Financial Accounting Report: Healius Healthcare, AASB 16, and Concepts

VerifiedAdded on 2022/11/09

|14

|2909

|184

Report

AI Summary

This report provides a comprehensive analysis of Healius Healthcare's financial accounting practices, focusing on the application of key accounting concepts and the adoption of AASB 16. The report begins with an overview of essential accounting concepts such as the going concern, accrual, consistency, materiality, and conservatism principles, illustrating their application within Healius's financial statements. The core of the analysis centers on AASB 16, detailing the changes introduced by the new lease standard, the classification of leases, and the impact of these changes on Healius's financial reporting, including the recognition of lease liabilities and right-of-use assets. The report contrasts AASB 16 with its predecessor, AASB 117, highlighting the transitional provisions and the effects of the transition on the company's financial position, objectives, and cash flows. Furthermore, it examines the key disclosures made by Healius regarding its accounting for leases, providing specific examples from the company's financial reports to illustrate the practical implications of the new standard. The report concludes by summarizing the overall impact of AASB 16 on Healius Healthcare and its financial reporting practices.

Running head: ACCOUNTING

Accounting

Name of the Student

Name of the University

Author Note

Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTS

Table of Contents

Introduction......................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Accounting Concepts...................................................................................................................2

AASB 16......................................................................................................................................4

Application of AASB 16 from AASB 117..................................................................................6

Conclusion.......................................................................................................................................9

References..................................................................................................................................10

Appendix....................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................2

Discussion and Analysis..................................................................................................................2

Accounting Concepts...................................................................................................................2

AASB 16......................................................................................................................................4

Application of AASB 16 from AASB 117..................................................................................6

Conclusion.......................................................................................................................................9

References..................................................................................................................................10

Appendix....................................................................................................................................12

2ACCOUNTS

Introduction

Accounting concepts and principles are the key basis upon which the financial statement

of a company is prepared. The company that has been taken into consideration for the purpose of

analysis is the Healius Healthcare Company that has been considered. The important accounting

concepts that has been used by the company wile preparing the financial statement of the

company has been well outlined and presented in the financial statement of the company. The

application of the AASB 16 that comes into effect from the 1st January, 2019 has been well taken

into consideration. The application of AASB 16 and the effect of the implication of the same on

the financial statement of the company will be taken into analysis of the report. AASB 117 will

be scrapped in the year 2018. The primary purpose of this accounting standard was to provide

the users of the financial statements with information about the impact of the company’s lease

agreements on financial position, objectives and the cash flows of the organisation for a

particular year. The application of the same will be done by all the companies for the purpose of

reporting and classifying all the lease transactions carried on by the company.

Discussion and Analysis

Accounting Concepts

Like many of the corporate entities conducting business in the modern day business

environment, Healius also prepares its annual financial statements using different accounting

concepts. The primary of them is the going concern concept. This concept suggests that every

business conducts its business with the intention to carry on with it for the foreseeable future and

not shut it down at the earliest available opportunity (Enofe et al. 2013). As suggested by the

2019 annual reports of the organisation, the directors analyse the ability of the entity in

Introduction

Accounting concepts and principles are the key basis upon which the financial statement

of a company is prepared. The company that has been taken into consideration for the purpose of

analysis is the Healius Healthcare Company that has been considered. The important accounting

concepts that has been used by the company wile preparing the financial statement of the

company has been well outlined and presented in the financial statement of the company. The

application of the AASB 16 that comes into effect from the 1st January, 2019 has been well taken

into consideration. The application of AASB 16 and the effect of the implication of the same on

the financial statement of the company will be taken into analysis of the report. AASB 117 will

be scrapped in the year 2018. The primary purpose of this accounting standard was to provide

the users of the financial statements with information about the impact of the company’s lease

agreements on financial position, objectives and the cash flows of the organisation for a

particular year. The application of the same will be done by all the companies for the purpose of

reporting and classifying all the lease transactions carried on by the company.

Discussion and Analysis

Accounting Concepts

Like many of the corporate entities conducting business in the modern day business

environment, Healius also prepares its annual financial statements using different accounting

concepts. The primary of them is the going concern concept. This concept suggests that every

business conducts its business with the intention to carry on with it for the foreseeable future and

not shut it down at the earliest available opportunity (Enofe et al. 2013). As suggested by the

2019 annual reports of the organisation, the directors analyse the ability of the entity in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTS

continuing as a going concern at the time of preparing the financial statements (Healius.com.au

2019). As it has not been suggested that the company plans to liquidate or wind itself up in the

near future, the statements suggest that Healius is a going concern that will conduct its business

for the foreseeable future. Another important concept which has been used by Healius in its

financial statements is the accrual concept. This concept states that any revenues or

expenditures or related obligations are to be recognised in the books of accounts as and when

they occur. It means that an expenditure already incurred in the current year should be

recognised in this year itself and not when the payment related to the expenditure is made by the

business. In its financial statements, Healius has recorded various items like current and non-

current trade payables and accruals. Although the payment for them would not be made in 2019

itself, they have been included the financial statements due to their existing obligation in the

current year. This improves the reliability of the financial statements (Azmi and Mohamed

2014).The next relevant concept that has been used is the consistency concept. This suggests that

an accounting concept that has been adopted in a particular year should be followed in the future

accounting periods as well. This is to ensure that the financial results obtained in different years

are due to the same underlying assumptions and principles that were followed (Peterson,

Schmardebeck and Wilks 2015). Any change in the accounting methods used in the treatment of

any particular item should be stated in the financial statements. The consistency concept is also

related to the recommendations and suggestions of the governing body guiding the preparation of

the financial statements. Particular items like leases, assets and contingencies should be recorded

in a manner that is consistent with the suggestions of the AASB. Otherwise, they would lead to

the company being penalised for not following accepted guidelines in preparing the financial

statements (Healius.com.au 2019). The materiality concept has also been used appropriately by

continuing as a going concern at the time of preparing the financial statements (Healius.com.au

2019). As it has not been suggested that the company plans to liquidate or wind itself up in the

near future, the statements suggest that Healius is a going concern that will conduct its business

for the foreseeable future. Another important concept which has been used by Healius in its

financial statements is the accrual concept. This concept states that any revenues or

expenditures or related obligations are to be recognised in the books of accounts as and when

they occur. It means that an expenditure already incurred in the current year should be

recognised in this year itself and not when the payment related to the expenditure is made by the

business. In its financial statements, Healius has recorded various items like current and non-

current trade payables and accruals. Although the payment for them would not be made in 2019

itself, they have been included the financial statements due to their existing obligation in the

current year. This improves the reliability of the financial statements (Azmi and Mohamed

2014).The next relevant concept that has been used is the consistency concept. This suggests that

an accounting concept that has been adopted in a particular year should be followed in the future

accounting periods as well. This is to ensure that the financial results obtained in different years

are due to the same underlying assumptions and principles that were followed (Peterson,

Schmardebeck and Wilks 2015). Any change in the accounting methods used in the treatment of

any particular item should be stated in the financial statements. The consistency concept is also

related to the recommendations and suggestions of the governing body guiding the preparation of

the financial statements. Particular items like leases, assets and contingencies should be recorded

in a manner that is consistent with the suggestions of the AASB. Otherwise, they would lead to

the company being penalised for not following accepted guidelines in preparing the financial

statements (Healius.com.au 2019). The materiality concept has also been used appropriately by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTS

the entity in preparing its financial statements. This concept suggests that items that are

presented in the financial statements should be recorded in a manner that is a proper reflection of

the impact that they have would have on the entity as a whole (Eilifsen and Messier Jr 2014).

This is the reason why the purchase of a minor office item like a pen is treated as a petty expense

and not as the purchase of an asset to be used in the business. In case of Healius, the materiality

concept has been appropriately applied in the identification of the appropriate assets and

classifying them on the basis of the impact that they are likely to have on the organisation as a

whole. Every specific asset has not been mentioned while the changes in the fair values of the

prominent assets have been stated appropriately (Healius.com.au 2019). Irrelevant assets have

been omitted from the financial statements to the highest possible extent. The conservatism

concept has also been applied by Healius in preparing its financial statements. This concept

suggests that as soon as the entity has knowledge about the non-accrual or non-realisation of an

asset, it should immediately mention the same in the financial statements or stop recording that

particular item in its books of accounts (Mora and Walker 2015). This is to ensure that the

information provided by the financial statements is a representation of the true and fair view of

the financial position of the firm. Due to this concept, Healius has made a separate mention of

the contingent liabilities separately in the financial statements and classified them as work

related or property related payments. This informs the shareholders that the liabilities may or

may not be received at the future date.

AASB 16

A lease is an agreement in which a company or an individual, known as the lessee,

obtains the right to use an asset for a specific period of time and makes lease payments in

exchange for the same. The AASB 16 has been the guiding accounting standard in relation to the

the entity in preparing its financial statements. This concept suggests that items that are

presented in the financial statements should be recorded in a manner that is a proper reflection of

the impact that they have would have on the entity as a whole (Eilifsen and Messier Jr 2014).

This is the reason why the purchase of a minor office item like a pen is treated as a petty expense

and not as the purchase of an asset to be used in the business. In case of Healius, the materiality

concept has been appropriately applied in the identification of the appropriate assets and

classifying them on the basis of the impact that they are likely to have on the organisation as a

whole. Every specific asset has not been mentioned while the changes in the fair values of the

prominent assets have been stated appropriately (Healius.com.au 2019). Irrelevant assets have

been omitted from the financial statements to the highest possible extent. The conservatism

concept has also been applied by Healius in preparing its financial statements. This concept

suggests that as soon as the entity has knowledge about the non-accrual or non-realisation of an

asset, it should immediately mention the same in the financial statements or stop recording that

particular item in its books of accounts (Mora and Walker 2015). This is to ensure that the

information provided by the financial statements is a representation of the true and fair view of

the financial position of the firm. Due to this concept, Healius has made a separate mention of

the contingent liabilities separately in the financial statements and classified them as work

related or property related payments. This informs the shareholders that the liabilities may or

may not be received at the future date.

AASB 16

A lease is an agreement in which a company or an individual, known as the lessee,

obtains the right to use an asset for a specific period of time and makes lease payments in

exchange for the same. The AASB 16 has been the guiding accounting standard in relation to the

5ACCOUNTS

recognition, measurement, disclosure and presentation of leases and their related agreements

entered into by a company in a particular financial year. The primary purpose of this accounting

standard was to provide the users of the financial statements with information about the impact

of the company’s lease agreements on financial position, objectives and the cash flows of the

organisation for a particular year. The accounting aspects that are related to the leases were

guided by the Accounting Standard AASB 117. Previously, the provisions of AASB 16

suggested that the leases related to some of the assets like property and equipment were to be

recognised as off-balance sheet items. This meant that there was no mention of these particular

leases in the balance sheets of an entity. Leases were classified as either operating or financial

leases on the basis of their nature (Ifrs.org. 2019). This nature was determined using a complex

set of rules. The new amendments made to this standard have been in effect from 1 January

2019. As per the latest amendments, the entities should recognise all of their assets and liabilities

in the balance sheet (Aasb.gov.au. 2019). This makes sure that the along with the value of the

leases, the books of accounts reflect the right to use a particular asset by the company. The

classification of the leases of a company as either financial leases or operating leases has been

omitted and in its place, most of the lease agreements are capitalised in the balance sheet. This is

done by recognising the lease liability that needs to be paid and the right to use an asset from the

lease, which is stated as an asset in the books of accounts. Paragraph 51 of AASB 16 suggests

that the new amendments that have been made are aimed at helping users in assessing the

position of an entity through the information provided about the leases in the financial

statements, notes to accounts, income statement and the statement of the cash flows of an entity

for a particular year.

recognition, measurement, disclosure and presentation of leases and their related agreements

entered into by a company in a particular financial year. The primary purpose of this accounting

standard was to provide the users of the financial statements with information about the impact

of the company’s lease agreements on financial position, objectives and the cash flows of the

organisation for a particular year. The accounting aspects that are related to the leases were

guided by the Accounting Standard AASB 117. Previously, the provisions of AASB 16

suggested that the leases related to some of the assets like property and equipment were to be

recognised as off-balance sheet items. This meant that there was no mention of these particular

leases in the balance sheets of an entity. Leases were classified as either operating or financial

leases on the basis of their nature (Ifrs.org. 2019). This nature was determined using a complex

set of rules. The new amendments made to this standard have been in effect from 1 January

2019. As per the latest amendments, the entities should recognise all of their assets and liabilities

in the balance sheet (Aasb.gov.au. 2019). This makes sure that the along with the value of the

leases, the books of accounts reflect the right to use a particular asset by the company. The

classification of the leases of a company as either financial leases or operating leases has been

omitted and in its place, most of the lease agreements are capitalised in the balance sheet. This is

done by recognising the lease liability that needs to be paid and the right to use an asset from the

lease, which is stated as an asset in the books of accounts. Paragraph 51 of AASB 16 suggests

that the new amendments that have been made are aimed at helping users in assessing the

position of an entity through the information provided about the leases in the financial

statements, notes to accounts, income statement and the statement of the cash flows of an entity

for a particular year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTS

The changes have been required to be implemented by the organisations who have

entered into a lease agreement in a given financial year for which the financial statements are

being prepared. In case of Healius, the company has stated that the implementation of AASB 16

in preparing the financial statements is expected to increase its underlying NPAT for the

financial year 2020 (Healius.com.au 2019). In the financial reports of 2019, the company has

suggested that it has not adopted the AASB 16 for accounting for leases as it is not required to do

the same. In the notes to the accounts, the company has stated the impact that adopting AASB 16

would have on its future endeavours. It suggests that the changes suggested by the AASB 16

would remove the distinction between most of the lease assets of the company except for leases

that are short term in nature and of those related to assets which are low in terms of value. From

1 July 2019, the company will begin to measure the value of its liabilities on the basis of the

future lease payments that it will be required to pay (Healius.com.au 2019). With regards to the

right-of-use assets approach, the largest valued assets would be calculated on the basis of the

present value of the assets using the discount rates applicable on the date of transition. Any

accumulated depreciation or amortisation on the assets would be removed from the value of the

assets. Due to the adoption of AASB 16, the company estimates that the value of the liabilities

would go up by $1.2 billion and Right-of-use assets would approximately go up by $1.1 billion

(Healius.com.au. 2019). The company expects to recognise this adjusted amount as its net loss in

the financial statements prepared at the end of the year.

Application of AASB 16 from AASB 117

The application of the AASB 16 that comes into effect from the 1st January, 2019 has

been well taken into consideration by the Healius Company. The application of AASB 16 and

the effect of the implication of the same on the financial statement of the company has been well

The changes have been required to be implemented by the organisations who have

entered into a lease agreement in a given financial year for which the financial statements are

being prepared. In case of Healius, the company has stated that the implementation of AASB 16

in preparing the financial statements is expected to increase its underlying NPAT for the

financial year 2020 (Healius.com.au 2019). In the financial reports of 2019, the company has

suggested that it has not adopted the AASB 16 for accounting for leases as it is not required to do

the same. In the notes to the accounts, the company has stated the impact that adopting AASB 16

would have on its future endeavours. It suggests that the changes suggested by the AASB 16

would remove the distinction between most of the lease assets of the company except for leases

that are short term in nature and of those related to assets which are low in terms of value. From

1 July 2019, the company will begin to measure the value of its liabilities on the basis of the

future lease payments that it will be required to pay (Healius.com.au 2019). With regards to the

right-of-use assets approach, the largest valued assets would be calculated on the basis of the

present value of the assets using the discount rates applicable on the date of transition. Any

accumulated depreciation or amortisation on the assets would be removed from the value of the

assets. Due to the adoption of AASB 16, the company estimates that the value of the liabilities

would go up by $1.2 billion and Right-of-use assets would approximately go up by $1.1 billion

(Healius.com.au. 2019). The company expects to recognise this adjusted amount as its net loss in

the financial statements prepared at the end of the year.

Application of AASB 16 from AASB 117

The application of the AASB 16 that comes into effect from the 1st January, 2019 has

been well taken into consideration by the Healius Company. The application of AASB 16 and

the effect of the implication of the same on the financial statement of the company has been well

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTS

considered in the financial report presented by the company (Niescho 2018). The old standard

that guides companies for leases that is AASB 117, will be scrapped in the year 2018 and the

application of the same will be done by all the companies for the purpose of reporting and

classifying all the lease transactions carried on by the company. The company has stated that due

to the adoption of the new applicable accounting standard AASB 16, will increase the estimates

that have been made by the company and that the value of the liabilities reported in the financial

statement would go up by $1.2 billion (Brumm and Liu 2019). The Right-of-use assets would

approximately go up by $1.1 billion (Healius.com.au. 2019). The company will be recognizing

the adjusted amount as its net loss in the financial statements prepared at the end of the year after

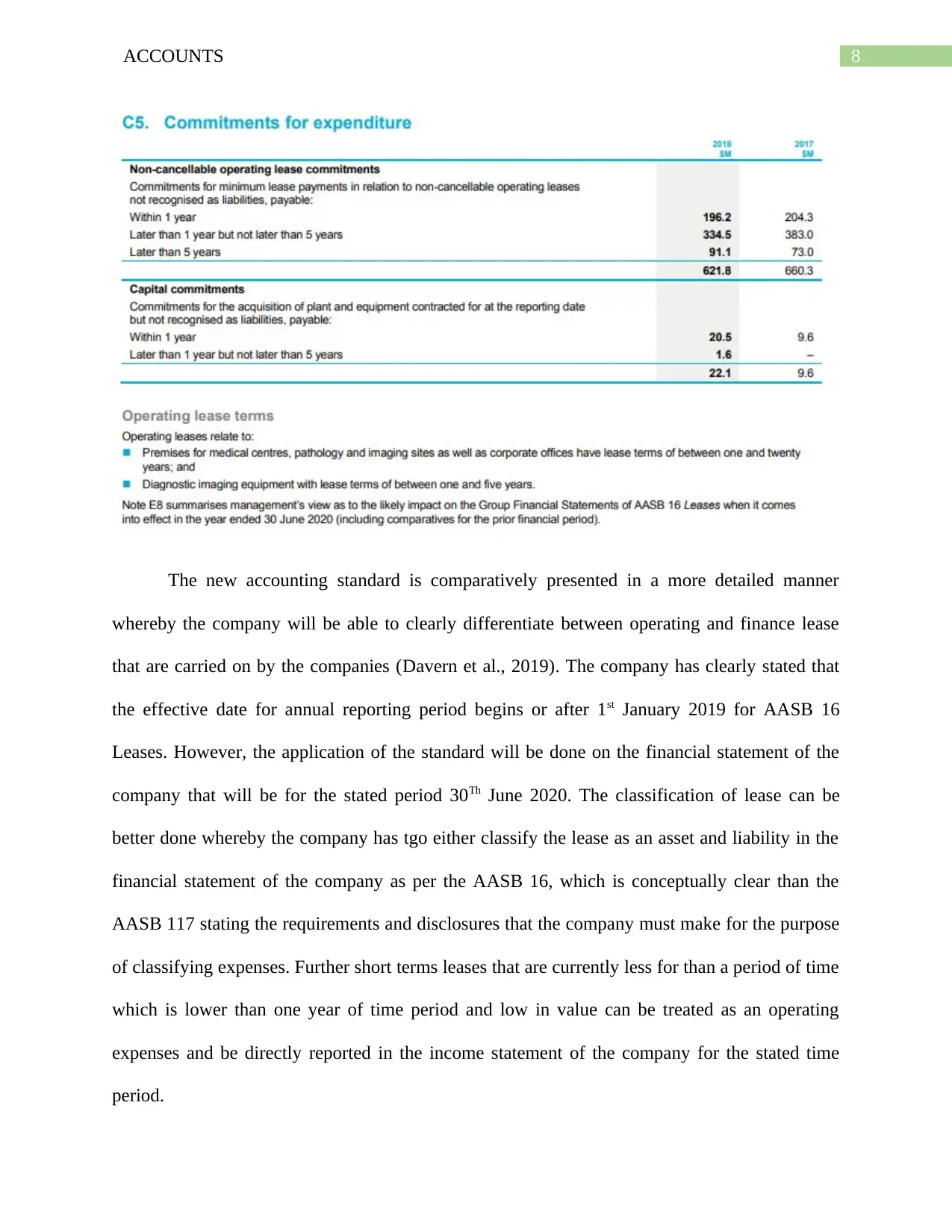

the application of new accounting standard in the current year. The key operating lease that are

directly attributed with the company are specially in the field of the premises for various medical

centres, pathology, imaging sites and other corporate offices that the company has taken on a

lease basis and the tenure of the lease varies from asset classification which is usually in time

period of one year to twenty years of time frame. There are other various equipment like the

diagnostic imagining equipment that the company has considered for the purpose of better

operational work is also taken on a lease who time period are currently between one-five years of

period (Healius.com.au 2019). A key snapshot of the commitment for the various expenditures

that would be incurred by the company for the stated time period has been well defined in the

table given below:

considered in the financial report presented by the company (Niescho 2018). The old standard

that guides companies for leases that is AASB 117, will be scrapped in the year 2018 and the

application of the same will be done by all the companies for the purpose of reporting and

classifying all the lease transactions carried on by the company. The company has stated that due

to the adoption of the new applicable accounting standard AASB 16, will increase the estimates

that have been made by the company and that the value of the liabilities reported in the financial

statement would go up by $1.2 billion (Brumm and Liu 2019). The Right-of-use assets would

approximately go up by $1.1 billion (Healius.com.au. 2019). The company will be recognizing

the adjusted amount as its net loss in the financial statements prepared at the end of the year after

the application of new accounting standard in the current year. The key operating lease that are

directly attributed with the company are specially in the field of the premises for various medical

centres, pathology, imaging sites and other corporate offices that the company has taken on a

lease basis and the tenure of the lease varies from asset classification which is usually in time

period of one year to twenty years of time frame. There are other various equipment like the

diagnostic imagining equipment that the company has considered for the purpose of better

operational work is also taken on a lease who time period are currently between one-five years of

period (Healius.com.au 2019). A key snapshot of the commitment for the various expenditures

that would be incurred by the company for the stated time period has been well defined in the

table given below:

8ACCOUNTS

The new accounting standard is comparatively presented in a more detailed manner

whereby the company will be able to clearly differentiate between operating and finance lease

that are carried on by the companies (Davern et al., 2019). The company has clearly stated that

the effective date for annual reporting period begins or after 1st January 2019 for AASB 16

Leases. However, the application of the standard will be done on the financial statement of the

company that will be for the stated period 30Th June 2020. The classification of lease can be

better done whereby the company has tgo either classify the lease as an asset and liability in the

financial statement of the company as per the AASB 16, which is conceptually clear than the

AASB 117 stating the requirements and disclosures that the company must make for the purpose

of classifying expenses. Further short terms leases that are currently less for than a period of time

which is lower than one year of time period and low in value can be treated as an operating

expenses and be directly reported in the income statement of the company for the stated time

period.

The new accounting standard is comparatively presented in a more detailed manner

whereby the company will be able to clearly differentiate between operating and finance lease

that are carried on by the companies (Davern et al., 2019). The company has clearly stated that

the effective date for annual reporting period begins or after 1st January 2019 for AASB 16

Leases. However, the application of the standard will be done on the financial statement of the

company that will be for the stated period 30Th June 2020. The classification of lease can be

better done whereby the company has tgo either classify the lease as an asset and liability in the

financial statement of the company as per the AASB 16, which is conceptually clear than the

AASB 117 stating the requirements and disclosures that the company must make for the purpose

of classifying expenses. Further short terms leases that are currently less for than a period of time

which is lower than one year of time period and low in value can be treated as an operating

expenses and be directly reported in the income statement of the company for the stated time

period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTS

Conclusion

The accounting concepts used by the Healius Company has helped the accounting

information users such as the stakeholders of the company well related the accounting principles

with appropriate accounting standard in order to assess the materiality of the financial statement

presented. The old standard that guides companies for leases that is AASB 117, will be scrapped

in the year 2018 and the application of the same will be done by all the companies for the

purpose of reporting and classifying all the lease transactions carried on by the company. The

application of the AASB 16 would be a comprehensive and a detailed lease application

accounting standard that would be helping the company in better classification, reporting and

making necessary disclosures about the lease that is reported in the books of accounts.

Conclusion

The accounting concepts used by the Healius Company has helped the accounting

information users such as the stakeholders of the company well related the accounting principles

with appropriate accounting standard in order to assess the materiality of the financial statement

presented. The old standard that guides companies for leases that is AASB 117, will be scrapped

in the year 2018 and the application of the same will be done by all the companies for the

purpose of reporting and classifying all the lease transactions carried on by the company. The

application of the AASB 16 would be a comprehensive and a detailed lease application

accounting standard that would be helping the company in better classification, reporting and

making necessary disclosures about the lease that is reported in the books of accounts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTS

References

Aasb.gov.au. 2019. [Online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 25 Sep.

2019].

Azmi, A.H. and Mohamed, N., 2014. Readiness of Malaysian public sector employees in moving

towards accrual accounting for improve accountability: The case of Ministry of Education

(MOE). Procedia-Social and Behavioral Sciences, 164, pp.106-111.

Brumm, L. and Liu, J., 2019. New leasing accounting standard. Taxation in Australia, 53(8),

p.449.

Davern, M., Gyles, N., Potter, B. and Yang, V., 2019. Implementing AASB 15 revenue from

contracts with customers: the preparer perspective. Accounting Research Journal, (just-

accepted), pp.00-00.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Enofe, A.E., Maugham, C., Otuya, S. and Ovie, C., 2013. Audit report and going concern

assumption in the face of corporate scandals in Nigeria. Research Journal of Finance and

Accounting, 4(11), pp.149-155.

Healius.com.au. (2019). [online] Available at:

https://www.healius.com.au/globalassets/corporate/pdfs/annual-reports/2018/final-2018-ar-

8545_phc_ar18_all_lr.pdf [Accessed 25 Sep. 2019].

References

Aasb.gov.au. 2019. [Online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB16_02-16.pdf [Accessed 25 Sep.

2019].

Azmi, A.H. and Mohamed, N., 2014. Readiness of Malaysian public sector employees in moving

towards accrual accounting for improve accountability: The case of Ministry of Education

(MOE). Procedia-Social and Behavioral Sciences, 164, pp.106-111.

Brumm, L. and Liu, J., 2019. New leasing accounting standard. Taxation in Australia, 53(8),

p.449.

Davern, M., Gyles, N., Potter, B. and Yang, V., 2019. Implementing AASB 15 revenue from

contracts with customers: the preparer perspective. Accounting Research Journal, (just-

accepted), pp.00-00.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Enofe, A.E., Maugham, C., Otuya, S. and Ovie, C., 2013. Audit report and going concern

assumption in the face of corporate scandals in Nigeria. Research Journal of Finance and

Accounting, 4(11), pp.149-155.

Healius.com.au. (2019). [online] Available at:

https://www.healius.com.au/globalassets/corporate/pdfs/annual-reports/2018/final-2018-ar-

8545_phc_ar18_all_lr.pdf [Accessed 25 Sep. 2019].

11ACCOUNTS

Healius.com.au. 2019. [Online] Available at:

https://www.healius.com.au/globalassets/corporate/pdfs/asx-announcements/2019/annual-report-

to-shareholders-1963669.pdf [Accessed 25 Sep. 2019].

Ifrs.org. (2019). [Online] Available at: https://www.ifrs.org/-/media/project/leases/ifrs/published-

documents/ifrs16-effects-analysis.pdf [Accessed 25 Sep. 2019].

Limited, P. 2019. Annual Reports | Healius Limited. [online] Healius.com.au. Available at:

https://www.healius.com.au/invest-in-us/reports/annual-reports/ [Accessed 25 Sep. 2019].

Mora, A. and Walker, M., 2015. The implications of research on accounting conservatism for

accounting standard setting. Accounting and Business Research, 45(5), pp.620-650.

Niescho, C., 2018. Triple whammy. Company Director, 34(5), p.62.

Peterson, K., Schmardebeck, R. and Wilks, T.J., 2015. The earnings quality and information

processing effects of accounting consistency. The accounting review, 90(6), pp.2483-2514.

Healius.com.au. 2019. [Online] Available at:

https://www.healius.com.au/globalassets/corporate/pdfs/asx-announcements/2019/annual-report-

to-shareholders-1963669.pdf [Accessed 25 Sep. 2019].

Ifrs.org. (2019). [Online] Available at: https://www.ifrs.org/-/media/project/leases/ifrs/published-

documents/ifrs16-effects-analysis.pdf [Accessed 25 Sep. 2019].

Limited, P. 2019. Annual Reports | Healius Limited. [online] Healius.com.au. Available at:

https://www.healius.com.au/invest-in-us/reports/annual-reports/ [Accessed 25 Sep. 2019].

Mora, A. and Walker, M., 2015. The implications of research on accounting conservatism for

accounting standard setting. Accounting and Business Research, 45(5), pp.620-650.

Niescho, C., 2018. Triple whammy. Company Director, 34(5), p.62.

Peterson, K., Schmardebeck, R. and Wilks, T.J., 2015. The earnings quality and information

processing effects of accounting consistency. The accounting review, 90(6), pp.2483-2514.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.