Accounting Report: Walk About Ltd Break-Even and Profit Analysis

VerifiedAdded on 2022/12/29

|10

|1944

|51

Report

AI Summary

This accounting report examines break-even analysis, profit calculations, and management accounting techniques using Walk About Ltd as a case study. The report begins by calculating the break-even point in units and amount, followed by profit calculations based on different sales volumes and advertising campaign costs. It then discusses the limitations of break-even analysis. The second part of the report focuses on management accounting, explaining its importance and how it differs from financial accounting. It also highlights three key techniques management accountants use to achieve business objectives, including capital budgeting, marginal costing, and budgetary control, providing detailed explanations of each technique and their applications. The report concludes with a list of references used.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1..................................................................................................................................3

(a) Computing break even point in units and amount of Product A of Walk About Ltd............3

(b) Calculating profit on the sale of 75000 units.........................................................................3

(c) Computation of net profit when Walk About Ltd incurs advertising campaign cost of

£10000.........................................................................................................................................4

(d) Limitations of break even point.............................................................................................4

QUESTION 2..................................................................................................................................5

A) Importance of management accounting, and the way it differ from financial accounting

provides........................................................................................................................................5

Differences between management and financial accounting.......................................................6

Three techniques through which management accountant can attain business objectives..........6

REFERENCES................................................................................................................................8

QUESTION 1..................................................................................................................................3

(a) Computing break even point in units and amount of Product A of Walk About Ltd............3

(b) Calculating profit on the sale of 75000 units.........................................................................3

(c) Computation of net profit when Walk About Ltd incurs advertising campaign cost of

£10000.........................................................................................................................................4

(d) Limitations of break even point.............................................................................................4

QUESTION 2..................................................................................................................................5

A) Importance of management accounting, and the way it differ from financial accounting

provides........................................................................................................................................5

Differences between management and financial accounting.......................................................6

Three techniques through which management accountant can attain business objectives..........6

REFERENCES................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1

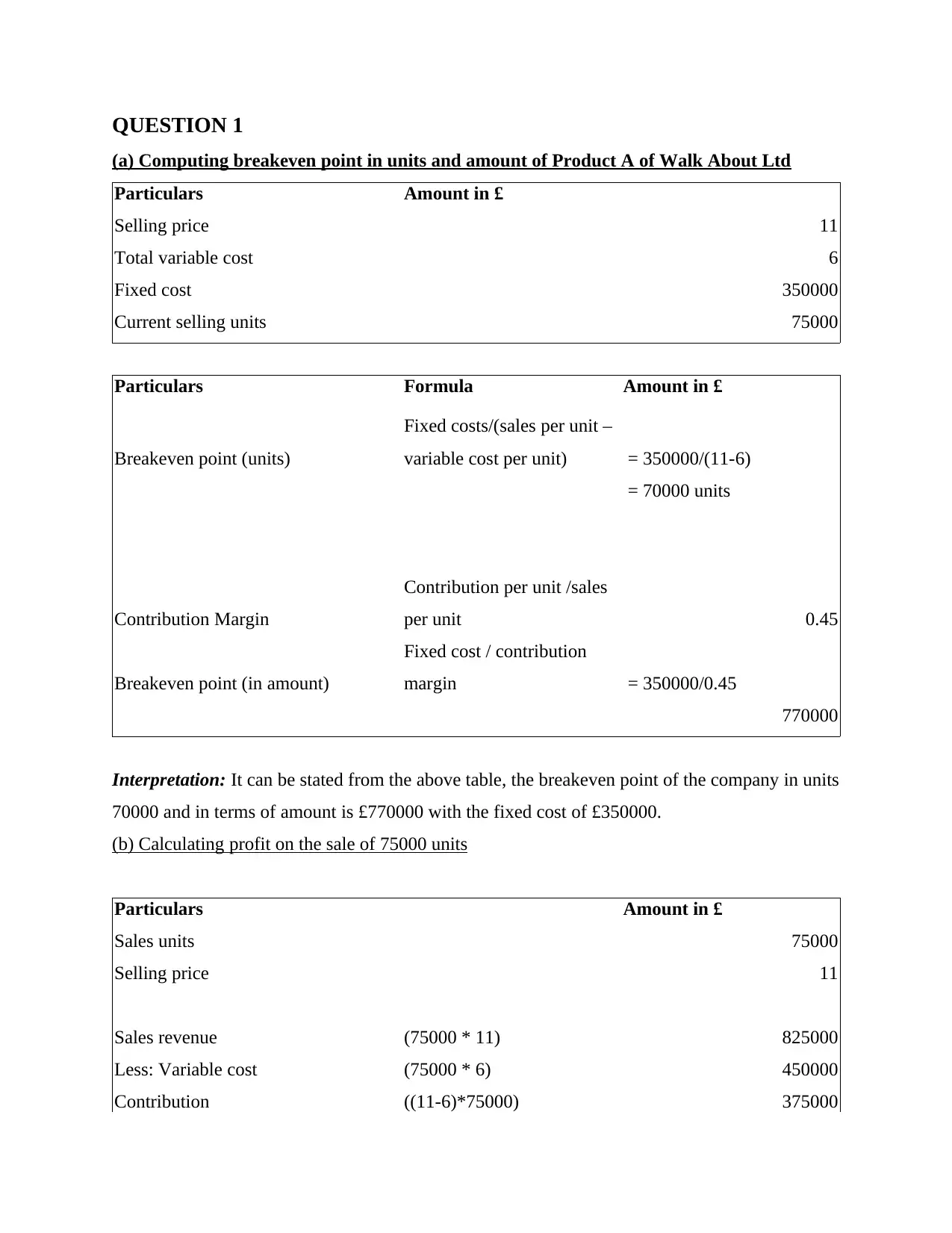

(a) Computing breakeven point in units and amount of Product A of Walk About Ltd

Particulars Amount in £

Selling price 11

Total variable cost 6

Fixed cost 350000

Current selling units 75000

Particulars Formula Amount in £

Breakeven point (units)

Fixed costs/(sales per unit –

variable cost per unit) = 350000/(11-6)

= 70000 units

Contribution Margin

Contribution per unit /sales

per unit 0.45

Breakeven point (in amount)

Fixed cost / contribution

margin = 350000/0.45

770000

Interpretation: It can be stated from the above table, the breakeven point of the company in units

70000 and in terms of amount is £770000 with the fixed cost of £350000.

(b) Calculating profit on the sale of 75000 units

Particulars Amount in £

Sales units 75000

Selling price 11

Sales revenue (75000 * 11) 825000

Less: Variable cost (75000 * 6) 450000

Contribution ((11-6)*75000) 375000

(a) Computing breakeven point in units and amount of Product A of Walk About Ltd

Particulars Amount in £

Selling price 11

Total variable cost 6

Fixed cost 350000

Current selling units 75000

Particulars Formula Amount in £

Breakeven point (units)

Fixed costs/(sales per unit –

variable cost per unit) = 350000/(11-6)

= 70000 units

Contribution Margin

Contribution per unit /sales

per unit 0.45

Breakeven point (in amount)

Fixed cost / contribution

margin = 350000/0.45

770000

Interpretation: It can be stated from the above table, the breakeven point of the company in units

70000 and in terms of amount is £770000 with the fixed cost of £350000.

(b) Calculating profit on the sale of 75000 units

Particulars Amount in £

Sales units 75000

Selling price 11

Sales revenue (75000 * 11) 825000

Less: Variable cost (75000 * 6) 450000

Contribution ((11-6)*75000) 375000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

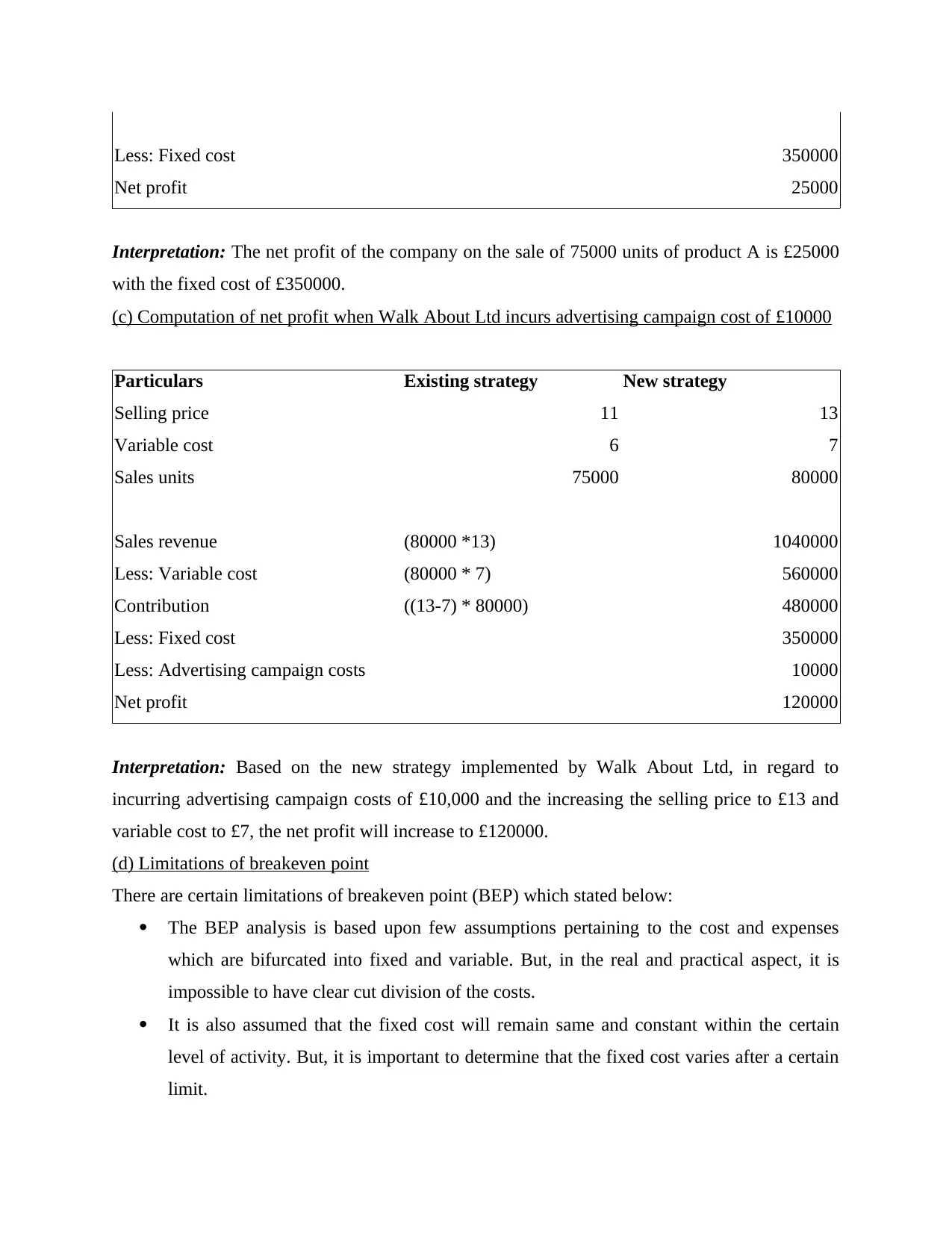

Less: Fixed cost 350000

Net profit 25000

Interpretation: The net profit of the company on the sale of 75000 units of product A is £25000

with the fixed cost of £350000.

(c) Computation of net profit when Walk About Ltd incurs advertising campaign cost of £10000

Particulars Existing strategy New strategy

Selling price 11 13

Variable cost 6 7

Sales units 75000 80000

Sales revenue (80000 *13) 1040000

Less: Variable cost (80000 * 7) 560000

Contribution ((13-7) * 80000) 480000

Less: Fixed cost 350000

Less: Advertising campaign costs 10000

Net profit 120000

Interpretation: Based on the new strategy implemented by Walk About Ltd, in regard to

incurring advertising campaign costs of £10,000 and the increasing the selling price to £13 and

variable cost to £7, the net profit will increase to £120000.

(d) Limitations of breakeven point

There are certain limitations of breakeven point (BEP) which stated below:

The BEP analysis is based upon few assumptions pertaining to the cost and expenses

which are bifurcated into fixed and variable. But, in the real and practical aspect, it is

impossible to have clear cut division of the costs.

It is also assumed that the fixed cost will remain same and constant within the certain

level of activity. But, it is important to determine that the fixed cost varies after a certain

limit.

Net profit 25000

Interpretation: The net profit of the company on the sale of 75000 units of product A is £25000

with the fixed cost of £350000.

(c) Computation of net profit when Walk About Ltd incurs advertising campaign cost of £10000

Particulars Existing strategy New strategy

Selling price 11 13

Variable cost 6 7

Sales units 75000 80000

Sales revenue (80000 *13) 1040000

Less: Variable cost (80000 * 7) 560000

Contribution ((13-7) * 80000) 480000

Less: Fixed cost 350000

Less: Advertising campaign costs 10000

Net profit 120000

Interpretation: Based on the new strategy implemented by Walk About Ltd, in regard to

incurring advertising campaign costs of £10,000 and the increasing the selling price to £13 and

variable cost to £7, the net profit will increase to £120000.

(d) Limitations of breakeven point

There are certain limitations of breakeven point (BEP) which stated below:

The BEP analysis is based upon few assumptions pertaining to the cost and expenses

which are bifurcated into fixed and variable. But, in the real and practical aspect, it is

impossible to have clear cut division of the costs.

It is also assumed that the fixed cost will remain same and constant within the certain

level of activity. But, it is important to determine that the fixed cost varies after a certain

limit.

It also has taken unrealistic assumption in regard to the product sells price which states

that it will remain same irrespective of the level of activity and fixed cost might vary with

respect to change in the level of output (Breakeven Analysis - Strengths and Limitations.

2020). The selling price remaining the same gives the straight revenue line which is not

right. Along with that the selling price of the product is dependent upon the various

factors which are external to the business such as demand and supply, competition etc.

which is very difficult to remain same or constant.

Many businesses sell more than 1 product so under such circumstances it becomes

difficult to carry out the BEP analysis. Along with this, the product mix to remain

unchanged is also difficult in practice.

QUESTION 2

A) Importance of management accounting, and the way it differs from financial accounting

provides

Management accounting is process of preparing and maintaining financial data,

document or information by manager so that it can several decisions that can be fruitful for

organisation in short and longer time frame. There are numerous importance of preparation and

management of numerous account for company which can be illustrated as follows:

It helps in reviewing actual performance of organisation: Management accounting is

important as it contained all necessary information related to finance and business statistic so that

exact steps can be taken in order to gain more profit from products.

Planning: Secondly, management accounting is important as it represent financial as well as

non-financial information at regular interval so that manager can easily have evaluated

performance and plan steps that need to be taken in order to achieve end goals (Dahal, 2018). So,

it helps manager in planning several strategies that could be used by firm to manage resources,

development of budget for meeting all expense.

Provide reliability: Another importance of management accounting is that it helps in building

reliability of business so that customers can easily trust the company. Various stakeholder such

as investors or employees can easily trust company as management accounting ensure accuracy

of accounts.

that it will remain same irrespective of the level of activity and fixed cost might vary with

respect to change in the level of output (Breakeven Analysis - Strengths and Limitations.

2020). The selling price remaining the same gives the straight revenue line which is not

right. Along with that the selling price of the product is dependent upon the various

factors which are external to the business such as demand and supply, competition etc.

which is very difficult to remain same or constant.

Many businesses sell more than 1 product so under such circumstances it becomes

difficult to carry out the BEP analysis. Along with this, the product mix to remain

unchanged is also difficult in practice.

QUESTION 2

A) Importance of management accounting, and the way it differs from financial accounting

provides

Management accounting is process of preparing and maintaining financial data,

document or information by manager so that it can several decisions that can be fruitful for

organisation in short and longer time frame. There are numerous importance of preparation and

management of numerous account for company which can be illustrated as follows:

It helps in reviewing actual performance of organisation: Management accounting is

important as it contained all necessary information related to finance and business statistic so that

exact steps can be taken in order to gain more profit from products.

Planning: Secondly, management accounting is important as it represent financial as well as

non-financial information at regular interval so that manager can easily have evaluated

performance and plan steps that need to be taken in order to achieve end goals (Dahal, 2018). So,

it helps manager in planning several strategies that could be used by firm to manage resources,

development of budget for meeting all expense.

Provide reliability: Another importance of management accounting is that it helps in building

reliability of business so that customers can easily trust the company. Various stakeholder such

as investors or employees can easily trust company as management accounting ensure accuracy

of accounts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Differences between management and financial accounting

Management and financial accounting differ from each other’s as management

accounting is related to collecting of account data in order to prepare financial statements.

Whereas management accounting is including all information related to internal process that are

helpful in making records of businesses transaction. There are various categories on the basis of

which differences can be easily made between management and financial accounts that are

explained as follows:

System: It can be illustrating that management accounting focused on various bottleneck

operations so that company profitability can be enhanced while financial accounting care about

the way profit can be generated.

Timing: Management accounting report must be prepared at frequently basis so that manager

has sufficient information in order to act in particular manners for growth and success of

enterprise. On the other hand, financial accounts are due on specific period or end of each year or

every quarter so that necessary decision can be taken by manager.

Report focusing: It is another key difference between financial and management accounting that

is it lead to preparation of financial statement so that it can be shared to public as well as internal

and external stakeholder. While management accounting emphasis on operations reporting that

need to be shared within firm so that necessary decision can be made by manager (Dávila, 2019).

Standard: In order to prepare financial accounting, manager needs to follow various accounting

standard as compared to management accounting as it is just made for internal consumptions.

More accurate information: It can be stated that financial accounting relies on more accurate

data, statistic and facts so that exact report can be made related to financial information of

company. While management accounting frequently contained estimates data rather than proven

facts.

Three techniques through which management accountant can attain business objectives

From the above analysis it is clear that the management accounting is very helpful for the

company in managing the business operations of the company. this is particularly because of the

reason that when the management accounting is used then this assist the company in managing

the operations in proper and effective manner (Al-Khasawneh, Endut and Rashid, 2020). These

management accounting assist the company in creating a good business decision making as the

Management and financial accounting differ from each other’s as management

accounting is related to collecting of account data in order to prepare financial statements.

Whereas management accounting is including all information related to internal process that are

helpful in making records of businesses transaction. There are various categories on the basis of

which differences can be easily made between management and financial accounts that are

explained as follows:

System: It can be illustrating that management accounting focused on various bottleneck

operations so that company profitability can be enhanced while financial accounting care about

the way profit can be generated.

Timing: Management accounting report must be prepared at frequently basis so that manager

has sufficient information in order to act in particular manners for growth and success of

enterprise. On the other hand, financial accounts are due on specific period or end of each year or

every quarter so that necessary decision can be taken by manager.

Report focusing: It is another key difference between financial and management accounting that

is it lead to preparation of financial statement so that it can be shared to public as well as internal

and external stakeholder. While management accounting emphasis on operations reporting that

need to be shared within firm so that necessary decision can be made by manager (Dávila, 2019).

Standard: In order to prepare financial accounting, manager needs to follow various accounting

standard as compared to management accounting as it is just made for internal consumptions.

More accurate information: It can be stated that financial accounting relies on more accurate

data, statistic and facts so that exact report can be made related to financial information of

company. While management accounting frequently contained estimates data rather than proven

facts.

Three techniques through which management accountant can attain business objectives

From the above analysis it is clear that the management accounting is very helpful for the

company in managing the business operations of the company. this is particularly because of the

reason that when the management accounting is used then this assist the company in managing

the operations in proper and effective manner (Al-Khasawneh, Endut and Rashid, 2020). These

management accounting assist the company in creating a good business decision making as the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

use of financial accounts provide a guidance to the employees. The major techniques which the

management accountant can use in order to attain the business objectives are as follows-

Capital Budgeting: it is a most important technique of management accounting. This

technique helps in find out which investment is beneficial for the company and how much profit

it generates, it is a process of evaluating investment and huge expenses in order to obtain the best

return on investment. Organisation would like to invest in all profitable projects but due to

limitation on the availability of capital an organisation has to choose between different projects

through using these techniques: pay back and post payback period and NPV, ARR, IRR

company find out most profitable project. This capital budgeting assists the company in

managing the objective of the business as this assist company in selecting the best alternative for

the purpose of the investment. This will help the company in selecting the best suitable option

which is beneficial for the company.

Marginal Costing: it is the technique which is used for finding out the extra cost

incurred on additional unit of goods and it helps to fix the selling price of the product by using

contribution, fixed and variable cost. In this technique variable cost per unit always remains

constant. And fixed cost does not change with an increase or decrease in production level, it can

help an organization for optimize their production through economies of scale. The use of

marginal costing is helpful in attaining the business objective as this involves the fixed cost and

variable cost and this provide a data to company that how they can manage the cost of the

company (Jbarah, 2018).

Budgetary control: The management accountant uses the technique for planning and

controlling the various activities of the business, it is important technique for directing a business

in desired direction. it is the process by which budgets are prepared for the future and compared

with the actual performance for finding out the variances through this management takes right

decisions, if there are any loopholes then it is removed by working on it and increase

performance and it also helps to co-ordinate the activities of the organisation. Budgetary control

clearly defines the responsibility and promote coordination and communication between

employees. This budget assists the company in managing the business and try to attain the

objective of effective and productive working. The major reason for this is that when the budget

is made then this provides assistance to the company that how they have to work.

management accountant can use in order to attain the business objectives are as follows-

Capital Budgeting: it is a most important technique of management accounting. This

technique helps in find out which investment is beneficial for the company and how much profit

it generates, it is a process of evaluating investment and huge expenses in order to obtain the best

return on investment. Organisation would like to invest in all profitable projects but due to

limitation on the availability of capital an organisation has to choose between different projects

through using these techniques: pay back and post payback period and NPV, ARR, IRR

company find out most profitable project. This capital budgeting assists the company in

managing the objective of the business as this assist company in selecting the best alternative for

the purpose of the investment. This will help the company in selecting the best suitable option

which is beneficial for the company.

Marginal Costing: it is the technique which is used for finding out the extra cost

incurred on additional unit of goods and it helps to fix the selling price of the product by using

contribution, fixed and variable cost. In this technique variable cost per unit always remains

constant. And fixed cost does not change with an increase or decrease in production level, it can

help an organization for optimize their production through economies of scale. The use of

marginal costing is helpful in attaining the business objective as this involves the fixed cost and

variable cost and this provide a data to company that how they can manage the cost of the

company (Jbarah, 2018).

Budgetary control: The management accountant uses the technique for planning and

controlling the various activities of the business, it is important technique for directing a business

in desired direction. it is the process by which budgets are prepared for the future and compared

with the actual performance for finding out the variances through this management takes right

decisions, if there are any loopholes then it is removed by working on it and increase

performance and it also helps to co-ordinate the activities of the organisation. Budgetary control

clearly defines the responsibility and promote coordination and communication between

employees. This budget assists the company in managing the business and try to attain the

objective of effective and productive working. The major reason for this is that when the budget

is made then this provides assistance to the company that how they have to work.

REFERENCES

Books and Journal

Al-Khasawneh, S., Endut, W. and Rashid, N., 2020. Relationship between Modern Management

Accounting Techniques and Organizational Performance of Industrial Sector Listed in

Amman Stock Exchange. International Journal of Management, Accounting and

Economics, 7(5), pp.212-234.

Dahal, R. K., 2018. Management Accounting and Control System. NCC Journal, 3(1). pp.153-

166.

Dávila, A., 2019. Emerging Themes in Management Accounting and Control Research. Revista

de Contabilidad-Spanish Accounting Review, 22(1). pp.1-5.

Jbarah, S.S., 2018. The impact of strategic management accounting techniques in taking

investment decisions in the jordanian industrial companies. International Business

Research, 11(1), pp.145-156.

Online

Breakeven Analysis - Strengths and Limitations. 2020. [Online]. Available

Through:<https://www.tutor2u.net/business/reference/breakeven-analysis-strengths-and-

limitations>.

Books and Journal

Al-Khasawneh, S., Endut, W. and Rashid, N., 2020. Relationship between Modern Management

Accounting Techniques and Organizational Performance of Industrial Sector Listed in

Amman Stock Exchange. International Journal of Management, Accounting and

Economics, 7(5), pp.212-234.

Dahal, R. K., 2018. Management Accounting and Control System. NCC Journal, 3(1). pp.153-

166.

Dávila, A., 2019. Emerging Themes in Management Accounting and Control Research. Revista

de Contabilidad-Spanish Accounting Review, 22(1). pp.1-5.

Jbarah, S.S., 2018. The impact of strategic management accounting techniques in taking

investment decisions in the jordanian industrial companies. International Business

Research, 11(1), pp.145-156.

Online

Breakeven Analysis - Strengths and Limitations. 2020. [Online]. Available

Through:<https://www.tutor2u.net/business/reference/breakeven-analysis-strengths-and-

limitations>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.