ACC341 Assignment 2: Analysis of Accounting Ethics and Regulations

VerifiedAdded on 2023/01/04

|11

|2890

|50

Report

AI Summary

This report analyzes an accounting issue related to financial planning conflicts, as reported in an Australian Broadcasting Corporation news article. The report examines the conflict between accountant financial planners and the Accounting Professional and Ethical Standards Board (APESB) regarding conflicted payments. The report links the issue to the ACC341 topic of Professionalism and Ethics in Accounting, and applies both public interest theory and self-interest theory to explain the different positions of the APESB and the lobby groups. The report then examines an exposure draft by the International Accounting Standards Board (IASB) regarding the amendment of IAS 16, analyzing the views of various groups through their comment letters. The behavior of the IASB is analyzed using public interest theory. The report further applies the theories of public interest, private interest, and capture to analyze the comment letters. The report concludes by evaluating the underlying assumptions of the applied theories and perspectives of regulation. The assignment demonstrates the ability to critically analyze accounting issues and apply relevant theories and regulations.

Accounting Theory 1

Accounting Theory

Name

Institution

Accounting Theory

Name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory 2

Question one: Analysis of the chosen news article

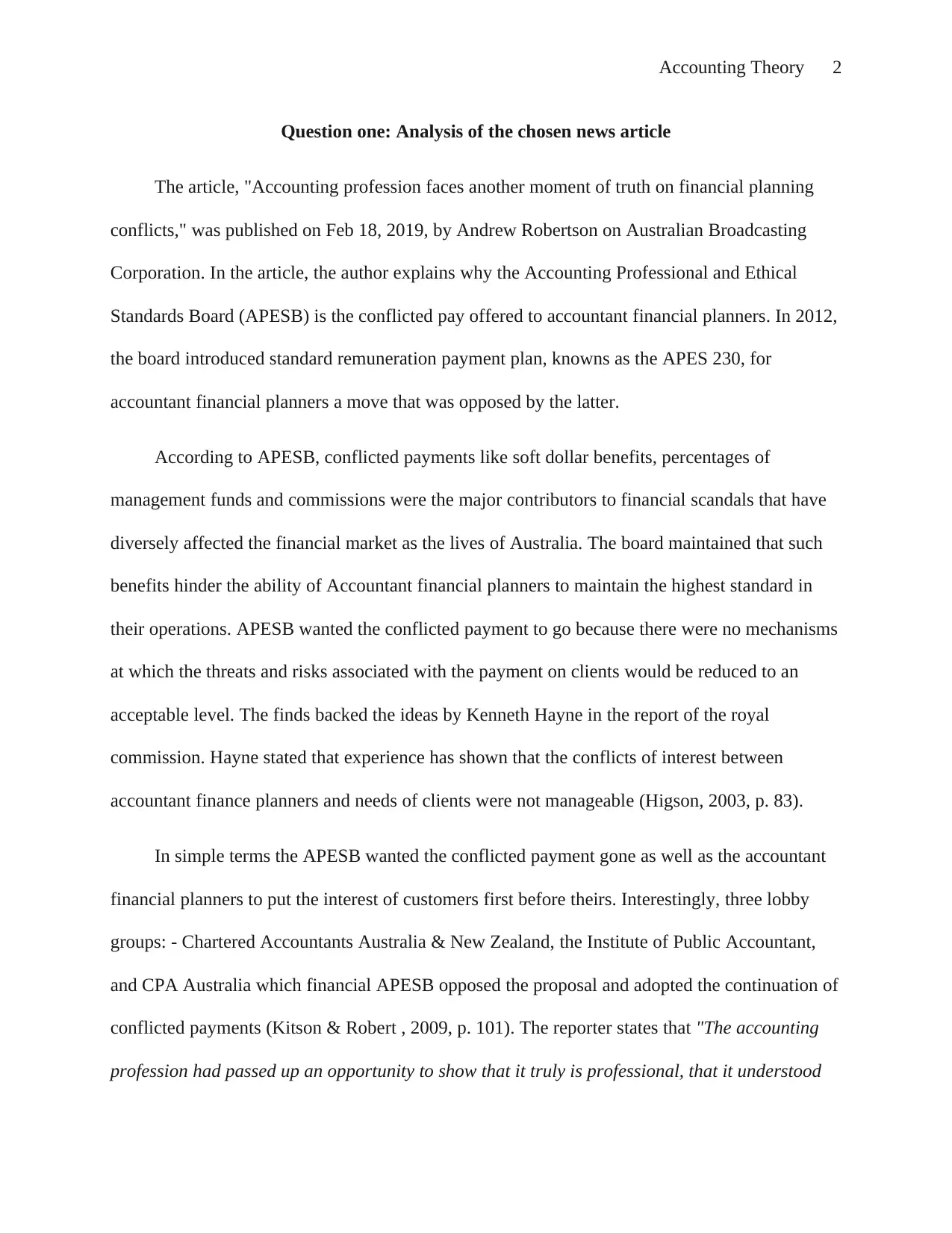

The article, "Accounting profession faces another moment of truth on financial planning

conflicts," was published on Feb 18, 2019, by Andrew Robertson on Australian Broadcasting

Corporation. In the article, the author explains why the Accounting Professional and Ethical

Standards Board (APESB) is the conflicted pay offered to accountant financial planners. In 2012,

the board introduced standard remuneration payment plan, knowns as the APES 230, for

accountant financial planners a move that was opposed by the latter.

According to APESB, conflicted payments like soft dollar benefits, percentages of

management funds and commissions were the major contributors to financial scandals that have

diversely affected the financial market as the lives of Australia. The board maintained that such

benefits hinder the ability of Accountant financial planners to maintain the highest standard in

their operations. APESB wanted the conflicted payment to go because there were no mechanisms

at which the threats and risks associated with the payment on clients would be reduced to an

acceptable level. The finds backed the ideas by Kenneth Hayne in the report of the royal

commission. Hayne stated that experience has shown that the conflicts of interest between

accountant finance planners and needs of clients were not manageable (Higson, 2003, p. 83).

In simple terms the APESB wanted the conflicted payment gone as well as the accountant

financial planners to put the interest of customers first before theirs. Interestingly, three lobby

groups: - Chartered Accountants Australia & New Zealand, the Institute of Public Accountant,

and CPA Australia which financial APESB opposed the proposal and adopted the continuation of

conflicted payments (Kitson & Robert , 2009, p. 101). The reporter states that "The accounting

profession had passed up an opportunity to show that it truly is professional, that it understood

Question one: Analysis of the chosen news article

The article, "Accounting profession faces another moment of truth on financial planning

conflicts," was published on Feb 18, 2019, by Andrew Robertson on Australian Broadcasting

Corporation. In the article, the author explains why the Accounting Professional and Ethical

Standards Board (APESB) is the conflicted pay offered to accountant financial planners. In 2012,

the board introduced standard remuneration payment plan, knowns as the APES 230, for

accountant financial planners a move that was opposed by the latter.

According to APESB, conflicted payments like soft dollar benefits, percentages of

management funds and commissions were the major contributors to financial scandals that have

diversely affected the financial market as the lives of Australia. The board maintained that such

benefits hinder the ability of Accountant financial planners to maintain the highest standard in

their operations. APESB wanted the conflicted payment to go because there were no mechanisms

at which the threats and risks associated with the payment on clients would be reduced to an

acceptable level. The finds backed the ideas by Kenneth Hayne in the report of the royal

commission. Hayne stated that experience has shown that the conflicts of interest between

accountant finance planners and needs of clients were not manageable (Higson, 2003, p. 83).

In simple terms the APESB wanted the conflicted payment gone as well as the accountant

financial planners to put the interest of customers first before theirs. Interestingly, three lobby

groups: - Chartered Accountants Australia & New Zealand, the Institute of Public Accountant,

and CPA Australia which financial APESB opposed the proposal and adopted the continuation of

conflicted payments (Kitson & Robert , 2009, p. 101). The reporter states that "The accounting

profession had passed up an opportunity to show that it truly is professional, that it understood

Accounting Theory 3

its fiduciary duty, that accountant financial planners really could be trusted to act in their

customers' best interest (Robertson, 2019)." In the future, it will be hard for account finance

planners to convince customers that they are acting to the best of their interests. Moreover, the

client cannot trust that accountant financial planners base their service of high standard and

professionalism. The lobby groups were supposed to put the interest of clients first by adopting

APESB's proposal but chose to reject it (Deegan, 2013, p. 35).

Link the major issues and ACC341 topics and theories:

a) The issue and ACC341 topics

The issue covered in the article relates to the ACC341 topic of Professionalism and ethics

in accounting that was covered in the second week. The topic outlines the need for accounting

professionals to observe ethical codes when executing their mandate. Abiding by ethical codes

and professionalism help accountants to demonstrate fairness and honesty, maintain trust and

promote their profession. New professionals are required to undertake ethics and professionalism

training that will help them to protect the profession’s reputation. Professional behaviour is a

fundamental principle of accounting ethics (Jones & Riah-Belkaoui, 2010, p. 97). Accountants

its fiduciary duty, that accountant financial planners really could be trusted to act in their

customers' best interest (Robertson, 2019)." In the future, it will be hard for account finance

planners to convince customers that they are acting to the best of their interests. Moreover, the

client cannot trust that accountant financial planners base their service of high standard and

professionalism. The lobby groups were supposed to put the interest of clients first by adopting

APESB's proposal but chose to reject it (Deegan, 2013, p. 35).

Link the major issues and ACC341 topics and theories:

a) The issue and ACC341 topics

The issue covered in the article relates to the ACC341 topic of Professionalism and ethics

in accounting that was covered in the second week. The topic outlines the need for accounting

professionals to observe ethical codes when executing their mandate. Abiding by ethical codes

and professionalism help accountants to demonstrate fairness and honesty, maintain trust and

promote their profession. New professionals are required to undertake ethics and professionalism

training that will help them to protect the profession’s reputation. Professional behaviour is a

fundamental principle of accounting ethics (Jones & Riah-Belkaoui, 2010, p. 97). Accountants

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory 4

are required to adhere to the laws within a given jurisdiction. Professional behaviour prohibits the

accountant was engaging in actions that would negatively affect the profession’s reputation as

well as go against the expectation of business partners, the community and other stakeholders.

The link between the topic and the article arises from the impact of conflicted payments on the

Professionalism and reputation of accountant financial planners. APESB holds that continued

application of conflicted payments jeopardizes the expected high standard and professionalism

operations from accountant financial planners (Barth & Landsman, 2010).

b) Accounting theories explaining the issue

There two theories that can be used to describe the issue discussed in the article. The two

most appropriate theories that can be used to demonstrate the situation are the public interest

theory and the self-interest theory. Public interest theory is used to analyze the views of the

APESB on conflicted payments. On the other hand, the self-interest theory is used to demonstrate

the position of the accountant financial planners on conflicted payments.

i) Public interest theory

Public interest theory assumes that the market is inefficient and imperfect. The market

should be regulated to make it economically perfect and efficient. Generally, public interest

theory introduces regulations that benefit the rights of the public at large or protect the public

from exploitation. The theory supports the creation of a legislative instrument to overcome

imperfect competition, undesired market results, and unbalanced market operation. In the case of

conflicted payments, APESB was formed to develop a solution to the risks associated with the

payment system (Wolk, 2009, p. 72). The board holds that the payments system does not serve

the interest of the public. For example, conflicted payments have been associated with the global

are required to adhere to the laws within a given jurisdiction. Professional behaviour prohibits the

accountant was engaging in actions that would negatively affect the profession’s reputation as

well as go against the expectation of business partners, the community and other stakeholders.

The link between the topic and the article arises from the impact of conflicted payments on the

Professionalism and reputation of accountant financial planners. APESB holds that continued

application of conflicted payments jeopardizes the expected high standard and professionalism

operations from accountant financial planners (Barth & Landsman, 2010).

b) Accounting theories explaining the issue

There two theories that can be used to describe the issue discussed in the article. The two

most appropriate theories that can be used to demonstrate the situation are the public interest

theory and the self-interest theory. Public interest theory is used to analyze the views of the

APESB on conflicted payments. On the other hand, the self-interest theory is used to demonstrate

the position of the accountant financial planners on conflicted payments.

i) Public interest theory

Public interest theory assumes that the market is inefficient and imperfect. The market

should be regulated to make it economically perfect and efficient. Generally, public interest

theory introduces regulations that benefit the rights of the public at large or protect the public

from exploitation. The theory supports the creation of a legislative instrument to overcome

imperfect competition, undesired market results, and unbalanced market operation. In the case of

conflicted payments, APESB was formed to develop a solution to the risks associated with the

payment system (Wolk, 2009, p. 72). The board holds that the payments system does not serve

the interest of the public. For example, conflicted payments have been associated with the global

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory 5

financial crisis which has had a severe impact on the Australians. Therefore, the board came up

with the APES 230 regulation which sought to do away with the conflicted payments for

accountant financial planners. The regulation introduced a performance-based payment system

which would address the needs of all stakeholders. APESB wanted to restore high standards and

professional ethics in the performance in the accounting profession (Mathews & Perera, 1996, p.

104).

ii) Self-interest theory

Self-interest theory states that human beings are selfish. The selfish nature of human beings

forces human beings to go against established moral behaviours. The theory states that humans

put their self-interest first before public interest when it is material involved. The accountant

financial planners opposed the move to abolish conflicted payments because it limits their ability

to make extra money. Although Kenneth Hayne found out that the amounts contributed to the

failure of moral values and professional behaviours, the accounting lobby groups opposed the

move to safeguard earnings for accountants. In this case, the lobby groups chose to protect the

rights of the accountant over those of the clients as required by professional ethics (Wolk, Dodd ,

& Rozycki, 2017, p. 81).

In conclusion, accountants have been accused of using favourable accounting regulation to

create financial statements that serve their interest. In additional, accountants apply accounting

regulations to increase their earnings, especially under a performance-based payment system. In

the article, accountant financial planners use conflicted payments to increase their profits at the

expense of their clients and other stakeholders. This is an accounting issue which would lead to a

financial crisis if not addressed adequately.

financial crisis which has had a severe impact on the Australians. Therefore, the board came up

with the APES 230 regulation which sought to do away with the conflicted payments for

accountant financial planners. The regulation introduced a performance-based payment system

which would address the needs of all stakeholders. APESB wanted to restore high standards and

professional ethics in the performance in the accounting profession (Mathews & Perera, 1996, p.

104).

ii) Self-interest theory

Self-interest theory states that human beings are selfish. The selfish nature of human beings

forces human beings to go against established moral behaviours. The theory states that humans

put their self-interest first before public interest when it is material involved. The accountant

financial planners opposed the move to abolish conflicted payments because it limits their ability

to make extra money. Although Kenneth Hayne found out that the amounts contributed to the

failure of moral values and professional behaviours, the accounting lobby groups opposed the

move to safeguard earnings for accountants. In this case, the lobby groups chose to protect the

rights of the accountant over those of the clients as required by professional ethics (Wolk, Dodd ,

& Rozycki, 2017, p. 81).

In conclusion, accountants have been accused of using favourable accounting regulation to

create financial statements that serve their interest. In additional, accountants apply accounting

regulations to increase their earnings, especially under a performance-based payment system. In

the article, accountant financial planners use conflicted payments to increase their profits at the

expense of their clients and other stakeholders. This is an accounting issue which would lead to a

financial crisis if not addressed adequately.

Accounting Theory 6

Question Two: Exposure draft and public comments

a. The major issues covered in the exposure draft

The International Accounting Standards Board (IASB) public a draft proposal which sought

to amend the application of IAS 16. The proposed amendments were meant to redefine the

recognition of proceeds realized from Property, Plant, and Equipment (PPE) before their intended

use. The proposal proposed the recognition of sales and costs associated with PPEs in the profit

and Loss statement instead of deducting the sales from the cost of the associated PPE

(International Accounting Standards Board, 2019).

IASB believes in the due process; hence the proposed amendment was published to collect

public comments. All the comments were posted in IASB after seeking the consent of the

respondents. Approximately 50 comment letters were collected and published on the website.

b. Views of various groups on the proposed amendment

This section discusses four comment letters that were collected from accounting bodies,

corporate bodies, and companies who seek to express their views on the proposed amendment.

Confederation of Swedish Enterprise

The Confederation of Swedish Enterprise submitted their comment to IASB on Sep 20,

2017. The Enterprise welcomed both the proposed changes to IAS 16 and the reasons listed by

the IASB to support the exposure draft.

Japan Foreign Trade Council (JFTC)

Members of the JFTC comes from the Japanese trading companies and companies.

Therefore, the core mandate on the council is to respond to the proposed changes in the

Question Two: Exposure draft and public comments

a. The major issues covered in the exposure draft

The International Accounting Standards Board (IASB) public a draft proposal which sought

to amend the application of IAS 16. The proposed amendments were meant to redefine the

recognition of proceeds realized from Property, Plant, and Equipment (PPE) before their intended

use. The proposal proposed the recognition of sales and costs associated with PPEs in the profit

and Loss statement instead of deducting the sales from the cost of the associated PPE

(International Accounting Standards Board, 2019).

IASB believes in the due process; hence the proposed amendment was published to collect

public comments. All the comments were posted in IASB after seeking the consent of the

respondents. Approximately 50 comment letters were collected and published on the website.

b. Views of various groups on the proposed amendment

This section discusses four comment letters that were collected from accounting bodies,

corporate bodies, and companies who seek to express their views on the proposed amendment.

Confederation of Swedish Enterprise

The Confederation of Swedish Enterprise submitted their comment to IASB on Sep 20,

2017. The Enterprise welcomed both the proposed changes to IAS 16 and the reasons listed by

the IASB to support the exposure draft.

Japan Foreign Trade Council (JFTC)

Members of the JFTC comes from the Japanese trading companies and companies.

Therefore, the core mandate on the council is to respond to the proposed changes in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory 7

accounting standard both locally and internationally on behalf of its members. The council stated

that IASB should consider the impact of the proposed amendment on operational management

and business performance. The council raised several concerns in reference on whether or not it

supported the proposal. First, the adoption of the project would rise company profit during the

testing period because deprecation is excluded from the cost. The profit would be lowered during

ordinary activity period when depreciation is included in the price. Therefore, income and profit

realized during the testing period would not present the real performance of a business

(Hendersen, Pierson, & Herbohn, 2014, p. 128). Second, the cost is likely to exceed revenue

when selling prices are reduced during the testing period. The difference should be included in

the cost of acquiring the asset to ensure normal operations. Generally, the council maintained that

the impact of the proposed amendment would differ based on the product, testing period,

business and industry. Therefore, IASB should conduct more research on the effects of the

proposed change on the performance and operations of companies (Godfrey, Hodgson, Tarca,

Hamiliton, & Holmes, 2010, p. 34).

GAAP Advisors

GAAP Advisors chose to disagree with the exposure draft based on some reasons. First,

proposed focussed on a narrow focus of addressing sales proceeding during the testing period and

lacked the backing of a conceptual basis. Second, the proposal was not consistent with other

IFRS principles. Third, it is an irony of how an entity can use an item of PPE to generate revenue

yet such a thing has not been put into use. Lastly, the proposed amendment create would create

inconsistencies with the IAS standards and the IFRS framework.

Ernst & Young (EY)

accounting standard both locally and internationally on behalf of its members. The council stated

that IASB should consider the impact of the proposed amendment on operational management

and business performance. The council raised several concerns in reference on whether or not it

supported the proposal. First, the adoption of the project would rise company profit during the

testing period because deprecation is excluded from the cost. The profit would be lowered during

ordinary activity period when depreciation is included in the price. Therefore, income and profit

realized during the testing period would not present the real performance of a business

(Hendersen, Pierson, & Herbohn, 2014, p. 128). Second, the cost is likely to exceed revenue

when selling prices are reduced during the testing period. The difference should be included in

the cost of acquiring the asset to ensure normal operations. Generally, the council maintained that

the impact of the proposed amendment would differ based on the product, testing period,

business and industry. Therefore, IASB should conduct more research on the effects of the

proposed change on the performance and operations of companies (Godfrey, Hodgson, Tarca,

Hamiliton, & Holmes, 2010, p. 34).

GAAP Advisors

GAAP Advisors chose to disagree with the exposure draft based on some reasons. First,

proposed focussed on a narrow focus of addressing sales proceeding during the testing period and

lacked the backing of a conceptual basis. Second, the proposal was not consistent with other

IFRS principles. Third, it is an irony of how an entity can use an item of PPE to generate revenue

yet such a thing has not been put into use. Lastly, the proposed amendment create would create

inconsistencies with the IAS standards and the IFRS framework.

Ernst & Young (EY)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory 8

Ernst & Young disagreed with the proposed change. The company held that the proposal

failed to address the arising issues such as determination of when an item of PPE is ready for the

intended use and the difficulty in allocating costs of such assets.

Generally, the proposal was fully supported by the Confederation of Swedish Enterprise. The

other three respondents raised several issues that required to be addressed adequately.

c. The behaviour of IASB using public interest theory

Public interest theory assumes that there are imperfection and inefficiencies in the market

which can only be rectified by regulating the operations in the market. The theory states that

regulators have to control the market for the best interest of the public by protecting them from

exploitation. IASB stated that users rely on the financial statement to make decisions. The

proposal would lead to objectivity in treating the revenue collected from PPE assets during the

testing period. The proposal was meant to safeguard the public interest (Baker, 2005, p. 690).

d. Analyzing the comment letters using the theories of public interest, private interest, and

capture

As mentioned earlier, public interest theory states that regulations should be formed to

safeguard the rights and interests of the public at large. Likewise, Private interest theory human

beings are selfish and would take actions that promote their interest. Therefore, the different

groups would support the proposal if it would serve their interest. Lastly, capture theory tastes

that regulation agencies comprise of members who are the past or future employees of a given

industry. Therefore, regulators act in the interest of the sector instead of safeguarding the interest

of the public (Baker, 2005, p. 695).

Ernst & Young disagreed with the proposed change. The company held that the proposal

failed to address the arising issues such as determination of when an item of PPE is ready for the

intended use and the difficulty in allocating costs of such assets.

Generally, the proposal was fully supported by the Confederation of Swedish Enterprise. The

other three respondents raised several issues that required to be addressed adequately.

c. The behaviour of IASB using public interest theory

Public interest theory assumes that there are imperfection and inefficiencies in the market

which can only be rectified by regulating the operations in the market. The theory states that

regulators have to control the market for the best interest of the public by protecting them from

exploitation. IASB stated that users rely on the financial statement to make decisions. The

proposal would lead to objectivity in treating the revenue collected from PPE assets during the

testing period. The proposal was meant to safeguard the public interest (Baker, 2005, p. 690).

d. Analyzing the comment letters using the theories of public interest, private interest, and

capture

As mentioned earlier, public interest theory states that regulations should be formed to

safeguard the rights and interests of the public at large. Likewise, Private interest theory human

beings are selfish and would take actions that promote their interest. Therefore, the different

groups would support the proposal if it would serve their interest. Lastly, capture theory tastes

that regulation agencies comprise of members who are the past or future employees of a given

industry. Therefore, regulators act in the interest of the sector instead of safeguarding the interest

of the public (Baker, 2005, p. 695).

Accounting Theory 9

Private interest theory can best explain the comments made by different entities on the

proposed amendment. Each group had its position on the treatment of sales proceeding realized

PPEs before their intended use. Each group when through the proposal to find out whether or not

it serves their interests. The decision to agree or disagree with the project was based on how best

it would serve the interest of the respondents who aired their views (Baldwin, Cave, & Lodge,

2012, p. 68).

e. Evaluating the underlying assumptions of the applied theories and perspectives of

regulation.

In conclusion, IASB had the best interest of the users of the financial statement when the

proposal was made. The project was intended to bring a uniform treatment of the revenue in

question to allow comparability of performance between different entities as well as reliability of

the same statements. On the other hand, each lobby group can only support the proposal if they

intend to promote their interests. Remember that human beings are selfish. Although each

respondent has cited the objectivity principle of financial reporting as the reason for accepting or

rejecting the proposal, it is evident that they are looking for an accounting policy that aligns with

their goals and objectives (Fryer, 2014, p. 51). The IASB comprises of past and future accounting

profession which can be captured by the influence of business entities to favour the interest of the

industry. The proposal might be adopted if the IASB still plan to safeguard the public interest

after reading the comments. Likewise, the project might be rejected if the interest of the industry

outweighs the public interest (Gaffikin, 2008, p. 80).

Private interest theory can best explain the comments made by different entities on the

proposed amendment. Each group had its position on the treatment of sales proceeding realized

PPEs before their intended use. Each group when through the proposal to find out whether or not

it serves their interests. The decision to agree or disagree with the project was based on how best

it would serve the interest of the respondents who aired their views (Baldwin, Cave, & Lodge,

2012, p. 68).

e. Evaluating the underlying assumptions of the applied theories and perspectives of

regulation.

In conclusion, IASB had the best interest of the users of the financial statement when the

proposal was made. The project was intended to bring a uniform treatment of the revenue in

question to allow comparability of performance between different entities as well as reliability of

the same statements. On the other hand, each lobby group can only support the proposal if they

intend to promote their interests. Remember that human beings are selfish. Although each

respondent has cited the objectivity principle of financial reporting as the reason for accepting or

rejecting the proposal, it is evident that they are looking for an accounting policy that aligns with

their goals and objectives (Fryer, 2014, p. 51). The IASB comprises of past and future accounting

profession which can be captured by the influence of business entities to favour the interest of the

industry. The proposal might be adopted if the IASB still plan to safeguard the public interest

after reading the comments. Likewise, the project might be rejected if the interest of the industry

outweighs the public interest (Gaffikin, 2008, p. 80).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounting Theory 10

References

Baker, C. R. (2005). What is the meaning of ‘the public interest’ Examining the ideology of the

American accounting profession. Accounting, Auditing and Accountability Journal, 18,

690-703.

Baldwin, R., Cave, M., & Lodge, M. (2012). Understanding Regulation: Theory, Strategy, and

Practice (illustrated, revised ed.). Nairobi: OUP Oxford.

Barth, M. E., & Landsman, W. R. (2010). How did financial reporting contribute to the financial

crisis? European Accounting Review, 19(3), 399-423.

Deegan, C. (2013). Financial accounting theory (4th Edition ed.). North Ryde, N.S.W: McGraw-

Hill Education.

Fryer, M. (2014). Ethics Theory and Business Practice. London: SAGE Publications.

Gaffikin, M. (2008). Accounting Theory. Frenchs Forest: Pearson Edmundson.

Godfrey, J., Hodgson, A., Tarca, A., Hamiliton, J., & Holmes, S. (2010). Accounting Theory.

Brisbane: John Wiley & Sons.

Hendersen, S., Pierson, G., & Herbohn, K. (2014). Issues in Financial Accounting. Sydney:

Pearson.

Higson, A. (2003). Corporate Financial Reporting: Theory and Practice (1 ed.). New Jersey:

SAGE.

International Accounting Standards Board. (2019, May 9). Exposure Draft and comment letters—

Property, Plant and Equipment—Proceeds before Intended Use (Proposed amendments

to IAS 16) . Retrieved from IFRS: https://www.ifrs.org/projects/work-plan/property-plant-

References

Baker, C. R. (2005). What is the meaning of ‘the public interest’ Examining the ideology of the

American accounting profession. Accounting, Auditing and Accountability Journal, 18,

690-703.

Baldwin, R., Cave, M., & Lodge, M. (2012). Understanding Regulation: Theory, Strategy, and

Practice (illustrated, revised ed.). Nairobi: OUP Oxford.

Barth, M. E., & Landsman, W. R. (2010). How did financial reporting contribute to the financial

crisis? European Accounting Review, 19(3), 399-423.

Deegan, C. (2013). Financial accounting theory (4th Edition ed.). North Ryde, N.S.W: McGraw-

Hill Education.

Fryer, M. (2014). Ethics Theory and Business Practice. London: SAGE Publications.

Gaffikin, M. (2008). Accounting Theory. Frenchs Forest: Pearson Edmundson.

Godfrey, J., Hodgson, A., Tarca, A., Hamiliton, J., & Holmes, S. (2010). Accounting Theory.

Brisbane: John Wiley & Sons.

Hendersen, S., Pierson, G., & Herbohn, K. (2014). Issues in Financial Accounting. Sydney:

Pearson.

Higson, A. (2003). Corporate Financial Reporting: Theory and Practice (1 ed.). New Jersey:

SAGE.

International Accounting Standards Board. (2019, May 9). Exposure Draft and comment letters—

Property, Plant and Equipment—Proceeds before Intended Use (Proposed amendments

to IAS 16) . Retrieved from IFRS: https://www.ifrs.org/projects/work-plan/property-plant-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting Theory 11

and-equipment-proceeds-before-intended-use/comment-letters-projects/ed-property-plant-

and-equipment/#consultation

Jones, S., & Riah-Belkaoui, A. (2010). Accounting Theory. Australia: Nelson.

Kitson, A., & Robert , C. (2009). Ethical Issues in Accounting. London: Palgrave.

Mathews, M. R., & Perera, M. H. (1996). Accounting Theory and Development . Sydney: Nelson.

Robertson, A. (2019, Feb 18). Accounting profession faces another moment of truth on financial

planning conflicts. Retrieved from ABC News: https://www.abc.net.au/news/2019-02-

18/financial-planning-accountants-and-conflicted-remuneration/10820526

Wolk, H. I. (2009). Accounting Theory (1 ed.). London: SAGE Publications Lt.

Wolk, H. I., Dodd , J. L., & Rozycki, J. J. (2017). Accounting Theory: Conceptual Issues in a

Political and Economic Environment (1 ed.). London: SAGE Publications.

and-equipment-proceeds-before-intended-use/comment-letters-projects/ed-property-plant-

and-equipment/#consultation

Jones, S., & Riah-Belkaoui, A. (2010). Accounting Theory. Australia: Nelson.

Kitson, A., & Robert , C. (2009). Ethical Issues in Accounting. London: Palgrave.

Mathews, M. R., & Perera, M. H. (1996). Accounting Theory and Development . Sydney: Nelson.

Robertson, A. (2019, Feb 18). Accounting profession faces another moment of truth on financial

planning conflicts. Retrieved from ABC News: https://www.abc.net.au/news/2019-02-

18/financial-planning-accountants-and-conflicted-remuneration/10820526

Wolk, H. I. (2009). Accounting Theory (1 ed.). London: SAGE Publications Lt.

Wolk, H. I., Dodd , J. L., & Rozycki, J. J. (2017). Accounting Theory: Conceptual Issues in a

Political and Economic Environment (1 ed.). London: SAGE Publications.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.