Executive Pay and Agency Theory: Tabcorp Case Study Analysis

VerifiedAdded on 2023/06/11

|13

|2741

|93

Report

AI Summary

This report delves into the complexities of executive compensation, examining its relationship with agency theory and performance measurement. It analyzes how organizations balance the need to incentivize managers with the risks associated with performance-based pay. The report includes an analysis of Tabcorp's remuneration report, focusing on short-term and long-term compensation components, performance-based pay proportions, and accounting performance measures used for bonus determination. It also discusses potential accounting decisions a CEO might make to maximize their bonus and how agency theory explains various remuneration components. Furthermore, the report addresses agency problems between managers and shareholders, such as dividend retention and horizon problems, and suggests mitigation strategies. Finally, it explores lending problems during economic downturns, highlighting the role of managerial risk aversion and agency problems in averting risks, with recommendations for banks to mitigate these risks through thorough credit checks, customer relationship building, and establishing clear credit terms.

Running head: ACCOUNTING THEORY

Accounting Theory

Name of Student:

Name of University:

Author’s Note:

Accounting Theory

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2..................................................................................................................3

Part A...........................................................................................................................................3

Part B...........................................................................................................................................5

Part C...........................................................................................................................................5

Part D...........................................................................................................................................6

Part E...........................................................................................................................................6

Answer to Question 3......................................................................................................................6

Answer to Question 4......................................................................................................................8

References......................................................................................................................................10

Table of Contents

Answer to Question 1......................................................................................................................2

Answer to Question 2..................................................................................................................3

Part A...........................................................................................................................................3

Part B...........................................................................................................................................5

Part C...........................................................................................................................................5

Part D...........................................................................................................................................6

Part E...........................................................................................................................................6

Answer to Question 3......................................................................................................................6

Answer to Question 4......................................................................................................................8

References......................................................................................................................................10

2ACCOUNTING THEORY

Answer to Question 1

The outcry for the executive compensation is depicted with companies which are seen to

be having movement towards performance-based compensation. It has been identified that in

general the corporate boards of directors increasingly provide the compensation under the greater

portion of the executive pay in form of the contingent compensation arrangements instead of

guaranteed salary base. The contingent compensation in many situations are responsible

introducing the element of risk to the executives. In situations where the executive receives the

amount of the salary in form of the fixed salary then it is regardless of the performance of the

company. It needs to be further identified that the various types of the information gathered for

the different types of the sources associated to the various types of the consideration for the

aspects are fixed base of salary is identified with regardless of how a company performs in

general (Ferlay et al. 2015).

The term “contingent compensation” or "performance-based compensation" refers to the

various types of the methods of the compensation focused on the merit spay of the long-term

incentive compensation. In general, the executive compensation is seen to include various types

of the contingent compensation mostly in short-term bonus plan payments and lon-term

compensations like stock options and stock bonuses (Schaeck and Cihák 2014).

The short-term incentive is seen to be based on the different types of the consideration

which are seen to be considered as per the typical compensation given to the executives which

seen to be considered as per the association of the data related to the certain measures of the

performance of the company. Typically the board compensation for the compensation committee

in considered outside in terms of the plan established with the various types of the benchmarks

Answer to Question 1

The outcry for the executive compensation is depicted with companies which are seen to

be having movement towards performance-based compensation. It has been identified that in

general the corporate boards of directors increasingly provide the compensation under the greater

portion of the executive pay in form of the contingent compensation arrangements instead of

guaranteed salary base. The contingent compensation in many situations are responsible

introducing the element of risk to the executives. In situations where the executive receives the

amount of the salary in form of the fixed salary then it is regardless of the performance of the

company. It needs to be further identified that the various types of the information gathered for

the different types of the sources associated to the various types of the consideration for the

aspects are fixed base of salary is identified with regardless of how a company performs in

general (Ferlay et al. 2015).

The term “contingent compensation” or "performance-based compensation" refers to the

various types of the methods of the compensation focused on the merit spay of the long-term

incentive compensation. In general, the executive compensation is seen to include various types

of the contingent compensation mostly in short-term bonus plan payments and lon-term

compensations like stock options and stock bonuses (Schaeck and Cihák 2014).

The short-term incentive is seen to be based on the different types of the consideration

which are seen to be considered as per the typical compensation given to the executives which

seen to be considered as per the association of the data related to the certain measures of the

performance of the company. Typically the board compensation for the compensation committee

in considered outside in terms of the plan established with the various types of the benchmarks

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY

which are needed to be considered with the various types of the factors which are directly

associated to the firms for measuring the categories of information like EPS, ROA and ROE. In

case the company intends to achieve the various types of the consideration of the information

which are not meeting the goal then only a small amount of bonus is paid. The most evident form

of the long-term compensation is associated to the stock options which are seen to be given as

per the right of the holder. It needs to be also discerned that in general the stock price of a

company is fixed at the grant date (Financial Times 2015).

The equity theory is identified as variation of the balance theory which considers that the

behaviour is initiated, sustained and directed by the important outcomes and objectives of the

work performance. It needs to be further discerned that the equity theory holds the internal

balance of the of the psychological tensions. This theory is applicable in the workplace and

concentrating on Festinger’s theory of the cognitive dissonance. A more likely result of the

perception of this consideration has been seen to be focused toward the various types of the

depictions which are considered with reducing the productivity (OECD 2015).

Answer to Question 2

The following excerpts of the information have been extracted from the remuneration

report of Tabcorp, which is a publicly listed company in Australia.

Part A

The target mix of the CEO and MD is seen to be stated with 67% of at risk performance

and 50% equity based. The short term executive KMP is seen to be delivered as per the mix of

cash and restricted shares.

which are needed to be considered with the various types of the factors which are directly

associated to the firms for measuring the categories of information like EPS, ROA and ROE. In

case the company intends to achieve the various types of the consideration of the information

which are not meeting the goal then only a small amount of bonus is paid. The most evident form

of the long-term compensation is associated to the stock options which are seen to be given as

per the right of the holder. It needs to be also discerned that in general the stock price of a

company is fixed at the grant date (Financial Times 2015).

The equity theory is identified as variation of the balance theory which considers that the

behaviour is initiated, sustained and directed by the important outcomes and objectives of the

work performance. It needs to be further discerned that the equity theory holds the internal

balance of the of the psychological tensions. This theory is applicable in the workplace and

concentrating on Festinger’s theory of the cognitive dissonance. A more likely result of the

perception of this consideration has been seen to be focused toward the various types of the

depictions which are considered with reducing the productivity (OECD 2015).

Answer to Question 2

The following excerpts of the information have been extracted from the remuneration

report of Tabcorp, which is a publicly listed company in Australia.

Part A

The target mix of the CEO and MD is seen to be stated with 67% of at risk performance

and 50% equity based. The short term executive KMP is seen to be delivered as per the mix of

cash and restricted shares.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY

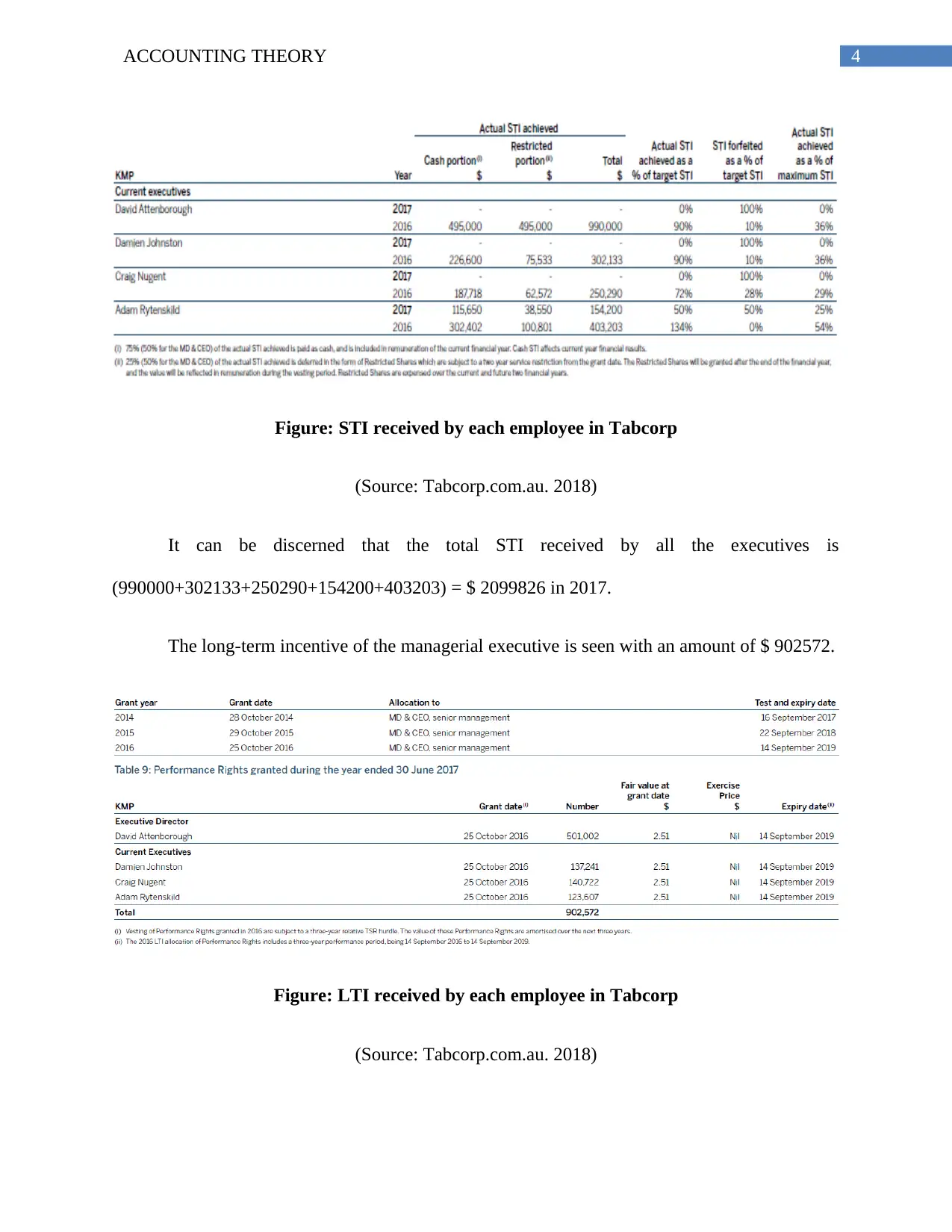

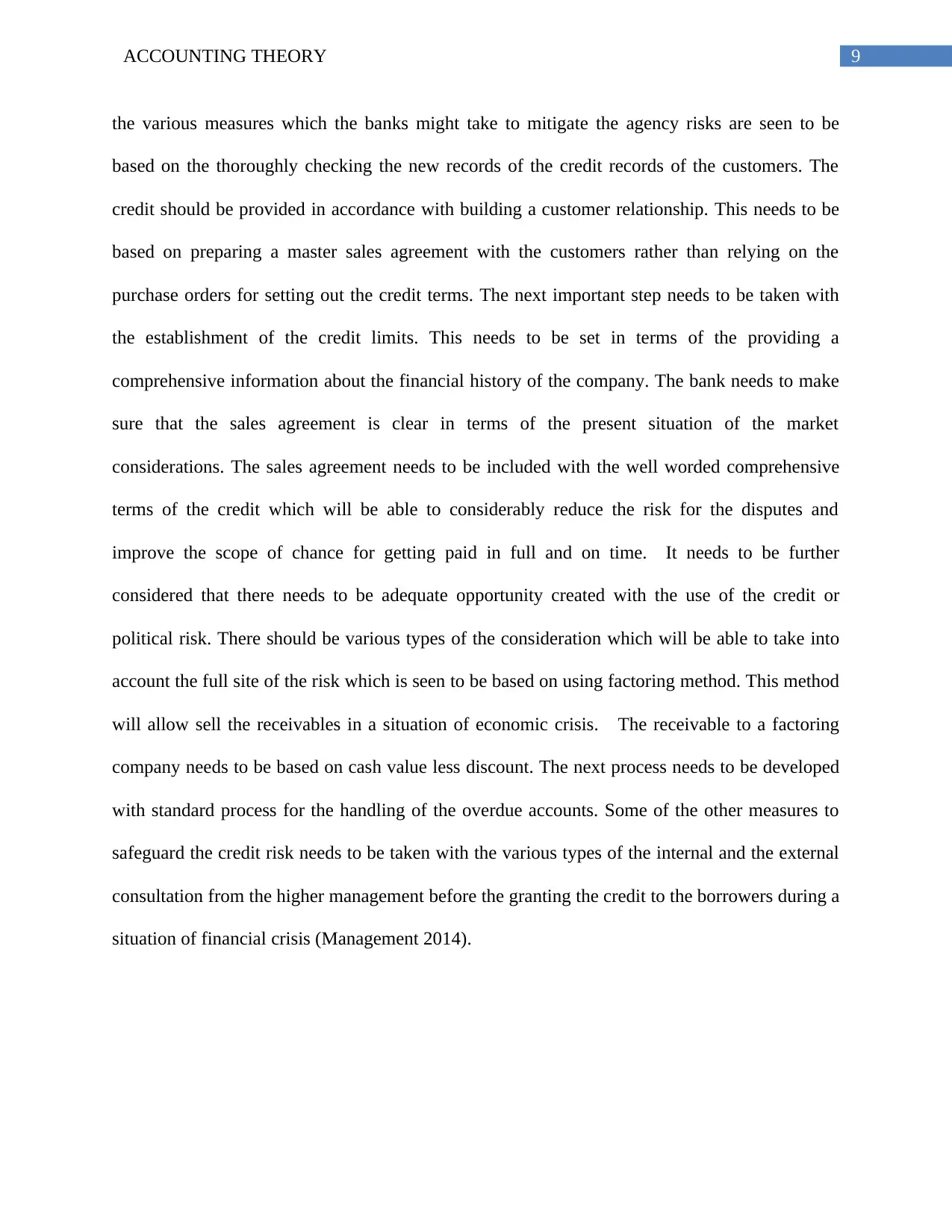

Figure: STI received by each employee in Tabcorp

(Source: Tabcorp.com.au. 2018)

It can be discerned that the total STI received by all the executives is

(990000+302133+250290+154200+403203) = $ 2099826 in 2017.

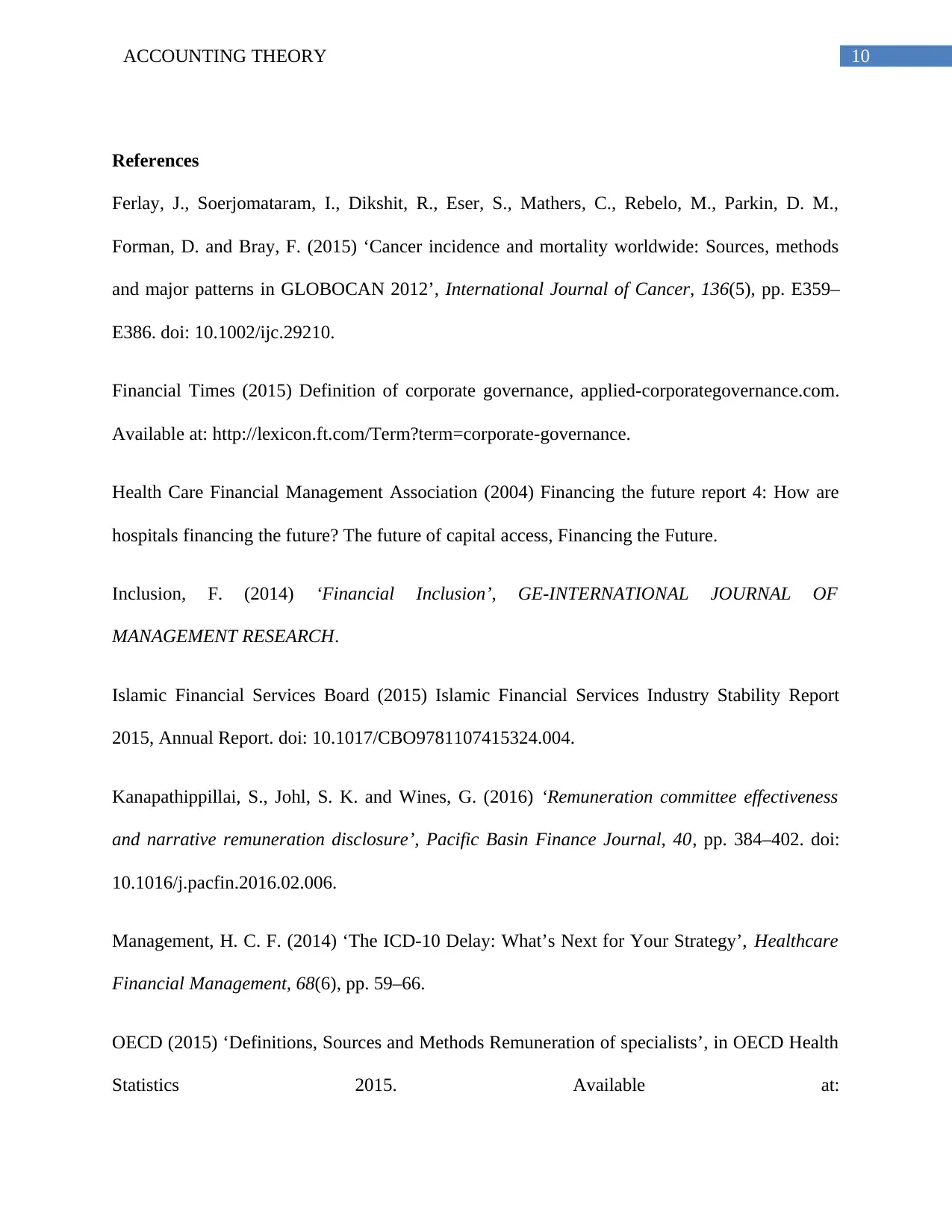

The long-term incentive of the managerial executive is seen with an amount of $ 902572.

Figure: LTI received by each employee in Tabcorp

(Source: Tabcorp.com.au. 2018)

Figure: STI received by each employee in Tabcorp

(Source: Tabcorp.com.au. 2018)

It can be discerned that the total STI received by all the executives is

(990000+302133+250290+154200+403203) = $ 2099826 in 2017.

The long-term incentive of the managerial executive is seen with an amount of $ 902572.

Figure: LTI received by each employee in Tabcorp

(Source: Tabcorp.com.au. 2018)

5ACCOUNTING THEORY

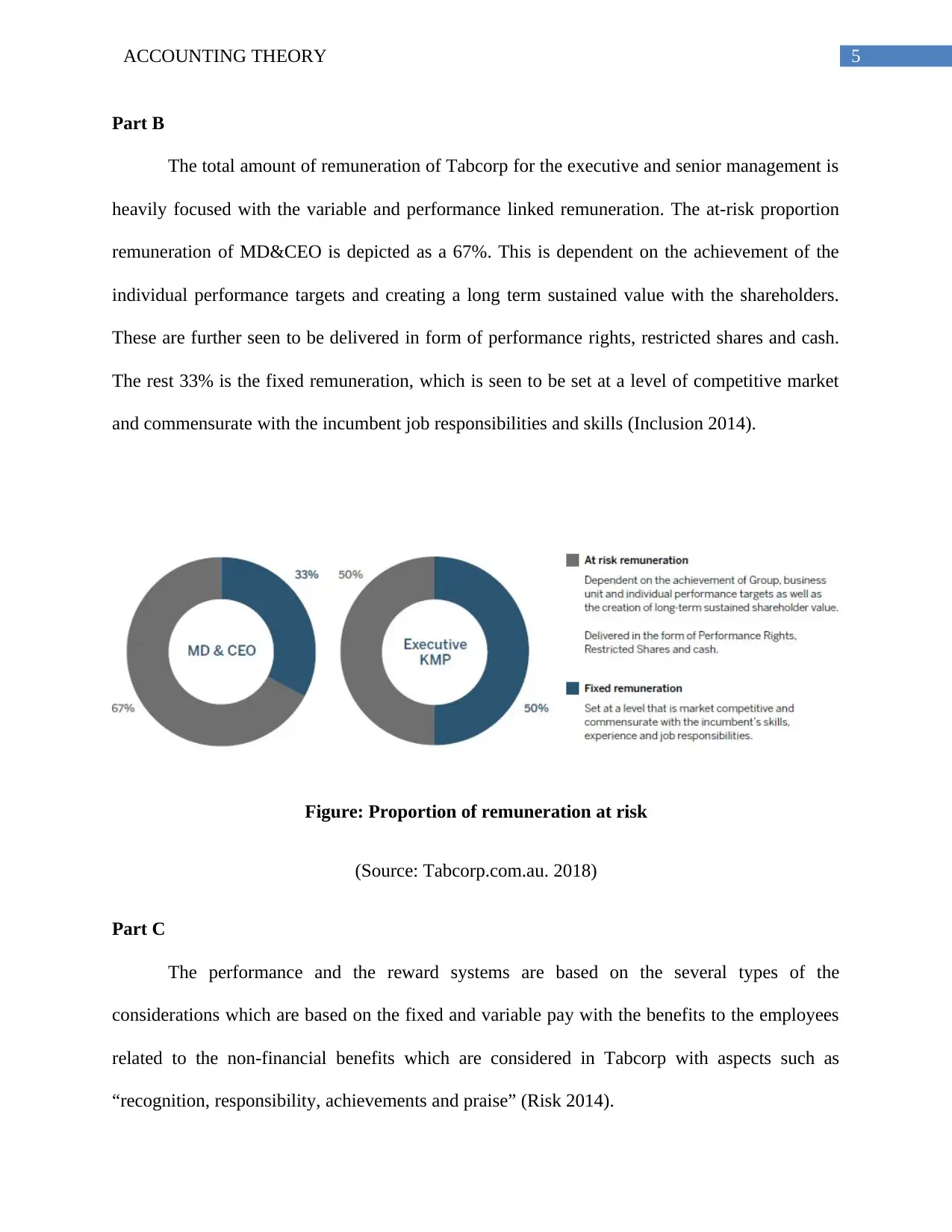

Part B

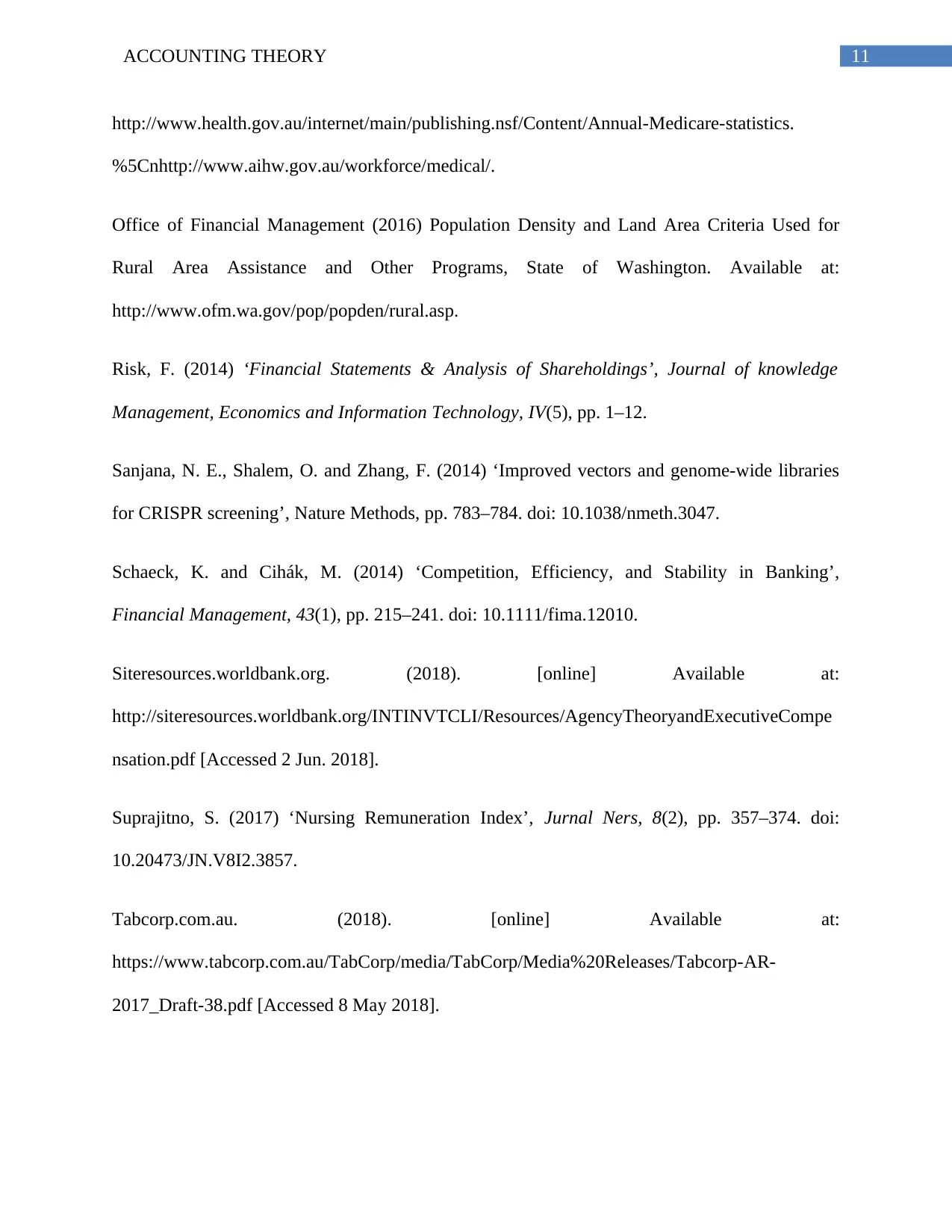

The total amount of remuneration of Tabcorp for the executive and senior management is

heavily focused with the variable and performance linked remuneration. The at-risk proportion

remuneration of MD&CEO is depicted as a 67%. This is dependent on the achievement of the

individual performance targets and creating a long term sustained value with the shareholders.

These are further seen to be delivered in form of performance rights, restricted shares and cash.

The rest 33% is the fixed remuneration, which is seen to be set at a level of competitive market

and commensurate with the incumbent job responsibilities and skills (Inclusion 2014).

Figure: Proportion of remuneration at risk

(Source: Tabcorp.com.au. 2018)

Part C

The performance and the reward systems are based on the several types of the

considerations which are based on the fixed and variable pay with the benefits to the employees

related to the non-financial benefits which are considered in Tabcorp with aspects such as

“recognition, responsibility, achievements and praise” (Risk 2014).

Part B

The total amount of remuneration of Tabcorp for the executive and senior management is

heavily focused with the variable and performance linked remuneration. The at-risk proportion

remuneration of MD&CEO is depicted as a 67%. This is dependent on the achievement of the

individual performance targets and creating a long term sustained value with the shareholders.

These are further seen to be delivered in form of performance rights, restricted shares and cash.

The rest 33% is the fixed remuneration, which is seen to be set at a level of competitive market

and commensurate with the incumbent job responsibilities and skills (Inclusion 2014).

Figure: Proportion of remuneration at risk

(Source: Tabcorp.com.au. 2018)

Part C

The performance and the reward systems are based on the several types of the

considerations which are based on the fixed and variable pay with the benefits to the employees

related to the non-financial benefits which are considered in Tabcorp with aspects such as

“recognition, responsibility, achievements and praise” (Risk 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY

Part D

There is significant scope for the company for taking accounting decisions which may

maximise bonus of the CEO. These needs to be considered with the different types of the

considerations for recognizing job values with several range of benefits provided to the

employee. These benefits are further seen to be considered with the performance management

techniques. It needs to be further seen that there are several types of the measures for taking into

considerations the different types of the aspects of the “market-rate and job analyses based on

performance management”. The company also needs to identify the various types of the issues

which are prevalent in terms of the attainment of the organizational goals and employee

performance (Health Care Financial Management Association 2014).

Part E

A study conducted on enterprises aims to show to what extent agency theory has been

able to explain the various aspects of CEO compensation on the state-owned enterprises (SOEs)

in China during 1980s. The study is able to discern that there has been a significant amount of

sensitivity related to the variance of performance. Based on the application of the agency theory

the price sensitivity among the CEO pay is seen to increase with marginal return to executive

action where the price sensitive increases with the managerial control rights, worker incentives

and profit retention rates of the firms (Siteresources.worldbank.org 2018).

Answer to Question 3

It needs to be understood that the separation of the control and ownership suggests that

managers will be able to act on their own interest which may not be in favour of the

shareholders. It needs to be further depicted that there may be several instances in which the

Part D

There is significant scope for the company for taking accounting decisions which may

maximise bonus of the CEO. These needs to be considered with the different types of the

considerations for recognizing job values with several range of benefits provided to the

employee. These benefits are further seen to be considered with the performance management

techniques. It needs to be further seen that there are several types of the measures for taking into

considerations the different types of the aspects of the “market-rate and job analyses based on

performance management”. The company also needs to identify the various types of the issues

which are prevalent in terms of the attainment of the organizational goals and employee

performance (Health Care Financial Management Association 2014).

Part E

A study conducted on enterprises aims to show to what extent agency theory has been

able to explain the various aspects of CEO compensation on the state-owned enterprises (SOEs)

in China during 1980s. The study is able to discern that there has been a significant amount of

sensitivity related to the variance of performance. Based on the application of the agency theory

the price sensitivity among the CEO pay is seen to increase with marginal return to executive

action where the price sensitive increases with the managerial control rights, worker incentives

and profit retention rates of the firms (Siteresources.worldbank.org 2018).

Answer to Question 3

It needs to be understood that the separation of the control and ownership suggests that

managers will be able to act on their own interest which may not be in favour of the

shareholders. It needs to be further depicted that there may be several instances in which the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY

interest of the interests of the shareholders due to the problem of the human capital. The

managers prefer diversification of risk rather than increasing the value of the firm with higher

risk projects (Sanjana, Shalem and Zhang 2014).

The two specific problems of relationship between shareholders and managers are stated below

as follows:

Dividend Retention Problem

In this problem of the agency theory the managers prefer to pay out less of the future

earning’s in terms of dividends rather than paying their own pre-requisites.

Horizon Problem

The horizon problem is considered with the situation where the managers are interested

in the cash flows which might impact on the remuneration for a certain time when they remain

with the firm. Despite of this, there has been several considerations which has been able to state

that there have been several instances of the firm in which shareholders may have a long-term

interest in the cash flows of the firm, because the share price is equal to the present value of the

shareholders for all the future cash flows (Islamic Financial Services Board 2015).

Some of the main examples to avert such risks needs to be considered with the various

types of the consideration which are seen to be related to the Bonus schemes which can reduce

he managers remuneration index in terms of the firm’s performance which are having a high

correlation with the firm’s value. For instance, these may be considered with the items such as

share prices and earnings. This has been further seen to be understood with the different types of

the considerations which are associated to the managerial compensation and performance ex ante

interest of the interests of the shareholders due to the problem of the human capital. The

managers prefer diversification of risk rather than increasing the value of the firm with higher

risk projects (Sanjana, Shalem and Zhang 2014).

The two specific problems of relationship between shareholders and managers are stated below

as follows:

Dividend Retention Problem

In this problem of the agency theory the managers prefer to pay out less of the future

earning’s in terms of dividends rather than paying their own pre-requisites.

Horizon Problem

The horizon problem is considered with the situation where the managers are interested

in the cash flows which might impact on the remuneration for a certain time when they remain

with the firm. Despite of this, there has been several considerations which has been able to state

that there have been several instances of the firm in which shareholders may have a long-term

interest in the cash flows of the firm, because the share price is equal to the present value of the

shareholders for all the future cash flows (Islamic Financial Services Board 2015).

Some of the main examples to avert such risks needs to be considered with the various

types of the consideration which are seen to be related to the Bonus schemes which can reduce

he managers remuneration index in terms of the firm’s performance which are having a high

correlation with the firm’s value. For instance, these may be considered with the items such as

share prices and earnings. This has been further seen to be understood with the different types of

the considerations which are associated to the managerial compensation and performance ex ante

8ACCOUNTING THEORY

without the consideration for relying on the ex post mechanism like renegotiating with the salary

(Suprajitno 2017).

Remunerations may be also linked to the various types of the dividend payout ratios or

the options for the share bonus schemes. It is seen to be more likely that a bonus plan will be

able to reward the managers only there is an expected level of the profit of the frim for a certain

period. Only then there will be a considerable amount of increase in the revenue of the company

and the mangers will be able to increase their bonus thereby increasing the profitability of the

firm (Office of Financial Management 2016).

Answer to Question 4

In general, there has been several types of the lending problems which are associated to

lending in a situation of economic downturn. In this context the presence of the various types of

the manager agency problems and managerial risk aversion problems will be able to avert

significant degree of risk which are seen to be associated to the different aspect of the

consideration of the data which are seen to be associated to the managerial risk aversion and

agency problems. The empirical model of bank tends to focus on the disciplinary role of

franchise value and ownership structure, thereby posing risk to the banks. In several cases the

risk is depicted to be lower at banks with no insider holdings. This has been able to significantly

suggest the various types of the considerations which are associated to the problems which

affects the banks in major way (Kanapathippillai, Johl and Wines 2016).

There are several previous literatures which has been able to state on the agency

problems which provides the explanation for the increased risk taking in bank in 1980s. Some of

without the consideration for relying on the ex post mechanism like renegotiating with the salary

(Suprajitno 2017).

Remunerations may be also linked to the various types of the dividend payout ratios or

the options for the share bonus schemes. It is seen to be more likely that a bonus plan will be

able to reward the managers only there is an expected level of the profit of the frim for a certain

period. Only then there will be a considerable amount of increase in the revenue of the company

and the mangers will be able to increase their bonus thereby increasing the profitability of the

firm (Office of Financial Management 2016).

Answer to Question 4

In general, there has been several types of the lending problems which are associated to

lending in a situation of economic downturn. In this context the presence of the various types of

the manager agency problems and managerial risk aversion problems will be able to avert

significant degree of risk which are seen to be associated to the different aspect of the

consideration of the data which are seen to be associated to the managerial risk aversion and

agency problems. The empirical model of bank tends to focus on the disciplinary role of

franchise value and ownership structure, thereby posing risk to the banks. In several cases the

risk is depicted to be lower at banks with no insider holdings. This has been able to significantly

suggest the various types of the considerations which are associated to the problems which

affects the banks in major way (Kanapathippillai, Johl and Wines 2016).

There are several previous literatures which has been able to state on the agency

problems which provides the explanation for the increased risk taking in bank in 1980s. Some of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY

the various measures which the banks might take to mitigate the agency risks are seen to be

based on the thoroughly checking the new records of the credit records of the customers. The

credit should be provided in accordance with building a customer relationship. This needs to be

based on preparing a master sales agreement with the customers rather than relying on the

purchase orders for setting out the credit terms. The next important step needs to be taken with

the establishment of the credit limits. This needs to be set in terms of the providing a

comprehensive information about the financial history of the company. The bank needs to make

sure that the sales agreement is clear in terms of the present situation of the market

considerations. The sales agreement needs to be included with the well worded comprehensive

terms of the credit which will be able to considerably reduce the risk for the disputes and

improve the scope of chance for getting paid in full and on time. It needs to be further

considered that there needs to be adequate opportunity created with the use of the credit or

political risk. There should be various types of the consideration which will be able to take into

account the full site of the risk which is seen to be based on using factoring method. This method

will allow sell the receivables in a situation of economic crisis. The receivable to a factoring

company needs to be based on cash value less discount. The next process needs to be developed

with standard process for the handling of the overdue accounts. Some of the other measures to

safeguard the credit risk needs to be taken with the various types of the internal and the external

consultation from the higher management before the granting the credit to the borrowers during a

situation of financial crisis (Management 2014).

the various measures which the banks might take to mitigate the agency risks are seen to be

based on the thoroughly checking the new records of the credit records of the customers. The

credit should be provided in accordance with building a customer relationship. This needs to be

based on preparing a master sales agreement with the customers rather than relying on the

purchase orders for setting out the credit terms. The next important step needs to be taken with

the establishment of the credit limits. This needs to be set in terms of the providing a

comprehensive information about the financial history of the company. The bank needs to make

sure that the sales agreement is clear in terms of the present situation of the market

considerations. The sales agreement needs to be included with the well worded comprehensive

terms of the credit which will be able to considerably reduce the risk for the disputes and

improve the scope of chance for getting paid in full and on time. It needs to be further

considered that there needs to be adequate opportunity created with the use of the credit or

political risk. There should be various types of the consideration which will be able to take into

account the full site of the risk which is seen to be based on using factoring method. This method

will allow sell the receivables in a situation of economic crisis. The receivable to a factoring

company needs to be based on cash value less discount. The next process needs to be developed

with standard process for the handling of the overdue accounts. Some of the other measures to

safeguard the credit risk needs to be taken with the various types of the internal and the external

consultation from the higher management before the granting the credit to the borrowers during a

situation of financial crisis (Management 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY

References

Ferlay, J., Soerjomataram, I., Dikshit, R., Eser, S., Mathers, C., Rebelo, M., Parkin, D. M.,

Forman, D. and Bray, F. (2015) ‘Cancer incidence and mortality worldwide: Sources, methods

and major patterns in GLOBOCAN 2012’, International Journal of Cancer, 136(5), pp. E359–

E386. doi: 10.1002/ijc.29210.

Financial Times (2015) Definition of corporate governance, applied-corporategovernance.com.

Available at: http://lexicon.ft.com/Term?term=corporate-governance.

Health Care Financial Management Association (2004) Financing the future report 4: How are

hospitals financing the future? The future of capital access, Financing the Future.

Inclusion, F. (2014) ‘Financial Inclusion’, GE-INTERNATIONAL JOURNAL OF

MANAGEMENT RESEARCH.

Islamic Financial Services Board (2015) Islamic Financial Services Industry Stability Report

2015, Annual Report. doi: 10.1017/CBO9781107415324.004.

Kanapathippillai, S., Johl, S. K. and Wines, G. (2016) ‘Remuneration committee effectiveness

and narrative remuneration disclosure’, Pacific Basin Finance Journal, 40, pp. 384–402. doi:

10.1016/j.pacfin.2016.02.006.

Management, H. C. F. (2014) ‘The ICD-10 Delay: What’s Next for Your Strategy’, Healthcare

Financial Management, 68(6), pp. 59–66.

OECD (2015) ‘Definitions, Sources and Methods Remuneration of specialists’, in OECD Health

Statistics 2015. Available at:

References

Ferlay, J., Soerjomataram, I., Dikshit, R., Eser, S., Mathers, C., Rebelo, M., Parkin, D. M.,

Forman, D. and Bray, F. (2015) ‘Cancer incidence and mortality worldwide: Sources, methods

and major patterns in GLOBOCAN 2012’, International Journal of Cancer, 136(5), pp. E359–

E386. doi: 10.1002/ijc.29210.

Financial Times (2015) Definition of corporate governance, applied-corporategovernance.com.

Available at: http://lexicon.ft.com/Term?term=corporate-governance.

Health Care Financial Management Association (2004) Financing the future report 4: How are

hospitals financing the future? The future of capital access, Financing the Future.

Inclusion, F. (2014) ‘Financial Inclusion’, GE-INTERNATIONAL JOURNAL OF

MANAGEMENT RESEARCH.

Islamic Financial Services Board (2015) Islamic Financial Services Industry Stability Report

2015, Annual Report. doi: 10.1017/CBO9781107415324.004.

Kanapathippillai, S., Johl, S. K. and Wines, G. (2016) ‘Remuneration committee effectiveness

and narrative remuneration disclosure’, Pacific Basin Finance Journal, 40, pp. 384–402. doi:

10.1016/j.pacfin.2016.02.006.

Management, H. C. F. (2014) ‘The ICD-10 Delay: What’s Next for Your Strategy’, Healthcare

Financial Management, 68(6), pp. 59–66.

OECD (2015) ‘Definitions, Sources and Methods Remuneration of specialists’, in OECD Health

Statistics 2015. Available at:

11ACCOUNTING THEORY

http://www.health.gov.au/internet/main/publishing.nsf/Content/Annual-Medicare-statistics.

%5Cnhttp://www.aihw.gov.au/workforce/medical/.

Office of Financial Management (2016) Population Density and Land Area Criteria Used for

Rural Area Assistance and Other Programs, State of Washington. Available at:

http://www.ofm.wa.gov/pop/popden/rural.asp.

Risk, F. (2014) ‘Financial Statements & Analysis of Shareholdings’, Journal of knowledge

Management, Economics and Information Technology, IV(5), pp. 1–12.

Sanjana, N. E., Shalem, O. and Zhang, F. (2014) ‘Improved vectors and genome-wide libraries

for CRISPR screening’, Nature Methods, pp. 783–784. doi: 10.1038/nmeth.3047.

Schaeck, K. and Cihák, M. (2014) ‘Competition, Efficiency, and Stability in Banking’,

Financial Management, 43(1), pp. 215–241. doi: 10.1111/fima.12010.

Siteresources.worldbank.org. (2018). [online] Available at:

http://siteresources.worldbank.org/INTINVTCLI/Resources/AgencyTheoryandExecutiveCompe

nsation.pdf [Accessed 2 Jun. 2018].

Suprajitno, S. (2017) ‘Nursing Remuneration Index’, Jurnal Ners, 8(2), pp. 357–374. doi:

10.20473/JN.V8I2.3857.

Tabcorp.com.au. (2018). [online] Available at:

https://www.tabcorp.com.au/TabCorp/media/TabCorp/Media%20Releases/Tabcorp-AR-

2017_Draft-38.pdf [Accessed 8 May 2018].

http://www.health.gov.au/internet/main/publishing.nsf/Content/Annual-Medicare-statistics.

%5Cnhttp://www.aihw.gov.au/workforce/medical/.

Office of Financial Management (2016) Population Density and Land Area Criteria Used for

Rural Area Assistance and Other Programs, State of Washington. Available at:

http://www.ofm.wa.gov/pop/popden/rural.asp.

Risk, F. (2014) ‘Financial Statements & Analysis of Shareholdings’, Journal of knowledge

Management, Economics and Information Technology, IV(5), pp. 1–12.

Sanjana, N. E., Shalem, O. and Zhang, F. (2014) ‘Improved vectors and genome-wide libraries

for CRISPR screening’, Nature Methods, pp. 783–784. doi: 10.1038/nmeth.3047.

Schaeck, K. and Cihák, M. (2014) ‘Competition, Efficiency, and Stability in Banking’,

Financial Management, 43(1), pp. 215–241. doi: 10.1111/fima.12010.

Siteresources.worldbank.org. (2018). [online] Available at:

http://siteresources.worldbank.org/INTINVTCLI/Resources/AgencyTheoryandExecutiveCompe

nsation.pdf [Accessed 2 Jun. 2018].

Suprajitno, S. (2017) ‘Nursing Remuneration Index’, Jurnal Ners, 8(2), pp. 357–374. doi:

10.20473/JN.V8I2.3857.

Tabcorp.com.au. (2018). [online] Available at:

https://www.tabcorp.com.au/TabCorp/media/TabCorp/Media%20Releases/Tabcorp-AR-

2017_Draft-38.pdf [Accessed 8 May 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.