Application of Conceptual Framework and Sustainability Reporting: Austal Limited and Sibanye Gold Ltd

VerifiedAdded on 2022/11/11

|22

|5033

|488

AI Summary

The report evaluates the usefulness of CF and other voluntary frameworks such as GRI and integrated reporting for development of sustainable reports. It analyzes the history, benefits and limitations of CF and demonstrates its applications within Austal Limited. It also compares GRI and integrated reporting and theories applied for developing content of sustainability reporting. The report evaluates the reporting framework of Sibanye Gold Ltd and compares it with Austal Limited.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ACCT20074 Contemporary Accounting Theory

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

The report has examined the usefulness of CF and other voluntary frameworks such as

GRI an integrated reporting for development of sustaible reports. This has been carried out by

analyzing the history, benefits and limitations of CF and also demonstrating its applications

within a selected business entity in Australia, Austal Limited. It is followed by providing a

discussion about the difference between GRI and integrated reporting and theories that have been

applied for developing content of sustainability reporting. The various criteria of integrated

reports have been developed in the context of selected South African company, that is, Sibanye

Gold Ltd (SGL).

2

The report has examined the usefulness of CF and other voluntary frameworks such as

GRI an integrated reporting for development of sustaible reports. This has been carried out by

analyzing the history, benefits and limitations of CF and also demonstrating its applications

within a selected business entity in Australia, Austal Limited. It is followed by providing a

discussion about the difference between GRI and integrated reporting and theories that have been

applied for developing content of sustainability reporting. The various criteria of integrated

reports have been developed in the context of selected South African company, that is, Sibanye

Gold Ltd (SGL).

2

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................5

Part A: Evaluation of conceptual framework and application of it in the chosen company...........6

Section A: History and Development of the CF for Financial Reporting....................................6

Section B: Concerns of Australian Professionals Regarding the Application of IASB/IFRS CF

for Financial Reporting................................................................................................................7

Section C: Significant Potential Benefits and Limitations of CF for Financial Reporting..........7

Section D: Use of conceptual framework to evaluate the annual report of Austal Limited........8

D (I): Number of financial statements and their components......................................................8

D (II): Principle of recognition and measurement bases used for assets, revenue and liabilities

....................................................................................................................................................10

D (III): Qualitative characteristics of financial information that have been presented in the

financial statements of Austral Group.......................................................................................10

Part B: Evaluation of integrating reporting/sustainability reporting and application of same in

South Africa Company includes the comparison with one of Australian Company.....................13

Section A: Comparison of Global Reporting Initiative (GRI) and International Integrated

Reporting Framework for Social Responsibility Reporting......................................................13

Section B: Conventional Accounting Strengths and Limitations for Explaining the Contents of

Sustainability and Integrated Reports........................................................................................13

Section C: Applicability of Theories for Explaining the Contents of Sustainability and

Integrated Reporting..................................................................................................................14

Section D: Use of different components of the integrated reporting to evaluate the reporting

framework of the selected South African Company (Sibanye Gold Limited)...........................15

Section E: Comparison of reporting practices by Australian Company and South African

Company....................................................................................................................................17

3

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................5

Part A: Evaluation of conceptual framework and application of it in the chosen company...........6

Section A: History and Development of the CF for Financial Reporting....................................6

Section B: Concerns of Australian Professionals Regarding the Application of IASB/IFRS CF

for Financial Reporting................................................................................................................7

Section C: Significant Potential Benefits and Limitations of CF for Financial Reporting..........7

Section D: Use of conceptual framework to evaluate the annual report of Austal Limited........8

D (I): Number of financial statements and their components......................................................8

D (II): Principle of recognition and measurement bases used for assets, revenue and liabilities

....................................................................................................................................................10

D (III): Qualitative characteristics of financial information that have been presented in the

financial statements of Austral Group.......................................................................................10

Part B: Evaluation of integrating reporting/sustainability reporting and application of same in

South Africa Company includes the comparison with one of Australian Company.....................13

Section A: Comparison of Global Reporting Initiative (GRI) and International Integrated

Reporting Framework for Social Responsibility Reporting......................................................13

Section B: Conventional Accounting Strengths and Limitations for Explaining the Contents of

Sustainability and Integrated Reports........................................................................................13

Section C: Applicability of Theories for Explaining the Contents of Sustainability and

Integrated Reporting..................................................................................................................14

Section D: Use of different components of the integrated reporting to evaluate the reporting

framework of the selected South African Company (Sibanye Gold Limited)...........................15

Section E: Comparison of reporting practices by Australian Company and South African

Company....................................................................................................................................17

3

Conclusion.....................................................................................................................................19

References......................................................................................................................................20

4

References......................................................................................................................................20

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction

Conceptual framework (CF) can be defined as coherent system of interrelated objectives

and fundamentals that is leading to the development of consistent standards and prescribing the

nature and quality of financial accounting within businesses. On the other hand, sustainable

reporting can be regarded as the practice of providing information about social and

environmental performance of an organization. This report has been prepared in the context of

examining the application of conceptual framework for financial reporting and other voluntary

frameworks such as GRI and integrated reporting framework to develop sustainable reports.

5

Conceptual framework (CF) can be defined as coherent system of interrelated objectives

and fundamentals that is leading to the development of consistent standards and prescribing the

nature and quality of financial accounting within businesses. On the other hand, sustainable

reporting can be regarded as the practice of providing information about social and

environmental performance of an organization. This report has been prepared in the context of

examining the application of conceptual framework for financial reporting and other voluntary

frameworks such as GRI and integrated reporting framework to develop sustainable reports.

5

Part A: Evaluation of conceptual framework and application of it in the chosen company

Section A: History and Development of the CF for Financial Reporting

The conceptual framework is developed for providing assistance to the developers of

financial reports regarding the selection of accounting policies on the basis of theoretical

principles mainly of relevance and faithful presentation. The framework has been developed on

the basis of normative theory which provides guidance regarding the theoretical principles to be

used for carrying out accounting processes.

The framework has initially being developed by the IASB and it has been revised under

the common efforts of both IASB and FASB for the purpose of driving improvement within the

conceptual framework. The conceptual framework has been revised by the IASB and it has

largely been adopted by the countries aiming for complying with international accounting

standards for promoting uniformity in the financial reporting system. The framework is now

largely being applied by business corporations across the world. The CF’s have been developed

in a number (Barth, 2008). There has been the development of Accounting Principles Board

(APB) in the USA for providing the accounting principles to be followed during financial

reporting. The Board is criticized for lack of any real framework for guiding the financial

reporting. There was establishment of a Trueblood Committee in the year 1971 which developed

the Trueblood Report. It has provided about 12 objectives and 7 qualitative criteria to be present

within a financial report (Dean and Clarke, 2003). These objectives and characteristics were not

found to be adequate for providing decision-making information to the users. As such, the APB

is replaced by FASB and released six statements of financial accounting concepts from the year

1978 to 1985. The FASB has joined IASB in the year 2005 for developing a revised CF which

has now being adopted within the US (Macías and Muiño, 2011).

In the UK, Accounting Standards Board (ASB) has adopted the International Accounting

Standards’ Committee (IASC) that is consistent with the US and Australian frameworks. On the

other hand, in Australia there have been only four statement accounting concepts about defining

the reporting entity, objective of general purpose financial reporting, providing qualitative

principles for reporting financial information and stating the definition of recognizing the

financial statement elements. The framework has not provided the statements regarding the

6

Section A: History and Development of the CF for Financial Reporting

The conceptual framework is developed for providing assistance to the developers of

financial reports regarding the selection of accounting policies on the basis of theoretical

principles mainly of relevance and faithful presentation. The framework has been developed on

the basis of normative theory which provides guidance regarding the theoretical principles to be

used for carrying out accounting processes.

The framework has initially being developed by the IASB and it has been revised under

the common efforts of both IASB and FASB for the purpose of driving improvement within the

conceptual framework. The conceptual framework has been revised by the IASB and it has

largely been adopted by the countries aiming for complying with international accounting

standards for promoting uniformity in the financial reporting system. The framework is now

largely being applied by business corporations across the world. The CF’s have been developed

in a number (Barth, 2008). There has been the development of Accounting Principles Board

(APB) in the USA for providing the accounting principles to be followed during financial

reporting. The Board is criticized for lack of any real framework for guiding the financial

reporting. There was establishment of a Trueblood Committee in the year 1971 which developed

the Trueblood Report. It has provided about 12 objectives and 7 qualitative criteria to be present

within a financial report (Dean and Clarke, 2003). These objectives and characteristics were not

found to be adequate for providing decision-making information to the users. As such, the APB

is replaced by FASB and released six statements of financial accounting concepts from the year

1978 to 1985. The FASB has joined IASB in the year 2005 for developing a revised CF which

has now being adopted within the US (Macías and Muiño, 2011).

In the UK, Accounting Standards Board (ASB) has adopted the International Accounting

Standards’ Committee (IASC) that is consistent with the US and Australian frameworks. On the

other hand, in Australia there have been only four statement accounting concepts about defining

the reporting entity, objective of general purpose financial reporting, providing qualitative

principles for reporting financial information and stating the definition of recognizing the

financial statement elements. The framework has not provided the statements regarding the

6

measurement concept and therefore is not widely accepted. The Australia adopted the IASBCF

after the decision of Financial Reporting Council in the year 2015 for improving comparability

of its financial reporting system (Chua, Chee and Cheong, 2012). The joint efforts of FASB and

IASB for convergence of accounting standards is leading to the global acceptance of the CF

principles in the financial reporting system of business entities on a global level (Seng, 2014).

Section B: Concerns of Australian Professionals Regarding the Application of IASB/IFRS

CF for Financial Reporting

The Australian accounting professionals such as Certified Public Accountants (CPAs)

and other accounting professional bodies within the country have shred their various concerns

that are associated with the application of CF in financial reporting as provided by the AASB.

The major concern that is present in this context related to considering the financial reporting

thresholds as per the Corporations Act 2001 that have not been given consideration by the AASB

(Lonergan, 2005). In addition to this, there have also been issues shared in regards to cost-benefit

analysis of the framework. There has been inappropriate analysis conducted in regards to

increasing costs required for adopting the new CF of financial reporting as camped to its benefits

achieved. The higher costs would be incurred in providing training to the accounting

professionals and implemented widespread changes in the financial reporting system. This

requires comprehensive and detailed cost-benefits analysis to be conducted before processed

with the acceptance of the AASB proposals (Wong, 2004).

The major challenge that has been identified by the accounting professionals in this

regard is relating to the adoption of IASB framework for small and medium-sized entities. There

is requirement of developing separate framework for controlling the financial reporting of these

corporations. This is because application of the IASB standard would require higher costs for

these entities in comparison to the benefits to be realized. These entities possess limited financial

resources and therefore it would be very difficult for them to comply with all the IASB principles

(AASB adoption of IASB standards by 2005, 2004).

Section C: Significant Potential Benefits and Limitations of CF for Financial Reporting

The various accounting researchers have highlighted the following concerns relating to

the CF that has been discussed under its significant benefits and limitations headings as follows:

7

after the decision of Financial Reporting Council in the year 2015 for improving comparability

of its financial reporting system (Chua, Chee and Cheong, 2012). The joint efforts of FASB and

IASB for convergence of accounting standards is leading to the global acceptance of the CF

principles in the financial reporting system of business entities on a global level (Seng, 2014).

Section B: Concerns of Australian Professionals Regarding the Application of IASB/IFRS

CF for Financial Reporting

The Australian accounting professionals such as Certified Public Accountants (CPAs)

and other accounting professional bodies within the country have shred their various concerns

that are associated with the application of CF in financial reporting as provided by the AASB.

The major concern that is present in this context related to considering the financial reporting

thresholds as per the Corporations Act 2001 that have not been given consideration by the AASB

(Lonergan, 2005). In addition to this, there have also been issues shared in regards to cost-benefit

analysis of the framework. There has been inappropriate analysis conducted in regards to

increasing costs required for adopting the new CF of financial reporting as camped to its benefits

achieved. The higher costs would be incurred in providing training to the accounting

professionals and implemented widespread changes in the financial reporting system. This

requires comprehensive and detailed cost-benefits analysis to be conducted before processed

with the acceptance of the AASB proposals (Wong, 2004).

The major challenge that has been identified by the accounting professionals in this

regard is relating to the adoption of IASB framework for small and medium-sized entities. There

is requirement of developing separate framework for controlling the financial reporting of these

corporations. This is because application of the IASB standard would require higher costs for

these entities in comparison to the benefits to be realized. These entities possess limited financial

resources and therefore it would be very difficult for them to comply with all the IASB principles

(AASB adoption of IASB standards by 2005, 2004).

Section C: Significant Potential Benefits and Limitations of CF for Financial Reporting

The various accounting researchers have highlighted the following concerns relating to

the CF that has been discussed under its significant benefits and limitations headings as follows:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Benefits

The application of CF into financial reporting has facilitated in removal of all the

inconsistencies present within the accounting principles and lead to the establishment of

more logical and consistent accounting standards

The large number of countries around the world have adopted the CF and therefore its

widespread adoption is leading towards improving the international comparability across

different accounting rules and policies (Silvia, 2016)

It has improved the accountability and transparency in business operations and resulting

in providing the financial information to the users that is more useful in decision-making

It has also caused the need for improving credibility in the accounting standard-setting

procedures as the accounting professionals need to work as per the CF fundamentals

which requires depiction of high relevant and reliable information (Fajard, 2016)

Limitations

The issue of measurement has not yet been resolved under the CF as there has been the

presence of different measurement approaches by business entities across the world for

recognition of assets and liabilities. This can result in causing the issue related with

measurement in accounting (Tschopp and Nastanski, 2014)

There is no usefulness of its integration for smaller business entities

It has only taken into considering the financial performance and relatively ignored the

need for developing a framework for reporting the social and environmental performance

(Pacter, 2013)

Section D: Use of conceptual framework to evaluate the annual report of Austal Limited

D (I): Number of financial statements and their components

This part requires the evaluation of annual report of Austal Group Limited for year 2018

through using the conceptual framework. The purpose is to check whether Ingenia Communities

Group has been successful to apply all the guidelines and information provided in the conceptual

framework (Conceptual Framework, 2018).

8

The application of CF into financial reporting has facilitated in removal of all the

inconsistencies present within the accounting principles and lead to the establishment of

more logical and consistent accounting standards

The large number of countries around the world have adopted the CF and therefore its

widespread adoption is leading towards improving the international comparability across

different accounting rules and policies (Silvia, 2016)

It has improved the accountability and transparency in business operations and resulting

in providing the financial information to the users that is more useful in decision-making

It has also caused the need for improving credibility in the accounting standard-setting

procedures as the accounting professionals need to work as per the CF fundamentals

which requires depiction of high relevant and reliable information (Fajard, 2016)

Limitations

The issue of measurement has not yet been resolved under the CF as there has been the

presence of different measurement approaches by business entities across the world for

recognition of assets and liabilities. This can result in causing the issue related with

measurement in accounting (Tschopp and Nastanski, 2014)

There is no usefulness of its integration for smaller business entities

It has only taken into considering the financial performance and relatively ignored the

need for developing a framework for reporting the social and environmental performance

(Pacter, 2013)

Section D: Use of conceptual framework to evaluate the annual report of Austal Limited

D (I): Number of financial statements and their components

This part requires the evaluation of annual report of Austal Group Limited for year 2018

through using the conceptual framework. The purpose is to check whether Ingenia Communities

Group has been successful to apply all the guidelines and information provided in the conceptual

framework (Conceptual Framework, 2018).

8

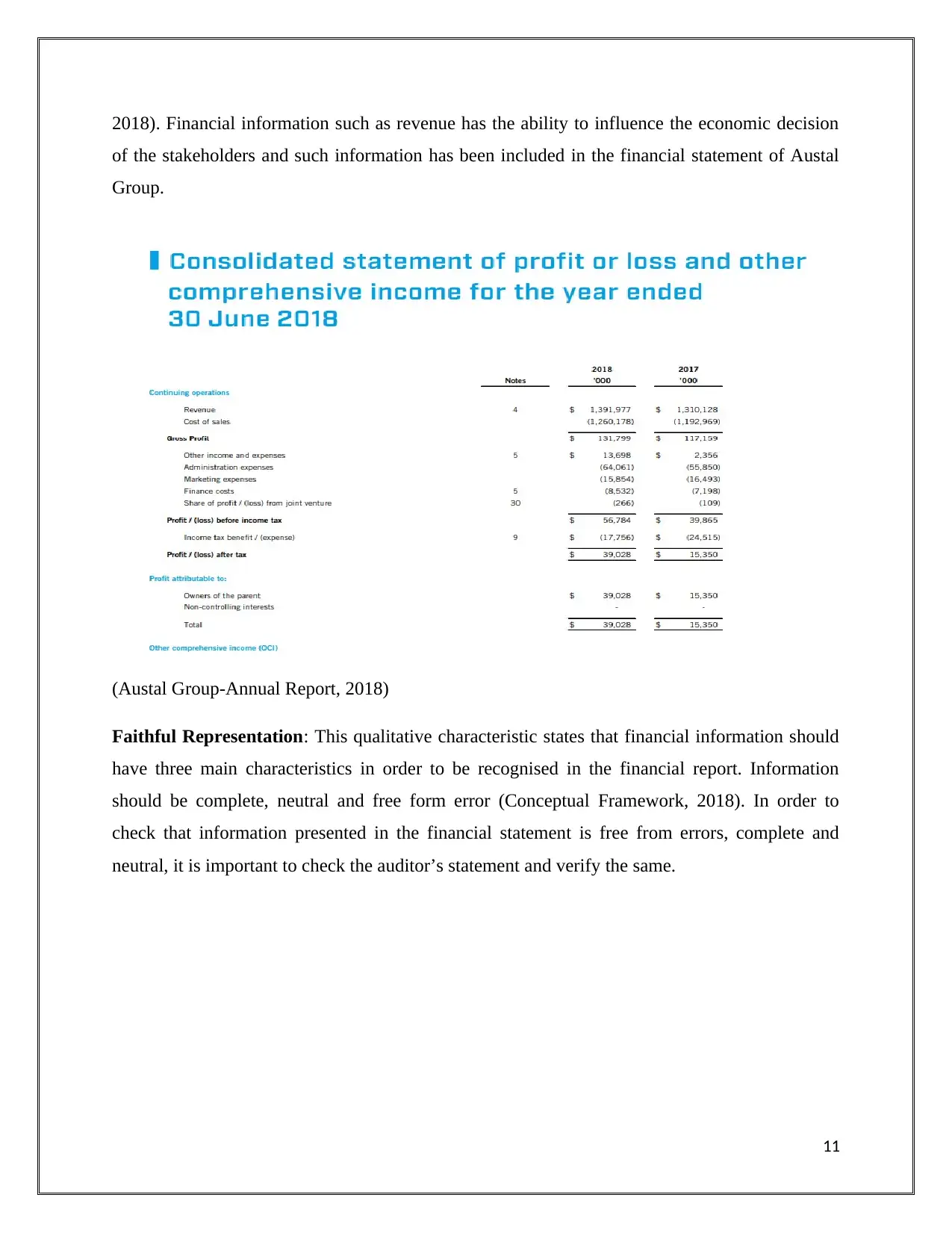

According to the conceptual framework company needs to produce four major categories

of financial statements or reports. Following are the major components of financial statements

that Austal Group Limited has prepared as per the conceptual framework:

Income Statement or statement of financial performance: Income statement is the most

important financial statement prepared to reflect the financial performance of the company

during the specific period. In annual report of Austal Group Limited only consolidated income

statement is provided which shows the financial performance of the holding company as well as

all the subsidiaries. This statement provides information on revenue and expenses (Austal

Group-Annual Report, 2018).

Balance sheet or statement of financial position: Austal Group Limited has provided only

consolidated balance sheet that reflects the financial position of the parent company as well as all

the subsidiaries. The basic elements of the statement of financial positions are assets, liabilities

and equity.

Statement of change in equity: Contribution and distribution made by shareholders are being

disclosed in this statement. This statement is also prepared as consolidated statement.

Statement of cash flow: This statement discloses information on the cash flows various

activities such as operating activity, financing activity and investing activity. It is also presented

as consolidated statement to provide cash flow information for whole group (Austal Group-

Annual Report, 2018).

In addition to above statement, there is need to provide the notes to financial statement to

provide details of measurement, recognition and other information. Notes to accounts is the most

important part of financial statement as it discloses information on methods, assumptions and

judgments that have been used to estimate the amount of all financial elements. In addition to

this it provides information on any change in accounting methods, policies, estimation and

assumptions (Austal Group-Annual Report, 2018).

9

of financial statements or reports. Following are the major components of financial statements

that Austal Group Limited has prepared as per the conceptual framework:

Income Statement or statement of financial performance: Income statement is the most

important financial statement prepared to reflect the financial performance of the company

during the specific period. In annual report of Austal Group Limited only consolidated income

statement is provided which shows the financial performance of the holding company as well as

all the subsidiaries. This statement provides information on revenue and expenses (Austal

Group-Annual Report, 2018).

Balance sheet or statement of financial position: Austal Group Limited has provided only

consolidated balance sheet that reflects the financial position of the parent company as well as all

the subsidiaries. The basic elements of the statement of financial positions are assets, liabilities

and equity.

Statement of change in equity: Contribution and distribution made by shareholders are being

disclosed in this statement. This statement is also prepared as consolidated statement.

Statement of cash flow: This statement discloses information on the cash flows various

activities such as operating activity, financing activity and investing activity. It is also presented

as consolidated statement to provide cash flow information for whole group (Austal Group-

Annual Report, 2018).

In addition to above statement, there is need to provide the notes to financial statement to

provide details of measurement, recognition and other information. Notes to accounts is the most

important part of financial statement as it discloses information on methods, assumptions and

judgments that have been used to estimate the amount of all financial elements. In addition to

this it provides information on any change in accounting methods, policies, estimation and

assumptions (Austal Group-Annual Report, 2018).

9

D (II): Principle of recognition and measurement bases used for assets, revenue and

liabilities

Revenue: Austal Group recognised most of its revenue through the construction

business. IFRS 15 deals with all types of revenue contracts including construction

contracts. Austal Group recognizes revenue when it is probable that economic benefits

will flow to the company and such revenue can be measured in terms of monetary value.

Revenue is measured at fair value of the consideration received or receivable. Austal

Group makes use of percentage of completion method to recognize the actual revenue

and cost related to such revenue (Conceptual Framework, 2018).

Assets: There are many assets that company present in their balance sheet and there have

different recognition principle and measurement bases of each asset. Cash and cash

equivalents consists of cash and short term deposits with three months of maturity. Trade

receivables are measured as the sales amount less any allowances made for the amount of

uncollectible. Receivables have been recognized on the basis of credit terms given to the

customers and information given in the invoice. Inventory are measured at lower of net

realizable value and cost, and it is recognised at weighted average cost basis. Plant,

property and equipment is being recognised at historical cost basis which means cost less

any accumulated depreciation or impairment. Intangible asset that has been acquired are

initially measured at cost less any impairment losses and amortisation (Austal Group-

Annual Report, 2018).

Liabilities: Trade payable have been measured at amortized cost and they are recognised

when company become obliged to make the payments in future in respect to expenses.

Provisions are recognised when there is obligation to settle the future obligation that has

been arising due to past event. Borrowings are initially recognised at fair value of the

amount received minus any value paid for transaction cost. After that they are measured

at amortized cost through using the effective interest method (Austal Group-Annual

Report, 2018).

D (III): Qualitative characteristics of financial information that have been presented in the

financial statements of Austral Group

Relevance: Relevance means financial information should have predictive and confirmative

value that has capability to influence the economic decision of the users (Conceptual Framework,

10

liabilities

Revenue: Austal Group recognised most of its revenue through the construction

business. IFRS 15 deals with all types of revenue contracts including construction

contracts. Austal Group recognizes revenue when it is probable that economic benefits

will flow to the company and such revenue can be measured in terms of monetary value.

Revenue is measured at fair value of the consideration received or receivable. Austal

Group makes use of percentage of completion method to recognize the actual revenue

and cost related to such revenue (Conceptual Framework, 2018).

Assets: There are many assets that company present in their balance sheet and there have

different recognition principle and measurement bases of each asset. Cash and cash

equivalents consists of cash and short term deposits with three months of maturity. Trade

receivables are measured as the sales amount less any allowances made for the amount of

uncollectible. Receivables have been recognized on the basis of credit terms given to the

customers and information given in the invoice. Inventory are measured at lower of net

realizable value and cost, and it is recognised at weighted average cost basis. Plant,

property and equipment is being recognised at historical cost basis which means cost less

any accumulated depreciation or impairment. Intangible asset that has been acquired are

initially measured at cost less any impairment losses and amortisation (Austal Group-

Annual Report, 2018).

Liabilities: Trade payable have been measured at amortized cost and they are recognised

when company become obliged to make the payments in future in respect to expenses.

Provisions are recognised when there is obligation to settle the future obligation that has

been arising due to past event. Borrowings are initially recognised at fair value of the

amount received minus any value paid for transaction cost. After that they are measured

at amortized cost through using the effective interest method (Austal Group-Annual

Report, 2018).

D (III): Qualitative characteristics of financial information that have been presented in the

financial statements of Austral Group

Relevance: Relevance means financial information should have predictive and confirmative

value that has capability to influence the economic decision of the users (Conceptual Framework,

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2018). Financial information such as revenue has the ability to influence the economic decision

of the stakeholders and such information has been included in the financial statement of Austal

Group.

(Austal Group-Annual Report, 2018)

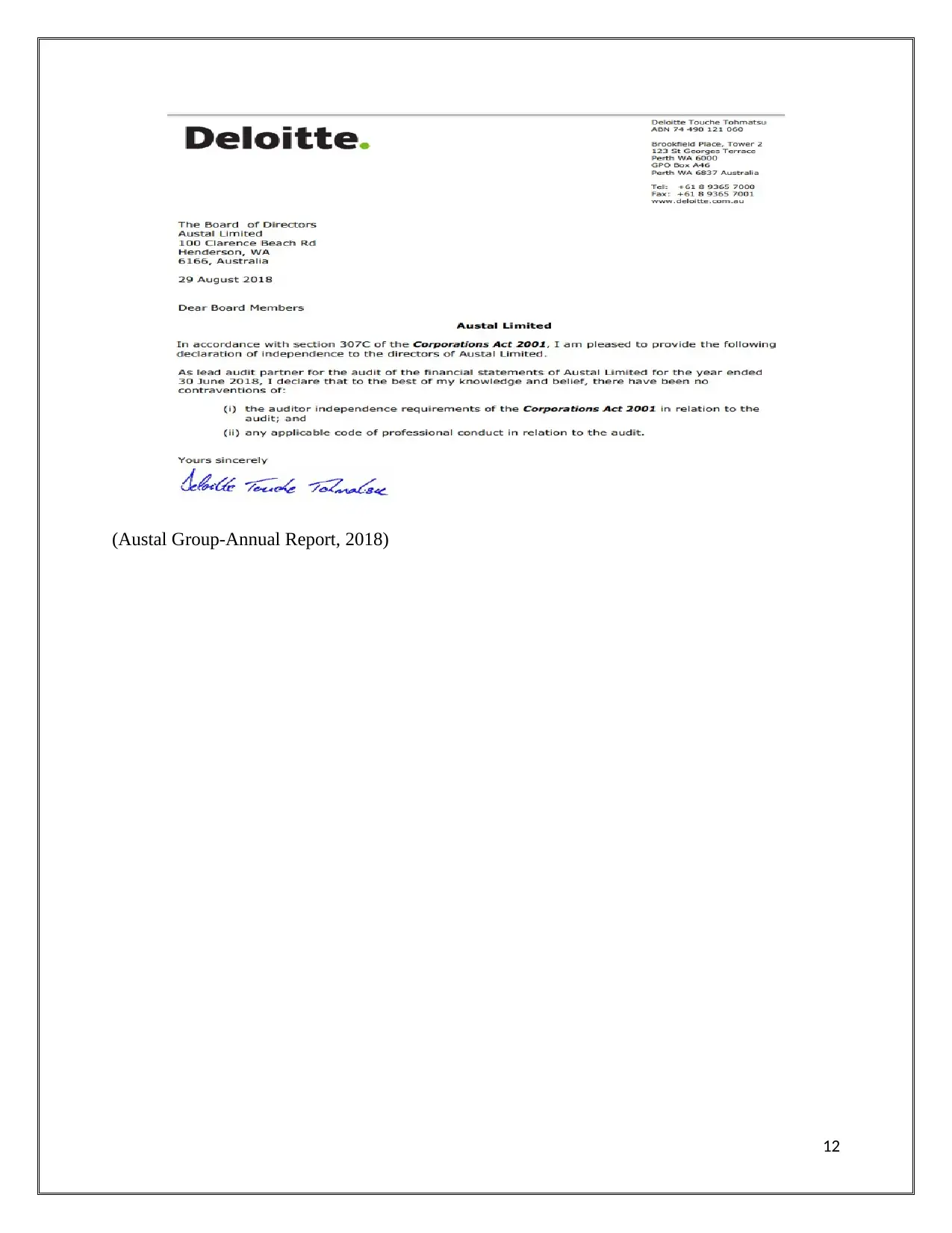

Faithful Representation: This qualitative characteristic states that financial information should

have three main characteristics in order to be recognised in the financial report. Information

should be complete, neutral and free form error (Conceptual Framework, 2018). In order to

check that information presented in the financial statement is free from errors, complete and

neutral, it is important to check the auditor’s statement and verify the same.

11

of the stakeholders and such information has been included in the financial statement of Austal

Group.

(Austal Group-Annual Report, 2018)

Faithful Representation: This qualitative characteristic states that financial information should

have three main characteristics in order to be recognised in the financial report. Information

should be complete, neutral and free form error (Conceptual Framework, 2018). In order to

check that information presented in the financial statement is free from errors, complete and

neutral, it is important to check the auditor’s statement and verify the same.

11

(Austal Group-Annual Report, 2018)

12

12

Part B: Evaluation of integrating reporting/sustainability reporting and application of

same in South Africa Company includes the comparison with one of Australian Company

Section A: Comparison of Global Reporting Initiative (GRI) and International Integrated

Reporting Framework for Social Responsibility Reporting

There has been increasing pressure on corporations from the investors to disclose the

information regarding their social and environmental performance for assessing the legitimacy

and accountability of the business operations. As such, there has been the development of

various types of voluntary framework to assist the business entities regarding the social and

environmental disclosures. The sustainability reporting guidelines have been developed in this

context that have established the GRI framework to provide the international standards to be

used by business for disclosing social and environmental performance. The GRI framework has

provided the principles only for developing the sustainable reports and does not include any

guidance in relating to reporting of financial data (GRI, 2017).

The principles for defining report content includes inclusiveness of stakeholders’,

materiality, sustainability context and completeness. Integrated reporting can be regarded as a

step further GRI framework that emphasizes the business to adopt an integrated approach besides

focusing only on sustainability risks. It requires the business to report on each aspect whether

financial or non-financial and also demonstrating the ways that a reporting entity integrates

wider risks and opportunities into its long-term strategy making and daily operational activities.

The principles provided by the International Integrated Reporting Council (IIRC) for developing

integrated reports are strategic focus, connectivity of information, relationships with

stakeholders’, materiality, conciseness, reliability and consistency. However, GRI and IIRC are

working in collaboration with each other for supporting the development of integrated and

sustainability reporting (The IIRC, 2017).

Section B: Conventional Accounting Strengths and Limitations for Explaining the

Contents of Sustainability and Integrated Reports

The conventional accounting systems such as CF used for the purpose of developing

financial reports through very useful for reporting of financial information but does not prove to

be of any use for developing disclosures relating to social and environmental performances of

13

same in South Africa Company includes the comparison with one of Australian Company

Section A: Comparison of Global Reporting Initiative (GRI) and International Integrated

Reporting Framework for Social Responsibility Reporting

There has been increasing pressure on corporations from the investors to disclose the

information regarding their social and environmental performance for assessing the legitimacy

and accountability of the business operations. As such, there has been the development of

various types of voluntary framework to assist the business entities regarding the social and

environmental disclosures. The sustainability reporting guidelines have been developed in this

context that have established the GRI framework to provide the international standards to be

used by business for disclosing social and environmental performance. The GRI framework has

provided the principles only for developing the sustainable reports and does not include any

guidance in relating to reporting of financial data (GRI, 2017).

The principles for defining report content includes inclusiveness of stakeholders’,

materiality, sustainability context and completeness. Integrated reporting can be regarded as a

step further GRI framework that emphasizes the business to adopt an integrated approach besides

focusing only on sustainability risks. It requires the business to report on each aspect whether

financial or non-financial and also demonstrating the ways that a reporting entity integrates

wider risks and opportunities into its long-term strategy making and daily operational activities.

The principles provided by the International Integrated Reporting Council (IIRC) for developing

integrated reports are strategic focus, connectivity of information, relationships with

stakeholders’, materiality, conciseness, reliability and consistency. However, GRI and IIRC are

working in collaboration with each other for supporting the development of integrated and

sustainability reporting (The IIRC, 2017).

Section B: Conventional Accounting Strengths and Limitations for Explaining the

Contents of Sustainability and Integrated Reports

The conventional accounting systems such as CF used for the purpose of developing

financial reports through very useful for reporting of financial information but does not prove to

be of any use for developing disclosures relating to social and environmental performances of

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

businesses. The significant limitations that are associated with the conventional system of

accounting for financial reporting can be explained as follows:

There is no explicit consideration given in the CF for preparation of financial reports

about meeting the needs and expectations of diverse group of stakeholders. As such, it

does not provide any guidance in relation to present the non-financial nature of

information that may be required by its community members to analyze whether the

business operations does not negatively impact the society (Dragomir, 2011)

It only helps in conveying the financial information and is not useful for stating any type

of information that helps in assessing the integrity and accountability in the operational

activities. The ethical and governance outlook of the company cannot be conveyed

through its use which may be required by the investors for ensuring that a company is

conducting its various activities in an ethical manner (Ivan, 2009)

Materiality as provided by the CF is only helpful for disclosing information which can

be quantified in monetary terms such as financial information. The social and

environmental performance of a company cannot be quantified on monetary basis and

therefore cannot be disclosed as per the materiality concept of CF.

Also, the CF recognized expenses on the basis of costs incurred and recognized revenue

on the basis of profits attained. However, it is difficult to assess accurately the social

costs and profits and therefore CF may prove to be inadequate for the purpose of social

reporting (Information Resources, 2015)

Section C: Applicability of Theories for Explaining the Contents of Sustainability and

Integrated Reporting

The sustainability context used by business entities across the world for preparing of their

sustainable or integrated information can be adequately explained with the use of stakeholder

and legitimacy theory. The voluntary frameworks such as GRI or integrated reports have been

developed in accordance with the views presented within the stakeholder theory. The stakeholder

theory has stated that businesses are held responsible for all its stakeholders that are associated

with its operational activities such as employees, suppliers, local communities, creditors and

others. Therefore, the theory has emphasized on the importance of meeting the varying interests

of all the stakeholders besides only shareholders. Thus, it has emphasized on the need of

14

accounting for financial reporting can be explained as follows:

There is no explicit consideration given in the CF for preparation of financial reports

about meeting the needs and expectations of diverse group of stakeholders. As such, it

does not provide any guidance in relation to present the non-financial nature of

information that may be required by its community members to analyze whether the

business operations does not negatively impact the society (Dragomir, 2011)

It only helps in conveying the financial information and is not useful for stating any type

of information that helps in assessing the integrity and accountability in the operational

activities. The ethical and governance outlook of the company cannot be conveyed

through its use which may be required by the investors for ensuring that a company is

conducting its various activities in an ethical manner (Ivan, 2009)

Materiality as provided by the CF is only helpful for disclosing information which can

be quantified in monetary terms such as financial information. The social and

environmental performance of a company cannot be quantified on monetary basis and

therefore cannot be disclosed as per the materiality concept of CF.

Also, the CF recognized expenses on the basis of costs incurred and recognized revenue

on the basis of profits attained. However, it is difficult to assess accurately the social

costs and profits and therefore CF may prove to be inadequate for the purpose of social

reporting (Information Resources, 2015)

Section C: Applicability of Theories for Explaining the Contents of Sustainability and

Integrated Reporting

The sustainability context used by business entities across the world for preparing of their

sustainable or integrated information can be adequately explained with the use of stakeholder

and legitimacy theory. The voluntary frameworks such as GRI or integrated reports have been

developed in accordance with the views presented within the stakeholder theory. The stakeholder

theory has stated that businesses are held responsible for all its stakeholders that are associated

with its operational activities such as employees, suppliers, local communities, creditors and

others. Therefore, the theory has emphasized on the importance of meeting the varying interests

of all the stakeholders besides only shareholders. Thus, it has emphasized on the need of

14

sustainable reporting of organizations by providing information regarding its social and

environmental impacts which helps in ensuring that it is taking measures for meeting the need of

local communities and environment (Manetti, 2011). On the other hand, the legitimacy theory

has also advocated in assisting the contents of sustainability or integrated reporting through

placing emphasizes on the need for business entities to develop their legitimate image within the

society in which it exists for gathering its continued support. The theory has directed the business

organizations to take measures for ensuring that depicts that they are conducting their different

activities under the acceptable norms of society. As such, they develop the content of its

sustainable reports in a manner so as to develop a legitimate image ion the mind of its different

stakeholders (Villiers and Maroun, 2017).

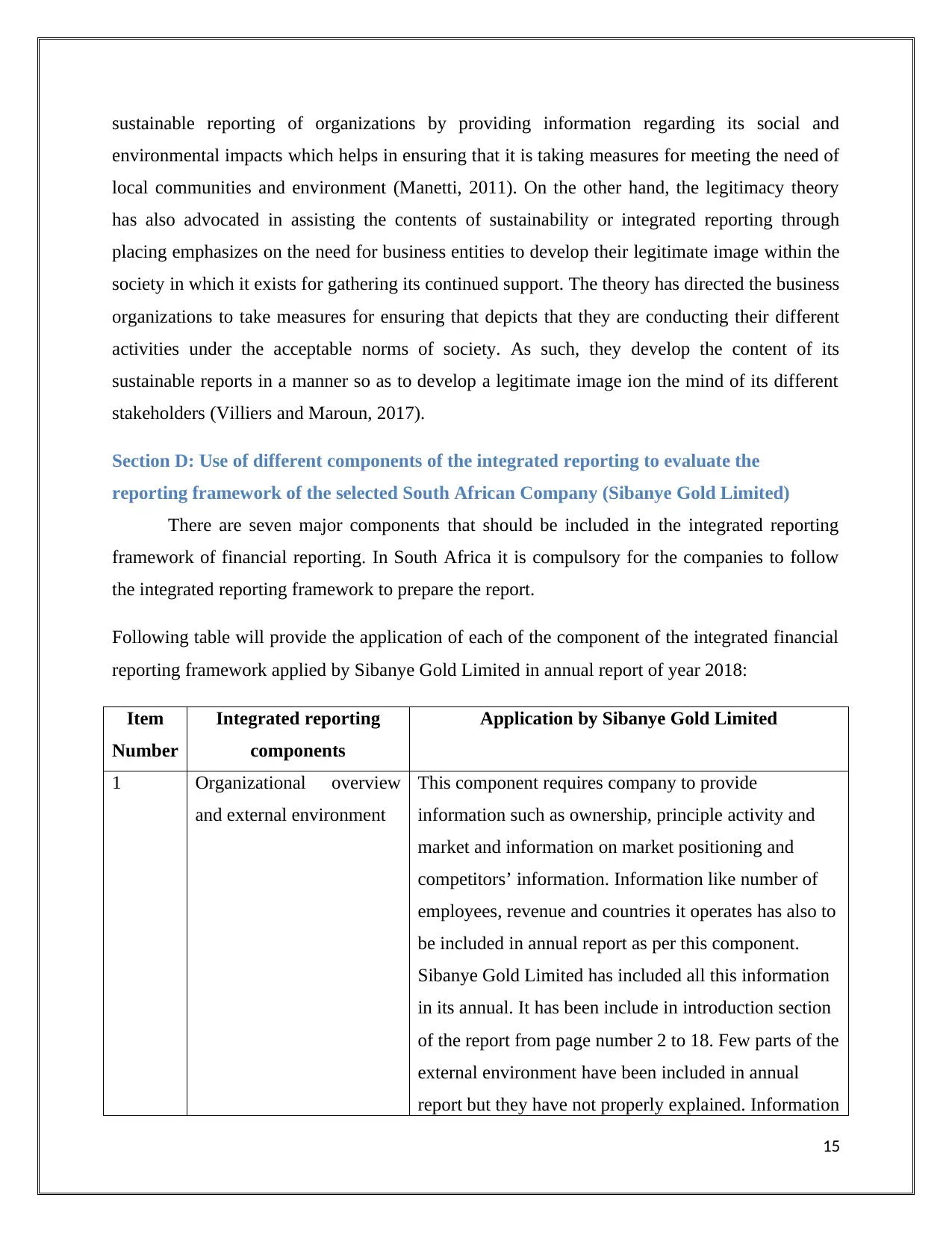

Section D: Use of different components of the integrated reporting to evaluate the

reporting framework of the selected South African Company (Sibanye Gold Limited)

There are seven major components that should be included in the integrated reporting

framework of financial reporting. In South Africa it is compulsory for the companies to follow

the integrated reporting framework to prepare the report.

Following table will provide the application of each of the component of the integrated financial

reporting framework applied by Sibanye Gold Limited in annual report of year 2018:

Item

Number

Integrated reporting

components

Application by Sibanye Gold Limited

1 Organizational overview

and external environment

This component requires company to provide

information such as ownership, principle activity and

market and information on market positioning and

competitors’ information. Information like number of

employees, revenue and countries it operates has also to

be included in annual report as per this component.

Sibanye Gold Limited has included all this information

in its annual. It has been include in introduction section

of the report from page number 2 to 18. Few parts of the

external environment have been included in annual

report but they have not properly explained. Information

15

environmental impacts which helps in ensuring that it is taking measures for meeting the need of

local communities and environment (Manetti, 2011). On the other hand, the legitimacy theory

has also advocated in assisting the contents of sustainability or integrated reporting through

placing emphasizes on the need for business entities to develop their legitimate image within the

society in which it exists for gathering its continued support. The theory has directed the business

organizations to take measures for ensuring that depicts that they are conducting their different

activities under the acceptable norms of society. As such, they develop the content of its

sustainable reports in a manner so as to develop a legitimate image ion the mind of its different

stakeholders (Villiers and Maroun, 2017).

Section D: Use of different components of the integrated reporting to evaluate the

reporting framework of the selected South African Company (Sibanye Gold Limited)

There are seven major components that should be included in the integrated reporting

framework of financial reporting. In South Africa it is compulsory for the companies to follow

the integrated reporting framework to prepare the report.

Following table will provide the application of each of the component of the integrated financial

reporting framework applied by Sibanye Gold Limited in annual report of year 2018:

Item

Number

Integrated reporting

components

Application by Sibanye Gold Limited

1 Organizational overview

and external environment

This component requires company to provide

information such as ownership, principle activity and

market and information on market positioning and

competitors’ information. Information like number of

employees, revenue and countries it operates has also to

be included in annual report as per this component.

Sibanye Gold Limited has included all this information

in its annual. It has been include in introduction section

of the report from page number 2 to 18. Few parts of the

external environment have been included in annual

report but they have not properly explained. Information

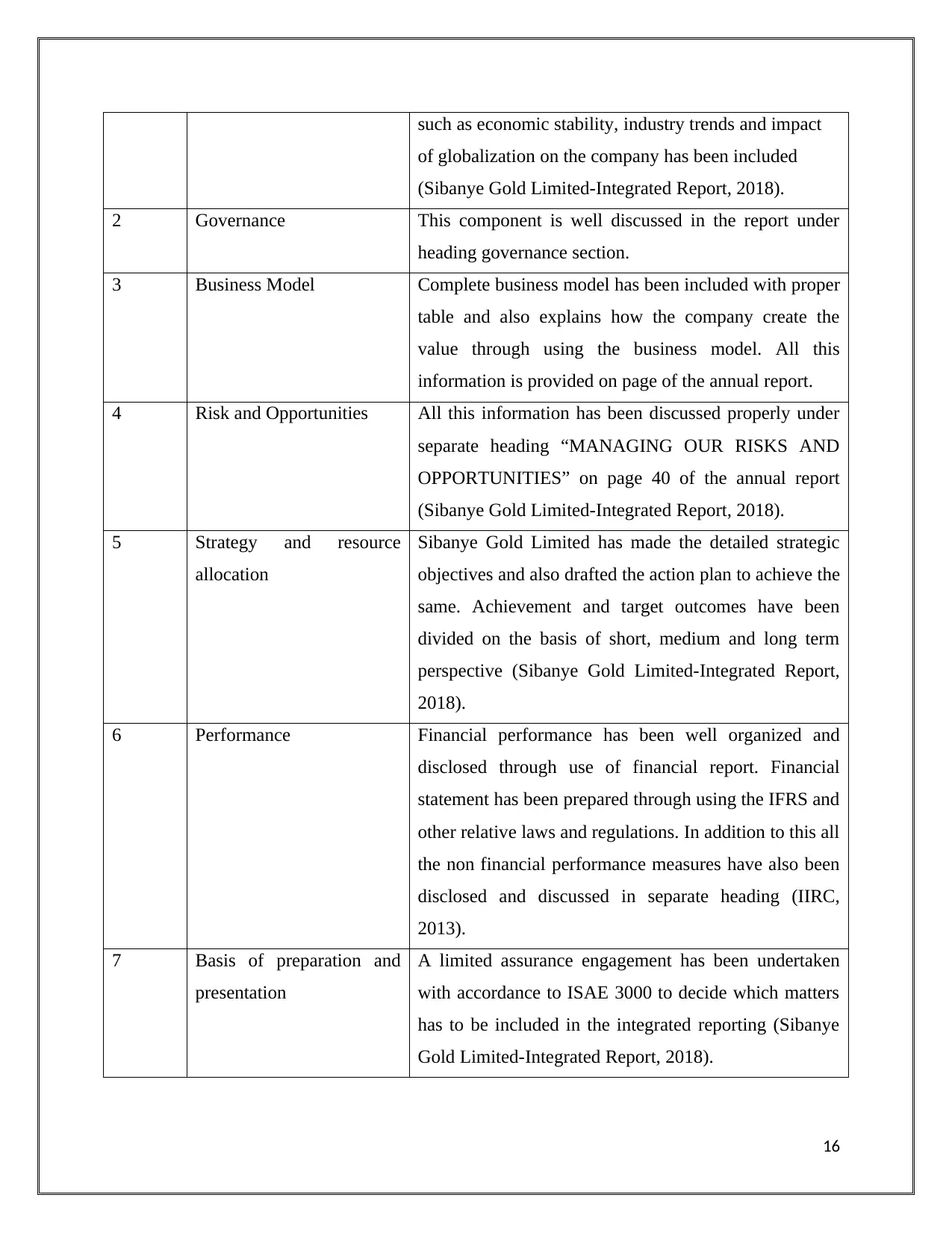

15

such as economic stability, industry trends and impact

of globalization on the company has been included

(Sibanye Gold Limited-Integrated Report, 2018).

2 Governance This component is well discussed in the report under

heading governance section.

3 Business Model Complete business model has been included with proper

table and also explains how the company create the

value through using the business model. All this

information is provided on page of the annual report.

4 Risk and Opportunities All this information has been discussed properly under

separate heading “MANAGING OUR RISKS AND

OPPORTUNITIES” on page 40 of the annual report

(Sibanye Gold Limited-Integrated Report, 2018).

5 Strategy and resource

allocation

Sibanye Gold Limited has made the detailed strategic

objectives and also drafted the action plan to achieve the

same. Achievement and target outcomes have been

divided on the basis of short, medium and long term

perspective (Sibanye Gold Limited-Integrated Report,

2018).

6 Performance Financial performance has been well organized and

disclosed through use of financial report. Financial

statement has been prepared through using the IFRS and

other relative laws and regulations. In addition to this all

the non financial performance measures have also been

disclosed and discussed in separate heading (IIRC,

2013).

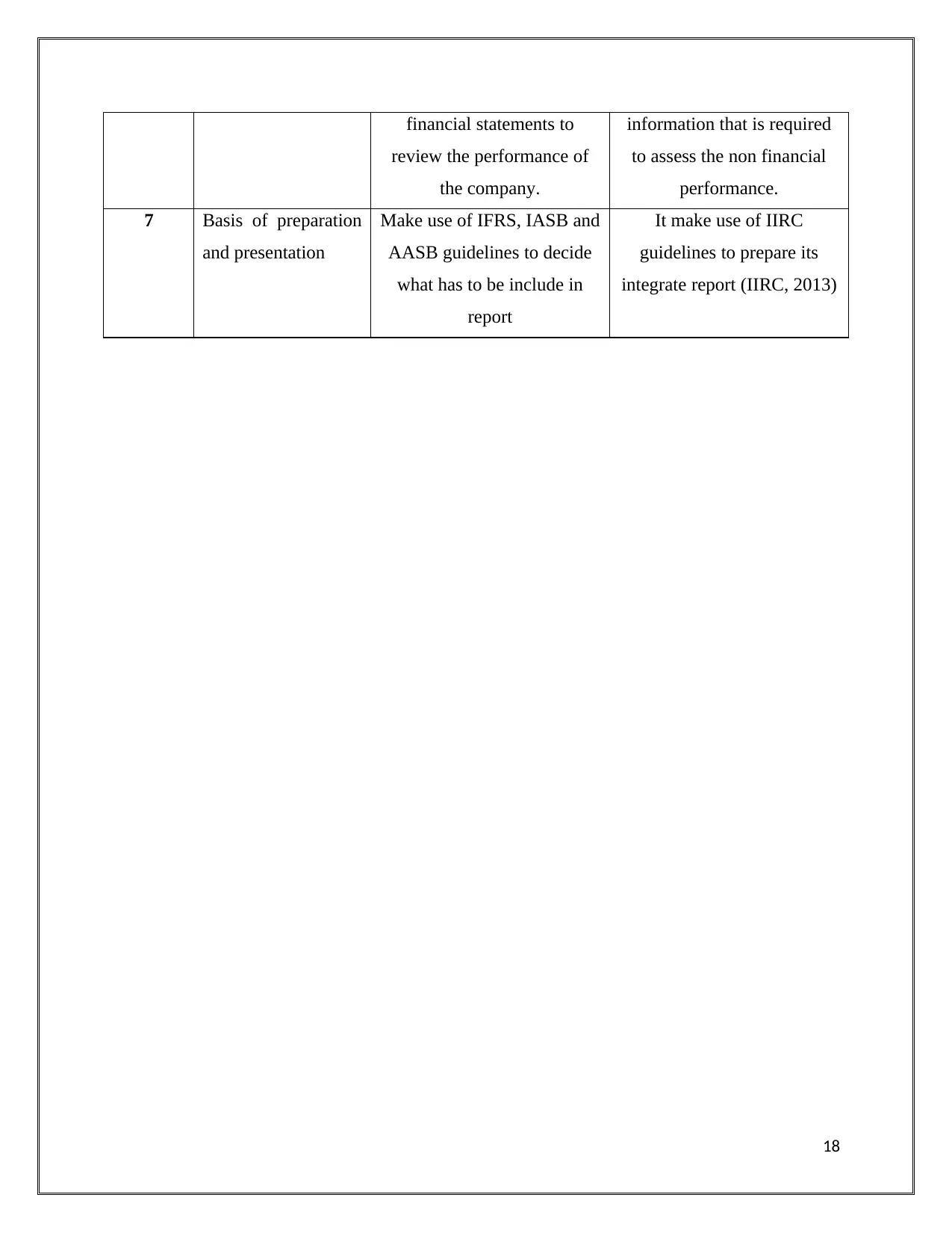

7 Basis of preparation and

presentation

A limited assurance engagement has been undertaken

with accordance to ISAE 3000 to decide which matters

has to be included in the integrated reporting (Sibanye

Gold Limited-Integrated Report, 2018).

16

of globalization on the company has been included

(Sibanye Gold Limited-Integrated Report, 2018).

2 Governance This component is well discussed in the report under

heading governance section.

3 Business Model Complete business model has been included with proper

table and also explains how the company create the

value through using the business model. All this

information is provided on page of the annual report.

4 Risk and Opportunities All this information has been discussed properly under

separate heading “MANAGING OUR RISKS AND

OPPORTUNITIES” on page 40 of the annual report

(Sibanye Gold Limited-Integrated Report, 2018).

5 Strategy and resource

allocation

Sibanye Gold Limited has made the detailed strategic

objectives and also drafted the action plan to achieve the

same. Achievement and target outcomes have been

divided on the basis of short, medium and long term

perspective (Sibanye Gold Limited-Integrated Report,

2018).

6 Performance Financial performance has been well organized and

disclosed through use of financial report. Financial

statement has been prepared through using the IFRS and

other relative laws and regulations. In addition to this all

the non financial performance measures have also been

disclosed and discussed in separate heading (IIRC,

2013).

7 Basis of preparation and

presentation

A limited assurance engagement has been undertaken

with accordance to ISAE 3000 to decide which matters

has to be included in the integrated reporting (Sibanye

Gold Limited-Integrated Report, 2018).

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Section E: Comparison of reporting practices by Australian Company and South African

Company

On evaluating the annual report of Austal Group Limited (Australian Company) it has

been found this company does not prepare the integrated report but it produce other reports such

as corporate governance report for reporting the corporate social responsibility. There is no

report produce by the company to report on the sustainability performance (ASX Announcement,

2018).

Comparison of contents of reports prepared by Australian Company with the index

integrated report of South African Company

Number

s

Components Australian Company South African Company

1 Organizational

overview and

external environment

Very few information is

included such as company

performance, overview,

employees detail but failed to

provide discussion on

external environment.

Both parts has been

discussed.

2 Governance Only corporate governance

has been included (Corporate

Governance, 2018)

All parts of governance has

been included in the report

3 Business Model Not included Included separately

4 Risk and

Opportunities

Not included in its reports Discussed properly

5 Strategy and

resource allocation

No such information is

provided in its reports

Well discussed in table

format so that it is easy to

understand.

6 Performance Only financial performance

in included in its annual

report and some part of

corporate governance is

included. It only contains

This report provides

complete performance

overview in its integrated

report. It has financial

statements and all other

17

Company

On evaluating the annual report of Austal Group Limited (Australian Company) it has

been found this company does not prepare the integrated report but it produce other reports such

as corporate governance report for reporting the corporate social responsibility. There is no

report produce by the company to report on the sustainability performance (ASX Announcement,

2018).

Comparison of contents of reports prepared by Australian Company with the index

integrated report of South African Company

Number

s

Components Australian Company South African Company

1 Organizational

overview and

external environment

Very few information is

included such as company

performance, overview,

employees detail but failed to

provide discussion on

external environment.

Both parts has been

discussed.

2 Governance Only corporate governance

has been included (Corporate

Governance, 2018)

All parts of governance has

been included in the report

3 Business Model Not included Included separately

4 Risk and

Opportunities

Not included in its reports Discussed properly

5 Strategy and

resource allocation

No such information is

provided in its reports

Well discussed in table

format so that it is easy to

understand.

6 Performance Only financial performance

in included in its annual

report and some part of

corporate governance is

included. It only contains

This report provides

complete performance

overview in its integrated

report. It has financial

statements and all other

17

financial statements to

review the performance of

the company.

information that is required

to assess the non financial

performance.

7 Basis of preparation

and presentation

Make use of IFRS, IASB and

AASB guidelines to decide

what has to be include in

report

It make use of IIRC

guidelines to prepare its

integrate report (IIRC, 2013)

18

review the performance of

the company.

information that is required

to assess the non financial

performance.

7 Basis of preparation

and presentation

Make use of IFRS, IASB and

AASB guidelines to decide

what has to be include in

report

It make use of IIRC

guidelines to prepare its

integrate report (IIRC, 2013)

18

Conclusion

The report has inferred that CF for financial reporting has been developed to enrich the

integrity within the development and presentation of financial statements. However, there have

been various challenges faced by business entities in Australia and other countries for adopting

the CF for developing financial reports. It has also emphasized on the difference between global

reporting initiative standards and the integrated reporting framework standards for the

development of sustainable reports. There has been development of separate framework to

develop the sustainable reports due to inadequacy of conventional accounting practices in

disclosures of information relating to social and environmental performance.

19

The report has inferred that CF for financial reporting has been developed to enrich the

integrity within the development and presentation of financial statements. However, there have

been various challenges faced by business entities in Australia and other countries for adopting

the CF for developing financial reports. It has also emphasized on the difference between global

reporting initiative standards and the integrated reporting framework standards for the

development of sustainable reports. There has been development of separate framework to

develop the sustainable reports due to inadequacy of conventional accounting practices in

disclosures of information relating to social and environmental performance.

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

AASB adoption of IASB standards by 2005. (2004). Retrieved June 2, 2019, from

https://www.aasb.gov.au/admin/file/content102/c3/Background_to_AASB_adoption_of_

IASB_standards_by_2005.pdf

ASX Announcement. (2018). Retrieved June 3, 2019, from http://investor.austal.com/news-

releases?a9aa094b_year%5Bvalue%5D=2018

Austal Group-Annual Report. (2018). Retrieved June 3, 2019, from

http://investor.austal.com/static-files/6aa9d4f2-2a67-4416-a56c-dbf792a15f09

Barth, M.E. (2008). Global Financial Reporting: Implications for U.S. Academics. Accounting

Review, 83(5), pp. 1159-1179.

Chua, Y. Chee S. and Cheong, G.C. (2012). The Impact of Mandatory IFRS Adoption on

Accounting Quality: Evidence from Australia. Journal of International Accounting

Research: Spring, 11(1), pp. 119-146.

Conceptual Framework. (2018). IFRS Foundation. Retrieved June 3, 2019, from

https://www.ifrs.org/-/media/project/conceptual-framework/fact-sheet-project-summary-

and-feedback-statement/conceptual-framework-project-summary.pdf

Corporate Governance. (2018). Austal Group. Retrieved June 3, 2019, from

http://investor.austal.com/corporate-governance/highlights

Dean, G. and Clarke, F. (2003). An Evolving Conceptual Framework. Abacus, 39(3), pp. 279-

283.

Dragomir, V.D. (2011). Accounting for Sustainability: the quest for a conceptual framework. Int.

J. Critical Accounting 3 (4), pp. 385-397.

Faisal, F., Tower, G. and Rusmin, R. (2012). Legitimising Corporate Sustainability Reporting

Throughout the World. Australasian Accounting, Business and Finance Journal, 6(2),

pp.19-34.

20

AASB adoption of IASB standards by 2005. (2004). Retrieved June 2, 2019, from

https://www.aasb.gov.au/admin/file/content102/c3/Background_to_AASB_adoption_of_

IASB_standards_by_2005.pdf

ASX Announcement. (2018). Retrieved June 3, 2019, from http://investor.austal.com/news-

releases?a9aa094b_year%5Bvalue%5D=2018

Austal Group-Annual Report. (2018). Retrieved June 3, 2019, from

http://investor.austal.com/static-files/6aa9d4f2-2a67-4416-a56c-dbf792a15f09

Barth, M.E. (2008). Global Financial Reporting: Implications for U.S. Academics. Accounting

Review, 83(5), pp. 1159-1179.

Chua, Y. Chee S. and Cheong, G.C. (2012). The Impact of Mandatory IFRS Adoption on

Accounting Quality: Evidence from Australia. Journal of International Accounting

Research: Spring, 11(1), pp. 119-146.

Conceptual Framework. (2018). IFRS Foundation. Retrieved June 3, 2019, from

https://www.ifrs.org/-/media/project/conceptual-framework/fact-sheet-project-summary-

and-feedback-statement/conceptual-framework-project-summary.pdf

Corporate Governance. (2018). Austal Group. Retrieved June 3, 2019, from

http://investor.austal.com/corporate-governance/highlights

Dean, G. and Clarke, F. (2003). An Evolving Conceptual Framework. Abacus, 39(3), pp. 279-

283.

Dragomir, V.D. (2011). Accounting for Sustainability: the quest for a conceptual framework. Int.

J. Critical Accounting 3 (4), pp. 385-397.

Faisal, F., Tower, G. and Rusmin, R. (2012). Legitimising Corporate Sustainability Reporting

Throughout the World. Australasian Accounting, Business and Finance Journal, 6(2),

pp.19-34.

20

Fajard, C.L. (2016). Convergence of Accounting Standards World Wide - An Update. Journal of

Applied Business and Economics, 18(6), pp. 1-13.

GRI. (2017). GRI works with IIRC and leading companies to eliminate reporting confusion.

Retrieved 2 June, 2019, from https://www.globalreporting.org/information/news-and-

press-center/Pages/GRI-works-with-IIRC-and-leading-companies-to-eliminate-reporting-

confusion.aspx

IIRC. (2013). The International <IR> Framework. Retrieved 2 June, 2019, from

http://integratedreporting.org/wp-content/uploads/2015/03/13-12-08-THE-

INTERNATIONAL-IR-FRAMEWORK-2-1.pdf

Information Resources. (2015). Business Law and Ethics: Concepts, Methodologies, Tools, and

Applications: Concepts, Methodologies, Tools, and Applications.US: IGI Global.

Ivan, O. (2009). Sustainability in accounting – basis: a conceptual framework. Annales

Universitatis Apulensis Series Oeconomica, 11(1), pp.106-116.

Lonergan, W. (2005). The emasculation of accounting standard setting in Australia. Retrieved

June 2, 2019, from https://www.finsia.com/docs/default-source/jassa-new/jassa-

2003/3_2003_emasculation_accounting.pdf?sfvrsn=4b28de93_6

Macías, M., and Muiño, F. (2011). “Examining dual accounting systems in Europe,” The

International Journal of Accounting, 46(1), pp. 51–78.

Manetti, G. (2011). The quality of stakeholder engagement in sustainability reporting: Empirical

evidence and critical points. Corporate Social Responsibility and Environmental

Management, 18(2), pp.110–122.

Pacter, P. (2013). “What Have IASB and FASB Convergence Efforts Achieved?” Journal of

Accountancy 215 (2).

Seng, T.B. (2014). IASB Conceptual Framework: what busy CPAs need to know. Retrieved June

3, 2019, from http://app1.hkicpa.org.hk/APLUS/2014/06/pdf/44_Large_Source.pdf

21

Applied Business and Economics, 18(6), pp. 1-13.

GRI. (2017). GRI works with IIRC and leading companies to eliminate reporting confusion.

Retrieved 2 June, 2019, from https://www.globalreporting.org/information/news-and-

press-center/Pages/GRI-works-with-IIRC-and-leading-companies-to-eliminate-reporting-

confusion.aspx

IIRC. (2013). The International <IR> Framework. Retrieved 2 June, 2019, from

http://integratedreporting.org/wp-content/uploads/2015/03/13-12-08-THE-

INTERNATIONAL-IR-FRAMEWORK-2-1.pdf

Information Resources. (2015). Business Law and Ethics: Concepts, Methodologies, Tools, and

Applications: Concepts, Methodologies, Tools, and Applications.US: IGI Global.

Ivan, O. (2009). Sustainability in accounting – basis: a conceptual framework. Annales

Universitatis Apulensis Series Oeconomica, 11(1), pp.106-116.

Lonergan, W. (2005). The emasculation of accounting standard setting in Australia. Retrieved

June 2, 2019, from https://www.finsia.com/docs/default-source/jassa-new/jassa-

2003/3_2003_emasculation_accounting.pdf?sfvrsn=4b28de93_6

Macías, M., and Muiño, F. (2011). “Examining dual accounting systems in Europe,” The

International Journal of Accounting, 46(1), pp. 51–78.

Manetti, G. (2011). The quality of stakeholder engagement in sustainability reporting: Empirical

evidence and critical points. Corporate Social Responsibility and Environmental

Management, 18(2), pp.110–122.

Pacter, P. (2013). “What Have IASB and FASB Convergence Efforts Achieved?” Journal of

Accountancy 215 (2).

Seng, T.B. (2014). IASB Conceptual Framework: what busy CPAs need to know. Retrieved June

3, 2019, from http://app1.hkicpa.org.hk/APLUS/2014/06/pdf/44_Large_Source.pdf

21

Sibanye Gold Limited-Integrated Report. (2018). Retrieved June 3, 2019, from

https://www.sibanyestillwater.com/investors/financial-reporting/annual-reports/2018

Silvia, A. (2016). “Cautiousness on convergence of accounting standards across countries.”

Corporate Communications: An International Journal 21 (3), pp.246-267.

The IIRC. (2017). Corporate Reporting Dialogue. Retrieved 2 June, 2019, from

https://integratedreporting.org/corporate-reporting-dialogue/

Tschopp, D. and Nastanski, M. (2014). The harmonization and convergence of corporate social

responsibility reporting standards. Journal of Business Ethics 125, pp.147-162.

Villiers, C. and Maroun, W. (2017). Sustainability Accounting and Integrated Reporting. US:

Routledge.

Wong, P. (2004). Challenges and Successes in Implementing International Standards: Achieving

Convergence to IFRSS and ISAS. Retrieved June 3, 2019, from

http://www.cimaglobal.com/Documents/ImportedDocuments/ifac_report_challengesucce

ss_111004.pdf

22

https://www.sibanyestillwater.com/investors/financial-reporting/annual-reports/2018

Silvia, A. (2016). “Cautiousness on convergence of accounting standards across countries.”

Corporate Communications: An International Journal 21 (3), pp.246-267.

The IIRC. (2017). Corporate Reporting Dialogue. Retrieved 2 June, 2019, from

https://integratedreporting.org/corporate-reporting-dialogue/

Tschopp, D. and Nastanski, M. (2014). The harmonization and convergence of corporate social

responsibility reporting standards. Journal of Business Ethics 125, pp.147-162.

Villiers, C. and Maroun, W. (2017). Sustainability Accounting and Integrated Reporting. US:

Routledge.

Wong, P. (2004). Challenges and Successes in Implementing International Standards: Achieving

Convergence to IFRSS and ISAS. Retrieved June 3, 2019, from

http://www.cimaglobal.com/Documents/ImportedDocuments/ifac_report_challengesucce

ss_111004.pdf

22

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.