Accounting Theory and Current Issues: Tutorial Questions Assignment

VerifiedAdded on 2023/01/06

|12

|2322

|78

Homework Assignment

AI Summary

This assignment provides solutions to tutorial questions covering various aspects of accounting theory and current issues. The content includes journal entries for machine revaluation, depreciation calculations, and the application of AASB 116. It also addresses the fair value of lease assets, including present value calculations, and explores topics such as weekly payroll and sick leave expenses. Furthermore, the assignment delves into Earnings Per Share (EPS) calculations, differentiating between basic and diluted EPS, and includes the preparation of journal entries for foreign currency transactions. Lastly, it examines Corporate Social Responsibility (CSR) and the legitimacy of companies.

Accounting Theory and

Current Issues

Current Issues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

QUESTION 3- Week 3...............................................................................................................................3

Provide journal entries necessary to account...........................................................................................3

QUESTION 2 – Week 5..............................................................................................................................5

Fair value of lease assets.........................................................................................................................5

QUESTION 2 – Week 6..............................................................................................................................6

QUESTION 3 – Week 9..............................................................................................................................8

(a) Basic EPS amount..............................................................................................................................8

QUESTION 3 – Week 10............................................................................................................................9

a. Exchange rates.....................................................................................................................................9

b. Prepare the journal entries...................................................................................................................9

QUESTION 3 – Week 11............................................................................................................................9

(a) Term of CSR......................................................................................................................................9

(b) Legitimacy of companies.................................................................................................................10

CONCLUSION.........................................................................................................................................11

REFERENCES..........................................................................................................................................12

INTRODUCTION.......................................................................................................................................3

QUESTION 3- Week 3...............................................................................................................................3

Provide journal entries necessary to account...........................................................................................3

QUESTION 2 – Week 5..............................................................................................................................5

Fair value of lease assets.........................................................................................................................5

QUESTION 2 – Week 6..............................................................................................................................6

QUESTION 3 – Week 9..............................................................................................................................8

(a) Basic EPS amount..............................................................................................................................8

QUESTION 3 – Week 10............................................................................................................................9

a. Exchange rates.....................................................................................................................................9

b. Prepare the journal entries...................................................................................................................9

QUESTION 3 – Week 11............................................................................................................................9

(a) Term of CSR......................................................................................................................................9

(b) Legitimacy of companies.................................................................................................................10

CONCLUSION.........................................................................................................................................11

REFERENCES..........................................................................................................................................12

INTRODUCTION

Accounting theory is a collection of concepts, structures and techniques used in the

analysis and implementation of financial reporting concepts. An analysis of both the traditional

principles and accounting standards in the manner of accounting practices which are altered and

applied to the legislative system. The regulating financial statements and financial reports are

subject of the research of accounting theory (Croes and Rivera, 2017). A guideline for efficient

accounting and auditing is given by accounting theory. The theory of accounting encompasses

the premises and techniques used in financial statements, including an analysis of accounting

rules and the review regime. In present time organizations face different issues in accounting like

tax cuts, traditional accounting and many others that impact on the business in adverse manner.

In this report consist of different questions related to accounting theory and related issues.

QUESTION 3- Week 3

Provide journal entries necessary to account

On 30th June, 2020:

Machine Cost: $650000

Accumulated Depreciation: $110000

Value after Revaluation: $450000

Useful Life of machine: 5 year

Residual Value: $50000

On 1st July 2023

Fair Value of Machine: $460000

Computation of value of machine and revolution effects:

Machine Cost 650000

Less: Accumulated 110000

Accounting theory is a collection of concepts, structures and techniques used in the

analysis and implementation of financial reporting concepts. An analysis of both the traditional

principles and accounting standards in the manner of accounting practices which are altered and

applied to the legislative system. The regulating financial statements and financial reports are

subject of the research of accounting theory (Croes and Rivera, 2017). A guideline for efficient

accounting and auditing is given by accounting theory. The theory of accounting encompasses

the premises and techniques used in financial statements, including an analysis of accounting

rules and the review regime. In present time organizations face different issues in accounting like

tax cuts, traditional accounting and many others that impact on the business in adverse manner.

In this report consist of different questions related to accounting theory and related issues.

QUESTION 3- Week 3

Provide journal entries necessary to account

On 30th June, 2020:

Machine Cost: $650000

Accumulated Depreciation: $110000

Value after Revaluation: $450000

Useful Life of machine: 5 year

Residual Value: $50000

On 1st July 2023

Fair Value of Machine: $460000

Computation of value of machine and revolution effects:

Machine Cost 650000

Less: Accumulated 110000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Depreciation

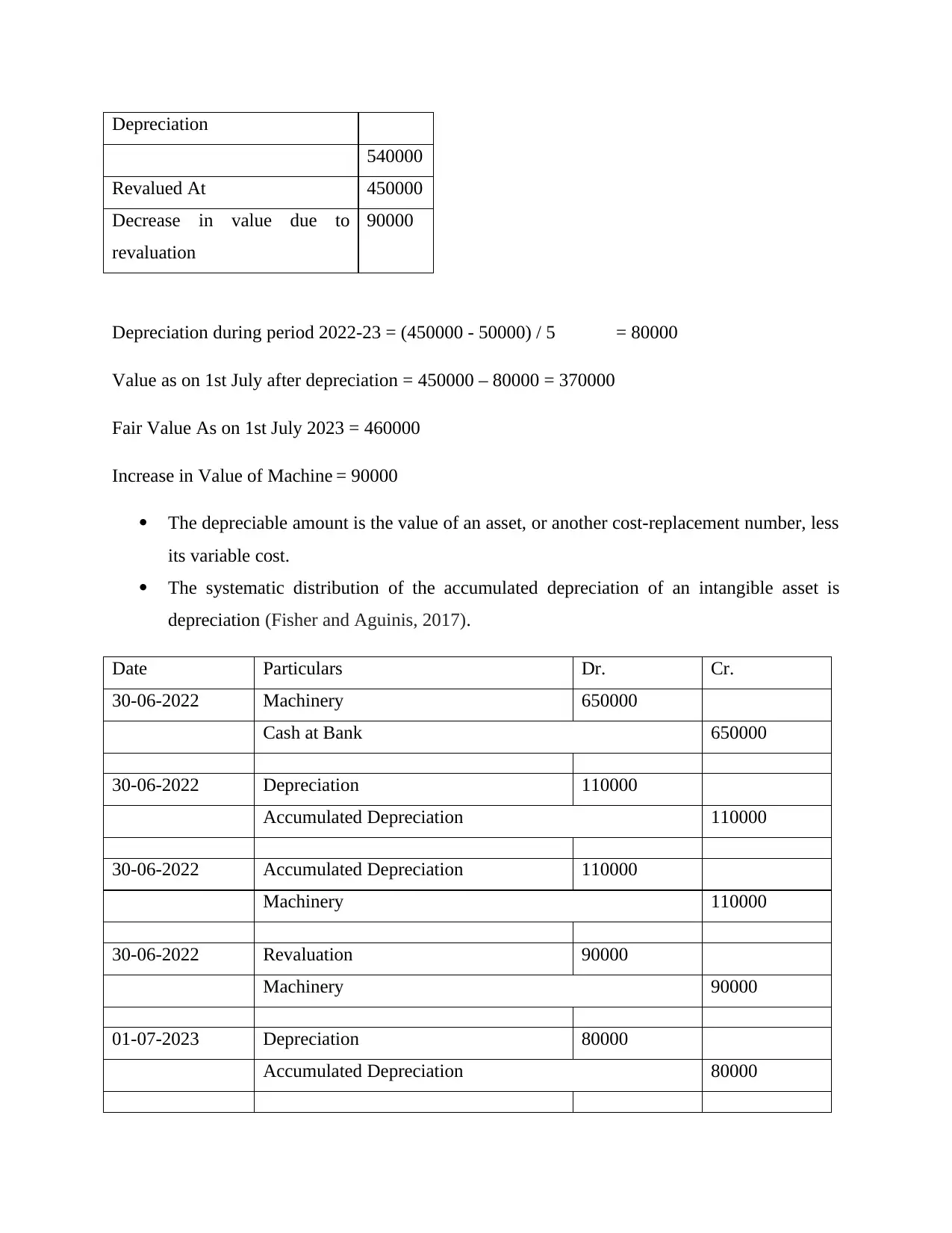

540000

Revalued At 450000

Decrease in value due to

revaluation

90000

Depreciation during period 2022-23 = (450000 - 50000) / 5 = 80000

Value as on 1st July after depreciation = 450000 – 80000 = 370000

Fair Value As on 1st July 2023 = 460000

Increase in Value of Machine = 90000

The depreciable amount is the value of an asset, or another cost-replacement number, less

its variable cost.

The systematic distribution of the accumulated depreciation of an intangible asset is

depreciation (Fisher and Aguinis, 2017).

Date Particulars Dr. Cr.

30-06-2022 Machinery 650000

Cash at Bank 650000

30-06-2022 Depreciation 110000

Accumulated Depreciation 110000

30-06-2022 Accumulated Depreciation 110000

Machinery 110000

30-06-2022 Revaluation 90000

Machinery 90000

01-07-2023 Depreciation 80000

Accumulated Depreciation 80000

540000

Revalued At 450000

Decrease in value due to

revaluation

90000

Depreciation during period 2022-23 = (450000 - 50000) / 5 = 80000

Value as on 1st July after depreciation = 450000 – 80000 = 370000

Fair Value As on 1st July 2023 = 460000

Increase in Value of Machine = 90000

The depreciable amount is the value of an asset, or another cost-replacement number, less

its variable cost.

The systematic distribution of the accumulated depreciation of an intangible asset is

depreciation (Fisher and Aguinis, 2017).

Date Particulars Dr. Cr.

30-06-2022 Machinery 650000

Cash at Bank 650000

30-06-2022 Depreciation 110000

Accumulated Depreciation 110000

30-06-2022 Accumulated Depreciation 110000

Machinery 110000

30-06-2022 Revaluation 90000

Machinery 90000

01-07-2023 Depreciation 80000

Accumulated Depreciation 80000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

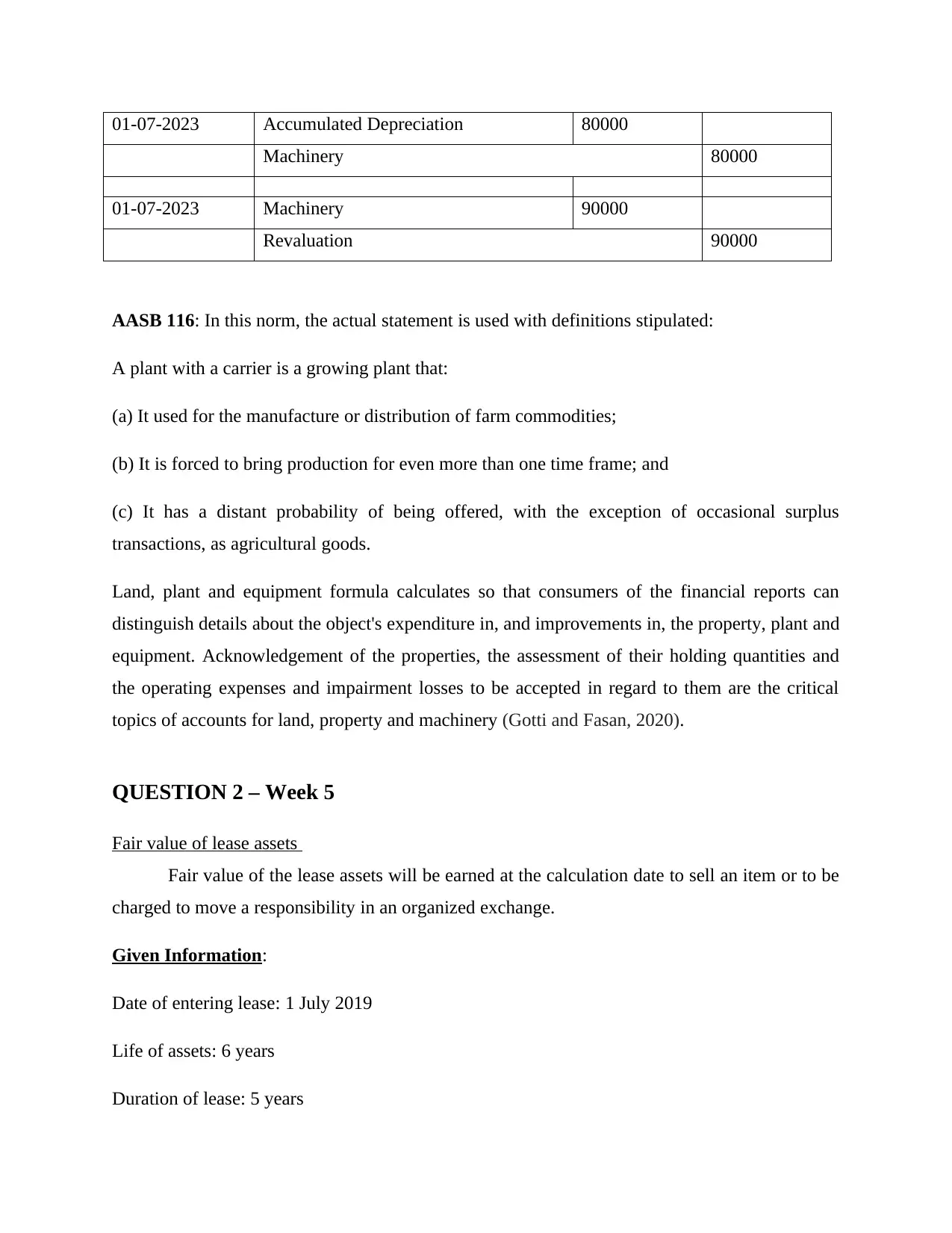

01-07-2023 Accumulated Depreciation 80000

Machinery 80000

01-07-2023 Machinery 90000

Revaluation 90000

AASB 116: In this norm, the actual statement is used with definitions stipulated:

A plant with a carrier is a growing plant that:

(a) It used for the manufacture or distribution of farm commodities;

(b) It is forced to bring production for even more than one time frame; and

(c) It has a distant probability of being offered, with the exception of occasional surplus

transactions, as agricultural goods.

Land, plant and equipment formula calculates so that consumers of the financial reports can

distinguish details about the object's expenditure in, and improvements in, the property, plant and

equipment. Acknowledgement of the properties, the assessment of their holding quantities and

the operating expenses and impairment losses to be accepted in regard to them are the critical

topics of accounts for land, property and machinery (Gotti and Fasan, 2020).

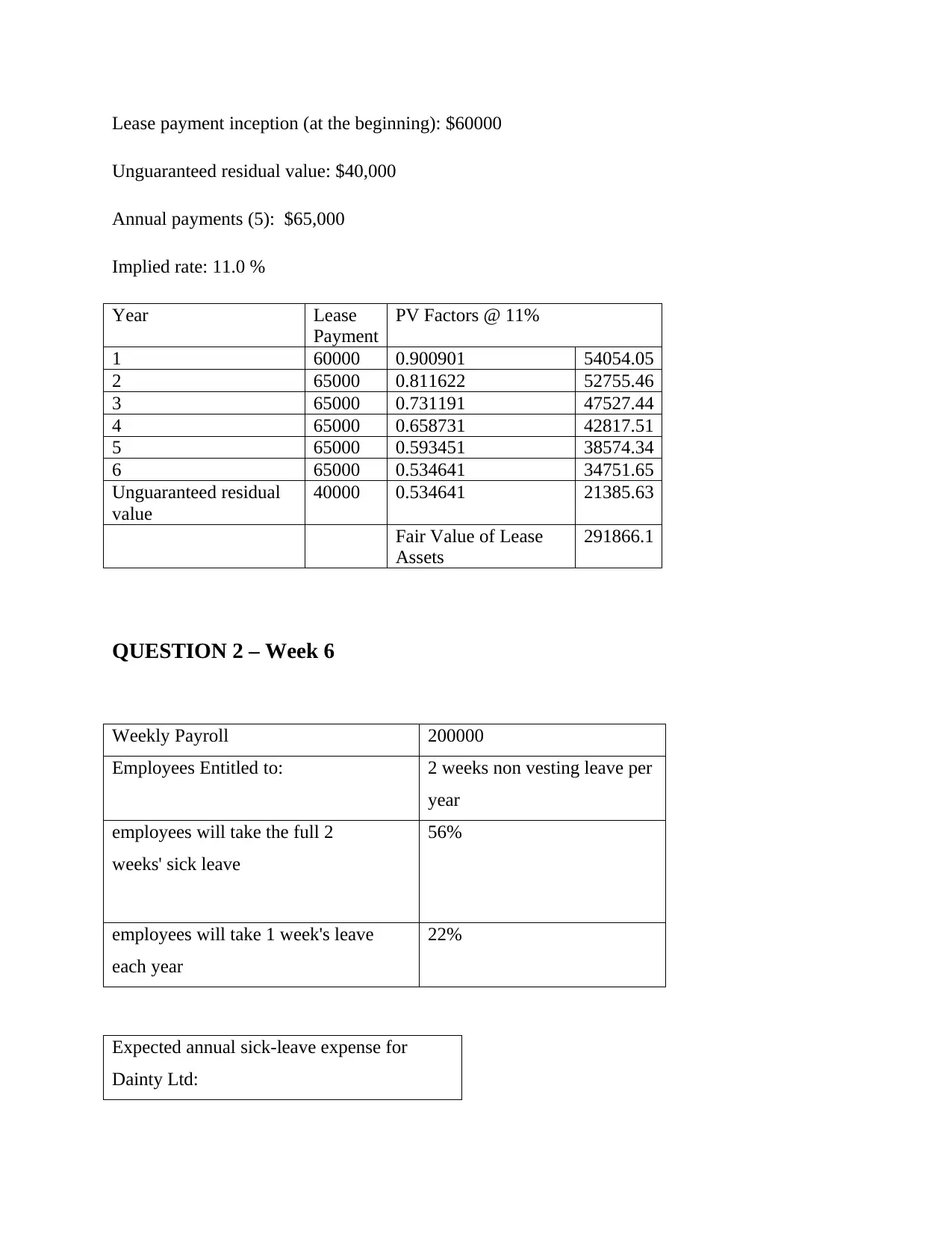

QUESTION 2 – Week 5

Fair value of lease assets

Fair value of the lease assets will be earned at the calculation date to sell an item or to be

charged to move a responsibility in an organized exchange.

Given Information:

Date of entering lease: 1 July 2019

Life of assets: 6 years

Duration of lease: 5 years

Machinery 80000

01-07-2023 Machinery 90000

Revaluation 90000

AASB 116: In this norm, the actual statement is used with definitions stipulated:

A plant with a carrier is a growing plant that:

(a) It used for the manufacture or distribution of farm commodities;

(b) It is forced to bring production for even more than one time frame; and

(c) It has a distant probability of being offered, with the exception of occasional surplus

transactions, as agricultural goods.

Land, plant and equipment formula calculates so that consumers of the financial reports can

distinguish details about the object's expenditure in, and improvements in, the property, plant and

equipment. Acknowledgement of the properties, the assessment of their holding quantities and

the operating expenses and impairment losses to be accepted in regard to them are the critical

topics of accounts for land, property and machinery (Gotti and Fasan, 2020).

QUESTION 2 – Week 5

Fair value of lease assets

Fair value of the lease assets will be earned at the calculation date to sell an item or to be

charged to move a responsibility in an organized exchange.

Given Information:

Date of entering lease: 1 July 2019

Life of assets: 6 years

Duration of lease: 5 years

Lease payment inception (at the beginning): $60000

Unguaranteed residual value: $40,000

Annual payments (5): $65,000

Implied rate: 11.0 %

Year Lease

Payment

PV Factors @ 11%

1 60000 0.900901 54054.05

2 65000 0.811622 52755.46

3 65000 0.731191 47527.44

4 65000 0.658731 42817.51

5 65000 0.593451 38574.34

6 65000 0.534641 34751.65

Unguaranteed residual

value

40000 0.534641 21385.63

Fair Value of Lease

Assets

291866.1

QUESTION 2 – Week 6

Weekly Payroll 200000

Employees Entitled to: 2 weeks non vesting leave per

year

employees will take the full 2

weeks' sick leave

56%

employees will take 1 week's leave

each year

22%

Expected annual sick-leave expense for

Dainty Ltd:

Unguaranteed residual value: $40,000

Annual payments (5): $65,000

Implied rate: 11.0 %

Year Lease

Payment

PV Factors @ 11%

1 60000 0.900901 54054.05

2 65000 0.811622 52755.46

3 65000 0.731191 47527.44

4 65000 0.658731 42817.51

5 65000 0.593451 38574.34

6 65000 0.534641 34751.65

Unguaranteed residual

value

40000 0.534641 21385.63

Fair Value of Lease

Assets

291866.1

QUESTION 2 – Week 6

Weekly Payroll 200000

Employees Entitled to: 2 weeks non vesting leave per

year

employees will take the full 2

weeks' sick leave

56%

employees will take 1 week's leave

each year

22%

Expected annual sick-leave expense for

Dainty Ltd:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

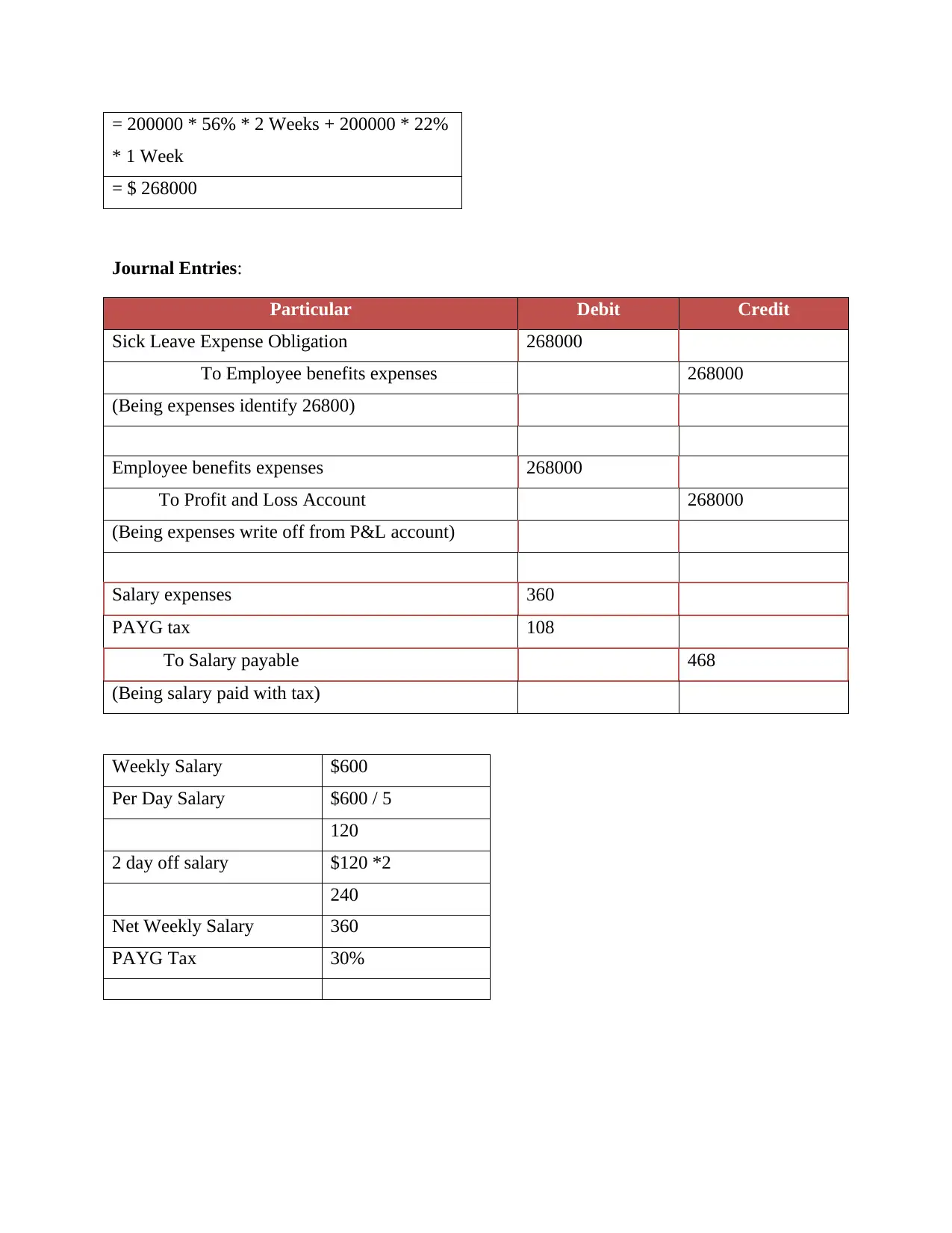

= 200000 * 56% * 2 Weeks + 200000 * 22%

* 1 Week

= $ 268000

Journal Entries:

Particular Debit Credit

Sick Leave Expense Obligation 268000

To Employee benefits expenses 268000

(Being expenses identify 26800)

Employee benefits expenses 268000

To Profit and Loss Account 268000

(Being expenses write off from P&L account)

Salary expenses 360

PAYG tax 108

To Salary payable 468

(Being salary paid with tax)

Weekly Salary $600

Per Day Salary $600 / 5

120

2 day off salary $120 *2

240

Net Weekly Salary 360

PAYG Tax 30%

* 1 Week

= $ 268000

Journal Entries:

Particular Debit Credit

Sick Leave Expense Obligation 268000

To Employee benefits expenses 268000

(Being expenses identify 26800)

Employee benefits expenses 268000

To Profit and Loss Account 268000

(Being expenses write off from P&L account)

Salary expenses 360

PAYG tax 108

To Salary payable 468

(Being salary paid with tax)

Weekly Salary $600

Per Day Salary $600 / 5

120

2 day off salary $120 *2

240

Net Weekly Salary 360

PAYG Tax 30%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

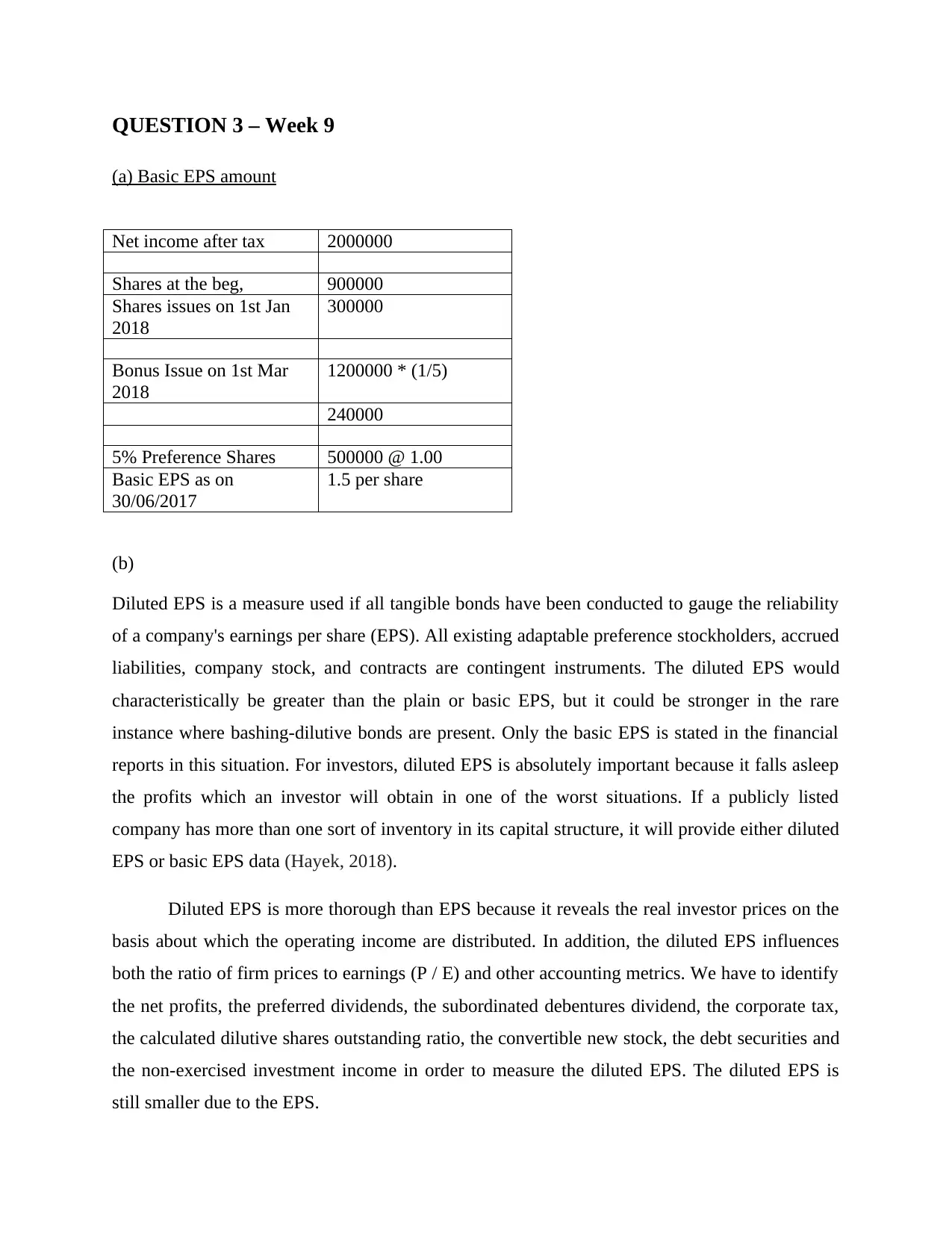

QUESTION 3 – Week 9

(a) Basic EPS amount

Net income after tax 2000000

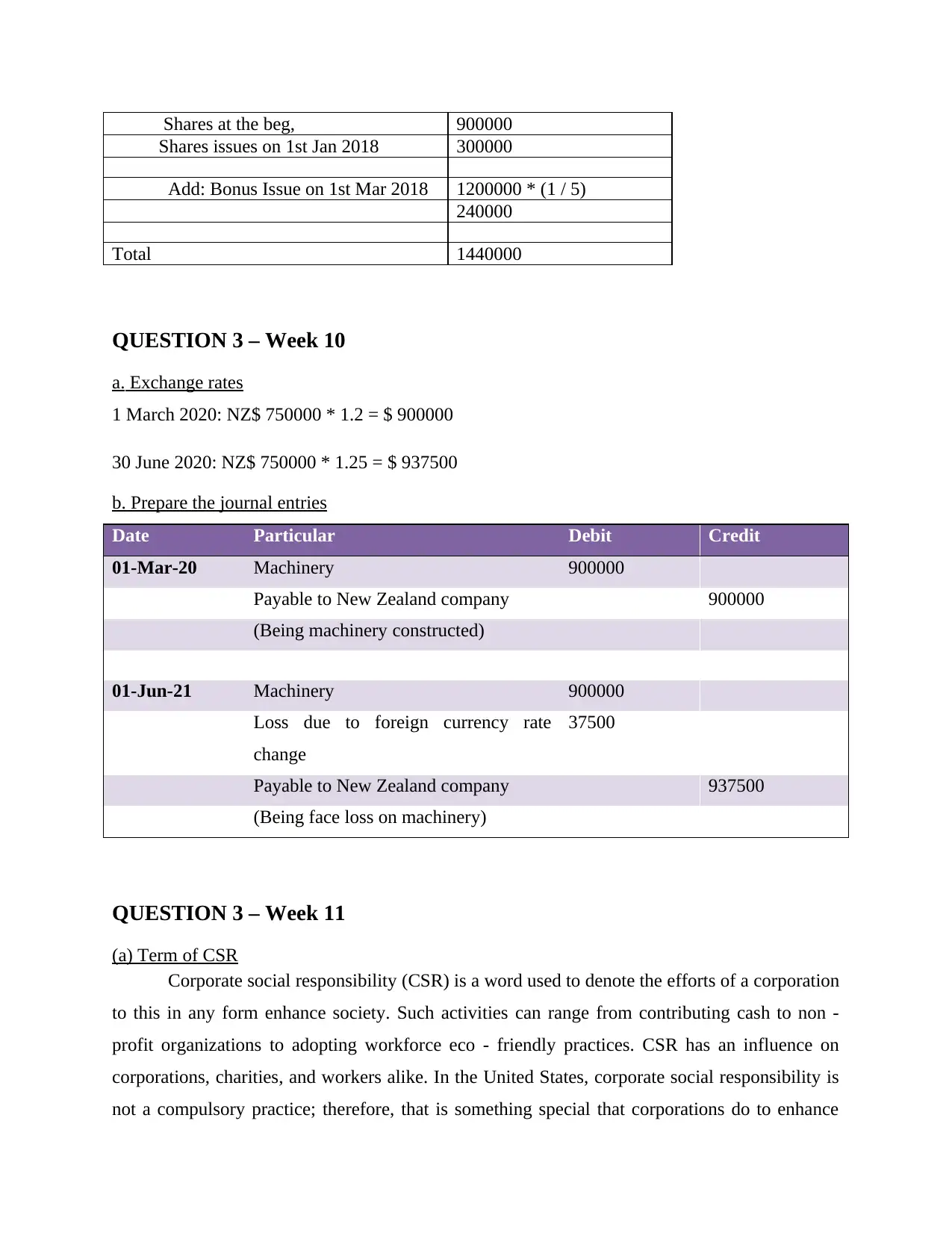

Shares at the beg, 900000

Shares issues on 1st Jan

2018

300000

Bonus Issue on 1st Mar

2018

1200000 * (1/5)

240000

5% Preference Shares 500000 @ 1.00

Basic EPS as on

30/06/2017

1.5 per share

(b)

Diluted EPS is a measure used if all tangible bonds have been conducted to gauge the reliability

of a company's earnings per share (EPS). All existing adaptable preference stockholders, accrued

liabilities, company stock, and contracts are contingent instruments. The diluted EPS would

characteristically be greater than the plain or basic EPS, but it could be stronger in the rare

instance where bashing-dilutive bonds are present. Only the basic EPS is stated in the financial

reports in this situation. For investors, diluted EPS is absolutely important because it falls asleep

the profits which an investor will obtain in one of the worst situations. If a publicly listed

company has more than one sort of inventory in its capital structure, it will provide either diluted

EPS or basic EPS data (Hayek, 2018).

Diluted EPS is more thorough than EPS because it reveals the real investor prices on the

basis about which the operating income are distributed. In addition, the diluted EPS influences

both the ratio of firm prices to earnings (P / E) and other accounting metrics. We have to identify

the net profits, the preferred dividends, the subordinated debentures dividend, the corporate tax,

the calculated dilutive shares outstanding ratio, the convertible new stock, the debt securities and

the non-exercised investment income in order to measure the diluted EPS. The diluted EPS is

still smaller due to the EPS.

(a) Basic EPS amount

Net income after tax 2000000

Shares at the beg, 900000

Shares issues on 1st Jan

2018

300000

Bonus Issue on 1st Mar

2018

1200000 * (1/5)

240000

5% Preference Shares 500000 @ 1.00

Basic EPS as on

30/06/2017

1.5 per share

(b)

Diluted EPS is a measure used if all tangible bonds have been conducted to gauge the reliability

of a company's earnings per share (EPS). All existing adaptable preference stockholders, accrued

liabilities, company stock, and contracts are contingent instruments. The diluted EPS would

characteristically be greater than the plain or basic EPS, but it could be stronger in the rare

instance where bashing-dilutive bonds are present. Only the basic EPS is stated in the financial

reports in this situation. For investors, diluted EPS is absolutely important because it falls asleep

the profits which an investor will obtain in one of the worst situations. If a publicly listed

company has more than one sort of inventory in its capital structure, it will provide either diluted

EPS or basic EPS data (Hayek, 2018).

Diluted EPS is more thorough than EPS because it reveals the real investor prices on the

basis about which the operating income are distributed. In addition, the diluted EPS influences

both the ratio of firm prices to earnings (P / E) and other accounting metrics. We have to identify

the net profits, the preferred dividends, the subordinated debentures dividend, the corporate tax,

the calculated dilutive shares outstanding ratio, the convertible new stock, the debt securities and

the non-exercised investment income in order to measure the diluted EPS. The diluted EPS is

still smaller due to the EPS.

,,,,,,,,,,,Shares at the beg, 900000

……..Shares issues on 1st Jan 2018 300000

………Add: Bonus Issue on 1st Mar 2018 1200000 * (1 / 5)

240000

Total 1440000

QUESTION 3 – Week 10

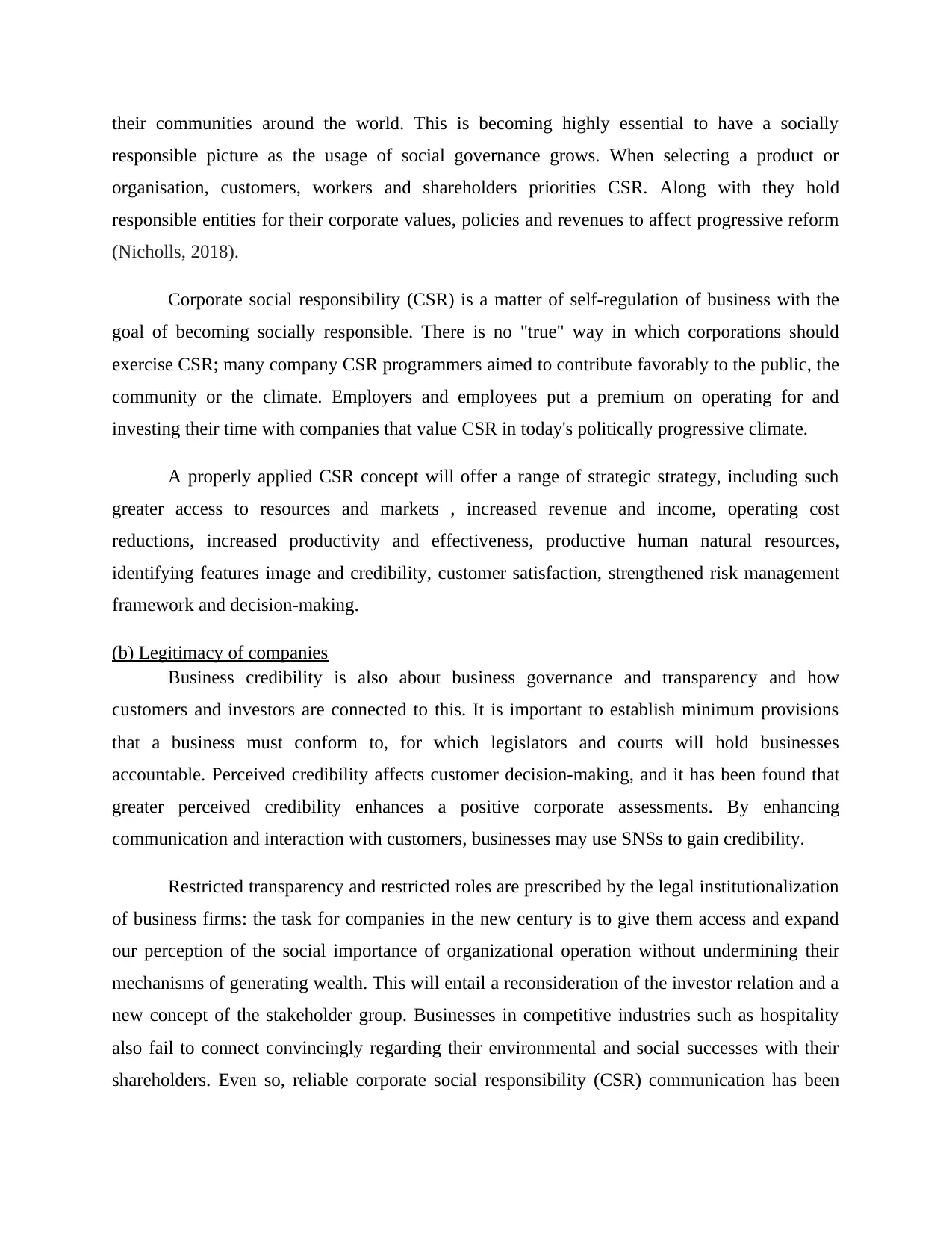

a. Exchange rates

1 March 2020: NZ$ 750000 * 1.2 = $ 900000

30 June 2020: NZ$ 750000 * 1.25 = $ 937500

b. Prepare the journal entries

Date Particular Debit Credit

01-Mar-20 Machinery 900000

Payable to New Zealand company 900000

(Being machinery constructed)

01-Jun-21 Machinery 900000

Loss due to foreign currency rate

change

37500

Payable to New Zealand company 937500

(Being face loss on machinery)

QUESTION 3 – Week 11

(a) Term of CSR

Corporate social responsibility (CSR) is a word used to denote the efforts of a corporation

to this in any form enhance society. Such activities can range from contributing cash to non -

profit organizations to adopting workforce eco - friendly practices. CSR has an influence on

corporations, charities, and workers alike. In the United States, corporate social responsibility is

not a compulsory practice; therefore, that is something special that corporations do to enhance

……..Shares issues on 1st Jan 2018 300000

………Add: Bonus Issue on 1st Mar 2018 1200000 * (1 / 5)

240000

Total 1440000

QUESTION 3 – Week 10

a. Exchange rates

1 March 2020: NZ$ 750000 * 1.2 = $ 900000

30 June 2020: NZ$ 750000 * 1.25 = $ 937500

b. Prepare the journal entries

Date Particular Debit Credit

01-Mar-20 Machinery 900000

Payable to New Zealand company 900000

(Being machinery constructed)

01-Jun-21 Machinery 900000

Loss due to foreign currency rate

change

37500

Payable to New Zealand company 937500

(Being face loss on machinery)

QUESTION 3 – Week 11

(a) Term of CSR

Corporate social responsibility (CSR) is a word used to denote the efforts of a corporation

to this in any form enhance society. Such activities can range from contributing cash to non -

profit organizations to adopting workforce eco - friendly practices. CSR has an influence on

corporations, charities, and workers alike. In the United States, corporate social responsibility is

not a compulsory practice; therefore, that is something special that corporations do to enhance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

their communities around the world. This is becoming highly essential to have a socially

responsible picture as the usage of social governance grows. When selecting a product or

organisation, customers, workers and shareholders priorities CSR. Along with they hold

responsible entities for their corporate values, policies and revenues to affect progressive reform

(Nicholls, 2018).

Corporate social responsibility (CSR) is a matter of self-regulation of business with the

goal of becoming socially responsible. There is no "true" way in which corporations should

exercise CSR; many company CSR programmers aimed to contribute favorably to the public, the

community or the climate. Employers and employees put a premium on operating for and

investing their time with companies that value CSR in today's politically progressive climate.

A properly applied CSR concept will offer a range of strategic strategy, including such

greater access to resources and markets , increased revenue and income, operating cost

reductions, increased productivity and effectiveness, productive human natural resources,

identifying features image and credibility, customer satisfaction, strengthened risk management

framework and decision-making.

(b) Legitimacy of companies

Business credibility is also about business governance and transparency and how

customers and investors are connected to this. It is important to establish minimum provisions

that a business must conform to, for which legislators and courts will hold businesses

accountable. Perceived credibility affects customer decision-making, and it has been found that

greater perceived credibility enhances a positive corporate assessments. By enhancing

communication and interaction with customers, businesses may use SNSs to gain credibility.

Restricted transparency and restricted roles are prescribed by the legal institutionalization

of business firms: the task for companies in the new century is to give them access and expand

our perception of the social importance of organizational operation without undermining their

mechanisms of generating wealth. This will entail a reconsideration of the investor relation and a

new concept of the stakeholder group. Businesses in competitive industries such as hospitality

also fail to connect convincingly regarding their environmental and social successes with their

shareholders. Even so, reliable corporate social responsibility (CSR) communication has been

responsible picture as the usage of social governance grows. When selecting a product or

organisation, customers, workers and shareholders priorities CSR. Along with they hold

responsible entities for their corporate values, policies and revenues to affect progressive reform

(Nicholls, 2018).

Corporate social responsibility (CSR) is a matter of self-regulation of business with the

goal of becoming socially responsible. There is no "true" way in which corporations should

exercise CSR; many company CSR programmers aimed to contribute favorably to the public, the

community or the climate. Employers and employees put a premium on operating for and

investing their time with companies that value CSR in today's politically progressive climate.

A properly applied CSR concept will offer a range of strategic strategy, including such

greater access to resources and markets , increased revenue and income, operating cost

reductions, increased productivity and effectiveness, productive human natural resources,

identifying features image and credibility, customer satisfaction, strengthened risk management

framework and decision-making.

(b) Legitimacy of companies

Business credibility is also about business governance and transparency and how

customers and investors are connected to this. It is important to establish minimum provisions

that a business must conform to, for which legislators and courts will hold businesses

accountable. Perceived credibility affects customer decision-making, and it has been found that

greater perceived credibility enhances a positive corporate assessments. By enhancing

communication and interaction with customers, businesses may use SNSs to gain credibility.

Restricted transparency and restricted roles are prescribed by the legal institutionalization

of business firms: the task for companies in the new century is to give them access and expand

our perception of the social importance of organizational operation without undermining their

mechanisms of generating wealth. This will entail a reconsideration of the investor relation and a

new concept of the stakeholder group. Businesses in competitive industries such as hospitality

also fail to connect convincingly regarding their environmental and social successes with their

shareholders. Even so, reliable corporate social responsibility (CSR) communication has been

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

developing theory, but never implementation of sustainable, as an indicator of credibility for

organizations in society. The aim of this paper is to assess a CSR website's trustworthiness as a

primary indicator of validity (rational, mental and moral) digital and analog.

CONCLUSION

As per above discussion it has been concluded that the conceptual system of accounting

theory is connected by all concepts of accounting. This structure is established by the Financial

Accounting Principles Board (FASB), an autonomous body working to formulate and evaluate

the main goals of governmental and corporate enterprises' financial reporting. In addition,

accounting theory can be considered to be the rational rationale that helps analyze accounting

practices and direct them. Accounting theory will help establish new business practices and

techniques as legislative requirements change.

organizations in society. The aim of this paper is to assess a CSR website's trustworthiness as a

primary indicator of validity (rational, mental and moral) digital and analog.

CONCLUSION

As per above discussion it has been concluded that the conceptual system of accounting

theory is connected by all concepts of accounting. This structure is established by the Financial

Accounting Principles Board (FASB), an autonomous body working to formulate and evaluate

the main goals of governmental and corporate enterprises' financial reporting. In addition,

accounting theory can be considered to be the rational rationale that helps analyze accounting

practices and direct them. Accounting theory will help establish new business practices and

techniques as legislative requirements change.

REFERENCES

Books and Journal

Croes, R. and Rivera, M. A., 2017. Tourism’s potential to benefit the poor: A social accounting

matrix model applied to Ecuador. Tourism Economics. 23(1). pp.29-48.

De Villiers, C., Venter, E. R. and Hsiao, P. C. K., 2017. Integrated reporting: background,

measurement issues, approaches and an agenda for future research. Accounting &

Finance. 57(4). pp.937-959.

Fisher, G. and Aguinis, H., 2017. Using theory elaboration to make theoretical

advancements. Organizational Research Methods. 20(3). pp.438-464.

Gotti, G. and Fasan, M., 2020. International Accounting Research: The Italian Context. Journal

of International Accounting Research. 19(1). pp.73-83.

Hayek, C. C., 2018. The State of the Literature on Audit Committee Compensation and Its

Implications for Practice and Research. Current Issues in Auditing. 12(2). pp.A1-A11.

Jones, J. P., Long, J. H. and Stanley, J. D., 2019. Pane in the Glass: A Review of the Accounting

Cycle. Issues in Accounting Education. 34(1). pp.35-50.

Nicholls, A., 2018. A general theory of social impact accounting: Materiality, uncertainty and

empowerment. Journal of Social Entrepreneurship. 9(2). pp.132-153.

Simon, C. A., Smith, J. L. and Zimbelman, M. F., 2020. How Fraud Risk Decomposition Affects

Auditors' Fraud Risk Assessments. Current Issues in Auditing. 14(1). pp.P26-P32.

Zeff, S. A., 2019. A Personal View of the Evolution of the Accounting Professoriate. Accounting

Perspectives. 18(3). pp.159-185.

Books and Journal

Croes, R. and Rivera, M. A., 2017. Tourism’s potential to benefit the poor: A social accounting

matrix model applied to Ecuador. Tourism Economics. 23(1). pp.29-48.

De Villiers, C., Venter, E. R. and Hsiao, P. C. K., 2017. Integrated reporting: background,

measurement issues, approaches and an agenda for future research. Accounting &

Finance. 57(4). pp.937-959.

Fisher, G. and Aguinis, H., 2017. Using theory elaboration to make theoretical

advancements. Organizational Research Methods. 20(3). pp.438-464.

Gotti, G. and Fasan, M., 2020. International Accounting Research: The Italian Context. Journal

of International Accounting Research. 19(1). pp.73-83.

Hayek, C. C., 2018. The State of the Literature on Audit Committee Compensation and Its

Implications for Practice and Research. Current Issues in Auditing. 12(2). pp.A1-A11.

Jones, J. P., Long, J. H. and Stanley, J. D., 2019. Pane in the Glass: A Review of the Accounting

Cycle. Issues in Accounting Education. 34(1). pp.35-50.

Nicholls, A., 2018. A general theory of social impact accounting: Materiality, uncertainty and

empowerment. Journal of Social Entrepreneurship. 9(2). pp.132-153.

Simon, C. A., Smith, J. L. and Zimbelman, M. F., 2020. How Fraud Risk Decomposition Affects

Auditors' Fraud Risk Assessments. Current Issues in Auditing. 14(1). pp.P26-P32.

Zeff, S. A., 2019. A Personal View of the Evolution of the Accounting Professoriate. Accounting

Perspectives. 18(3). pp.159-185.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.