Corporate Accounting and IFRS in Australia

VerifiedAdded on 2020/04/01

|15

|4324

|114

AI Summary

This assignment examines corporate accounting principles within Australia's context. It delves into the implementation of International Financial Reporting Standards (IFRS) and analyzes their influence on financial reporting practices. Students are expected to demonstrate an understanding of Australian corporate law, accounting standards, and the role of IFRS in shaping financial disclosures for companies operating in Australia.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting Theory

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

This report addresses the importance and significance of developing high quality

financial reports by the business entities for promoting transparency in the business

operations. The report has highlighted the difference in the accounting policies and estimates

adopted by the business entities as per their nature of operations. It has been analyzed from

the report that difference in the accounting policies exist because there is no unified theory of

accounting acceptable. There are various theories of accounting such as positive and

normative theory that are used by the accounting professionals in the development of their

financial reports. The analysis of the accounting disclosures of Commonwealth bank has

depicted that the banking group has selected the accounting policies as per the industry norms

for remaining competitive in the industry. The financial statements comply with the

conceptual, accounting framework principles thereby ensuring their high quality and meeting

the needs of end-users adequately. The accounting strategies adopted as per the strategic

goals and objectives of the Group. There is flexibility in the accounting policies adopted for

meeting the changes in the external business environment. The issues of concern in the

financial reports requiring more disclosure has also been identified in the report as red flags.

This report addresses the importance and significance of developing high quality

financial reports by the business entities for promoting transparency in the business

operations. The report has highlighted the difference in the accounting policies and estimates

adopted by the business entities as per their nature of operations. It has been analyzed from

the report that difference in the accounting policies exist because there is no unified theory of

accounting acceptable. There are various theories of accounting such as positive and

normative theory that are used by the accounting professionals in the development of their

financial reports. The analysis of the accounting disclosures of Commonwealth bank has

depicted that the banking group has selected the accounting policies as per the industry norms

for remaining competitive in the industry. The financial statements comply with the

conceptual, accounting framework principles thereby ensuring their high quality and meeting

the needs of end-users adequately. The accounting strategies adopted as per the strategic

goals and objectives of the Group. There is flexibility in the accounting policies adopted for

meeting the changes in the external business environment. The issues of concern in the

financial reports requiring more disclosure has also been identified in the report as red flags.

Contents

Introduction................................................................................................................................4

Section 1: Identify Key Accounting Policies.............................................................................4

Section 2: Assess Accounting Flexibility..................................................................................5

Section 3: Evaluate Accounting Strategy...................................................................................6

Section 4: Evaluate the Quality of Disclosure...........................................................................7

Section 5: Identify Potential Red Flags......................................................................................9

Section 6: Compliant with the Conceptual Framework...........................................................11

Conclusion................................................................................................................................12

References................................................................................................................................14

Introduction................................................................................................................................4

Section 1: Identify Key Accounting Policies.............................................................................4

Section 2: Assess Accounting Flexibility..................................................................................5

Section 3: Evaluate Accounting Strategy...................................................................................6

Section 4: Evaluate the Quality of Disclosure...........................................................................7

Section 5: Identify Potential Red Flags......................................................................................9

Section 6: Compliant with the Conceptual Framework...........................................................11

Conclusion................................................................................................................................12

References................................................................................................................................14

Introduction

The business corporations around the world need to develop and publish their annual

disclosures that enclose the information regarding their financial performance. The full

disclosure principle requires a business entity to provide all the necessary information to

support the decision-making process of the end-users. The accounting disclosures are

developed by the business entities as per the accounting policies and rules developed by the

accounting standard-setting bodies such as IASB. The IASB (International Accounting

Standards Board) holds the responsibility of providing standard guidelines to the business

entities around the world regarding the development of the financial reports. The IASB has

developed the conceptual accounting framework that needs to be adopted by the businesses

globally for preparing the financial reports and meeting the stakeholder expectations. The

AASB has developed the accounting standards that need to be followed by all the business

entities operating in Australia as per the IASB accounting rules. However, the accounting

disclosures of various business entities are largely influenced by the political forces that

impact the accounting choices of a particular entity (Bazley, Hancock and Robinson, 2014).

In this context, the present report aims to present an evaluation of the accounting strategies

and choices of an ASX listed corporation. The company selected for the purpose is

Commonwealth Bank, a world-recognized Australian bank involved in providing financial

services to the population of the country. The annual report of the bank for the last two

financial years, 2016 and 2017, are analyzed and examined for assessing its compliance with

conceptual framework principles.

Section 1: Identify Key Accounting Policies

The accounting policies of Commonwealth Bank of Australia are decided by the

board of directors and they have the power to change the same at any time. Commonwealth

Bank of Australia is a leading provider of integrated financial services and is based in

Australia. The company is a profit earning entity and is operating globally. The company

deals in various kinds of products, they provide services in retail, institutional and business

banking and wealth management products (Commonwealth Bank of Australia, 2017). The

accounting policies of the company are made quite effective. The accounting policies of the

firm are based on historical cost convention. There are certain assets and liabilities which are

measured at fair value. The losses that have been occurred due to the damage of asset are

The business corporations around the world need to develop and publish their annual

disclosures that enclose the information regarding their financial performance. The full

disclosure principle requires a business entity to provide all the necessary information to

support the decision-making process of the end-users. The accounting disclosures are

developed by the business entities as per the accounting policies and rules developed by the

accounting standard-setting bodies such as IASB. The IASB (International Accounting

Standards Board) holds the responsibility of providing standard guidelines to the business

entities around the world regarding the development of the financial reports. The IASB has

developed the conceptual accounting framework that needs to be adopted by the businesses

globally for preparing the financial reports and meeting the stakeholder expectations. The

AASB has developed the accounting standards that need to be followed by all the business

entities operating in Australia as per the IASB accounting rules. However, the accounting

disclosures of various business entities are largely influenced by the political forces that

impact the accounting choices of a particular entity (Bazley, Hancock and Robinson, 2014).

In this context, the present report aims to present an evaluation of the accounting strategies

and choices of an ASX listed corporation. The company selected for the purpose is

Commonwealth Bank, a world-recognized Australian bank involved in providing financial

services to the population of the country. The annual report of the bank for the last two

financial years, 2016 and 2017, are analyzed and examined for assessing its compliance with

conceptual framework principles.

Section 1: Identify Key Accounting Policies

The accounting policies of Commonwealth Bank of Australia are decided by the

board of directors and they have the power to change the same at any time. Commonwealth

Bank of Australia is a leading provider of integrated financial services and is based in

Australia. The company is a profit earning entity and is operating globally. The company

deals in various kinds of products, they provide services in retail, institutional and business

banking and wealth management products (Commonwealth Bank of Australia, 2017). The

accounting policies of the company are made quite effective. The accounting policies of the

firm are based on historical cost convention. There are certain assets and liabilities which are

measured at fair value. The losses that have been occurred due to the damage of asset are

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

being reversed. The accounting policies are having remained consistent with the standards

provided by the AASB. Apart from this the operations and other accounting policies are

based on the principle of IFRS. Securities sold under the repurchased agreement on the

guidelines provided by the AASB (Ordelheide, 2016).

The interest expenses of the cost are settled on the basis of amortized cost. Interest

expenses include cost of issue that was initially identified as the part of carrying cost. The

income received from the interest is brought into accounting by using effective interest

method (Commonwealth Bank of Australia, 2017). It calculates amortized cost of a financial

instrument. The equities are classified as available for sale financial assets. The financial

statement of the company provides a consolidated data of the business of the company in an

effective way. In addition to this the assets of the company are classified on the basis of fair

value and are divided into three categories, trading, insurance and other. The firm also uses

derivative financial instruments, this aspect includes various things such as forward rate

agreements, future options, credit swaps etc (Commonwealth Bank of Australia, 2017).

Section 2: Assess Accounting Flexibility

The firm Commonwealth Bank of Australia is following its accounting policies based

on the guidelines of the AASB. The AASB has made it mandatory for all the firms to comply

with the rules and guidelines prescribed by AASB (Walton, 2011). The financial statements

and the accounting policies of the Commonwealth Bank of Australia are prepared by the

board of directors (Commonwealth Bank of Australia, 2017). The bank is operating in

various countries and hence it a global firm. Apart from this, the company is the parent firm

for all its subsidiaries. The board of directors is not only responsible for preparing the

accounts of the main company but also of its subsidiaries. The principle accounting policies

are adopted on the basis of the guidelines prescribed by the AASB. The financial report of the

firm is presented in Australian dollars. The general purpose financial report is prepared in

accordance to the norms provided by the AASB (Bazley, Hancock and Robinson, 2014).

The accounting principles and policies comply with the International Financial

Reporting Standards. In addition to this the interpretations are issued by the International

Accounting Standards Board (IASB) and IFRS interpretations committee. The amount

presented in the financial statements is rounded up to remain in accordance with the ASIC

Corporations Instrument 2016/191 (Commonwealth Bank of Australia, 2017). The firm has

made amendments in its accounting policies so that it can align closely with the economic

provided by the AASB. Apart from this the operations and other accounting policies are

based on the principle of IFRS. Securities sold under the repurchased agreement on the

guidelines provided by the AASB (Ordelheide, 2016).

The interest expenses of the cost are settled on the basis of amortized cost. Interest

expenses include cost of issue that was initially identified as the part of carrying cost. The

income received from the interest is brought into accounting by using effective interest

method (Commonwealth Bank of Australia, 2017). It calculates amortized cost of a financial

instrument. The equities are classified as available for sale financial assets. The financial

statement of the company provides a consolidated data of the business of the company in an

effective way. In addition to this the assets of the company are classified on the basis of fair

value and are divided into three categories, trading, insurance and other. The firm also uses

derivative financial instruments, this aspect includes various things such as forward rate

agreements, future options, credit swaps etc (Commonwealth Bank of Australia, 2017).

Section 2: Assess Accounting Flexibility

The firm Commonwealth Bank of Australia is following its accounting policies based

on the guidelines of the AASB. The AASB has made it mandatory for all the firms to comply

with the rules and guidelines prescribed by AASB (Walton, 2011). The financial statements

and the accounting policies of the Commonwealth Bank of Australia are prepared by the

board of directors (Commonwealth Bank of Australia, 2017). The bank is operating in

various countries and hence it a global firm. Apart from this, the company is the parent firm

for all its subsidiaries. The board of directors is not only responsible for preparing the

accounts of the main company but also of its subsidiaries. The principle accounting policies

are adopted on the basis of the guidelines prescribed by the AASB. The financial report of the

firm is presented in Australian dollars. The general purpose financial report is prepared in

accordance to the norms provided by the AASB (Bazley, Hancock and Robinson, 2014).

The accounting principles and policies comply with the International Financial

Reporting Standards. In addition to this the interpretations are issued by the International

Accounting Standards Board (IASB) and IFRS interpretations committee. The amount

presented in the financial statements is rounded up to remain in accordance with the ASIC

Corporations Instrument 2016/191 (Commonwealth Bank of Australia, 2017). The firm has

made amendments in its accounting policies so that it can align closely with the economic

substances. The operations of the subsidiaries are also maintained on the guidelines presented

by the AASB. The accounts of the subsidiaries are presented in consolidated form. All the

transactions between the segments are conducted on an arm’s length basis. All these practices

by the Commonwealth Bank of Australia prove that the company follows the accounting

principles as prescribed by the AASB. The top level management of the firm is engaged in

making accounting policies, they do not adopt the path of flexibility, and they have adopted

the accounting principles and policies as prescribed by the ASSB (Dagwell, Wines, and

Lambert, 2015).

Section 3: Evaluate Accounting Strategy

The Commonwealth bank is attributed to be leading provider of financial

services in Australia and has diversified its business operations in many countries around the

world, that is, New Zeeland, Asia, the United Sates and the United Kingdom. As such, the

banking corporation accounting strategy is to select the most appropriate accounting policies

and choices that enable it to meet its corporate objectives of global expansion (Knight, 2004).

The bank has determined its selection of accounting policies that enables it to remain

competitive in the in the banking industry of Australia. The corporate, institutional and

government clients of the Commonwealth Group incorporate the use of relationship

management model that is based on industry expertise and insights. The services offered by

the clients include debt raising, financial and commodities risk management, transactional

banking capabilities for stretching the Group’s competitive position in the market. The annual

disclosure has also provided a description of the accounting policies adopted for identifying

and measuring the material risks such as credit risk, material risk and funding risk. The

banking corporations has also implemented an Internal Control Capital Adequacy

Assessment Process (ICAAP) as per the industry norms in order to develop an understanding

and quantifying the material risks to develop strategic ensures for overcoming the risk

identified (Commonwealth Bank of Australia, 2017). The banking corporation has also

implemented laws, regulations, legislation, rules and codes of conducts as per the industry

norms. Also, the Group has adopted accounting policies regarding its audit as per the

accounting process and controls of the industry. The Group has ensured that its audit team

has adequate skills and competencies required for auditing a complex banking institution

(Kenny, 2009).

by the AASB. The accounts of the subsidiaries are presented in consolidated form. All the

transactions between the segments are conducted on an arm’s length basis. All these practices

by the Commonwealth Bank of Australia prove that the company follows the accounting

principles as prescribed by the AASB. The top level management of the firm is engaged in

making accounting policies, they do not adopt the path of flexibility, and they have adopted

the accounting principles and policies as prescribed by the ASSB (Dagwell, Wines, and

Lambert, 2015).

Section 3: Evaluate Accounting Strategy

The Commonwealth bank is attributed to be leading provider of financial

services in Australia and has diversified its business operations in many countries around the

world, that is, New Zeeland, Asia, the United Sates and the United Kingdom. As such, the

banking corporation accounting strategy is to select the most appropriate accounting policies

and choices that enable it to meet its corporate objectives of global expansion (Knight, 2004).

The bank has determined its selection of accounting policies that enables it to remain

competitive in the in the banking industry of Australia. The corporate, institutional and

government clients of the Commonwealth Group incorporate the use of relationship

management model that is based on industry expertise and insights. The services offered by

the clients include debt raising, financial and commodities risk management, transactional

banking capabilities for stretching the Group’s competitive position in the market. The annual

disclosure has also provided a description of the accounting policies adopted for identifying

and measuring the material risks such as credit risk, material risk and funding risk. The

banking corporations has also implemented an Internal Control Capital Adequacy

Assessment Process (ICAAP) as per the industry norms in order to develop an understanding

and quantifying the material risks to develop strategic ensures for overcoming the risk

identified (Commonwealth Bank of Australia, 2017). The banking corporation has also

implemented laws, regulations, legislation, rules and codes of conducts as per the industry

norms. Also, the Group has adopted accounting policies regarding its audit as per the

accounting process and controls of the industry. The Group has ensured that its audit team

has adequate skills and competencies required for auditing a complex banking institution

(Kenny, 2009).

The major competitor of the bank is regarded to be Westpac, an Australia bank

holding a prominent position in the ‘big four’ banks of Australia. As such, both the banks are

operating in Australia and therefore need to comply with the AASB standards and

Corporations Act 2001 (2016 Westpac Group Annual Report, 2016). The basic accounting

policies adopted for the development of general purpose financial reports is provided under

notes to financial statements section by both the banks. However, there exists some

difference between the accounting policies ad estimates of Commonwealth bank as compared

to Westpac as pre their nature of business operations. The Banking Corporation has disclosed

in its financial report regarding the changed accounting policies in relation to the recognition

of Global Asset management of long-term incentives offered to some employees in wealth

management. As per the new accounting policy, the long-term incentives of the managers are

recognized as expenditure when they are actually given rather than vesting them over the

period as per the previous accounting policy (Commonwealth Bank of Australia, 2017)

This change has been introduced in order to aligning the accounting policy as per the

economic environment in which the Group operates. The change introduced has resulted in

reducing its net profit after tax, retained earnings, decreasing its total assets and enhancing its

total liabilities. This change in the accounting policy has been done as per the positive theory

of accounting (PAT) as per which managers tend to adopt a particular accounting approach in

order to achieve a defined set of objectives and goals. The change in the incentive policies for

managers has been done as per the external economic conditions. The accounting transactions

relating to long-term incentives of the managers are structured as per its new strategic goals

of linking the accounting policies with the economic substance of the arrangements

(Henderson et al., 2015).

The Group has also disclosed its accounting strategy in relation to the incentives

offered to the managers for managing its earnings. The superannuation plans provided by the

banking corporation are calculated by independent fund actuaries. Also, the benefits offered

to the employees are recognized in the income statements and the unpaid contributions are

included under liability section in the balance sheet (Sheridan, 2016). This is done to ensure

that incentives offered to the managers for earning management is not related to the equity

position and therefore ensuring that managers does not involve in any fraudulent activities for

maximizing their personal benefits (Hussey and Ong, 2017).

holding a prominent position in the ‘big four’ banks of Australia. As such, both the banks are

operating in Australia and therefore need to comply with the AASB standards and

Corporations Act 2001 (2016 Westpac Group Annual Report, 2016). The basic accounting

policies adopted for the development of general purpose financial reports is provided under

notes to financial statements section by both the banks. However, there exists some

difference between the accounting policies ad estimates of Commonwealth bank as compared

to Westpac as pre their nature of business operations. The Banking Corporation has disclosed

in its financial report regarding the changed accounting policies in relation to the recognition

of Global Asset management of long-term incentives offered to some employees in wealth

management. As per the new accounting policy, the long-term incentives of the managers are

recognized as expenditure when they are actually given rather than vesting them over the

period as per the previous accounting policy (Commonwealth Bank of Australia, 2017)

This change has been introduced in order to aligning the accounting policy as per the

economic environment in which the Group operates. The change introduced has resulted in

reducing its net profit after tax, retained earnings, decreasing its total assets and enhancing its

total liabilities. This change in the accounting policy has been done as per the positive theory

of accounting (PAT) as per which managers tend to adopt a particular accounting approach in

order to achieve a defined set of objectives and goals. The change in the incentive policies for

managers has been done as per the external economic conditions. The accounting transactions

relating to long-term incentives of the managers are structured as per its new strategic goals

of linking the accounting policies with the economic substance of the arrangements

(Henderson et al., 2015).

The Group has also disclosed its accounting strategy in relation to the incentives

offered to the managers for managing its earnings. The superannuation plans provided by the

banking corporation are calculated by independent fund actuaries. Also, the benefits offered

to the employees are recognized in the income statements and the unpaid contributions are

included under liability section in the balance sheet (Sheridan, 2016). This is done to ensure

that incentives offered to the managers for earning management is not related to the equity

position and therefore ensuring that managers does not involve in any fraudulent activities for

maximizing their personal benefits (Hussey and Ong, 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

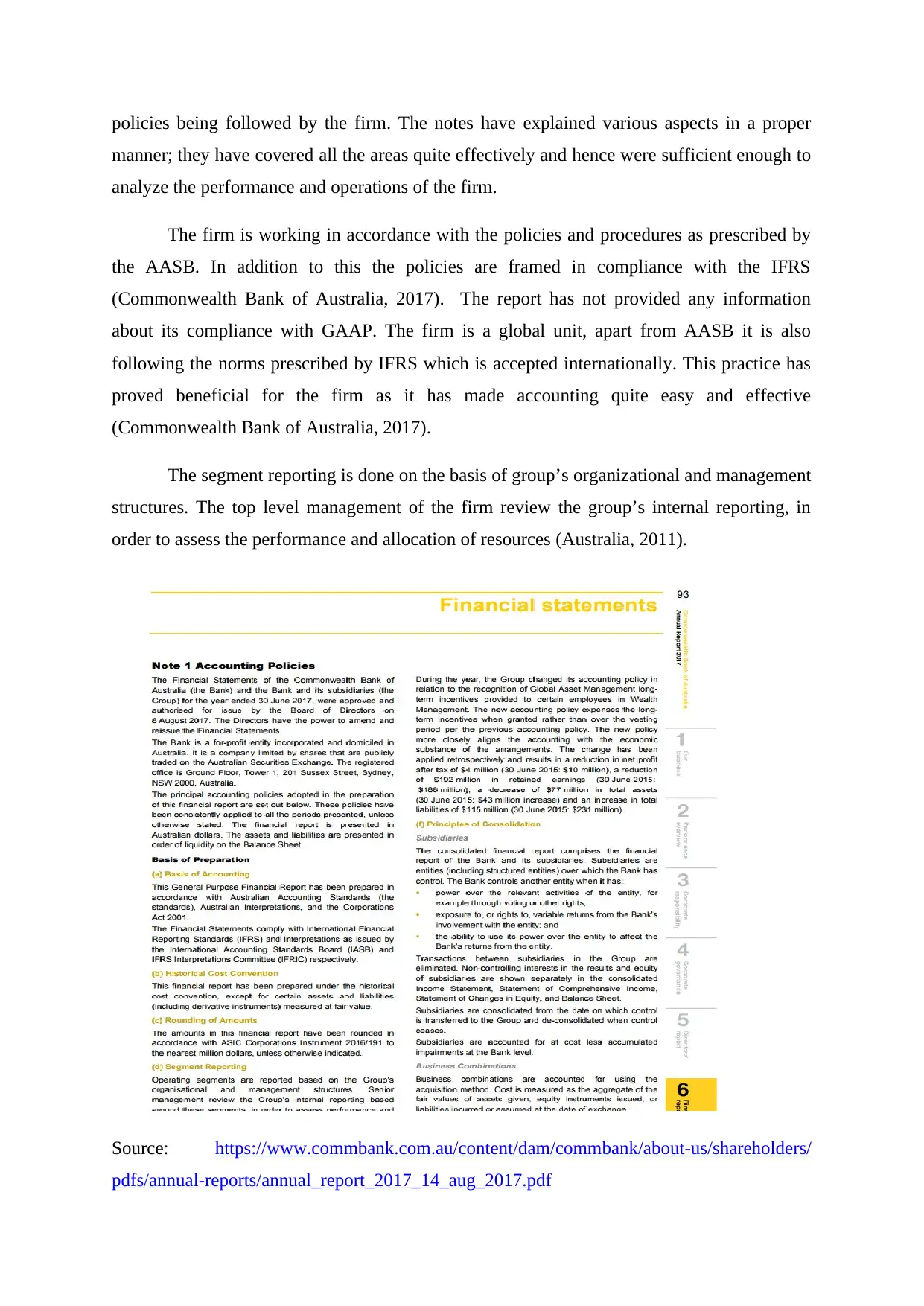

Section 4: Evaluate the Quality of Disclosure

The financial statement of Commonwealth Bank of Australia has covered various

aspects. The report has provided enough information about the purpose and vision of the

company. In addition to this the report has also provided the idea about the core function of

the firm. The firm, Commonwealth Bank of Australia is a global bank situated in Australia. It

is operating in various countries and the same information is provided in the report. The bank

deals in various services such as retail, institutional etc. all this information has been provided

subsequently (Commonwealth Bank of Australia, 2017). The footnotes in the report has

provided information about the accounting policies that is been followed by the firm. In

addition to this, the footnotes also discussed that the accounting policies implemented by the

firm is in accordance with the AASB (Hussey and Ong, 2005). It is evident from the report

that the foreign currency transactions are translated into functional currency using the

exchange rates which changes every day. There is no flexibility in the management of

accounting policies. The firm works in pure compliance with the AASB (Horngren et al.,

2012).

The disclosure provided by the firm is adequate as it has covered wide range of

information. It has provided information about the accounting policies that has been used by

the firm and the changes made by it in its policies. The accounting policies are followed

consistently and are in accordance with the guidelines prescribed by the AASB. The company

has framed its policies in accordance with the IFRS because it is a global unit and cannot

follow the regulations prescribed by its country only (Commonwealth Bank of Australia,

2017). The implementation of IFRS principle has certainly proved beneficial for the firm as

it has helped them in making their financial statements clearly with proper divisions in

accounting sections. The company regularly keeps a check on the accounting policies and

makes amendments in the same as prescribed by the AASB. The disclosure by the firm was

sufficient as it has provided a wide spectrum of data which is quite beneficial for the general

public, investors other parties. This will help them in deciding their future course of action

(Commonwealth Bank of Australia, 2017).

The footnotes have provided information about the accounting policies that has been

used by the firm. It has also provided information about the policies that has been amended.

The footnotes have covered information about the accounting principles and the procedure

through which the financial statement has been prepared (Commonwealth Bank of Australia,

2017). The footnotes were quite adequate to analyze the performance and the accounting

The financial statement of Commonwealth Bank of Australia has covered various

aspects. The report has provided enough information about the purpose and vision of the

company. In addition to this the report has also provided the idea about the core function of

the firm. The firm, Commonwealth Bank of Australia is a global bank situated in Australia. It

is operating in various countries and the same information is provided in the report. The bank

deals in various services such as retail, institutional etc. all this information has been provided

subsequently (Commonwealth Bank of Australia, 2017). The footnotes in the report has

provided information about the accounting policies that is been followed by the firm. In

addition to this, the footnotes also discussed that the accounting policies implemented by the

firm is in accordance with the AASB (Hussey and Ong, 2005). It is evident from the report

that the foreign currency transactions are translated into functional currency using the

exchange rates which changes every day. There is no flexibility in the management of

accounting policies. The firm works in pure compliance with the AASB (Horngren et al.,

2012).

The disclosure provided by the firm is adequate as it has covered wide range of

information. It has provided information about the accounting policies that has been used by

the firm and the changes made by it in its policies. The accounting policies are followed

consistently and are in accordance with the guidelines prescribed by the AASB. The company

has framed its policies in accordance with the IFRS because it is a global unit and cannot

follow the regulations prescribed by its country only (Commonwealth Bank of Australia,

2017). The implementation of IFRS principle has certainly proved beneficial for the firm as

it has helped them in making their financial statements clearly with proper divisions in

accounting sections. The company regularly keeps a check on the accounting policies and

makes amendments in the same as prescribed by the AASB. The disclosure by the firm was

sufficient as it has provided a wide spectrum of data which is quite beneficial for the general

public, investors other parties. This will help them in deciding their future course of action

(Commonwealth Bank of Australia, 2017).

The footnotes have provided information about the accounting policies that has been

used by the firm. It has also provided information about the policies that has been amended.

The footnotes have covered information about the accounting principles and the procedure

through which the financial statement has been prepared (Commonwealth Bank of Australia,

2017). The footnotes were quite adequate to analyze the performance and the accounting

policies being followed by the firm. The notes have explained various aspects in a proper

manner; they have covered all the areas quite effectively and hence were sufficient enough to

analyze the performance and operations of the firm.

The firm is working in accordance with the policies and procedures as prescribed by

the AASB. In addition to this the policies are framed in compliance with the IFRS

(Commonwealth Bank of Australia, 2017). The report has not provided any information

about its compliance with GAAP. The firm is a global unit, apart from AASB it is also

following the norms prescribed by IFRS which is accepted internationally. This practice has

proved beneficial for the firm as it has made accounting quite easy and effective

(Commonwealth Bank of Australia, 2017).

The segment reporting is done on the basis of group’s organizational and management

structures. The top level management of the firm review the group’s internal reporting, in

order to assess the performance and allocation of resources (Australia, 2011).

Source: https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/

pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf

manner; they have covered all the areas quite effectively and hence were sufficient enough to

analyze the performance and operations of the firm.

The firm is working in accordance with the policies and procedures as prescribed by

the AASB. In addition to this the policies are framed in compliance with the IFRS

(Commonwealth Bank of Australia, 2017). The report has not provided any information

about its compliance with GAAP. The firm is a global unit, apart from AASB it is also

following the norms prescribed by IFRS which is accepted internationally. This practice has

proved beneficial for the firm as it has made accounting quite easy and effective

(Commonwealth Bank of Australia, 2017).

The segment reporting is done on the basis of group’s organizational and management

structures. The top level management of the firm review the group’s internal reporting, in

order to assess the performance and allocation of resources (Australia, 2011).

Source: https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/

pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf

Section 5: Identify Potential Red Flags

The financial report of the banking Corporation has provided all the relevant

information related to the accounting policies adopted for preparing its general purpose

financial statements. However, there exists some accounting changes in the financial reports

of the banking corporation that requires more disclosure identified as red flags as follows:

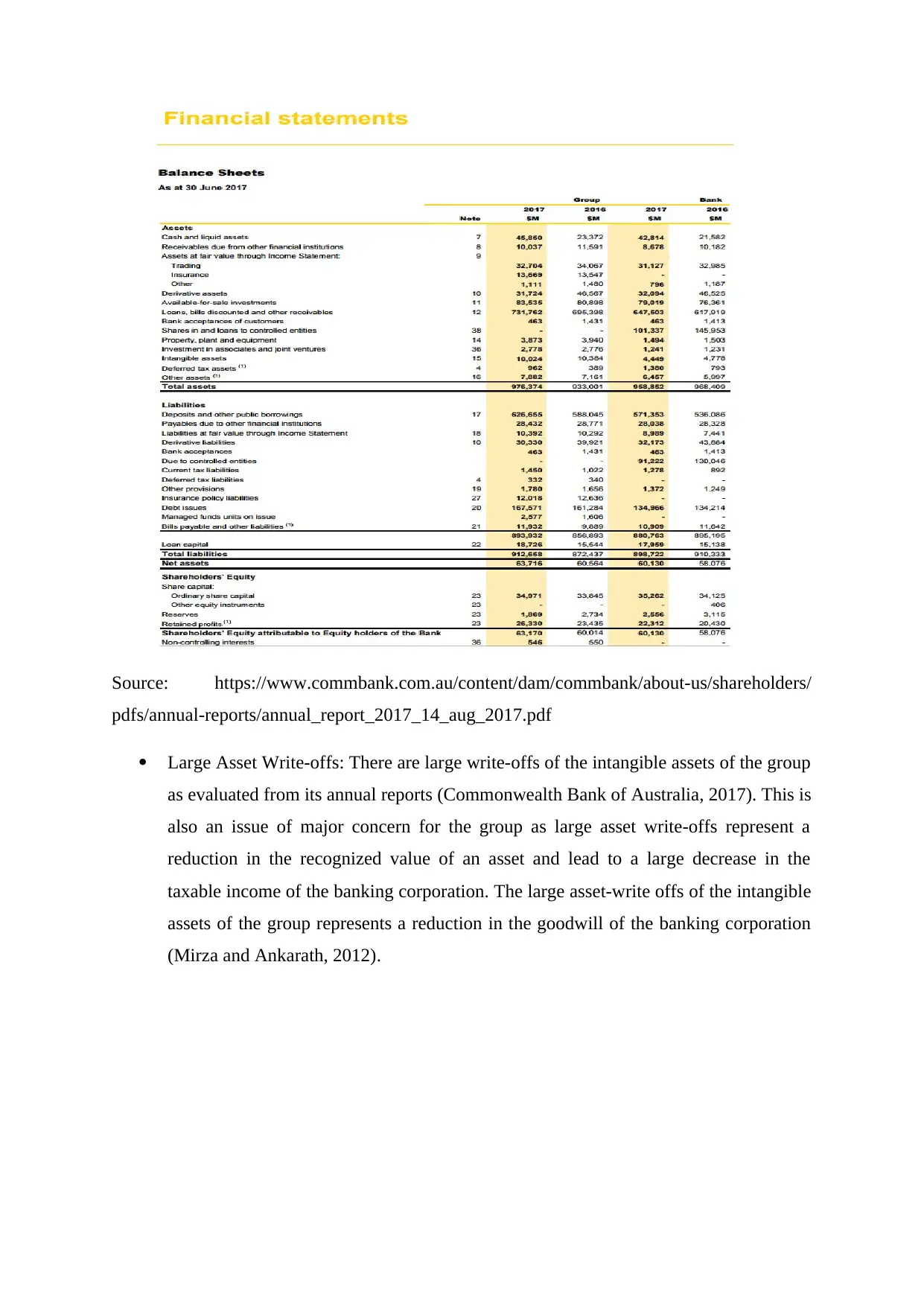

Unexplained Accounting Policy Changes: The comparison of the financial reports of

the banking corporation over the last tow years have indicted that there is reduction in

its retained earnings and total assets in the financial year 2017 as compared to that

that of the year 2015. The net profit after tax has been decline to $5 million as

compared to $10 million from 2016 to 2017. The retained earnings has decreased

from $192 million to $188 million and reported a reduction of 477 million in its total

assets and increase in its overall liabilities to $115 million (Commonwealth Bank of

Australia, 2017). This has resulted from the change in accounting policy of the

banking group for recognizing its long-term incentives. As such, the group has not

adequately explained the change in its accounting results with the adoption of the

significant accounting policy (Marley and Pedersen, 2015).

Increase in Receivables: The Group has also reported an increase in its loans, bills

discounted and other receivables in the year 2017 to $ 731,762 from $695,398 in the

year 2016 (Commonwealth Bank of Australia, 2017). There is no proper disclosure

reading the increase in its receivable by the banking corporation that is an issue of

major concern for the bank (Walton, 2011).

The financial report of the banking Corporation has provided all the relevant

information related to the accounting policies adopted for preparing its general purpose

financial statements. However, there exists some accounting changes in the financial reports

of the banking corporation that requires more disclosure identified as red flags as follows:

Unexplained Accounting Policy Changes: The comparison of the financial reports of

the banking corporation over the last tow years have indicted that there is reduction in

its retained earnings and total assets in the financial year 2017 as compared to that

that of the year 2015. The net profit after tax has been decline to $5 million as

compared to $10 million from 2016 to 2017. The retained earnings has decreased

from $192 million to $188 million and reported a reduction of 477 million in its total

assets and increase in its overall liabilities to $115 million (Commonwealth Bank of

Australia, 2017). This has resulted from the change in accounting policy of the

banking group for recognizing its long-term incentives. As such, the group has not

adequately explained the change in its accounting results with the adoption of the

significant accounting policy (Marley and Pedersen, 2015).

Increase in Receivables: The Group has also reported an increase in its loans, bills

discounted and other receivables in the year 2017 to $ 731,762 from $695,398 in the

year 2016 (Commonwealth Bank of Australia, 2017). There is no proper disclosure

reading the increase in its receivable by the banking corporation that is an issue of

major concern for the bank (Walton, 2011).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Source: https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/

pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf

Large Asset Write-offs: There are large write-offs of the intangible assets of the group

as evaluated from its annual reports (Commonwealth Bank of Australia, 2017). This is

also an issue of major concern for the group as large asset write-offs represent a

reduction in the recognized value of an asset and lead to a large decrease in the

taxable income of the banking corporation. The large asset-write offs of the intangible

assets of the group represents a reduction in the goodwill of the banking corporation

(Mirza and Ankarath, 2012).

pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf

Large Asset Write-offs: There are large write-offs of the intangible assets of the group

as evaluated from its annual reports (Commonwealth Bank of Australia, 2017). This is

also an issue of major concern for the group as large asset write-offs represent a

reduction in the recognized value of an asset and lead to a large decrease in the

taxable income of the banking corporation. The large asset-write offs of the intangible

assets of the group represents a reduction in the goodwill of the banking corporation

(Mirza and Ankarath, 2012).

Source: https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/

pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf

Section 6: Compliant with the Conceptual Framework

It is quite important for a firm to remain competitive in the market, however various

factors affects its competitiveness. The political factors play an important role in accounting

standard setting environment (Marley and Pedersen, 2015). The firm is operating in various

countries and is a globally functioning entity. Various countries have different political

environment, some boots the firm while others restricts its operations. Thus it plays a major

role in setting standard for accounting. Commonwealth Bank of Australia has tried its best to

remain in compliance with the political factors of every country in which it is operating

(Commonwealth Bank of Australia, 2017). Every firm which is operating in a particular

political setting has to follow the regulations prescribed by the political factors. In some

countries it is quite essential to make the financial disclosures keeping in mind the impact on

the economic environment. thus to remain competitive in the international market,

Commonwealth Bank of Australia has made policies so that it can remain in compliance with

pdfs/annual-reports/annual_report_2017_14_aug_2017.pdf

Section 6: Compliant with the Conceptual Framework

It is quite important for a firm to remain competitive in the market, however various

factors affects its competitiveness. The political factors play an important role in accounting

standard setting environment (Marley and Pedersen, 2015). The firm is operating in various

countries and is a globally functioning entity. Various countries have different political

environment, some boots the firm while others restricts its operations. Thus it plays a major

role in setting standard for accounting. Commonwealth Bank of Australia has tried its best to

remain in compliance with the political factors of every country in which it is operating

(Commonwealth Bank of Australia, 2017). Every firm which is operating in a particular

political setting has to follow the regulations prescribed by the political factors. In some

countries it is quite essential to make the financial disclosures keeping in mind the impact on

the economic environment. thus to remain competitive in the international market,

Commonwealth Bank of Australia has made policies so that it can remain in compliance with

the political factors of the countries in which it is operating (Pietra, McLeay and Ronen,

2013).

The AASB has made it mandatory for the profit earning firms to follow the rules which

are prescribed by the AASB itself (Marley and Pedersen, 2015). The firm has not adopted

any other flexible route for their accounting policies. In addition to this, ASSB has also made

it mandatory to work in accordance with the norms delegated by IFRS so that the firm can

remain viable internationally as well. The disclosures made by the firm is quite essential and

effective as it helps the general public, investors other to decide their future course of action

as to invest in the firm or not (Hoffman, 2016). In addition to this, the disclosures made by

the firm helps in gaining information about the performance and productivity of the firm in

the global market. The disclosures about the accounting policies and other aspects help in

building goodwill of the organization (Commonwealth Bank of Australia, 2017).

Conclusion

It can be inferred from the overall discussion held in the report that development and

publishing of proper annul disclosures is essential for business entities in order to promote

their sustainable growth and development. The business corporations operating in Australia

need to prepare their financial reports as per the AASB standards and the Corporations Act

2001. The AASB has directed all the business entities of Australia to comply with the

conceptual accounting framework principles as per the IASB accounting rules and

conventions. The analysis of the annual disclosure of the Commonwealth bank has revealed

that it has effectively adopted the conceptual accounting framework principles by providing

all the relevant, reliable, comparable and understandable information in its annual disclosure

statements. The accounting disclosure is prepared as per the industry norms in order to

remain competitive and also there is change in some accounting policies as per the mangers

decision to achieve certain desired set of objectives. The bank operates its business

corporation globally and therefore need to adopt some changes in its annual disclosures as per

the political environment of different countries. The potential area of concern for the banking

corporation is reduction in net worth over the subsequent years from 2015to 2017 and

increase of its receivables and large write-offs of its intangible assets. The banking group is

recommended to develop and implement proper strategies for overcoming these existing red

flags identified in its annual report disclosure.

2013).

The AASB has made it mandatory for the profit earning firms to follow the rules which

are prescribed by the AASB itself (Marley and Pedersen, 2015). The firm has not adopted

any other flexible route for their accounting policies. In addition to this, ASSB has also made

it mandatory to work in accordance with the norms delegated by IFRS so that the firm can

remain viable internationally as well. The disclosures made by the firm is quite essential and

effective as it helps the general public, investors other to decide their future course of action

as to invest in the firm or not (Hoffman, 2016). In addition to this, the disclosures made by

the firm helps in gaining information about the performance and productivity of the firm in

the global market. The disclosures about the accounting policies and other aspects help in

building goodwill of the organization (Commonwealth Bank of Australia, 2017).

Conclusion

It can be inferred from the overall discussion held in the report that development and

publishing of proper annul disclosures is essential for business entities in order to promote

their sustainable growth and development. The business corporations operating in Australia

need to prepare their financial reports as per the AASB standards and the Corporations Act

2001. The AASB has directed all the business entities of Australia to comply with the

conceptual accounting framework principles as per the IASB accounting rules and

conventions. The analysis of the annual disclosure of the Commonwealth bank has revealed

that it has effectively adopted the conceptual accounting framework principles by providing

all the relevant, reliable, comparable and understandable information in its annual disclosure

statements. The accounting disclosure is prepared as per the industry norms in order to

remain competitive and also there is change in some accounting policies as per the mangers

decision to achieve certain desired set of objectives. The bank operates its business

corporation globally and therefore need to adopt some changes in its annual disclosures as per

the political environment of different countries. The potential area of concern for the banking

corporation is reduction in net worth over the subsequent years from 2015to 2017 and

increase of its receivables and large write-offs of its intangible assets. The banking group is

recommended to develop and implement proper strategies for overcoming these existing red

flags identified in its annual report disclosure.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

2016 Westpac Group Annual Report. 2016. [Online] Available at:

https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/ic/

2016_Westpac_Annual_Report [Accessed on: 18 September 2017].

Australia. 2011. Australian Corporations & Securities Legislation 2011: Corporations Act

2001, ASIC Act 2001, related regulations. CCH Australia Limited.

Bazley, M., Hancock, P. and Robinson, P. 2014. Contemporary Accounting PDF. Cengage

Learning Australia.

Commonwealth Bank of Australia. 2017. Annual report. [Online] Available at:

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-

reports/annual_report_2017_14_aug_2017.pdf [Accessed on: 18 September 2017].

Dagwell, R., Wines, G. and Lambert, C. 2015. Corporate Accounting in Australia. Pearson

Higher Education AU.

Henderson, S. et al. 2015. Issues in Financial Accounting. Pearson Higher Education AU.

Hoffman, C.W. 2016. Revising the Conceptual Framework of the International Standards:

IASB Proposals Met with Support and Skepticism. World Journal of Business and

Management 2 (1), pp. 1-32.

Horngren, C. et al. 2012. Financial Accounting. Pearson Higher Education AU.

Hussey, R. and Ong, A. 2005. International Financial Reporting Standards Desk Reference:

Overview, Guide, and Dictionary. John Wiley & Sons.

Hussey, R. and Ong, A. 2017. Corporate Financial Reporting. Springer.

Kenny, G. 2009. Diversification Strategy: How to Grow a Business by Diversifying

Successfully. Kogan Page Publishers.

Knight, J. 2004. Internationalization Remodeled: Definition, Approaches, and Rationales.

Journal of Studies in International Education 8 (5), pp. 5-29.

Marley, S. and Pedersen, J. 2015. Accounting for Business: An Introduction. ed, 2. Pearson

Higher Education AU.

2016 Westpac Group Annual Report. 2016. [Online] Available at:

https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/ic/

2016_Westpac_Annual_Report [Accessed on: 18 September 2017].

Australia. 2011. Australian Corporations & Securities Legislation 2011: Corporations Act

2001, ASIC Act 2001, related regulations. CCH Australia Limited.

Bazley, M., Hancock, P. and Robinson, P. 2014. Contemporary Accounting PDF. Cengage

Learning Australia.

Commonwealth Bank of Australia. 2017. Annual report. [Online] Available at:

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/annual-

reports/annual_report_2017_14_aug_2017.pdf [Accessed on: 18 September 2017].

Dagwell, R., Wines, G. and Lambert, C. 2015. Corporate Accounting in Australia. Pearson

Higher Education AU.

Henderson, S. et al. 2015. Issues in Financial Accounting. Pearson Higher Education AU.

Hoffman, C.W. 2016. Revising the Conceptual Framework of the International Standards:

IASB Proposals Met with Support and Skepticism. World Journal of Business and

Management 2 (1), pp. 1-32.

Horngren, C. et al. 2012. Financial Accounting. Pearson Higher Education AU.

Hussey, R. and Ong, A. 2005. International Financial Reporting Standards Desk Reference:

Overview, Guide, and Dictionary. John Wiley & Sons.

Hussey, R. and Ong, A. 2017. Corporate Financial Reporting. Springer.

Kenny, G. 2009. Diversification Strategy: How to Grow a Business by Diversifying

Successfully. Kogan Page Publishers.

Knight, J. 2004. Internationalization Remodeled: Definition, Approaches, and Rationales.

Journal of Studies in International Education 8 (5), pp. 5-29.

Marley, S. and Pedersen, J. 2015. Accounting for Business: An Introduction. ed, 2. Pearson

Higher Education AU.

Marley, S. and Pedersen, J. 2015. Accounting for Business: An Introduction. ed, 2. Pearson

Higher Education AU.

Mirza, A. and Ankarath, N. 2012. Wiley International Trends in Financial Reporting under

IFRS: Including Comparisons with US GAAP, China GAAP, and India Accounting

Standards. John Wiley & Sons.

Mumba, C. 2013. Understanding Accounting and Finance: Theory and Practice. USA:

Trafford Publishing.

Ordelheide, D. 2016. Transnational Accounting. Springer.

Pietra, R., McLeay, S and Ronen, J. 2013. Accounting and Regulation: New Insights on

Governance, Markets and Institutions. Springer Science & Business Media.

Sheridan, T. 2016. Managerial Fraud: Executive Impression Management, Beyond Red

Flags. Routledge.

Walton, P. 2011. A Global History of Accounting, Financial Reporting and Public Policy:

Asia and Oceania. Emerald Group Publishing.

Walton, P. 2011. A Global History of Accounting, Financial Reporting and Public Policy:

Asia and Oceania. Emerald Group Publishing.

Wolk, H., Dodd, J. and Rozycki. J. 2012. Accounting Theory: Conceptual Issues in a

Political and Economic Environment. SAGE.

Higher Education AU.

Mirza, A. and Ankarath, N. 2012. Wiley International Trends in Financial Reporting under

IFRS: Including Comparisons with US GAAP, China GAAP, and India Accounting

Standards. John Wiley & Sons.

Mumba, C. 2013. Understanding Accounting and Finance: Theory and Practice. USA:

Trafford Publishing.

Ordelheide, D. 2016. Transnational Accounting. Springer.

Pietra, R., McLeay, S and Ronen, J. 2013. Accounting and Regulation: New Insights on

Governance, Markets and Institutions. Springer Science & Business Media.

Sheridan, T. 2016. Managerial Fraud: Executive Impression Management, Beyond Red

Flags. Routledge.

Walton, P. 2011. A Global History of Accounting, Financial Reporting and Public Policy:

Asia and Oceania. Emerald Group Publishing.

Walton, P. 2011. A Global History of Accounting, Financial Reporting and Public Policy:

Asia and Oceania. Emerald Group Publishing.

Wolk, H., Dodd, J. and Rozycki. J. 2012. Accounting Theory: Conceptual Issues in a

Political and Economic Environment. SAGE.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.