Accounting Theory and Current Issues Name of the University Author(s)

VerifiedAdded on 2023/04/22

|17

|4015

|185

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING THEORY AND CURRENT ISSUES

Accounting Theory and Current Issues

Name of the Student

Name of the University

Authors Note

Course ID

Accounting Theory and Current Issues

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING THEORY AND CURRENT ISSUES

Executive summary:

According to the discussions held in the report, IFRS practices are reducing the financial

position of the company as this is not focusing on the qualitative analysis of the financial

data. Additionally, the report is also concerned about the Australian Government who should

not implement new change in Corporation Act. Asset revaluation is another important aspect

which is being discussed here. Asset impairment of BHP Billiton is also highlighted here.

Lastly, this discussion highlights the facts related to the lease standards and limitation of the

former lease standards.

Executive summary:

According to the discussions held in the report, IFRS practices are reducing the financial

position of the company as this is not focusing on the qualitative analysis of the financial

data. Additionally, the report is also concerned about the Australian Government who should

not implement new change in Corporation Act. Asset revaluation is another important aspect

which is being discussed here. Asset impairment of BHP Billiton is also highlighted here.

Lastly, this discussion highlights the facts related to the lease standards and limitation of the

former lease standards.

2ACCOUNTING THEORY AND CURRENT ISSUES

Table of Contents

Introduction................................................................................................................................4

Assessment A.............................................................................................................................4

Assessment B.............................................................................................................................6

Assessment C.............................................................................................................................7

Requirement a........................................................................................................................7

Requirement b........................................................................................................................8

Requirement c........................................................................................................................8

Assessment D.............................................................................................................................9

Requirement i.........................................................................................................................9

Requirement ii:.......................................................................................................................9

Requirement iii:....................................................................................................................10

Requirement iv:....................................................................................................................10

Requirement v:.....................................................................................................................10

Requirement vi:....................................................................................................................11

Requirement vii....................................................................................................................11

Requirement viii...................................................................................................................11

Assessment E...........................................................................................................................11

Requirement i.......................................................................................................................11

Requirement ii......................................................................................................................12

Requirement iii.....................................................................................................................12

Table of Contents

Introduction................................................................................................................................4

Assessment A.............................................................................................................................4

Assessment B.............................................................................................................................6

Assessment C.............................................................................................................................7

Requirement a........................................................................................................................7

Requirement b........................................................................................................................8

Requirement c........................................................................................................................8

Assessment D.............................................................................................................................9

Requirement i.........................................................................................................................9

Requirement ii:.......................................................................................................................9

Requirement iii:....................................................................................................................10

Requirement iv:....................................................................................................................10

Requirement v:.....................................................................................................................10

Requirement vi:....................................................................................................................11

Requirement vii....................................................................................................................11

Requirement viii...................................................................................................................11

Assessment E...........................................................................................................................11

Requirement i.......................................................................................................................11

Requirement ii......................................................................................................................12

Requirement iii.....................................................................................................................12

3ACCOUNTING THEORY AND CURRENT ISSUES

Requirement iv.....................................................................................................................12

Requirement v......................................................................................................................13

Conclusion................................................................................................................................13

References:...............................................................................................................................14

Requirement iv.....................................................................................................................12

Requirement v......................................................................................................................13

Conclusion................................................................................................................................13

References:...............................................................................................................................14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING THEORY AND CURRENT ISSUES

Introduction

The purpose of this report is to highlight the objectives and functionalities of different

accounting theories along with different account issues. This report is subjected to five

different segments as objectives of this paper. First part is consisting the analysis of different

financial practices those are not present in recent functions of IFRS. The second part is

aiming to discuss the objective of Australian Government to amend Corporations Act via the

accounting theories (Henderson et al., 2015). The third part is all about the review of the

choice of owner of firms for evaluating the property, plant and equipment (PPE). Apart from

these three account theories those have vital impact on the second part of this report are

public interest theory, capture theory and economic interest group theory, hence the impacts

and benefits of these theories are influencing the Corporations Act.

Assessment A

Financial reporting is a key point for the users who indulge themselves for nurturing

the financial information. The financial qualitative characteristics are nothing but the

relevance and obliged representation (Macve, 2015). Beside this the expanded financial

characteristics are understanding the fundamental facts of financial facts , verification of the

financial aspects, suitability of facts those are being presented in financial discussions and on

top of all these the comparability of all discussed facts. This report is going to discuss all

opinions of financial reporting practices of IFRS from different individual perspectives and

these individuals will be expressing their concerns.

According to the former AXA head, Geoff Roberts has taken the responsibility of

analysing the financial reports of the firm and this will be helpful in classifying the financial

investment characteristics. This specific distinctive feature helps the firm in understanding

the greater aspects of investment with respect to the company objectives (Khan, 2015). The

Introduction

The purpose of this report is to highlight the objectives and functionalities of different

accounting theories along with different account issues. This report is subjected to five

different segments as objectives of this paper. First part is consisting the analysis of different

financial practices those are not present in recent functions of IFRS. The second part is

aiming to discuss the objective of Australian Government to amend Corporations Act via the

accounting theories (Henderson et al., 2015). The third part is all about the review of the

choice of owner of firms for evaluating the property, plant and equipment (PPE). Apart from

these three account theories those have vital impact on the second part of this report are

public interest theory, capture theory and economic interest group theory, hence the impacts

and benefits of these theories are influencing the Corporations Act.

Assessment A

Financial reporting is a key point for the users who indulge themselves for nurturing

the financial information. The financial qualitative characteristics are nothing but the

relevance and obliged representation (Macve, 2015). Beside this the expanded financial

characteristics are understanding the fundamental facts of financial facts , verification of the

financial aspects, suitability of facts those are being presented in financial discussions and on

top of all these the comparability of all discussed facts. This report is going to discuss all

opinions of financial reporting practices of IFRS from different individual perspectives and

these individuals will be expressing their concerns.

According to the former AXA head, Geoff Roberts has taken the responsibility of

analysing the financial reports of the firm and this will be helpful in classifying the financial

investment characteristics. This specific distinctive feature helps the firm in understanding

the greater aspects of investment with respect to the company objectives (Khan, 2015). The

5ACCOUNTING THEORY AND CURRENT ISSUES

financial reporting practices of IFRS is a mixture of different features though it fails in

making the financial investors understand about the financial reports those are prepared for

classifying the company’s financial investment features. Hence, this is impacting the

companies who are following the method of financial investment objectives of IFRS.

As per the statement of Terry Brown, lesser the knowledge is for financial accounting

theories, the more it will harmful for the investors who are spending time for interpreting the

IFRS accounting of certain companies (Hoitash et al., 2017). This particular instinct also

proves that the IFRS accounting processes have less understandable features in terms of

investments. According to Terry Brown the basic technical knowledge any financial

accounting theory should be clear concise to the investors along with their user in terms of

understanding the facts, rules oriented to their investment policies and characterization of

assets where they are investing money and classification of aspects where they should invest

and where they should not (Lafond et al., 2016). Therefore, absence of these factors in IFRS

theory misleads the user along with the investors while taking part in some investments and

performance improving facts.

David Craig express his concern through this fact the investors and user are not

focusing on the financial information under the IFRS practices in companies as this is making

the financial process complicated for them. This particular aspect highlights that the IFRS

practice are not satisfying qualitative characteristics of financial information (Dutta &

Patatoukas, 2016). Companies can make their existence through relevant financial

information as it strengthens their position and faithful information makes company pretend

that they are actually using relevant financial data. David Craig wanted to highlight this fact

that the companies are lacking behind in showing the relevant and faithful nature in their

financial investments under the IFRS reporting practices.

financial reporting practices of IFRS is a mixture of different features though it fails in

making the financial investors understand about the financial reports those are prepared for

classifying the company’s financial investment features. Hence, this is impacting the

companies who are following the method of financial investment objectives of IFRS.

As per the statement of Terry Brown, lesser the knowledge is for financial accounting

theories, the more it will harmful for the investors who are spending time for interpreting the

IFRS accounting of certain companies (Hoitash et al., 2017). This particular instinct also

proves that the IFRS accounting processes have less understandable features in terms of

investments. According to Terry Brown the basic technical knowledge any financial

accounting theory should be clear concise to the investors along with their user in terms of

understanding the facts, rules oriented to their investment policies and characterization of

assets where they are investing money and classification of aspects where they should invest

and where they should not (Lafond et al., 2016). Therefore, absence of these factors in IFRS

theory misleads the user along with the investors while taking part in some investments and

performance improving facts.

David Craig express his concern through this fact the investors and user are not

focusing on the financial information under the IFRS practices in companies as this is making

the financial process complicated for them. This particular aspect highlights that the IFRS

practice are not satisfying qualitative characteristics of financial information (Dutta &

Patatoukas, 2016). Companies can make their existence through relevant financial

information as it strengthens their position and faithful information makes company pretend

that they are actually using relevant financial data. David Craig wanted to highlight this fact

that the companies are lacking behind in showing the relevant and faithful nature in their

financial investments under the IFRS reporting practices.

6ACCOUNTING THEORY AND CURRENT ISSUES

The above explained sections are mentioning a single objective- financial firms

required the needful information about their financial resources to fulfil their aims in

preparing the financial reporting. Consequently, without the qualitative financial reporting

practices, following this particular objective is completely impossible.

Assessment B

Public Interest Theory: This theory highlights the facts that the solution should be

economically feasible enough to satisfy the business needs. There are particular regulations

those are published for this very reason. Hence, public wellbeing is the important concern in

establishing this theory (Campbell et al., 2018). The concerned condition can be judged with

respect to this theory as the public’s wellbeing is included in to this. Apart from this new

regulations can also be included to the existing corporate act. According to this theory,

companies generally neglect the social and environmental responsibilities; hence a new

regulation is needed for ensuring the compatibility with public interests. Hence, this theory

supports establishment of new regulation in Corporations Act.

Capture Theory: According to the principle of capture theory, the regulators are eligible for

changing the objectives of the existing regulators and also they can establish particular

regulations for the need of public (Chychyla et al., 2018). Hence, the regulators can only

satisfy their needs after certain period of establishing these regulations. Here comes the

benefit of capture theory which shows the actual interest behind the establishment of a new

regulation from the regulator end. Additionally this is also possible for the regulators to

identify the groups which are gaining benefit over the new regulations developed (Beaumont,

2015). We can now discuss the factual basis of the implication of Capture theory with respect

to the concerned scenario here which shows it is not beneficial to modify the Corporations

Act as this can be manipulated after certain period once the personal need is met.

The above explained sections are mentioning a single objective- financial firms

required the needful information about their financial resources to fulfil their aims in

preparing the financial reporting. Consequently, without the qualitative financial reporting

practices, following this particular objective is completely impossible.

Assessment B

Public Interest Theory: This theory highlights the facts that the solution should be

economically feasible enough to satisfy the business needs. There are particular regulations

those are published for this very reason. Hence, public wellbeing is the important concern in

establishing this theory (Campbell et al., 2018). The concerned condition can be judged with

respect to this theory as the public’s wellbeing is included in to this. Apart from this new

regulations can also be included to the existing corporate act. According to this theory,

companies generally neglect the social and environmental responsibilities; hence a new

regulation is needed for ensuring the compatibility with public interests. Hence, this theory

supports establishment of new regulation in Corporations Act.

Capture Theory: According to the principle of capture theory, the regulators are eligible for

changing the objectives of the existing regulators and also they can establish particular

regulations for the need of public (Chychyla et al., 2018). Hence, the regulators can only

satisfy their needs after certain period of establishing these regulations. Here comes the

benefit of capture theory which shows the actual interest behind the establishment of a new

regulation from the regulator end. Additionally this is also possible for the regulators to

identify the groups which are gaining benefit over the new regulations developed (Beaumont,

2015). We can now discuss the factual basis of the implication of Capture theory with respect

to the concerned scenario here which shows it is not beneficial to modify the Corporations

Act as this can be manipulated after certain period once the personal need is met.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND CURRENT ISSUES

Consequently the market forces will be making the companies responsible for the

environmental and social benefits of their own.

Economic Interest Group Theory of Regulation: The economic interest group theory of

regulation states that different policies can easily impact the regulations and these are

operated through the demand and supply chain features. In accordance with this theory the

government comes under the category for supply and the investors incur the functions for

demands. Government of any country establishes different set of regulations for the benefit of

common people along with several business industries (Warren & Jones, 2018). Hence,

government is main entity who pushes the business industries to follow their set of

regulations that they can modify at any point of time. This discussion supports the fact of

Australian Government who takes the decision in introducing the regulations in Corporation

Act which satisfies business as well as environmental responsibilities (Mullinova, 2016). This

fact will ensure the objective of wellbeing of the common people along with the business

objectives. However, this theory includes the consumers in the process of making the

development of the regulations. Hence this particular theory will indulge the development of

regulations for business as well as common people. Apart from this, it will also help in

keeping equal balance in between business and consumer needs.

Assessment C

Requirement a

According to the situations in the financial market this can be stated that the business

organizations are adopting this culture of not protecting the needs of consumers and they

mostly focusing on their objective related to cost-model. In addition to these facts this can be

also highlighted that there is possibility that the assets may increase and may decrease as well

(Schipper et al., 2017). Depending on the increase the shareholders decides the financial

Consequently the market forces will be making the companies responsible for the

environmental and social benefits of their own.

Economic Interest Group Theory of Regulation: The economic interest group theory of

regulation states that different policies can easily impact the regulations and these are

operated through the demand and supply chain features. In accordance with this theory the

government comes under the category for supply and the investors incur the functions for

demands. Government of any country establishes different set of regulations for the benefit of

common people along with several business industries (Warren & Jones, 2018). Hence,

government is main entity who pushes the business industries to follow their set of

regulations that they can modify at any point of time. This discussion supports the fact of

Australian Government who takes the decision in introducing the regulations in Corporation

Act which satisfies business as well as environmental responsibilities (Mullinova, 2016). This

fact will ensure the objective of wellbeing of the common people along with the business

objectives. However, this theory includes the consumers in the process of making the

development of the regulations. Hence this particular theory will indulge the development of

regulations for business as well as common people. Apart from this, it will also help in

keeping equal balance in between business and consumer needs.

Assessment C

Requirement a

According to the situations in the financial market this can be stated that the business

organizations are adopting this culture of not protecting the needs of consumers and they

mostly focusing on their objective related to cost-model. In addition to these facts this can be

also highlighted that there is possibility that the assets may increase and may decrease as well

(Schipper et al., 2017). Depending on the increase the shareholders decides the financial

8ACCOUNTING THEORY AND CURRENT ISSUES

leverage ratio to be fixed. There are specific motivations that change the mind of firm

directors for not doing their revaluation of PPE.

Huge associated cost feature is one of the important motivations that influence the

investors in revaluing their PPE. The huge revaluation charge may increase the company’s

expenditure which will be directly impacting on their profit margin. These charges may

include time to complete the revaluation, cost to manage this revaluation process and the fees

which is paid for managing the revaluation officers (Downs, 2017). Second important

motivation for the shareholders in not revaluating the assets is revaluation of assets is

considered as the blockage in maintaining the traditional costing policies involved within the

revaluation process. This happens as the historical costing process is still considered as the

best policy to revaluate the assets and this provides less scope of manipulation of assets.

Requirement b

There are chances that the financial statement of a company might get affected for

decision of not revaluating the assets. First chance is, the revaluation might stop the

increment or decrement of the number of asset in the financial statement of the company

(Elliott, 2017). This situation may create abnormal profit or loss amount when the asset will

be deposed to the market. This might also create such situations where the asset value will be

lesser in balance sheet while being compared to the market value.

Requirement c

As per the discussion held in the last part of this report, this can be identified that the

decision of not to revaluating the assets can lead to diminishing wealth of the company and

this may impact the shareholder in a negative aspect (Klychova et al., 2015). The company

may lose the faith of their shareholders as the shareholders will be unhappy about the return

from the investments, because of the company’s decreasing profit margin. Additionally, the

leverage ratio to be fixed. There are specific motivations that change the mind of firm

directors for not doing their revaluation of PPE.

Huge associated cost feature is one of the important motivations that influence the

investors in revaluing their PPE. The huge revaluation charge may increase the company’s

expenditure which will be directly impacting on their profit margin. These charges may

include time to complete the revaluation, cost to manage this revaluation process and the fees

which is paid for managing the revaluation officers (Downs, 2017). Second important

motivation for the shareholders in not revaluating the assets is revaluation of assets is

considered as the blockage in maintaining the traditional costing policies involved within the

revaluation process. This happens as the historical costing process is still considered as the

best policy to revaluate the assets and this provides less scope of manipulation of assets.

Requirement b

There are chances that the financial statement of a company might get affected for

decision of not revaluating the assets. First chance is, the revaluation might stop the

increment or decrement of the number of asset in the financial statement of the company

(Elliott, 2017). This situation may create abnormal profit or loss amount when the asset will

be deposed to the market. This might also create such situations where the asset value will be

lesser in balance sheet while being compared to the market value.

Requirement c

As per the discussion held in the last part of this report, this can be identified that the

decision of not to revaluating the assets can lead to diminishing wealth of the company and

this may impact the shareholder in a negative aspect (Klychova et al., 2015). The company

may lose the faith of their shareholders as the shareholders will be unhappy about the return

from the investments, because of the company’s decreasing profit margin. Additionally, the

9ACCOUNTING THEORY AND CURRENT ISSUES

shareholders will not be able to judge the actual value of their company asset as the process

revaluation will not be present in the company. These consequences are nothing but the

impact of not revaluating the assets for companies who are using assets for building their

positions in the financial market.

Assessment D

Requirement i

The annual report of BHP Billiton for the year ended 2018 provides the information

relating to the impairment of its non-current assets. As evident from the annual report BHP

Billiton has carried out an impairment testing for all its assets where an indication of

impairment is available (Barron et al., 2016). For the impairment purpose the goodwill has

been tested on yearly basis. On noticing that the assets value is greater than the recoverable

value, the asset is impaired and the loss of impairment is charged to profit and loss account.

The total amount of impairment from its continuing information for the year stood $2,353

which included the goodwill and other intangible assets. The information is available under

notes 10 of the annual report.

Requirement ii:

The impairment testing is performed by BHP Billiton when it is indication of

impairment. The impairment testing is conduced when the amount of assets is exceeding the

recoverable amount (Bhp.com 2019). BHP Billiton impairs the assets and the loss originating

from impairment is charged to the statement of income in order to lower down the carrying

amount into the balance sheet to its recoverable amount.

shareholders will not be able to judge the actual value of their company asset as the process

revaluation will not be present in the company. These consequences are nothing but the

impact of not revaluating the assets for companies who are using assets for building their

positions in the financial market.

Assessment D

Requirement i

The annual report of BHP Billiton for the year ended 2018 provides the information

relating to the impairment of its non-current assets. As evident from the annual report BHP

Billiton has carried out an impairment testing for all its assets where an indication of

impairment is available (Barron et al., 2016). For the impairment purpose the goodwill has

been tested on yearly basis. On noticing that the assets value is greater than the recoverable

value, the asset is impaired and the loss of impairment is charged to profit and loss account.

The total amount of impairment from its continuing information for the year stood $2,353

which included the goodwill and other intangible assets. The information is available under

notes 10 of the annual report.

Requirement ii:

The impairment testing is performed by BHP Billiton when it is indication of

impairment. The impairment testing is conduced when the amount of assets is exceeding the

recoverable amount (Bhp.com 2019). BHP Billiton impairs the assets and the loss originating

from impairment is charged to the statement of income in order to lower down the carrying

amount into the balance sheet to its recoverable amount.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ACCOUNTING THEORY AND CURRENT ISSUES

Requirement iii:

As understood from the annual report of BHP Billiton, the company has not recorded

any impairment expenses as there was no impairment performed during the year 2018.

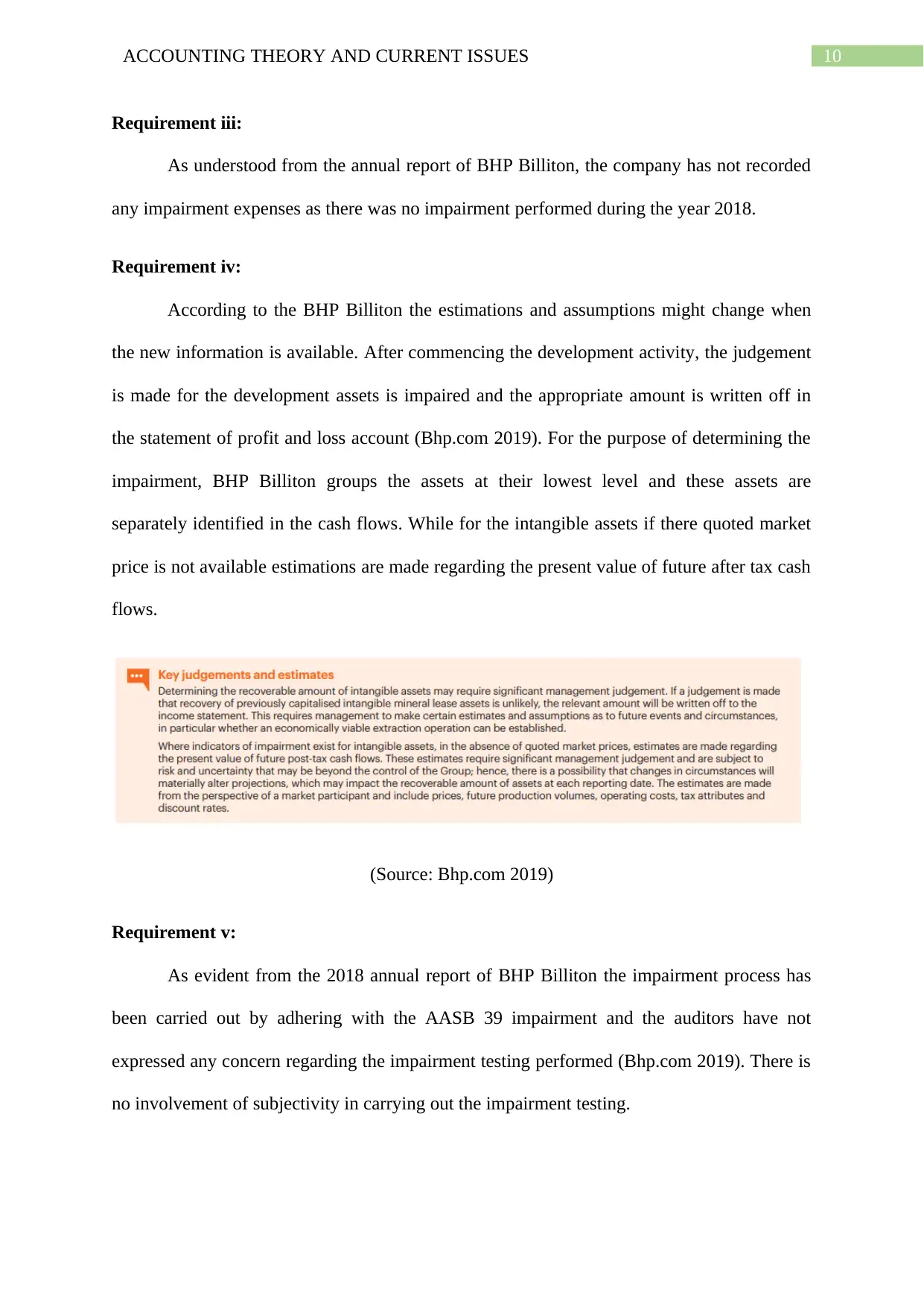

Requirement iv:

According to the BHP Billiton the estimations and assumptions might change when

the new information is available. After commencing the development activity, the judgement

is made for the development assets is impaired and the appropriate amount is written off in

the statement of profit and loss account (Bhp.com 2019). For the purpose of determining the

impairment, BHP Billiton groups the assets at their lowest level and these assets are

separately identified in the cash flows. While for the intangible assets if there quoted market

price is not available estimations are made regarding the present value of future after tax cash

flows.

(Source: Bhp.com 2019)

Requirement v:

As evident from the 2018 annual report of BHP Billiton the impairment process has

been carried out by adhering with the AASB 39 impairment and the auditors have not

expressed any concern regarding the impairment testing performed (Bhp.com 2019). There is

no involvement of subjectivity in carrying out the impairment testing.

Requirement iii:

As understood from the annual report of BHP Billiton, the company has not recorded

any impairment expenses as there was no impairment performed during the year 2018.

Requirement iv:

According to the BHP Billiton the estimations and assumptions might change when

the new information is available. After commencing the development activity, the judgement

is made for the development assets is impaired and the appropriate amount is written off in

the statement of profit and loss account (Bhp.com 2019). For the purpose of determining the

impairment, BHP Billiton groups the assets at their lowest level and these assets are

separately identified in the cash flows. While for the intangible assets if there quoted market

price is not available estimations are made regarding the present value of future after tax cash

flows.

(Source: Bhp.com 2019)

Requirement v:

As evident from the 2018 annual report of BHP Billiton the impairment process has

been carried out by adhering with the AASB 39 impairment and the auditors have not

expressed any concern regarding the impairment testing performed (Bhp.com 2019). There is

no involvement of subjectivity in carrying out the impairment testing.

11ACCOUNTING THEORY AND CURRENT ISSUES

On the event of any subjectivity or influence BHP Billiton might not represent the

impairment testing of its assets based on the reason that it can reduce the carrying amount of

the asset in the balance sheet. This may not enable the investors from making any

investments.

Requirement vi:

The interesting part of information provided is the impairment account that provides a

detailed information regarding the impairment performed its non-current assets and other

intangible assets by laying down the amount of impairment in a column wise. While the

confusing part is that the information may not provide the investors to obtain the actual view

of lease impairment that is not discussed in the annual report in a detailed manner.

Requirement vii

From the information gained it is understood that BHP Billiton makes the appropriate

estimations and judgements regarding the quoted market price of its intangible assets and the

after tax cash flows generated. All this aspects results in the subjectivity of impairment

testing procedure.

Requirement viii

According to the IFRS 13 fair value refers to the price that would be obtained

following the sale of the asset or the amount that is paid for transferring a liability in the form

of orderly transactions amid the market participants based on their measurement date (Stice et

al., 2015).

Assessment E

Requirement i

According to the former lease standard, there is obligation to be followed by the

companies where they should classify their lease policies as operating or finance lease, along

On the event of any subjectivity or influence BHP Billiton might not represent the

impairment testing of its assets based on the reason that it can reduce the carrying amount of

the asset in the balance sheet. This may not enable the investors from making any

investments.

Requirement vi:

The interesting part of information provided is the impairment account that provides a

detailed information regarding the impairment performed its non-current assets and other

intangible assets by laying down the amount of impairment in a column wise. While the

confusing part is that the information may not provide the investors to obtain the actual view

of lease impairment that is not discussed in the annual report in a detailed manner.

Requirement vii

From the information gained it is understood that BHP Billiton makes the appropriate

estimations and judgements regarding the quoted market price of its intangible assets and the

after tax cash flows generated. All this aspects results in the subjectivity of impairment

testing procedure.

Requirement viii

According to the IFRS 13 fair value refers to the price that would be obtained

following the sale of the asset or the amount that is paid for transferring a liability in the form

of orderly transactions amid the market participants based on their measurement date (Stice et

al., 2015).

Assessment E

Requirement i

According to the former lease standard, there is obligation to be followed by the

companies where they should classify their lease policies as operating or finance lease, along

12ACCOUNTING THEORY AND CURRENT ISSUES

with this they should not add their lease their lease in their balance sheet (Stockenstrand &

Nilsson, 2017). This helps the companies in keeping their position in a good way they don’t

have to show their materialistic actual leases in balance sheet.

Requirement ii

Long term operating leases are impactful liabilities for the company and also they

face several changes in their financial position because of these liabilities (Trotman &

Carson, 2018). As per the scenario getting discussed here, many of the retail companies are

having huge liabilities that they are not showing in their balance sheet which is maintaining

their financial position in the market. Apart from this, the lease liabilities are 66 percent more

than the balance sheet liabilities in actual scenarios.

Requirement iii

The lease amount for an aircraft company will be higher than bearing their own

expenses in making an aircraft fleet. Hence, the first company should their lease liabilities in

their balance sheet which is not happening in the former lease standards (Larson et al., 2017).

The benefit of this policy is that all the companies are being treated as same amount of good

will they are having. Therefore, each company is not at all getting a fair chance to prove their

work efficiency according to the challenges they are incorporating in their financial

development period.

Requirement iv

According to the chairperson of IASB, companies needs to bear the cost for creating

new lease standards. Additionally, they are liable to show the liable lease amount they have

incurred in their business which will reduce their financial position in market (Baker &

Burlaud, 2015). Hence, these reasons might cause the unpopularity of the company in terms

of the market evaluation process.

with this they should not add their lease their lease in their balance sheet (Stockenstrand &

Nilsson, 2017). This helps the companies in keeping their position in a good way they don’t

have to show their materialistic actual leases in balance sheet.

Requirement ii

Long term operating leases are impactful liabilities for the company and also they

face several changes in their financial position because of these liabilities (Trotman &

Carson, 2018). As per the scenario getting discussed here, many of the retail companies are

having huge liabilities that they are not showing in their balance sheet which is maintaining

their financial position in the market. Apart from this, the lease liabilities are 66 percent more

than the balance sheet liabilities in actual scenarios.

Requirement iii

The lease amount for an aircraft company will be higher than bearing their own

expenses in making an aircraft fleet. Hence, the first company should their lease liabilities in

their balance sheet which is not happening in the former lease standards (Larson et al., 2017).

The benefit of this policy is that all the companies are being treated as same amount of good

will they are having. Therefore, each company is not at all getting a fair chance to prove their

work efficiency according to the challenges they are incorporating in their financial

development period.

Requirement iv

According to the chairperson of IASB, companies needs to bear the cost for creating

new lease standards. Additionally, they are liable to show the liable lease amount they have

incurred in their business which will reduce their financial position in market (Baker &

Burlaud, 2015). Hence, these reasons might cause the unpopularity of the company in terms

of the market evaluation process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13ACCOUNTING THEORY AND CURRENT ISSUES

Requirement v

First reason to be highlighted is the investors will be able to know the assets their

companies are operating as lease liabilities and also they will come across their right to use

those assets for the betterment of the company (Hoyle et al., 2015). This will be helpful for

the investors and shareholders for judging the financial position of their companies in terms

of assets and liabilities.

Conclusion

This can be concluded that the financial practices of IFRS have several disadvantages

in real scenario where the company face challenges as they are facing issues in terms of

shareholder knowledge, as the financial practice is incompatible of providing faithful

representation, understandability and relevant financial data. Apart from this, the above

discussion is also elaborating about the fact that the government should not make any

changes to the Corporation Act as this is reducing the chance of making balance in between

consumer and business process. Consequently, BHP Billiton did not reported about the

impairment loss, they considered the different methods of testing impairments and they

proceeded with that. At the end of discussion we found that the establishment of new lease

standards is benefitting the companies in improving their financial reporting standards.

Requirement v

First reason to be highlighted is the investors will be able to know the assets their

companies are operating as lease liabilities and also they will come across their right to use

those assets for the betterment of the company (Hoyle et al., 2015). This will be helpful for

the investors and shareholders for judging the financial position of their companies in terms

of assets and liabilities.

Conclusion

This can be concluded that the financial practices of IFRS have several disadvantages

in real scenario where the company face challenges as they are facing issues in terms of

shareholder knowledge, as the financial practice is incompatible of providing faithful

representation, understandability and relevant financial data. Apart from this, the above

discussion is also elaborating about the fact that the government should not make any

changes to the Corporation Act as this is reducing the chance of making balance in between

consumer and business process. Consequently, BHP Billiton did not reported about the

impairment loss, they considered the different methods of testing impairments and they

proceeded with that. At the end of discussion we found that the establishment of new lease

standards is benefitting the companies in improving their financial reporting standards.

14ACCOUNTING THEORY AND CURRENT ISSUES

References:

Baker, C. R., & Burlaud, A. (2015). The historical evolution from accounting theory to

conceptual framework in financial standards setting. The CPA Journal, 85(8), 54.

Barron, O. E., Chung, S. G., & Yong, K. O. (2016). The effect of Statement of Financial

Accounting Standards No. 157 Fair Value Measurements on analysts’ information

environment. Journal of Accounting and Public Policy, 35(4), 395-416.

Beaumont, S. J. (2015). An investigation of the short‐and long‐run relations between

executive cash bonus payments and firm financial performance: a pitch. Accounting

& Finance, 55(2), 337-343.

Bhp.com (2019). Retrieved from https://www.bhp.com/-/media/documents/investors/annual-

reports/2018/bhpannualreport2018.pdf

Campbell, J. L., Khan, U., & Pierce, S. (2018). The effect of mandatory disclosure on market

inefficiencies: Evidence from Statement of Financial Accounting Standard Number

161. Columbia Business School Research Paper, (17-94).

Chychyla, R., Leone, A. J., & Minutti-Meza, M. (2018). Complexity of financial reporting

standards and accounting expertise. Journal of Accounting and Economics.

Downs, L. C. (2017). Financial Accounting.

Dutta, S., & Patatoukas, P. N. (2016). Identifying conditional conservatism in financial

accounting data: theory and evidence. The Accounting Review, 92(4), 191-216.

Elliott, B. (2017). Financial Accounting and Reporting 18th Edition. Pearson Higher Ed.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

References:

Baker, C. R., & Burlaud, A. (2015). The historical evolution from accounting theory to

conceptual framework in financial standards setting. The CPA Journal, 85(8), 54.

Barron, O. E., Chung, S. G., & Yong, K. O. (2016). The effect of Statement of Financial

Accounting Standards No. 157 Fair Value Measurements on analysts’ information

environment. Journal of Accounting and Public Policy, 35(4), 395-416.

Beaumont, S. J. (2015). An investigation of the short‐and long‐run relations between

executive cash bonus payments and firm financial performance: a pitch. Accounting

& Finance, 55(2), 337-343.

Bhp.com (2019). Retrieved from https://www.bhp.com/-/media/documents/investors/annual-

reports/2018/bhpannualreport2018.pdf

Campbell, J. L., Khan, U., & Pierce, S. (2018). The effect of mandatory disclosure on market

inefficiencies: Evidence from Statement of Financial Accounting Standard Number

161. Columbia Business School Research Paper, (17-94).

Chychyla, R., Leone, A. J., & Minutti-Meza, M. (2018). Complexity of financial reporting

standards and accounting expertise. Journal of Accounting and Economics.

Downs, L. C. (2017). Financial Accounting.

Dutta, S., & Patatoukas, P. N. (2016). Identifying conditional conservatism in financial

accounting data: theory and evidence. The Accounting Review, 92(4), 191-216.

Elliott, B. (2017). Financial Accounting and Reporting 18th Edition. Pearson Higher Ed.

Henderson, S., Peirson, G., Herbohn, K., & Howieson, B. (2015). Issues in financial

accounting. Pearson Higher Education AU.

15ACCOUNTING THEORY AND CURRENT ISSUES

Hoitash, R., Hoitash, U., & Yezegel, A. (2017). The Effect of Accounting Reporting

Complexity on Financial Analysts.

Hoyle, J. B., Schaefer, T., & Doupnik, T. (2015). Advanced accounting. McGraw Hill.

Khan, M. (2015). Accounting: Financial. In Encyclopedia of Public Administration and

Public Policy, Third Edition-5 Volume Set (pp. 1-6). Routledge.

Klychova, G. S., Fakhretdinova, E. N., Klychova, A. S., & Antonova, N. V. (2015).

Development of accounting and financial reporting for small and medium-sized

businesses in accordance with international financial reporting standards. Asian

Social Science, 11(11), 318.

Lafond, C. A., McAleer, A. C., & Wentzel, K. (2016). Enhancing the Link between

Technology and Accounting in Introductory Courses: Evidence From

Students. Journal of the Academy of Business Education, 17.

Larson, M. P., Lewis, T. K., & Spilker, B. C. (2017). A case integrating financial and tax

accounting using the balance sheet approach to account for income taxes. Issues in

Accounting Education, 32(4), 41-49.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Mullinova, S. (2016). Use of the principles of IFRS (IAS) 39" Financial instruments:

recognition and assessment" for bank financial accounting. Modern European

Researches, (1), 60-64.

Schipper, K., Francis, J., & Weil, R. (2017). Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

Hoitash, R., Hoitash, U., & Yezegel, A. (2017). The Effect of Accounting Reporting

Complexity on Financial Analysts.

Hoyle, J. B., Schaefer, T., & Doupnik, T. (2015). Advanced accounting. McGraw Hill.

Khan, M. (2015). Accounting: Financial. In Encyclopedia of Public Administration and

Public Policy, Third Edition-5 Volume Set (pp. 1-6). Routledge.

Klychova, G. S., Fakhretdinova, E. N., Klychova, A. S., & Antonova, N. V. (2015).

Development of accounting and financial reporting for small and medium-sized

businesses in accordance with international financial reporting standards. Asian

Social Science, 11(11), 318.

Lafond, C. A., McAleer, A. C., & Wentzel, K. (2016). Enhancing the Link between

Technology and Accounting in Introductory Courses: Evidence From

Students. Journal of the Academy of Business Education, 17.

Larson, M. P., Lewis, T. K., & Spilker, B. C. (2017). A case integrating financial and tax

accounting using the balance sheet approach to account for income taxes. Issues in

Accounting Education, 32(4), 41-49.

Macve, R. (2015). A Conceptual Framework for Financial Accounting and Reporting:

Vision, Tool, Or Threat?. Routledge.

Mullinova, S. (2016). Use of the principles of IFRS (IAS) 39" Financial instruments:

recognition and assessment" for bank financial accounting. Modern European

Researches, (1), 60-64.

Schipper, K., Francis, J., & Weil, R. (2017). Financial Accounting: Introduction to Concepts,

Methods and Uses. Cengage Learning.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16ACCOUNTING THEORY AND CURRENT ISSUES

Stice, E. K., Stice, J. D., Albrecht, W. S., Swain, M. R., Duh, R. R., & Hsu, A. W. (2015).

Financial Accounting-IFRS Edition.

Stockenstrand, A. K., & Nilsson, F. (Eds.). (2017). Bank Regulation: Effects on Strategy,

Financial Accounting and Management Control (Vol. 19). Taylor & Francis.

Trotman, K., & Carson, E. (2018). Financial accounting: an integrated approach. Cengage

AU.

Warren, C., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

Stice, E. K., Stice, J. D., Albrecht, W. S., Swain, M. R., Duh, R. R., & Hsu, A. W. (2015).

Financial Accounting-IFRS Edition.

Stockenstrand, A. K., & Nilsson, F. (Eds.). (2017). Bank Regulation: Effects on Strategy,

Financial Accounting and Management Control (Vol. 19). Taylor & Francis.

Trotman, K., & Carson, E. (2018). Financial accounting: an integrated approach. Cengage

AU.

Warren, C., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.