Sydney Metro College: FNSACC501 Financial Performance Analysis

VerifiedAdded on 2023/06/08

|22

|3880

|211

Homework Assignment

AI Summary

This accounting assignment, completed for the FNSACC501 course at Sydney Metro College, provides a comprehensive analysis of financial and business performance. It includes a theoretical assessment covering topics such as tax deductions, expense control, financial planning, risk management, short-term finance options, client grievance resolution, client rights, sources of financial information, compliance obligations, and forecasting techniques. The assignment also features a case study and practical assessment, requiring the student to analyze a client's financial situation, provide advice, and address specific business scenarios. The student provides detailed answers to questions regarding financial statements, business structure, and client communication, demonstrating a strong understanding of accounting principles and financial management.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the university:

Authors Note:

Accounting

Name of the Student:

Name of the university:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING

Table of Contents

Task 1: theory assessment:.........................................................................................................2

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................7

Task 2: the Case study and Practical Assessment......................................................................8

Answer to Question 1.................................................................................................................8

Answer to Question 2.................................................................................................................9

Answer to Question 3...............................................................................................................10

Answer to Question 4...............................................................................................................10

Answer to Question 5...............................................................................................................10

An answer to question 2: LMB motors:...................................................................................11

A)..............................................................................................................................................11

B)..............................................................................................................................................11

d)..............................................................................................................................................15

E)..............................................................................................................................................16

F)..............................................................................................................................................16

Reference..................................................................................................................................20

Table of Contents

Task 1: theory assessment:.........................................................................................................2

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................7

Task 2: the Case study and Practical Assessment......................................................................8

Answer to Question 1.................................................................................................................8

Answer to Question 2.................................................................................................................9

Answer to Question 3...............................................................................................................10

Answer to Question 4...............................................................................................................10

Answer to Question 5...............................................................................................................10

An answer to question 2: LMB motors:...................................................................................11

A)..............................................................................................................................................11

B)..............................................................................................................................................11

d)..............................................................................................................................................15

E)..............................................................................................................................................16

F)..............................................................................................................................................16

Reference..................................................................................................................................20

2ACCOUNTING

Task 1: theory assessment:

Answer to question 1:

1. In accordance with the rules of Income Tax Assessment Act, 1997 and ATO

guidelines, the assessee will be eligible to claim the expense without any valid

receipts are payments to PYAG, superannuation funds, Union Fees, and others. In all

other expenses, the deduction is available under section 8-1 of the Income Tax

Assessment Act 1997 if appropriate documentation is available (Libby 2017).

2. The expenditure on wages, vehicles, and the telephone can be controlled by making

fixed allowance payments. The company will pay a set amount of allowance based on

assumptions and expected costs.

3. If the accountant follows the basic principles of integrity, objectivity, competence,

and confidentiality in providing the professional service. Then the accountant is said

to be clear in the recommendations.

4. The plans for financial planning extract that summarises the scope of a client's

objectives is as follows:

Establishing and defining the client-planner relationship.

Asserting clients data and goals

Evaluating the client's financial situation

Fining alternatives

Implementing recommendations

Making changes in the recommendations.

5. The key areas that can cause significant taxation issues in business are as follows:

unpaid present entitlements and trusts

converting trust into a company

Low-interest loans to super funds

Task 1: theory assessment:

Answer to question 1:

1. In accordance with the rules of Income Tax Assessment Act, 1997 and ATO

guidelines, the assessee will be eligible to claim the expense without any valid

receipts are payments to PYAG, superannuation funds, Union Fees, and others. In all

other expenses, the deduction is available under section 8-1 of the Income Tax

Assessment Act 1997 if appropriate documentation is available (Libby 2017).

2. The expenditure on wages, vehicles, and the telephone can be controlled by making

fixed allowance payments. The company will pay a set amount of allowance based on

assumptions and expected costs.

3. If the accountant follows the basic principles of integrity, objectivity, competence,

and confidentiality in providing the professional service. Then the accountant is said

to be clear in the recommendations.

4. The plans for financial planning extract that summarises the scope of a client's

objectives is as follows:

Establishing and defining the client-planner relationship.

Asserting clients data and goals

Evaluating the client's financial situation

Fining alternatives

Implementing recommendations

Making changes in the recommendations.

5. The key areas that can cause significant taxation issues in business are as follows:

unpaid present entitlements and trusts

converting trust into a company

Low-interest loans to super funds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING

6. After ascertaining the risk to the company, the management should implement the

following to managing the risk

Risk avoidance

Reduction

Sharing

Retention.

7. The short-term finance options are

Overdraft agreement

Financing of accounts receivable

Advance for supply

8. To solve the grievances of the client the following steps or action can be taken.

Understand the problem

Analysis of the sources of the problem

Importance of the problem

Available options to solve the problem

Choosing the best and effective alternative available for solving the problem.

9. The five aspects of the legislation that protects a client's rights and responsibilities are

as follows

be treated with respect and dignity

having the right to privacy

right of confidentiality

10. The mains source of information at the time of considering the financing and the

investing are annual reports, and financial statements. Confirmation from the vendors

(Schaltegger and Burritt 2017).

11. The compliance obligations are found in the statutory discloser statement.

6. After ascertaining the risk to the company, the management should implement the

following to managing the risk

Risk avoidance

Reduction

Sharing

Retention.

7. The short-term finance options are

Overdraft agreement

Financing of accounts receivable

Advance for supply

8. To solve the grievances of the client the following steps or action can be taken.

Understand the problem

Analysis of the sources of the problem

Importance of the problem

Available options to solve the problem

Choosing the best and effective alternative available for solving the problem.

9. The five aspects of the legislation that protects a client's rights and responsibilities are

as follows

be treated with respect and dignity

having the right to privacy

right of confidentiality

10. The mains source of information at the time of considering the financing and the

investing are annual reports, and financial statements. Confirmation from the vendors

(Schaltegger and Burritt 2017).

11. The compliance obligations are found in the statutory discloser statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING

The forms are CFO Form, Accounting reporting Policy.

12. The changes in the legislation are found in the notes and statutory discloser of

account portion.

13. The charges will be calculated on the rate of taxes of the government.

14. The charges levied by state or territory governments are as follows

GST

Income tax

Wealth tax

Gambling tax

Horse racing tax

15. The benefits and application of the methods for presenting and formatting financial

data are as follows:

Summarised statements

Collective formatting

Easy to understand

Higher efficiency

Uniformity

16. As per the section 8-1 of the ITAA 97 all, the expenses that are contributory in

producing the assessable income are to be treated as the business expense.

17. The allowance is there for a business that manages on behalf of trust are trusts are not

taxed, low liability, capital gain tax discount, and others

18. The measure or technique uses historical data as inputs to make the business trends

forecasting. In addition to that, determine the future prospects of the company or the

business orientation (Hoyle et al. 2015).

The benefits are:

The forms are CFO Form, Accounting reporting Policy.

12. The changes in the legislation are found in the notes and statutory discloser of

account portion.

13. The charges will be calculated on the rate of taxes of the government.

14. The charges levied by state or territory governments are as follows

GST

Income tax

Wealth tax

Gambling tax

Horse racing tax

15. The benefits and application of the methods for presenting and formatting financial

data are as follows:

Summarised statements

Collective formatting

Easy to understand

Higher efficiency

Uniformity

16. As per the section 8-1 of the ITAA 97 all, the expenses that are contributory in

producing the assessable income are to be treated as the business expense.

17. The allowance is there for a business that manages on behalf of trust are trusts are not

taxed, low liability, capital gain tax discount, and others

18. The measure or technique uses historical data as inputs to make the business trends

forecasting. In addition to that, determine the future prospects of the company or the

business orientation (Hoyle et al. 2015).

The benefits are:

5ACCOUNTING

Easy to plan

Effective

Time-saving

19. The no-profit organizations are those entities that do not perform the activities to earn

profits instead; they perform the activities for social causes.

They are required to make the statutory return for the GST and claiming the Credits.

20. The methods to represent the present client's performance objective are as follows

To provide adequate feedback to each performer

To be responsive to the change in the behaviour and the adopting effective

work habits

Provide adequate data to the managers so they can judge and analysis and

make the decision regarding the assignments.

21. The cash is a valuable and liquefied asset to the company or the business

organization. There are several methods of controlling the cash out them two are

hereby discussed:

Establishing cash handling policies: the cash handling policy is

required to be implemented in the business as it regulated the

possession of cash.

Keep Logs: the cash is liquid assets therefore, it is important for the

company to record all the cash inflow and outflow statements.

22. At the time of establishing the business, the business must comply with some

statutory obligations such as not opposing the public policy, all adequate discloser

regarding the business legislature are filled in an effective manner (Jaffe and Irizarry

2014).

Easy to plan

Effective

Time-saving

19. The no-profit organizations are those entities that do not perform the activities to earn

profits instead; they perform the activities for social causes.

They are required to make the statutory return for the GST and claiming the Credits.

20. The methods to represent the present client's performance objective are as follows

To provide adequate feedback to each performer

To be responsive to the change in the behaviour and the adopting effective

work habits

Provide adequate data to the managers so they can judge and analysis and

make the decision regarding the assignments.

21. The cash is a valuable and liquefied asset to the company or the business

organization. There are several methods of controlling the cash out them two are

hereby discussed:

Establishing cash handling policies: the cash handling policy is

required to be implemented in the business as it regulated the

possession of cash.

Keep Logs: the cash is liquid assets therefore, it is important for the

company to record all the cash inflow and outflow statements.

22. At the time of establishing the business, the business must comply with some

statutory obligations such as not opposing the public policy, all adequate discloser

regarding the business legislature are filled in an effective manner (Jaffe and Irizarry

2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING

23. The financing is an important and material issue, for seeking advice on that financial

expert such as chartered accountant and other qualified are to be considered.

24. For reviewing the business finance, the following information is to be regarded to

make suitable decision and analysis the data.

Identifying the industry economic characteristics

Identify company strategies

Analysing the probabilities and the business risks.

25. In the financial management, the focus will be on the collective and effective

management of customer and market analysis review. The market and the customer

trends are the factors that contribute to the maximum impact on the business

statements (Maskell et al. 2016).

26. The following questioner can report the current and new objectives

What are the main business functions?

Sources of inflows and outflows

Financial policies

Methods of accounting and others

The financial policies file note is made for the financial officer.

27. The ratio used to understand the financial stability is the Debt / Equity ratio,

The debt-equity is the measure of finance sources of the business. If the debt is more

than the equity or equal to equity then the financial position of the client will be

treated as restful (Qvortrup 2015).

28. The consequences for a client not meeting reporting deadlines in accordance with the

ATO then in that case penalty will be imposed for every 28 days period up to a

maximum five penalties.

29. Two of the many forecasting techniques is as follows:

23. The financing is an important and material issue, for seeking advice on that financial

expert such as chartered accountant and other qualified are to be considered.

24. For reviewing the business finance, the following information is to be regarded to

make suitable decision and analysis the data.

Identifying the industry economic characteristics

Identify company strategies

Analysing the probabilities and the business risks.

25. In the financial management, the focus will be on the collective and effective

management of customer and market analysis review. The market and the customer

trends are the factors that contribute to the maximum impact on the business

statements (Maskell et al. 2016).

26. The following questioner can report the current and new objectives

What are the main business functions?

Sources of inflows and outflows

Financial policies

Methods of accounting and others

The financial policies file note is made for the financial officer.

27. The ratio used to understand the financial stability is the Debt / Equity ratio,

The debt-equity is the measure of finance sources of the business. If the debt is more

than the equity or equal to equity then the financial position of the client will be

treated as restful (Qvortrup 2015).

28. The consequences for a client not meeting reporting deadlines in accordance with the

ATO then in that case penalty will be imposed for every 28 days period up to a

maximum five penalties.

29. Two of the many forecasting techniques is as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

Qualitative and quantitative technic: the qualitative and quantitative technic in

the forecasting represents a bundle of historical information to analysis and the

trends, and the business activates regulations.

Average method: the average method of considered both of historical and

predicted and making an assessment on the averages of findings.

30. key features of the secretary's financial management are as follows:

Communication: the communication of the finical data is to the financial

manager and the secretary.

Performance: the activities that are performed in relation to the financial

management of the business are required to be evaluated by the secretary

31. Categorise sources of information on financial products and markets are as follows:

External sources: market analysis, customer trend, growth rate, and others

Internal source: product disclose statements, information circulars, books of

accounts and others.

32. The risk management options relating to financial and business performance are as

follows:

error of calculation

error of prediction

change in market factors

change in consumer behaviour and others

Answer to question 2:

1. The client's objective in the relevant case study is to make review and adjustment to

lower the tax liability regarding the income taxes and the Goods and Service taxes.

Qualitative and quantitative technic: the qualitative and quantitative technic in

the forecasting represents a bundle of historical information to analysis and the

trends, and the business activates regulations.

Average method: the average method of considered both of historical and

predicted and making an assessment on the averages of findings.

30. key features of the secretary's financial management are as follows:

Communication: the communication of the finical data is to the financial

manager and the secretary.

Performance: the activities that are performed in relation to the financial

management of the business are required to be evaluated by the secretary

31. Categorise sources of information on financial products and markets are as follows:

External sources: market analysis, customer trend, growth rate, and others

Internal source: product disclose statements, information circulars, books of

accounts and others.

32. The risk management options relating to financial and business performance are as

follows:

error of calculation

error of prediction

change in market factors

change in consumer behaviour and others

Answer to question 2:

1. The client's objective in the relevant case study is to make review and adjustment to

lower the tax liability regarding the income taxes and the Goods and Service taxes.

8ACCOUNTING

2. In the given case the business assets of the clients are equipment, vehicle, building

and inventories which worth $550000

3. The clients business is regarded as medium scale business operations as the revenue is

greater than 1 million but lower than 20 million.

4. The business of the client is Veterinary services.

5. Extra information that re provided in the case study is relating to internal reports

regarding part-time administrative staff that includes fortnightly payroll and payment

of accounts and banking transactions.

Task 2: the Case study and Practical Assessment

Answer to Question 1

Email:

Dear

Molly Smith,

(Subject- information of objectives)

It is grateful to provide services to provide solution to the problems. The dignity and

sincerity of the current performance as an accountant will be assigned into the work. It will

be ensured that the required financial advice will be contributory and beneficial to your

financial issues.

The purpose of the email is to understand the financial prospects and the requirement

of the business. Moreover, the choice of ideas and objectives of the client.

2. In the given case the business assets of the clients are equipment, vehicle, building

and inventories which worth $550000

3. The clients business is regarded as medium scale business operations as the revenue is

greater than 1 million but lower than 20 million.

4. The business of the client is Veterinary services.

5. Extra information that re provided in the case study is relating to internal reports

regarding part-time administrative staff that includes fortnightly payroll and payment

of accounts and banking transactions.

Task 2: the Case study and Practical Assessment

Answer to Question 1

Email:

Dear

Molly Smith,

(Subject- information of objectives)

It is grateful to provide services to provide solution to the problems. The dignity and

sincerity of the current performance as an accountant will be assigned into the work. It will

be ensured that the required financial advice will be contributory and beneficial to your

financial issues.

The purpose of the email is to understand the financial prospects and the requirement

of the business. Moreover, the choice of ideas and objectives of the client.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING

All the aspects of your business and the details are required to conform to make an in-

depth analysis of the financial position of the company. For more information and

understanding, you are requested to answer the followings.

1. What is the objective of the business?

2. What procedure of accounting is conducted?

3. What is the payment procedures of your business ( creditor/ debtor)

It will be glad if you kindly respond to our questions for the better assessment of your

business regarding the financial requirements.

Thanking You,

Date: With Regards,

(Accountant)

Answer to Question 2

There are certain requirements that are required to be full filled and certain specific

legal requirements are to be addressed at the time of establishing, structuring and financing of

a business (Otley 2016). There are some propaganda and obligation in relation to the

financing that is required to be solved are as follows:

Registering business name

Understanding of federal taxation system

State and local taxes

Permit of business and license

Business laws and regulations.

All the aspects of your business and the details are required to conform to make an in-

depth analysis of the financial position of the company. For more information and

understanding, you are requested to answer the followings.

1. What is the objective of the business?

2. What procedure of accounting is conducted?

3. What is the payment procedures of your business ( creditor/ debtor)

It will be glad if you kindly respond to our questions for the better assessment of your

business regarding the financial requirements.

Thanking You,

Date: With Regards,

(Accountant)

Answer to Question 2

There are certain requirements that are required to be full filled and certain specific

legal requirements are to be addressed at the time of establishing, structuring and financing of

a business (Otley 2016). There are some propaganda and obligation in relation to the

financing that is required to be solved are as follows:

Registering business name

Understanding of federal taxation system

State and local taxes

Permit of business and license

Business laws and regulations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING

Answer to Question 3

Based on the requirements of the client, there is some initial steps that are to be

followed by the client (Molly Smith) in the commencement of the business:

a. Appoint an accountant for the bookkeeping and accounting.

b. Follow the applicable Accounting Standards ( AAS 1, 2, 3, 16, and others)

c. Register for the GST

d. Pay returns to the taxation Authorities.

The above implementations are to be made with a period of 3-4 weeks.

Answer to Question 4

The Questions to be asked in the role play:

What is her new address?

What influence her to shift the business address?

Am I able to resolve your any doubts?

Answer to Question 5

In order to help the client perusing any of the material changes, as first the reason for

such change is required to be understood in addition to the business objectives and needs.

Further, the client's response and the legality of such a change are required (Francis et al.

2015). Further, the accounting technique, business activities, legislation, and others are to be

monitored.

Answer to Question 3

Based on the requirements of the client, there is some initial steps that are to be

followed by the client (Molly Smith) in the commencement of the business:

a. Appoint an accountant for the bookkeeping and accounting.

b. Follow the applicable Accounting Standards ( AAS 1, 2, 3, 16, and others)

c. Register for the GST

d. Pay returns to the taxation Authorities.

The above implementations are to be made with a period of 3-4 weeks.

Answer to Question 4

The Questions to be asked in the role play:

What is her new address?

What influence her to shift the business address?

Am I able to resolve your any doubts?

Answer to Question 5

In order to help the client perusing any of the material changes, as first the reason for

such change is required to be understood in addition to the business objectives and needs.

Further, the client's response and the legality of such a change are required (Francis et al.

2015). Further, the accounting technique, business activities, legislation, and others are to be

monitored.

11ACCOUNTING

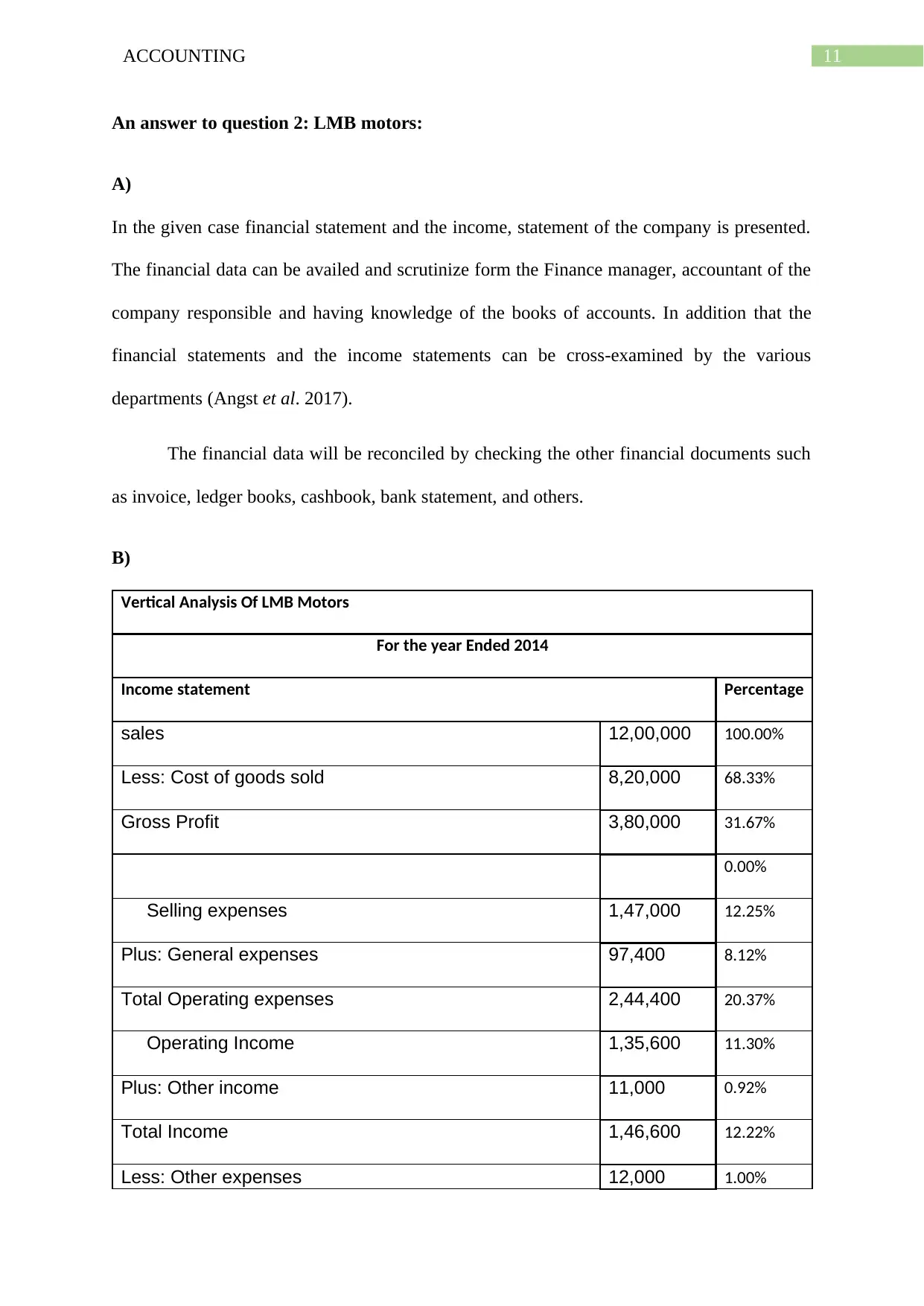

An answer to question 2: LMB motors:

A)

In the given case financial statement and the income, statement of the company is presented.

The financial data can be availed and scrutinize form the Finance manager, accountant of the

company responsible and having knowledge of the books of accounts. In addition that the

financial statements and the income statements can be cross-examined by the various

departments (Angst et al. 2017).

The financial data will be reconciled by checking the other financial documents such

as invoice, ledger books, cashbook, bank statement, and others.

B)

Vertical Analysis Of LMB Motors

For the year Ended 2014

Income statement Percentage

sales 12,00,000 100.00%

Less: Cost of goods sold 8,20,000 68.33%

Gross Profit 3,80,000 31.67%

0.00%

Selling expenses 1,47,000 12.25%

Plus: General expenses 97,400 8.12%

Total Operating expenses 2,44,400 20.37%

Operating Income 1,35,600 11.30%

Plus: Other income 11,000 0.92%

Total Income 1,46,600 12.22%

Less: Other expenses 12,000 1.00%

An answer to question 2: LMB motors:

A)

In the given case financial statement and the income, statement of the company is presented.

The financial data can be availed and scrutinize form the Finance manager, accountant of the

company responsible and having knowledge of the books of accounts. In addition that the

financial statements and the income statements can be cross-examined by the various

departments (Angst et al. 2017).

The financial data will be reconciled by checking the other financial documents such

as invoice, ledger books, cashbook, bank statement, and others.

B)

Vertical Analysis Of LMB Motors

For the year Ended 2014

Income statement Percentage

sales 12,00,000 100.00%

Less: Cost of goods sold 8,20,000 68.33%

Gross Profit 3,80,000 31.67%

0.00%

Selling expenses 1,47,000 12.25%

Plus: General expenses 97,400 8.12%

Total Operating expenses 2,44,400 20.37%

Operating Income 1,35,600 11.30%

Plus: Other income 11,000 0.92%

Total Income 1,46,600 12.22%

Less: Other expenses 12,000 1.00%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

![BSBFIM601 Manage Finances: Assessment Report, [Semester], [College]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fxm%2F162b9d69229e4e1db10d1eff3736f19c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.