University Accounting Assignment: Financial Statement Analysis, 2024

VerifiedAdded on 2022/12/27

|18

|3081

|2

Homework Assignment

AI Summary

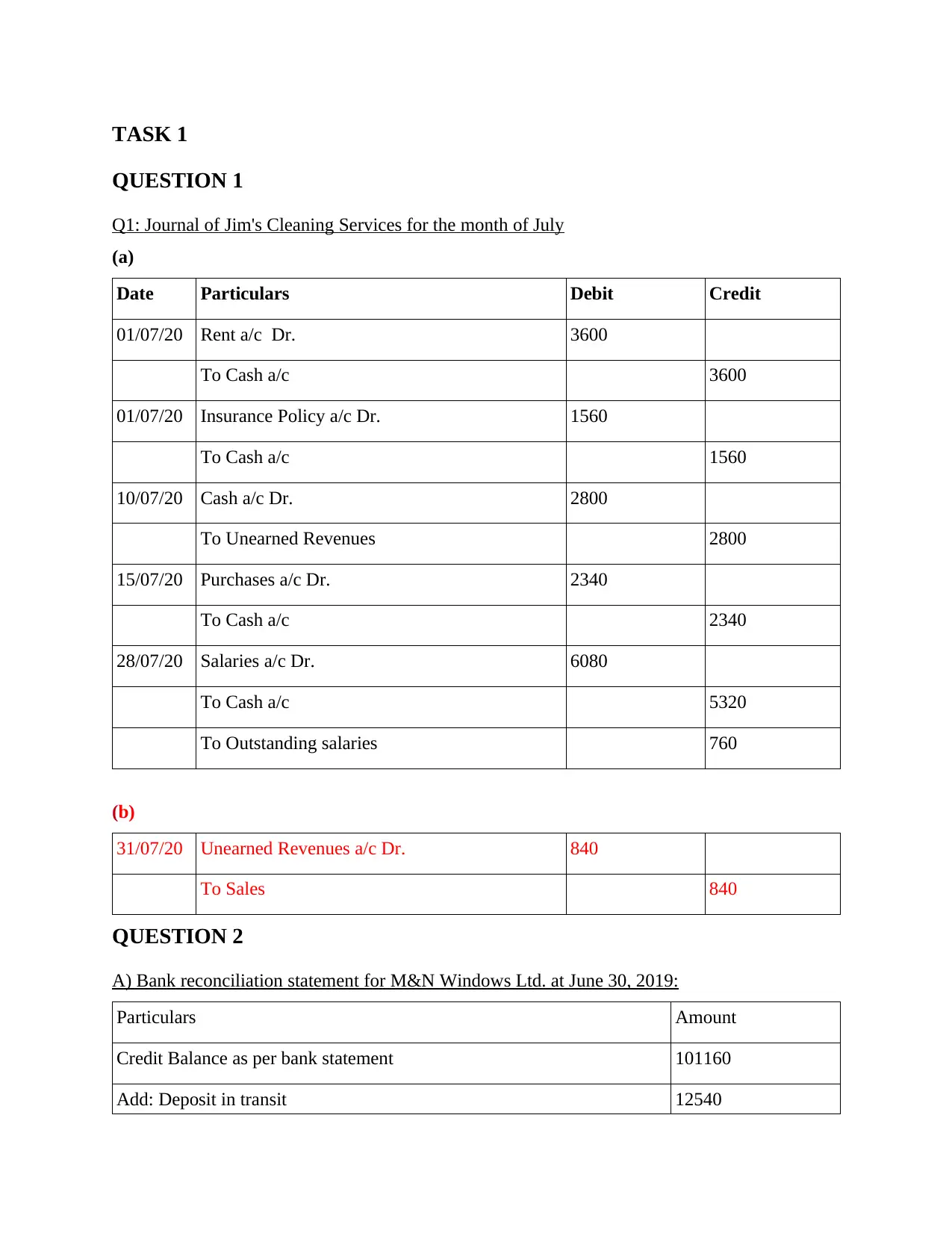

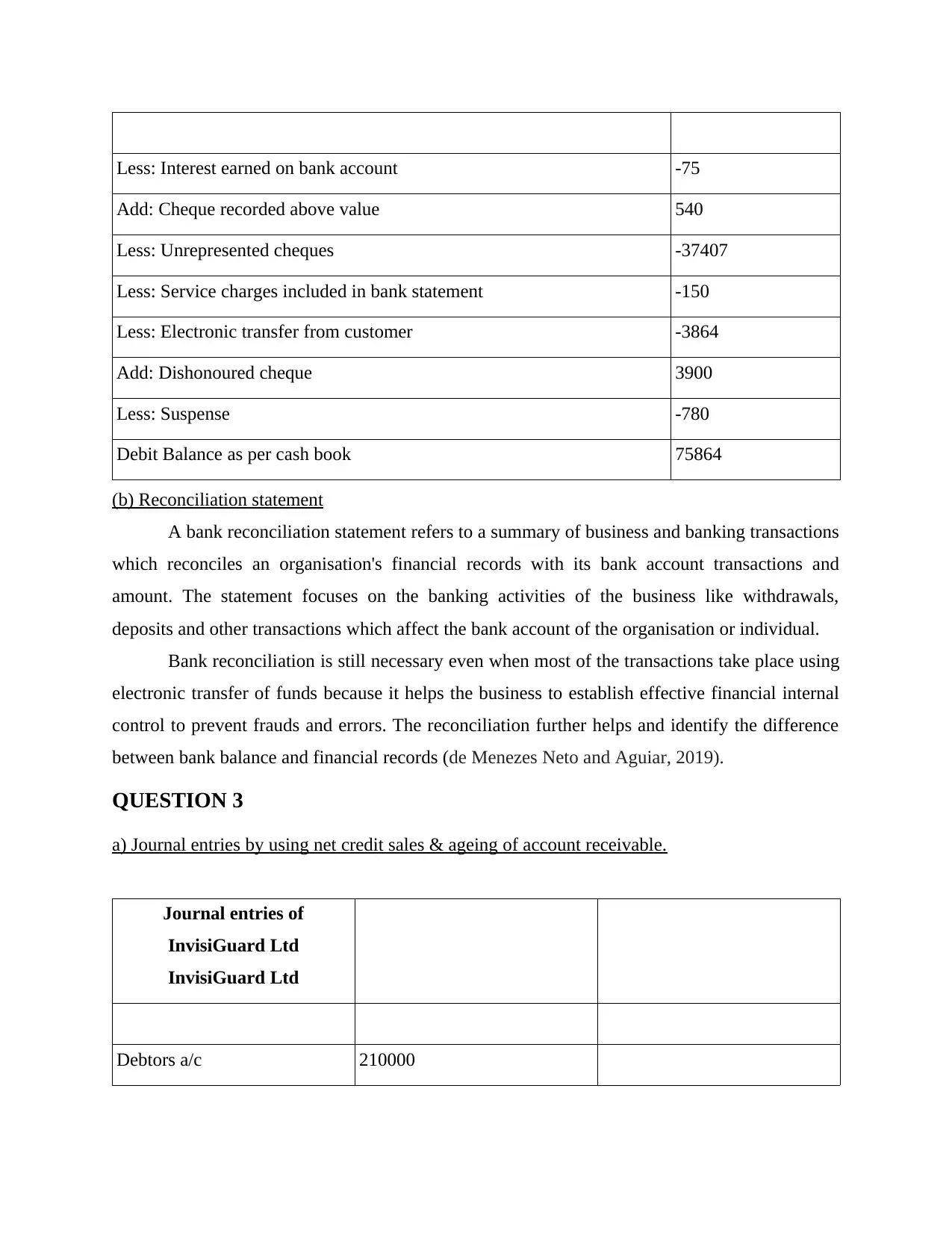

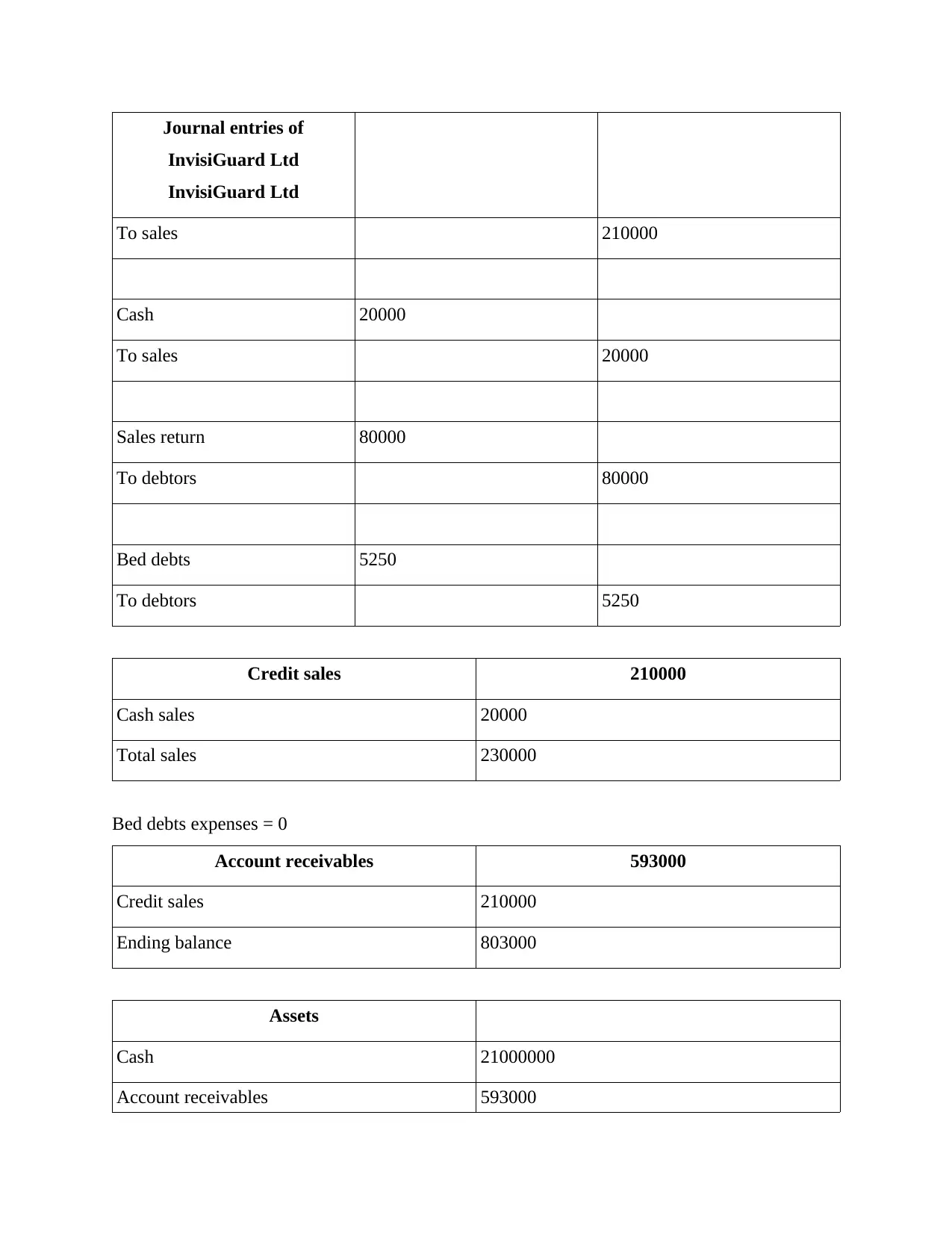

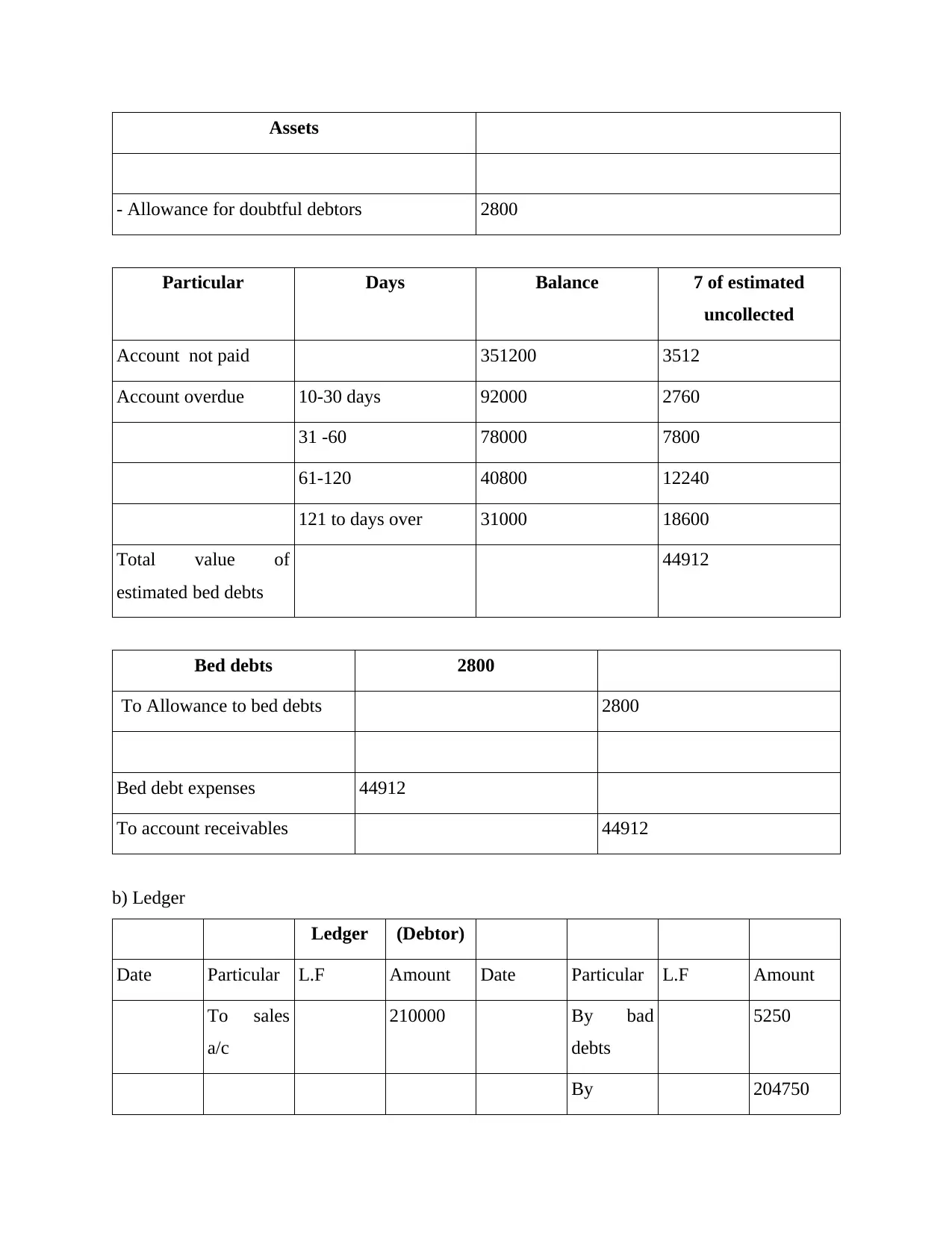

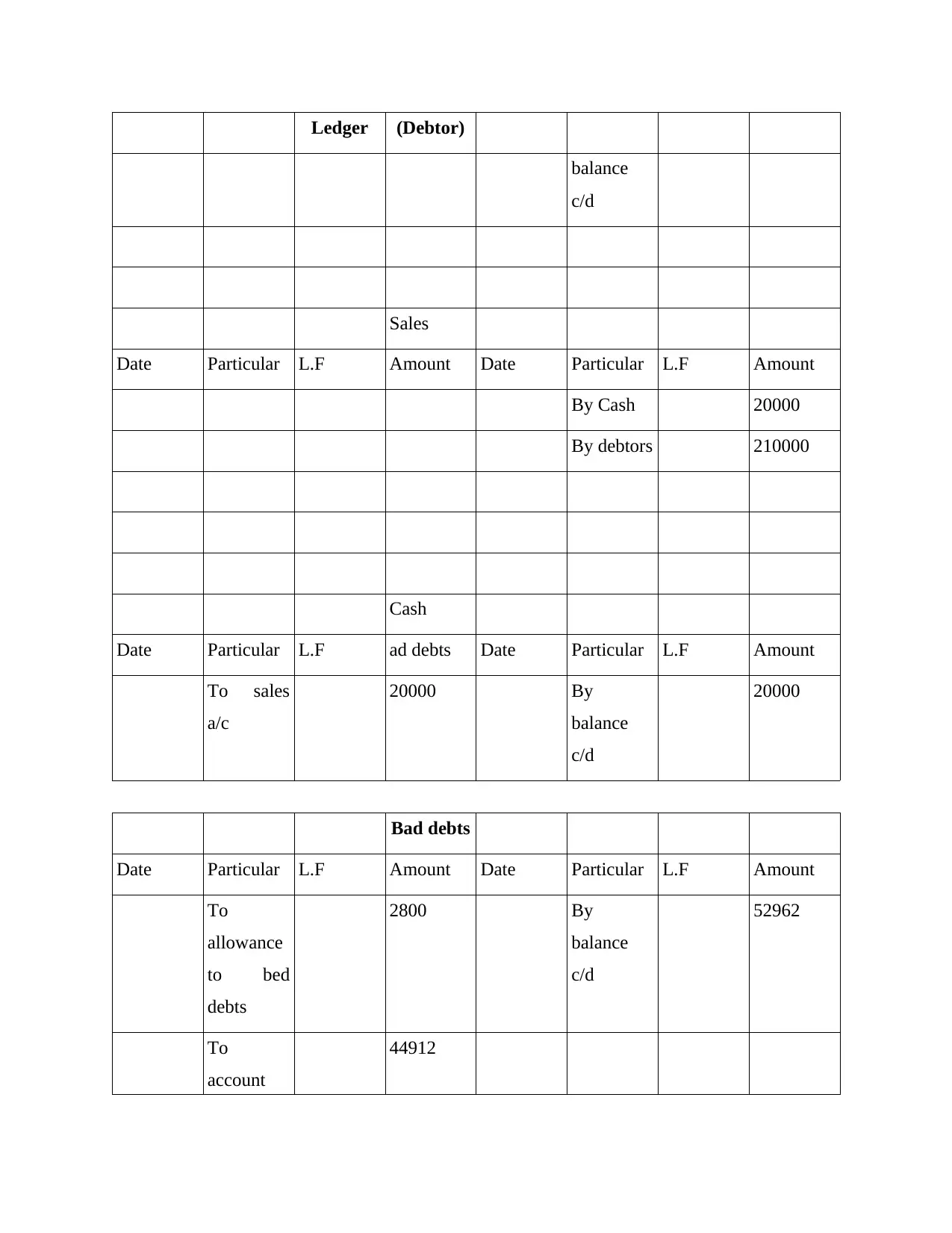

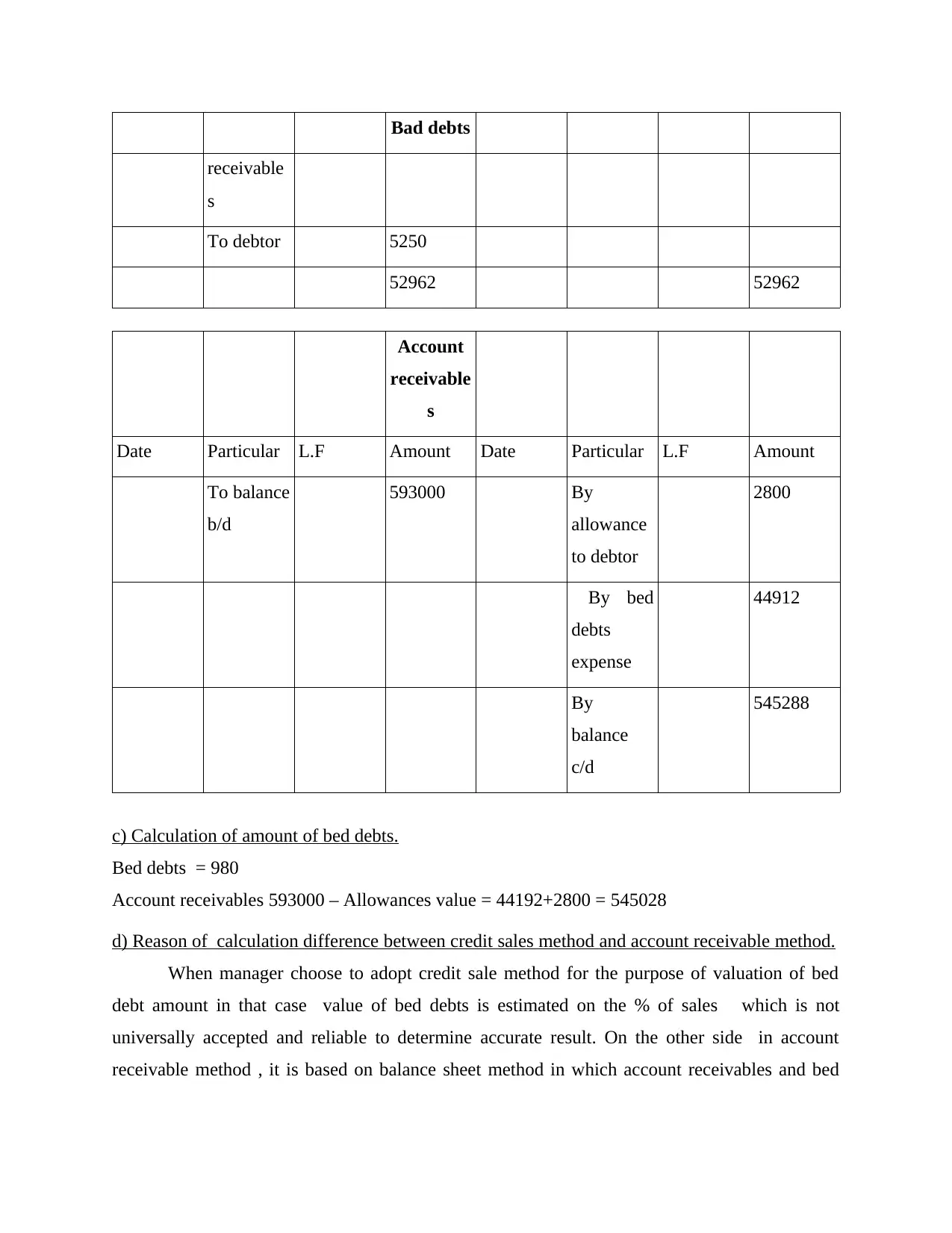

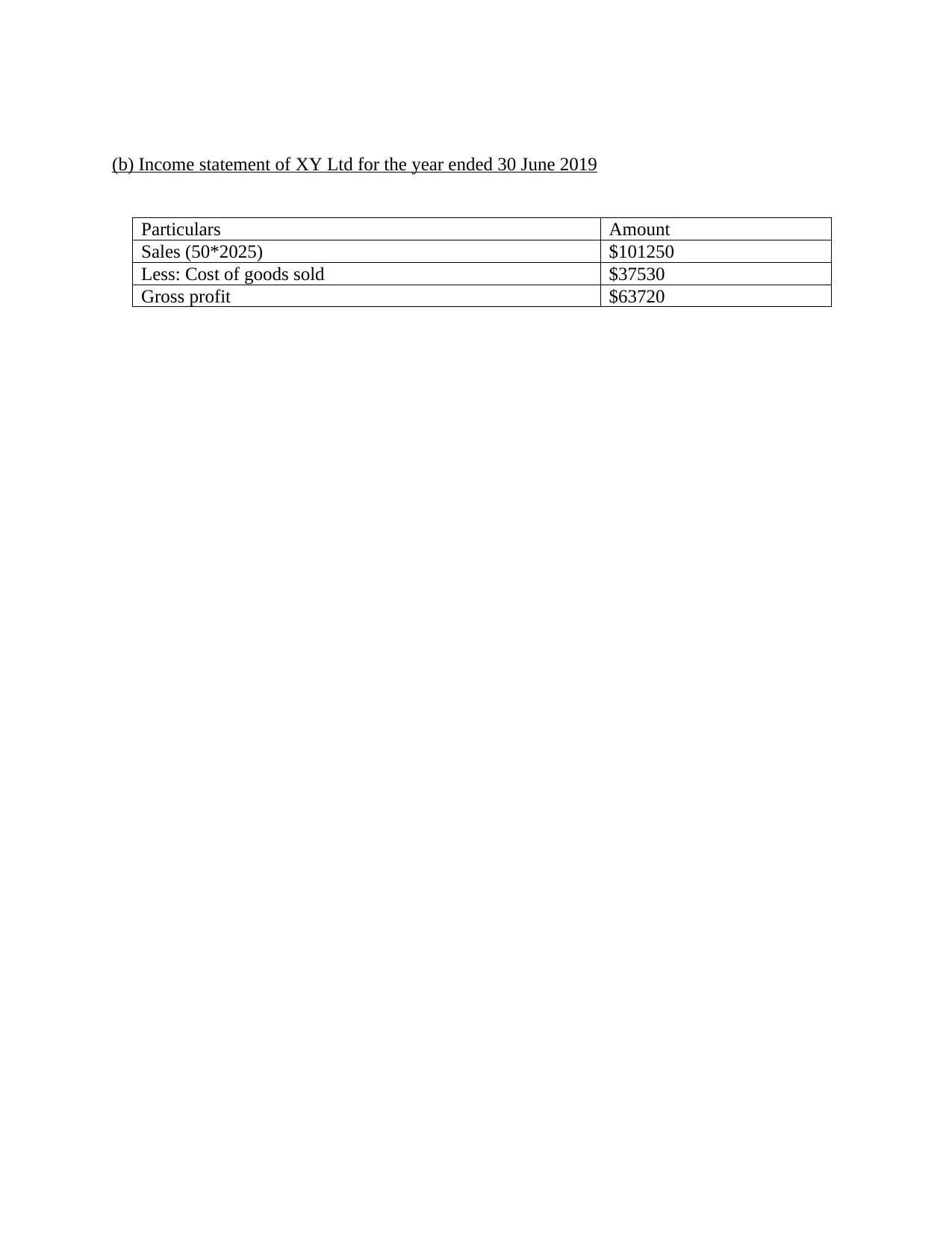

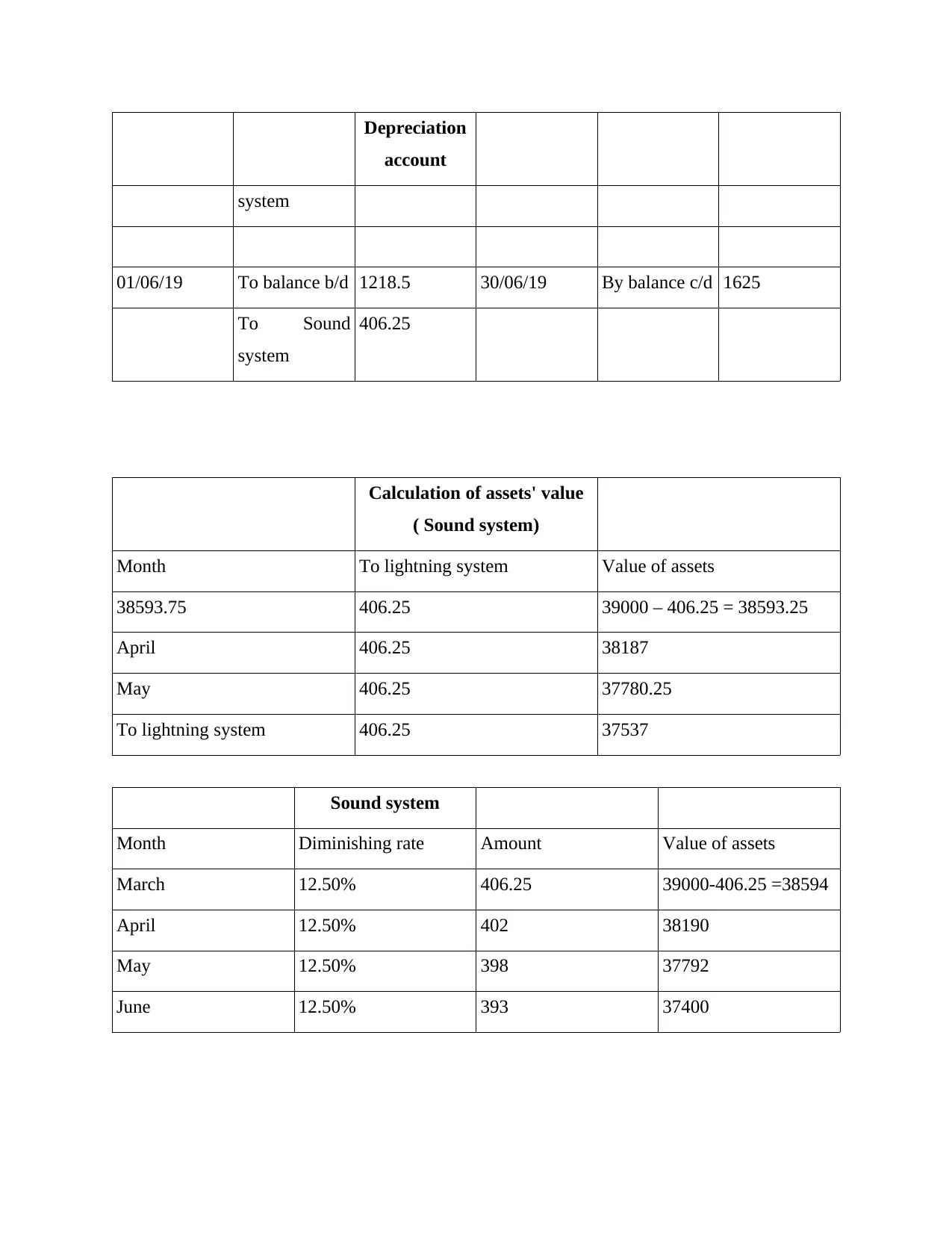

This document presents a comprehensive solution to an accounting assignment, covering a wide array of financial accounting concepts. The solution begins with journal entries for Jim's Cleaning Services, illustrating the recording of various transactions. It then provides a bank reconciliation statement for M&N Windows Ltd., clarifying the process of reconciling bank and business records. The assignment further delves into accounting for receivables, including journal entries for bad debts and the aging of accounts receivable. The solution then addresses inventory costing methods, specifically FIFO, to determine ending inventory and cost of goods sold, along with an income statement for XY Ltd. Depreciation methods, including straight-line and diminishing balance, are explored to calculate asset values. Finally, the assignment discusses liabilities, categorizing them into current, non-current, and contingent liabilities, providing examples and explanations for each type. The assignment helps students to understand and apply key accounting principles to real-world financial scenarios.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.