Accounting Treatment and Journal Entries for Various Financial Events

VerifiedAdded on 2023/06/03

|11

|1825

|116

Homework Assignment

AI Summary

This assignment provides solutions for various accounting scenarios, including changes in accounting estimates, prior period errors, post-reporting date events, and fraudulent activities, with corresponding journal entries and disclosures based on AASB standards. It covers share issuance, forfeiture, and re-issuance, including detailed calculations for amounts refunded to shareholders. Furthermore, it addresses the determination of current and deferred tax liabilities, along with relevant journal entries and depreciation calculations. The assignment also explores the revaluation of assets, including journal entries for depreciation, revaluation gains, and asset sales. Finally, it details the determination and allocation of impairment losses across cash-generating units (CGUs) and provides the necessary journal entries, with references to AASB 136 and other relevant standards. Desklib offers a wide range of similar solved assignments and past papers to support students in their studies.

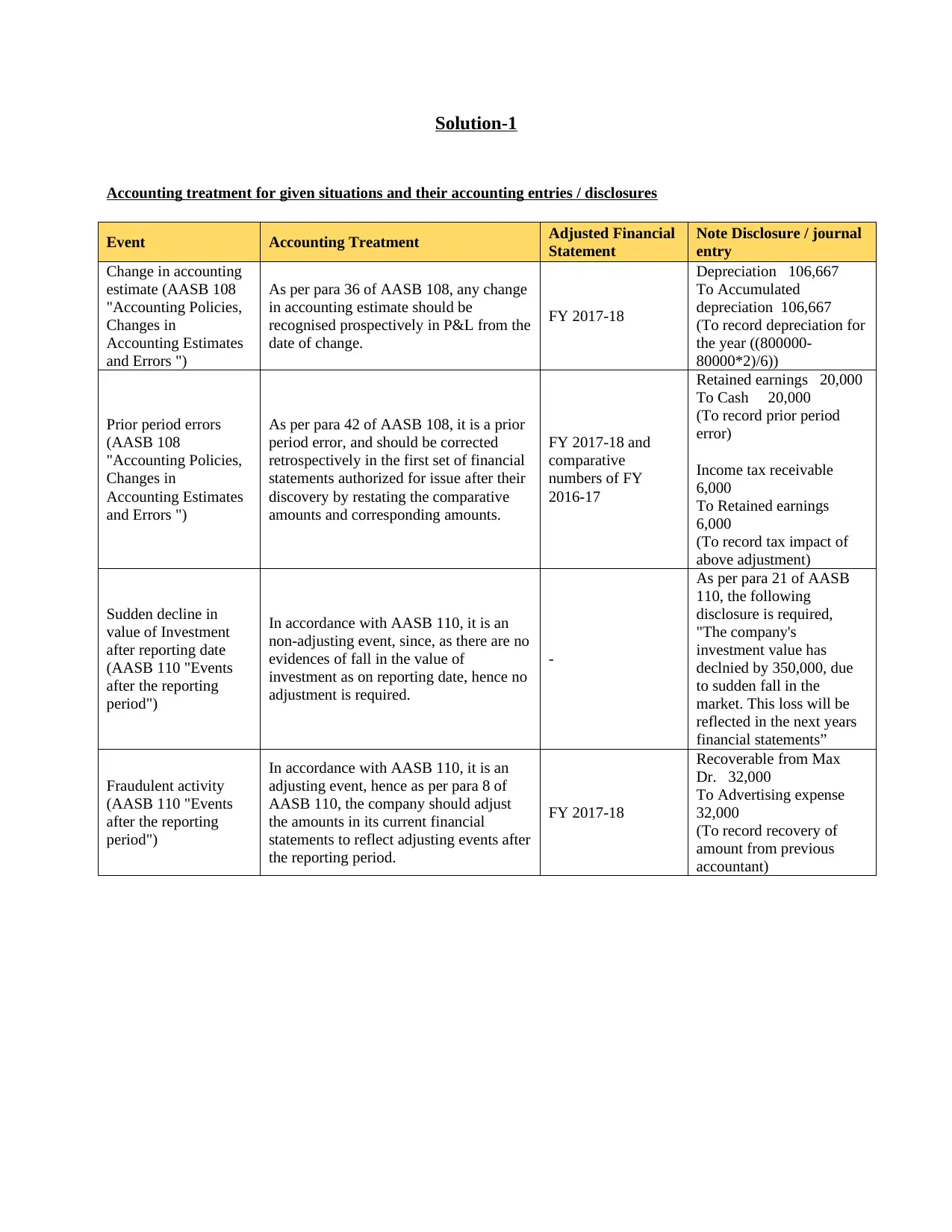

Solution-1

Accounting treatment for given situations and their accounting entries / disclosures

Event Accounting Treatment Adjusted Financial

Statement

Note Disclosure / journal

entry

Change in accounting

estimate (AASB 108

"Accounting Policies,

Changes in

Accounting Estimates

and Errors ")

As per para 36 of AASB 108, any change

in accounting estimate should be

recognised prospectively in P&L from the

date of change.

FY 2017-18

Depreciation 106,667

To Accumulated

depreciation 106,667

(To record depreciation for

the year ((800000-

80000*2)/6))

Prior period errors

(AASB 108

"Accounting Policies,

Changes in

Accounting Estimates

and Errors ")

As per para 42 of AASB 108, it is a prior

period error, and should be corrected

retrospectively in the first set of financial

statements authorized for issue after their

discovery by restating the comparative

amounts and corresponding amounts.

FY 2017-18 and

comparative

numbers of FY

2016-17

Retained earnings 20,000

To Cash 20,000

(To record prior period

error)

Income tax receivable

6,000

To Retained earnings

6,000

(To record tax impact of

above adjustment)

Sudden decline in

value of Investment

after reporting date

(AASB 110 "Events

after the reporting

period")

In accordance with AASB 110, it is an

non-adjusting event, since, as there are no

evidences of fall in the value of

investment as on reporting date, hence no

adjustment is required.

-

As per para 21 of AASB

110, the following

disclosure is required,

"The company's

investment value has

declnied by 350,000, due

to sudden fall in the

market. This loss will be

reflected in the next years

financial statements”

Fraudulent activity

(AASB 110 "Events

after the reporting

period")

In accordance with AASB 110, it is an

adjusting event, hence as per para 8 of

AASB 110, the company should adjust

the amounts in its current financial

statements to reflect adjusting events after

the reporting period.

FY 2017-18

Recoverable from Max

Dr. 32,000

To Advertising expense

32,000

(To record recovery of

amount from previous

accountant)

Accounting treatment for given situations and their accounting entries / disclosures

Event Accounting Treatment Adjusted Financial

Statement

Note Disclosure / journal

entry

Change in accounting

estimate (AASB 108

"Accounting Policies,

Changes in

Accounting Estimates

and Errors ")

As per para 36 of AASB 108, any change

in accounting estimate should be

recognised prospectively in P&L from the

date of change.

FY 2017-18

Depreciation 106,667

To Accumulated

depreciation 106,667

(To record depreciation for

the year ((800000-

80000*2)/6))

Prior period errors

(AASB 108

"Accounting Policies,

Changes in

Accounting Estimates

and Errors ")

As per para 42 of AASB 108, it is a prior

period error, and should be corrected

retrospectively in the first set of financial

statements authorized for issue after their

discovery by restating the comparative

amounts and corresponding amounts.

FY 2017-18 and

comparative

numbers of FY

2016-17

Retained earnings 20,000

To Cash 20,000

(To record prior period

error)

Income tax receivable

6,000

To Retained earnings

6,000

(To record tax impact of

above adjustment)

Sudden decline in

value of Investment

after reporting date

(AASB 110 "Events

after the reporting

period")

In accordance with AASB 110, it is an

non-adjusting event, since, as there are no

evidences of fall in the value of

investment as on reporting date, hence no

adjustment is required.

-

As per para 21 of AASB

110, the following

disclosure is required,

"The company's

investment value has

declnied by 350,000, due

to sudden fall in the

market. This loss will be

reflected in the next years

financial statements”

Fraudulent activity

(AASB 110 "Events

after the reporting

period")

In accordance with AASB 110, it is an

adjusting event, hence as per para 8 of

AASB 110, the company should adjust

the amounts in its current financial

statements to reflect adjusting events after

the reporting period.

FY 2017-18

Recoverable from Max

Dr. 32,000

To Advertising expense

32,000

(To record recovery of

amount from previous

accountant)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

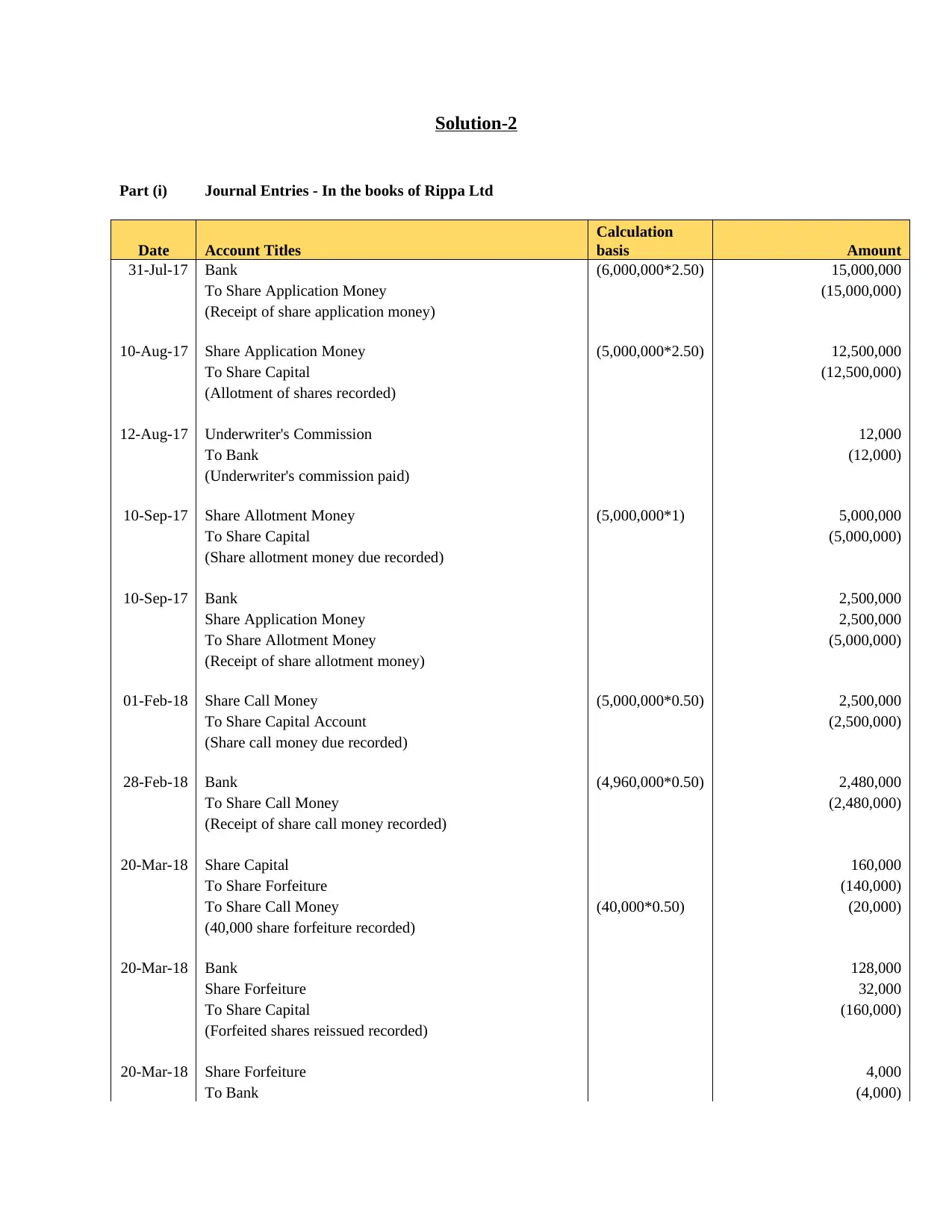

Solution-2

Part (i) Journal Entries - In the books of Rippa Ltd

Date Account Titles

Calculation

basis Amount

31-Jul-17 Bank (6,000,000*2.50) 15,000,000

To Share Application Money (15,000,000)

(Receipt of share application money)

10-Aug-17 Share Application Money (5,000,000*2.50) 12,500,000

To Share Capital (12,500,000)

(Allotment of shares recorded)

12-Aug-17 Underwriter's Commission 12,000

To Bank (12,000)

(Underwriter's commission paid)

10-Sep-17 Share Allotment Money (5,000,000*1) 5,000,000

To Share Capital (5,000,000)

(Share allotment money due recorded)

10-Sep-17 Bank 2,500,000

Share Application Money 2,500,000

To Share Allotment Money (5,000,000)

(Receipt of share allotment money)

01-Feb-18 Share Call Money (5,000,000*0.50) 2,500,000

To Share Capital Account (2,500,000)

(Share call money due recorded)

28-Feb-18 Bank (4,960,000*0.50) 2,480,000

To Share Call Money (2,480,000)

(Receipt of share call money recorded)

20-Mar-18 Share Capital 160,000

To Share Forfeiture (140,000)

To Share Call Money (40,000*0.50) (20,000)

(40,000 share forfeiture recorded)

20-Mar-18 Bank 128,000

Share Forfeiture 32,000

To Share Capital (160,000)

(Forfeited shares reissued recorded)

20-Mar-18 Share Forfeiture 4,000

To Bank (4,000)

Part (i) Journal Entries - In the books of Rippa Ltd

Date Account Titles

Calculation

basis Amount

31-Jul-17 Bank (6,000,000*2.50) 15,000,000

To Share Application Money (15,000,000)

(Receipt of share application money)

10-Aug-17 Share Application Money (5,000,000*2.50) 12,500,000

To Share Capital (12,500,000)

(Allotment of shares recorded)

12-Aug-17 Underwriter's Commission 12,000

To Bank (12,000)

(Underwriter's commission paid)

10-Sep-17 Share Allotment Money (5,000,000*1) 5,000,000

To Share Capital (5,000,000)

(Share allotment money due recorded)

10-Sep-17 Bank 2,500,000

Share Application Money 2,500,000

To Share Allotment Money (5,000,000)

(Receipt of share allotment money)

01-Feb-18 Share Call Money (5,000,000*0.50) 2,500,000

To Share Capital Account (2,500,000)

(Share call money due recorded)

28-Feb-18 Bank (4,960,000*0.50) 2,480,000

To Share Call Money (2,480,000)

(Receipt of share call money recorded)

20-Mar-18 Share Capital 160,000

To Share Forfeiture (140,000)

To Share Call Money (40,000*0.50) (20,000)

(40,000 share forfeiture recorded)

20-Mar-18 Bank 128,000

Share Forfeiture 32,000

To Share Capital (160,000)

(Forfeited shares reissued recorded)

20-Mar-18 Share Forfeiture 4,000

To Bank (4,000)

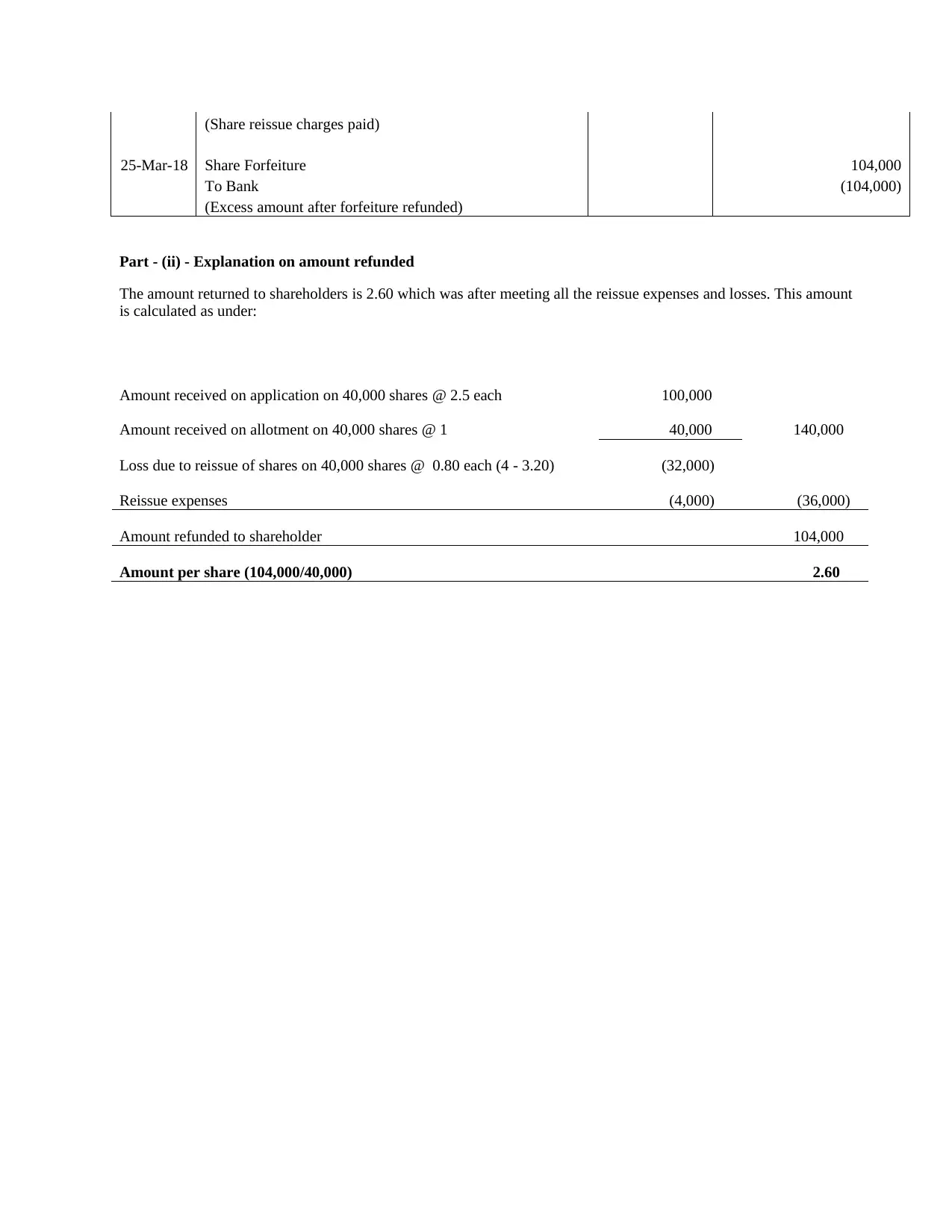

(Share reissue charges paid)

25-Mar-18 Share Forfeiture 104,000

To Bank (104,000)

(Excess amount after forfeiture refunded)

Part - (ii) - Explanation on amount refunded

The amount returned to shareholders is 2.60 which was after meeting all the reissue expenses and losses. This amount

is calculated as under:

Amount received on application on 40,000 shares @ 2.5 each 100,000

Amount received on allotment on 40,000 shares @ 1 40,000 140,000

Loss due to reissue of shares on 40,000 shares @ 0.80 each (4 - 3.20) (32,000)

Reissue expenses (4,000) (36,000)

Amount refunded to shareholder 104,000

Amount per share (104,000/40,000) 2.60

25-Mar-18 Share Forfeiture 104,000

To Bank (104,000)

(Excess amount after forfeiture refunded)

Part - (ii) - Explanation on amount refunded

The amount returned to shareholders is 2.60 which was after meeting all the reissue expenses and losses. This amount

is calculated as under:

Amount received on application on 40,000 shares @ 2.5 each 100,000

Amount received on allotment on 40,000 shares @ 1 40,000 140,000

Loss due to reissue of shares on 40,000 shares @ 0.80 each (4 - 3.20) (32,000)

Reissue expenses (4,000) (36,000)

Amount refunded to shareholder 104,000

Amount per share (104,000/40,000) 2.60

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Solution-3

Part - (i) Determination of balances of current tax liability as at 30 June, 2018

Particulars Amount

Accounting profit before tax 555,800

Less: Expenses allowed / Incomes disallowed

Government grant (50,000)

Depreciation as per tax * (120,000)

Annual leave (4,000)

Insurance expense (25,000)

Warranty expense (2,000)

Doubtful debts written off (2,000)

Add: Expenses disallowed

Depreciation as per accounts 100,000

Annual leave 25,000

Insurance expense 18,000

Warranty expense 18,500

Doubtful debts expense 34,000

Entertainment expense 4,500

Taxable income 552,800

Current tax liability (552,800 * 30%) 165,840

Determination of balances of deferred tax assets / liability as at 30 June, 2018

Particulars As per accounting

books

As per taxation

books

Temporary

Differences

Assets

Accounts receivable 218,000 250,000 32,000

Prepaid insurance 7,000 - (7,000)

Equipment 630,000 600,000 (30,000)

Motor Vehicle 90,000 100,000 10,000

Liabilities

Provision for annual leaves 21,000 - 21,000

Provision for warranty expenses 16,500 - 16,500

Total temporary differences 42,500

Deferred tax asset @ 30% 12,750

Part - (ii) - Journal entries

Account Titles Amount

Part - (i) Determination of balances of current tax liability as at 30 June, 2018

Particulars Amount

Accounting profit before tax 555,800

Less: Expenses allowed / Incomes disallowed

Government grant (50,000)

Depreciation as per tax * (120,000)

Annual leave (4,000)

Insurance expense (25,000)

Warranty expense (2,000)

Doubtful debts written off (2,000)

Add: Expenses disallowed

Depreciation as per accounts 100,000

Annual leave 25,000

Insurance expense 18,000

Warranty expense 18,500

Doubtful debts expense 34,000

Entertainment expense 4,500

Taxable income 552,800

Current tax liability (552,800 * 30%) 165,840

Determination of balances of deferred tax assets / liability as at 30 June, 2018

Particulars As per accounting

books

As per taxation

books

Temporary

Differences

Assets

Accounts receivable 218,000 250,000 32,000

Prepaid insurance 7,000 - (7,000)

Equipment 630,000 600,000 (30,000)

Motor Vehicle 90,000 100,000 10,000

Liabilities

Provision for annual leaves 21,000 - 21,000

Provision for warranty expenses 16,500 - 16,500

Total temporary differences 42,500

Deferred tax asset @ 30% 12,750

Part - (ii) - Journal entries

Account Titles Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

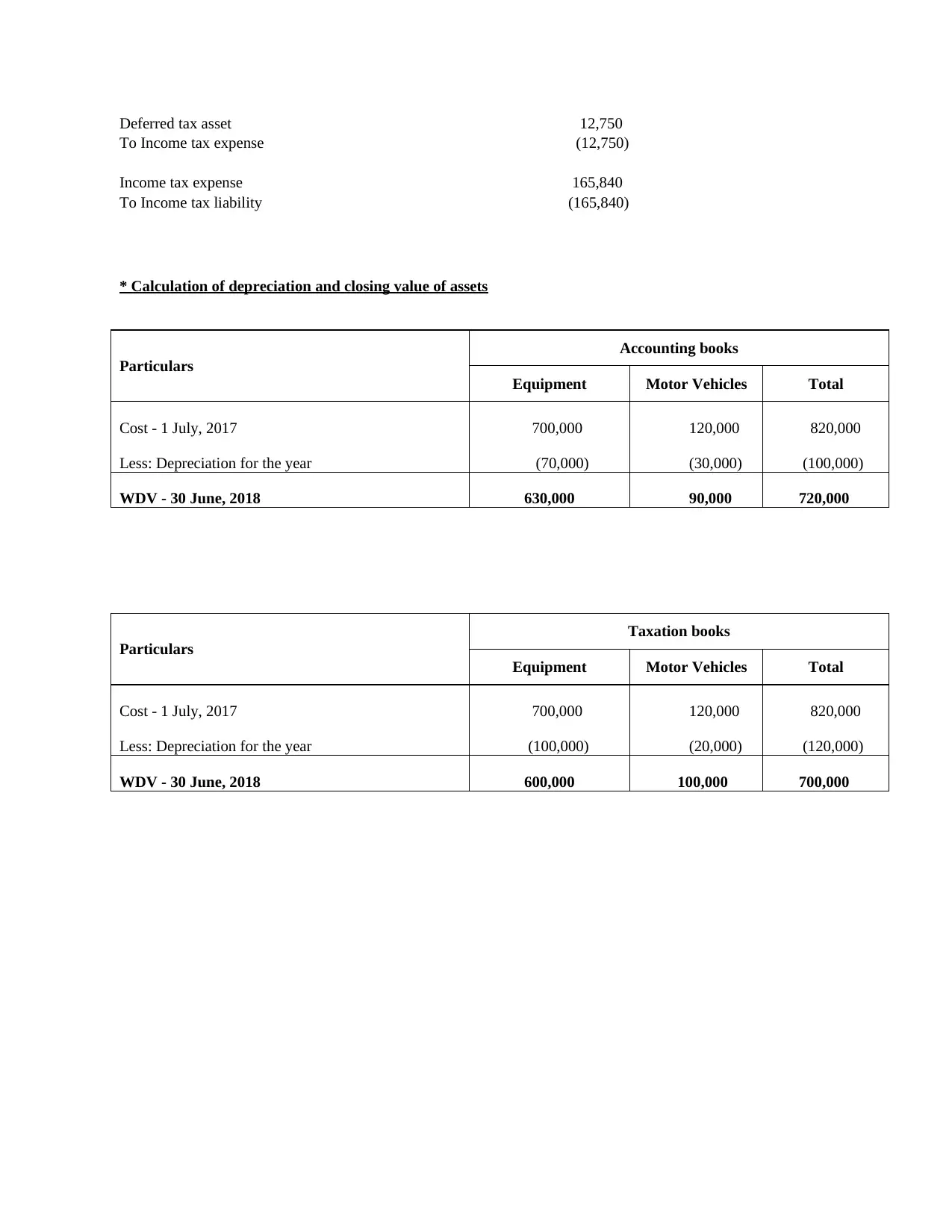

Deferred tax asset 12,750

To Income tax expense (12,750)

Income tax expense 165,840

To Income tax liability (165,840)

* Calculation of depreciation and closing value of assets

Particulars

Accounting books

Equipment Motor Vehicles Total

Cost - 1 July, 2017 700,000 120,000 820,000

Less: Depreciation for the year (70,000) (30,000) (100,000)

WDV - 30 June, 2018 630,000 90,000 720,000

Particulars

Taxation books

Equipment Motor Vehicles Total

Cost - 1 July, 2017 700,000 120,000 820,000

Less: Depreciation for the year (100,000) (20,000) (120,000)

WDV - 30 June, 2018 600,000 100,000 700,000

To Income tax expense (12,750)

Income tax expense 165,840

To Income tax liability (165,840)

* Calculation of depreciation and closing value of assets

Particulars

Accounting books

Equipment Motor Vehicles Total

Cost - 1 July, 2017 700,000 120,000 820,000

Less: Depreciation for the year (70,000) (30,000) (100,000)

WDV - 30 June, 2018 630,000 90,000 720,000

Particulars

Taxation books

Equipment Motor Vehicles Total

Cost - 1 July, 2017 700,000 120,000 820,000

Less: Depreciation for the year (100,000) (20,000) (120,000)

WDV - 30 June, 2018 600,000 100,000 700,000

Solution-4

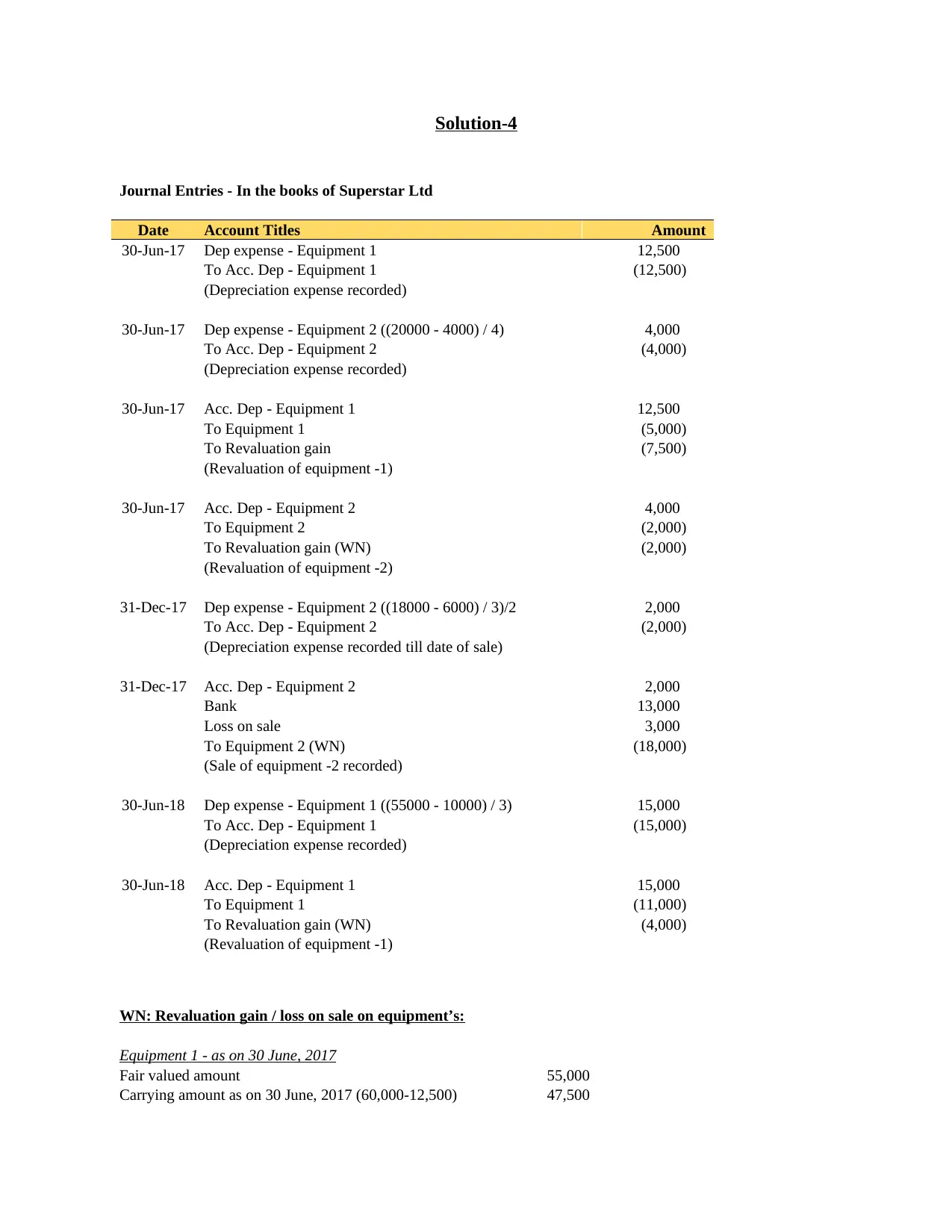

Journal Entries - In the books of Superstar Ltd

Date Account Titles Amount

30-Jun-17 Dep expense - Equipment 1 12,500

To Acc. Dep - Equipment 1 (12,500)

(Depreciation expense recorded)

30-Jun-17 Dep expense - Equipment 2 ((20000 - 4000) / 4) 4,000

To Acc. Dep - Equipment 2 (4,000)

(Depreciation expense recorded)

30-Jun-17 Acc. Dep - Equipment 1 12,500

To Equipment 1 (5,000)

To Revaluation gain (7,500)

(Revaluation of equipment -1)

30-Jun-17 Acc. Dep - Equipment 2 4,000

To Equipment 2 (2,000)

To Revaluation gain (WN) (2,000)

(Revaluation of equipment -2)

31-Dec-17 Dep expense - Equipment 2 ((18000 - 6000) / 3)/2 2,000

To Acc. Dep - Equipment 2 (2,000)

(Depreciation expense recorded till date of sale)

31-Dec-17 Acc. Dep - Equipment 2 2,000

Bank 13,000

Loss on sale 3,000

To Equipment 2 (WN) (18,000)

(Sale of equipment -2 recorded)

30-Jun-18 Dep expense - Equipment 1 ((55000 - 10000) / 3) 15,000

To Acc. Dep - Equipment 1 (15,000)

(Depreciation expense recorded)

30-Jun-18 Acc. Dep - Equipment 1 15,000

To Equipment 1 (11,000)

To Revaluation gain (WN) (4,000)

(Revaluation of equipment -1)

WN: Revaluation gain / loss on sale on equipment’s:

Equipment 1 - as on 30 June, 2017

Fair valued amount 55,000

Carrying amount as on 30 June, 2017 (60,000-12,500) 47,500

Journal Entries - In the books of Superstar Ltd

Date Account Titles Amount

30-Jun-17 Dep expense - Equipment 1 12,500

To Acc. Dep - Equipment 1 (12,500)

(Depreciation expense recorded)

30-Jun-17 Dep expense - Equipment 2 ((20000 - 4000) / 4) 4,000

To Acc. Dep - Equipment 2 (4,000)

(Depreciation expense recorded)

30-Jun-17 Acc. Dep - Equipment 1 12,500

To Equipment 1 (5,000)

To Revaluation gain (7,500)

(Revaluation of equipment -1)

30-Jun-17 Acc. Dep - Equipment 2 4,000

To Equipment 2 (2,000)

To Revaluation gain (WN) (2,000)

(Revaluation of equipment -2)

31-Dec-17 Dep expense - Equipment 2 ((18000 - 6000) / 3)/2 2,000

To Acc. Dep - Equipment 2 (2,000)

(Depreciation expense recorded till date of sale)

31-Dec-17 Acc. Dep - Equipment 2 2,000

Bank 13,000

Loss on sale 3,000

To Equipment 2 (WN) (18,000)

(Sale of equipment -2 recorded)

30-Jun-18 Dep expense - Equipment 1 ((55000 - 10000) / 3) 15,000

To Acc. Dep - Equipment 1 (15,000)

(Depreciation expense recorded)

30-Jun-18 Acc. Dep - Equipment 1 15,000

To Equipment 1 (11,000)

To Revaluation gain (WN) (4,000)

(Revaluation of equipment -1)

WN: Revaluation gain / loss on sale on equipment’s:

Equipment 1 - as on 30 June, 2017

Fair valued amount 55,000

Carrying amount as on 30 June, 2017 (60,000-12,500) 47,500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gain on revaluation 7,500

Equipment 1 - as on 30 June, 2018

Fair valued amount 44,000

Carrying amount as on 30 June, 2018 (55,000-15,000) 40,000

Gain on revaluation 4,000

Equipment 2 - as on 30 June, 2017

Fair valued amount 18,000

Carrying amount as on 30 June, 2017 (20,000-4,000) 16,000

Gain on revaluation 2,000

Equipment 2 - as on 30 June, 2018

Carrying amount as on 31 Dec, 2017 (18,000-2,000) 16,000

Proceeds from sale 13,000

Loss on sale 3,000

Equipment 1 - as on 30 June, 2018

Fair valued amount 44,000

Carrying amount as on 30 June, 2018 (55,000-15,000) 40,000

Gain on revaluation 4,000

Equipment 2 - as on 30 June, 2017

Fair valued amount 18,000

Carrying amount as on 30 June, 2017 (20,000-4,000) 16,000

Gain on revaluation 2,000

Equipment 2 - as on 30 June, 2018

Carrying amount as on 31 Dec, 2017 (18,000-2,000) 16,000

Proceeds from sale 13,000

Loss on sale 3,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Solution-5

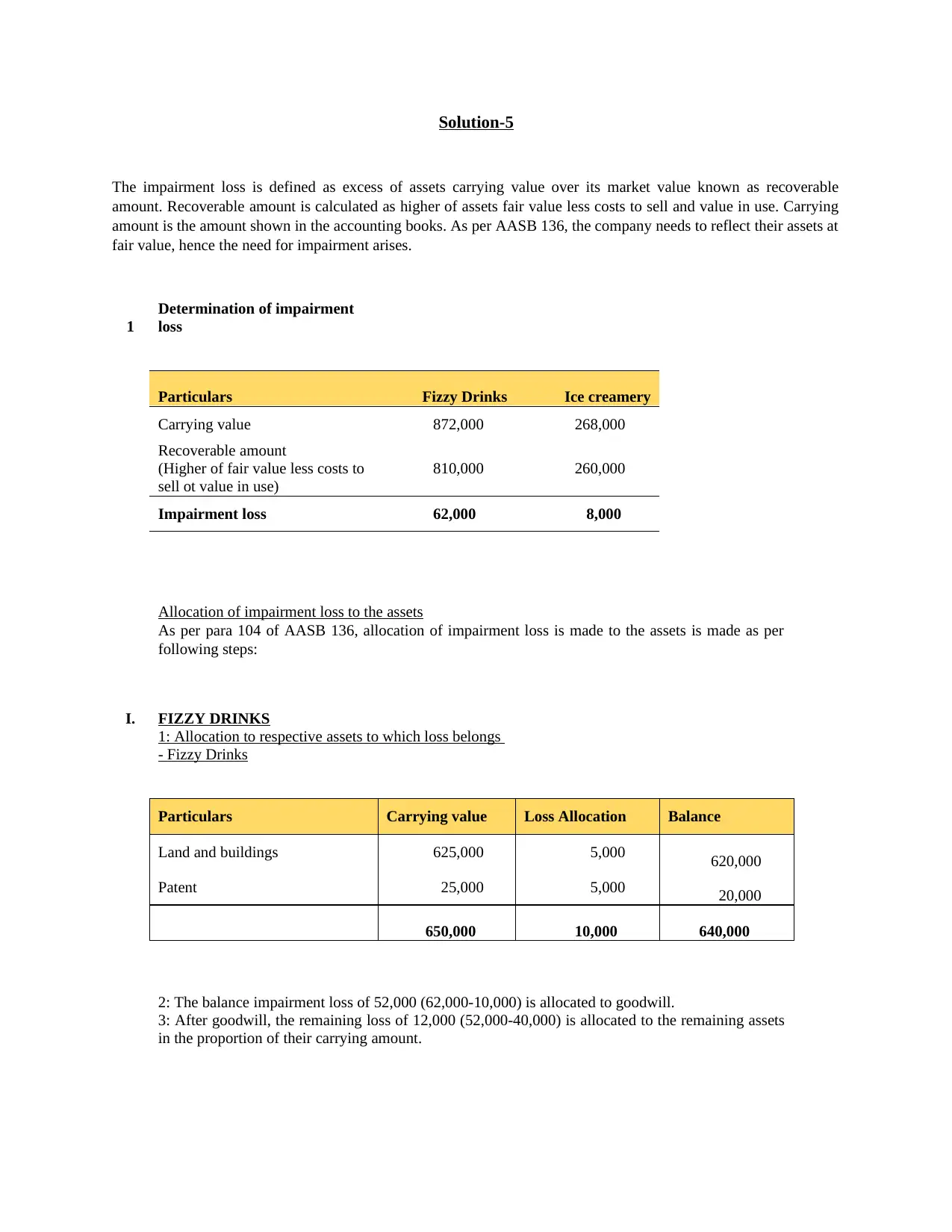

The impairment loss is defined as excess of assets carrying value over its market value known as recoverable

amount. Recoverable amount is calculated as higher of assets fair value less costs to sell and value in use. Carrying

amount is the amount shown in the accounting books. As per AASB 136, the company needs to reflect their assets at

fair value, hence the need for impairment arises.

1

Determination of impairment

loss

Particulars Fizzy Drinks Ice creamery

Carrying value 872,000 268,000

Recoverable amount

(Higher of fair value less costs to

sell ot value in use)

810,000 260,000

Impairment loss 62,000 8,000

Allocation of impairment loss to the assets

As per para 104 of AASB 136, allocation of impairment loss is made to the assets is made as per

following steps:

I. FIZZY DRINKS

1: Allocation to respective assets to which loss belongs

- Fizzy Drinks

Particulars Carrying value Loss Allocation Balance

Land and buildings 625,000 5,000 620,000

Patent 25,000 5,000 20,000

650,000 10,000 640,000

2: The balance impairment loss of 52,000 (62,000-10,000) is allocated to goodwill.

3: After goodwill, the remaining loss of 12,000 (52,000-40,000) is allocated to the remaining assets

in the proportion of their carrying amount.

The impairment loss is defined as excess of assets carrying value over its market value known as recoverable

amount. Recoverable amount is calculated as higher of assets fair value less costs to sell and value in use. Carrying

amount is the amount shown in the accounting books. As per AASB 136, the company needs to reflect their assets at

fair value, hence the need for impairment arises.

1

Determination of impairment

loss

Particulars Fizzy Drinks Ice creamery

Carrying value 872,000 268,000

Recoverable amount

(Higher of fair value less costs to

sell ot value in use)

810,000 260,000

Impairment loss 62,000 8,000

Allocation of impairment loss to the assets

As per para 104 of AASB 136, allocation of impairment loss is made to the assets is made as per

following steps:

I. FIZZY DRINKS

1: Allocation to respective assets to which loss belongs

- Fizzy Drinks

Particulars Carrying value Loss Allocation Balance

Land and buildings 625,000 5,000 620,000

Patent 25,000 5,000 20,000

650,000 10,000 640,000

2: The balance impairment loss of 52,000 (62,000-10,000) is allocated to goodwill.

3: After goodwill, the remaining loss of 12,000 (52,000-40,000) is allocated to the remaining assets

in the proportion of their carrying amount.

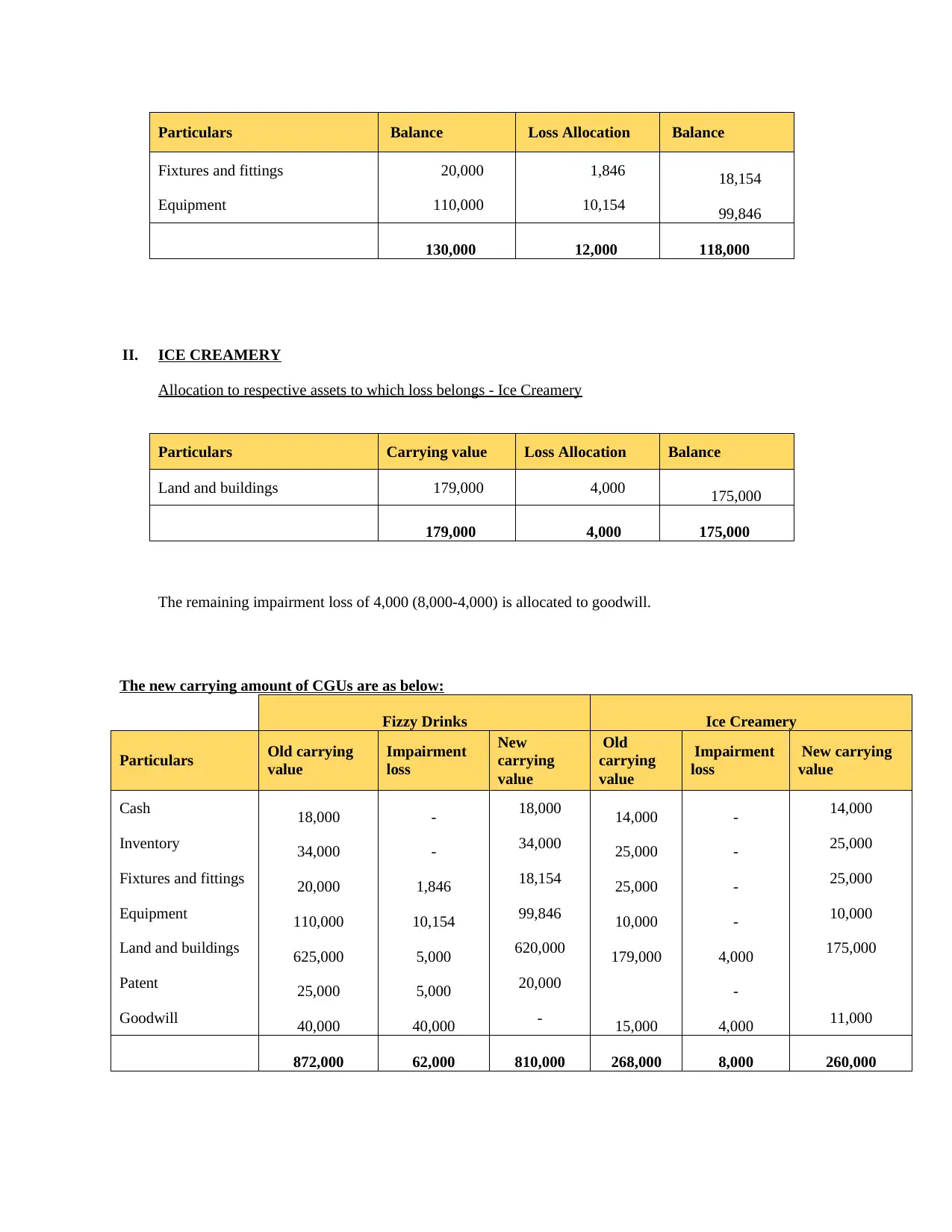

Particulars Balance Loss Allocation Balance

Fixtures and fittings 20,000 1,846 18,154

Equipment 110,000 10,154 99,846

130,000 12,000 118,000

II. ICE CREAMERY

Allocation to respective assets to which loss belongs - Ice Creamery

Particulars Carrying value Loss Allocation Balance

Land and buildings 179,000 4,000 175,000

179,000 4,000 175,000

The remaining impairment loss of 4,000 (8,000-4,000) is allocated to goodwill.

The new carrying amount of CGUs are as below:

Fizzy Drinks Ice Creamery

Particulars Old carrying

value

Impairment

loss

New

carrying

value

Old

carrying

value

Impairment

loss

New carrying

value

Cash 18,000 - 18,000 14,000 - 14,000

Inventory 34,000 - 34,000 25,000 - 25,000

Fixtures and fittings 20,000 1,846 18,154 25,000 - 25,000

Equipment 110,000 10,154 99,846 10,000 - 10,000

Land and buildings 625,000 5,000 620,000 179,000 4,000 175,000

Patent 25,000 5,000 20,000 -

Goodwill 40,000 40,000 - 15,000 4,000 11,000

872,000 62,000 810,000 268,000 8,000 260,000

Fixtures and fittings 20,000 1,846 18,154

Equipment 110,000 10,154 99,846

130,000 12,000 118,000

II. ICE CREAMERY

Allocation to respective assets to which loss belongs - Ice Creamery

Particulars Carrying value Loss Allocation Balance

Land and buildings 179,000 4,000 175,000

179,000 4,000 175,000

The remaining impairment loss of 4,000 (8,000-4,000) is allocated to goodwill.

The new carrying amount of CGUs are as below:

Fizzy Drinks Ice Creamery

Particulars Old carrying

value

Impairment

loss

New

carrying

value

Old

carrying

value

Impairment

loss

New carrying

value

Cash 18,000 - 18,000 14,000 - 14,000

Inventory 34,000 - 34,000 25,000 - 25,000

Fixtures and fittings 20,000 1,846 18,154 25,000 - 25,000

Equipment 110,000 10,154 99,846 10,000 - 10,000

Land and buildings 625,000 5,000 620,000 179,000 4,000 175,000

Patent 25,000 5,000 20,000 -

Goodwill 40,000 40,000 - 15,000 4,000 11,000

872,000 62,000 810,000 268,000 8,000 260,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Journal Entry as on 30 June, 2018

Account Titles Amount

Fizzy Drinks

Impairment Loss 62,000

Fixtures and fittings (1,846)

Equipment (10,154)

Land and buildings (5,000)

Patent (5,000)

Goodwill (40,000)

Ice creamery

Impairment Loss 8,000

Land and buildings (4,000)

Goodwill (4,000)

Account Titles Amount

Fizzy Drinks

Impairment Loss 62,000

Fixtures and fittings (1,846)

Equipment (10,154)

Land and buildings (5,000)

Patent (5,000)

Goodwill (40,000)

Ice creamery

Impairment Loss 8,000

Land and buildings (4,000)

Goodwill (4,000)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References:

http://www.aasb.gov.au/admin/file/content105/c9/AASB110_08-15.pdf

https://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-09.pdf

http://www.aasb.gov.au/admin/file/content105/c9/AASB108_07-04_COMPjan15_07-15.pdf

http://www.aasb.gov.au/admin/file/content105/c9/AASB110_08-15.pdf

https://www.aasb.gov.au/admin/file/content102/c3/AASB136_07-04_ERDRjun10_07-09.pdf

http://www.aasb.gov.au/admin/file/content105/c9/AASB108_07-04_COMPjan15_07-15.pdf

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.