Analysis of Acer Company's Corporate Governance, Auditor Independence and CEO-Chairman Split

VerifiedAdded on 2023/06/14

|9

|1534

|283

AI Summary

This report provides a detailed analysis of Acer Company's corporate governance, auditor independence, and CEO-chairman split. It evaluates the management and board's response to corporate governance matters, the independence of the auditor, and whether the CEO and chairman positions are held by the same person. The report includes a critical review, review of enforcement status, and implications of the same person holding both positions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCE

Finance

Name of the Student:

Name of the University:

Authors Note:

Finance

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE

Table of Contents

Introduction:...............................................................................................................................1

Critical review of the management and the board of directors in response to the corporate

governance matters.....................................................................................................................2

Review on the independence of the auditor:..............................................................................3

Evaluation of whether the position of the chief executive officer and the chairmen of the

company split or it is held by the same person..........................................................................5

Conclusion:................................................................................................................................6

Referencing................................................................................................................................8

Table of Contents

Introduction:...............................................................................................................................1

Critical review of the management and the board of directors in response to the corporate

governance matters.....................................................................................................................2

Review on the independence of the auditor:..............................................................................3

Evaluation of whether the position of the chief executive officer and the chairmen of the

company split or it is held by the same person..........................................................................5

Conclusion:................................................................................................................................6

Referencing................................................................................................................................8

FINANCE

Introduction:

In this report the detailed analysis of Acer Company is undertaken in respect of

various aspects of the company like the board’s and the executive managements response

towards the corporate governance , the state of independence of the auditors of the company

and the existence of any split between chairperson and the chief executive officers of the

company.

Critical review of the management and the board of directors in response to the

corporate governance matters

In response to the corporate governance, the company lays down certain enforcement

status and then evaluates the position of the company in respect of the compliance with its

enforcement status (Dodd, 2017). The enforcement status and the corresponding compliance

status of the company are as follows:

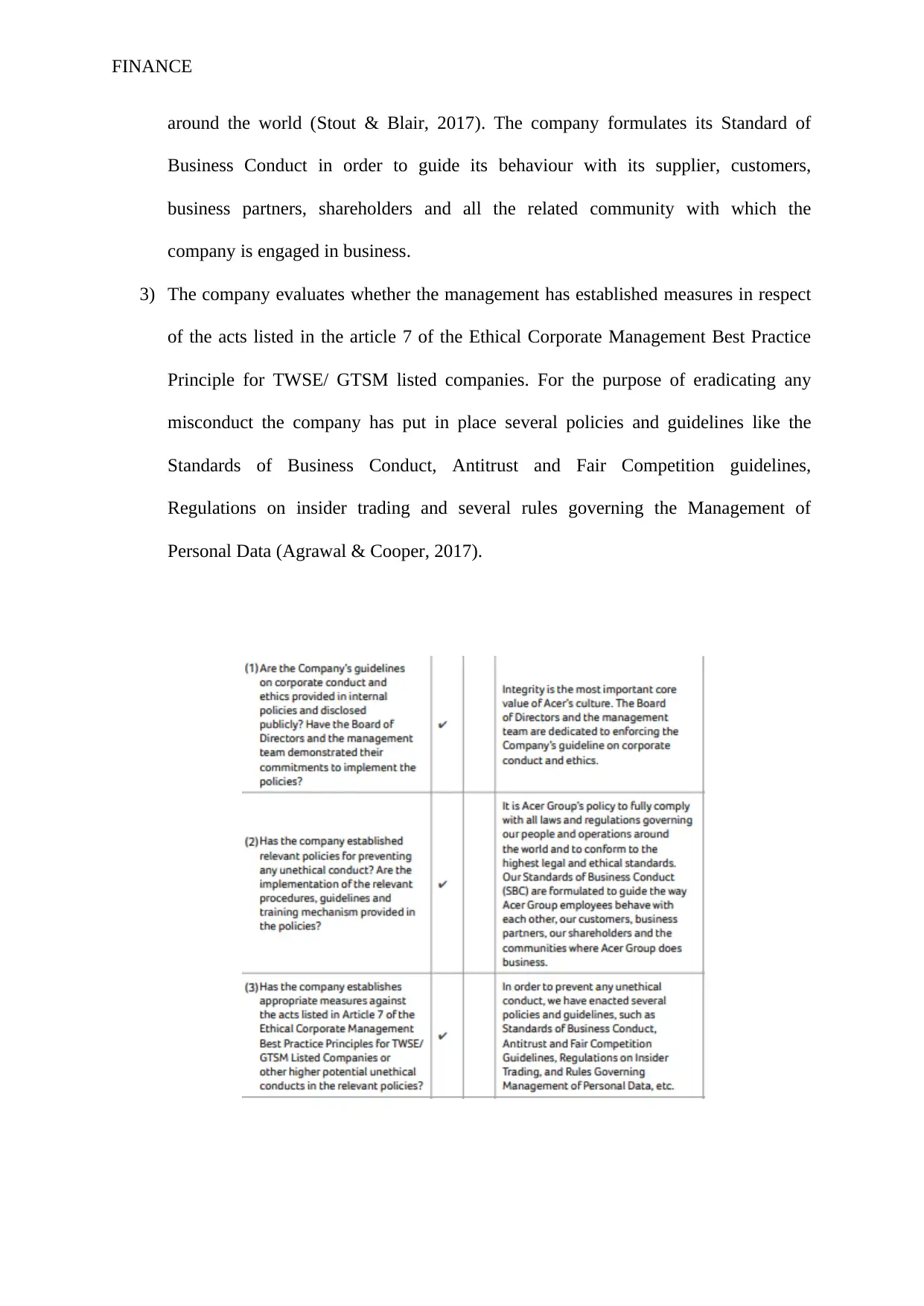

1) The company evaluates whether it has incorporated its guidelines on ethical conduct

in its internal policies and the company has disclosed the same publicly. The company

also evaluates if the management has been able to demonstrate their commitment

towards the prescribed policies (Kraakman & Hansmann, 2017). After the evaluation

that the management and the board of directors have stayed true to its motto that

integrity is the highest principle in Acer. Consequently, they have shown

determination in implementing the company’s guidelines.

2) The company evaluates whether the management and the board has established any

mechanism to avoid any unethical conduct. In addition to that the company finds out

the inclusion of the same procedures in the policies of the company. As per the

representation of the management it is one of the most important policy of the

company is to adhere to all the rules and regulations applicable on the company

Introduction:

In this report the detailed analysis of Acer Company is undertaken in respect of

various aspects of the company like the board’s and the executive managements response

towards the corporate governance , the state of independence of the auditors of the company

and the existence of any split between chairperson and the chief executive officers of the

company.

Critical review of the management and the board of directors in response to the

corporate governance matters

In response to the corporate governance, the company lays down certain enforcement

status and then evaluates the position of the company in respect of the compliance with its

enforcement status (Dodd, 2017). The enforcement status and the corresponding compliance

status of the company are as follows:

1) The company evaluates whether it has incorporated its guidelines on ethical conduct

in its internal policies and the company has disclosed the same publicly. The company

also evaluates if the management has been able to demonstrate their commitment

towards the prescribed policies (Kraakman & Hansmann, 2017). After the evaluation

that the management and the board of directors have stayed true to its motto that

integrity is the highest principle in Acer. Consequently, they have shown

determination in implementing the company’s guidelines.

2) The company evaluates whether the management and the board has established any

mechanism to avoid any unethical conduct. In addition to that the company finds out

the inclusion of the same procedures in the policies of the company. As per the

representation of the management it is one of the most important policy of the

company is to adhere to all the rules and regulations applicable on the company

FINANCE

around the world (Stout & Blair, 2017). The company formulates its Standard of

Business Conduct in order to guide its behaviour with its supplier, customers,

business partners, shareholders and all the related community with which the

company is engaged in business.

3) The company evaluates whether the management has established measures in respect

of the acts listed in the article 7 of the Ethical Corporate Management Best Practice

Principle for TWSE/ GTSM listed companies. For the purpose of eradicating any

misconduct the company has put in place several policies and guidelines like the

Standards of Business Conduct, Antitrust and Fair Competition guidelines,

Regulations on insider trading and several rules governing the Management of

Personal Data (Agrawal & Cooper, 2017).

around the world (Stout & Blair, 2017). The company formulates its Standard of

Business Conduct in order to guide its behaviour with its supplier, customers,

business partners, shareholders and all the related community with which the

company is engaged in business.

3) The company evaluates whether the management has established measures in respect

of the acts listed in the article 7 of the Ethical Corporate Management Best Practice

Principle for TWSE/ GTSM listed companies. For the purpose of eradicating any

misconduct the company has put in place several policies and guidelines like the

Standards of Business Conduct, Antitrust and Fair Competition guidelines,

Regulations on insider trading and several rules governing the Management of

Personal Data (Agrawal & Cooper, 2017).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCE

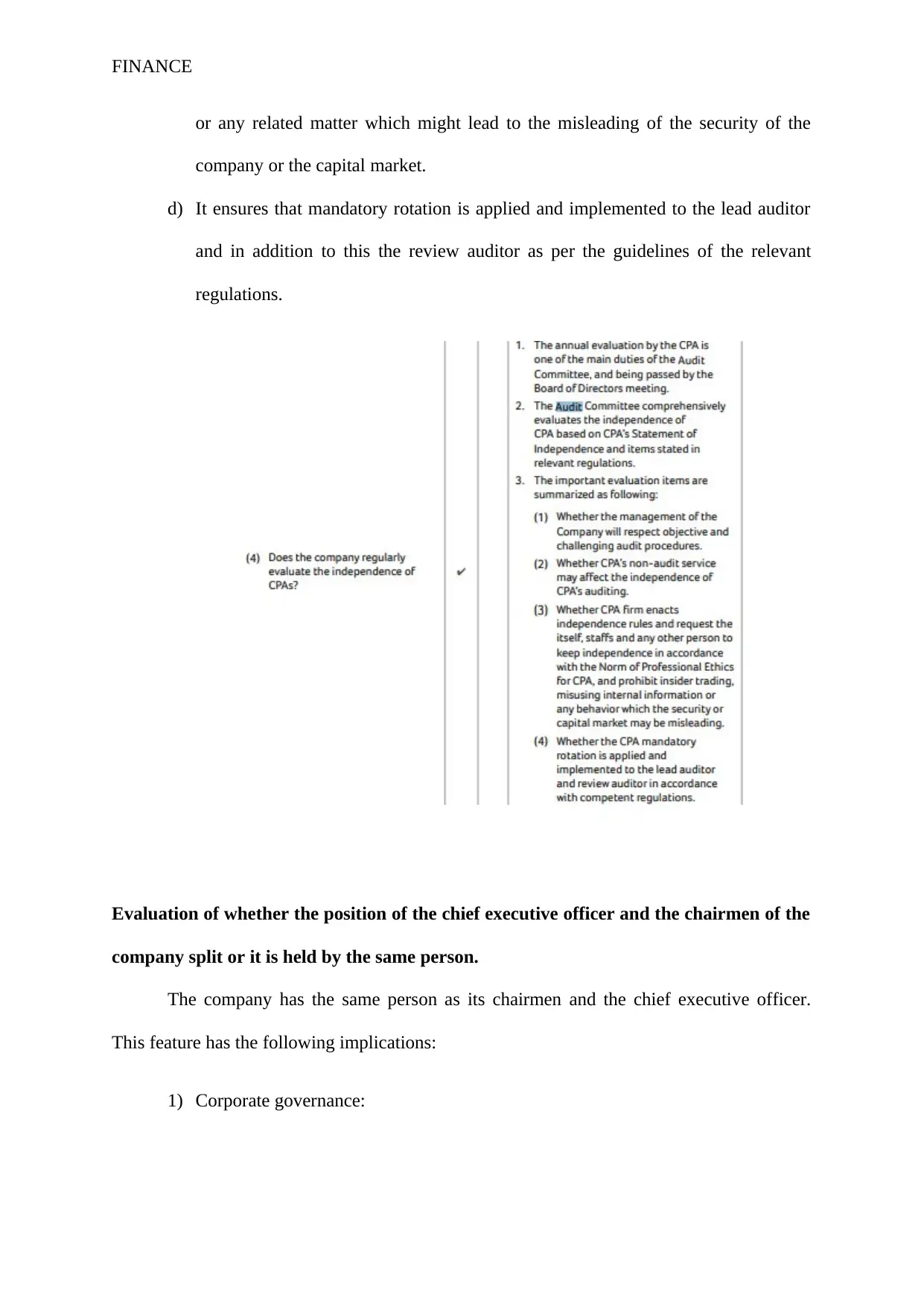

Review on the independence of the auditor:

The company in its annual report has clearly stated the various enforcement statuses that

regulate or address the issue of ensuring the independence of the auditor. The detailed

procedure or the enforcement statuses applied by the company are as follows:

1) It has specifically assigned the duty of ensuring the independence of the auditors to

the audit committee and the same has been communicated to the shareholders via the

annual report of the company.

2) The Audit committee of the company regularly engages in evaluation of the

independence of the CPAs based on the statements laid down in the CPAs statement

of independence and along with the various stipulations laid down by the relevant

regulations (McCahery et al., 2016).

3) Some of the most important evaluation items of the committee include the following:

a) The capability of the management of respecting the various challenging and

objective audit procedures applied by the auditor

b) It evaluates whether the auditor is rendering any non-audit service to the company

and whether the same is restricting his independence of his auditing procedures.

c) It continuously evaluates whether the auditing firm itself has enacted any

independence rules for itself, its staff and other persons. It is for ensuring the

independence in accordance with the Norm of Professional Ethics for CPA

(Coffee & Palia, 2016). It also evaluates whether it is committed and capable of

prohibiting insider trading and other matters like misuse of material information

Review on the independence of the auditor:

The company in its annual report has clearly stated the various enforcement statuses that

regulate or address the issue of ensuring the independence of the auditor. The detailed

procedure or the enforcement statuses applied by the company are as follows:

1) It has specifically assigned the duty of ensuring the independence of the auditors to

the audit committee and the same has been communicated to the shareholders via the

annual report of the company.

2) The Audit committee of the company regularly engages in evaluation of the

independence of the CPAs based on the statements laid down in the CPAs statement

of independence and along with the various stipulations laid down by the relevant

regulations (McCahery et al., 2016).

3) Some of the most important evaluation items of the committee include the following:

a) The capability of the management of respecting the various challenging and

objective audit procedures applied by the auditor

b) It evaluates whether the auditor is rendering any non-audit service to the company

and whether the same is restricting his independence of his auditing procedures.

c) It continuously evaluates whether the auditing firm itself has enacted any

independence rules for itself, its staff and other persons. It is for ensuring the

independence in accordance with the Norm of Professional Ethics for CPA

(Coffee & Palia, 2016). It also evaluates whether it is committed and capable of

prohibiting insider trading and other matters like misuse of material information

FINANCE

or any related matter which might lead to the misleading of the security of the

company or the capital market.

d) It ensures that mandatory rotation is applied and implemented to the lead auditor

and in addition to this the review auditor as per the guidelines of the relevant

regulations.

Evaluation of whether the position of the chief executive officer and the chairmen of the

company split or it is held by the same person.

The company has the same person as its chairmen and the chief executive officer.

This feature has the following implications:

1) Corporate governance:

or any related matter which might lead to the misleading of the security of the

company or the capital market.

d) It ensures that mandatory rotation is applied and implemented to the lead auditor

and in addition to this the review auditor as per the guidelines of the relevant

regulations.

Evaluation of whether the position of the chief executive officer and the chairmen of the

company split or it is held by the same person.

The company has the same person as its chairmen and the chief executive officer.

This feature has the following implications:

1) Corporate governance:

FINANCE

The chief executive officer of the company is responsible for ensuring that the

actions of the company are in conjunction with the objectives and the goals of the

company. In case the company has the same person as its chairperson then the

liability of the adhering to the actions required to be performed fells upon the

same person who is responsible for determining the effectiveness and efficiency

of the decisions and the actions taken (Larcker & Tayan, 2015). This results in the

risk of self-appraisal and may result in higher inefficiencies in the operations of

the entity.

2) Independence of the audit committee:

The statutory requirements lay down that the audit committee must be comprised

of only non-executive directors. The companies put such kinds of guidelines in

place in order to curb the increasing amount of violations in the corporate

governance norms (Samra, 2016). But, the audit committee in the end has the

obligation to report back to the chairperson of the board and in case the chief

executive officer of the company is also the chairperson of the board of directors

the effectiveness of such measures reduce drastically and in some cases they

become nullified.

3) Compensation in respect of the executive members:

In case the chairperson and the chief executive officer of the company are the

same person decision in respect of his remuneration has to be taken by the same

person. This can lead to conflict of interest and loss of profits attributable to

shareholders.

Conclusion:

In the report, it is found that the company has well enforcement status in place that

helps the management to determine the compliance in respect of them. Due to the readily

The chief executive officer of the company is responsible for ensuring that the

actions of the company are in conjunction with the objectives and the goals of the

company. In case the company has the same person as its chairperson then the

liability of the adhering to the actions required to be performed fells upon the

same person who is responsible for determining the effectiveness and efficiency

of the decisions and the actions taken (Larcker & Tayan, 2015). This results in the

risk of self-appraisal and may result in higher inefficiencies in the operations of

the entity.

2) Independence of the audit committee:

The statutory requirements lay down that the audit committee must be comprised

of only non-executive directors. The companies put such kinds of guidelines in

place in order to curb the increasing amount of violations in the corporate

governance norms (Samra, 2016). But, the audit committee in the end has the

obligation to report back to the chairperson of the board and in case the chief

executive officer of the company is also the chairperson of the board of directors

the effectiveness of such measures reduce drastically and in some cases they

become nullified.

3) Compensation in respect of the executive members:

In case the chairperson and the chief executive officer of the company are the

same person decision in respect of his remuneration has to be taken by the same

person. This can lead to conflict of interest and loss of profits attributable to

shareholders.

Conclusion:

In the report, it is found that the company has well enforcement status in place that

helps the management to determine the compliance in respect of them. Due to the readily

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE

available measures of corporate governance the management is focussed on taking adequate

and appropriate steps in this respect. The audit committee makes sure about the conduct of

independent audit by the help of its own prescribed enforcement status. The company has the

same person as the chief executive officer and the chairperson of the board. This may result

in conflict of interest.

available measures of corporate governance the management is focussed on taking adequate

and appropriate steps in this respect. The audit committee makes sure about the conduct of

independent audit by the help of its own prescribed enforcement status. The company has the

same person as the chief executive officer and the chairperson of the board. This may result

in conflict of interest.

FINANCE

Referencing

Agrawal, A., & Cooper, T. (2017). Corporate governance consequences of accounting

scandals: Evidence from top management, CFO and auditor turnover. Quarterly

Journal of Finance, 7(01), 1650014.

Coffee Jr, J. C., & Palia, D. (2016). The wolf at the door: The impact of hedge fund activism

on corporate governance. Annals of Corporate Governance, 1(1), 1-94.

Dodd, E. M. (2017). For whom are corporate managers trustees?. In Corporate

Governance (pp. 29-47). Gower.

Kraakman, R., & Hansmann, H. (2017). The end of history for corporate law. In Corporate

Governance (pp. 49-78). Gower.

Larcker, D., & Tayan, B. (2015). Corporate governance matters: A closer look at

organizational choices and their consequences. Pearson Education.

McCahery, J. A., Sautner, Z., & Starks, L. T. (2016). Behind the scenes: The corporate

governance preferences of institutional investors. The Journal of Finance, 71(6),

2905-2932.

Samra, E. (2016). Corporate governance in Islamic financial institutions.

Stout, L. A., & Blair, M. M. (2017). A team production theory of corporate law. In Corporate

Governance (pp. 169-250). Gower.

Referencing

Agrawal, A., & Cooper, T. (2017). Corporate governance consequences of accounting

scandals: Evidence from top management, CFO and auditor turnover. Quarterly

Journal of Finance, 7(01), 1650014.

Coffee Jr, J. C., & Palia, D. (2016). The wolf at the door: The impact of hedge fund activism

on corporate governance. Annals of Corporate Governance, 1(1), 1-94.

Dodd, E. M. (2017). For whom are corporate managers trustees?. In Corporate

Governance (pp. 29-47). Gower.

Kraakman, R., & Hansmann, H. (2017). The end of history for corporate law. In Corporate

Governance (pp. 49-78). Gower.

Larcker, D., & Tayan, B. (2015). Corporate governance matters: A closer look at

organizational choices and their consequences. Pearson Education.

McCahery, J. A., Sautner, Z., & Starks, L. T. (2016). Behind the scenes: The corporate

governance preferences of institutional investors. The Journal of Finance, 71(6),

2905-2932.

Samra, E. (2016). Corporate governance in Islamic financial institutions.

Stout, L. A., & Blair, M. M. (2017). A team production theory of corporate law. In Corporate

Governance (pp. 169-250). Gower.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.