Cost Identification and Income Statement Analysis

VerifiedAdded on 2023/01/18

|4

|2003

|54

AI Summary

This article discusses cost identification and income statement analysis for Sports Strength. It explains the different types of costs and their impact on operating income. It also calculates the break-even point and margin of safety. The article presents two plans to increase operating profit and recommends the more effective plan. References are provided for further reading.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Activity 1

1. Cost identification:

a. Mixed cost, as it is increasing with increase in volumes sold and it is difficult to

estimate the costs of petrol per unit of sales.

b. Mixed cost, as it is increasing with increase in jerseys sold and has a fixed

component of $12,000.

c. Fixed cost, as monthly credit cards rental remain the same irrespective of the

amount/ volume of sales made (Alexander, 2016).

d. Variable costs, as it is directly related to the number of units sold. It changes with

the number of units sold.

e. Variable costs, as it is directly related to the number of units sold. It changes with

the number of units produced.

f. Step costs, as costs remain fixed up to a certain level of sales, after which it

increases. Step costs are variable, but only change at discrete points.

g. Fixed cost, as website hosting costs remain the same irrespective of the amount/

volume of sales made (Choy, 2018).

2. Income Statement Analysis:

a. Operating profit equation for Sports Strength is:

20x = 16x + 190,000 (x=units sold).

Break-even = 190,000/4 = 47,500 units. Hence, the company shall start earning

operating income if it sells more than 47,500 units.

b. Operating income = $17,900. Therefore, units sold = (17,900+190,000)/4 = 51,975

units.

Let the number of units expected to be sold be ‘y’. Therefore,

16% of y = y – 51975. y = 51975/0.84 = 61875.

Therefore, units below expectations = 61875-51975 = 9900 (Jefferson, 2017). Hence,

extra income tax that would have been generated had the jerseys been sold as per

expectations:

9900*$(20-16)*30% = $9900*4*0.30 = $11,880.

c. Assuming fixed costs remain the same, the total expense would be:

70,000*16 + 190,000 = $(1,120,000 + 190,000) = $1,310,000

d. If the messenger’s offer is accepted, it will add to the existing fixed costs of $190,000

by $35,000. The total fixed costs would be $(190,000+35,000) = $225,000.

Therefore, the new operating income equation would be: 20x = 16x + 225,000

(x=units sold).

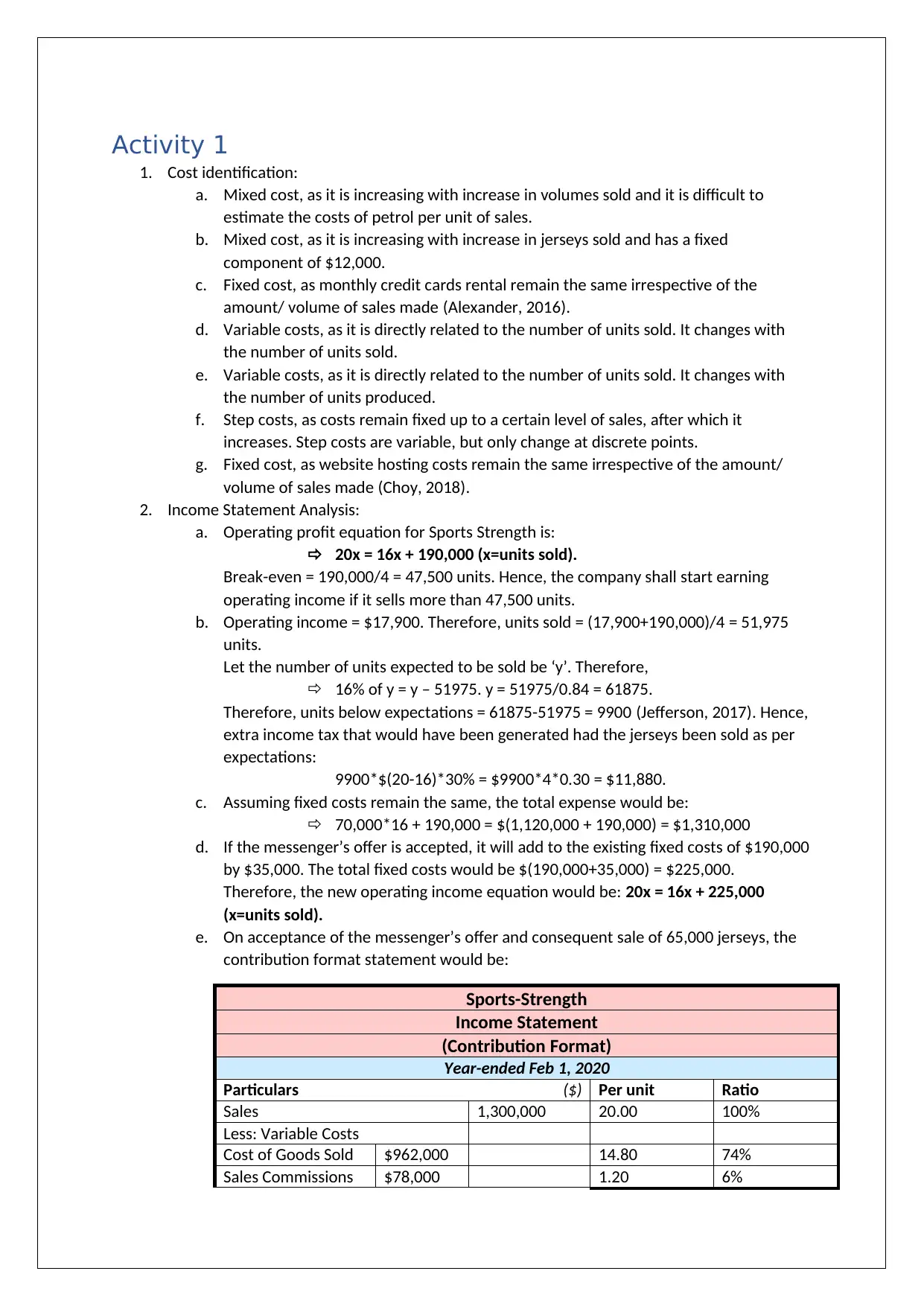

e. On acceptance of the messenger’s offer and consequent sale of 65,000 jerseys, the

contribution format statement would be:

Sports-Strength

Income Statement

(Contribution Format)

Year-ended Feb 1, 2020

Particulars ($) Per unit Ratio

Sales 1,300,000 20.00 100%

Less: Variable Costs

Cost of Goods Sold $962,000 14.80 74%

Sales Commissions $78,000 1.20 6%

1. Cost identification:

a. Mixed cost, as it is increasing with increase in volumes sold and it is difficult to

estimate the costs of petrol per unit of sales.

b. Mixed cost, as it is increasing with increase in jerseys sold and has a fixed

component of $12,000.

c. Fixed cost, as monthly credit cards rental remain the same irrespective of the

amount/ volume of sales made (Alexander, 2016).

d. Variable costs, as it is directly related to the number of units sold. It changes with

the number of units sold.

e. Variable costs, as it is directly related to the number of units sold. It changes with

the number of units produced.

f. Step costs, as costs remain fixed up to a certain level of sales, after which it

increases. Step costs are variable, but only change at discrete points.

g. Fixed cost, as website hosting costs remain the same irrespective of the amount/

volume of sales made (Choy, 2018).

2. Income Statement Analysis:

a. Operating profit equation for Sports Strength is:

20x = 16x + 190,000 (x=units sold).

Break-even = 190,000/4 = 47,500 units. Hence, the company shall start earning

operating income if it sells more than 47,500 units.

b. Operating income = $17,900. Therefore, units sold = (17,900+190,000)/4 = 51,975

units.

Let the number of units expected to be sold be ‘y’. Therefore,

16% of y = y – 51975. y = 51975/0.84 = 61875.

Therefore, units below expectations = 61875-51975 = 9900 (Jefferson, 2017). Hence,

extra income tax that would have been generated had the jerseys been sold as per

expectations:

9900*$(20-16)*30% = $9900*4*0.30 = $11,880.

c. Assuming fixed costs remain the same, the total expense would be:

70,000*16 + 190,000 = $(1,120,000 + 190,000) = $1,310,000

d. If the messenger’s offer is accepted, it will add to the existing fixed costs of $190,000

by $35,000. The total fixed costs would be $(190,000+35,000) = $225,000.

Therefore, the new operating income equation would be: 20x = 16x + 225,000

(x=units sold).

e. On acceptance of the messenger’s offer and consequent sale of 65,000 jerseys, the

contribution format statement would be:

Sports-Strength

Income Statement

(Contribution Format)

Year-ended Feb 1, 2020

Particulars ($) Per unit Ratio

Sales 1,300,000 20.00 100%

Less: Variable Costs

Cost of Goods Sold $962,000 14.80 74%

Sales Commissions $78,000 1.20 6%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

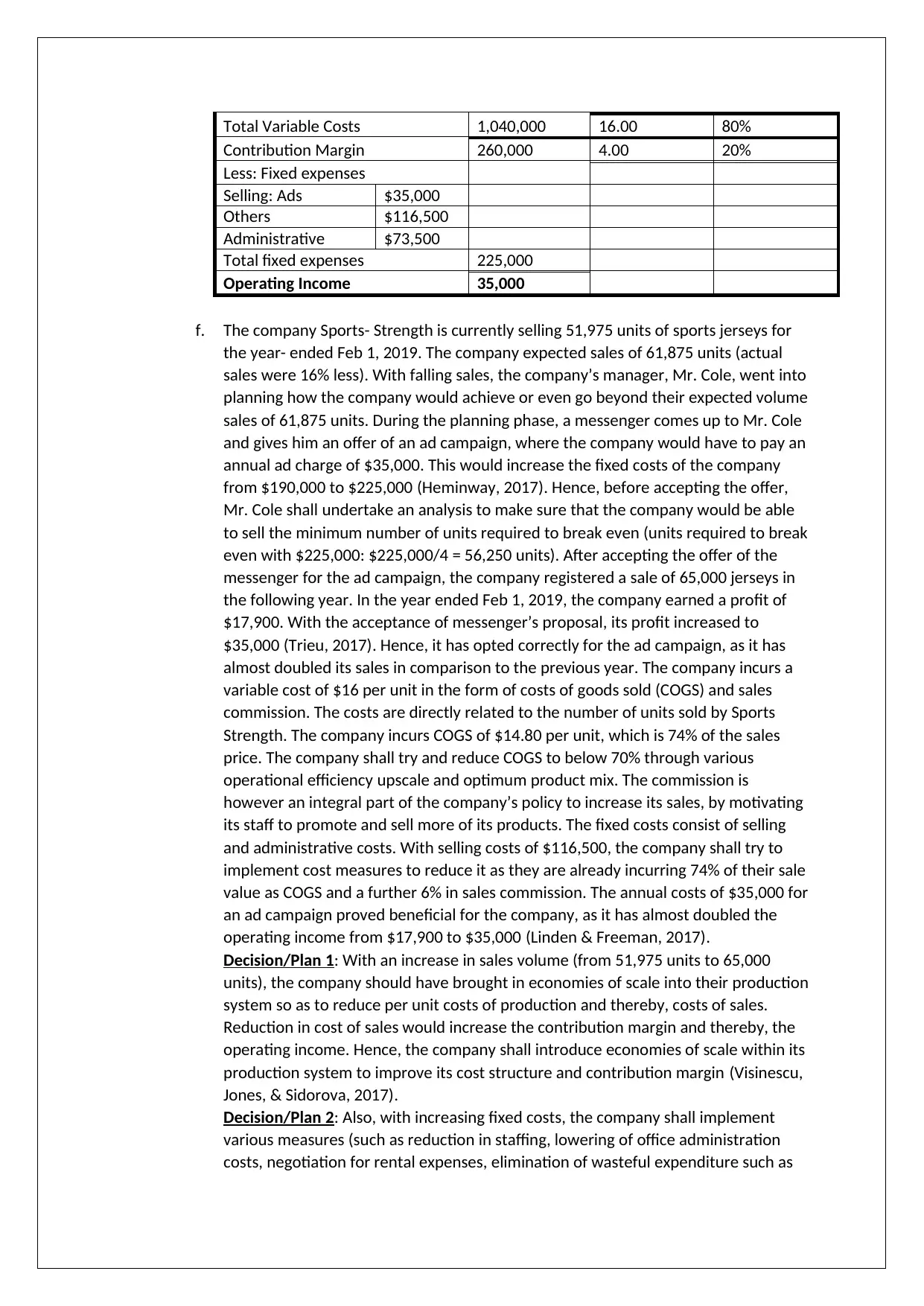

Total Variable Costs 1,040,000 16.00 80%

Contribution Margin 260,000 4.00 20%

Less: Fixed expenses

Selling: Ads $35,000

Others $116,500

Administrative $73,500

Total fixed expenses 225,000

Operating Income 35,000

f. The company Sports- Strength is currently selling 51,975 units of sports jerseys for

the year- ended Feb 1, 2019. The company expected sales of 61,875 units (actual

sales were 16% less). With falling sales, the company’s manager, Mr. Cole, went into

planning how the company would achieve or even go beyond their expected volume

sales of 61,875 units. During the planning phase, a messenger comes up to Mr. Cole

and gives him an offer of an ad campaign, where the company would have to pay an

annual ad charge of $35,000. This would increase the fixed costs of the company

from $190,000 to $225,000 (Heminway, 2017). Hence, before accepting the offer,

Mr. Cole shall undertake an analysis to make sure that the company would be able

to sell the minimum number of units required to break even (units required to break

even with $225,000: $225,000/4 = 56,250 units). After accepting the offer of the

messenger for the ad campaign, the company registered a sale of 65,000 jerseys in

the following year. In the year ended Feb 1, 2019, the company earned a profit of

$17,900. With the acceptance of messenger’s proposal, its profit increased to

$35,000 (Trieu, 2017). Hence, it has opted correctly for the ad campaign, as it has

almost doubled its sales in comparison to the previous year. The company incurs a

variable cost of $16 per unit in the form of costs of goods sold (COGS) and sales

commission. The costs are directly related to the number of units sold by Sports

Strength. The company incurs COGS of $14.80 per unit, which is 74% of the sales

price. The company shall try and reduce COGS to below 70% through various

operational efficiency upscale and optimum product mix. The commission is

however an integral part of the company’s policy to increase its sales, by motivating

its staff to promote and sell more of its products. The fixed costs consist of selling

and administrative costs. With selling costs of $116,500, the company shall try to

implement cost measures to reduce it as they are already incurring 74% of their sale

value as COGS and a further 6% in sales commission. The annual costs of $35,000 for

an ad campaign proved beneficial for the company, as it has almost doubled the

operating income from $17,900 to $35,000 (Linden & Freeman, 2017).

Decision/Plan 1: With an increase in sales volume (from 51,975 units to 65,000

units), the company should have brought in economies of scale into their production

system so as to reduce per unit costs of production and thereby, costs of sales.

Reduction in cost of sales would increase the contribution margin and thereby, the

operating income. Hence, the company shall introduce economies of scale within its

production system to improve its cost structure and contribution margin (Visinescu,

Jones, & Sidorova, 2017).

Decision/Plan 2: Also, with increasing fixed costs, the company shall implement

various measures (such as reduction in staffing, lowering of office administration

costs, negotiation for rental expenses, elimination of wasteful expenditure such as

Contribution Margin 260,000 4.00 20%

Less: Fixed expenses

Selling: Ads $35,000

Others $116,500

Administrative $73,500

Total fixed expenses 225,000

Operating Income 35,000

f. The company Sports- Strength is currently selling 51,975 units of sports jerseys for

the year- ended Feb 1, 2019. The company expected sales of 61,875 units (actual

sales were 16% less). With falling sales, the company’s manager, Mr. Cole, went into

planning how the company would achieve or even go beyond their expected volume

sales of 61,875 units. During the planning phase, a messenger comes up to Mr. Cole

and gives him an offer of an ad campaign, where the company would have to pay an

annual ad charge of $35,000. This would increase the fixed costs of the company

from $190,000 to $225,000 (Heminway, 2017). Hence, before accepting the offer,

Mr. Cole shall undertake an analysis to make sure that the company would be able

to sell the minimum number of units required to break even (units required to break

even with $225,000: $225,000/4 = 56,250 units). After accepting the offer of the

messenger for the ad campaign, the company registered a sale of 65,000 jerseys in

the following year. In the year ended Feb 1, 2019, the company earned a profit of

$17,900. With the acceptance of messenger’s proposal, its profit increased to

$35,000 (Trieu, 2017). Hence, it has opted correctly for the ad campaign, as it has

almost doubled its sales in comparison to the previous year. The company incurs a

variable cost of $16 per unit in the form of costs of goods sold (COGS) and sales

commission. The costs are directly related to the number of units sold by Sports

Strength. The company incurs COGS of $14.80 per unit, which is 74% of the sales

price. The company shall try and reduce COGS to below 70% through various

operational efficiency upscale and optimum product mix. The commission is

however an integral part of the company’s policy to increase its sales, by motivating

its staff to promote and sell more of its products. The fixed costs consist of selling

and administrative costs. With selling costs of $116,500, the company shall try to

implement cost measures to reduce it as they are already incurring 74% of their sale

value as COGS and a further 6% in sales commission. The annual costs of $35,000 for

an ad campaign proved beneficial for the company, as it has almost doubled the

operating income from $17,900 to $35,000 (Linden & Freeman, 2017).

Decision/Plan 1: With an increase in sales volume (from 51,975 units to 65,000

units), the company should have brought in economies of scale into their production

system so as to reduce per unit costs of production and thereby, costs of sales.

Reduction in cost of sales would increase the contribution margin and thereby, the

operating income. Hence, the company shall introduce economies of scale within its

production system to improve its cost structure and contribution margin (Visinescu,

Jones, & Sidorova, 2017).

Decision/Plan 2: Also, with increasing fixed costs, the company shall implement

various measures (such as reduction in staffing, lowering of office administration

costs, negotiation for rental expenses, elimination of wasteful expenditure such as

credit card rentals) so as to increase profits and channel resources towards more

appropriate tasks (Vieira, O’Dwyer, & Schneider, 2017).

Activity 2

a. Operating profit equation for Sports Strength is: 20x = 16x + 190,000 (x=units sold). Break-

even = 190,000/4 = 47,500 units. Break even sales = 47,500*$20 = $950,000. Hence, the

company shall start earning operating income if it sells more than 47,500 units.

b. Actual units sold = 207,900/4 = 51,975 units. Therefore, margin of safety:

(Actual units sold – Break even sales)/ Break even sales = (51975-47500)/47500 = 9.42%

Margin of safety (units) = 4475 units; Margin of safety ($) = 4475*20 = $89,500.

This indicates that Sports-Strength sold 9.42% more units than required to break even.

c. All other things being equal, the change in cost of goods sold to $15.30 per unit would

decrease operating income by $(15.30-14.80)*51975 = $25,987.50.

Therefore, operating income = $(17,900-25987.5) = $(8,087.50)

d. Plan 1: Increase in sales price to $20.50 per unit and additional advertising of $15,000.

Operating income (OI) = $[51975*(20.50-15.30-0.06*20.50)-190,000-15000]

OI = $[51975*3.97-190000] = $[206340.75-190000] = $1,340.75

Plan 2: Reducing commission to 4% of sales price, increasing salaries by $22,000 and doing

an ad campaign costing $10,000. This shall increase sales volume by 16%.

Operating income (OI) = $[51975*1.16*(20.00-15.30-0.04*20.00)-190,000-22,000-10000]

OI = $[60291*3.9-190000] = $[235134.90-222000] = $13,134.90

e. Though the company incurs an advertising cost of $ 15000 in plan 1, its operating income is

significantly reduced. This is because the increase in sales amount is not as much as increase

in the costs of marketing (Kim, Schmidgall, & Damitio, 2017).

f. Plan 2 shall be recommended to the management of the company because it results in

increase in increase in operating profit by a significant amount. Other than this, the

campaign focuses to increase its customer base rather than increasing the selling price of

the commodity. This shall be great for the organization both in short term and long term.

Enjoying a large clientele is what any organization desires. Also the cost of marketing is

much lower than the first plan (Sithole, Chandler, Abeysekera, & Paas, 2017).

appropriate tasks (Vieira, O’Dwyer, & Schneider, 2017).

Activity 2

a. Operating profit equation for Sports Strength is: 20x = 16x + 190,000 (x=units sold). Break-

even = 190,000/4 = 47,500 units. Break even sales = 47,500*$20 = $950,000. Hence, the

company shall start earning operating income if it sells more than 47,500 units.

b. Actual units sold = 207,900/4 = 51,975 units. Therefore, margin of safety:

(Actual units sold – Break even sales)/ Break even sales = (51975-47500)/47500 = 9.42%

Margin of safety (units) = 4475 units; Margin of safety ($) = 4475*20 = $89,500.

This indicates that Sports-Strength sold 9.42% more units than required to break even.

c. All other things being equal, the change in cost of goods sold to $15.30 per unit would

decrease operating income by $(15.30-14.80)*51975 = $25,987.50.

Therefore, operating income = $(17,900-25987.5) = $(8,087.50)

d. Plan 1: Increase in sales price to $20.50 per unit and additional advertising of $15,000.

Operating income (OI) = $[51975*(20.50-15.30-0.06*20.50)-190,000-15000]

OI = $[51975*3.97-190000] = $[206340.75-190000] = $1,340.75

Plan 2: Reducing commission to 4% of sales price, increasing salaries by $22,000 and doing

an ad campaign costing $10,000. This shall increase sales volume by 16%.

Operating income (OI) = $[51975*1.16*(20.00-15.30-0.04*20.00)-190,000-22,000-10000]

OI = $[60291*3.9-190000] = $[235134.90-222000] = $13,134.90

e. Though the company incurs an advertising cost of $ 15000 in plan 1, its operating income is

significantly reduced. This is because the increase in sales amount is not as much as increase

in the costs of marketing (Kim, Schmidgall, & Damitio, 2017).

f. Plan 2 shall be recommended to the management of the company because it results in

increase in increase in operating profit by a significant amount. Other than this, the

campaign focuses to increase its customer base rather than increasing the selling price of

the commodity. This shall be great for the organization both in short term and long term.

Enjoying a large clientele is what any organization desires. Also the cost of marketing is

much lower than the first plan (Sithole, Chandler, Abeysekera, & Paas, 2017).

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4),

411-431.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 2(1), 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law,

and Organic Documents. SSRN, 5(2), 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, 1(2), 353-354.

Kim, M., Schmidgall, R., & Damitio, J. (2017). Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of

Hospitality & Tourism Administration, , 18(1), 23-40.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making.

Business Ethics Quarterly, 27(3), 353-379. doi:https://doi.org/10.1017/beq.2017.1

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved

from http://psycnet.apa.org/buy/2016-21263-001

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

Vieira, R., O’Dwyer, B., & Schneider, R. (2017). Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1), 25-32.

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4),

411-431.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 2(1), 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law,

and Organic Documents. SSRN, 5(2), 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, 1(2), 353-354.

Kim, M., Schmidgall, R., & Damitio, J. (2017). Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of

Hospitality & Tourism Administration, , 18(1), 23-40.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making.

Business Ethics Quarterly, 27(3), 353-379. doi:https://doi.org/10.1017/beq.2017.1

Sithole, S., Chandler, P., Abeysekera, I., & Paas, F. (2017). Benefits of guided self-management of

attention on learning accounting. Journal of Educational Psychology, 109(2), 220. Retrieved

from http://psycnet.apa.org/buy/2016-21263-001

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93, 111-124.

Vieira, R., O’Dwyer, B., & Schneider, R. (2017). Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1), 25-32.

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), 58-66.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.