Accounting Theory and Practice: IFRS Adoption in Australia Analysis

VerifiedAdded on 2021/05/30

|17

|3929

|38

Report

AI Summary

This report examines the impact of the adoption of International Financial Reporting Standards (IFRS) on Australian accounting practices, with a specific focus on the retail giant Wesfarmers. The analysis covers the transition from Australian Generally Accepted Accounting Principles (AGAAP) to IFRS, comparing financial statements from pre- and post-IFRS periods (2003 and 2007). The report delves into four major implications of IFRS adoption: the preparation of consolidated financial statements, changes in business combinations, impairment of assets, and the recognition and measurement of financial instruments. It highlights the creation of a project team by Wesfarmers to ensure a smooth transition. The report details the changes in accounting treatment for goodwill, restructuring provisions, and the assessment of asset impairment. Furthermore, it compiles the contributions of IFRS adoption, emphasizing how the implementation has affected the financial reporting landscape and improved comparability across sectors and countries. The report also covers the impact of IFRS on Wesfarmers' key financial indicators in its energy section.

Running head: ACCOUNTING THEORY AND PRACTICE

Name of the Student

Name of the University

Author note

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND PRACTICE

Executive Summary:

The adoption of the International Financial reporting Standards have been a debate of

international controversy and debates for a long period of time. This has been one of the most

controversial elements in the financial accounting and reporting world. It has been thirteen

long years since the adoption of the standards in the country of Australia. Numerous

researches have been done about the relative advantages and the disadvantages provided by

the adoption of the IFRS standards. In this project report, the major implications of the

adoption of the international accounting standards in the Australian context have been done.

This analysis and the reporting of the major implications of the standards have been done in

the context of the annual reports of the famous retail giant of Australia, Wesfarmers. Along

with statement and the explanation of the different changes and the past policies of the

different accounting practices has been done. In association with this, a compilation of the

contribution of this adoption has also been presented.

Executive Summary:

The adoption of the International Financial reporting Standards have been a debate of

international controversy and debates for a long period of time. This has been one of the most

controversial elements in the financial accounting and reporting world. It has been thirteen

long years since the adoption of the standards in the country of Australia. Numerous

researches have been done about the relative advantages and the disadvantages provided by

the adoption of the IFRS standards. In this project report, the major implications of the

adoption of the international accounting standards in the Australian context have been done.

This analysis and the reporting of the major implications of the standards have been done in

the context of the annual reports of the famous retail giant of Australia, Wesfarmers. Along

with statement and the explanation of the different changes and the past policies of the

different accounting practices has been done. In association with this, a compilation of the

contribution of this adoption has also been presented.

2ACCOUNTING THEORY AND PRACTICE

Table of Contents

Four Major Implications of International Accounting:..............................................................3

Background of IFRS:.............................................................................................................3

Wesfarmers: A Brief Overview:............................................................................................5

Preparation for the accounting changes by Wesfarmers:.......................................................6

Preparation of the consolidated financial statements......................................................7

Business Combinations:..................................................................................................8

Impairment of Assets......................................................................................................9

Recognition and measurement of the financial instruments of Wesfarmers.................10

Contribution of IFRS adoption:...............................................................................................13

References:...............................................................................................................................15

Table of Contents

Four Major Implications of International Accounting:..............................................................3

Background of IFRS:.............................................................................................................3

Wesfarmers: A Brief Overview:............................................................................................5

Preparation for the accounting changes by Wesfarmers:.......................................................6

Preparation of the consolidated financial statements......................................................7

Business Combinations:..................................................................................................8

Impairment of Assets......................................................................................................9

Recognition and measurement of the financial instruments of Wesfarmers.................10

Contribution of IFRS adoption:...............................................................................................13

References:...............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND PRACTICE

Four Major Implications of International Accounting:

Background of IFRS:

The adoption of the International Financial Accounting Standards had long been

engaged in major debates and discussions across panel of accounting experts, finance experts

ranging from various countries. The adoption of IFRS and its implications had caused a huge

uproar in the Australian financial market and among the government as well as to both the

public as well as the private sector players. The Australian companies as well as the other

business entities in the country had adopted the IFRS in the year 2005 from 1St January. Since

then, there have been endless debates about its relative importance, advantages and

disadvantages. Since then, ten years have passed and the AASB started reviewing the entire

implementation process since the year 2005 and some important points had been pointed out

since then (Healy and Whalen. 2000). The report has concluded that the transition process has

been really smooth and effective, the adoption of IFRS principles of accounting has provided

many advantages to the Australian companies in many ways, most notably by enabling the

financial statements as well as their creators and users to move across sectors as well as

countries for comparison purposes. Moreover, the preparation of the financial statements in

accordance with the new principles of IFRS has been cost saving. Thus, as can be seen that

there are many advantages which has been provided to the users and the creators of the

financial statements. In this report, the impact of the adoption of the new accounting policies

such as the IFRS on the accounting policies of Australia like the AGAAP has been provided

and discussed. The impact has been shown by comparing the financial performance and

annual reports of two different years of a particular Australian company. In this case, the two

periods which have been chosen are 2003 (Pre-IFRS) and 2007 (Post-IFRS).

Four Major Implications of International Accounting:

Background of IFRS:

The adoption of the International Financial Accounting Standards had long been

engaged in major debates and discussions across panel of accounting experts, finance experts

ranging from various countries. The adoption of IFRS and its implications had caused a huge

uproar in the Australian financial market and among the government as well as to both the

public as well as the private sector players. The Australian companies as well as the other

business entities in the country had adopted the IFRS in the year 2005 from 1St January. Since

then, there have been endless debates about its relative importance, advantages and

disadvantages. Since then, ten years have passed and the AASB started reviewing the entire

implementation process since the year 2005 and some important points had been pointed out

since then (Healy and Whalen. 2000). The report has concluded that the transition process has

been really smooth and effective, the adoption of IFRS principles of accounting has provided

many advantages to the Australian companies in many ways, most notably by enabling the

financial statements as well as their creators and users to move across sectors as well as

countries for comparison purposes. Moreover, the preparation of the financial statements in

accordance with the new principles of IFRS has been cost saving. Thus, as can be seen that

there are many advantages which has been provided to the users and the creators of the

financial statements. In this report, the impact of the adoption of the new accounting policies

such as the IFRS on the accounting policies of Australia like the AGAAP has been provided

and discussed. The impact has been shown by comparing the financial performance and

annual reports of two different years of a particular Australian company. In this case, the two

periods which have been chosen are 2003 (Pre-IFRS) and 2007 (Post-IFRS).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND PRACTICE

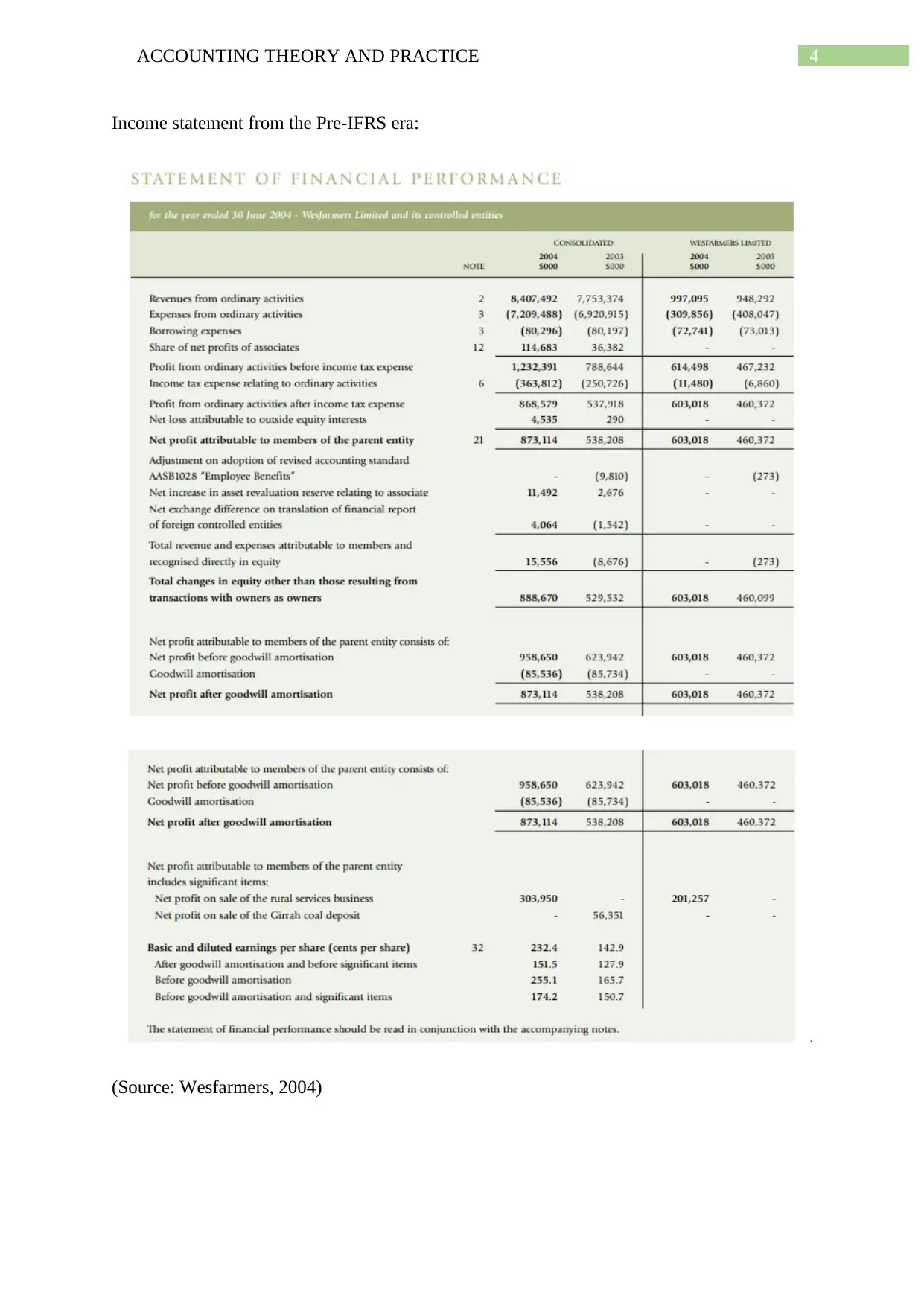

Income statement from the Pre-IFRS era:

(Source: Wesfarmers, 2004)

Income statement from the Pre-IFRS era:

(Source: Wesfarmers, 2004)

5ACCOUNTING THEORY AND PRACTICE

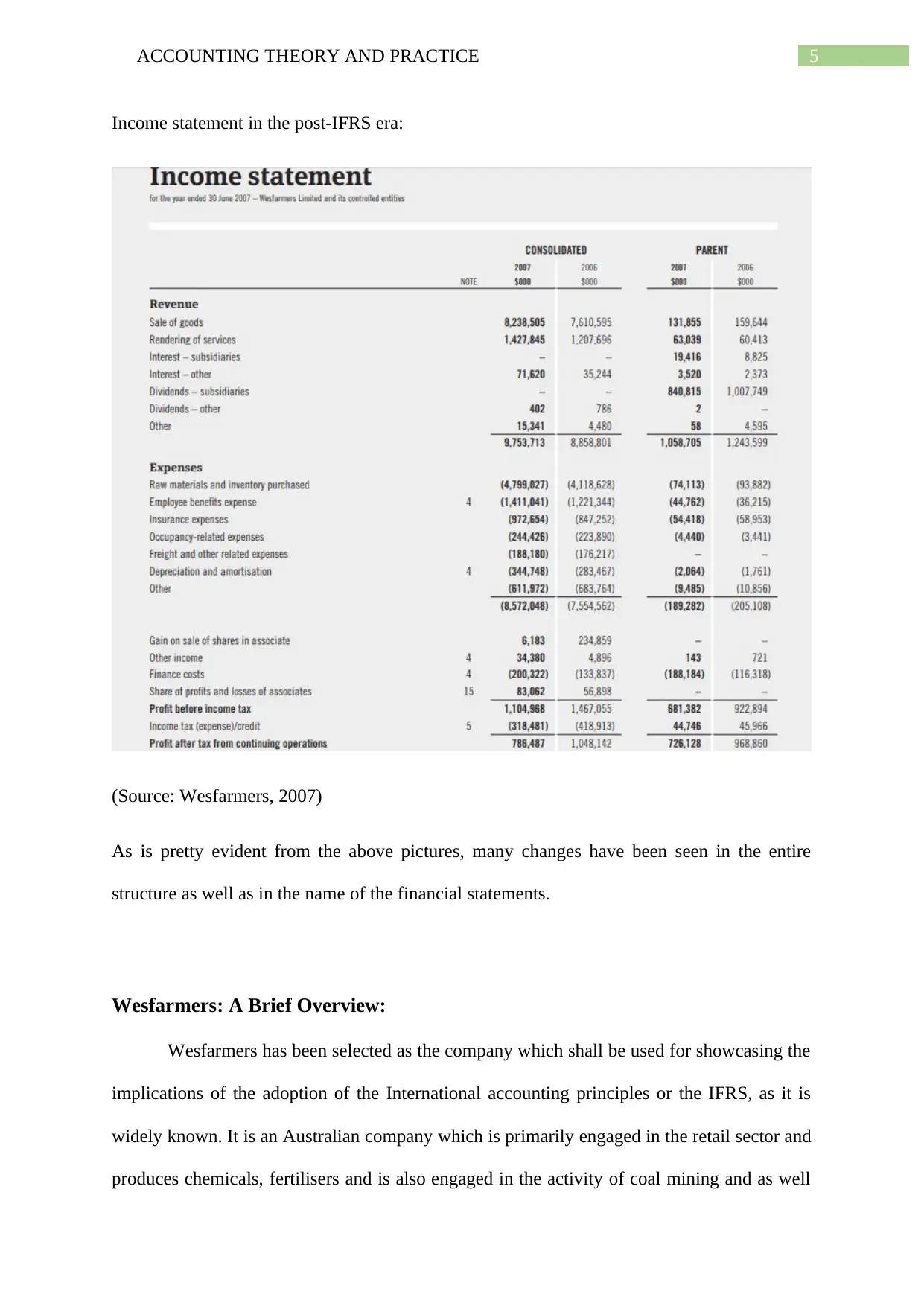

Income statement in the post-IFRS era:

(Source: Wesfarmers, 2007)

As is pretty evident from the above pictures, many changes have been seen in the entire

structure as well as in the name of the financial statements.

Wesfarmers: A Brief Overview:

Wesfarmers has been selected as the company which shall be used for showcasing the

implications of the adoption of the International accounting principles or the IFRS, as it is

widely known. It is an Australian company which is primarily engaged in the retail sector and

produces chemicals, fertilisers and is also engaged in the activity of coal mining and as well

Income statement in the post-IFRS era:

(Source: Wesfarmers, 2007)

As is pretty evident from the above pictures, many changes have been seen in the entire

structure as well as in the name of the financial statements.

Wesfarmers: A Brief Overview:

Wesfarmers has been selected as the company which shall be used for showcasing the

implications of the adoption of the International accounting principles or the IFRS, as it is

widely known. It is an Australian company which is primarily engaged in the retail sector and

produces chemicals, fertilisers and is also engaged in the activity of coal mining and as well

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND PRACTICE

as in the production of industrial as well as safety products. It is the largest company in the

Australian sub-continent in terms of revenue. It was one of the first companies in the island

continent to support the need and the implementation of an international accounting system.

It needed a uniform accounting principle in order to enable the users as well as the creators of

the financial statements in order to ensure the comparison of the financial statements.

Preparation for the accounting changes by Wesfarmers:

In order to ensure a smooth and effective transition from the AGAAP accounting

principles to the IFRS principles, certain important steps had been taken by the management

of Wesfarmers. These steps have been designed to ensure a smooth and effective transition

into the new accounting standards of IFRS. Some of these prominent measures have been

discussed below:

1. Creation of a Project team, which would primarily deal with the entire conversion

process from the previous standards to the IFRS standards.

2. The Project team would consist of a Project Sponsor, a Steering Committee, a full

time Project Accountant and a Project Working Party (Wesfarmers.com.au, 2018).

3. The Project Accountant along with the working party members along with the support

and the essential guidance from the steering committee would assess the impact the

adoption of the new IFRS principles and standards on the training systems, internal

control structure, financial reporting and the accounting policies of the company.

4. Thereafter the issues and the problems with the new standards would be identified and

a project report would be prepared, which would be sent to the Audit committee of the

company for the purpose deciding on the future course of action.

5. Thereafter, the Audit committee would then take the matter to the senior

management, in order to provide the relative guidance for the creation of the relevant

as in the production of industrial as well as safety products. It is the largest company in the

Australian sub-continent in terms of revenue. It was one of the first companies in the island

continent to support the need and the implementation of an international accounting system.

It needed a uniform accounting principle in order to enable the users as well as the creators of

the financial statements in order to ensure the comparison of the financial statements.

Preparation for the accounting changes by Wesfarmers:

In order to ensure a smooth and effective transition from the AGAAP accounting

principles to the IFRS principles, certain important steps had been taken by the management

of Wesfarmers. These steps have been designed to ensure a smooth and effective transition

into the new accounting standards of IFRS. Some of these prominent measures have been

discussed below:

1. Creation of a Project team, which would primarily deal with the entire conversion

process from the previous standards to the IFRS standards.

2. The Project team would consist of a Project Sponsor, a Steering Committee, a full

time Project Accountant and a Project Working Party (Wesfarmers.com.au, 2018).

3. The Project Accountant along with the working party members along with the support

and the essential guidance from the steering committee would assess the impact the

adoption of the new IFRS principles and standards on the training systems, internal

control structure, financial reporting and the accounting policies of the company.

4. Thereafter the issues and the problems with the new standards would be identified and

a project report would be prepared, which would be sent to the Audit committee of the

company for the purpose deciding on the future course of action.

5. Thereafter, the Audit committee would then take the matter to the senior

management, in order to provide the relative guidance for the creation of the relevant

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND PRACTICE

changes for the proper implementation of the new rules as proposed by the IFRS

principles.

6. Thereafter as per the changes and the reconsideration in case of some major

implications, by the senior management of the company, the resultant standards of the

IFRS would be adopted and consequently implemented by the company.

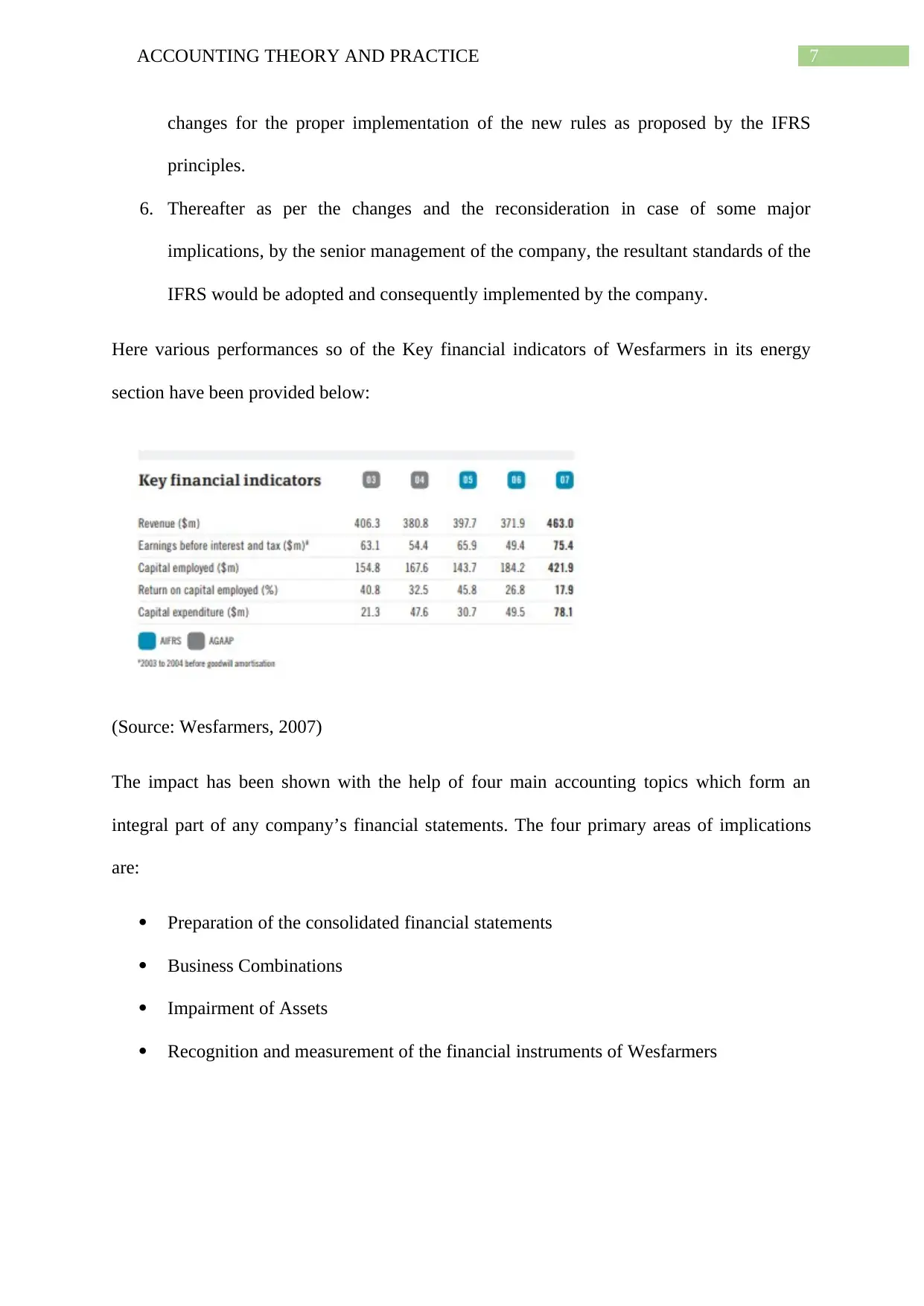

Here various performances so of the Key financial indicators of Wesfarmers in its energy

section have been provided below:

(Source: Wesfarmers, 2007)

The impact has been shown with the help of four main accounting topics which form an

integral part of any company’s financial statements. The four primary areas of implications

are:

Preparation of the consolidated financial statements

Business Combinations

Impairment of Assets

Recognition and measurement of the financial instruments of Wesfarmers

changes for the proper implementation of the new rules as proposed by the IFRS

principles.

6. Thereafter as per the changes and the reconsideration in case of some major

implications, by the senior management of the company, the resultant standards of the

IFRS would be adopted and consequently implemented by the company.

Here various performances so of the Key financial indicators of Wesfarmers in its energy

section have been provided below:

(Source: Wesfarmers, 2007)

The impact has been shown with the help of four main accounting topics which form an

integral part of any company’s financial statements. The four primary areas of implications

are:

Preparation of the consolidated financial statements

Business Combinations

Impairment of Assets

Recognition and measurement of the financial instruments of Wesfarmers

8ACCOUNTING THEORY AND PRACTICE

Each of the implications of the adoption of the IFRS on each of these portions have been

discussed below with the help of the annual reports and the financial statements of the

company of Wesfarmers. The implications are as follows:

Preparation of the consolidated financial statements: One of the most

important aspects of the adoption of the international accounting statements has been

on the preparation of the financial statements. In accordance with the relevant

principles of the IFRS, it is mandatorily required by the companies operating in the

Australian economy, to prepare consolidated financial statements. It is required to be

prepared for those companies, which have a holding interest in the shares and in the

management of any other company (Daske et al., 2013). This company acts as the

subsidiary of the parent company. In this case, the subsidiary company becomes a part

of the parent company. Thus, in this case, it is mandatorily required by the company

officials or the finance officials of Wesfarmers as well as of other companies who

have such a situation to prepare a consolidated financial statement. The companies or

the consolidated entities in accordance with the provisions of the IFRS, would be

required to prepare an opening balance sheet, along with the majority of restatement

adjustments, to be made, against the opening retained earnings. The presentation of

the financial statements of the company have also undergone a slight change and to

explain it better a pre and post picture of some of the important financial statements of

the Wesfarmers has been provided below:

Business Combinations: There has been a vast amount of changes in the scenario

of business combinations and according to the audit committee of Wesfarmers, the

following changes have been seen or are yet to be felt. In the case of business

combination, the change has mostly been seen in the treatment of goodwill. In the

Each of the implications of the adoption of the IFRS on each of these portions have been

discussed below with the help of the annual reports and the financial statements of the

company of Wesfarmers. The implications are as follows:

Preparation of the consolidated financial statements: One of the most

important aspects of the adoption of the international accounting statements has been

on the preparation of the financial statements. In accordance with the relevant

principles of the IFRS, it is mandatorily required by the companies operating in the

Australian economy, to prepare consolidated financial statements. It is required to be

prepared for those companies, which have a holding interest in the shares and in the

management of any other company (Daske et al., 2013). This company acts as the

subsidiary of the parent company. In this case, the subsidiary company becomes a part

of the parent company. Thus, in this case, it is mandatorily required by the company

officials or the finance officials of Wesfarmers as well as of other companies who

have such a situation to prepare a consolidated financial statement. The companies or

the consolidated entities in accordance with the provisions of the IFRS, would be

required to prepare an opening balance sheet, along with the majority of restatement

adjustments, to be made, against the opening retained earnings. The presentation of

the financial statements of the company have also undergone a slight change and to

explain it better a pre and post picture of some of the important financial statements of

the Wesfarmers has been provided below:

Business Combinations: There has been a vast amount of changes in the scenario

of business combinations and according to the audit committee of Wesfarmers, the

following changes have been seen or are yet to be felt. In the case of business

combination, the change has mostly been seen in the treatment of goodwill. In the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND PRACTICE

earlier case of the AGAAP, the goodwill of the company was amortised over a period

which would not exceed a period of twenty years.

Now in the case of IFRS, the amount of goodwill would no longer be amortised, contrary to

that it would be amortised but in accordance with the principles of impairment as has been

prescribed by IFRS. Goodwill will be written down to the maximum extent to which it would

be impaired. This will create a significant impact on the profits of the company, by

discontinuing the erstwhile amortisation expense. Then again, this impact or potential

increase of the goodwill would be short lived, provided if there isn’t any impairment of

goodwill.

In the case of restructuring of the business, in the earlier AGAAP rules, provisions would be

recognised for the restructuring, specifically for the purpose of the expected costs which

would be associated or linked with the consequent acquisition of any business. Whereas in

accordance with the rules of the IFRS, the provision would not be recognised, it will be

recognised only if there is an already existing provision mentioned in the books of accounts

of the acquire as on the date of acquisition (Loktionov, 2009). Nevertheless, it is highly

improbable to raise any kind of provisions in such circumstances or situation. This would

lead to the lowering of the amount of goodwill than what it should be in accordance with the

one which is present in accordance with the present accounting policy. A significant amount

of impact of this exercise would also be reflected in the profits of the company because this

exercise would result in the creation or in the increase in the expense of the company for the

first few years of the acquisition as and when the restructuring costs would be incurred.

Impairment of Assets: In the case of the old standards of AGAAP, the treatment of

the non-current assets of Wesfarmers was done in the following way. All the non-

current assets of the company are duly carried on the statement of the financial

earlier case of the AGAAP, the goodwill of the company was amortised over a period

which would not exceed a period of twenty years.

Now in the case of IFRS, the amount of goodwill would no longer be amortised, contrary to

that it would be amortised but in accordance with the principles of impairment as has been

prescribed by IFRS. Goodwill will be written down to the maximum extent to which it would

be impaired. This will create a significant impact on the profits of the company, by

discontinuing the erstwhile amortisation expense. Then again, this impact or potential

increase of the goodwill would be short lived, provided if there isn’t any impairment of

goodwill.

In the case of restructuring of the business, in the earlier AGAAP rules, provisions would be

recognised for the restructuring, specifically for the purpose of the expected costs which

would be associated or linked with the consequent acquisition of any business. Whereas in

accordance with the rules of the IFRS, the provision would not be recognised, it will be

recognised only if there is an already existing provision mentioned in the books of accounts

of the acquire as on the date of acquisition (Loktionov, 2009). Nevertheless, it is highly

improbable to raise any kind of provisions in such circumstances or situation. This would

lead to the lowering of the amount of goodwill than what it should be in accordance with the

one which is present in accordance with the present accounting policy. A significant amount

of impact of this exercise would also be reflected in the profits of the company because this

exercise would result in the creation or in the increase in the expense of the company for the

first few years of the acquisition as and when the restructuring costs would be incurred.

Impairment of Assets: In the case of the old standards of AGAAP, the treatment of

the non-current assets of Wesfarmers was done in the following way. All the non-

current assets of the company are duly carried on the statement of the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND PRACTICE

position (Statement of income) at an amount which is not greater than the recoverable

values of those non-current assets. The recoverable amount of any asset is ascertained

using a nominal cash flow procedure. Only when it is seen that the carrying amounts

of the assets are exceeding the recoverable amount, then it is consequently written

down.

Whereas in accordance with the new provisions of the IFRS, the recoverable amount of any

asset would be ascertained as the higher of the value in use or the net selling price of the

concerned asset. The net selling price is ascertained with the help of the active market. The

value in use would be determined by applying a discounted cash flow method. Then again, if

it is seen that the net selling price is lower than the carrying amount, as a result of which an

impairment loss would be taken note of and would be consequently recorded and

consequently the asset would be written down (Wesfarmers.com.au, 2018).

Secondly the recoverable amount test is performed on the different kinds of individual non-

current assets or groups of assets which aggregately generate net cash flows. In the case of

the IFRS principles, the audit committee of Wesfarmers makes some important points, that an

asset is defined in this standard as a cash generating unit or just like any other individual

asset. This cash generating unit being the smallest identifiable group of assets is independent

of the cash flows which are generated from other groups of cash flows. This change in the

accounting policy of the company in the case of recoverable account for non-current assets

has resulted in the classification of the Cash generating units which are now or which will be

at a lower level than they were previously, when they were used to carry out the impairment

testing procedure (Wesfarmers, 2007). The whole objective of this exercise is to identify and

recognise those kinds of assets and their groups which are required to be written down. This

whole exercise is performed to increase the likelihood of the process of asset impairment.

position (Statement of income) at an amount which is not greater than the recoverable

values of those non-current assets. The recoverable amount of any asset is ascertained

using a nominal cash flow procedure. Only when it is seen that the carrying amounts

of the assets are exceeding the recoverable amount, then it is consequently written

down.

Whereas in accordance with the new provisions of the IFRS, the recoverable amount of any

asset would be ascertained as the higher of the value in use or the net selling price of the

concerned asset. The net selling price is ascertained with the help of the active market. The

value in use would be determined by applying a discounted cash flow method. Then again, if

it is seen that the net selling price is lower than the carrying amount, as a result of which an

impairment loss would be taken note of and would be consequently recorded and

consequently the asset would be written down (Wesfarmers.com.au, 2018).

Secondly the recoverable amount test is performed on the different kinds of individual non-

current assets or groups of assets which aggregately generate net cash flows. In the case of

the IFRS principles, the audit committee of Wesfarmers makes some important points, that an

asset is defined in this standard as a cash generating unit or just like any other individual

asset. This cash generating unit being the smallest identifiable group of assets is independent

of the cash flows which are generated from other groups of cash flows. This change in the

accounting policy of the company in the case of recoverable account for non-current assets

has resulted in the classification of the Cash generating units which are now or which will be

at a lower level than they were previously, when they were used to carry out the impairment

testing procedure (Wesfarmers, 2007). The whole objective of this exercise is to identify and

recognise those kinds of assets and their groups which are required to be written down. This

whole exercise is performed to increase the likelihood of the process of asset impairment.

11ACCOUNTING THEORY AND PRACTICE

Recognition and measurement of the financial instruments of Wesfarmers:

The company of Wesfarmers along with the help of its audit committee and finance

experts have seen a tremendous amounts of changes in the process of recognising and

measuring of the different financial instruments of the retail company of Wesfarmers

and various other countries which are following the provisions of the IFRS.

In the case of the IFRS and its related provisions and treatment, the different financial

instruments are required to be classified into one of the following four categories, which in

turn would determine the accounting treatment of those items. The classification of the items

is as follows:

1. Loans and receivables: They are measured at the amortisation costs.

2. Instruments held till the period of maturity: They are also measured at amortisation

cost.

3. Financial instruments held for trading: It is measured at fair value with the fair value

changes being reflected in the statement for the financial performance or the statement

of income.

4. Instruments which are available for resale: These instruments are measured at fair

value with the fair value changes taken to equity.

This would result in a change in the current accounting policy that does not classify the

financial instruments. The future financial effect of this drastic change in the accounting

policy has yet not been calculated or known because the classification and the measurement

process is yet to be completed.

Hedging activities are also monitored on continuing basis and are written off from the

balance sheet of the company with any kind of profits or losses, which are recognised through

the statement of financial performance as per the old provisions of the AGAAP

Recognition and measurement of the financial instruments of Wesfarmers:

The company of Wesfarmers along with the help of its audit committee and finance

experts have seen a tremendous amounts of changes in the process of recognising and

measuring of the different financial instruments of the retail company of Wesfarmers

and various other countries which are following the provisions of the IFRS.

In the case of the IFRS and its related provisions and treatment, the different financial

instruments are required to be classified into one of the following four categories, which in

turn would determine the accounting treatment of those items. The classification of the items

is as follows:

1. Loans and receivables: They are measured at the amortisation costs.

2. Instruments held till the period of maturity: They are also measured at amortisation

cost.

3. Financial instruments held for trading: It is measured at fair value with the fair value

changes being reflected in the statement for the financial performance or the statement

of income.

4. Instruments which are available for resale: These instruments are measured at fair

value with the fair value changes taken to equity.

This would result in a change in the current accounting policy that does not classify the

financial instruments. The future financial effect of this drastic change in the accounting

policy has yet not been calculated or known because the classification and the measurement

process is yet to be completed.

Hedging activities are also monitored on continuing basis and are written off from the

balance sheet of the company with any kind of profits or losses, which are recognised through

the statement of financial performance as per the old provisions of the AGAAP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.