Accounting Theory and Current Issue

VerifiedAdded on 2023/01/10

|11

|2016

|70

AI Summary

This document provides study material on accounting theory and current issues. It includes topics such as long service leave benefits, journal entries, employee benefits, gross profit computation, EPS calculation, and more. The content covers various weeks and provides detailed explanations and calculations. It is relevant for accounting students studying accounting theory and current issues.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCOUNTING THEORY AND

CURRENT ISSUE

CURRENT ISSUE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

WEEK 6...........................................................................................................................................3

a) .................................................................................................................................................3

b) .................................................................................................................................................3

c)..................................................................................................................................................4

d)..................................................................................................................................................4

WEEK 7...........................................................................................................................................4

a) .................................................................................................................................................4

b) ................................................................................................................................................5

c)..................................................................................................................................................5

WEEK 8...........................................................................................................................................6

a)..................................................................................................................................................6

WEEK 9...........................................................................................................................................7

a) .................................................................................................................................................7

b)..................................................................................................................................................8

WEEK 10.........................................................................................................................................9

a)..................................................................................................................................................9

b)..................................................................................................................................................9

REFERENCES..............................................................................................................................11

WEEK 6...........................................................................................................................................3

a) .................................................................................................................................................3

b) .................................................................................................................................................3

c)..................................................................................................................................................4

d)..................................................................................................................................................4

WEEK 7...........................................................................................................................................4

a) .................................................................................................................................................4

b) ................................................................................................................................................5

c)..................................................................................................................................................5

WEEK 8...........................................................................................................................................6

a)..................................................................................................................................................6

WEEK 9...........................................................................................................................................7

a) .................................................................................................................................................7

b)..................................................................................................................................................8

WEEK 10.........................................................................................................................................9

a)..................................................................................................................................................9

b)..................................................................................................................................................9

REFERENCES..............................................................................................................................11

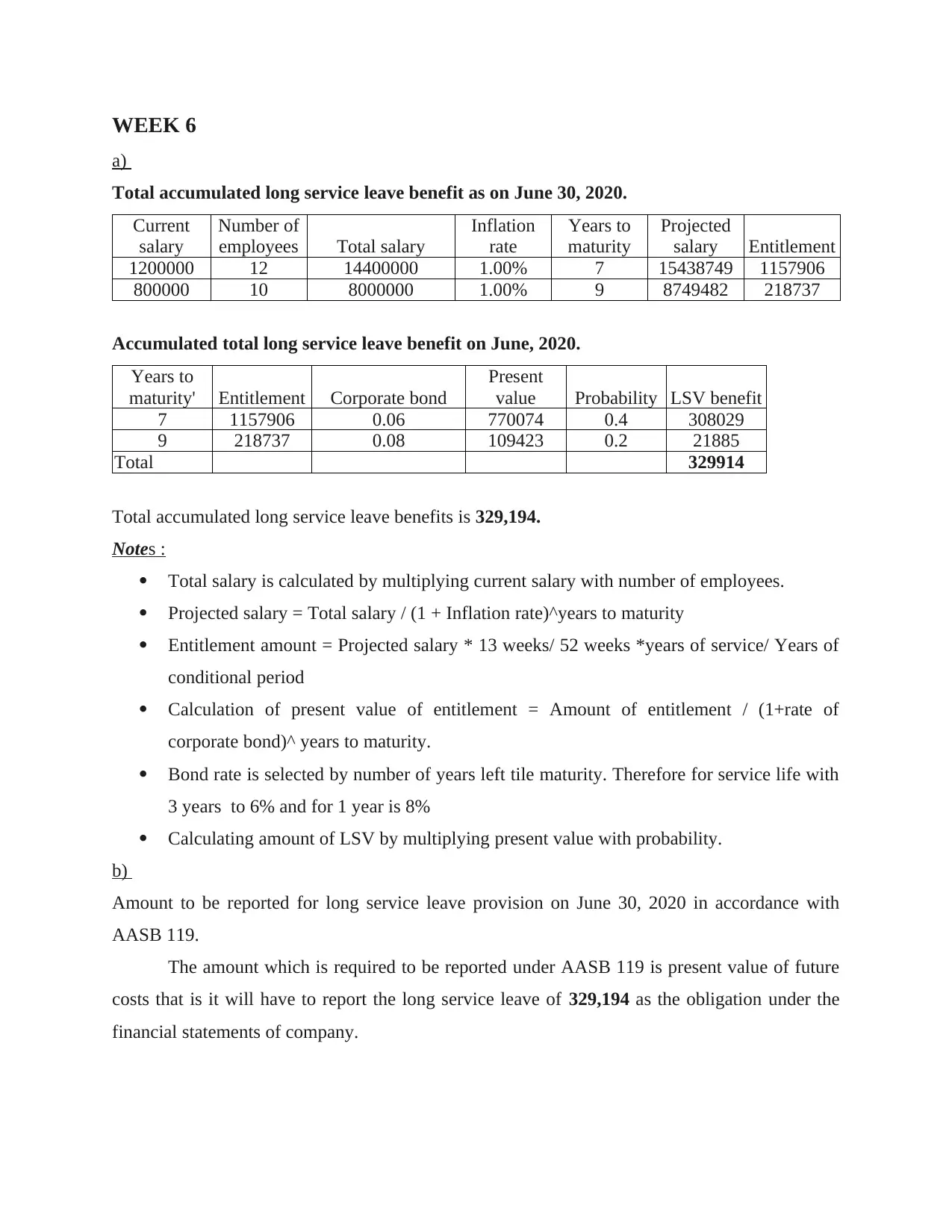

WEEK 6

a)

Total accumulated long service leave benefit as on June 30, 2020.

Current

salary

Number of

employees Total salary

Inflation

rate

Years to

maturity

Projected

salary Entitlement

1200000 12 14400000 1.00% 7 15438749 1157906

800000 10 8000000 1.00% 9 8749482 218737

Accumulated total long service leave benefit on June, 2020.

Years to

maturity' Entitlement Corporate bond

Present

value Probability LSV benefit

7 1157906 0.06 770074 0.4 308029

9 218737 0.08 109423 0.2 21885

Total 329914

Total accumulated long service leave benefits is 329,194.

Notes :

Total salary is calculated by multiplying current salary with number of employees.

Projected salary = Total salary / (1 + Inflation rate)^years to maturity

Entitlement amount = Projected salary * 13 weeks/ 52 weeks *years of service/ Years of

conditional period

Calculation of present value of entitlement = Amount of entitlement / (1+rate of

corporate bond)^ years to maturity.

Bond rate is selected by number of years left tile maturity. Therefore for service life with

3 years to 6% and for 1 year is 8%

Calculating amount of LSV by multiplying present value with probability.

b)

Amount to be reported for long service leave provision on June 30, 2020 in accordance with

AASB 119.

The amount which is required to be reported under AASB 119 is present value of future

costs that is it will have to report the long service leave of 329,194 as the obligation under the

financial statements of company.

a)

Total accumulated long service leave benefit as on June 30, 2020.

Current

salary

Number of

employees Total salary

Inflation

rate

Years to

maturity

Projected

salary Entitlement

1200000 12 14400000 1.00% 7 15438749 1157906

800000 10 8000000 1.00% 9 8749482 218737

Accumulated total long service leave benefit on June, 2020.

Years to

maturity' Entitlement Corporate bond

Present

value Probability LSV benefit

7 1157906 0.06 770074 0.4 308029

9 218737 0.08 109423 0.2 21885

Total 329914

Total accumulated long service leave benefits is 329,194.

Notes :

Total salary is calculated by multiplying current salary with number of employees.

Projected salary = Total salary / (1 + Inflation rate)^years to maturity

Entitlement amount = Projected salary * 13 weeks/ 52 weeks *years of service/ Years of

conditional period

Calculation of present value of entitlement = Amount of entitlement / (1+rate of

corporate bond)^ years to maturity.

Bond rate is selected by number of years left tile maturity. Therefore for service life with

3 years to 6% and for 1 year is 8%

Calculating amount of LSV by multiplying present value with probability.

b)

Amount to be reported for long service leave provision on June 30, 2020 in accordance with

AASB 119.

The amount which is required to be reported under AASB 119 is present value of future

costs that is it will have to report the long service leave of 329,194 as the obligation under the

financial statements of company.

c)

Journal entry

As company had opening provision of 12000 for same it will be making provision of 317,194

for year.

Journal entry for the provision

Long Service leave expense 317194

To Provision for long service leave 317194

d)

Employee benefits that are required to be discounted as per AASB 119

AASB 119 of employee benefits requires rate to be used of not for pro t entities of private

sector and for pro t entities of private sector for discounting the long term benefits of employees.

It is determined with reference to the market yield at end of period over corporate bonds. AASB

119 where deep market is not there it requires market yield on the government bonds should be

used for discounted the liabilities (AASB 119, 2019). As per the standard companies are required

to measure the obligation of future employee benefits on the current period. It is essential for the

company to record the future values by bringing them at present scale using the discount rate of

the corporate bonds applicable.

WEEK 7

a)

Computation of gross profit to be recognised every year when outcome could be reliably

estimated

Year Particulars Amount

2019 2000000*31.25% 625000

2020 2000000*81.25% 1625000

- Profit already recorded -625000

Profit for the year 1000000

2021 2000000*100% 2000000

- Profit already recorded -1625000

Profit for the year 375000

Calculation of % of completion

2019 2020 2021

Billings & collection 2000000 5000000 3000000

Journal entry

As company had opening provision of 12000 for same it will be making provision of 317,194

for year.

Journal entry for the provision

Long Service leave expense 317194

To Provision for long service leave 317194

d)

Employee benefits that are required to be discounted as per AASB 119

AASB 119 of employee benefits requires rate to be used of not for pro t entities of private

sector and for pro t entities of private sector for discounting the long term benefits of employees.

It is determined with reference to the market yield at end of period over corporate bonds. AASB

119 where deep market is not there it requires market yield on the government bonds should be

used for discounted the liabilities (AASB 119, 2019). As per the standard companies are required

to measure the obligation of future employee benefits on the current period. It is essential for the

company to record the future values by bringing them at present scale using the discount rate of

the corporate bonds applicable.

WEEK 7

a)

Computation of gross profit to be recognised every year when outcome could be reliably

estimated

Year Particulars Amount

2019 2000000*31.25% 625000

2020 2000000*81.25% 1625000

- Profit already recorded -625000

Profit for the year 1000000

2021 2000000*100% 2000000

- Profit already recorded -1625000

Profit for the year 375000

Calculation of % of completion

2019 2020 2021

Billings & collection 2000000 5000000 3000000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

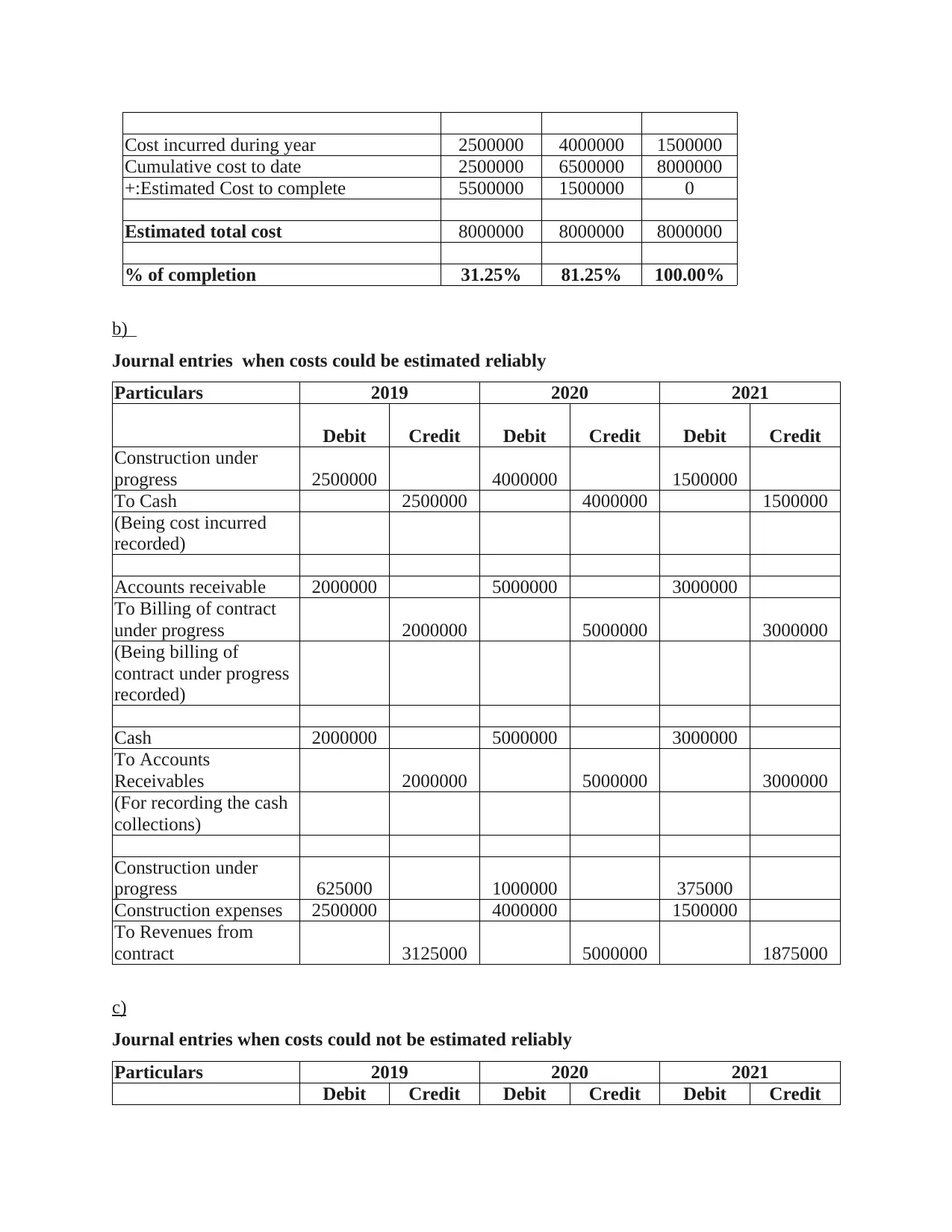

Cost incurred during year 2500000 4000000 1500000

Cumulative cost to date 2500000 6500000 8000000

+:Estimated Cost to complete 5500000 1500000 0

Estimated total cost 8000000 8000000 8000000

% of completion 31.25% 81.25% 100.00%

b)

Journal entries when costs could be estimated reliably

Particulars 2019 2020 2021

Debit Credit Debit Credit Debit Credit

Construction under

progress 2500000 4000000 1500000

To Cash 2500000 4000000 1500000

(Being cost incurred

recorded)

Accounts receivable 2000000 5000000 3000000

To Billing of contract

under progress 2000000 5000000 3000000

(Being billing of

contract under progress

recorded)

Cash 2000000 5000000 3000000

To Accounts

Receivables 2000000 5000000 3000000

(For recording the cash

collections)

Construction under

progress 625000 1000000 375000

Construction expenses 2500000 4000000 1500000

To Revenues from

contract 3125000 5000000 1875000

c)

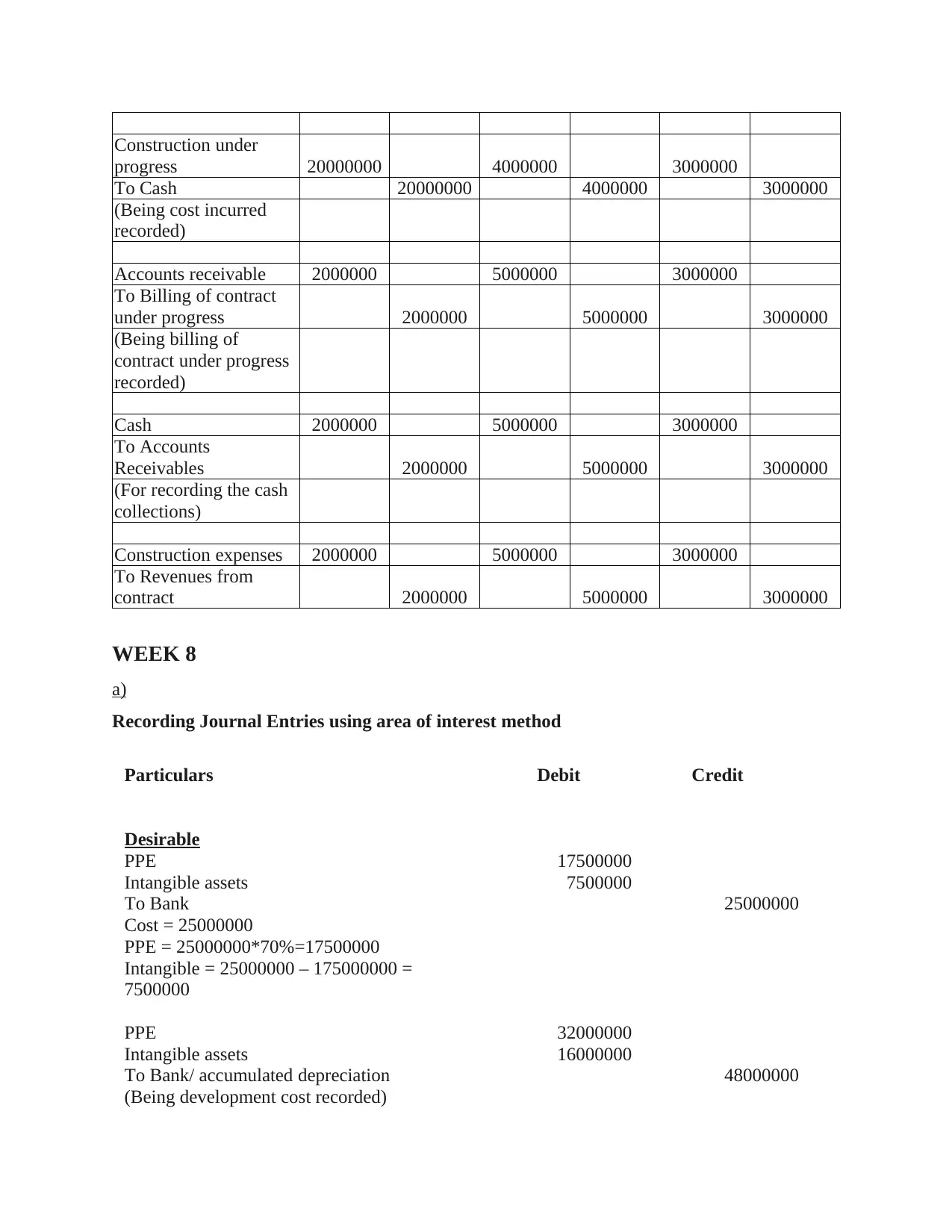

Journal entries when costs could not be estimated reliably

Particulars 2019 2020 2021

Debit Credit Debit Credit Debit Credit

Cumulative cost to date 2500000 6500000 8000000

+:Estimated Cost to complete 5500000 1500000 0

Estimated total cost 8000000 8000000 8000000

% of completion 31.25% 81.25% 100.00%

b)

Journal entries when costs could be estimated reliably

Particulars 2019 2020 2021

Debit Credit Debit Credit Debit Credit

Construction under

progress 2500000 4000000 1500000

To Cash 2500000 4000000 1500000

(Being cost incurred

recorded)

Accounts receivable 2000000 5000000 3000000

To Billing of contract

under progress 2000000 5000000 3000000

(Being billing of

contract under progress

recorded)

Cash 2000000 5000000 3000000

To Accounts

Receivables 2000000 5000000 3000000

(For recording the cash

collections)

Construction under

progress 625000 1000000 375000

Construction expenses 2500000 4000000 1500000

To Revenues from

contract 3125000 5000000 1875000

c)

Journal entries when costs could not be estimated reliably

Particulars 2019 2020 2021

Debit Credit Debit Credit Debit Credit

Construction under

progress 20000000 4000000 3000000

To Cash 20000000 4000000 3000000

(Being cost incurred

recorded)

Accounts receivable 2000000 5000000 3000000

To Billing of contract

under progress 2000000 5000000 3000000

(Being billing of

contract under progress

recorded)

Cash 2000000 5000000 3000000

To Accounts

Receivables 2000000 5000000 3000000

(For recording the cash

collections)

Construction expenses 2000000 5000000 3000000

To Revenues from

contract 2000000 5000000 3000000

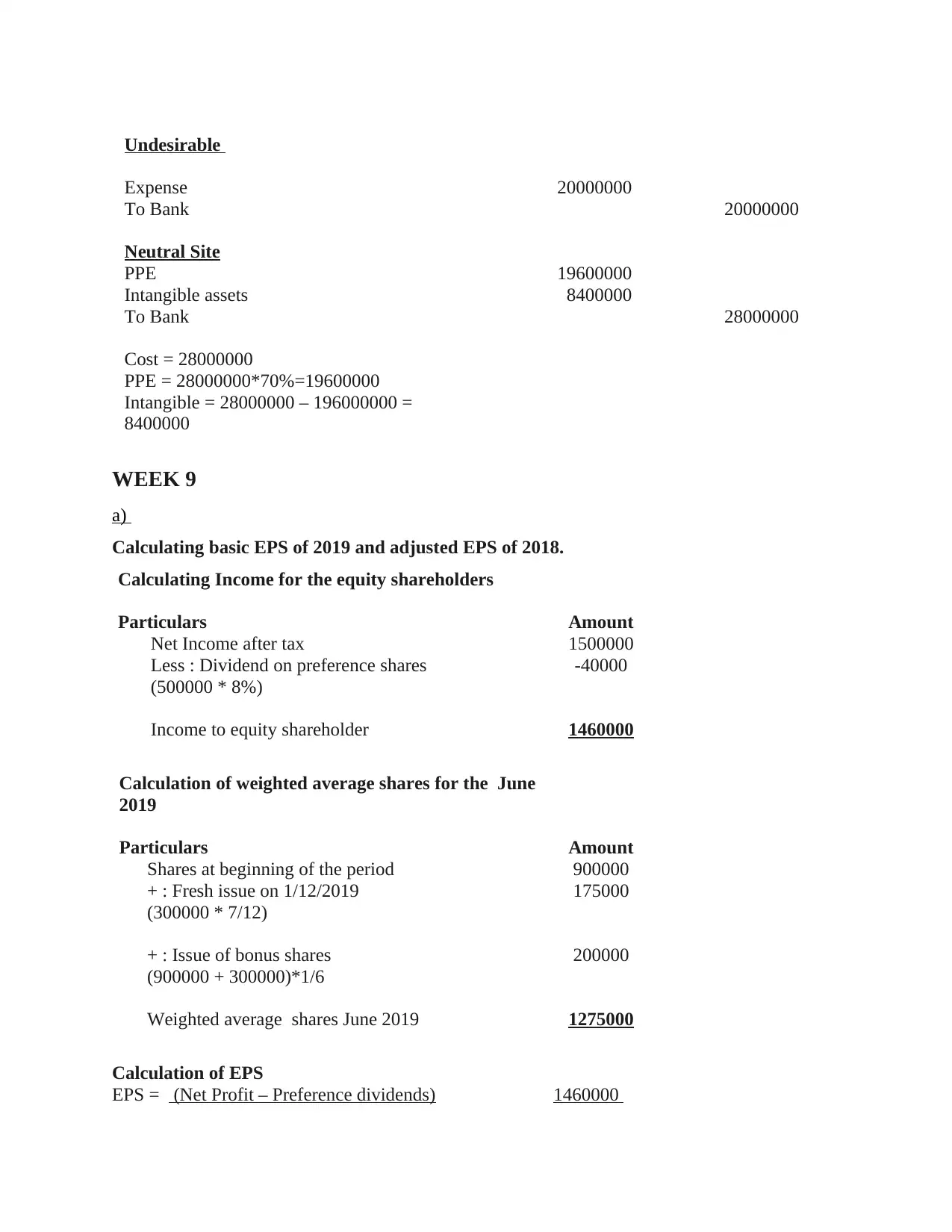

WEEK 8

a)

Recording Journal Entries using area of interest method

Particulars Debit Credit

Desirable

PPE 17500000

Intangible assets 7500000

To Bank 25000000

Cost = 25000000

PPE = 25000000*70%=17500000

Intangible = 25000000 – 175000000 =

7500000

PPE 32000000

Intangible assets 16000000

To Bank/ accumulated depreciation 48000000

(Being development cost recorded)

progress 20000000 4000000 3000000

To Cash 20000000 4000000 3000000

(Being cost incurred

recorded)

Accounts receivable 2000000 5000000 3000000

To Billing of contract

under progress 2000000 5000000 3000000

(Being billing of

contract under progress

recorded)

Cash 2000000 5000000 3000000

To Accounts

Receivables 2000000 5000000 3000000

(For recording the cash

collections)

Construction expenses 2000000 5000000 3000000

To Revenues from

contract 2000000 5000000 3000000

WEEK 8

a)

Recording Journal Entries using area of interest method

Particulars Debit Credit

Desirable

PPE 17500000

Intangible assets 7500000

To Bank 25000000

Cost = 25000000

PPE = 25000000*70%=17500000

Intangible = 25000000 – 175000000 =

7500000

PPE 32000000

Intangible assets 16000000

To Bank/ accumulated depreciation 48000000

(Being development cost recorded)

Undesirable

Expense 20000000

To Bank 20000000

Neutral Site

PPE 19600000

Intangible assets 8400000

To Bank 28000000

Cost = 28000000

PPE = 28000000*70%=19600000

Intangible = 28000000 – 196000000 =

8400000

WEEK 9

a)

Calculating basic EPS of 2019 and adjusted EPS of 2018.

Calculating Income for the equity shareholders

Particulars Amount

Net Income after tax 1500000

Less : Dividend on preference shares -40000

(500000 * 8%)

Income to equity shareholder 1460000

Calculation of weighted average shares for the June

2019

Particulars Amount

Shares at beginning of the period 900000

+ : Fresh issue on 1/12/2019 175000

(300000 * 7/12)

+ : Issue of bonus shares 200000

(900000 + 300000)*1/6

Weighted average shares June 2019 1275000

Calculation of EPS

EPS = (Net Profit – Preference dividends) 1460000

Expense 20000000

To Bank 20000000

Neutral Site

PPE 19600000

Intangible assets 8400000

To Bank 28000000

Cost = 28000000

PPE = 28000000*70%=19600000

Intangible = 28000000 – 196000000 =

8400000

WEEK 9

a)

Calculating basic EPS of 2019 and adjusted EPS of 2018.

Calculating Income for the equity shareholders

Particulars Amount

Net Income after tax 1500000

Less : Dividend on preference shares -40000

(500000 * 8%)

Income to equity shareholder 1460000

Calculation of weighted average shares for the June

2019

Particulars Amount

Shares at beginning of the period 900000

+ : Fresh issue on 1/12/2019 175000

(300000 * 7/12)

+ : Issue of bonus shares 200000

(900000 + 300000)*1/6

Weighted average shares June 2019 1275000

Calculation of EPS

EPS = (Net Profit – Preference dividends) 1460000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Average no. of shares outstanding ) 1275000

EPS = 1.145

Computation of Adjusted EPS for year 2018 of Alps ltd

Computing Adjusted EPS for 2018

Calculation of Earnings

Earnings = (EPS of 30/6/2018 * Fully paid up shares)

= 1.5 * 900000

1350000

Calculating weighted bonus shares

Bonus weighted shares

= (900000 + 900000 * 1/6)

= (900000 + 150000)

1050000

Calculation of adjusted EPS 2018

Adjusted EPS 2018

= (1350000 / 1050000)

1.286

b)

Diluted EPS

Diluted earnings per share are essentially earnings made over every share of public

company which is calculated on the assumptions that all securities which are convertible are duly

exercised. In place of taking existing stocks in consideration. In diluted earning per share it is

assumed that securities inclusive of convertible preference shares, convertible bonds, warrants,

stock options and other things that could be altered into stock which are actually altered. It is

important for the shareholders as it lays down earnings that shareholder would be getting in

worst scenarios. In a public listed company where there are different types of stocks in the

capital framework, they should provide information that pertains to both the diluted EPS and

basic EPS (Samaha, Khlif and Dahawy, 2016). Presentation of the information is for existing

operation and net income both and is provided on income statement of company.

Diluted EPS considers what will be happening if the diluted securities would have been

exercised. They are the securities which are not the common stocks but could be converted to the

EPS = 1.145

Computation of Adjusted EPS for year 2018 of Alps ltd

Computing Adjusted EPS for 2018

Calculation of Earnings

Earnings = (EPS of 30/6/2018 * Fully paid up shares)

= 1.5 * 900000

1350000

Calculating weighted bonus shares

Bonus weighted shares

= (900000 + 900000 * 1/6)

= (900000 + 150000)

1050000

Calculation of adjusted EPS 2018

Adjusted EPS 2018

= (1350000 / 1050000)

1.286

b)

Diluted EPS

Diluted earnings per share are essentially earnings made over every share of public

company which is calculated on the assumptions that all securities which are convertible are duly

exercised. In place of taking existing stocks in consideration. In diluted earning per share it is

assumed that securities inclusive of convertible preference shares, convertible bonds, warrants,

stock options and other things that could be altered into stock which are actually altered. It is

important for the shareholders as it lays down earnings that shareholder would be getting in

worst scenarios. In a public listed company where there are different types of stocks in the

capital framework, they should provide information that pertains to both the diluted EPS and

basic EPS (Samaha, Khlif and Dahawy, 2016). Presentation of the information is for existing

operation and net income both and is provided on income statement of company.

Diluted EPS considers what will be happening if the diluted securities would have been

exercised. They are the securities which are not the common stocks but could be converted to the

common stocks if holder exercise the option. On conversions dilutive securities increases

number of weighted shares effectively decreasing the EPS. For calculating diluted EPS it is

essential that impact of shares is dilutive. It is only the net income of company which is divided

by total of average shares of company and other convertible instruments. Net income of

company could be acquired from income statement and average shares are the average common

shares for entire year.

Example of the diluted EPS securities includes convertible preference shares, stock

options etc. Preferred stock which is convertible in nature means as it could be converted into the

common stock anytime in the future. Stock option is granted as the common benefit for

employee, that grants right to the buyer for purchasing common stock at set price and set time.

WEEK 10

a)

Journal Entries

Date Particulars Debit Credit

11/05/19 Purchases a/c 731707

To DFO ltd a/c 731707

(Being purchase recorded)

(300000 / 0.41)

30/06/19 DFO ltd a/c 34032

To Foreign Exchange profit or loss a/c 34032

(Being difference recorded in foreign exchange

profit or loss)

[(300000/0.41) – (300000/0.43)

14/08/20 DFO ltd a/c 769230

To Bank a/c 769230

(Being payment to creditor recorded )

(300000/0.39)

14/08/20 Foreign Exchange profit or loss a/c 71556

To DFO ltd a/c 71556

(Being effect of foreign exchange recorded)

[(300000/0.39) – (300000/0.43)

number of weighted shares effectively decreasing the EPS. For calculating diluted EPS it is

essential that impact of shares is dilutive. It is only the net income of company which is divided

by total of average shares of company and other convertible instruments. Net income of

company could be acquired from income statement and average shares are the average common

shares for entire year.

Example of the diluted EPS securities includes convertible preference shares, stock

options etc. Preferred stock which is convertible in nature means as it could be converted into the

common stock anytime in the future. Stock option is granted as the common benefit for

employee, that grants right to the buyer for purchasing common stock at set price and set time.

WEEK 10

a)

Journal Entries

Date Particulars Debit Credit

11/05/19 Purchases a/c 731707

To DFO ltd a/c 731707

(Being purchase recorded)

(300000 / 0.41)

30/06/19 DFO ltd a/c 34032

To Foreign Exchange profit or loss a/c 34032

(Being difference recorded in foreign exchange

profit or loss)

[(300000/0.41) – (300000/0.43)

14/08/20 DFO ltd a/c 769230

To Bank a/c 769230

(Being payment to creditor recorded )

(300000/0.39)

14/08/20 Foreign Exchange profit or loss a/c 71556

To DFO ltd a/c 71556

(Being effect of foreign exchange recorded)

[(300000/0.39) – (300000/0.43)

b)

Qualifying Asset

It could be defined as assets that takes substantial time period for keeping ready for the

intended use and sale. As per IAS 23 substantial period is period of twelve months. Period

shorter or longer than the specified period is considerable as per IAS 23. Qualifying assets could

be anything which takes time to get ready for the use which could properties, plant, equipments

or the investment properties during construction period and it also covers intangible assets under

development phase. IAS 23 excludes two type of asset from the scope which would otherwise

have been qualifying assets which are qualifying asset that are measured at fair value like

biological assets and inventories which are produced or manufactured in big quantities on

repetitive basis and takes substantial period for getting ready for the sale.

Borrowing cost is directly attributable construction, acquisition or production of the

qualifying assets forms part of cost of the asset, therefore is required to be capitalised. When

company borrows funds the cost which are eligible for the capitalisation are actual cost incurred

minus the income earned on temporary investments of the borrowings. Where fund is part of

general pool, amount eligible is determined through application of capitalisation rate over the

expenditure on assets. Capitalisation rate is weighted average of borrowing cost applicable to

general pool. The capitalisation is commenced when the expenditures are incurred, borrowings

cost are incurred and other activities which are essential for making asset for the intended use or

the sale are under progress. Company can suspend capitalisation over the where development of

the asset is interrupted. It should cease substantially when all the activities related to preparation

of asset for intended use or the sale are completed.

Examples

1. Fixed assets which take substantial time in getting for the intended use or the sale.

2. Investments could be regarded as qualifying assets is it is taking considerable time to

make the investment ready for use or the sale.

Qualifying Asset

It could be defined as assets that takes substantial time period for keeping ready for the

intended use and sale. As per IAS 23 substantial period is period of twelve months. Period

shorter or longer than the specified period is considerable as per IAS 23. Qualifying assets could

be anything which takes time to get ready for the use which could properties, plant, equipments

or the investment properties during construction period and it also covers intangible assets under

development phase. IAS 23 excludes two type of asset from the scope which would otherwise

have been qualifying assets which are qualifying asset that are measured at fair value like

biological assets and inventories which are produced or manufactured in big quantities on

repetitive basis and takes substantial period for getting ready for the sale.

Borrowing cost is directly attributable construction, acquisition or production of the

qualifying assets forms part of cost of the asset, therefore is required to be capitalised. When

company borrows funds the cost which are eligible for the capitalisation are actual cost incurred

minus the income earned on temporary investments of the borrowings. Where fund is part of

general pool, amount eligible is determined through application of capitalisation rate over the

expenditure on assets. Capitalisation rate is weighted average of borrowing cost applicable to

general pool. The capitalisation is commenced when the expenditures are incurred, borrowings

cost are incurred and other activities which are essential for making asset for the intended use or

the sale are under progress. Company can suspend capitalisation over the where development of

the asset is interrupted. It should cease substantially when all the activities related to preparation

of asset for intended use or the sale are completed.

Examples

1. Fixed assets which take substantial time in getting for the intended use or the sale.

2. Investments could be regarded as qualifying assets is it is taking considerable time to

make the investment ready for use or the sale.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Samaha, K., Khlif, H. and Dahawy, K., 2016. Compliance with IAS/IFRS and its determinants:

A meta-analysis. Journal of Accounting, Business and Management (JABM). 23(1). pp.41-

63.

Folkinshteyn, D. and Romeo, G., 2017. Twenty-five years of effective US and Foreign Tax Rates

for Large and Small Firms and their Effect on EPS. Journal of Applied Business and

Economics.

Online

AASB 119. 2019. [Online]. Available through :

<https://www.nexia.com.au/news/accounting/use-discount-rates-measuring-employee-benefits>.

Books and Journals

Samaha, K., Khlif, H. and Dahawy, K., 2016. Compliance with IAS/IFRS and its determinants:

A meta-analysis. Journal of Accounting, Business and Management (JABM). 23(1). pp.41-

63.

Folkinshteyn, D. and Romeo, G., 2017. Twenty-five years of effective US and Foreign Tax Rates

for Large and Small Firms and their Effect on EPS. Journal of Applied Business and

Economics.

Online

AASB 119. 2019. [Online]. Available through :

<https://www.nexia.com.au/news/accounting/use-discount-rates-measuring-employee-benefits>.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.