ACCTG 211 Assignment 2 Answer Booklet

VerifiedAdded on 2023/06/14

|7

|1401

|485

AI Summary

This ACCTG 211 Assignment 2 Answer Booklet includes Statement of Cash Flows for Henk Ltd, Jack Ltd, Melanie Ltd and Damian Ltd. It also covers the impact of legal system on accounting and partial statement of cash flows for Damian Ltd.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Family Name:

First names: AUID number:

Note:

ASSIGNMENT 2 ANSWER BOOKLET (14 pages)

This assignment is due online by 6 pm* on Friday 16th March 2018. *Do not submit at exactly

6 pm as it will be recorded as being late, i.e., it will not be accepted for marking.

It is your responsibility to ensure the Assignment 2 Answer Booklet is successfully submitted,

the format is not changed, it is downloadable and readable by the ACCTG 211 markers.

QUESTION 1

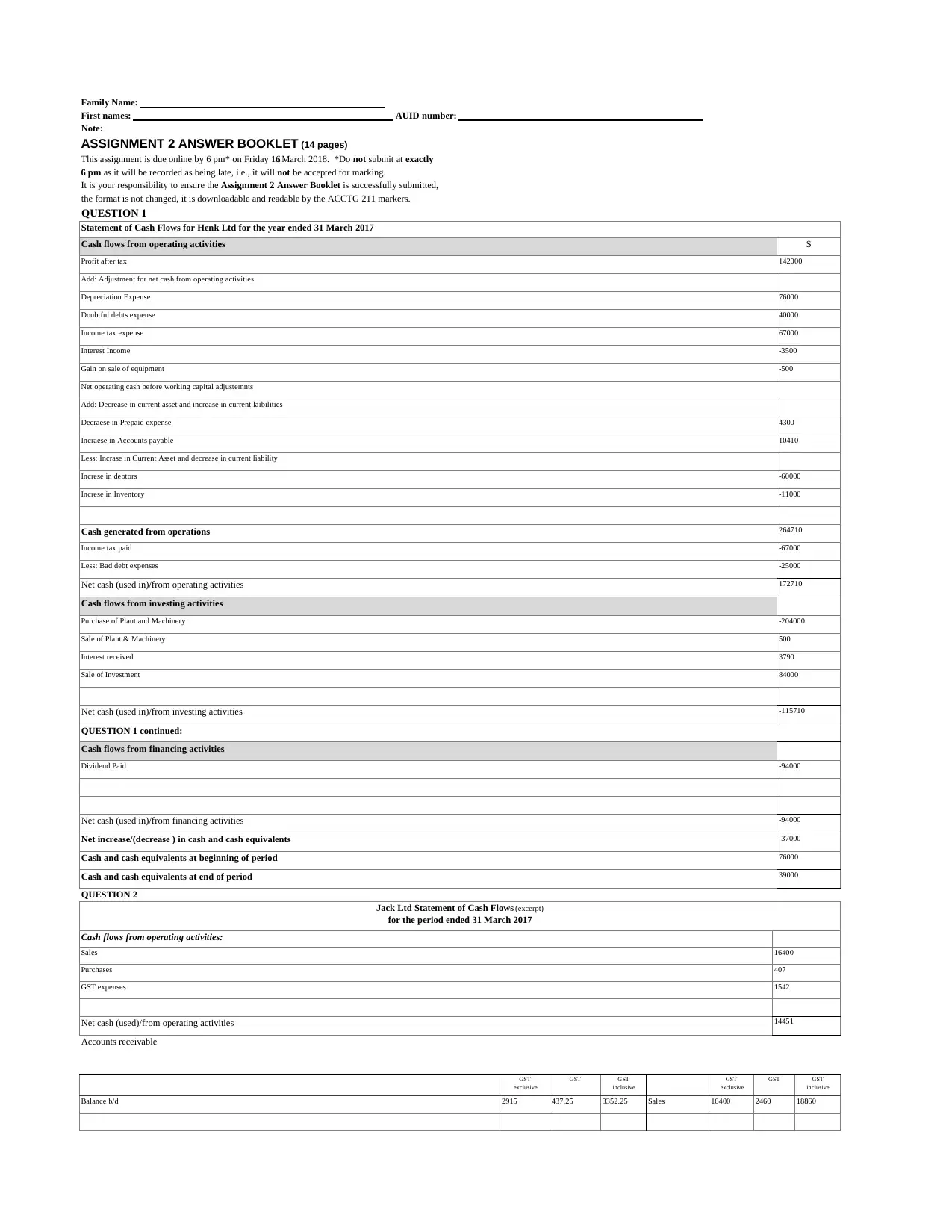

Statement of Cash Flows for Henk Ltd for the year ended 31 March 2017

QUESTION 2

Accounts receivable

GST

inclusive

Balance b/d 18860

Cash flows from operating activities $

Profit after tax 142000

Add: Adjustment for net cash from operating activities

Depreciation Expense 76000

Doubtful debts expense 40000

Income tax expense 67000

Interest Income -3500

Gain on sale of equipment -500

Net operating cash before working capital adjustemnts

Add: Decrease in current asset and increase in current laibilities

Decraese in Prepaid expense 4300

Incraese in Accounts payable 10410

Less: Incrase in Current Asset and decrease in current liability

Increse in debtors -60000

Increse in Inventory -11000

Cash generated from operations 264710

Income tax paid -67000

Less: Bad debt expenses -25000

Net cash (used in)/from operating activities 172710

Cash flows from investing activities

Purchase of Plant and Machinery -204000

Sale of Plant & Machinery 500

Interest received 3790

Sale of Investment 84000

Net cash (used in)/from investing activities -115710

QUESTION 1 continued:

Cash flows from financing activities

Dividend Paid -94000

Net cash (used in)/from financing activities -94000

Net increase/(decrease ) in cash and cash equivalents -37000

Cash and cash equivalents at beginning of period 76000

Cash and cash equivalents at end of period 39000

Jack Ltd Statement of Cash Flows (excerpt)

for the period ended 31 March 2017

Cash flows from operating activities:

Sales 16400

Purchases 407

GST expenses 1542

Net cash (used)/from operating activities 14451

GST

exclusive

GST GST

inclusive

GST

exclusive

GST

2915 437.25 3352.25 Sales 16400 2460

First names: AUID number:

Note:

ASSIGNMENT 2 ANSWER BOOKLET (14 pages)

This assignment is due online by 6 pm* on Friday 16th March 2018. *Do not submit at exactly

6 pm as it will be recorded as being late, i.e., it will not be accepted for marking.

It is your responsibility to ensure the Assignment 2 Answer Booklet is successfully submitted,

the format is not changed, it is downloadable and readable by the ACCTG 211 markers.

QUESTION 1

Statement of Cash Flows for Henk Ltd for the year ended 31 March 2017

QUESTION 2

Accounts receivable

GST

inclusive

Balance b/d 18860

Cash flows from operating activities $

Profit after tax 142000

Add: Adjustment for net cash from operating activities

Depreciation Expense 76000

Doubtful debts expense 40000

Income tax expense 67000

Interest Income -3500

Gain on sale of equipment -500

Net operating cash before working capital adjustemnts

Add: Decrease in current asset and increase in current laibilities

Decraese in Prepaid expense 4300

Incraese in Accounts payable 10410

Less: Incrase in Current Asset and decrease in current liability

Increse in debtors -60000

Increse in Inventory -11000

Cash generated from operations 264710

Income tax paid -67000

Less: Bad debt expenses -25000

Net cash (used in)/from operating activities 172710

Cash flows from investing activities

Purchase of Plant and Machinery -204000

Sale of Plant & Machinery 500

Interest received 3790

Sale of Investment 84000

Net cash (used in)/from investing activities -115710

QUESTION 1 continued:

Cash flows from financing activities

Dividend Paid -94000

Net cash (used in)/from financing activities -94000

Net increase/(decrease ) in cash and cash equivalents -37000

Cash and cash equivalents at beginning of period 76000

Cash and cash equivalents at end of period 39000

Jack Ltd Statement of Cash Flows (excerpt)

for the period ended 31 March 2017

Cash flows from operating activities:

Sales 16400

Purchases 407

GST expenses 1542

Net cash (used)/from operating activities 14451

GST

exclusive

GST GST

inclusive

GST

exclusive

GST

2915 437.25 3352.25 Sales 16400 2460

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

3036

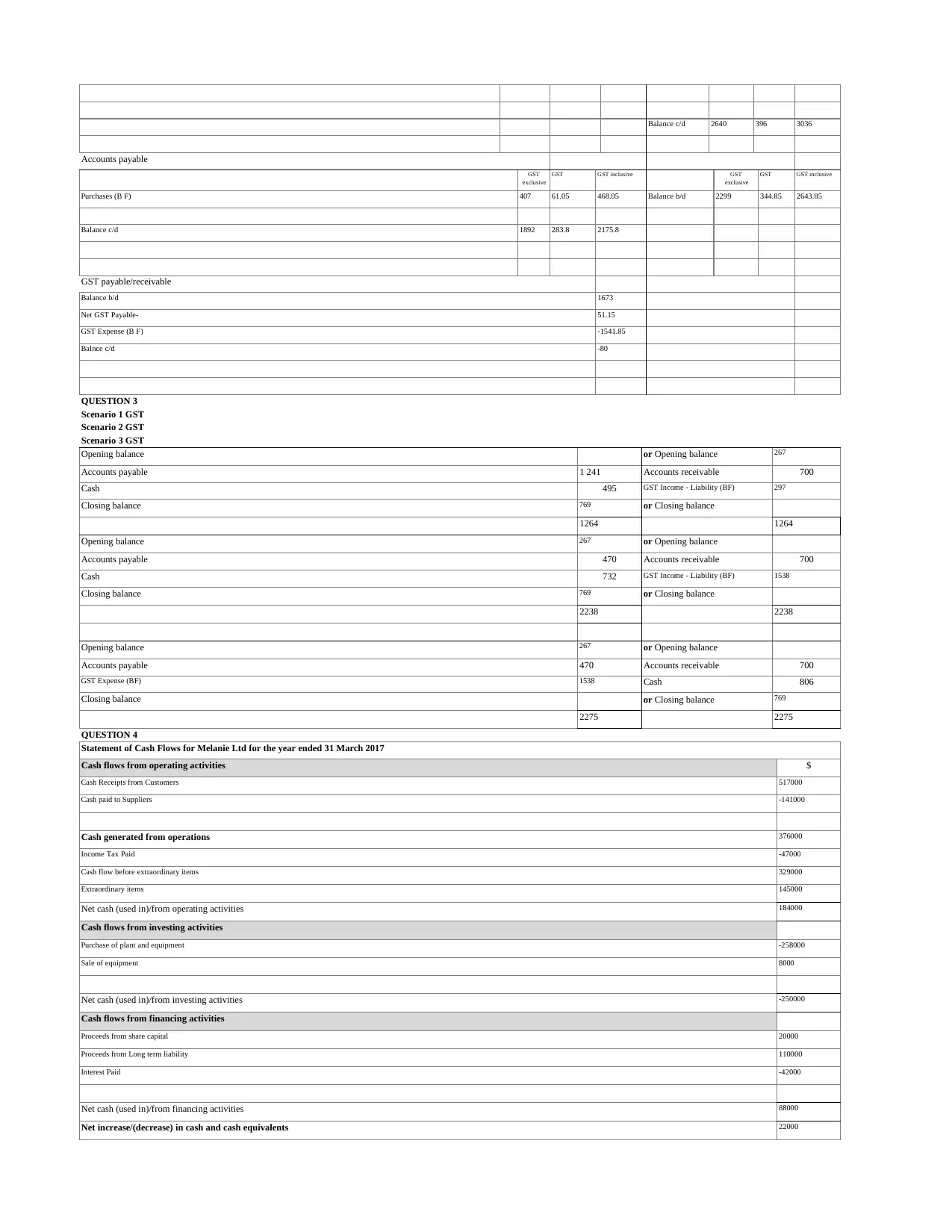

Accounts payable

GST

exclusive

GST inclusive

407 2643.85

1892

GST payable/receivable

QUESTION 3

Scenario 1 GST

Scenario 2 GST

Scenario 3 GST

QUESTION 4

Balance c/d 2640 396

GST GST inclusive GST

exclusive

GST

Purchases (B F) 61.05 468.05 Balance b/d 2299 344.85

Balance c/d 283.8 2175.8

Balance b/d 1673

Net GST Payable- 51.15

GST Expense (B F) -1541.85

Balnce c/d -80

Opening balance or Opening balance 267

Accounts payable 1 241 Accounts receivable 700

Cash 495 GST Income - Liability (BF) 297

Closing balance 769 or Closing balance

1264 1264

Opening balance 267 or Opening balance

Accounts payable 470 Accounts receivable 700

Cash 732 GST Income - Liability (BF) 1538

Closing balance 769 or Closing balance

2238 2238

Opening balance 267 or Opening balance

Accounts payable 470 Accounts receivable 700

GST Expense (BF) 1538 Cash 806

Closing balance or Closing balance 769

2275 2275

Statement of Cash Flows for Melanie Ltd for the year ended 31 March 2017

Cash flows from operating activities $

Cash Receipts from Customers 517000

Cash paid to Suppliers -141000

Cash generated from operations 376000

Income Tax Paid -47000

Cash flow before extraordinary items 329000

Extraordinary items 145000

Net cash (used in)/from operating activities 184000

Cash flows from investing activities

Purchase of plant and equipment -258000

Sale of equipment 8000

Net cash (used in)/from investing activities -250000

Cash flows from financing activities

Proceeds from share capital 20000

Proceeds from Long term liability 110000

Interest Paid -42000

Net cash (used in)/from financing activities 88000

Net increase/(decrease) in cash and cash equivalents 22000

Accounts payable

GST

exclusive

GST inclusive

407 2643.85

1892

GST payable/receivable

QUESTION 3

Scenario 1 GST

Scenario 2 GST

Scenario 3 GST

QUESTION 4

Balance c/d 2640 396

GST GST inclusive GST

exclusive

GST

Purchases (B F) 61.05 468.05 Balance b/d 2299 344.85

Balance c/d 283.8 2175.8

Balance b/d 1673

Net GST Payable- 51.15

GST Expense (B F) -1541.85

Balnce c/d -80

Opening balance or Opening balance 267

Accounts payable 1 241 Accounts receivable 700

Cash 495 GST Income - Liability (BF) 297

Closing balance 769 or Closing balance

1264 1264

Opening balance 267 or Opening balance

Accounts payable 470 Accounts receivable 700

Cash 732 GST Income - Liability (BF) 1538

Closing balance 769 or Closing balance

2238 2238

Opening balance 267 or Opening balance

Accounts payable 470 Accounts receivable 700

GST Expense (BF) 1538 Cash 806

Closing balance or Closing balance 769

2275 2275

Statement of Cash Flows for Melanie Ltd for the year ended 31 March 2017

Cash flows from operating activities $

Cash Receipts from Customers 517000

Cash paid to Suppliers -141000

Cash generated from operations 376000

Income Tax Paid -47000

Cash flow before extraordinary items 329000

Extraordinary items 145000

Net cash (used in)/from operating activities 184000

Cash flows from investing activities

Purchase of plant and equipment -258000

Sale of equipment 8000

Net cash (used in)/from investing activities -250000

Cash flows from financing activities

Proceeds from share capital 20000

Proceeds from Long term liability 110000

Interest Paid -42000

Net cash (used in)/from financing activities 88000

Net increase/(decrease) in cash and cash equivalents 22000

QUESTION 4 continued:

QUESTION 5

QUESTION 6

QUESTION 7

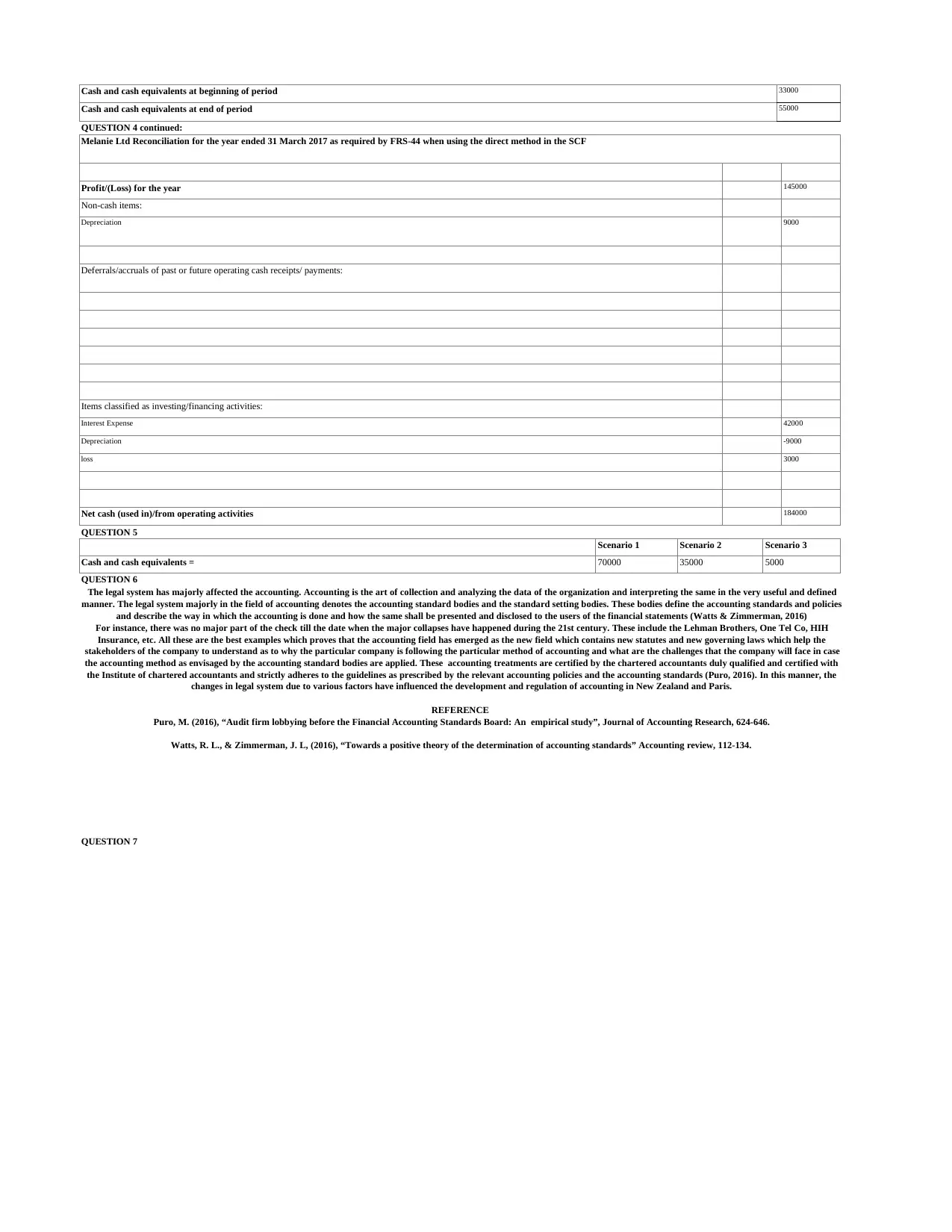

Cash and cash equivalents at beginning of period 33000

Cash and cash equivalents at end of period 55000

Melanie Ltd Reconciliation for the year ended 31 March 2017 as required by FRS-44 when using the direct method in the SCF

Profit/(Loss) for the year 145000

Non-cash items:

Depreciation 9000

Deferrals/accruals of past or future operating cash receipts/ payments:

Items classified as investing/financing activities:

Interest Expense 42000

Depreciation -9000

loss 3000

Scenario 1 Scenario 2 Scenario 3

Net cash (used in)/from operating activities 184000

Cash and cash equivalents = 70000 35000 5000

The legal system has majorly affected the accounting. Accounting is the art of collection and analyzing the data of the organization and interpreting the same in the very useful and defined

manner. The legal system majorly in the field of accounting denotes the accounting standard bodies and the standard setting bodies. These bodies define the accounting standards and policies

and describe the way in which the accounting is done and how the same shall be presented and disclosed to the users of the financial statements (Watts & Zimmerman, 2016)

For instance, there was no major part of the check till the date when the major collapses have happened during the 21st century. These include the Lehman Brothers, One Tel Co, HIH

Insurance, etc. All these are the best examples which proves that the accounting field has emerged as the new field which contains new statutes and new governing laws which help the

stakeholders of the company to understand as to why the particular company is following the particular method of accounting and what are the challenges that the company will face in case

the accounting method as envisaged by the accounting standard bodies are applied. These accounting treatments are certified by the chartered accountants duly qualified and certified with

the Institute of chartered accountants and strictly adheres to the guidelines as prescribed by the relevant accounting policies and the accounting standards (Puro, 2016). In this manner, the

changes in legal system due to various factors have influenced the development and regulation of accounting in New Zealand and Paris.

REFERENCE

Puro, M. (2016), “Audit firm lobbying before the Financial Accounting Standards Board: An empirical study”, Journal of Accounting Research, 624-646.

Watts, R. L., & Zimmerman, J. L, (2016), “Towards a positive theory of the determination of accounting standards” Accounting review, 112-134.

QUESTION 5

QUESTION 6

QUESTION 7

Cash and cash equivalents at beginning of period 33000

Cash and cash equivalents at end of period 55000

Melanie Ltd Reconciliation for the year ended 31 March 2017 as required by FRS-44 when using the direct method in the SCF

Profit/(Loss) for the year 145000

Non-cash items:

Depreciation 9000

Deferrals/accruals of past or future operating cash receipts/ payments:

Items classified as investing/financing activities:

Interest Expense 42000

Depreciation -9000

loss 3000

Scenario 1 Scenario 2 Scenario 3

Net cash (used in)/from operating activities 184000

Cash and cash equivalents = 70000 35000 5000

The legal system has majorly affected the accounting. Accounting is the art of collection and analyzing the data of the organization and interpreting the same in the very useful and defined

manner. The legal system majorly in the field of accounting denotes the accounting standard bodies and the standard setting bodies. These bodies define the accounting standards and policies

and describe the way in which the accounting is done and how the same shall be presented and disclosed to the users of the financial statements (Watts & Zimmerman, 2016)

For instance, there was no major part of the check till the date when the major collapses have happened during the 21st century. These include the Lehman Brothers, One Tel Co, HIH

Insurance, etc. All these are the best examples which proves that the accounting field has emerged as the new field which contains new statutes and new governing laws which help the

stakeholders of the company to understand as to why the particular company is following the particular method of accounting and what are the challenges that the company will face in case

the accounting method as envisaged by the accounting standard bodies are applied. These accounting treatments are certified by the chartered accountants duly qualified and certified with

the Institute of chartered accountants and strictly adheres to the guidelines as prescribed by the relevant accounting policies and the accounting standards (Puro, 2016). In this manner, the

changes in legal system due to various factors have influenced the development and regulation of accounting in New Zealand and Paris.

REFERENCE

Puro, M. (2016), “Audit firm lobbying before the Financial Accounting Standards Board: An empirical study”, Journal of Accounting Research, 624-646.

Watts, R. L., & Zimmerman, J. L, (2016), “Towards a positive theory of the determination of accounting standards” Accounting review, 112-134.

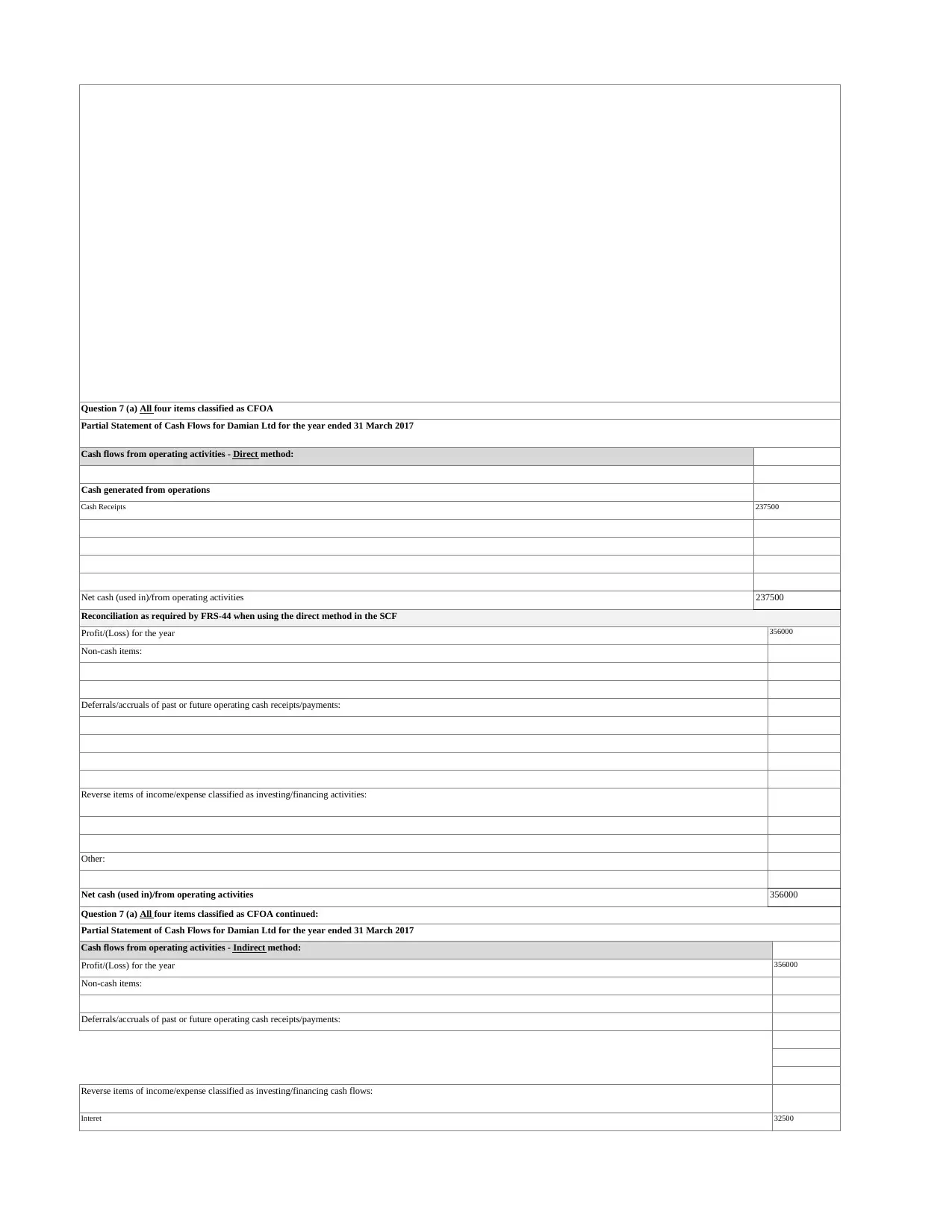

Question 7 (a) All four items classified as CFOA

Partial Statement of Cash Flows for Damian Ltd for the year ended 31 March 2017

Cash flows from operating activities - Direct method:

Cash generated from operations

Cash Receipts 237500

Net cash (used in)/from operating activities 237500

Reconciliation as required by FRS-44 when using the direct method in the SCF

Profit/(Loss) for the year 356000

Non-cash items:

Deferrals/accruals of past or future operating cash receipts/payments:

Reverse items of income/expense classified as investing/financing activities:

Other:

Net cash (used in)/from operating activities 356000

Question 7 (a) All four items classified as CFOA continued:

Partial Statement of Cash Flows for Damian Ltd for the year ended 31 March 2017

Cash flows from operating activities - Indirect method:

Profit/(Loss) for the year 356000

Non-cash items:

32500

Deferrals/accruals of past or future operating cash receipts/payments:

Interet

Reverse items of income/expense classified as investing/financing cash flows:

Partial Statement of Cash Flows for Damian Ltd for the year ended 31 March 2017

Cash flows from operating activities - Direct method:

Cash generated from operations

Cash Receipts 237500

Net cash (used in)/from operating activities 237500

Reconciliation as required by FRS-44 when using the direct method in the SCF

Profit/(Loss) for the year 356000

Non-cash items:

Deferrals/accruals of past or future operating cash receipts/payments:

Reverse items of income/expense classified as investing/financing activities:

Other:

Net cash (used in)/from operating activities 356000

Question 7 (a) All four items classified as CFOA continued:

Partial Statement of Cash Flows for Damian Ltd for the year ended 31 March 2017

Cash flows from operating activities - Indirect method:

Profit/(Loss) for the year 356000

Non-cash items:

32500

Deferrals/accruals of past or future operating cash receipts/payments:

Interet

Reverse items of income/expense classified as investing/financing cash flows:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

86000

Reverse items of income/expense to be shown separately as CFOA:

Dividend

Cash generated from operations 237500

Net cash (used in)/from operating activities $

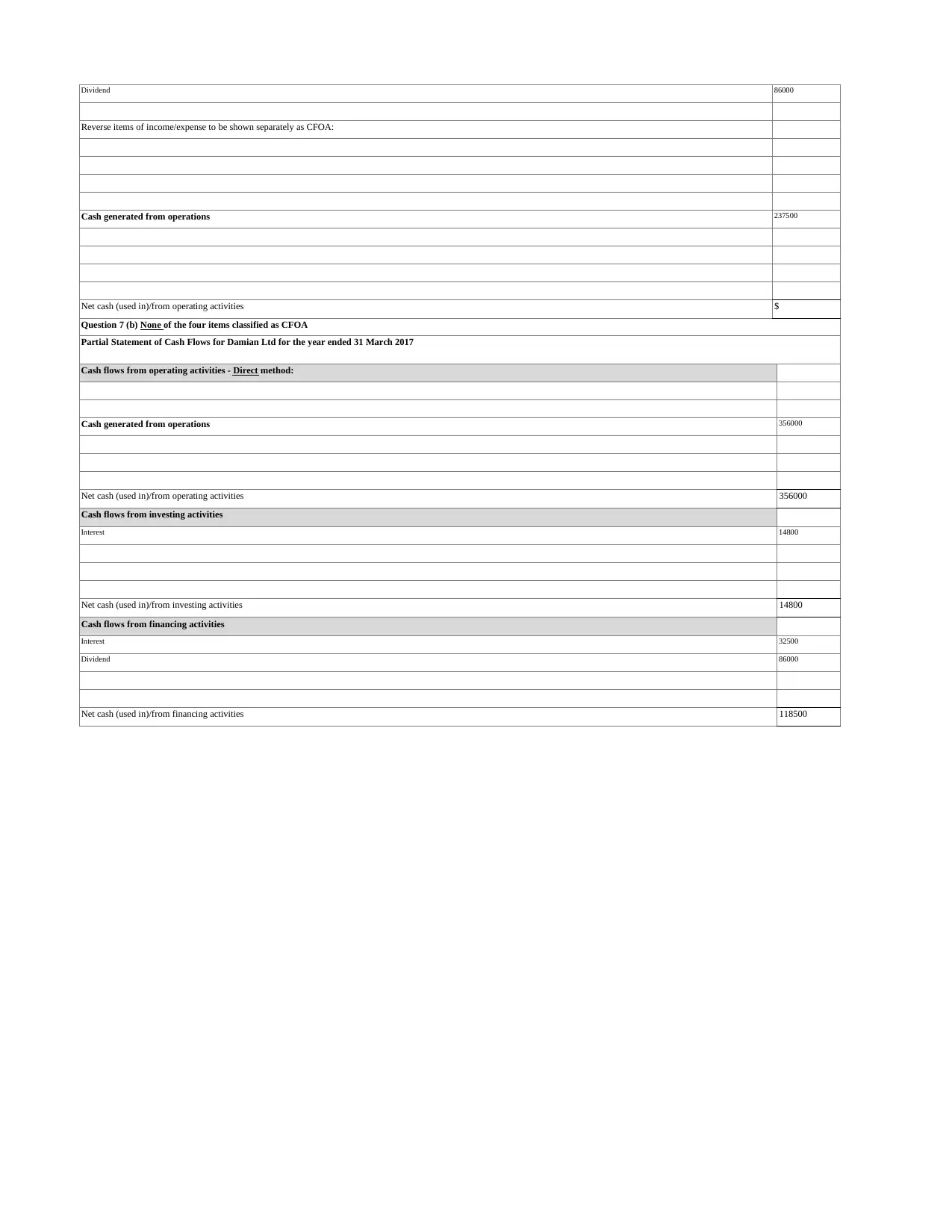

Question 7 (b) None of the four items classified as CFOA

Partial Statement of Cash Flows for Damian Ltd for the year ended 31 March 2017

Cash flows from operating activities - Direct method:

Cash generated from operations 356000

Net cash (used in)/from operating activities 356000

Cash flows from investing activities

Interest 14800

Net cash (used in)/from investing activities 14800

Net cash (used in)/from financing activities 118500

Cash flows from financing activities

Interest 32500

Dividend 86000

Reverse items of income/expense to be shown separately as CFOA:

Dividend

Cash generated from operations 237500

Net cash (used in)/from operating activities $

Question 7 (b) None of the four items classified as CFOA

Partial Statement of Cash Flows for Damian Ltd for the year ended 31 March 2017

Cash flows from operating activities - Direct method:

Cash generated from operations 356000

Net cash (used in)/from operating activities 356000

Cash flows from investing activities

Interest 14800

Net cash (used in)/from investing activities 14800

Net cash (used in)/from financing activities 118500

Cash flows from financing activities

Interest 32500

Dividend 86000

A/R 130 Balance b/d290

p L 100

Balance c/d260

390 390

Allowance for doubtful debts

p L 100

Balance c/d260

390 390

Allowance for doubtful debts

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.