Corporate Governance Analysis of Acer Computers

VerifiedAdded on 2023/06/14

|9

|1124

|208

AI Summary

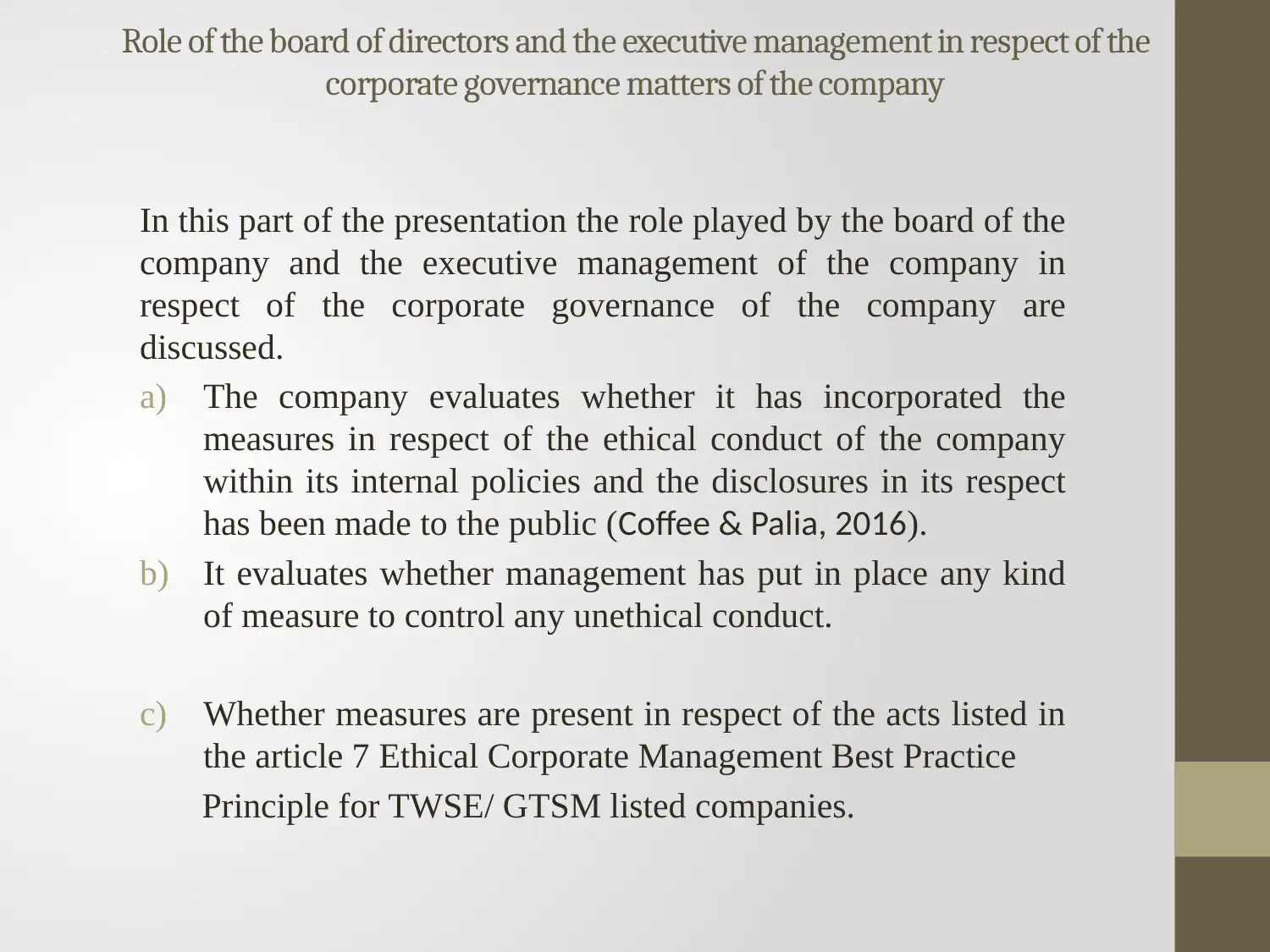

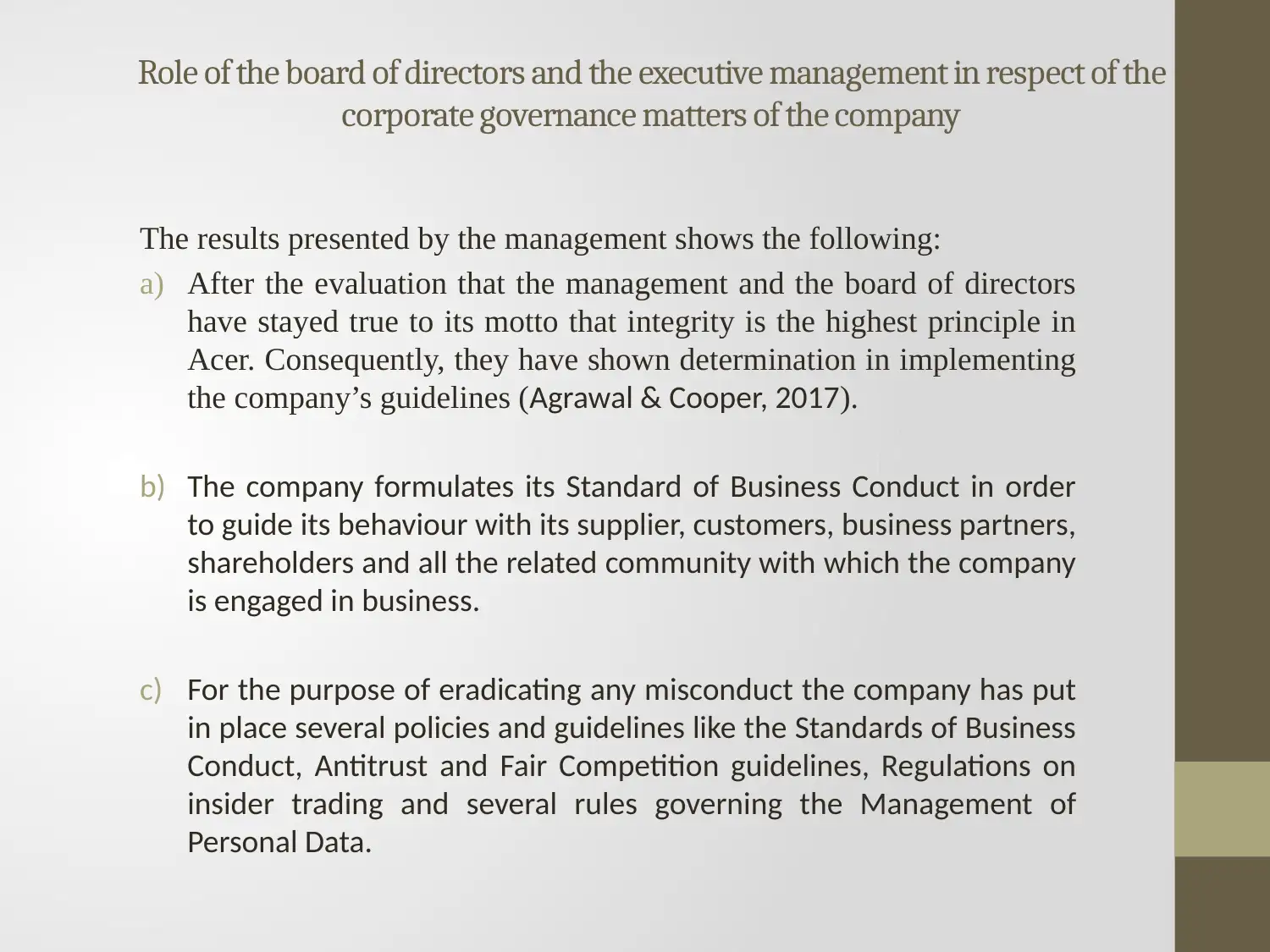

This presentation provides a detailed analysis of various aspects of ACER computers including the role of the board of directors and the executive management in respect of the corporate governance matters of the company, independence of the auditor in conduct of his duty, and the presence of split between the identity of the chairperson and the chief executive officer.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.