Accounting Theory and Current Issues

VerifiedAdded on 2023/01/11

|8

|1792

|38

AI Summary

This study material explores various examples where information in financial statements is relevant but not faithfully represented, examples where information is not relevant but faithfully represented, and examples where information is both relevant and faithfully represented. It also discusses the relationship between social contract and organizational legitimacy, and how organizations can use corporate disclosure policy to maintain or regain organizational legitimacy. Additionally, it includes journal entries and calculations related to impairment of goodwill and interest rate implicit in a lease.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting theory and

current issue

current issue

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Table of Contents.............................................................................................................................2

WEEK 1...........................................................................................................................................1

a. Example where information is relevant but not faithfully represented....................................1

b. Example where information is not relevant but faithfully represented...................................1

c. Example where information is relevant and faithfully represented.........................................1

WEEK 2...........................................................................................................................................2

a. Social contract and the way in which it relates to organisational legitimacy..........................2

b. Two ways in which organisations can use corporate disclosure policy to maintain or regain

organisational legitimacy.............................................................................................................2

WEEK 3...........................................................................................................................................3

Journal entries..............................................................................................................................3

WEEK 4...........................................................................................................................................4

a. Journals entries.........................................................................................................................4

b. Determination of impairment of goodwill amount..................................................................4

WEEK 5...........................................................................................................................................5

a. Prove that the interest rate implicit in the lease is 10%...........................................................5

b. Entries in the books of Fisher Ltd............................................................................................5

c. Entries in the books of XFinance Ltd......................................................................................5

REFERENCES................................................................................................................................6

Table of Contents.............................................................................................................................2

WEEK 1...........................................................................................................................................1

a. Example where information is relevant but not faithfully represented....................................1

b. Example where information is not relevant but faithfully represented...................................1

c. Example where information is relevant and faithfully represented.........................................1

WEEK 2...........................................................................................................................................2

a. Social contract and the way in which it relates to organisational legitimacy..........................2

b. Two ways in which organisations can use corporate disclosure policy to maintain or regain

organisational legitimacy.............................................................................................................2

WEEK 3...........................................................................................................................................3

Journal entries..............................................................................................................................3

WEEK 4...........................................................................................................................................4

a. Journals entries.........................................................................................................................4

b. Determination of impairment of goodwill amount..................................................................4

WEEK 5...........................................................................................................................................5

a. Prove that the interest rate implicit in the lease is 10%...........................................................5

b. Entries in the books of Fisher Ltd............................................................................................5

c. Entries in the books of XFinance Ltd......................................................................................5

REFERENCES................................................................................................................................6

WEEK 1

a. Example where information is relevant but not faithfully represented

In financial statements the information which is recorded by accounting professionals of an

entity is relevant as they record it in the right account. The details that are mentioned in final

accounts such as trading, profit and loss account, balance sheet and cash flow statement could be

unfaithful because sometimes the information is changed by them to present a good image in the

market or reduce the tax liability (Baker, 2017). All these final accounts are used to represent

actual position of business and if a company is not able to generate good profits then it may bias

the data which is recorded in them. Mistakes in the statements may also take place unknowingly.

For example, if the accounting professional forgets to record any transaction in journal then it

will also result in unfaithful information because the details will not be accurate and complete.

b. Example where information is not relevant but faithfully represented

All the internal reports which are generated by the management are used by managers for

the purpose of recording detailed and faithful information in the books. It can help to analyse the

appropriate information so that strategic decisions for future could be formulated. If these reports

are not formulated then it may create issues for the management to analyse the business

performance and reach to a decision of improving it appropriately. There are various

management reports which are inventory management, cost accounting, performance, budget etc.

All of them have faithful information which is used by companies to make sure that effective

strategies for future are formulated so that business could be developed (Deb, 2019).

c. Example where information is relevant and faithfully represented

Auditor’s report is the place where all the information recorded is relevant and faithful. The

main responsibility of an auditor is to analyse the final accounts and figure out the mistakes in it

so that an accurate report could be delivered to the stakeholders. All the final accounts such as

income statement, balance sheet and cash flow are evaluated by an auditor and then a report is

generated on the basis of it which is highly accurate and faithful (Schroeder, Clark and Cathey,

2019). With the help of it all the stakeholders such as investors, creditors, suppliers, customers,

government etc. can determine the actual position of business and make further decisions. All of

them the report of auditors used to analyse that the company in which they are planning to invest

or already invested will be able to provide them good returns in future or not.

1

a. Example where information is relevant but not faithfully represented

In financial statements the information which is recorded by accounting professionals of an

entity is relevant as they record it in the right account. The details that are mentioned in final

accounts such as trading, profit and loss account, balance sheet and cash flow statement could be

unfaithful because sometimes the information is changed by them to present a good image in the

market or reduce the tax liability (Baker, 2017). All these final accounts are used to represent

actual position of business and if a company is not able to generate good profits then it may bias

the data which is recorded in them. Mistakes in the statements may also take place unknowingly.

For example, if the accounting professional forgets to record any transaction in journal then it

will also result in unfaithful information because the details will not be accurate and complete.

b. Example where information is not relevant but faithfully represented

All the internal reports which are generated by the management are used by managers for

the purpose of recording detailed and faithful information in the books. It can help to analyse the

appropriate information so that strategic decisions for future could be formulated. If these reports

are not formulated then it may create issues for the management to analyse the business

performance and reach to a decision of improving it appropriately. There are various

management reports which are inventory management, cost accounting, performance, budget etc.

All of them have faithful information which is used by companies to make sure that effective

strategies for future are formulated so that business could be developed (Deb, 2019).

c. Example where information is relevant and faithfully represented

Auditor’s report is the place where all the information recorded is relevant and faithful. The

main responsibility of an auditor is to analyse the final accounts and figure out the mistakes in it

so that an accurate report could be delivered to the stakeholders. All the final accounts such as

income statement, balance sheet and cash flow are evaluated by an auditor and then a report is

generated on the basis of it which is highly accurate and faithful (Schroeder, Clark and Cathey,

2019). With the help of it all the stakeholders such as investors, creditors, suppliers, customers,

government etc. can determine the actual position of business and make further decisions. All of

them the report of auditors used to analyse that the company in which they are planning to invest

or already invested will be able to provide them good returns in future or not.

1

WEEK 2

a. Social contract and the way in which it relates to organisational legitimacy

Social contract can be defined as a type of agreement which is formulated by the members

on a society so that they can contribute or the development of it. Main purpose of it is to make

sure that appropriate benefits to the society are provided so that the individuals who are living in

it can live freely. Organisational legitimacy can be defined as the initiative of a company to

establish social values and perform such activities that are focused with societal development.

Main purpose of it is to assure the societies that the entity is operating its business by following

the values that are formulated by community. With the help of it, growth of economy could be

focused.

Social contracts and organisational legitimacy are related with each other because while

focusing upon development of society the organisations can use social contracts. With the help

of it, the business entities can sign an agreement with other parties that it will be working for

welfare of community in upcoming period. While planning to take part in societal development

activities social contract is one of the key elements which should be focused by companies as it

can help to accomplish all the future goals and objectives (Sharma, 2019).

b. Two ways in which organisations can use corporate disclosure policy to maintain or regain

organisational legitimacy

Corporate disclosure policy can be defined as an approach which is highly focused with

material information and the circumstances due to which the level of confidentiality of data

could be affected. There are various ways in which organisations can use it to maintain or regain

organisational legitimacy. Some of them which could be focused by an organisation are as

follows:

Corporate disclosure policy could be used by companies to make sure that the

information which is used by them to formulate final accounts are appropriate or not. It

could be used by companies to maintain the organisational legitimacy by making sure

that the details that are recorded in accounts are appropriate or not. It can help to

formulate specific decisions for future so that the business can attain growth and reach

the goals such as societal development (Zeff, 2018).

2

a. Social contract and the way in which it relates to organisational legitimacy

Social contract can be defined as a type of agreement which is formulated by the members

on a society so that they can contribute or the development of it. Main purpose of it is to make

sure that appropriate benefits to the society are provided so that the individuals who are living in

it can live freely. Organisational legitimacy can be defined as the initiative of a company to

establish social values and perform such activities that are focused with societal development.

Main purpose of it is to assure the societies that the entity is operating its business by following

the values that are formulated by community. With the help of it, growth of economy could be

focused.

Social contracts and organisational legitimacy are related with each other because while

focusing upon development of society the organisations can use social contracts. With the help

of it, the business entities can sign an agreement with other parties that it will be working for

welfare of community in upcoming period. While planning to take part in societal development

activities social contract is one of the key elements which should be focused by companies as it

can help to accomplish all the future goals and objectives (Sharma, 2019).

b. Two ways in which organisations can use corporate disclosure policy to maintain or regain

organisational legitimacy

Corporate disclosure policy can be defined as an approach which is highly focused with

material information and the circumstances due to which the level of confidentiality of data

could be affected. There are various ways in which organisations can use it to maintain or regain

organisational legitimacy. Some of them which could be focused by an organisation are as

follows:

Corporate disclosure policy could be used by companies to make sure that the

information which is used by them to formulate final accounts are appropriate or not. It

could be used by companies to maintain the organisational legitimacy by making sure

that the details that are recorded in accounts are appropriate or not. It can help to

formulate specific decisions for future so that the business can attain growth and reach

the goals such as societal development (Zeff, 2018).

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Corporate disclosure policy is focused with prevention of abuse of undisclosed material

information and monitoring of the market rumours. While planning to maintain or regain

organisational legitimacy it could be focused. By using the policy the companies will be

able to ignore abuse of material information which will help to establish a positive market

image and work for development of society.

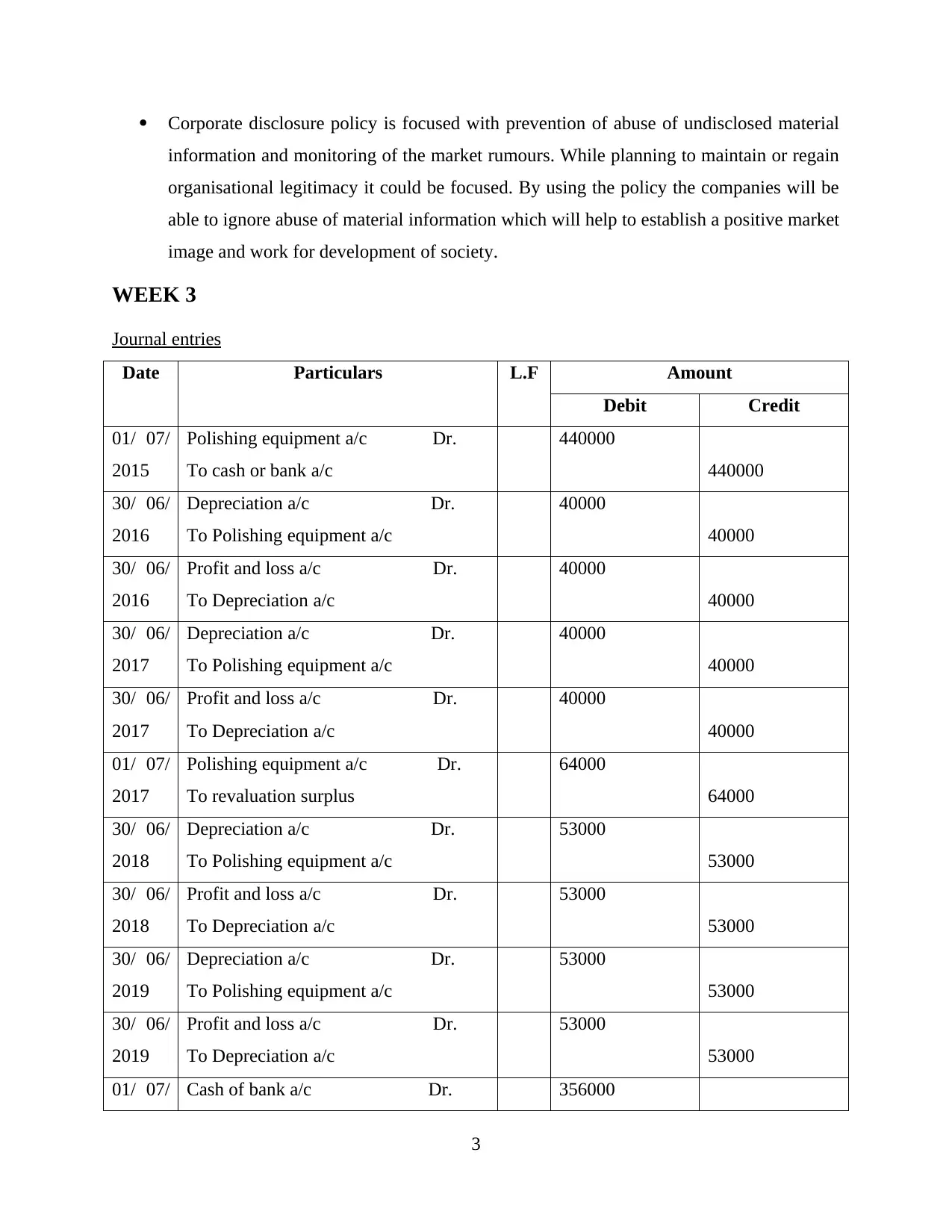

WEEK 3

Journal entries

Date Particulars L.F Amount

Debit Credit

01/ 07/

2015

Polishing equipment a/c Dr.

To cash or bank a/c

440000

440000

30/ 06/

2016

Depreciation a/c Dr.

To Polishing equipment a/c

40000

40000

30/ 06/

2016

Profit and loss a/c Dr.

To Depreciation a/c

40000

40000

30/ 06/

2017

Depreciation a/c Dr.

To Polishing equipment a/c

40000

40000

30/ 06/

2017

Profit and loss a/c Dr.

To Depreciation a/c

40000

40000

01/ 07/

2017

Polishing equipment a/c Dr.

To revaluation surplus

64000

64000

30/ 06/

2018

Depreciation a/c Dr.

To Polishing equipment a/c

53000

53000

30/ 06/

2018

Profit and loss a/c Dr.

To Depreciation a/c

53000

53000

30/ 06/

2019

Depreciation a/c Dr.

To Polishing equipment a/c

53000

53000

30/ 06/

2019

Profit and loss a/c Dr.

To Depreciation a/c

53000

53000

01/ 07/ Cash of bank a/c Dr. 356000

3

information and monitoring of the market rumours. While planning to maintain or regain

organisational legitimacy it could be focused. By using the policy the companies will be

able to ignore abuse of material information which will help to establish a positive market

image and work for development of society.

WEEK 3

Journal entries

Date Particulars L.F Amount

Debit Credit

01/ 07/

2015

Polishing equipment a/c Dr.

To cash or bank a/c

440000

440000

30/ 06/

2016

Depreciation a/c Dr.

To Polishing equipment a/c

40000

40000

30/ 06/

2016

Profit and loss a/c Dr.

To Depreciation a/c

40000

40000

30/ 06/

2017

Depreciation a/c Dr.

To Polishing equipment a/c

40000

40000

30/ 06/

2017

Profit and loss a/c Dr.

To Depreciation a/c

40000

40000

01/ 07/

2017

Polishing equipment a/c Dr.

To revaluation surplus

64000

64000

30/ 06/

2018

Depreciation a/c Dr.

To Polishing equipment a/c

53000

53000

30/ 06/

2018

Profit and loss a/c Dr.

To Depreciation a/c

53000

53000

30/ 06/

2019

Depreciation a/c Dr.

To Polishing equipment a/c

53000

53000

30/ 06/

2019

Profit and loss a/c Dr.

To Depreciation a/c

53000

53000

01/ 07/ Cash of bank a/c Dr. 356000

3

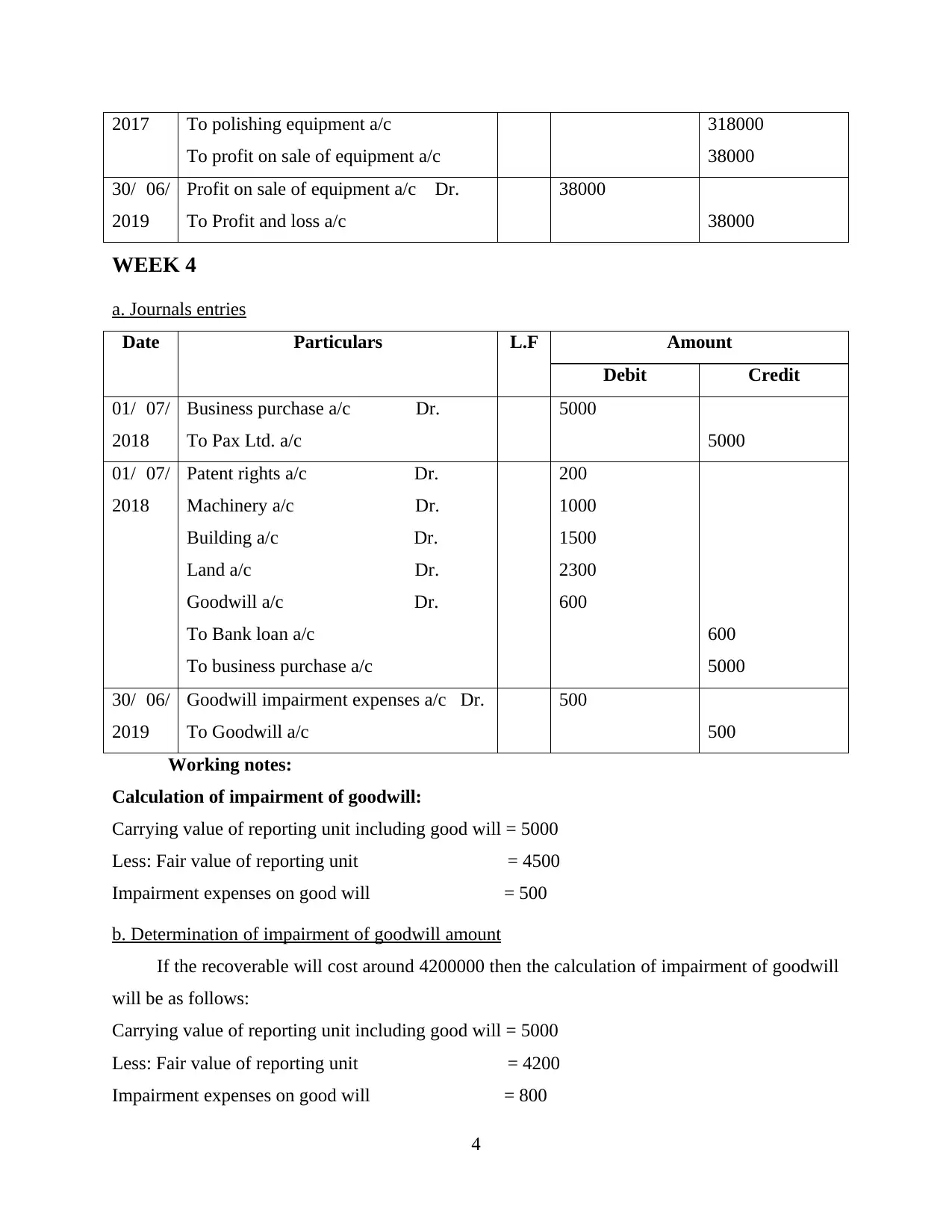

2017 To polishing equipment a/c

To profit on sale of equipment a/c

318000

38000

30/ 06/

2019

Profit on sale of equipment a/c Dr.

To Profit and loss a/c

38000

38000

WEEK 4

a. Journals entries

Date Particulars L.F Amount

Debit Credit

01/ 07/

2018

Business purchase a/c Dr.

To Pax Ltd. a/c

5000

5000

01/ 07/

2018

Patent rights a/c Dr.

Machinery a/c Dr.

Building a/c Dr.

Land a/c Dr.

Goodwill a/c Dr.

To Bank loan a/c

To business purchase a/c

200

1000

1500

2300

600

600

5000

30/ 06/

2019

Goodwill impairment expenses a/c Dr.

To Goodwill a/c

500

500

Working notes:

Calculation of impairment of goodwill:

Carrying value of reporting unit including good will = 5000

Less: Fair value of reporting unit = 4500

Impairment expenses on good will = 500

b. Determination of impairment of goodwill amount

If the recoverable will cost around 4200000 then the calculation of impairment of goodwill

will be as follows:

Carrying value of reporting unit including good will = 5000

Less: Fair value of reporting unit = 4200

Impairment expenses on good will = 800

4

To profit on sale of equipment a/c

318000

38000

30/ 06/

2019

Profit on sale of equipment a/c Dr.

To Profit and loss a/c

38000

38000

WEEK 4

a. Journals entries

Date Particulars L.F Amount

Debit Credit

01/ 07/

2018

Business purchase a/c Dr.

To Pax Ltd. a/c

5000

5000

01/ 07/

2018

Patent rights a/c Dr.

Machinery a/c Dr.

Building a/c Dr.

Land a/c Dr.

Goodwill a/c Dr.

To Bank loan a/c

To business purchase a/c

200

1000

1500

2300

600

600

5000

30/ 06/

2019

Goodwill impairment expenses a/c Dr.

To Goodwill a/c

500

500

Working notes:

Calculation of impairment of goodwill:

Carrying value of reporting unit including good will = 5000

Less: Fair value of reporting unit = 4500

Impairment expenses on good will = 500

b. Determination of impairment of goodwill amount

If the recoverable will cost around 4200000 then the calculation of impairment of goodwill

will be as follows:

Carrying value of reporting unit including good will = 5000

Less: Fair value of reporting unit = 4200

Impairment expenses on good will = 800

4

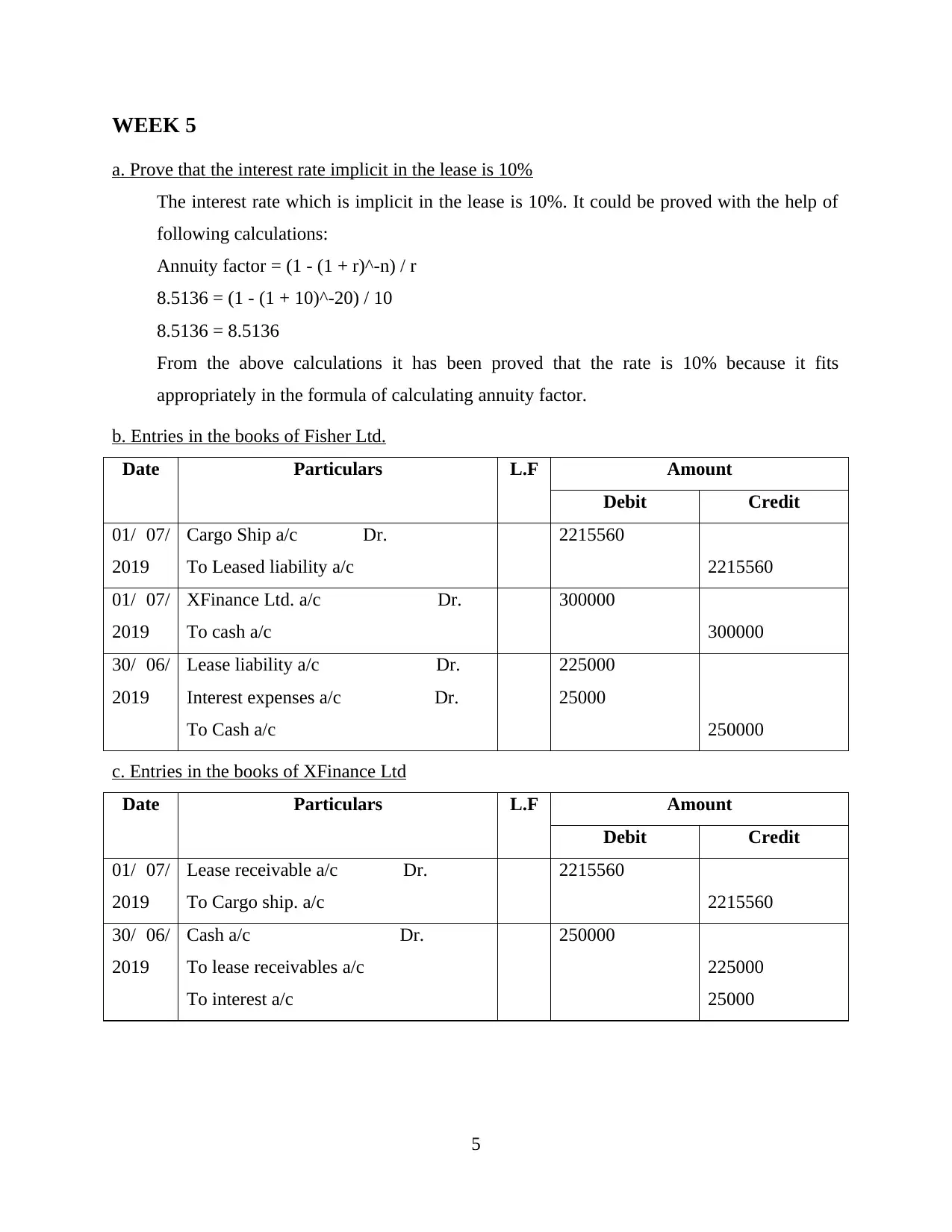

WEEK 5

a. Prove that the interest rate implicit in the lease is 10%

The interest rate which is implicit in the lease is 10%. It could be proved with the help of

following calculations:

Annuity factor = (1 - (1 + r)^-n) / r

8.5136 = (1 - (1 + 10)^-20) / 10

8.5136 = 8.5136

From the above calculations it has been proved that the rate is 10% because it fits

appropriately in the formula of calculating annuity factor.

b. Entries in the books of Fisher Ltd.

Date Particulars L.F Amount

Debit Credit

01/ 07/

2019

Cargo Ship a/c Dr.

To Leased liability a/c

2215560

2215560

01/ 07/

2019

XFinance Ltd. a/c Dr.

To cash a/c

300000

300000

30/ 06/

2019

Lease liability a/c Dr.

Interest expenses a/c Dr.

To Cash a/c

225000

25000

250000

c. Entries in the books of XFinance Ltd

Date Particulars L.F Amount

Debit Credit

01/ 07/

2019

Lease receivable a/c Dr.

To Cargo ship. a/c

2215560

2215560

30/ 06/

2019

Cash a/c Dr.

To lease receivables a/c

To interest a/c

250000

225000

25000

5

a. Prove that the interest rate implicit in the lease is 10%

The interest rate which is implicit in the lease is 10%. It could be proved with the help of

following calculations:

Annuity factor = (1 - (1 + r)^-n) / r

8.5136 = (1 - (1 + 10)^-20) / 10

8.5136 = 8.5136

From the above calculations it has been proved that the rate is 10% because it fits

appropriately in the formula of calculating annuity factor.

b. Entries in the books of Fisher Ltd.

Date Particulars L.F Amount

Debit Credit

01/ 07/

2019

Cargo Ship a/c Dr.

To Leased liability a/c

2215560

2215560

01/ 07/

2019

XFinance Ltd. a/c Dr.

To cash a/c

300000

300000

30/ 06/

2019

Lease liability a/c Dr.

Interest expenses a/c Dr.

To Cash a/c

225000

25000

250000

c. Entries in the books of XFinance Ltd

Date Particulars L.F Amount

Debit Credit

01/ 07/

2019

Lease receivable a/c Dr.

To Cargo ship. a/c

2215560

2215560

30/ 06/

2019

Cash a/c Dr.

To lease receivables a/c

To interest a/c

250000

225000

25000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Baker, C. R., 2017. The influence of accounting theory on the FASB conceptual

framework. Accounting Historians Journal. 44(2). pp.109-124.

Deb, R., 2019. Accounting Theory Coherence Revisited. Management and Labour Studies.

44(1). pp.36-57.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Sharma, U., 2019. Giving contingency theory of management accounting and control a critical

edge. International Journal of Critical Accounting. 11(1). pp.16-25.

Zeff, S. A., 2018. My accounting theory seminar. Accounting Historians Journal. 45(1). pp.135-

140.

6

Books and Journals:

Baker, C. R., 2017. The influence of accounting theory on the FASB conceptual

framework. Accounting Historians Journal. 44(2). pp.109-124.

Deb, R., 2019. Accounting Theory Coherence Revisited. Management and Labour Studies.

44(1). pp.36-57.

Schroeder, R. G., Clark, M. W. and Cathey, J. M., 2019. Financial accounting theory and

analysis: text and cases. John Wiley & Sons.

Sharma, U., 2019. Giving contingency theory of management accounting and control a critical

edge. International Journal of Critical Accounting. 11(1). pp.16-25.

Zeff, S. A., 2018. My accounting theory seminar. Accounting Historians Journal. 45(1). pp.135-

140.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.