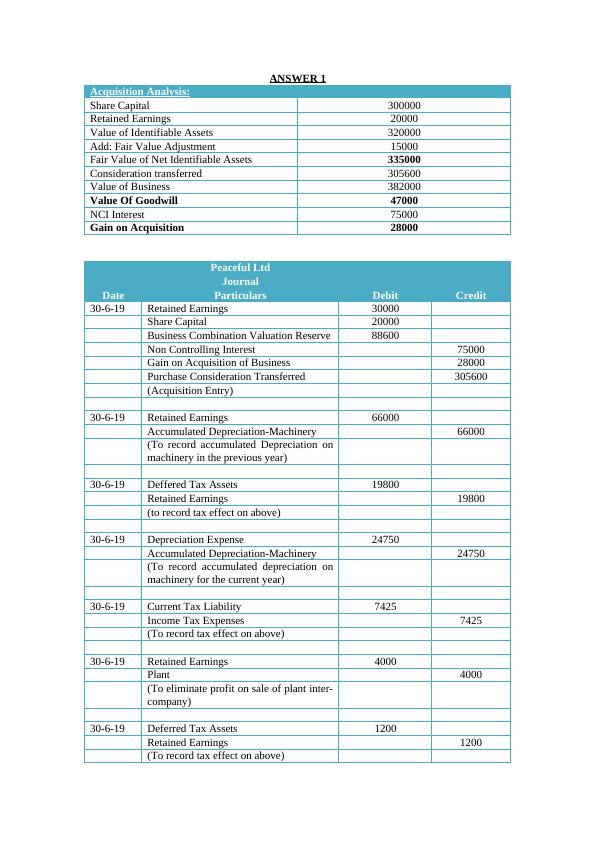

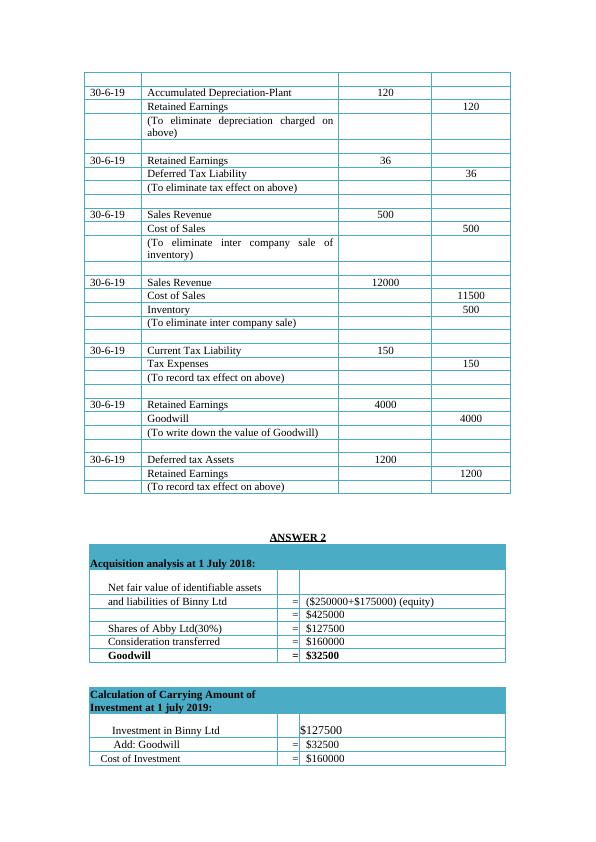

Journal Entries for Acquisition Analysis, Investment Calculation and Transaction A and B

Consolidation: Non-controlling interests

4 Pages698 Words278 Views

Added on 2023-04-22

About This Document

This document contains journal entries for Acquisition Analysis, Investment Calculation and Transaction A and B. It includes details such as date, particulars, debit, and credit.

Journal Entries for Acquisition Analysis, Investment Calculation and Transaction A and B

Consolidation: Non-controlling interests

Added on 2023-04-22

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Corporate Accounting

|11

|1664

|98

Consolidation Journal Entries for Ghostbusters Ltd at 30 June 2020

|6

|1248

|454

Consolidated Financial Statements for Lotus Limited and Troy Limited

|7

|885

|56

Corporate Accounting System

|11

|1616

|279

Acquisition Analysis of Sublime Ltd || Assignment

|7

|1506

|41

Consolidation of Financials for Ghostbusters Ltd: Steps, Entries, and Worksheet

|5

|1448

|201