Preparation of Financial Statement and Evaluating Balance Sheet

VerifiedAdded on 2023/01/04

|11

|2995

|61

AI Summary

This document provides information on the preparation of financial statements and evaluating why the statement of financial position balances. It also includes a detailed analysis and interpretation of the financial performance and position of Chocco plc.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

QUESTION 1.............................................................................................................................3

a) Preparation of financial statement......................................................................................3

b) Evaluating why the statement of financial position balances............................................4

QUESTION 2.............................................................................................................................4

a) Schedule of ratios for Chocco plc for 2019 and 2018........................................................4

b) Analysing and interpreting the financial performance and position of Chocco plc..........6

REFERENCES.........................................................................................................................11

QUESTION 1.............................................................................................................................3

a) Preparation of financial statement......................................................................................3

b) Evaluating why the statement of financial position balances............................................4

QUESTION 2.............................................................................................................................4

a) Schedule of ratios for Chocco plc for 2019 and 2018........................................................4

b) Analysing and interpreting the financial performance and position of Chocco plc..........6

REFERENCES.........................................................................................................................11

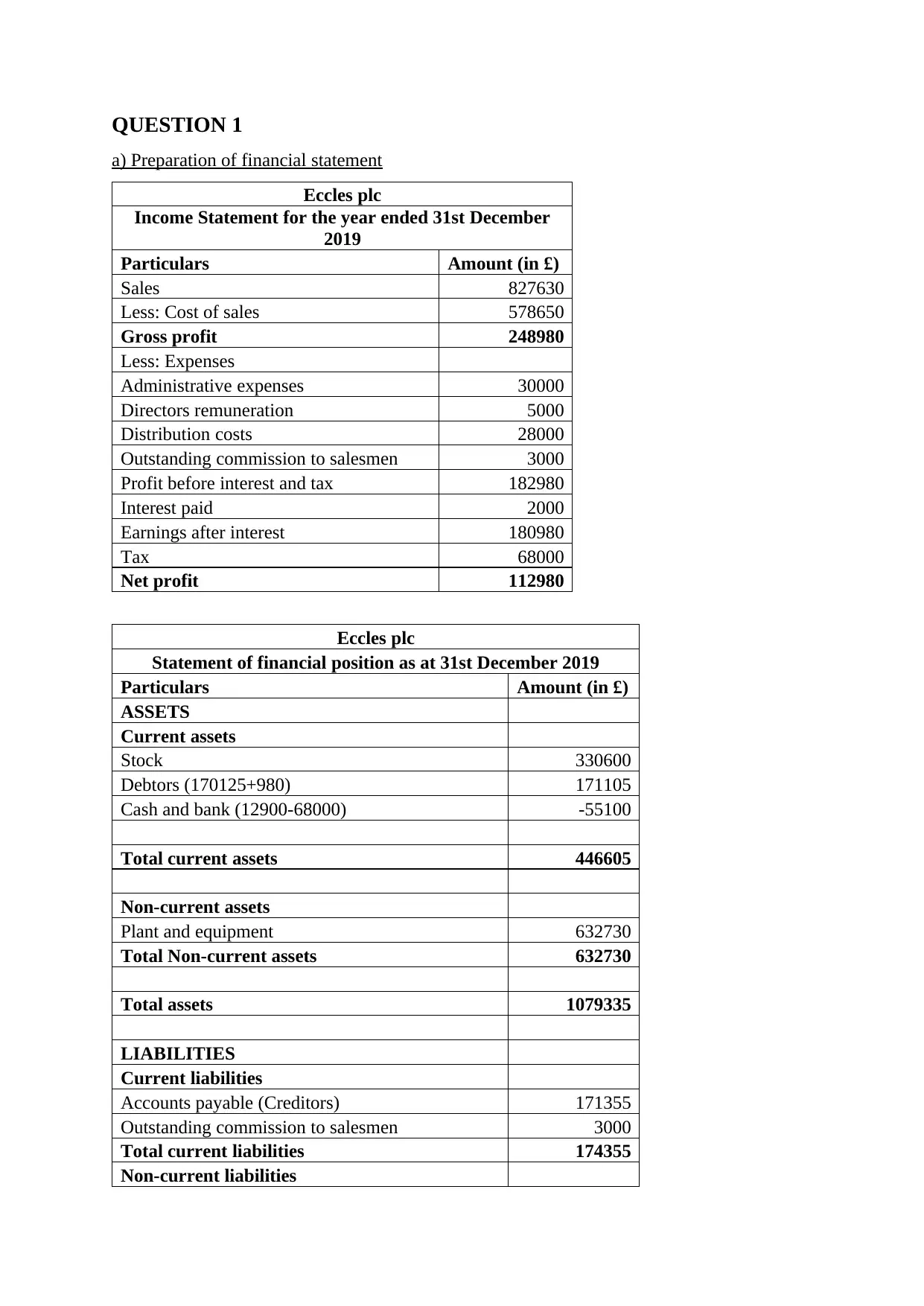

QUESTION 1

a) Preparation of financial statement

Eccles plc

Income Statement for the year ended 31st December

2019

Particulars Amount (in £)

Sales 827630

Less: Cost of sales 578650

Gross profit 248980

Less: Expenses

Administrative expenses 30000

Directors remuneration 5000

Distribution costs 28000

Outstanding commission to salesmen 3000

Profit before interest and tax 182980

Interest paid 2000

Earnings after interest 180980

Tax 68000

Net profit 112980

Eccles plc

Statement of financial position as at 31st December 2019

Particulars Amount (in £)

ASSETS

Current assets

Stock 330600

Debtors (170125+980) 171105

Cash and bank (12900-68000) -55100

Total current assets 446605

Non-current assets

Plant and equipment 632730

Total Non-current assets 632730

Total assets 1079335

LIABILITIES

Current liabilities

Accounts payable (Creditors) 171355

Outstanding commission to salesmen 3000

Total current liabilities 174355

Non-current liabilities

a) Preparation of financial statement

Eccles plc

Income Statement for the year ended 31st December

2019

Particulars Amount (in £)

Sales 827630

Less: Cost of sales 578650

Gross profit 248980

Less: Expenses

Administrative expenses 30000

Directors remuneration 5000

Distribution costs 28000

Outstanding commission to salesmen 3000

Profit before interest and tax 182980

Interest paid 2000

Earnings after interest 180980

Tax 68000

Net profit 112980

Eccles plc

Statement of financial position as at 31st December 2019

Particulars Amount (in £)

ASSETS

Current assets

Stock 330600

Debtors (170125+980) 171105

Cash and bank (12900-68000) -55100

Total current assets 446605

Non-current assets

Plant and equipment 632730

Total Non-current assets 632730

Total assets 1079335

LIABILITIES

Current liabilities

Accounts payable (Creditors) 171355

Outstanding commission to salesmen 3000

Total current liabilities 174355

Non-current liabilities

Share capital (310000+300000) 610000

4% Debentures 100000

Retained profits at 1st January 2018 (132000-

50000) 82000

Net profit for the year ended 31st December 2019 112980

Total Non-current liabilities 904980

Total liabilities 1079335

b) Evaluating why the statement of financial position balances

The statement of position is one of the most important financial statements as it

provides information on the firms’ assets, liabilities and any difference between the two as of

the date of that accounting period. This statement must reflect the basic accounting principles

and the standards. The balance sheet is prepared in such a way that all the assets of a business

entity is equivalent to the sum total of entire amount of liabilities and the equity (Daniel,

Marioara and Isabela, 2017). The reason why balance sheet is always at the equilibrium is

because of the reason that the assets of the firm might have being financed from the internal

sources, for instance, the share capital and the profits of the company or from the external

sources like lenders, loan from the bank, trade creditors and so forth. Therefore, the total

assets of the business must be equivalent to the amount of the capital invested by the business

owners in the form of share capital or profits or any other form of borrowings, thus, the total

assets of the entity must to equivalent to the sum total of the total liabilities and equity of that

entity. This has resulted into the accounting equation of Total assets = Total liabilities +

Equity.

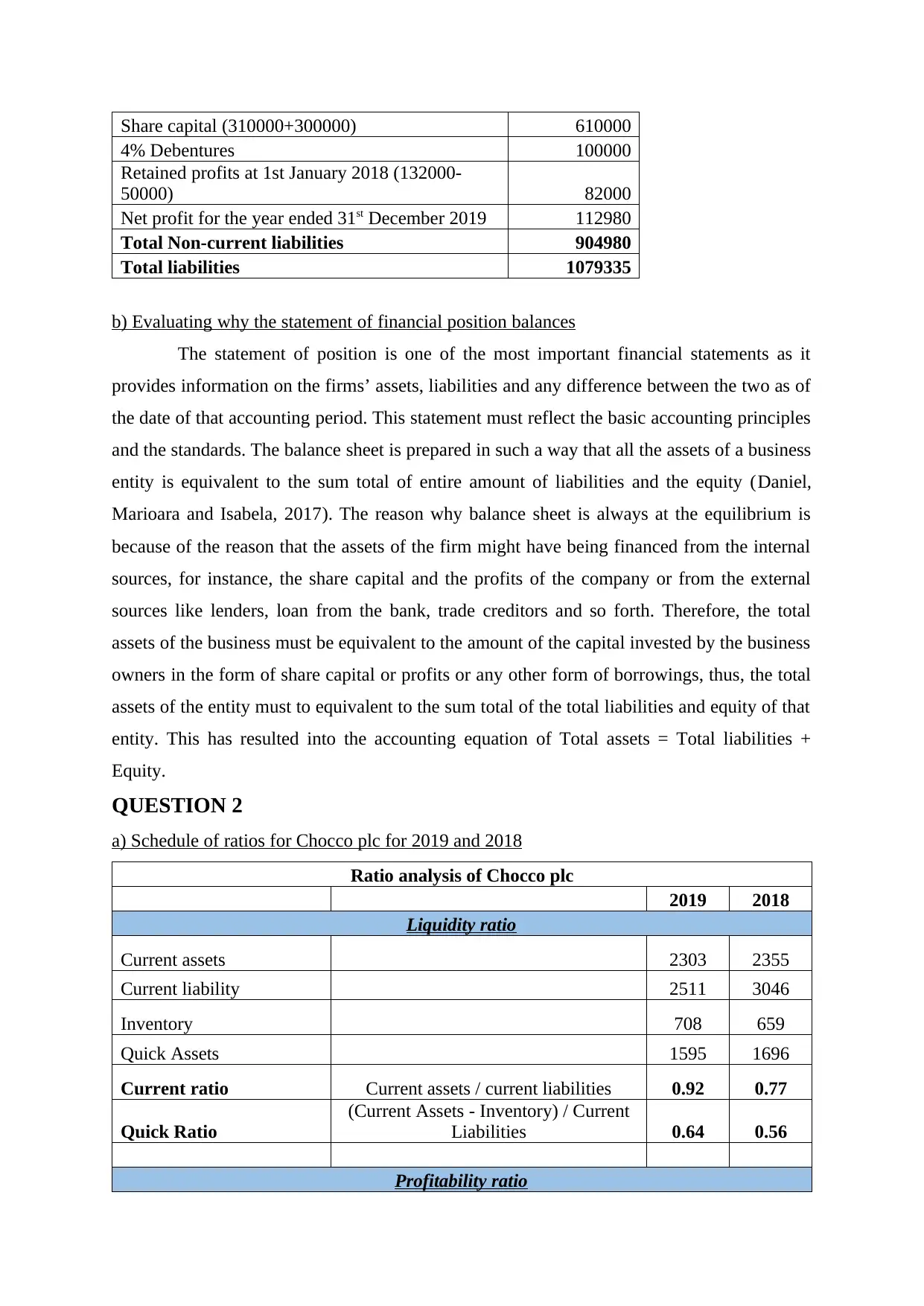

QUESTION 2

a) Schedule of ratios for Chocco plc for 2019 and 2018

Ratio analysis of Chocco plc

2019 2018

Liquidity ratio

Current assets 2303 2355

Current liability 2511 3046

Inventory 708 659

Quick Assets 1595 1696

Current ratio Current assets / current liabilities 0.92 0.77

Quick Ratio

(Current Assets - Inventory) / Current

Liabilities 0.64 0.56

Profitability ratio

4% Debentures 100000

Retained profits at 1st January 2018 (132000-

50000) 82000

Net profit for the year ended 31st December 2019 112980

Total Non-current liabilities 904980

Total liabilities 1079335

b) Evaluating why the statement of financial position balances

The statement of position is one of the most important financial statements as it

provides information on the firms’ assets, liabilities and any difference between the two as of

the date of that accounting period. This statement must reflect the basic accounting principles

and the standards. The balance sheet is prepared in such a way that all the assets of a business

entity is equivalent to the sum total of entire amount of liabilities and the equity (Daniel,

Marioara and Isabela, 2017). The reason why balance sheet is always at the equilibrium is

because of the reason that the assets of the firm might have being financed from the internal

sources, for instance, the share capital and the profits of the company or from the external

sources like lenders, loan from the bank, trade creditors and so forth. Therefore, the total

assets of the business must be equivalent to the amount of the capital invested by the business

owners in the form of share capital or profits or any other form of borrowings, thus, the total

assets of the entity must to equivalent to the sum total of the total liabilities and equity of that

entity. This has resulted into the accounting equation of Total assets = Total liabilities +

Equity.

QUESTION 2

a) Schedule of ratios for Chocco plc for 2019 and 2018

Ratio analysis of Chocco plc

2019 2018

Liquidity ratio

Current assets 2303 2355

Current liability 2511 3046

Inventory 708 659

Quick Assets 1595 1696

Current ratio Current assets / current liabilities 0.92 0.77

Quick Ratio

(Current Assets - Inventory) / Current

Liabilities 0.64 0.56

Profitability ratio

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

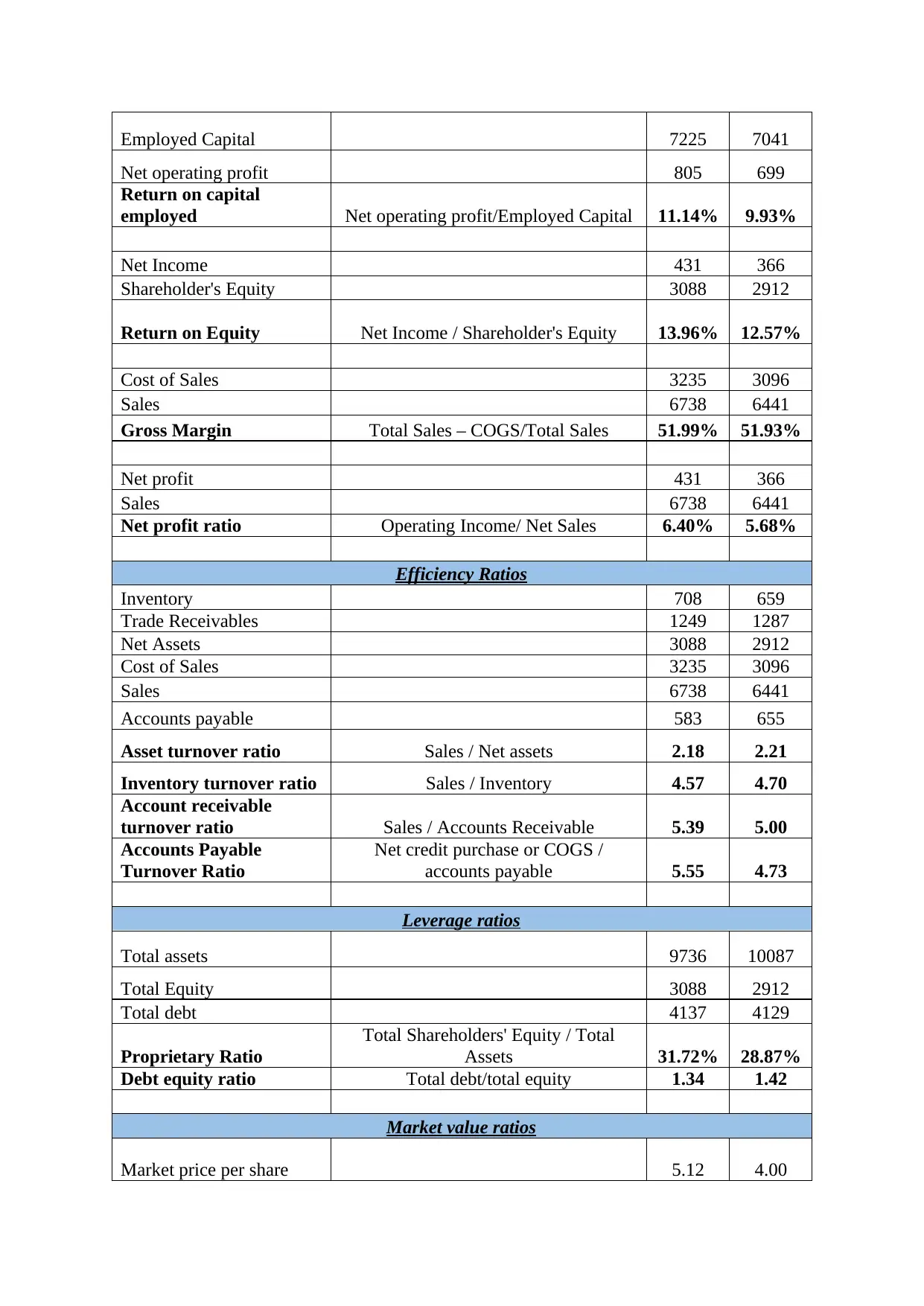

Employed Capital 7225 7041

Net operating profit 805 699

Return on capital

employed Net operating profit/Employed Capital 11.14% 9.93%

Net Income 431 366

Shareholder's Equity 3088 2912

Return on Equity Net Income / Shareholder's Equity 13.96% 12.57%

Cost of Sales 3235 3096

Sales 6738 6441

Gross Margin Total Sales – COGS/Total Sales 51.99% 51.93%

Net profit 431 366

Sales 6738 6441

Net profit ratio Operating Income/ Net Sales 6.40% 5.68%

Efficiency Ratios

Inventory 708 659

Trade Receivables 1249 1287

Net Assets 3088 2912

Cost of Sales 3235 3096

Sales 6738 6441

Accounts payable 583 655

Asset turnover ratio Sales / Net assets 2.18 2.21

Inventory turnover ratio Sales / Inventory 4.57 4.70

Account receivable

turnover ratio Sales / Accounts Receivable 5.39 5.00

Accounts Payable

Turnover Ratio

Net credit purchase or COGS /

accounts payable 5.55 4.73

Leverage ratios

Total assets 9736 10087

Total Equity 3088 2912

Total debt 4137 4129

Proprietary Ratio

Total Shareholders' Equity / Total

Assets 31.72% 28.87%

Debt equity ratio Total debt/total equity 1.34 1.42

Market value ratios

Market price per share 5.12 4.00

Net operating profit 805 699

Return on capital

employed Net operating profit/Employed Capital 11.14% 9.93%

Net Income 431 366

Shareholder's Equity 3088 2912

Return on Equity Net Income / Shareholder's Equity 13.96% 12.57%

Cost of Sales 3235 3096

Sales 6738 6441

Gross Margin Total Sales – COGS/Total Sales 51.99% 51.93%

Net profit 431 366

Sales 6738 6441

Net profit ratio Operating Income/ Net Sales 6.40% 5.68%

Efficiency Ratios

Inventory 708 659

Trade Receivables 1249 1287

Net Assets 3088 2912

Cost of Sales 3235 3096

Sales 6738 6441

Accounts payable 583 655

Asset turnover ratio Sales / Net assets 2.18 2.21

Inventory turnover ratio Sales / Inventory 4.57 4.70

Account receivable

turnover ratio Sales / Accounts Receivable 5.39 5.00

Accounts Payable

Turnover Ratio

Net credit purchase or COGS /

accounts payable 5.55 4.73

Leverage ratios

Total assets 9736 10087

Total Equity 3088 2912

Total debt 4137 4129

Proprietary Ratio

Total Shareholders' Equity / Total

Assets 31.72% 28.87%

Debt equity ratio Total debt/total equity 1.34 1.42

Market value ratios

Market price per share 5.12 4.00

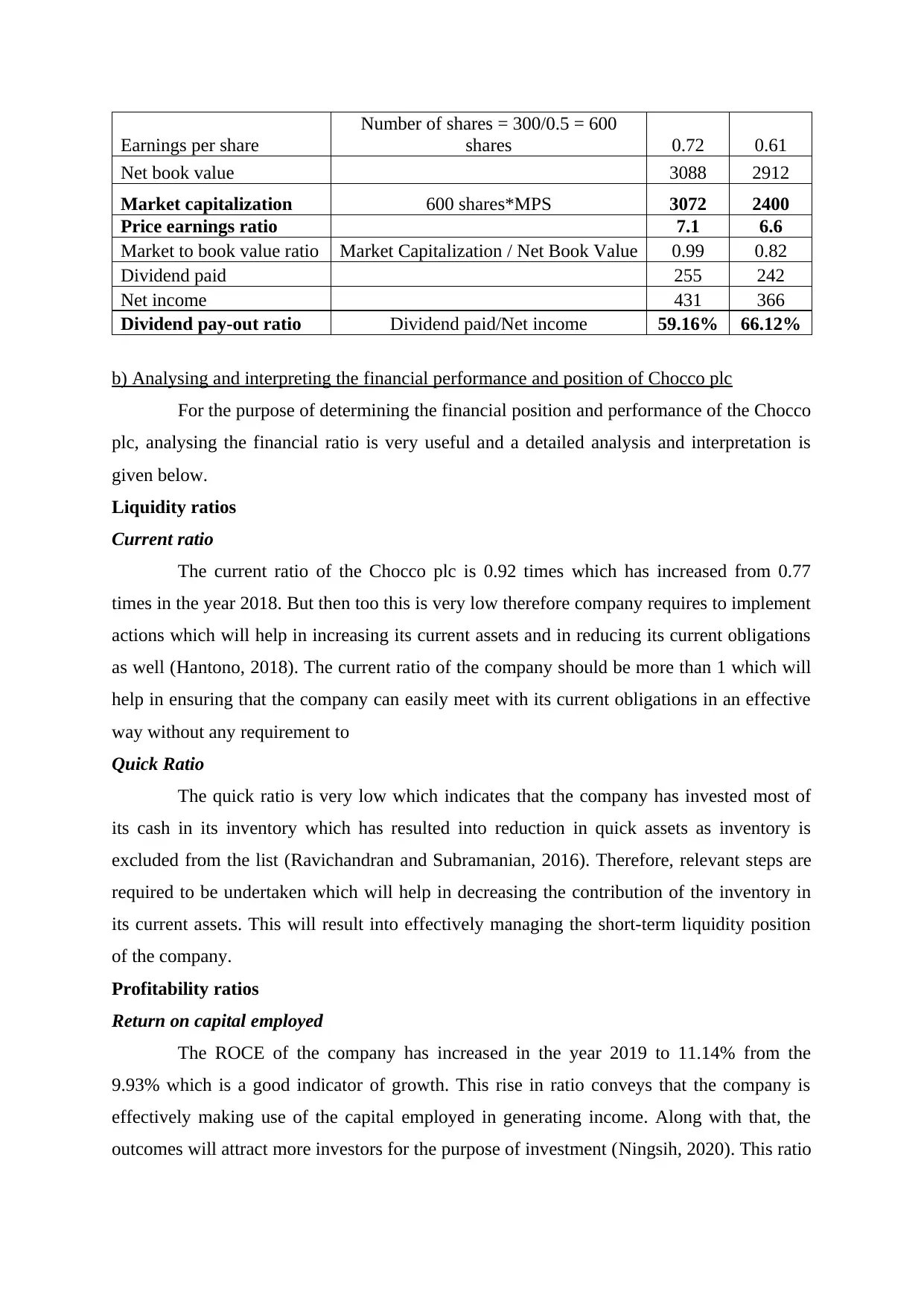

Earnings per share

Number of shares = 300/0.5 = 600

shares 0.72 0.61

Net book value 3088 2912

Market capitalization 600 shares*MPS 3072 2400

Price earnings ratio 7.1 6.6

Market to book value ratio Market Capitalization / Net Book Value 0.99 0.82

Dividend paid 255 242

Net income 431 366

Dividend pay-out ratio Dividend paid/Net income 59.16% 66.12%

b) Analysing and interpreting the financial performance and position of Chocco plc

For the purpose of determining the financial position and performance of the Chocco

plc, analysing the financial ratio is very useful and a detailed analysis and interpretation is

given below.

Liquidity ratios

Current ratio

The current ratio of the Chocco plc is 0.92 times which has increased from 0.77

times in the year 2018. But then too this is very low therefore company requires to implement

actions which will help in increasing its current assets and in reducing its current obligations

as well (Hantono, 2018). The current ratio of the company should be more than 1 which will

help in ensuring that the company can easily meet with its current obligations in an effective

way without any requirement to

Quick Ratio

The quick ratio is very low which indicates that the company has invested most of

its cash in its inventory which has resulted into reduction in quick assets as inventory is

excluded from the list (Ravichandran and Subramanian, 2016). Therefore, relevant steps are

required to be undertaken which will help in decreasing the contribution of the inventory in

its current assets. This will result into effectively managing the short-term liquidity position

of the company.

Profitability ratios

Return on capital employed

The ROCE of the company has increased in the year 2019 to 11.14% from the

9.93% which is a good indicator of growth. This rise in ratio conveys that the company is

effectively making use of the capital employed in generating income. Along with that, the

outcomes will attract more investors for the purpose of investment (Ningsih, 2020). This ratio

Number of shares = 300/0.5 = 600

shares 0.72 0.61

Net book value 3088 2912

Market capitalization 600 shares*MPS 3072 2400

Price earnings ratio 7.1 6.6

Market to book value ratio Market Capitalization / Net Book Value 0.99 0.82

Dividend paid 255 242

Net income 431 366

Dividend pay-out ratio Dividend paid/Net income 59.16% 66.12%

b) Analysing and interpreting the financial performance and position of Chocco plc

For the purpose of determining the financial position and performance of the Chocco

plc, analysing the financial ratio is very useful and a detailed analysis and interpretation is

given below.

Liquidity ratios

Current ratio

The current ratio of the Chocco plc is 0.92 times which has increased from 0.77

times in the year 2018. But then too this is very low therefore company requires to implement

actions which will help in increasing its current assets and in reducing its current obligations

as well (Hantono, 2018). The current ratio of the company should be more than 1 which will

help in ensuring that the company can easily meet with its current obligations in an effective

way without any requirement to

Quick Ratio

The quick ratio is very low which indicates that the company has invested most of

its cash in its inventory which has resulted into reduction in quick assets as inventory is

excluded from the list (Ravichandran and Subramanian, 2016). Therefore, relevant steps are

required to be undertaken which will help in decreasing the contribution of the inventory in

its current assets. This will result into effectively managing the short-term liquidity position

of the company.

Profitability ratios

Return on capital employed

The ROCE of the company has increased in the year 2019 to 11.14% from the

9.93% which is a good indicator of growth. This rise in ratio conveys that the company is

effectively making use of the capital employed in generating income. Along with that, the

outcomes will attract more investors for the purpose of investment (Ningsih, 2020). This ratio

presents the long-term profitability of the company in terms of how well the assets of the

company is performing.

Return on Equity

The ROE of the company has shown an upward trend as it has increased to 13.96%

in contrast to 12.57% in the year 2018. Higher and growing ratio is more favourable from the

investor’s point of view (Mahdaleta, Muda and Nasir, 2016). This ratio depicts the efficiency

and effectiveness of the company in making use of the investor’s funds. Therefore, this

increase in percentage makes it favourable for the company.

Gross Profit Margin

The GP margin ratio of Chocco plc has not shown a major change which is because

of the reason that there is not such variation in the sales volume in comparison to its cost of

sales, which has resulted into similar ratio. In order to improve it further, it advisable for the

company to implement strategies which will help in reducing the cost of sales and along with

increasing revenue of the business.

Net Profit ratio

The NP margin of the company has risen to 6.40% in 2019 which means that the

company is working effectively which has resulted into the increase in the ratio (Behera and

Das, 2019). This rise is because of the increase in the revenue of the company along with its

net profit. Therefore, company should work in the similar and make efforts in further

reducing its operating and non-operating expenses gaining higher NP.

Efficiency ratios

Asset turnover ratio

The ATR of Chocco plc is reduced which means that company is lacking behind in

terms of effectively making use of its assets in generating greater revenue. Therefore, it

becomes important for the firm to impose new strategies which will help in analysing the

reason behind the fall in the ATR (Farooq, 2019). Along with that efforts are required to

implemented for ensuring optimum utilization of resources.

Inventory turnover ratio

The ITR of the company has declined which means that the company is facing

problem in respect to selling its goods. It is desirable to have higher ratio and in case of lower

ratio it depicts that the company overspend through the way of purchasing too much stock of

goods and is wasting its resources by storing the non-saleable stock items. This highlights

that company is not effective in quickly selling its inventory.

Account receivable turnover ratio

company is performing.

Return on Equity

The ROE of the company has shown an upward trend as it has increased to 13.96%

in contrast to 12.57% in the year 2018. Higher and growing ratio is more favourable from the

investor’s point of view (Mahdaleta, Muda and Nasir, 2016). This ratio depicts the efficiency

and effectiveness of the company in making use of the investor’s funds. Therefore, this

increase in percentage makes it favourable for the company.

Gross Profit Margin

The GP margin ratio of Chocco plc has not shown a major change which is because

of the reason that there is not such variation in the sales volume in comparison to its cost of

sales, which has resulted into similar ratio. In order to improve it further, it advisable for the

company to implement strategies which will help in reducing the cost of sales and along with

increasing revenue of the business.

Net Profit ratio

The NP margin of the company has risen to 6.40% in 2019 which means that the

company is working effectively which has resulted into the increase in the ratio (Behera and

Das, 2019). This rise is because of the increase in the revenue of the company along with its

net profit. Therefore, company should work in the similar and make efforts in further

reducing its operating and non-operating expenses gaining higher NP.

Efficiency ratios

Asset turnover ratio

The ATR of Chocco plc is reduced which means that company is lacking behind in

terms of effectively making use of its assets in generating greater revenue. Therefore, it

becomes important for the firm to impose new strategies which will help in analysing the

reason behind the fall in the ATR (Farooq, 2019). Along with that efforts are required to

implemented for ensuring optimum utilization of resources.

Inventory turnover ratio

The ITR of the company has declined which means that the company is facing

problem in respect to selling its goods. It is desirable to have higher ratio and in case of lower

ratio it depicts that the company overspend through the way of purchasing too much stock of

goods and is wasting its resources by storing the non-saleable stock items. This highlights

that company is not effective in quickly selling its inventory.

Account receivable turnover ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This ratio is important in measuring the efficiency of the entity in terms of how

many times it is able to convert its accounts receivables in cash. Higher the ratio better it is

for the company. This ratio of the company has shown an increase which is very minor as it

has increased to 5.39 times in contrast to the 5 times in 2018 (Umniati, Titisari and

Chomsatu, 2019). This depicts that the company is effective in collecting the due amount

from its account receivables 5.39 times in a year. From the cash flow point of view, the

company is able to collect the amount sooner which can be used making payment of the

obligations.

Accounts Payable Turnover Ratio

This ratio of the Chocco plc has increased which is favourable for the company. This

means that the company can make payment to its creditors 5.55 times in a year which helps in

building trust among the supplier’s and the vendors. The difference between the a/c

receivable and a/c payable turnover ratio is not much, therefore, the company requires to

implement strategy which will result into increasing its a/c payable turnover ratio so that after

receiving cash from its debtors it a make payment to its creditors efficiently without any need

for additional funds to be borrowed.

Leverage ratios

Proprietary Ratio

This ratio highlights the proportion of the shareholder’s equity in against the total

assets of the company. This ratio has shown an upward trend which is favourable for the

company as it highlights that the entity is making more use of the equity funds instead of debt

in the business dealings. The percentage has increased to 31.72% from 28.87% and is

therefore having additional space for the taking the debt in case of requirement

(BRÎNDESCU–OLARIU, 2016). Along with that, there is a decline in the total assets of the

company and an increase in the equity funds which has resulted into higher ratio. It is

important to note that the debt component has also increased in 2019 therefore, the good

percentage is due to the reduction the total assets.

Debt equity ratio

The debt equity ratio helps in determining the composition of the debt and equity in

the capital structure of the company. It is desirable to have the ratio of 1 but in case of

Chocco plc the ratio is 1.34 which has reduced in comparison to the previous year but is not

very low. This depicts that the entity is having more debt as compared to its equity which

incur risk for the entity therefore, measures are required to be undertaken which will help in

attaining the desired ratio.

many times it is able to convert its accounts receivables in cash. Higher the ratio better it is

for the company. This ratio of the company has shown an increase which is very minor as it

has increased to 5.39 times in contrast to the 5 times in 2018 (Umniati, Titisari and

Chomsatu, 2019). This depicts that the company is effective in collecting the due amount

from its account receivables 5.39 times in a year. From the cash flow point of view, the

company is able to collect the amount sooner which can be used making payment of the

obligations.

Accounts Payable Turnover Ratio

This ratio of the Chocco plc has increased which is favourable for the company. This

means that the company can make payment to its creditors 5.55 times in a year which helps in

building trust among the supplier’s and the vendors. The difference between the a/c

receivable and a/c payable turnover ratio is not much, therefore, the company requires to

implement strategy which will result into increasing its a/c payable turnover ratio so that after

receiving cash from its debtors it a make payment to its creditors efficiently without any need

for additional funds to be borrowed.

Leverage ratios

Proprietary Ratio

This ratio highlights the proportion of the shareholder’s equity in against the total

assets of the company. This ratio has shown an upward trend which is favourable for the

company as it highlights that the entity is making more use of the equity funds instead of debt

in the business dealings. The percentage has increased to 31.72% from 28.87% and is

therefore having additional space for the taking the debt in case of requirement

(BRÎNDESCU–OLARIU, 2016). Along with that, there is a decline in the total assets of the

company and an increase in the equity funds which has resulted into higher ratio. It is

important to note that the debt component has also increased in 2019 therefore, the good

percentage is due to the reduction the total assets.

Debt equity ratio

The debt equity ratio helps in determining the composition of the debt and equity in

the capital structure of the company. It is desirable to have the ratio of 1 but in case of

Chocco plc the ratio is 1.34 which has reduced in comparison to the previous year but is not

very low. This depicts that the entity is having more debt as compared to its equity which

incur risk for the entity therefore, measures are required to be undertaken which will help in

attaining the desired ratio.

Market value ratios

Price earnings ratio

The PER of Chocco plc has shown an increase in trend which highlights the growing

stocks of the company. Along with it, the ratio is high which depicts the stronger and positive

future performance of the entity and along with the same, the expectations of the investors in

regard to the future earnings will also increase and will be willing to pay more

(Altahtamouni, Matahen and Qazaq, 2020). But on the other hand, it is important to take a

look at the other side as well, which is, growth stocks are higher volatile in the which exerts

huge pressure on the entity to put in more efforts to justify with the higher valuation.

Market to book value ratio

This ratio is the financial metrics which is utilized for the purpose of evaluating the

current value of the stock of the company in contrast to its book value. The ratio has rise to

0.99 from 0.82 in 2018. The ratio lower than 1 indicates that the stock of the company is

undervalued which is considered as the bad investment which could mean that there is soe

thing wrong with the entity and also depicts that the company will be paying much more than

what will be left after entity goes bankrupt. The ratio grater than 1 refers to the overvaluation

of the stock conveying that the organization is performing well. The 0.99 is approximately 1,

thus, Chocco plc should implement the methods which will help in attaining the ratio of

greater than 1. Therefore, the stock value of the company is good or accurate.

Dividend pay-out ratio

The DPR of the company has declined in respect to its previous year which

highlights that the entity is reinvesting its earning into the projects which results into further

expansion of the business. Through, this company will be able to attain high growth

objectives which will consequently result into earning high level of capital gains for the

investors (Subburaj, 2019). Therefore, Chocco plc is in the position to attract more investors

who are more keen on earning higher potential profits from a significant increase in the share

price of the company and least interest in the income generated through dividend. This is

useful in determining what type of return the company is offering to the investors.

Thus, based on the ratio analysis of the financial statements of the Chocco plc, it can

be stated that the company is currently having a good financial position and performing very

well and sound. The most important things that the company requires to work upon is on

improving its short term liquidity position along needs to increase the number of time in a

year it collect due amount from its debtors as it is very low. In terms of solvency ratio, the

company needs to put more efforts in respect to reducing the amount of debt component in its

Price earnings ratio

The PER of Chocco plc has shown an increase in trend which highlights the growing

stocks of the company. Along with it, the ratio is high which depicts the stronger and positive

future performance of the entity and along with the same, the expectations of the investors in

regard to the future earnings will also increase and will be willing to pay more

(Altahtamouni, Matahen and Qazaq, 2020). But on the other hand, it is important to take a

look at the other side as well, which is, growth stocks are higher volatile in the which exerts

huge pressure on the entity to put in more efforts to justify with the higher valuation.

Market to book value ratio

This ratio is the financial metrics which is utilized for the purpose of evaluating the

current value of the stock of the company in contrast to its book value. The ratio has rise to

0.99 from 0.82 in 2018. The ratio lower than 1 indicates that the stock of the company is

undervalued which is considered as the bad investment which could mean that there is soe

thing wrong with the entity and also depicts that the company will be paying much more than

what will be left after entity goes bankrupt. The ratio grater than 1 refers to the overvaluation

of the stock conveying that the organization is performing well. The 0.99 is approximately 1,

thus, Chocco plc should implement the methods which will help in attaining the ratio of

greater than 1. Therefore, the stock value of the company is good or accurate.

Dividend pay-out ratio

The DPR of the company has declined in respect to its previous year which

highlights that the entity is reinvesting its earning into the projects which results into further

expansion of the business. Through, this company will be able to attain high growth

objectives which will consequently result into earning high level of capital gains for the

investors (Subburaj, 2019). Therefore, Chocco plc is in the position to attract more investors

who are more keen on earning higher potential profits from a significant increase in the share

price of the company and least interest in the income generated through dividend. This is

useful in determining what type of return the company is offering to the investors.

Thus, based on the ratio analysis of the financial statements of the Chocco plc, it can

be stated that the company is currently having a good financial position and performing very

well and sound. The most important things that the company requires to work upon is on

improving its short term liquidity position along needs to increase the number of time in a

year it collect due amount from its debtors as it is very low. In terms of solvency ratio, the

company needs to put more efforts in respect to reducing the amount of debt component in its

capital structure which will help in further reducing the financial burden borne by the

company.

company.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

Altahtamouni, F., Matahen, R. and Qazaq, A., 2020. The Mediating Role of the Capital

Structure, Growth Rate, and Dividend Policy in the Relationship Between Return on

Equity and Market to Book Value. International Journal of Financial

Research. 11(4).

Behera, B. and Das, A., 2019. Management Efficiency and Profitability: A Case Study of

Petrochemical Industry. Splint International Journal of Professionals. 6(3). pp.7-15.

BRÎNDESCU–OLARIU, D., 2016. Solvency ratio as a tool for bankruptcy

prediction. Ecoforum Journal. 5(2).

Daniel, A. C., Marioara, A. and Isabela, D., 2017. Annual Financial Statements as a Financial

Communication Support. Ovidius University Annals, Economic Sciences

Series. 17(1). pp.403-406.

Farooq, U., 2019. Impact of inventory turnover on the profitability of non-financial sector

firms in Pakistan. Journal of Finance and Accounting Research. 1(1). pp.34-51.

Hantono, H., 2018. The Effect of Current Ratio, Debt to Equity Ratio, Toward Return on

Assets (Case Study on Consumer Goods Company). ACCOUNTABILITY. 7(02).

pp.64-73.

Mahdaleta, E., Muda, I. and Nasir, G. M., 2016. Effects of capital structure and profitability

on corporate value with company size as the moderating variable of manufacturing

companies listed on Indonesia Stock Exchange. Academic Journal of Economic

Studies. 2(3). pp.30-43.

Ningsih, M., 2020. Liquidity and Profitability Ratio Analysis for Measuring The Financial

Performance of PT. Bank Bri Syariah 2012-2019 Period. Journal of Research in

Business, Economics, and Education. 2(4). pp.895-907.

Ravichandran, M. and Subramanian, M. V., 2016. A Study on Financial Performance

Analysis of Force Motors Limited. International Journal for Innovative Research in

Science & Technology. 2(11). pp.662-666.

Subburaj, L., 2019. IMPACT OF ACCOUNTING RATIO ANALYSIS IN MAKING OF

MEANINGFUL BUSINESS DECISIONS. INNOVATIONS IN BUSINESS AND

MANAGEMENT. p.193.

Umniati, R., Titisari, K. H. and Chomsatu, Y., 2019. The Influence of Current Ratio,

Inventory Turnover Ratio, Cash Turnover and Debt To Equity Ratio Against The

Return on Investment in The Production of Industrial Companies Listed on The

Stock Exchange of Malaysia in 2016. Benefit: Jurnal Manajemen dan Bisnis. 3(1).

pp.23-30.

Books and Journals

Altahtamouni, F., Matahen, R. and Qazaq, A., 2020. The Mediating Role of the Capital

Structure, Growth Rate, and Dividend Policy in the Relationship Between Return on

Equity and Market to Book Value. International Journal of Financial

Research. 11(4).

Behera, B. and Das, A., 2019. Management Efficiency and Profitability: A Case Study of

Petrochemical Industry. Splint International Journal of Professionals. 6(3). pp.7-15.

BRÎNDESCU–OLARIU, D., 2016. Solvency ratio as a tool for bankruptcy

prediction. Ecoforum Journal. 5(2).

Daniel, A. C., Marioara, A. and Isabela, D., 2017. Annual Financial Statements as a Financial

Communication Support. Ovidius University Annals, Economic Sciences

Series. 17(1). pp.403-406.

Farooq, U., 2019. Impact of inventory turnover on the profitability of non-financial sector

firms in Pakistan. Journal of Finance and Accounting Research. 1(1). pp.34-51.

Hantono, H., 2018. The Effect of Current Ratio, Debt to Equity Ratio, Toward Return on

Assets (Case Study on Consumer Goods Company). ACCOUNTABILITY. 7(02).

pp.64-73.

Mahdaleta, E., Muda, I. and Nasir, G. M., 2016. Effects of capital structure and profitability

on corporate value with company size as the moderating variable of manufacturing

companies listed on Indonesia Stock Exchange. Academic Journal of Economic

Studies. 2(3). pp.30-43.

Ningsih, M., 2020. Liquidity and Profitability Ratio Analysis for Measuring The Financial

Performance of PT. Bank Bri Syariah 2012-2019 Period. Journal of Research in

Business, Economics, and Education. 2(4). pp.895-907.

Ravichandran, M. and Subramanian, M. V., 2016. A Study on Financial Performance

Analysis of Force Motors Limited. International Journal for Innovative Research in

Science & Technology. 2(11). pp.662-666.

Subburaj, L., 2019. IMPACT OF ACCOUNTING RATIO ANALYSIS IN MAKING OF

MEANINGFUL BUSINESS DECISIONS. INNOVATIONS IN BUSINESS AND

MANAGEMENT. p.193.

Umniati, R., Titisari, K. H. and Chomsatu, Y., 2019. The Influence of Current Ratio,

Inventory Turnover Ratio, Cash Turnover and Debt To Equity Ratio Against The

Return on Investment in The Production of Industrial Companies Listed on The

Stock Exchange of Malaysia in 2016. Benefit: Jurnal Manajemen dan Bisnis. 3(1).

pp.23-30.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.