Comprehensive Report on AMP Limited's Accounting Theory and Financials

VerifiedAdded on 2020/04/01

|21

|4415

|40

Report

AI Summary

This report provides a comprehensive analysis of AMP Limited, an Australian financial services company. It details the company's accounting policies, including those related to asset valuation and recent amendments. The report explores the flexibility of these policies and evaluates AMP's accounting strategy, examining the preparation of financial statements, including the income statement, balance sheet, and cash flow statement. It also discusses positive and normative accounting theories, highlighting their applications and differences. The report further assesses the quality of AMP's financial disclosures and identifies potential red flags, concluding with an overview of the company's annual report. The report follows a three-step financial statement preparation process, outlining the debit and credit balances and their treatments.

Accounting Theory and Current Issue 1

Running Head: Accounting Theory and Current Issue

Accounting Theory and Current Issue

Running Head: Accounting Theory and Current Issue

Accounting Theory and Current Issue

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory and Current Issue 2

Executive Summary

AMP is an Australian company which provides financial advice, superannuation products,

investment products, insurance, and banking products including savings accounts and home

loans. The headquarters of the company are situated in Sydney, Australia. The foundation

director of AMP limited was David Jones. Amp limited was founded in 1848. During 2010,

AMP merged with AXA Asia pacific holdings.

Executive Summary

AMP is an Australian company which provides financial advice, superannuation products,

investment products, insurance, and banking products including savings accounts and home

loans. The headquarters of the company are situated in Sydney, Australia. The foundation

director of AMP limited was David Jones. Amp limited was founded in 1848. During 2010,

AMP merged with AXA Asia pacific holdings.

Accounting Theory and Current Issue 3

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Section 1: Accounting Policies Disclosure of AMP..................................................................5

Section 2: Flexibility of Accounting policies.............................................................................5

Section 3: Accounting Strategy Evaluation...............................................................................7

Section 4: Disclosure of the Quality of Financial Statements...................................................8

Section 5: Potential Red Flags of AMP...................................................................................10

Section 6: Annual Report of the Company..............................................................................10

Conclusion................................................................................................................................15

References................................................................................................................................16

Table of Contents

Executive Summary...................................................................................................................2

Introduction................................................................................................................................4

Section 1: Accounting Policies Disclosure of AMP..................................................................5

Section 2: Flexibility of Accounting policies.............................................................................5

Section 3: Accounting Strategy Evaluation...............................................................................7

Section 4: Disclosure of the Quality of Financial Statements...................................................8

Section 5: Potential Red Flags of AMP...................................................................................10

Section 6: Annual Report of the Company..............................................................................10

Conclusion................................................................................................................................15

References................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory and Current Issue 4

Introduction

This report is based on AMP limited. This report describes the accounting policies followed

by the company and the accounting strategies. The report also contains two years annual

audited data of AMP limited. The annual report of AMP includes the consolidated financial

position, consolidated income statement , consolidated statement of changes in equity and

consolidated cash flow statement. This report clearly describes the procedure of preparation

of financial statements. This is a three step process and consists of the examples related to the

preparation of cash flow statement, trading and profit & loss account, and balance sheet

(Parker and Northcott, 2016). The two theories of financial accounting i.e. positive and

normative are also discussed in this report.

Introduction

This report is based on AMP limited. This report describes the accounting policies followed

by the company and the accounting strategies. The report also contains two years annual

audited data of AMP limited. The annual report of AMP includes the consolidated financial

position, consolidated income statement , consolidated statement of changes in equity and

consolidated cash flow statement. This report clearly describes the procedure of preparation

of financial statements. This is a three step process and consists of the examples related to the

preparation of cash flow statement, trading and profit & loss account, and balance sheet

(Parker and Northcott, 2016). The two theories of financial accounting i.e. positive and

normative are also discussed in this report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory and Current Issue 5

Section 1: Accounting Policies Disclosure of AMP

Australian Accounting Standards Board (AASB) has issued certain guidelines for the

preperation of financial statements. At the time of recording the values in the financial

statements, these values are rounded to the nearest million dollars ($m). Accounting policies

are the policies which are applied by the company at the time of making financial sttaements.

These policies includes the value at which the assets and liabilities are recorded by the

company. The assets and liabilities related to investment contracts and life insurance

contracts are measured on a fair value basis and all the other assets and liabilities are valued

on the basis of historical cost. There are some amendments in the AMP accounting policies in

the year 2015 (Francis, et al., 2016). The amendments were AASB 2014-9 which was related

to the method of equity in separate financial statements and AASB 2015-5 which was related

to the investment entities. The person who is responsible for accounting estimates is the

management itself. The material misstatement risk of accounting estimates depends upon the

subjectivity and complexity associated with the process, the number and significance of

assumptions that are made, the availability and reliability of relevant data and the probability

of uncertainty associated with the assumptions (Kvaal, 2017). The accounting policy of AMP

related to inventories includes that inventories should be included in the financial statements

at the cost of inventory or its net realisable value whichever is lower. In case of intangible

assets, only those costs are being carried forward which creates future benefits for the

company. The critical factors related to accounting estimates are that the methods of

conducting business, circumstances of the industry in which the company is operating, other

external factors and new accounting pronouncements.

Section 2: Flexibility of accounting policies

The accounting flexibility differs from firm to firm. AMP is following the accounting policies

as per the Australian accounting standards board. So, members are not having enough power

Section 1: Accounting Policies Disclosure of AMP

Australian Accounting Standards Board (AASB) has issued certain guidelines for the

preperation of financial statements. At the time of recording the values in the financial

statements, these values are rounded to the nearest million dollars ($m). Accounting policies

are the policies which are applied by the company at the time of making financial sttaements.

These policies includes the value at which the assets and liabilities are recorded by the

company. The assets and liabilities related to investment contracts and life insurance

contracts are measured on a fair value basis and all the other assets and liabilities are valued

on the basis of historical cost. There are some amendments in the AMP accounting policies in

the year 2015 (Francis, et al., 2016). The amendments were AASB 2014-9 which was related

to the method of equity in separate financial statements and AASB 2015-5 which was related

to the investment entities. The person who is responsible for accounting estimates is the

management itself. The material misstatement risk of accounting estimates depends upon the

subjectivity and complexity associated with the process, the number and significance of

assumptions that are made, the availability and reliability of relevant data and the probability

of uncertainty associated with the assumptions (Kvaal, 2017). The accounting policy of AMP

related to inventories includes that inventories should be included in the financial statements

at the cost of inventory or its net realisable value whichever is lower. In case of intangible

assets, only those costs are being carried forward which creates future benefits for the

company. The critical factors related to accounting estimates are that the methods of

conducting business, circumstances of the industry in which the company is operating, other

external factors and new accounting pronouncements.

Section 2: Flexibility of accounting policies

The accounting flexibility differs from firm to firm. AMP is following the accounting policies

as per the Australian accounting standards board. So, members are not having enough power

Accounting Theory and Current Issue 6

to assess the accounting policies and estimates (Howieson, 2017). The accounting flexibility

of AMP is under the management. So, managers are only required to follow their guidelines.

If the power of flexibility is less with the managers then the accounting data will be less

informative. If managers are having high flexibility then the accounting information will

become more informative. Positive theory of financial accounting: Accounting gives the

investors and managers a standardized system to record the financial transaction of a

company in a consistent, transparent and informative way. Today's accounting systems

provides accurate methods for representing a company's performance by carefully applying

the accounting theories. Flexibility in accounting policies helps the managers to take

decisions immediately. The company is required to allow managers to change the accounting

policy as per the need of the organization. The two major theories of accounting are positive

accounting and normative accounting. Positive accounting theory is also known as PAT.

Positive accounting theories are based on observing particular phenomena. The aim of this

theory is that by observing a number of things the person will be able to predict the future.

Positive accounting theory was developed with a view to identify the best accounting theory

for the company from the various theories used by other companies (Loyeung, et al., 2016).

Some of the examples of positive accounting theories are stakeholder theory and legitimacy

theory. The main aim of Watts and Zimmerman’s positive accounting theory is based on the

aim of identifying the relationship between the individuals which are responsible for the

output of the firm. The relationship should be between the managers and the debtors of the

firm or it might be between the managers and the owners. According to positive accounting

theory, the organization should be aligned in such a way that it can integrate the interest of

owners and managers of the firm (Ward and Lowe, 2017). In PAT, the persons who are

having the authority for the preperation of financial statements are the managers (Lukka and

Modell, 2017). The cost occurred in establishing bond between the managers for the

to assess the accounting policies and estimates (Howieson, 2017). The accounting flexibility

of AMP is under the management. So, managers are only required to follow their guidelines.

If the power of flexibility is less with the managers then the accounting data will be less

informative. If managers are having high flexibility then the accounting information will

become more informative. Positive theory of financial accounting: Accounting gives the

investors and managers a standardized system to record the financial transaction of a

company in a consistent, transparent and informative way. Today's accounting systems

provides accurate methods for representing a company's performance by carefully applying

the accounting theories. Flexibility in accounting policies helps the managers to take

decisions immediately. The company is required to allow managers to change the accounting

policy as per the need of the organization. The two major theories of accounting are positive

accounting and normative accounting. Positive accounting theory is also known as PAT.

Positive accounting theories are based on observing particular phenomena. The aim of this

theory is that by observing a number of things the person will be able to predict the future.

Positive accounting theory was developed with a view to identify the best accounting theory

for the company from the various theories used by other companies (Loyeung, et al., 2016).

Some of the examples of positive accounting theories are stakeholder theory and legitimacy

theory. The main aim of Watts and Zimmerman’s positive accounting theory is based on the

aim of identifying the relationship between the individuals which are responsible for the

output of the firm. The relationship should be between the managers and the debtors of the

firm or it might be between the managers and the owners. According to positive accounting

theory, the organization should be aligned in such a way that it can integrate the interest of

owners and managers of the firm (Ward and Lowe, 2017). In PAT, the persons who are

having the authority for the preperation of financial statements are the managers (Lukka and

Modell, 2017). The cost occurred in establishing bond between the managers for the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory and Current Issue 7

preparation of financial statements is known as bonding cost. In positive accounting theory,

the cost incurred in monitoring or auditing of financial statements is known as monitoring

cost. Another assumption of PAT is that the actions of agents are controlled by contractual

arrangements otherwise it leads to residual loss. On the other hand, normative theory of

financial accounting is completely different from PAT. Normative theory of accounting:

Normative theory does not evaluate the present condition of company. Rather than discussing

what is happening in the company, normative theory guides the developers of accounting

policies on the basis of theoretical principle. The major disadvantage of normative theory is

that it is based on theoretical principles and on the other hand, the major advantage of PAT is

that it is more practical and is related to current events (Martins and Martins, 2017).

Normative theory is more suitable for the company because this theory first analysis the

nature, structure and the issues that the company is facing then suggest the most appropriate

solution to the company. This theory is totally based on practical approach so by adopting

this theory the company will definitely get the solution for its issues because the suggestion

provided by noemative theory is practically possible. Positive accounting theory is totally a

theoretical approach. So, it only suggests the theories which are already used by some

companies. The nature and structure of every company is different. So it is possible that one

theory is best suitable for a company and will result in failure for another company because

of differentiation in operations and the issues of the company. Positive accounting theory is

based on the universally accepted principles. Normative theory is just the opposite of it.

Section 3: Accounting Strategy Evaluation

The accounting strategy of a firm should be analyzed by its performance in financial

statements. The company is required to prepare a strategy for all the activities related to

finance that may happen in the near future. Accounting strategy helps to take immediate

measures at the time of financial crises. The complexity in the preparation of financial

preparation of financial statements is known as bonding cost. In positive accounting theory,

the cost incurred in monitoring or auditing of financial statements is known as monitoring

cost. Another assumption of PAT is that the actions of agents are controlled by contractual

arrangements otherwise it leads to residual loss. On the other hand, normative theory of

financial accounting is completely different from PAT. Normative theory of accounting:

Normative theory does not evaluate the present condition of company. Rather than discussing

what is happening in the company, normative theory guides the developers of accounting

policies on the basis of theoretical principle. The major disadvantage of normative theory is

that it is based on theoretical principles and on the other hand, the major advantage of PAT is

that it is more practical and is related to current events (Martins and Martins, 2017).

Normative theory is more suitable for the company because this theory first analysis the

nature, structure and the issues that the company is facing then suggest the most appropriate

solution to the company. This theory is totally based on practical approach so by adopting

this theory the company will definitely get the solution for its issues because the suggestion

provided by noemative theory is practically possible. Positive accounting theory is totally a

theoretical approach. So, it only suggests the theories which are already used by some

companies. The nature and structure of every company is different. So it is possible that one

theory is best suitable for a company and will result in failure for another company because

of differentiation in operations and the issues of the company. Positive accounting theory is

based on the universally accepted principles. Normative theory is just the opposite of it.

Section 3: Accounting Strategy Evaluation

The accounting strategy of a firm should be analyzed by its performance in financial

statements. The company is required to prepare a strategy for all the activities related to

finance that may happen in the near future. Accounting strategy helps to take immediate

measures at the time of financial crises. The complexity in the preparation of financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory and Current Issue 8

statement depends upon the nature of the firm. Accounting strategy involves recording of all

the financial transactions in proper accounting format so that these records can be further

used for the preperation of financial statements. AMP is related to providing financial advice

so it involves recording each and every transaction on regular basis. Financial statements

include balance sheet, trial balance and profit and loss account and cash flow statement.

Income statement includes the revenues and expenses of the firm and helps in calculating net

income of the firm (Bergh, et al., 2017). Trial balance and profit and loss account are

prepared to identify the sum total of expenses and revenues of the company to determine

whether there is a profit to the company or loss. The credit side of profit and loss account

includes the revenue from dividend and interest and the debit of profit and loss account

includes all the expenses made by the company like advertisement, insurance, salaries,

carriage outward, trade expenses and any other expense. Balance sheet is prepared to measure

the actual performance of the company. Balance sheet is the sum total of all the other

financial statements. Balance sheet includes the fixed assets, fixed liabilities, current assets,

current liabilities and equity shareholders and preference shareholders. The total of both

liabilities and assets is equal in balance sheet. The reason behind this balance is that the

company uses all its liabilities in the purchase of assets. Cash flow statement is divided in

three parts i.e. operating, financing and investing activities. Cash flow statement shows the

sources and uses of cash. There are two methods of preparing cash flow statement, one is

direct method. In direct method cash flow information is measured by directly subtracting the

expenses from cash receipts. In case of indirect method, one can arrive to cash flow

information by adding or subtracting non-cash items from net income (Newcastle University,

2017).

There are three steps for the preparation of financial statement (Chiapello, 2017) i.e.

understanding the meaning of debit and credit balances, analyse the debit and credit balances

statement depends upon the nature of the firm. Accounting strategy involves recording of all

the financial transactions in proper accounting format so that these records can be further

used for the preperation of financial statements. AMP is related to providing financial advice

so it involves recording each and every transaction on regular basis. Financial statements

include balance sheet, trial balance and profit and loss account and cash flow statement.

Income statement includes the revenues and expenses of the firm and helps in calculating net

income of the firm (Bergh, et al., 2017). Trial balance and profit and loss account are

prepared to identify the sum total of expenses and revenues of the company to determine

whether there is a profit to the company or loss. The credit side of profit and loss account

includes the revenue from dividend and interest and the debit of profit and loss account

includes all the expenses made by the company like advertisement, insurance, salaries,

carriage outward, trade expenses and any other expense. Balance sheet is prepared to measure

the actual performance of the company. Balance sheet is the sum total of all the other

financial statements. Balance sheet includes the fixed assets, fixed liabilities, current assets,

current liabilities and equity shareholders and preference shareholders. The total of both

liabilities and assets is equal in balance sheet. The reason behind this balance is that the

company uses all its liabilities in the purchase of assets. Cash flow statement is divided in

three parts i.e. operating, financing and investing activities. Cash flow statement shows the

sources and uses of cash. There are two methods of preparing cash flow statement, one is

direct method. In direct method cash flow information is measured by directly subtracting the

expenses from cash receipts. In case of indirect method, one can arrive to cash flow

information by adding or subtracting non-cash items from net income (Newcastle University,

2017).

There are three steps for the preparation of financial statement (Chiapello, 2017) i.e.

understanding the meaning of debit and credit balances, analyse the debit and credit balances

Accounting Theory and Current Issue 9

and treatment of debit and credit balances. Understanding the meaning of debit and credit

balances: The first step related to the preparation of financial statements is proper

understanding of debit and credit balances. It is divided into two parts. First is debit balance

in trial balance. The debit balance in trial balance consists of expenses and losses or deferred

revenue expenditure and assets (Vardon, et al., 2016). Second is credit balance of trial

balance. The credit balance consists of revenue and gains or liabilities, capital, provision and

reserves. The second step is analyzing which debit balance is an asset and which debit

balance is expenditure or loss. In the same way, which credit balance is a liability and which

credit balance is an income or gain. While analysing the debit balance, if the balance is being

recovered by the firm then it should be treated as an asset and if the balance should not be

recovered then it should be a loss to the firm (Cornell and Warne, 2016). On the other hand,

if the firm is liable to pay any amount to the creditor then it should be treated as liability to

the firm and if the firm is not liable to pay any amount to creditor then it should be treated as

gain. The third step of financial accounting process is the treatment of debit and credit

balance. Treatment of debit balances: The balances of losses and expenses on the basis of

direct or indirect are transferred to the debit side of either Profit & Loss Account or Trading

Account as the case may be. The deferred revenue expenses and assets are directly

transferred to the asset side of balance sheet. Treatment of credit balances: The balances of

revenues and gains on the basis of direct or indirect, are transferred to the credit side of either

Profit & Loss Account or Trading Account as the case may be (Bailey, 2016). The balances

of liabilities, provisions, capital and reserves are transferred to the liabilities side of the

balance sheet.

Section 4: Disclosure of the Quality of Financial Statements

AMP is maintaining transparency, accuracy and consistency in its accounting records. It

increases the quality of financial statements. Every company is required to disclose the

and treatment of debit and credit balances. Understanding the meaning of debit and credit

balances: The first step related to the preparation of financial statements is proper

understanding of debit and credit balances. It is divided into two parts. First is debit balance

in trial balance. The debit balance in trial balance consists of expenses and losses or deferred

revenue expenditure and assets (Vardon, et al., 2016). Second is credit balance of trial

balance. The credit balance consists of revenue and gains or liabilities, capital, provision and

reserves. The second step is analyzing which debit balance is an asset and which debit

balance is expenditure or loss. In the same way, which credit balance is a liability and which

credit balance is an income or gain. While analysing the debit balance, if the balance is being

recovered by the firm then it should be treated as an asset and if the balance should not be

recovered then it should be a loss to the firm (Cornell and Warne, 2016). On the other hand,

if the firm is liable to pay any amount to the creditor then it should be treated as liability to

the firm and if the firm is not liable to pay any amount to creditor then it should be treated as

gain. The third step of financial accounting process is the treatment of debit and credit

balance. Treatment of debit balances: The balances of losses and expenses on the basis of

direct or indirect are transferred to the debit side of either Profit & Loss Account or Trading

Account as the case may be. The deferred revenue expenses and assets are directly

transferred to the asset side of balance sheet. Treatment of credit balances: The balances of

revenues and gains on the basis of direct or indirect, are transferred to the credit side of either

Profit & Loss Account or Trading Account as the case may be (Bailey, 2016). The balances

of liabilities, provisions, capital and reserves are transferred to the liabilities side of the

balance sheet.

Section 4: Disclosure of the Quality of Financial Statements

AMP is maintaining transparency, accuracy and consistency in its accounting records. It

increases the quality of financial statements. Every company is required to disclose the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory and Current Issue 10

material information to its human resources. The goal is achieved with the contribution of

employees and if the company hides the material information from the employees then it will

become a little confusing for the employees that in which direction they have to work and if

the employees get to know about the hidden information then it will lower down their morale

because they will think that the company is not trusting them. In case of financial statements,

the balance at the end of each year is being carried forward to the next year. If there is any

material misstatement in one year then it is going to affect the quality of the financial

statement of next years till the mistake is identified by the company. The quality of disclosure

helps the company to avoid the interference of government in the operations of the company.

the quality fo financial statements also maintains the reputation of the company. GAAP refers

to generally accepted accounting principles. GAAP consists of the crucial principles of

accounting which increases the quality of financial records. GAAP helps in the maintenance

of consistency in accounting. GAAP helps to avoid the manager’s ability to misstate any

information in the financial statements. GAAP is a network of experts of accounting. GAAP

includes few best Australian minds. These experts helps in setting out the principles as per

the nature and structure of the company. The financial records of the company must be

disclosed in this way (Almeida and Fernando, 2017).

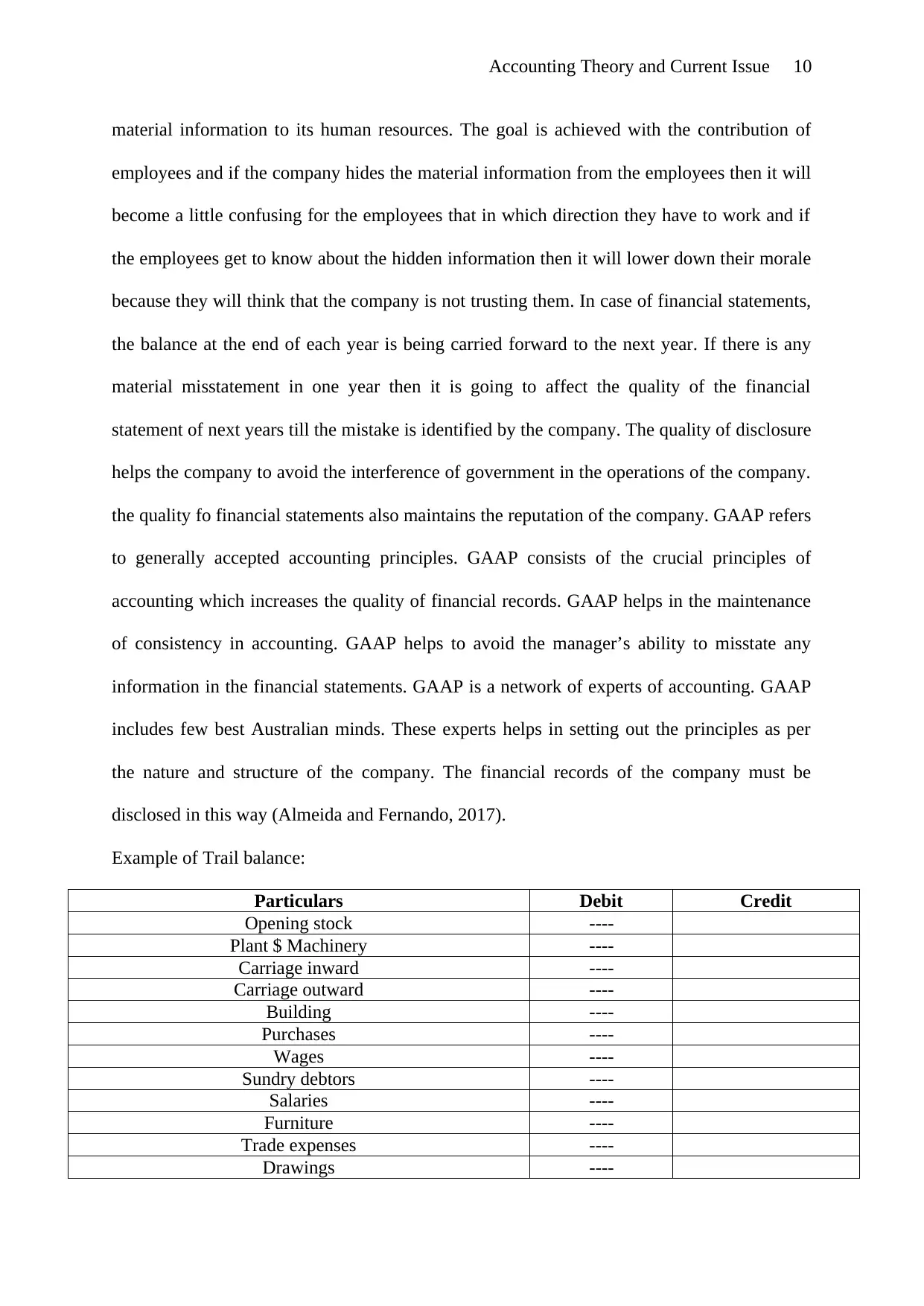

Example of Trail balance:

Particulars Debit Credit

Opening stock ----

Plant $ Machinery ----

Carriage inward ----

Carriage outward ----

Building ----

Purchases ----

Wages ----

Sundry debtors ----

Salaries ----

Furniture ----

Trade expenses ----

Drawings ----

material information to its human resources. The goal is achieved with the contribution of

employees and if the company hides the material information from the employees then it will

become a little confusing for the employees that in which direction they have to work and if

the employees get to know about the hidden information then it will lower down their morale

because they will think that the company is not trusting them. In case of financial statements,

the balance at the end of each year is being carried forward to the next year. If there is any

material misstatement in one year then it is going to affect the quality of the financial

statement of next years till the mistake is identified by the company. The quality of disclosure

helps the company to avoid the interference of government in the operations of the company.

the quality fo financial statements also maintains the reputation of the company. GAAP refers

to generally accepted accounting principles. GAAP consists of the crucial principles of

accounting which increases the quality of financial records. GAAP helps in the maintenance

of consistency in accounting. GAAP helps to avoid the manager’s ability to misstate any

information in the financial statements. GAAP is a network of experts of accounting. GAAP

includes few best Australian minds. These experts helps in setting out the principles as per

the nature and structure of the company. The financial records of the company must be

disclosed in this way (Almeida and Fernando, 2017).

Example of Trail balance:

Particulars Debit Credit

Opening stock ----

Plant $ Machinery ----

Carriage inward ----

Carriage outward ----

Building ----

Purchases ----

Wages ----

Sundry debtors ----

Salaries ----

Furniture ----

Trade expenses ----

Drawings ----

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory and Current Issue 11

Advertisement ----

Insurance ----

Discount on sales ----

Bad debts ----

Bills receivable ----

Bank balances ----

Capital ----

Sundry creditors ----

Sales ----

Bank loan ----

Interest received ----

Discount on purchases ----

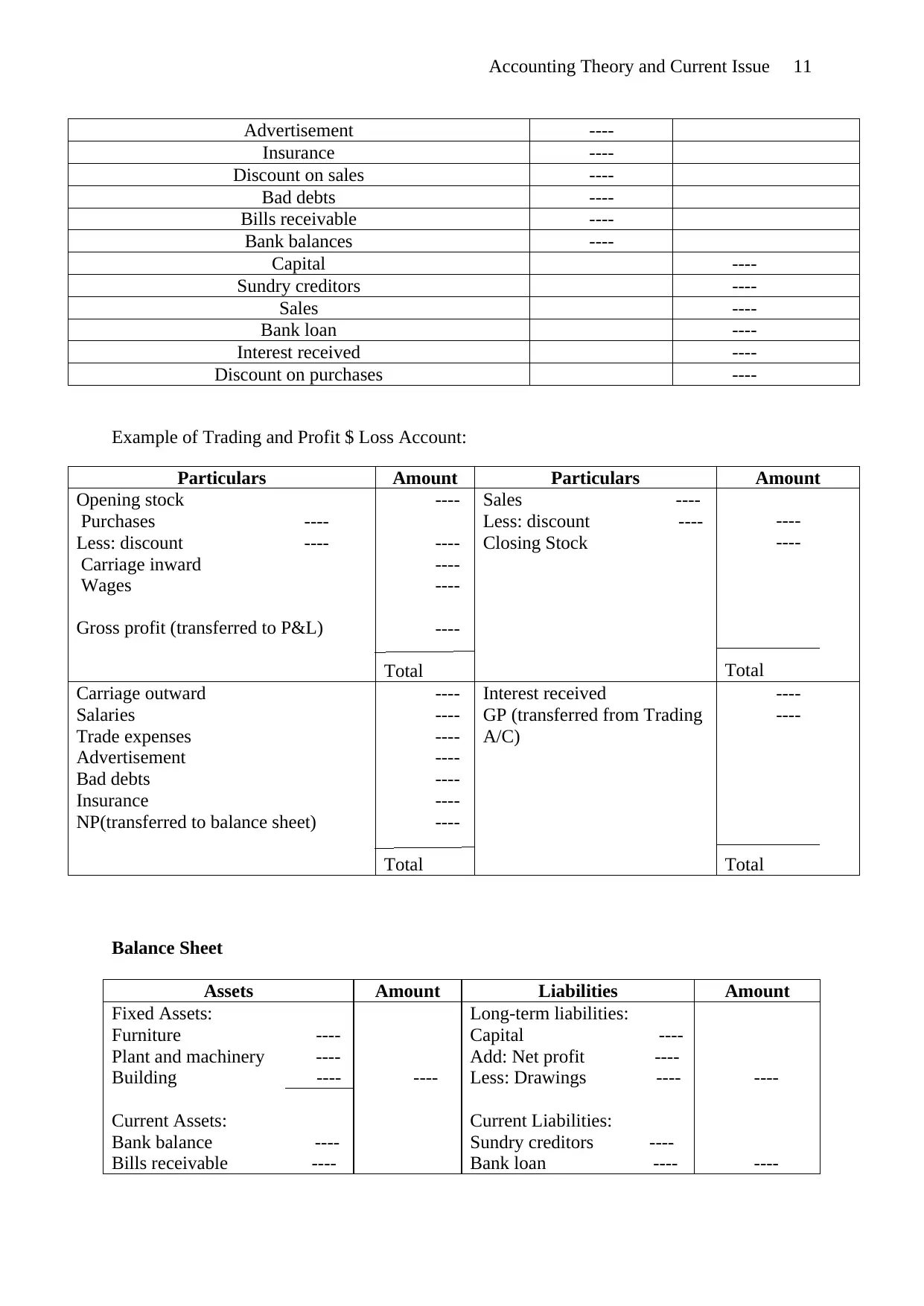

Example of Trading and Profit $ Loss Account:

Particulars Amount Particulars Amount

Opening stock

Purchases ----

Less: discount ----

Carriage inward

Wages

Gross profit (transferred to P&L)

----

----

----

----

----

Total

Sales ----

Less: discount ----

Closing Stock

----

----

Total

Carriage outward

Salaries

Trade expenses

Advertisement

Bad debts

Insurance

NP(transferred to balance sheet)

----

----

----

----

----

----

----

Total

Interest received

GP (transferred from Trading

A/C)

----

----

Total

Balance Sheet

Assets Amount Liabilities Amount

Fixed Assets:

Furniture ----

Plant and machinery ----

Building ----

Current Assets:

Bank balance ----

Bills receivable ----

----

Long-term liabilities:

Capital ----

Add: Net profit ----

Less: Drawings ----

Current Liabilities:

Sundry creditors ----

Bank loan ----

----

----

Advertisement ----

Insurance ----

Discount on sales ----

Bad debts ----

Bills receivable ----

Bank balances ----

Capital ----

Sundry creditors ----

Sales ----

Bank loan ----

Interest received ----

Discount on purchases ----

Example of Trading and Profit $ Loss Account:

Particulars Amount Particulars Amount

Opening stock

Purchases ----

Less: discount ----

Carriage inward

Wages

Gross profit (transferred to P&L)

----

----

----

----

----

Total

Sales ----

Less: discount ----

Closing Stock

----

----

Total

Carriage outward

Salaries

Trade expenses

Advertisement

Bad debts

Insurance

NP(transferred to balance sheet)

----

----

----

----

----

----

----

Total

Interest received

GP (transferred from Trading

A/C)

----

----

Total

Balance Sheet

Assets Amount Liabilities Amount

Fixed Assets:

Furniture ----

Plant and machinery ----

Building ----

Current Assets:

Bank balance ----

Bills receivable ----

----

Long-term liabilities:

Capital ----

Add: Net profit ----

Less: Drawings ----

Current Liabilities:

Sundry creditors ----

Bank loan ----

----

----

Accounting Theory and Current Issue 12

Sundry debtors ----

Closing stock ---- ----

Total Total

Section 5: Potential Red Flags of AMP

The red flags indicate the most crucial factors of the company which leads to fraud if not

properly analysed. The management is responsible for everything that is happening in the

company. Red flags are not the sign of happening of fraud. Red flag # 1 indicates inability to

reconcile financial accounts on regular basis. If the company is unable to update the

transactions done on regular basis then it leads to misrepresentation of transaction because of

which the chances of fraud increases within the organization. Misrepresentation is a form of

fraud which means intentional mistake in the recording of the actual transactions. Red flag #

2 is a sign of unexplained variances in the financial records. Negative variances occurs when

the actual revenues are lower than the revenues planned while making the strategy and

positive variances occurs when the actual expenses are lower than planned expenses. These

variances are required to described carefully by the managers. If there remains any kind of

unexplained variance then it leads to fraud within the organization. Red flag # 3 indicates the

inquiry about large quantities adjustment or significant dollar amount adjustments. It means

the company is required to analyse in detail the large quantity adjustments. While the

procurement of raw material, the company is required to determine the difference between

the pre-decided requirement of raw material and the actual quantity of raw material

purchased. If there is a huge difference then this will indicate the chances of fraud. So, the

company is required to focus on the quantity of material used to avoid the occurrence of

fraud. Red flag # 4 indicates illogical discrepancies in the budgeted and actual results.

Discrepancies are common in actual and budgeted results because the budgeted results are

estimated as per the internal and external environmental conditions in that particular period of

Sundry debtors ----

Closing stock ---- ----

Total Total

Section 5: Potential Red Flags of AMP

The red flags indicate the most crucial factors of the company which leads to fraud if not

properly analysed. The management is responsible for everything that is happening in the

company. Red flags are not the sign of happening of fraud. Red flag # 1 indicates inability to

reconcile financial accounts on regular basis. If the company is unable to update the

transactions done on regular basis then it leads to misrepresentation of transaction because of

which the chances of fraud increases within the organization. Misrepresentation is a form of

fraud which means intentional mistake in the recording of the actual transactions. Red flag #

2 is a sign of unexplained variances in the financial records. Negative variances occurs when

the actual revenues are lower than the revenues planned while making the strategy and

positive variances occurs when the actual expenses are lower than planned expenses. These

variances are required to described carefully by the managers. If there remains any kind of

unexplained variance then it leads to fraud within the organization. Red flag # 3 indicates the

inquiry about large quantities adjustment or significant dollar amount adjustments. It means

the company is required to analyse in detail the large quantity adjustments. While the

procurement of raw material, the company is required to determine the difference between

the pre-decided requirement of raw material and the actual quantity of raw material

purchased. If there is a huge difference then this will indicate the chances of fraud. So, the

company is required to focus on the quantity of material used to avoid the occurrence of

fraud. Red flag # 4 indicates illogical discrepancies in the budgeted and actual results.

Discrepancies are common in actual and budgeted results because the budgeted results are

estimated as per the internal and external environmental conditions in that particular period of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.