Accounting Theory and Current Issues

VerifiedAdded on 2023/04/21

|18

|4448

|392

AI Summary

This report discusses accounting theories and their application in major accounting issues. It analyzes the qualitative characteristics of financial reporting, the decision to amend Corporations Act, asset revaluation motivations, and the impact of lease standards on financial reporting.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING THEORY AND CURRENT ISSUES

Accounting Theory and Current Issues

Name of the Student

Name of the University

Author’s Note

Accounting Theory and Current Issues

Name of the Student

Name of the University

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING THEORY AND CURRENT ISSUES

Executive Summary

The findings of the report state that the IFRS standards of accounting lack certain qualitative

characteristics. This report also discusses about the decision of Australian Government to

implement new standard in Corporations Act. After that, this report discusses about the asset

revaluation motivating. This report also shows the asset impairment of Woolworths. Lastly,

this report shows the benefits of new lease standard along with the limitations of the former

lease standard.

Executive Summary

The findings of the report state that the IFRS standards of accounting lack certain qualitative

characteristics. This report also discusses about the decision of Australian Government to

implement new standard in Corporations Act. After that, this report discusses about the asset

revaluation motivating. This report also shows the asset impairment of Woolworths. Lastly,

this report shows the benefits of new lease standard along with the limitations of the former

lease standard.

2ACCOUNTING THEORY AND CURRENT ISSUES

Table of Contents

Introduction................................................................................................................................2

Assessment A.............................................................................................................................2

Assessment B.............................................................................................................................4

Assessment C.............................................................................................................................6

Requirement a........................................................................................................................6

Requirement b........................................................................................................................7

Requirement c........................................................................................................................7

Assessment D.............................................................................................................................8

Requirement i.........................................................................................................................8

Requirement ii........................................................................................................................8

Requirement iii.......................................................................................................................8

Requirement iv.......................................................................................................................9

Requirement v........................................................................................................................9

Requirement vi.....................................................................................................................10

Requirement vii....................................................................................................................10

Requirement viii...................................................................................................................10

Assessment E...........................................................................................................................10

Requirement i.......................................................................................................................10

Requirement ii......................................................................................................................11

Requirement iii.....................................................................................................................11

Requirement iv.....................................................................................................................11

Requirement v......................................................................................................................11

Conclusion................................................................................................................................12

References................................................................................................................................13

Table of Contents

Introduction................................................................................................................................2

Assessment A.............................................................................................................................2

Assessment B.............................................................................................................................4

Assessment C.............................................................................................................................6

Requirement a........................................................................................................................6

Requirement b........................................................................................................................7

Requirement c........................................................................................................................7

Assessment D.............................................................................................................................8

Requirement i.........................................................................................................................8

Requirement ii........................................................................................................................8

Requirement iii.......................................................................................................................8

Requirement iv.......................................................................................................................9

Requirement v........................................................................................................................9

Requirement vi.....................................................................................................................10

Requirement vii....................................................................................................................10

Requirement viii...................................................................................................................10

Assessment E...........................................................................................................................10

Requirement i.......................................................................................................................10

Requirement ii......................................................................................................................11

Requirement iii.....................................................................................................................11

Requirement iv.....................................................................................................................11

Requirement v......................................................................................................................11

Conclusion................................................................................................................................12

References................................................................................................................................13

3ACCOUNTING THEORY AND CURRENT ISSUES

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING THEORY AND CURRENT ISSUES

Introduction

The main aim of this report can be found in the discussion on different accounting

theories along with their application in some of the major accounting issues. The objectives

of the report can be divided into five parts. The aim of the first part of the report is to analysis

and valuation of certain qualitative characteristics of financial reporting that are missing in

the current financial reporting practices of IFRS. The aim of the next part of this report is to

analyse the decision of Australian Government to amend Corporations Act through three

accounting theories; they are public interest theory, capture theory and economic interest

group theory. The objective of the next part of the report is to review the decision of the

firms’ directors not to do the revaluation of the property, plant and equipment (PPE). The

next part of the report considers the analysis of the accounting practice for impairment in an

ASX listed company; and Woolworths Group Limited is considered for this purpose. The last

part of the report analytically reviews the impact of former and new lease standards on

company financial reporting.

Woolworths Group Limited (Woolworths) is one of the leading Australian companies

having operating in the retail industry throughout Australia and New Zealand. It is considered

as the second largest Australian company relating to revenue. Woolworths was established in

the year of 1924 and is headquartered at Bella Vista, New South Wales, Australia

(woolworthsgroup.com.au 2019).

Assessment A

Financial information become beneficial to the users when they have the needed

qualitative financial reporting characteristics. The fundamental qualitative characteristics are

relevance and faithful representation; and the enhancing qualitative characteristics are

comparability, verifiability, understandability and timeliness (iasplus.com 2019). The

Introduction

The main aim of this report can be found in the discussion on different accounting

theories along with their application in some of the major accounting issues. The objectives

of the report can be divided into five parts. The aim of the first part of the report is to analysis

and valuation of certain qualitative characteristics of financial reporting that are missing in

the current financial reporting practices of IFRS. The aim of the next part of this report is to

analyse the decision of Australian Government to amend Corporations Act through three

accounting theories; they are public interest theory, capture theory and economic interest

group theory. The objective of the next part of the report is to review the decision of the

firms’ directors not to do the revaluation of the property, plant and equipment (PPE). The

next part of the report considers the analysis of the accounting practice for impairment in an

ASX listed company; and Woolworths Group Limited is considered for this purpose. The last

part of the report analytically reviews the impact of former and new lease standards on

company financial reporting.

Woolworths Group Limited (Woolworths) is one of the leading Australian companies

having operating in the retail industry throughout Australia and New Zealand. It is considered

as the second largest Australian company relating to revenue. Woolworths was established in

the year of 1924 and is headquartered at Bella Vista, New South Wales, Australia

(woolworthsgroup.com.au 2019).

Assessment A

Financial information become beneficial to the users when they have the needed

qualitative financial reporting characteristics. The fundamental qualitative characteristics are

relevance and faithful representation; and the enhancing qualitative characteristics are

comparability, verifiability, understandability and timeliness (iasplus.com 2019). The

5ACCOUNTING THEORY AND CURRENT ISSUES

provided article includes the opinion of various individuals on adopting the financial

reporting practice of IFRS; and these individuals have expressed their concern over the

absence of certain qualitative characteristics in IFRS financial reporting practice (ey.com

2019).

It can be seen from the opinion of the former AXA head, Geoff Roberts that the

investor review the company’s investor reports and management briefing for understanding

the financial information of the firm. Hence, the appropriate qualitative characteristic in this

case of Understandability that is an enhancing characteristic and assists to increase the

financial reporting quality by making the financial information understandable to all class of

users. This characteristic helps the users in classifying and characterising the financial

information for their greater understandability. The financial reporting practice of IFRS is

compound which fails in proving the necessary understandability to the investors to review

the financial information provided in financial reports (ifrs.org 2019).

According to the statement of Terry Brown, the lack of technical accounting

knowledge can contribute to the misinterpretation by the investors at the time of investigating

the IFRS accounting of the companies. This situation also indicates towards the absence of

understandability which is an enhancing qualitative characteristic of financial reporting. The

statement of Terry Brown implies that the IFRS financial reporting practice fails in the

classification, characterization and presentation of financial information in clear and concise

manner to make it easily understandable to the users and investors in the presence of basic

technical knowledge. Hence, in the absence of the needed understandability, financial

information under IFRS practice can provide the users with the misleading information about

the financial position and performance of the firms (ey.com 2019).

provided article includes the opinion of various individuals on adopting the financial

reporting practice of IFRS; and these individuals have expressed their concern over the

absence of certain qualitative characteristics in IFRS financial reporting practice (ey.com

2019).

It can be seen from the opinion of the former AXA head, Geoff Roberts that the

investor review the company’s investor reports and management briefing for understanding

the financial information of the firm. Hence, the appropriate qualitative characteristic in this

case of Understandability that is an enhancing characteristic and assists to increase the

financial reporting quality by making the financial information understandable to all class of

users. This characteristic helps the users in classifying and characterising the financial

information for their greater understandability. The financial reporting practice of IFRS is

compound which fails in proving the necessary understandability to the investors to review

the financial information provided in financial reports (ifrs.org 2019).

According to the statement of Terry Brown, the lack of technical accounting

knowledge can contribute to the misinterpretation by the investors at the time of investigating

the IFRS accounting of the companies. This situation also indicates towards the absence of

understandability which is an enhancing qualitative characteristic of financial reporting. The

statement of Terry Brown implies that the IFRS financial reporting practice fails in the

classification, characterization and presentation of financial information in clear and concise

manner to make it easily understandable to the users and investors in the presence of basic

technical knowledge. Hence, in the absence of the needed understandability, financial

information under IFRS practice can provide the users with the misleading information about

the financial position and performance of the firms (ey.com 2019).

6ACCOUNTING THEORY AND CURRENT ISSUES

David Craig shows his concern over the fact that the investors are ignoring the

financial information of the companies under IFRS practice as this information is

complicating the actual financial position and performance of the companies. This particular

situation point to the absence of the fundamental qualitative characteristic of financial

information that are relevance and faithful representation. Relevant financial information in

showing the true financial position and performance of the companies; and faithful

representation of the financial information ensure the presence of relevant financial

information. The deep meaning of the statement of David Craig is that the financial

information of the companies under IFRS financial reporting practice is lacking both

relevance and faithful representation; and the effect of this phenomena can be seen in

obscuring the financial position of the firms from the provide financial information (ey.com

2019).

This situation demands to mention the central objective of financial reporting that is

to provide the users with the required financial information about the entities so that they can

make the needed decision for the firms’ resources. As per the above discussion, it is not

possible to satisfy this central objective in the absence of so many qualitative characteristics

of financial reporting (Zhang and Andrew 2014).

Assessment B

Public Interest Theory: The principle of public interest theory states that finding the

economically efficient solution of a problem is the main objective of the market regulators.

Specific regulations are introduced for this very purpose. Hence, the main aim behind this

introduction of regulation is to ensure the public wellbeing (Koopman, Mitchell and Thierer

2014). The provided situation can be reviewed with the principles of this theory as the

principle of this theory agrees on the introduction of new regulation in the existing

Corporations Act so that the responsibilities related to society and environment can be

David Craig shows his concern over the fact that the investors are ignoring the

financial information of the companies under IFRS practice as this information is

complicating the actual financial position and performance of the companies. This particular

situation point to the absence of the fundamental qualitative characteristic of financial

information that are relevance and faithful representation. Relevant financial information in

showing the true financial position and performance of the companies; and faithful

representation of the financial information ensure the presence of relevant financial

information. The deep meaning of the statement of David Craig is that the financial

information of the companies under IFRS financial reporting practice is lacking both

relevance and faithful representation; and the effect of this phenomena can be seen in

obscuring the financial position of the firms from the provide financial information (ey.com

2019).

This situation demands to mention the central objective of financial reporting that is

to provide the users with the required financial information about the entities so that they can

make the needed decision for the firms’ resources. As per the above discussion, it is not

possible to satisfy this central objective in the absence of so many qualitative characteristics

of financial reporting (Zhang and Andrew 2014).

Assessment B

Public Interest Theory: The principle of public interest theory states that finding the

economically efficient solution of a problem is the main objective of the market regulators.

Specific regulations are introduced for this very purpose. Hence, the main aim behind this

introduction of regulation is to ensure the public wellbeing (Koopman, Mitchell and Thierer

2014). The provided situation can be reviewed with the principles of this theory as the

principle of this theory agrees on the introduction of new regulation in the existing

Corporations Act so that the responsibilities related to society and environment can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND CURRENT ISSUES

included in them. As per this theory, it is needed to introduce the new regulation due to the

fact that the companies have the tendency to avoid both of their social and environmental

responsibilities for ensuring higher profitability. Hence, the presence of mandatory obligation

or regulation in the Corporations Act would put the obligation on the companies to comply

with their social as well as environmental responsibilities (Bös 2015). Thus, this particular

theory supports the introduction of new regulations in the Corporations Act.

Capture Theory: According to the principle of capture theory, the regulators have the

tendency to manipulate the existing regulators or to introduce specific regulation with the aim

to fulfil their personal interests. It implies that the regulations might serve the regulators for

fulfilling their own interests after a specific period. For this reason, the application of the

principle of capture theory helps in knowing the actual intention behind the introduction of

new regulations (Joskow 2014). It is also possible to identify the groups affecting with the

introduction of regulation. The current situation can be explained with the light of this theory

which states that it was the correct decision not to amend the Corporations Act due to the

presence of the fact that the introduced regulation might to mapiluated after a certain time for

the satisfaction of personal interests (Engstrom 2013). Moreover, the presence of market

forces would automatically create obligation on the companies to become socially and

environmentally responsible for their own benefits.

Economic Interest Group Theory of Regulation: According to the principles of economic

interest group of theory of regulation, the presence of different policies can be seen in the

regulation and they are affected with the forces of demand and supply. According to this

theory, the government can be considered in the side of supply where the interest group can

be seen in the side of supply (Gilens and Page 2014). The government of the countries

introduce regulations for the overall benefits of common people and business industries.

Hence, the government does the designing of the regulations and puts the obligation on the

included in them. As per this theory, it is needed to introduce the new regulation due to the

fact that the companies have the tendency to avoid both of their social and environmental

responsibilities for ensuring higher profitability. Hence, the presence of mandatory obligation

or regulation in the Corporations Act would put the obligation on the companies to comply

with their social as well as environmental responsibilities (Bös 2015). Thus, this particular

theory supports the introduction of new regulations in the Corporations Act.

Capture Theory: According to the principle of capture theory, the regulators have the

tendency to manipulate the existing regulators or to introduce specific regulation with the aim

to fulfil their personal interests. It implies that the regulations might serve the regulators for

fulfilling their own interests after a specific period. For this reason, the application of the

principle of capture theory helps in knowing the actual intention behind the introduction of

new regulations (Joskow 2014). It is also possible to identify the groups affecting with the

introduction of regulation. The current situation can be explained with the light of this theory

which states that it was the correct decision not to amend the Corporations Act due to the

presence of the fact that the introduced regulation might to mapiluated after a certain time for

the satisfaction of personal interests (Engstrom 2013). Moreover, the presence of market

forces would automatically create obligation on the companies to become socially and

environmentally responsible for their own benefits.

Economic Interest Group Theory of Regulation: According to the principles of economic

interest group of theory of regulation, the presence of different policies can be seen in the

regulation and they are affected with the forces of demand and supply. According to this

theory, the government can be considered in the side of supply where the interest group can

be seen in the side of supply (Gilens and Page 2014). The government of the countries

introduce regulations for the overall benefits of common people and business industries.

Hence, the government does the designing of the regulations and puts the obligation on the

8ACCOUNTING THEORY AND CURRENT ISSUES

industries to adopt them. This particular point of view supports the decision of Australian

Government to introduce regulation in the Corporations Act related to social and

environmental responsibilities. This would ensure the welfare of the business industries that

could lead to the welfare of the common people. However, according to the concept of this

particular theory, it would be needed for the government to include the consumers of the

business industry in the regulation development process. This initiate would lead to the

development of such regulations that would ultimately contribute to make both the business

industries and consumers beneficial (Berry and Wilcox 2018). In addition, it would be

majorly effective in balance creation between the consumers and the business industries.

Assessment C

Requirement a

The provided information indicates towards the fact that the business organizations

are selecting for the non-measurement of PPE at fair value as they are preferring to adopt the

‘cost model’ for the same purpose. In this context, it needs to be mentioned that asset

revaluation can be upward and downward (Malmendier, Opp and Saidi 2016). There can be

increase in asset value and shareholder’s equity or decrease in financial leverage ratio from

upward revaluation. In here, there are certain reasons that motivate the directors of the firms

not to revalue their PPE.

One of the major motivations for the directors not to revalue their PPE is the presence

of huge cost associated with the revaluation process. This huge amount of revaluation cost

can lead to the increase in the company’s expenses that can have the negative effect on the

company’s profitability. The ranges of this revaluation costs can be the fees paid to the

revaluation officers, the time consumer for the revaluation of the assets, costs to keep all the

records related to revaluation and the charges to the auditors (Christensen and Nikolaev

industries to adopt them. This particular point of view supports the decision of Australian

Government to introduce regulation in the Corporations Act related to social and

environmental responsibilities. This would ensure the welfare of the business industries that

could lead to the welfare of the common people. However, according to the concept of this

particular theory, it would be needed for the government to include the consumers of the

business industry in the regulation development process. This initiate would lead to the

development of such regulations that would ultimately contribute to make both the business

industries and consumers beneficial (Berry and Wilcox 2018). In addition, it would be

majorly effective in balance creation between the consumers and the business industries.

Assessment C

Requirement a

The provided information indicates towards the fact that the business organizations

are selecting for the non-measurement of PPE at fair value as they are preferring to adopt the

‘cost model’ for the same purpose. In this context, it needs to be mentioned that asset

revaluation can be upward and downward (Malmendier, Opp and Saidi 2016). There can be

increase in asset value and shareholder’s equity or decrease in financial leverage ratio from

upward revaluation. In here, there are certain reasons that motivate the directors of the firms

not to revalue their PPE.

One of the major motivations for the directors not to revalue their PPE is the presence

of huge cost associated with the revaluation process. This huge amount of revaluation cost

can lead to the increase in the company’s expenses that can have the negative effect on the

company’s profitability. The ranges of this revaluation costs can be the fees paid to the

revaluation officers, the time consumer for the revaluation of the assets, costs to keep all the

records related to revaluation and the charges to the auditors (Christensen and Nikolaev

9ACCOUNTING THEORY AND CURRENT ISSUES

2013). The second motivation for the directors can be the fact that asset revaluation is viewed

as inconsistent as it interrupts the tradition asset valuation practice of historical costing. This

is because historical cost accounting is considered as more effective process for asset

valuation as it proves less scope for manipulation in the income statements. These are the

major motivations for the directors not to revalue the PPE (Choi et al. 2013).

Requirement b

There would be certain effects on the financial statements of the companies for the

decision not to revalue the assets. First, the absence of the revaluation of the assets would

restrict the increase or decrease in the value of the assets in the statement of financial

position. This aspect would lead to the creation of abnormal amount of profit or loss at the

time of the disposal of that particular asset in the market at fair value. On the broader aspect,

it would affect the earnings of the companies as the earnings can be decreased due to this. At

the same time, this decision can lead to the decrease in the asset value in the balance sheet

due to not comparing the asset values with the market prices (Zinkeviciene and Vaisnoraite

2014).

Requirement c

It can be seen from the above discussion that the decision not to revalue the assets can

lead to the decrease in earnings for the companies that can affect the wealth of the

shareholders in the negative manner. The shareholders would not be able in getting the

desired percentage of return on their investments when the earnings of the company decrease.

In addition, the decision not to revalue the assets would provide the shareholders with

misleading information about the asset position of the companies as the shareholders would

not be able in judging any decrease in the asset value in the absence of the process of

revaluation. These are the negative effects of not to revalue the assets on the shareholders

(Yao, Percy and Hu 2015).

2013). The second motivation for the directors can be the fact that asset revaluation is viewed

as inconsistent as it interrupts the tradition asset valuation practice of historical costing. This

is because historical cost accounting is considered as more effective process for asset

valuation as it proves less scope for manipulation in the income statements. These are the

major motivations for the directors not to revalue the PPE (Choi et al. 2013).

Requirement b

There would be certain effects on the financial statements of the companies for the

decision not to revalue the assets. First, the absence of the revaluation of the assets would

restrict the increase or decrease in the value of the assets in the statement of financial

position. This aspect would lead to the creation of abnormal amount of profit or loss at the

time of the disposal of that particular asset in the market at fair value. On the broader aspect,

it would affect the earnings of the companies as the earnings can be decreased due to this. At

the same time, this decision can lead to the decrease in the asset value in the balance sheet

due to not comparing the asset values with the market prices (Zinkeviciene and Vaisnoraite

2014).

Requirement c

It can be seen from the above discussion that the decision not to revalue the assets can

lead to the decrease in earnings for the companies that can affect the wealth of the

shareholders in the negative manner. The shareholders would not be able in getting the

desired percentage of return on their investments when the earnings of the company decrease.

In addition, the decision not to revalue the assets would provide the shareholders with

misleading information about the asset position of the companies as the shareholders would

not be able in judging any decrease in the asset value in the absence of the process of

revaluation. These are the negative effects of not to revalue the assets on the shareholders

(Yao, Percy and Hu 2015).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ACCOUNTING THEORY AND CURRENT ISSUES

Assessment D

Requirement i

The 2018 Annual Report of Woolworths includes all the needed financial information

related to their assets and liabilities along with the depreciation, amortization and impairment.

It can be seen from the 2018 Annual Report of Woolworths that the company has tested the

carrying value of property, plant and equipment, goodwill and intangible assets for the

financial year 2018; and the company did not recognize any impairment of these assets in the

year 2018. However, in the year 2017, Woolworths recognized impairment of non-financial

assets of $38 million from continuing operations that include $21 million related to Big W

store’s property, plant and equipment and $17 million related to intangibles of Summergate.

This information can be found in the Note no. 3.5 of the 201 Annual Report of Woolworths

(woolworthsgroup.com.au 2019).

Requirement ii

According to the Note 3.5 of the 2018 Annual Report of Woolworths, the company

estimated the recoverable amount of the assets for the determination of the degree of

impairment loss, if any. The company considers the recoverable amount of an asset as the

greater of its value in use and its fair value less dispose cost. In case an asset does not

generate large independent cash inflows, Woolworths assesses their recoverable value in the

cash generating units.Woolworths recognizes impairment loss when the carrying value of the

asset or cash generating unit is greater than its recoverable value (woolworthsgroup.com.au

2019).

Requirement iii

It can be seen from the 2018 Annual Report of Woolworths that the company has not

recognized any impairment expenditure during the financial year 2018 as there was not any

impairment in the same year (woolworthsgroup.com.au 2019).

Assessment D

Requirement i

The 2018 Annual Report of Woolworths includes all the needed financial information

related to their assets and liabilities along with the depreciation, amortization and impairment.

It can be seen from the 2018 Annual Report of Woolworths that the company has tested the

carrying value of property, plant and equipment, goodwill and intangible assets for the

financial year 2018; and the company did not recognize any impairment of these assets in the

year 2018. However, in the year 2017, Woolworths recognized impairment of non-financial

assets of $38 million from continuing operations that include $21 million related to Big W

store’s property, plant and equipment and $17 million related to intangibles of Summergate.

This information can be found in the Note no. 3.5 of the 201 Annual Report of Woolworths

(woolworthsgroup.com.au 2019).

Requirement ii

According to the Note 3.5 of the 2018 Annual Report of Woolworths, the company

estimated the recoverable amount of the assets for the determination of the degree of

impairment loss, if any. The company considers the recoverable amount of an asset as the

greater of its value in use and its fair value less dispose cost. In case an asset does not

generate large independent cash inflows, Woolworths assesses their recoverable value in the

cash generating units.Woolworths recognizes impairment loss when the carrying value of the

asset or cash generating unit is greater than its recoverable value (woolworthsgroup.com.au

2019).

Requirement iii

It can be seen from the 2018 Annual Report of Woolworths that the company has not

recognized any impairment expenditure during the financial year 2018 as there was not any

impairment in the same year (woolworthsgroup.com.au 2019).

11ACCOUNTING THEORY AND CURRENT ISSUES

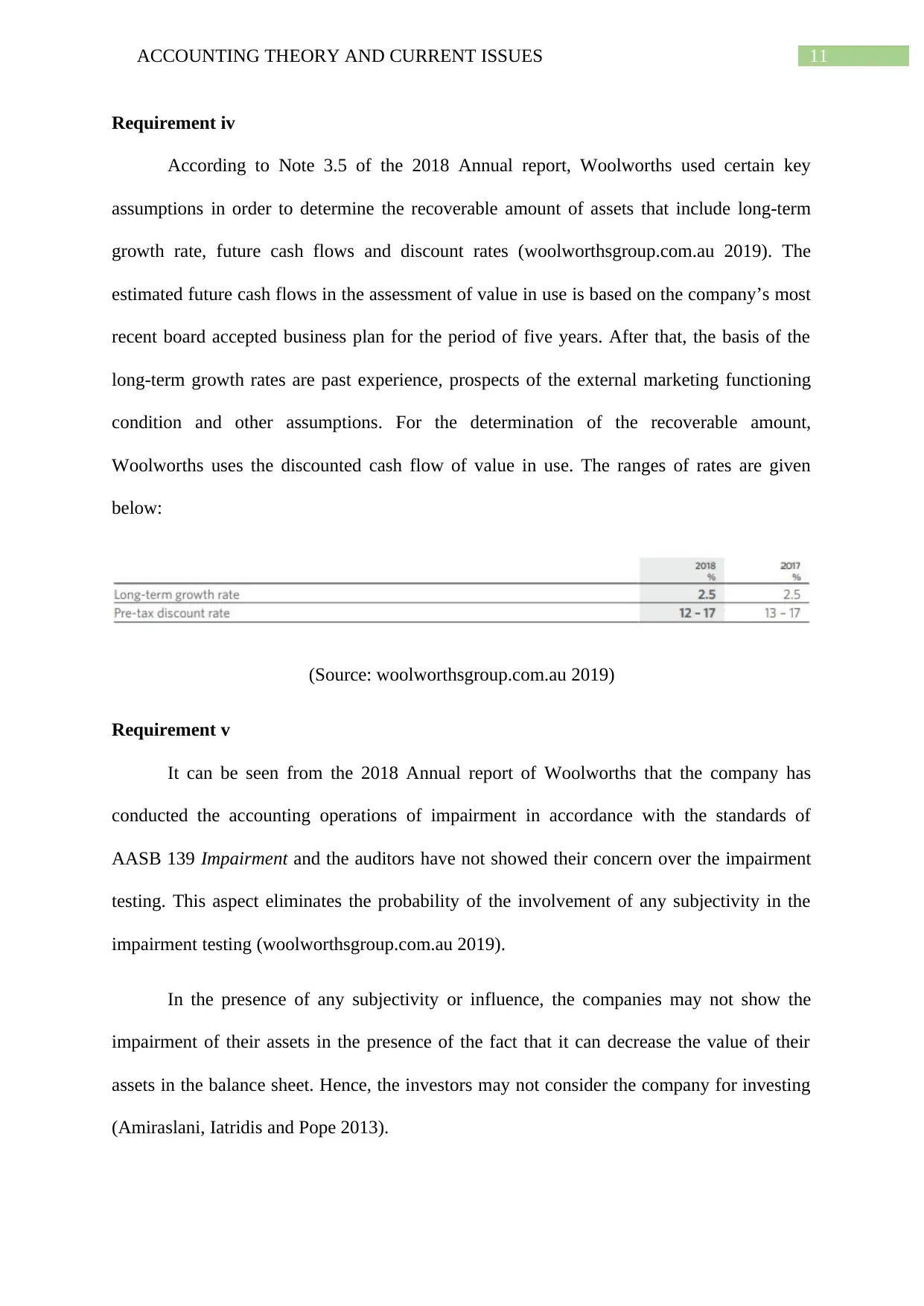

Requirement iv

According to Note 3.5 of the 2018 Annual report, Woolworths used certain key

assumptions in order to determine the recoverable amount of assets that include long-term

growth rate, future cash flows and discount rates (woolworthsgroup.com.au 2019). The

estimated future cash flows in the assessment of value in use is based on the company’s most

recent board accepted business plan for the period of five years. After that, the basis of the

long-term growth rates are past experience, prospects of the external marketing functioning

condition and other assumptions. For the determination of the recoverable amount,

Woolworths uses the discounted cash flow of value in use. The ranges of rates are given

below:

(Source: woolworthsgroup.com.au 2019)

Requirement v

It can be seen from the 2018 Annual report of Woolworths that the company has

conducted the accounting operations of impairment in accordance with the standards of

AASB 139 Impairment and the auditors have not showed their concern over the impairment

testing. This aspect eliminates the probability of the involvement of any subjectivity in the

impairment testing (woolworthsgroup.com.au 2019).

In the presence of any subjectivity or influence, the companies may not show the

impairment of their assets in the presence of the fact that it can decrease the value of their

assets in the balance sheet. Hence, the investors may not consider the company for investing

(Amiraslani, Iatridis and Pope 2013).

Requirement iv

According to Note 3.5 of the 2018 Annual report, Woolworths used certain key

assumptions in order to determine the recoverable amount of assets that include long-term

growth rate, future cash flows and discount rates (woolworthsgroup.com.au 2019). The

estimated future cash flows in the assessment of value in use is based on the company’s most

recent board accepted business plan for the period of five years. After that, the basis of the

long-term growth rates are past experience, prospects of the external marketing functioning

condition and other assumptions. For the determination of the recoverable amount,

Woolworths uses the discounted cash flow of value in use. The ranges of rates are given

below:

(Source: woolworthsgroup.com.au 2019)

Requirement v

It can be seen from the 2018 Annual report of Woolworths that the company has

conducted the accounting operations of impairment in accordance with the standards of

AASB 139 Impairment and the auditors have not showed their concern over the impairment

testing. This aspect eliminates the probability of the involvement of any subjectivity in the

impairment testing (woolworthsgroup.com.au 2019).

In the presence of any subjectivity or influence, the companies may not show the

impairment of their assets in the presence of the fact that it can decrease the value of their

assets in the balance sheet. Hence, the investors may not consider the company for investing

(Amiraslani, Iatridis and Pope 2013).

12ACCOUNTING THEORY AND CURRENT ISSUES

Requirement vi

The most interesting aspect in the impairment accounting of Woolworths is the

segregation of all the information related to impairment in the notes to the financial

statements such as method used in impairment, key judgments used and others. However, the

confusing aspect is that Woolworths has provided this information in haphazardly that can

create difficulty for the users to find the required information. It would be better in case all

the lease related information can be obtained from a single section in the annual report.

Requirement vii

One can gain the insight from analysing the impairment testing of Woolworths that

the testing of impairment largely depends on the correct use of assumptions and key

judgments; like discount rate, determination of cash flow and others. This aspect creates the

scope of subjectivity in the impairment testing process.

Requirement viii

Fair value measurement plays a crucial role in the process of impairment testing as

impairment loss is recognized when the carrying value of an asset is lower than its fair value.

Hence, fair value is the current market price of an asset that a company is subject to get at the

time of its selling. In impairment, the recoverable value of an asset is greater than its fair

value (Palea and Maino 2013).

Assessment E

Requirement i

Under the former lease standard, it is the obligation on the companies to classify their

leases as operating and finance lease; and they are not needed to report their leases in balance

sheet. This aspect provides the companies with the opportunity not to report their large

amount of lease liabilities in the balance sheet when the liabilities are actual and have

Requirement vi

The most interesting aspect in the impairment accounting of Woolworths is the

segregation of all the information related to impairment in the notes to the financial

statements such as method used in impairment, key judgments used and others. However, the

confusing aspect is that Woolworths has provided this information in haphazardly that can

create difficulty for the users to find the required information. It would be better in case all

the lease related information can be obtained from a single section in the annual report.

Requirement vii

One can gain the insight from analysing the impairment testing of Woolworths that

the testing of impairment largely depends on the correct use of assumptions and key

judgments; like discount rate, determination of cash flow and others. This aspect creates the

scope of subjectivity in the impairment testing process.

Requirement viii

Fair value measurement plays a crucial role in the process of impairment testing as

impairment loss is recognized when the carrying value of an asset is lower than its fair value.

Hence, fair value is the current market price of an asset that a company is subject to get at the

time of its selling. In impairment, the recoverable value of an asset is greater than its fair

value (Palea and Maino 2013).

Assessment E

Requirement i

Under the former lease standard, it is the obligation on the companies to classify their

leases as operating and finance lease; and they are not needed to report their leases in balance

sheet. This aspect provides the companies with the opportunity not to report their large

amount of lease liabilities in the balance sheet when the liabilities are actual and have

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13ACCOUNTING THEORY AND CURRENT ISSUES

material impact on the financial position of the companies (iasplus.com 2019). This is the

reason for the comment of the chairperson of IASB.

Requirement ii

Long-term operating leases are the actual liabilities of the companies and have

significant impact on the company’s financial position. As per the provided scenario, the

major retail companies had significant amount of operating lease liabilities and they did not

have to show them in the balance sheet as per the regulations. When compared to the balance

sheet liabilities, the lease liabilities were 66 times more than them.

Requirement iii

The financial obligation of an airline company having huge amount of leased aircraft

must be greater than the airline company having their own aircraft fleet. Thus, it is needed for

the first company to show these lease liabilities in the balance sheet that they do not have to

do under the former lease standard. Hence, they are equally treated as good as the former

company. It does not provide the fair chance for succeeding (Öztürk and Serçemeli 2016).

Requirement iv

According to the chairperson of IASB, companies will have to incur additional costs

for the adoption and implementation of the new lease standard. Most importantly, they have

to report their significant amount of lease liabilities in the balance sheet that will affect their

financial position hugely (iasplus.com 2019). These are the reasons for unpopularity.

Requirement v

The first reason is that the investors will be able to obtain information about the assets

and liabilities of the companies including the right-of-use lease assets and huge lease

liabilities. This will help the investors in assessing the correct financial standing of the

companies after considering all the assets and liabilities. Secondly, the obligation to report

material impact on the financial position of the companies (iasplus.com 2019). This is the

reason for the comment of the chairperson of IASB.

Requirement ii

Long-term operating leases are the actual liabilities of the companies and have

significant impact on the company’s financial position. As per the provided scenario, the

major retail companies had significant amount of operating lease liabilities and they did not

have to show them in the balance sheet as per the regulations. When compared to the balance

sheet liabilities, the lease liabilities were 66 times more than them.

Requirement iii

The financial obligation of an airline company having huge amount of leased aircraft

must be greater than the airline company having their own aircraft fleet. Thus, it is needed for

the first company to show these lease liabilities in the balance sheet that they do not have to

do under the former lease standard. Hence, they are equally treated as good as the former

company. It does not provide the fair chance for succeeding (Öztürk and Serçemeli 2016).

Requirement iv

According to the chairperson of IASB, companies will have to incur additional costs

for the adoption and implementation of the new lease standard. Most importantly, they have

to report their significant amount of lease liabilities in the balance sheet that will affect their

financial position hugely (iasplus.com 2019). These are the reasons for unpopularity.

Requirement v

The first reason is that the investors will be able to obtain information about the assets

and liabilities of the companies including the right-of-use lease assets and huge lease

liabilities. This will help the investors in assessing the correct financial standing of the

companies after considering all the assets and liabilities. Secondly, the obligation to report

14ACCOUNTING THEORY AND CURRENT ISSUES

the lease assets and liabilities in the balance sheet will provide the companies with the insight

whether leasing will be beneficial or buying in specific circumstances (Barone, Birt and

Moya 2014).

Conclusion

To infer, the financial reporting practice of IFRS has some major incompetence due to

the fact that it lacks some of the major qualitative characteristics of financial reporting like

understandability, faithful representation and relevance. The above discussion also shows the

perspective of decision related to the Australian Government’s decision not to introduce new

regulation in the existing Corporations Act. The above study shows that the directors do not

want to revalue their assets due to increased costs and inappropriateness with the historical

cost accounting. It can also be seen from the above that Woolworths did not have any

impairment losses in the year 2018 and they use different assumptions and key judgments for

impairment testing. Lastly, the introduction of new lease standard will be unpopular to some

companies, but it will bring improvement in financial reporting (iasplus.com 2019).

the lease assets and liabilities in the balance sheet will provide the companies with the insight

whether leasing will be beneficial or buying in specific circumstances (Barone, Birt and

Moya 2014).

Conclusion

To infer, the financial reporting practice of IFRS has some major incompetence due to

the fact that it lacks some of the major qualitative characteristics of financial reporting like

understandability, faithful representation and relevance. The above discussion also shows the

perspective of decision related to the Australian Government’s decision not to introduce new

regulation in the existing Corporations Act. The above study shows that the directors do not

want to revalue their assets due to increased costs and inappropriateness with the historical

cost accounting. It can also be seen from the above that Woolworths did not have any

impairment losses in the year 2018 and they use different assumptions and key judgments for

impairment testing. Lastly, the introduction of new lease standard will be unpopular to some

companies, but it will bring improvement in financial reporting (iasplus.com 2019).

15ACCOUNTING THEORY AND CURRENT ISSUES

References

Amiraslani, H., Iatridis, G.E. and Pope, P.F., 2013. Accounting for asset impairment: a test

for IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: A review of recent

literature. Accounting in Europe, 11(1), pp.35-54.

Berry, J.M. and Wilcox, C., 2018. The interest group society. Routledge.

Bös, D., 2015. Pricing and price regulation: an economic theory for public enterprises and

public utilities (Vol. 34). Elsevier.

Choi, T.H., Pae, J., Park, S. and Song, Y., 2013. Asset revaluations: motives and choice of

items to revalue. Asia-Pacific Journal of Accounting & Economics, 20(2), pp.144-171.

Christensen, H.B. and Nikolaev, V.V., 2013. Does fair value accounting for non-financial

assets pass the market test?. Review of Accounting Studies, 18(3), pp.734-775.

Engstrom, D.F., 2013. Corralling capture. Harv. JL & Pub. Pol'y, 36, p.31.

Ey.com. (2019). [online] Available at:

https://www.ey.com/Publication/vwLUAssets/Supplement_86_GL_IFRS/$FILE/

Supplement_86_GL_IFRS.pdf [Accessed 8 Jan. 2019].

Ey.com. (2019). [online] Available at: https://www.ey.com/Publication/vwLUAssets/ey-

applying-conceptual-framework-april2018/$FILE/ey-applying-conceptual-framework-

april2018.pdf [Accessed 8 Jan. 2019].

Gilens, M. and Page, B.I., 2014. Testing theories of American politics: Elites, interest groups,

and average citizens. Perspectives on politics, 12(3), pp.564-581.

References

Amiraslani, H., Iatridis, G.E. and Pope, P.F., 2013. Accounting for asset impairment: a test

for IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

Barone, E., Birt, J. and Moya, S., 2014. Lease accounting: A review of recent

literature. Accounting in Europe, 11(1), pp.35-54.

Berry, J.M. and Wilcox, C., 2018. The interest group society. Routledge.

Bös, D., 2015. Pricing and price regulation: an economic theory for public enterprises and

public utilities (Vol. 34). Elsevier.

Choi, T.H., Pae, J., Park, S. and Song, Y., 2013. Asset revaluations: motives and choice of

items to revalue. Asia-Pacific Journal of Accounting & Economics, 20(2), pp.144-171.

Christensen, H.B. and Nikolaev, V.V., 2013. Does fair value accounting for non-financial

assets pass the market test?. Review of Accounting Studies, 18(3), pp.734-775.

Engstrom, D.F., 2013. Corralling capture. Harv. JL & Pub. Pol'y, 36, p.31.

Ey.com. (2019). [online] Available at:

https://www.ey.com/Publication/vwLUAssets/Supplement_86_GL_IFRS/$FILE/

Supplement_86_GL_IFRS.pdf [Accessed 8 Jan. 2019].

Ey.com. (2019). [online] Available at: https://www.ey.com/Publication/vwLUAssets/ey-

applying-conceptual-framework-april2018/$FILE/ey-applying-conceptual-framework-

april2018.pdf [Accessed 8 Jan. 2019].

Gilens, M. and Page, B.I., 2014. Testing theories of American politics: Elites, interest groups,

and average citizens. Perspectives on politics, 12(3), pp.564-581.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16ACCOUNTING THEORY AND CURRENT ISSUES

Iasplus.com. (2019). Conceptual Framework for Financial Reporting 2018. [online]

Available at: https://www.iasplus.com/en/standards/other/framework [Accessed 8 Jan. 2019].

Iasplus.com. 2019. IAS 17 — Leases. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias17 [Accessed 8 Jan. 2019].

Iasplus.com. 2019. IFRS 16 — Leases. [online] Available at:

https://www.iasplus.com/en/standards/ifrs/ifrs-16 [Accessed 8 Jan. 2019].

Ifrs.org. (2019). [online] Available at: https://www.ifrs.org/-/media/project/conceptual-

framework/fact-sheet-project-summary-and-feedback-statement/conceptual-framework-

project-summary.pdf [Accessed 8 Jan. 2019].

Joskow, P.L., 2014. Incentive regulation in theory and practice: electricity distribution and

transmission networks. In Economic Regulation and Its Reform: What Have We

Learned? (pp. 291-344). University of Chicago Press.

Koopman, C., Mitchell, M. and Thierer, A., 2014. The sharing economy and consumer

protection regulation: The case for policy change. J. Bus. Entrepreneurship & L., 8, p.529.

Malmendier, U., Opp, M.M. and Saidi, F., 2016. Target revaluation after failed takeover

attempts: Cash versus stock. Journal of Financial Economics, 119(1), pp.92-106.

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on

Statement of Financial Position and Key Ratios: A Case Study on an Airline Company in

Turkey. Business and Economics Research Journal, 7(4), p.143.

Palea, V. and Maino, R., 2013. Private equity fair value measurement: a critical perspective

on IFRS 13. Australian Accounting Review, 23(3), pp.264-278.

Iasplus.com. (2019). Conceptual Framework for Financial Reporting 2018. [online]

Available at: https://www.iasplus.com/en/standards/other/framework [Accessed 8 Jan. 2019].

Iasplus.com. 2019. IAS 17 — Leases. [online] Available at:

https://www.iasplus.com/en/standards/ias/ias17 [Accessed 8 Jan. 2019].

Iasplus.com. 2019. IFRS 16 — Leases. [online] Available at:

https://www.iasplus.com/en/standards/ifrs/ifrs-16 [Accessed 8 Jan. 2019].

Ifrs.org. (2019). [online] Available at: https://www.ifrs.org/-/media/project/conceptual-

framework/fact-sheet-project-summary-and-feedback-statement/conceptual-framework-

project-summary.pdf [Accessed 8 Jan. 2019].

Joskow, P.L., 2014. Incentive regulation in theory and practice: electricity distribution and

transmission networks. In Economic Regulation and Its Reform: What Have We

Learned? (pp. 291-344). University of Chicago Press.

Koopman, C., Mitchell, M. and Thierer, A., 2014. The sharing economy and consumer

protection regulation: The case for policy change. J. Bus. Entrepreneurship & L., 8, p.529.

Malmendier, U., Opp, M.M. and Saidi, F., 2016. Target revaluation after failed takeover

attempts: Cash versus stock. Journal of Financial Economics, 119(1), pp.92-106.

Öztürk, M. and Serçemeli, M., 2016. Impact of New Standard" IFRS 16 Leases" on

Statement of Financial Position and Key Ratios: A Case Study on an Airline Company in

Turkey. Business and Economics Research Journal, 7(4), p.143.

Palea, V. and Maino, R., 2013. Private equity fair value measurement: a critical perspective

on IFRS 13. Australian Accounting Review, 23(3), pp.264-278.

17ACCOUNTING THEORY AND CURRENT ISSUES

Woolworthsgroup.com.au. 2019. 2018 Annual Report. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf [Accessed

8 Jan. 2019].

Woolworthsgroup.com.au. 2019. About Us - Woolworths Group. [online] Available at:

https://www.woolworthsgroup.com.au/page/about-us [Accessed 8 Jan. 2019].

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

Zhang, Y. and Andrew, J., 2014. Financialisation and the conceptual framework. Critical

perspectives on accounting, 25(1), pp.17-26.

Zinkeviciene, D. and Vaisnoraite, G., 2014. Factors affecting the choice of tangible fixed

asset accounting methods: Theoretical approach. European Scientific Journal, ESJ, 10(10).

Woolworthsgroup.com.au. 2019. 2018 Annual Report. [online] Available at:

https://www.woolworthsgroup.com.au/icms_docs/195396_annual-report-2018.pdf [Accessed

8 Jan. 2019].

Woolworthsgroup.com.au. 2019. About Us - Woolworths Group. [online] Available at:

https://www.woolworthsgroup.com.au/page/about-us [Accessed 8 Jan. 2019].

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and

audit fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

Zhang, Y. and Andrew, J., 2014. Financialisation and the conceptual framework. Critical

perspectives on accounting, 25(1), pp.17-26.

Zinkeviciene, D. and Vaisnoraite, G., 2014. Factors affecting the choice of tangible fixed

asset accounting methods: Theoretical approach. European Scientific Journal, ESJ, 10(10).

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.