CQUniversity Auditing and Ethics Report: ACCT20075 Analysis

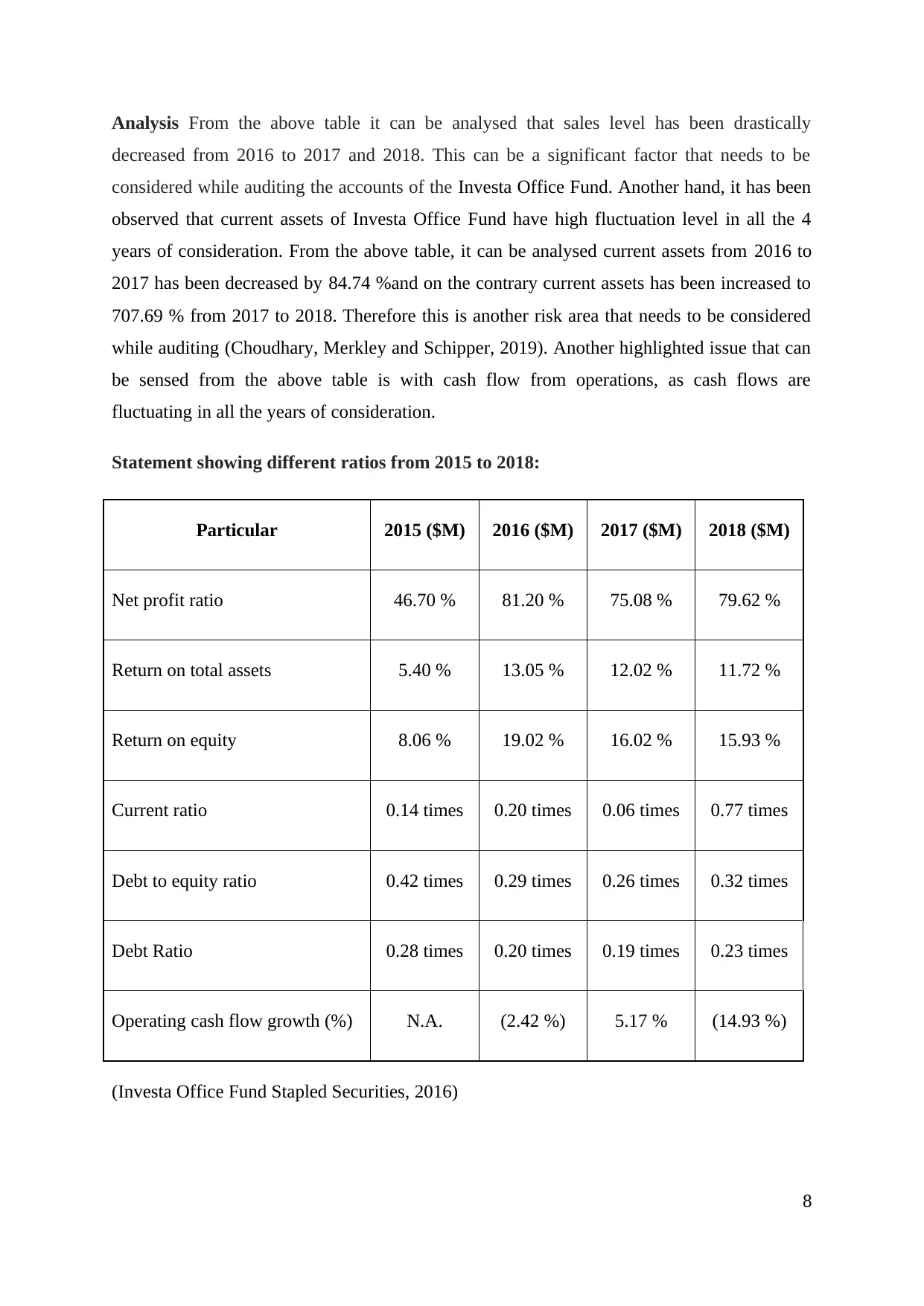

VerifiedAdded on 2023/03/17

|15

|2925

|85

Report

AI Summary

This report presents an analysis of an auditing assignment for ACCT20075, focusing on the financial statements of Investa Office Fund. The report begins with an introduction to auditing and then delves into the calculation and analysis of planning materiality, crucial for identifying material errors an...

ACCT20075 – Auditing and Ethic

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

Section 1- Planning materiality and contingencies....................................................................4

Calculation and analysis of planning materiality...................................................................4

Significant events from auditors perspective.........................................................................5

Section 2.....................................................................................................................................6

Section 3.....................................................................................................................................7

Cash flow activities................................................................................................................7

Primary cash receipts and cash payments..............................................................................7

Non-cash financing and investing activities...........................................................................7

Evaluation of going concern concept.....................................................................................7

Audit opinion..........................................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

2

Introduction................................................................................................................................3

Section 1- Planning materiality and contingencies....................................................................4

Calculation and analysis of planning materiality...................................................................4

Significant events from auditors perspective.........................................................................5

Section 2.....................................................................................................................................6

Section 3.....................................................................................................................................7

Cash flow activities................................................................................................................7

Primary cash receipts and cash payments..............................................................................7

Non-cash financing and investing activities...........................................................................7

Evaluation of going concern concept.....................................................................................7

Audit opinion..........................................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

2

Introduction

Auditing is the service in which various aspects of business operations and different process

are being analysed and tested. Audit and assurance service majorly analysis financial position

and business operations of the undertaken company. In this report, different aspects of

auditing have been applied and finding is reported. Investa Office Fund is the business

organisation that has been undertaken for applying different audit and assurance services.

Investa Office Fund is an ASX listed business organisation and core business operation is to

get renting office buildings and receiving rent as consideration. In this report, the financial

statement of Investa Office Fund has been considered and on that basis, audit planning has

proceeded. Firstly, the materiality level of the number of items of financial statements has

been determined. Then, financial statement analysis has been conducted to identify major risk

accounts or factors of Investa Office Fund. Cash transactions taken place during 2018 has

been analysed i.e. primary cash receipts and cash payments in this report. In the last section,

auditor’s audit opinion of 2018 has been analysed.

3

Auditing is the service in which various aspects of business operations and different process

are being analysed and tested. Audit and assurance service majorly analysis financial position

and business operations of the undertaken company. In this report, different aspects of

auditing have been applied and finding is reported. Investa Office Fund is the business

organisation that has been undertaken for applying different audit and assurance services.

Investa Office Fund is an ASX listed business organisation and core business operation is to

get renting office buildings and receiving rent as consideration. In this report, the financial

statement of Investa Office Fund has been considered and on that basis, audit planning has

proceeded. Firstly, the materiality level of the number of items of financial statements has

been determined. Then, financial statement analysis has been conducted to identify major risk

accounts or factors of Investa Office Fund. Cash transactions taken place during 2018 has

been analysed i.e. primary cash receipts and cash payments in this report. In the last section,

auditor’s audit opinion of 2018 has been analysed.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 1- Planning materiality and contingencies

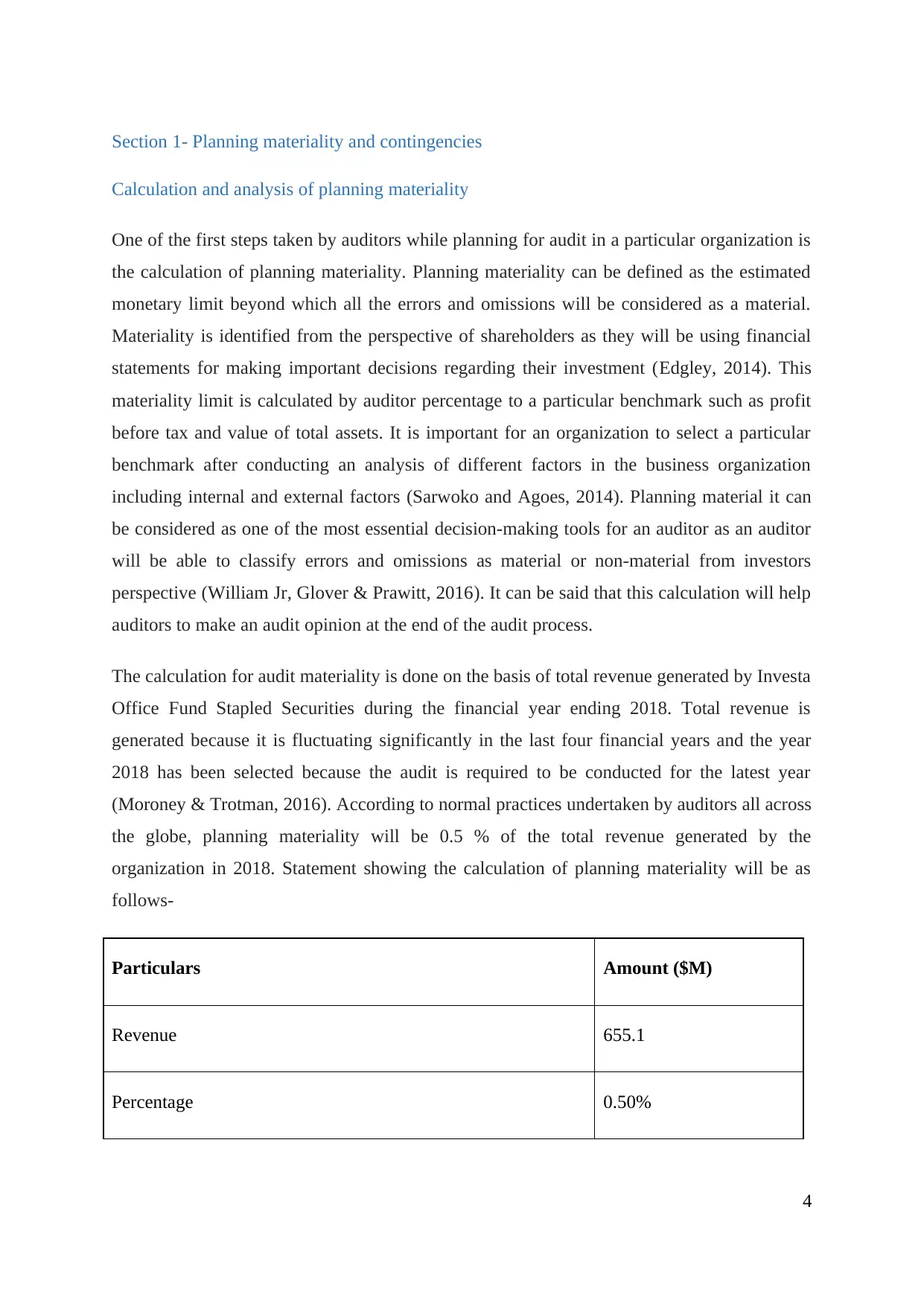

Calculation and analysis of planning materiality

One of the first steps taken by auditors while planning for audit in a particular organization is

the calculation of planning materiality. Planning materiality can be defined as the estimated

monetary limit beyond which all the errors and omissions will be considered as a material.

Materiality is identified from the perspective of shareholders as they will be using financial

statements for making important decisions regarding their investment (Edgley, 2014). This

materiality limit is calculated by auditor percentage to a particular benchmark such as profit

before tax and value of total assets. It is important for an organization to select a particular

benchmark after conducting an analysis of different factors in the business organization

including internal and external factors (Sarwoko and Agoes, 2014). Planning material it can

be considered as one of the most essential decision-making tools for an auditor as an auditor

will be able to classify errors and omissions as material or non-material from investors

perspective (William Jr, Glover & Prawitt, 2016). It can be said that this calculation will help

auditors to make an audit opinion at the end of the audit process.

The calculation for audit materiality is done on the basis of total revenue generated by Investa

Office Fund Stapled Securities during the financial year ending 2018. Total revenue is

generated because it is fluctuating significantly in the last four financial years and the year

2018 has been selected because the audit is required to be conducted for the latest year

(Moroney & Trotman, 2016). According to normal practices undertaken by auditors all across

the globe, planning materiality will be 0.5 % of the total revenue generated by the

organization in 2018. Statement showing the calculation of planning materiality will be as

follows-

Particulars Amount ($M)

Revenue 655.1

Percentage 0.50%

4

Calculation and analysis of planning materiality

One of the first steps taken by auditors while planning for audit in a particular organization is

the calculation of planning materiality. Planning materiality can be defined as the estimated

monetary limit beyond which all the errors and omissions will be considered as a material.

Materiality is identified from the perspective of shareholders as they will be using financial

statements for making important decisions regarding their investment (Edgley, 2014). This

materiality limit is calculated by auditor percentage to a particular benchmark such as profit

before tax and value of total assets. It is important for an organization to select a particular

benchmark after conducting an analysis of different factors in the business organization

including internal and external factors (Sarwoko and Agoes, 2014). Planning material it can

be considered as one of the most essential decision-making tools for an auditor as an auditor

will be able to classify errors and omissions as material or non-material from investors

perspective (William Jr, Glover & Prawitt, 2016). It can be said that this calculation will help

auditors to make an audit opinion at the end of the audit process.

The calculation for audit materiality is done on the basis of total revenue generated by Investa

Office Fund Stapled Securities during the financial year ending 2018. Total revenue is

generated because it is fluctuating significantly in the last four financial years and the year

2018 has been selected because the audit is required to be conducted for the latest year

(Moroney & Trotman, 2016). According to normal practices undertaken by auditors all across

the globe, planning materiality will be 0.5 % of the total revenue generated by the

organization in 2018. Statement showing the calculation of planning materiality will be as

follows-

Particulars Amount ($M)

Revenue 655.1

Percentage 0.50%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

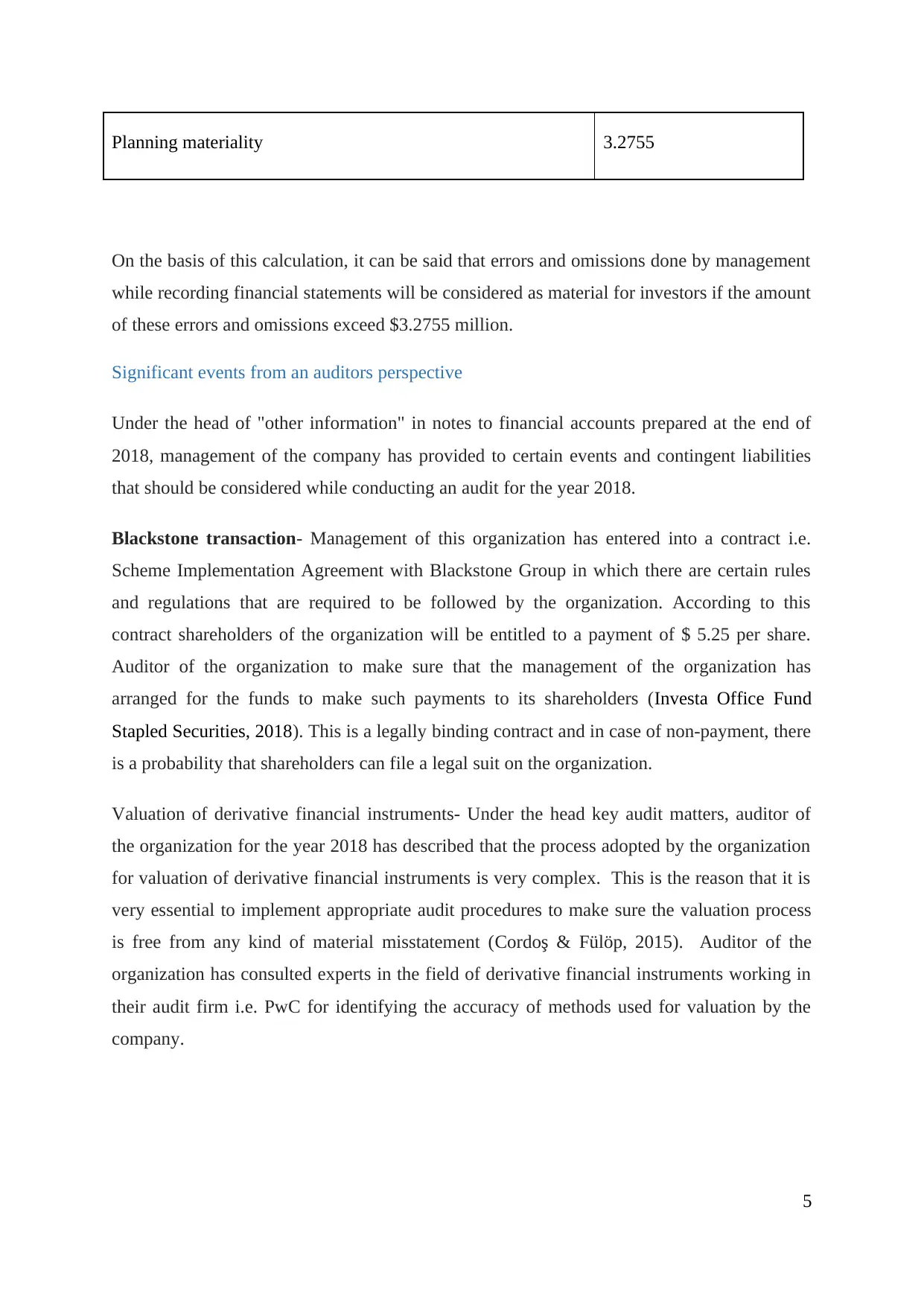

Planning materiality 3.2755

On the basis of this calculation, it can be said that errors and omissions done by management

while recording financial statements will be considered as material for investors if the amount

of these errors and omissions exceed $3.2755 million.

Significant events from an auditors perspective

Under the head of "other information" in notes to financial accounts prepared at the end of

2018, management of the company has provided to certain events and contingent liabilities

that should be considered while conducting an audit for the year 2018.

Blackstone transaction- Management of this organization has entered into a contract i.e.

Scheme Implementation Agreement with Blackstone Group in which there are certain rules

and regulations that are required to be followed by the organization. According to this

contract shareholders of the organization will be entitled to a payment of $ 5.25 per share.

Auditor of the organization to make sure that the management of the organization has

arranged for the funds to make such payments to its shareholders (Investa Office Fund

Stapled Securities, 2018). This is a legally binding contract and in case of non-payment, there

is a probability that shareholders can file a legal suit on the organization.

Valuation of derivative financial instruments- Under the head key audit matters, auditor of

the organization for the year 2018 has described that the process adopted by the organization

for valuation of derivative financial instruments is very complex. This is the reason that it is

very essential to implement appropriate audit procedures to make sure the valuation process

is free from any kind of material misstatement (Cordoş & Fülöp, 2015). Auditor of the

organization has consulted experts in the field of derivative financial instruments working in

their audit firm i.e. PwC for identifying the accuracy of methods used for valuation by the

company.

5

On the basis of this calculation, it can be said that errors and omissions done by management

while recording financial statements will be considered as material for investors if the amount

of these errors and omissions exceed $3.2755 million.

Significant events from an auditors perspective

Under the head of "other information" in notes to financial accounts prepared at the end of

2018, management of the company has provided to certain events and contingent liabilities

that should be considered while conducting an audit for the year 2018.

Blackstone transaction- Management of this organization has entered into a contract i.e.

Scheme Implementation Agreement with Blackstone Group in which there are certain rules

and regulations that are required to be followed by the organization. According to this

contract shareholders of the organization will be entitled to a payment of $ 5.25 per share.

Auditor of the organization to make sure that the management of the organization has

arranged for the funds to make such payments to its shareholders (Investa Office Fund

Stapled Securities, 2018). This is a legally binding contract and in case of non-payment, there

is a probability that shareholders can file a legal suit on the organization.

Valuation of derivative financial instruments- Under the head key audit matters, auditor of

the organization for the year 2018 has described that the process adopted by the organization

for valuation of derivative financial instruments is very complex. This is the reason that it is

very essential to implement appropriate audit procedures to make sure the valuation process

is free from any kind of material misstatement (Cordoş & Fülöp, 2015). Auditor of the

organization has consulted experts in the field of derivative financial instruments working in

their audit firm i.e. PwC for identifying the accuracy of methods used for valuation by the

company.

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

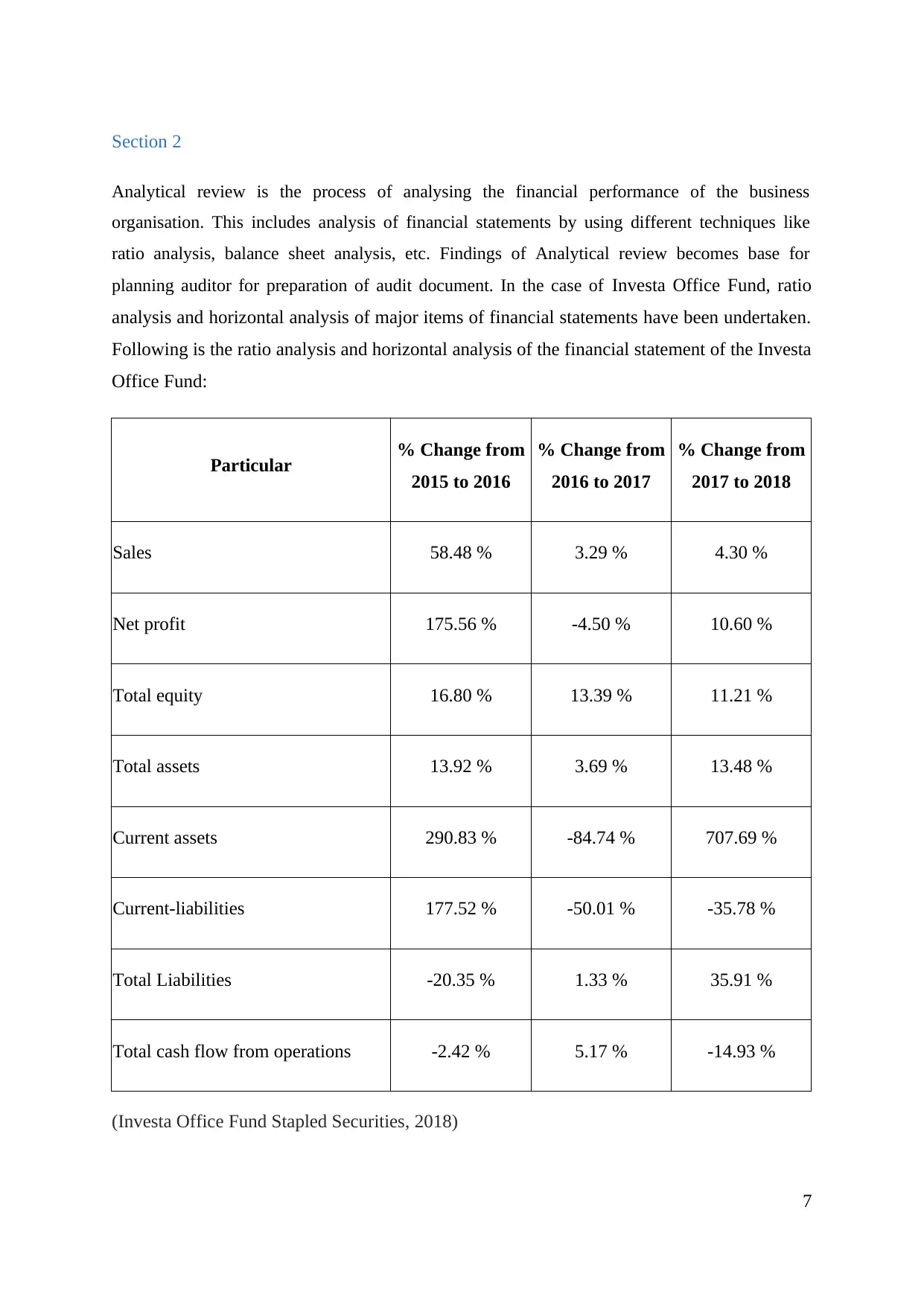

Section 2

Analytical review is the process of analysing the financial performance of the business

organisation. This includes analysis of financial statements by using different techniques like

ratio analysis, balance sheet analysis, etc. Findings of Analytical review becomes base for

planning auditor for preparation of audit document. In the case of Investa Office Fund, ratio

analysis and horizontal analysis of major items of financial statements have been undertaken.

Following is the ratio analysis and horizontal analysis of the financial statement of the Investa

Office Fund:

Particular % Change from

2015 to 2016

% Change from

2016 to 2017

% Change from

2017 to 2018

Sales 58.48 % 3.29 % 4.30 %

Net profit 175.56 % -4.50 % 10.60 %

Total equity 16.80 % 13.39 % 11.21 %

Total assets 13.92 % 3.69 % 13.48 %

Current assets 290.83 % -84.74 % 707.69 %

Current-liabilities 177.52 % -50.01 % -35.78 %

Total Liabilities -20.35 % 1.33 % 35.91 %

Total cash flow from operations -2.42 % 5.17 % -14.93 %

(Investa Office Fund Stapled Securities, 2018)

7

Analytical review is the process of analysing the financial performance of the business

organisation. This includes analysis of financial statements by using different techniques like

ratio analysis, balance sheet analysis, etc. Findings of Analytical review becomes base for

planning auditor for preparation of audit document. In the case of Investa Office Fund, ratio

analysis and horizontal analysis of major items of financial statements have been undertaken.

Following is the ratio analysis and horizontal analysis of the financial statement of the Investa

Office Fund:

Particular % Change from

2015 to 2016

% Change from

2016 to 2017

% Change from

2017 to 2018

Sales 58.48 % 3.29 % 4.30 %

Net profit 175.56 % -4.50 % 10.60 %

Total equity 16.80 % 13.39 % 11.21 %

Total assets 13.92 % 3.69 % 13.48 %

Current assets 290.83 % -84.74 % 707.69 %

Current-liabilities 177.52 % -50.01 % -35.78 %

Total Liabilities -20.35 % 1.33 % 35.91 %

Total cash flow from operations -2.42 % 5.17 % -14.93 %

(Investa Office Fund Stapled Securities, 2018)

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis From the above table it can be analysed that sales level has been drastically

decreased from 2016 to 2017 and 2018. This can be a significant factor that needs to be

considered while auditing the accounts of the Investa Office Fund. Another hand, it has been

observed that current assets of Investa Office Fund have high fluctuation level in all the 4

years of consideration. From the above table, it can be analysed current assets from 2016 to

2017 has been decreased by 84.74 %and on the contrary current assets has been increased to

707.69 % from 2017 to 2018. Therefore this is another risk area that needs to be considered

while auditing (Choudhary, Merkley and Schipper, 2019). Another highlighted issue that can

be sensed from the above table is with cash flow from operations, as cash flows are

fluctuating in all the years of consideration.

Statement showing different ratios from 2015 to 2018:

Particular 2015 ($M) 2016 ($M) 2017 ($M) 2018 ($M)

Net profit ratio 46.70 % 81.20 % 75.08 % 79.62 %

Return on total assets 5.40 % 13.05 % 12.02 % 11.72 %

Return on equity 8.06 % 19.02 % 16.02 % 15.93 %

Current ratio 0.14 times 0.20 times 0.06 times 0.77 times

Debt to equity ratio 0.42 times 0.29 times 0.26 times 0.32 times

Debt Ratio 0.28 times 0.20 times 0.19 times 0.23 times

Operating cash flow growth (%) N.A. (2.42 %) 5.17 % (14.93 %)

(Investa Office Fund Stapled Securities, 2016)

8

decreased from 2016 to 2017 and 2018. This can be a significant factor that needs to be

considered while auditing the accounts of the Investa Office Fund. Another hand, it has been

observed that current assets of Investa Office Fund have high fluctuation level in all the 4

years of consideration. From the above table, it can be analysed current assets from 2016 to

2017 has been decreased by 84.74 %and on the contrary current assets has been increased to

707.69 % from 2017 to 2018. Therefore this is another risk area that needs to be considered

while auditing (Choudhary, Merkley and Schipper, 2019). Another highlighted issue that can

be sensed from the above table is with cash flow from operations, as cash flows are

fluctuating in all the years of consideration.

Statement showing different ratios from 2015 to 2018:

Particular 2015 ($M) 2016 ($M) 2017 ($M) 2018 ($M)

Net profit ratio 46.70 % 81.20 % 75.08 % 79.62 %

Return on total assets 5.40 % 13.05 % 12.02 % 11.72 %

Return on equity 8.06 % 19.02 % 16.02 % 15.93 %

Current ratio 0.14 times 0.20 times 0.06 times 0.77 times

Debt to equity ratio 0.42 times 0.29 times 0.26 times 0.32 times

Debt Ratio 0.28 times 0.20 times 0.19 times 0.23 times

Operating cash flow growth (%) N.A. (2.42 %) 5.17 % (14.93 %)

(Investa Office Fund Stapled Securities, 2016)

8

From the above table, it can be analysed that liquidity is a major risk factor in the audit of the

Investa Office Fund. Since their current ratio is less than 1time in all the four years. Matters

to be addressed while auditing is related to verifying cash balances and obtaining balance

confirmation of debtor’s accounts. Relevant assertions that need to be considered are

accuracy i.e. to verify that cash transactions are recorded with the correct amount and all cash

transactions are recorded accurately. In the case of debtors, accuracy assertion will be applied

to access the correct amount of debtors are recorded or not. Occurrence assertion will be

applied while verifying debtors balance i.e. sales actually took place with the correct debtor

or not will be analysed (Chambers and Odar, 2015).

Audit procedure: cash receipts and cash payment will be verified from invoices. Nature of

cash receipt and payment will be analysed by considering the nature of the transaction. In the

case of debtors, external confirmation procedure will be used to access correctness of amount

and occurrence of a transaction.

Another risk factor is of operational efficiency in which net foreign exchange loss has been

highlighted in the income statement. In 2018, Investa Office Fund has $ 17.6 million net

foreign exchange loss which is quite a big amount. In 2017, there was no such loss. This has

also reduced overall profitability and if it is not correctly calculated then this will also reduce

income tax liability. Therefore, it becomes a key risk factor and analysis of amount involved

is the matter to be considered while auditing. Existence, accuracy, classification and

occurrence are some assertions that need to be considered while auditing.

Audit procedures: In order to the occurrence, business transactions are to be verified and

checked in terms of amount and place of incidence. For classification assertion, all the points

that make a transaction foreign exchange transaction will be applied on reported transactions.

For accuracy assertion, documents related to foreign transactions will be verified and should

be cross-checked with second parties involved in the transaction. Therefore external

confirmations are to be taken (Kachelmeier, Schmidt and Valentine, 2017). For existence

assertion, external confirmation procedure will be used to confirm the same.

9

Investa Office Fund. Since their current ratio is less than 1time in all the four years. Matters

to be addressed while auditing is related to verifying cash balances and obtaining balance

confirmation of debtor’s accounts. Relevant assertions that need to be considered are

accuracy i.e. to verify that cash transactions are recorded with the correct amount and all cash

transactions are recorded accurately. In the case of debtors, accuracy assertion will be applied

to access the correct amount of debtors are recorded or not. Occurrence assertion will be

applied while verifying debtors balance i.e. sales actually took place with the correct debtor

or not will be analysed (Chambers and Odar, 2015).

Audit procedure: cash receipts and cash payment will be verified from invoices. Nature of

cash receipt and payment will be analysed by considering the nature of the transaction. In the

case of debtors, external confirmation procedure will be used to access correctness of amount

and occurrence of a transaction.

Another risk factor is of operational efficiency in which net foreign exchange loss has been

highlighted in the income statement. In 2018, Investa Office Fund has $ 17.6 million net

foreign exchange loss which is quite a big amount. In 2017, there was no such loss. This has

also reduced overall profitability and if it is not correctly calculated then this will also reduce

income tax liability. Therefore, it becomes a key risk factor and analysis of amount involved

is the matter to be considered while auditing. Existence, accuracy, classification and

occurrence are some assertions that need to be considered while auditing.

Audit procedures: In order to the occurrence, business transactions are to be verified and

checked in terms of amount and place of incidence. For classification assertion, all the points

that make a transaction foreign exchange transaction will be applied on reported transactions.

For accuracy assertion, documents related to foreign transactions will be verified and should

be cross-checked with second parties involved in the transaction. Therefore external

confirmations are to be taken (Kachelmeier, Schmidt and Valentine, 2017). For existence

assertion, external confirmation procedure will be used to confirm the same.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 3

Cash flow activities

One of the most important components of the financial statement is the statement of cash

flow which represents a summary of cash activities undertaken by the organization in a

particular accounting period. At the end of the financial year, 2018 summary of cash

activities during the twelve months has been represented and divided into three categories for

better analysis and representation i.e. cash inflow-outflow from investing, financing and

operating activities (Kroes & Manikas, 2014). According to this cash flow statement total

cash outflow in the year 2018 is $0.3 million whereas it was an inflow of $1.9 million cash in

the year 2017. Total contribution from operating activity, financing activity and investing

activity in this net cash outflow was $129.9 million, -$118.7 million and -$11.5 million

(Investa Office Fund Stapled Securities, 2018). Therefore it can be said that the biggest

contributor to cash flow activities is operating activities as total inflow from operating

activities is highest in the year 2018.

Primary cash receipts and cash payments

Primary cash flows are for Investa Office Fund has been taken from the cash flow statement

of 2018. Cash flows are mainly from 3 activities i.e. operating, financing and investing

activities. Following statement showing different cash flows of Investa Office Fund during

2018:

Particulars Amount

Primary cash receipts

Receipts from customers (inclusive of GST) $ 247 million

Proceeds from borrowings $ 594 million

Primary cash Payments

10

Cash flow activities

One of the most important components of the financial statement is the statement of cash

flow which represents a summary of cash activities undertaken by the organization in a

particular accounting period. At the end of the financial year, 2018 summary of cash

activities during the twelve months has been represented and divided into three categories for

better analysis and representation i.e. cash inflow-outflow from investing, financing and

operating activities (Kroes & Manikas, 2014). According to this cash flow statement total

cash outflow in the year 2018 is $0.3 million whereas it was an inflow of $1.9 million cash in

the year 2017. Total contribution from operating activity, financing activity and investing

activity in this net cash outflow was $129.9 million, -$118.7 million and -$11.5 million

(Investa Office Fund Stapled Securities, 2018). Therefore it can be said that the biggest

contributor to cash flow activities is operating activities as total inflow from operating

activities is highest in the year 2018.

Primary cash receipts and cash payments

Primary cash flows are for Investa Office Fund has been taken from the cash flow statement

of 2018. Cash flows are mainly from 3 activities i.e. operating, financing and investing

activities. Following statement showing different cash flows of Investa Office Fund during

2018:

Particulars Amount

Primary cash receipts

Receipts from customers (inclusive of GST) $ 247 million

Proceeds from borrowings $ 594 million

Primary cash Payments

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payments to suppliers (inclusive of GST) $ 89.60 million

Payments for additions to investment

properties

$ 118.70 million

Repayments of borrowings $ 412 million

Distributions paid to unitholders $ 123.4 million

Non-cash financing and investing activities

Activities undertaken by the business organization in relation to investing and financing that

does not involve any inflow-outflow of cash. For example bonus shares issued to business,

organization would be considered as a financing activity but it would not be considered as a

cash financing activity if the bonus is issued out of reserves (Robinson, Henry, Pirie &

Broihahn, 2015). There are no such activities undertaken by the organization in the year 2018

according to the particulars provided in annual reports.

Evaluation of going concern concept

Auditor of the organization has considered the following factors while evaluating going

concern of Investa Office Fund Stapled Securities-

The decrease in a total number of customers and revenue of the organization as

compared to previous financial years.

Unavailability of working capital

A higher proportion of long term loans in the organization.

Unable to make payments in relation to interest and the principal amount of debt

(Amin, Krishnan & Yang, 2014).

11

Payments for additions to investment

properties

$ 118.70 million

Repayments of borrowings $ 412 million

Distributions paid to unitholders $ 123.4 million

Non-cash financing and investing activities

Activities undertaken by the business organization in relation to investing and financing that

does not involve any inflow-outflow of cash. For example bonus shares issued to business,

organization would be considered as a financing activity but it would not be considered as a

cash financing activity if the bonus is issued out of reserves (Robinson, Henry, Pirie &

Broihahn, 2015). There are no such activities undertaken by the organization in the year 2018

according to the particulars provided in annual reports.

Evaluation of going concern concept

Auditor of the organization has considered the following factors while evaluating going

concern of Investa Office Fund Stapled Securities-

The decrease in a total number of customers and revenue of the organization as

compared to previous financial years.

Unavailability of working capital

A higher proportion of long term loans in the organization.

Unable to make payments in relation to interest and the principal amount of debt

(Amin, Krishnan & Yang, 2014).

11

After evaluating these factors in Investa Office Fund Stapled Securities, it can be said that

there is no risk associated with going concern concept in the organization.

Audit opinion

Auditor of the organization has given an unmodified opinion to the financial statements of

Investa Office Fund Stapled Securities stating that financial statements are representing the

true and fair value of the business position.

12

there is no risk associated with going concern concept in the organization.

Audit opinion

Auditor of the organization has given an unmodified opinion to the financial statements of

Investa Office Fund Stapled Securities stating that financial statements are representing the

true and fair value of the business position.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Conclusion

An overall conclusion it can be said that the planning process of audit is very essential to

make sure that there are no material misstatements in financial statements. This report has

conducted a ratio analysis for Investa Office Fund Stapled Securities to identify major

problems with the business operations. The main focus of this report was on conducting an

evaluation of auditor report issued by auditors on the financial year ending 2018. On the basis

of analysing audit report and annual report, it can be said that management has followed

every rule and regulation during the process of preparing financial statements.

13

An overall conclusion it can be said that the planning process of audit is very essential to

make sure that there are no material misstatements in financial statements. This report has

conducted a ratio analysis for Investa Office Fund Stapled Securities to identify major

problems with the business operations. The main focus of this report was on conducting an

evaluation of auditor report issued by auditors on the financial year ending 2018. On the basis

of analysing audit report and annual report, it can be said that management has followed

every rule and regulation during the process of preparing financial statements.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Amin, K., Krishnan, J., & Yang, J. S. (2014). Going concern opinion and cost of

equity. Auditing: A Journal of Practice & Theory, 33(4), 1-39.

Chambers, A. D., & Odar, M. (2015). A new vision for internal audit. Managerial Auditing

Journal, 30(1), 34-55.

Choudhary, P., Merkley, K. J., & Schipper, K. (2019). Auditors’ quantitative materiality

judgments: Properties and implications for financial reporting reliability. In 28th

Annual Conference on Financial Economics and Accounting.

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction

of Key Audit Matters. Accounting & Management Information Systems/Contabilitate

si Informatica de Gestiune, 14(1).

Edgley, C. (2014). A genealogy of accounting materiality. Critical Perspectives on

Accounting, 25(3), 255-271.

Investa Office Fund Stapled Securities. (2016). Annual report 2015-2016. Retrievable at:

https://www.investa.com.au/www_investa/media/resources/presentations/iof/iof-fy16-

annual-financial-report.pdf

Investa Office Fund Stapled Securities. (2018). Annual Report 2018. Retrievable at:

https://www.investa.com.au/funds/oipp/iof-archive/performance-periodic-statement/reports-

presentations

Kachelmeier, S. J., Schmidt, J. J., & Valentine, K. (2017). The disclaimer effect of disclosing

critical audit matters in the auditor’s report. Working paper.

Kroes, J. R., & Manikas, A. S. (2014). Cash flow management and manufacturing firm

financial performance: A longitudinal perspective. International Journal of Production

Economics, 148, 37-50.

14

Amin, K., Krishnan, J., & Yang, J. S. (2014). Going concern opinion and cost of

equity. Auditing: A Journal of Practice & Theory, 33(4), 1-39.

Chambers, A. D., & Odar, M. (2015). A new vision for internal audit. Managerial Auditing

Journal, 30(1), 34-55.

Choudhary, P., Merkley, K. J., & Schipper, K. (2019). Auditors’ quantitative materiality

judgments: Properties and implications for financial reporting reliability. In 28th

Annual Conference on Financial Economics and Accounting.

Cordoş, G. S., & Fülöp, M. T. (2015). Understanding audit reporting changes: introduction

of Key Audit Matters. Accounting & Management Information Systems/Contabilitate

si Informatica de Gestiune, 14(1).

Edgley, C. (2014). A genealogy of accounting materiality. Critical Perspectives on

Accounting, 25(3), 255-271.

Investa Office Fund Stapled Securities. (2016). Annual report 2015-2016. Retrievable at:

https://www.investa.com.au/www_investa/media/resources/presentations/iof/iof-fy16-

annual-financial-report.pdf

Investa Office Fund Stapled Securities. (2018). Annual Report 2018. Retrievable at:

https://www.investa.com.au/funds/oipp/iof-archive/performance-periodic-statement/reports-

presentations

Kachelmeier, S. J., Schmidt, J. J., & Valentine, K. (2017). The disclaimer effect of disclosing

critical audit matters in the auditor’s report. Working paper.

Kroes, J. R., & Manikas, A. S. (2014). Cash flow management and manufacturing firm

financial performance: A longitudinal perspective. International Journal of Production

Economics, 148, 37-50.

14

Moroney, R., & Trotman, K. T. (2016). Differences in auditors' materiality assessments when

auditing financial statements and sustainability reports. Contemporary Accounting

Research, 33(2), 551-575.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

Sarwoko, & Agoes. (2014). An Empirical Analysis of Auditor's Industry Specialization,

Auditor's Independence and Audit Procedures on Audit Quality: Evidence from

Indonesia. Procedia - Social and Behavioral Sciences, 164(C), 271-281.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

15

auditing financial statements and sustainability reports. Contemporary Accounting

Research, 33(2), 551-575.

Robinson, T. R., Henry, E., Pirie, W. L., & Broihahn, M. A. (2015). International financial

statement analysis. John Wiley & Sons.

Sarwoko, & Agoes. (2014). An Empirical Analysis of Auditor's Industry Specialization,

Auditor's Independence and Audit Procedures on Audit Quality: Evidence from

Indonesia. Procedia - Social and Behavioral Sciences, 164(C), 271-281.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.