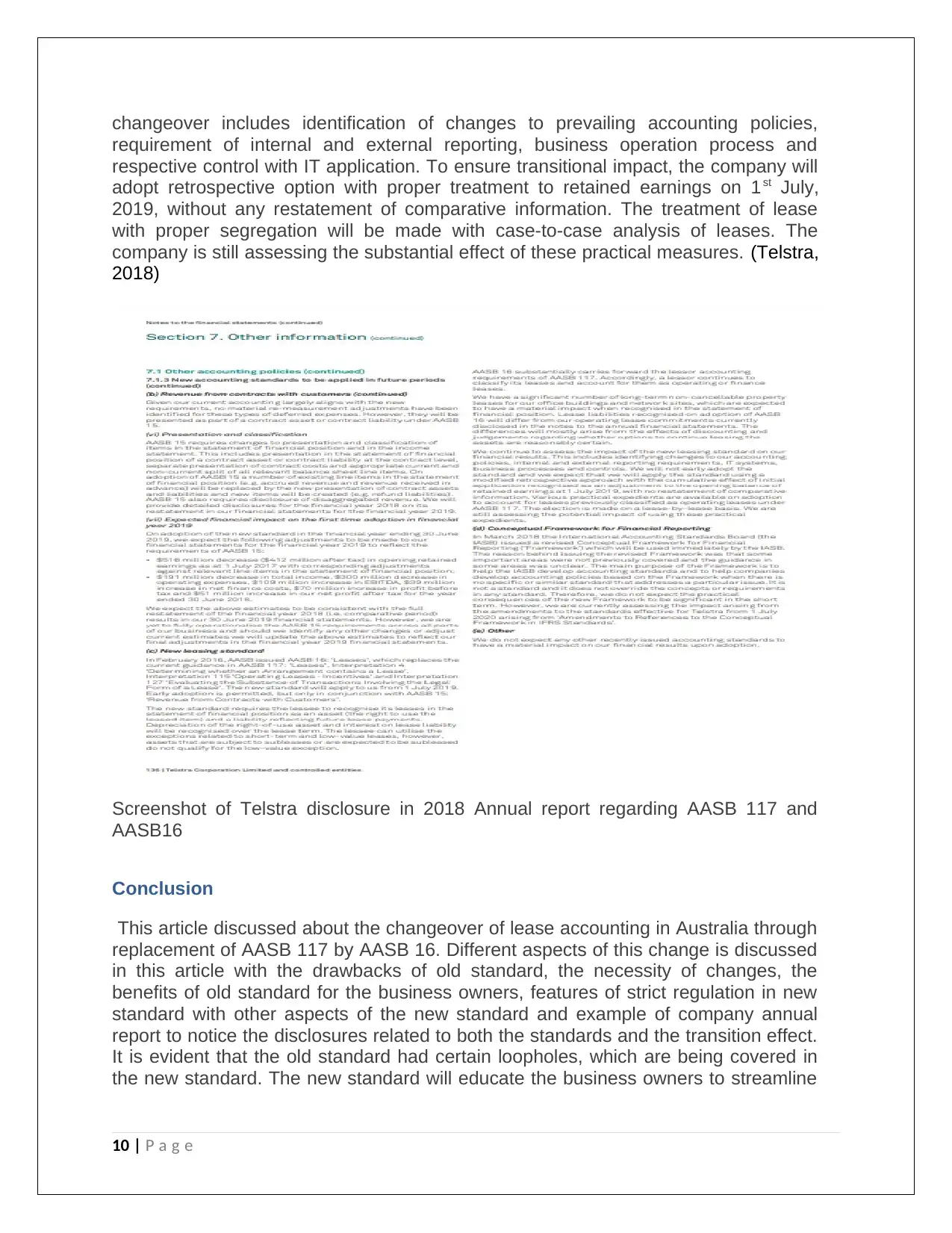

Disclosure of Lease accounting in Annual report 2018- Telstra(ASX Code TLS)

Telstra had disclosed certain views in their annual report 2018 related AASB 117 and

AASB 16. The report highlighted the amendments made in IFRS 16 for definition with

subsequent treatment of lease prevalent in AASB 117. The application date was

mentioned as 1st July, 2019. Early adoption is possible if prior implementation of

amended AASB 15 for revenue recognition from contracts and customers is done by

the company. AASB 16 needs to revisit the company accounting process related to

lease. The company has long term assets taken on lease in the form of building and

site office, which are to be continued with the upcoming IFRS 16 to convert them to

finance lease with reciprocal impact of right of use of asset concept. Adoption of new

standard will have impact in the annual financial reporting with possible difference

due to the effects of earlier discounting and respective decisions. The changeover of

accounting policy is certain related to adoption of AASB16 from 1st July, 2019. The

9 | P a g e

The comparison between lessee and lessor regarding implementation of IFRS 16 has

accounting impact between them.

Lessor accounting will not feature any significant changes compared to erstwhile

practice. The recognition of finance lease is not required by the lessor as the related

risk and award of the lease is not owned by the lessor. (BDO, 2018)

For Lessee accounting, due to conversion of leases to finance lease, main feature to

consider is ‘right of use approach’ for the lessee as per IFRS 16. There is limited scope

of application of operating lease when the lease is of short-term period(less than 12

months) or the referred asset is of low value. IFRS 16 proposes the recognition of

liability of lease of both liability and asset including the right of use of asset in the

balance sheet. The liability is to be calculated on the basis of present value of lease

payment with basic term of lease. In addition of recognition of ‘initial direct costs’ made

for the right to use of the asset with depreciation in straight-line method with elimination

of ‘leasing incentives’, lessee has to recognize all leases in the balance sheet. (Vistra,

2019)

Explanation of procurement of new assets-post AASB 16

The main benefit of lease accounting as per AASB 117 was with lessee to treat most

of the leases as operating types, with easier accounting implications and benefit of

incentives. When these benefits are not prevalent for lessee with effect of AASB 16,

the companies may tend to buy more assets without taken them on lease for the

reason of complexity of financial treatment and subsequent accounting disclosures

under AASB 16. In totality, the lessee has to provide financial disclosure under IFRS

16from 16.51 to 16.60 (10); the lessor has to provide disclosure from 16.89 to 16.92

(4), the finance lease attracts disclosure from 16.93 to 16.94 (92) and operating lease

demands disclosure 16.95 to 16.97 (3). (CPAAustralia, 2019)

Disclosure of Lease accounting in Annual report 2018- Telstra(ASX Code TLS)

Telstra had disclosed certain views in their annual report 2018 related AASB 117 and

AASB 16. The report highlighted the amendments made in IFRS 16 for definition with

subsequent treatment of lease prevalent in AASB 117. The application date was

mentioned as 1st July, 2019. Early adoption is possible if prior implementation of

amended AASB 15 for revenue recognition from contracts and customers is done by

the company. AASB 16 needs to revisit the company accounting process related to

lease. The company has long term assets taken on lease in the form of building and

site office, which are to be continued with the upcoming IFRS 16 to convert them to

finance lease with reciprocal impact of right of use of asset concept. Adoption of new

standard will have impact in the annual financial reporting with possible difference

due to the effects of earlier discounting and respective decisions. The changeover of

accounting policy is certain related to adoption of AASB16 from 1st July, 2019. The

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

changeover includes identification of changes to prevailing accounting policies,

requirement of internal and external reporting, business operation process and

respective control with IT application. To ensure transitional impact, the company will

adopt retrospective option with proper treatment to retained earnings on 1st July,

2019, without any restatement of comparative information. The treatment of lease

with proper segregation will be made with case-to-case analysis of leases. The

company is still assessing the substantial effect of these practical measures. (Telstra,

2018)

Screenshot of Telstra disclosure in 2018 Annual report regarding AASB 117 and

AASB16

Conclusion

This article discussed about the changeover of lease accounting in Australia through

replacement of AASB 117 by AASB 16. Different aspects of this change is discussed

in this article with the drawbacks of old standard, the necessity of changes, the

benefits of old standard for the business owners, features of strict regulation in new

standard with other aspects of the new standard and example of company annual

report to notice the disclosures related to both the standards and the transition effect.

It is evident that the old standard had certain loopholes, which are being covered in

the new standard. The new standard will educate the business owners to streamline

10 | P a g e

requirement of internal and external reporting, business operation process and

respective control with IT application. To ensure transitional impact, the company will

adopt retrospective option with proper treatment to retained earnings on 1st July,

2019, without any restatement of comparative information. The treatment of lease

with proper segregation will be made with case-to-case analysis of leases. The

company is still assessing the substantial effect of these practical measures. (Telstra,

2018)

Screenshot of Telstra disclosure in 2018 Annual report regarding AASB 117 and

AASB16

Conclusion

This article discussed about the changeover of lease accounting in Australia through

replacement of AASB 117 by AASB 16. Different aspects of this change is discussed

in this article with the drawbacks of old standard, the necessity of changes, the

benefits of old standard for the business owners, features of strict regulation in new

standard with other aspects of the new standard and example of company annual

report to notice the disclosures related to both the standards and the transition effect.

It is evident that the old standard had certain loopholes, which are being covered in

the new standard. The new standard will educate the business owners to streamline

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

their lease accounting for fair and prudent presentation of financial reports for the

stakeholders.

11 | P a g e

stakeholders.

11 | P a g e

References:

AASB, 2015. AASB 117- Leases. [Online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_08-15.pdf [Accessed 16 May 2019].

Advantage, 2013. Advantage of an Operating Lease. [Online] Available at:

https://www.advantageplusfinancing.com/advantage-of-operating-lease/ [Accessed 17 May 2019].

Azih, G., 2018. IFRS 16 Transition Summary and Two Full Examples for Lessees. [Online] Available at:

https://leasequery.com/blog/ifrs-16-transition-overview-and-examples-for-lessees/ [Accessed 17 May

2019].

BDO, 2018. IFRS IN PRACTICE – IFRS 16 LEASES. [Online] Available at:

https://www.bdo.global/getattachment/Services/Audit-Assurance/IFRS/IFRS-in-Practice/IFRS16-

Leases_print.pdf.aspx?lang=en-GB [Accessed 17 May 2019].

BDOAustralia, nd. New leases standard requires virtually all leases to be capitalised on the balance sheet.

[Online] Available at: https://www.bdo.com.au/en-au/accounting-news/accounting-news-february-

2016/new-leases-standard [Accessed 17 May 2019].

CPAAustralia, 2019. IFRS 16 Leases- fact Sheet. Fact Sheet. CPA Auatralia.

Deloitte, 2018. New IFRS 16 Leases standard - The impact on business valuation. Analytic. Deloitte.

Demski, J.S., 1988. Positive accounting theory: A review. Science Direct, 13(6), pp.623-29.

Finder, 2019. Guide to operating leases. [Online] Available at: https://www.finder.com.au/operating-

leases [Accessed 16 May 2019].

Fonteyn, S., 2017. The business impact of a new global accounting standard on commercial leases in

Australia. [Online] Available at: https://qsrmedia.com.au/./business-impact-new-global-accounting-

standard-commerc. [Accessed 17 May 2019].

Gummery, M., 2019. AASB 16 Leases-An Overview. [Online] Available at:

https://www.hlb.com.au/lessee-accounting-hlb-mann-judd/ [Accessed 16 May 2019].

Koo, J. & KordaMentha, 2016. Australia: Big changes to accounting for leases from 2019. [Online]

Available at:

http://www.mondaq.com/australia/x/509446/Forensic+Accounting/Big+changes+to+accounting+for+le

ases+from+2019 [Accessed 17 May 2019].

LLP, D., 2018. Leases - A guide to IFRS 16. Accounting guidelines. London: Deloitte.

McKinney, R., Hardidge, D. & Subramanian, R., 2018. The bottom line on leasing under IFRS 16. [Online]

Available at: https://www.intheblack.com/articles/2018/03/01/leasing-under-ifrs16 [Accessed 17 May

2019].

12 | P a g e

AASB, 2015. AASB 117- Leases. [Online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB117_08-15.pdf [Accessed 16 May 2019].

Advantage, 2013. Advantage of an Operating Lease. [Online] Available at:

https://www.advantageplusfinancing.com/advantage-of-operating-lease/ [Accessed 17 May 2019].

Azih, G., 2018. IFRS 16 Transition Summary and Two Full Examples for Lessees. [Online] Available at:

https://leasequery.com/blog/ifrs-16-transition-overview-and-examples-for-lessees/ [Accessed 17 May

2019].

BDO, 2018. IFRS IN PRACTICE – IFRS 16 LEASES. [Online] Available at:

https://www.bdo.global/getattachment/Services/Audit-Assurance/IFRS/IFRS-in-Practice/IFRS16-

Leases_print.pdf.aspx?lang=en-GB [Accessed 17 May 2019].

BDOAustralia, nd. New leases standard requires virtually all leases to be capitalised on the balance sheet.

[Online] Available at: https://www.bdo.com.au/en-au/accounting-news/accounting-news-february-

2016/new-leases-standard [Accessed 17 May 2019].

CPAAustralia, 2019. IFRS 16 Leases- fact Sheet. Fact Sheet. CPA Auatralia.

Deloitte, 2018. New IFRS 16 Leases standard - The impact on business valuation. Analytic. Deloitte.

Demski, J.S., 1988. Positive accounting theory: A review. Science Direct, 13(6), pp.623-29.

Finder, 2019. Guide to operating leases. [Online] Available at: https://www.finder.com.au/operating-

leases [Accessed 16 May 2019].

Fonteyn, S., 2017. The business impact of a new global accounting standard on commercial leases in

Australia. [Online] Available at: https://qsrmedia.com.au/./business-impact-new-global-accounting-

standard-commerc. [Accessed 17 May 2019].

Gummery, M., 2019. AASB 16 Leases-An Overview. [Online] Available at:

https://www.hlb.com.au/lessee-accounting-hlb-mann-judd/ [Accessed 16 May 2019].

Koo, J. & KordaMentha, 2016. Australia: Big changes to accounting for leases from 2019. [Online]

Available at:

http://www.mondaq.com/australia/x/509446/Forensic+Accounting/Big+changes+to+accounting+for+le

ases+from+2019 [Accessed 17 May 2019].

LLP, D., 2018. Leases - A guide to IFRS 16. Accounting guidelines. London: Deloitte.

McKinney, R., Hardidge, D. & Subramanian, R., 2018. The bottom line on leasing under IFRS 16. [Online]

Available at: https://www.intheblack.com/articles/2018/03/01/leasing-under-ifrs16 [Accessed 17 May

2019].

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.