Activity-Based Costing (ABC) Analysis: CIMIC Group and Beyond Report

VerifiedAdded on 2023/06/05

|15

|3697

|71

Report

AI Summary

This report provides an in-depth analysis of Activity-Based Costing (ABC), a crucial management accounting tool used for financial and managerial decision-making. It begins with an executive summary, followed by an introduction explaining the concept of ABC, its characteristics, and its application in organizations, particularly the CIMIC Group. The report analyzes two research journal articles, discussing their purposes, similarities, and differences in findings related to ABC's impact on business operations and cost management. It highlights four key outcomes derived from these studies, emphasizing the benefits of ABC in improving cost accuracy and decision-making. The report concludes by summarizing the usability of ABC in Australia and its significance in providing accurate product costing and enabling effective financial management. The report covers ABC's role in providing insights into product costing and its applications in business decision-making.

Activity-based costing (ABC) 1

Activity-based costing (ABC)

Activity-based costing (ABC)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-based costing (ABC) 2

Executive Summary

Management accounting tools are taken as those tools which are useful in the business for

financial and managerial decisions making. Activity based costing is one of them which

provide better understanding related to cost analysis, investment analysis, procurement

management, financial decision and so on. Use of ABC costing analysis is important in

business organisation which explains the financial findings in the context of business

decisions. This reading will describe activity based costing purpose and its management

within the organisation. It will include discussions over similarities and differences upon

issues related to activity based costing and its importance in business decisions making and

operations. At the end it will deliver outcomes and usability of management accounting tools

in Australia. This will provide the real nature & behaviour about product and costing.

Activity Base costing system provides not only the accurate cost of product bust also gives us

mechanism for managing costs. This system gave different type of level of utility.

Executive Summary

Management accounting tools are taken as those tools which are useful in the business for

financial and managerial decisions making. Activity based costing is one of them which

provide better understanding related to cost analysis, investment analysis, procurement

management, financial decision and so on. Use of ABC costing analysis is important in

business organisation which explains the financial findings in the context of business

decisions. This reading will describe activity based costing purpose and its management

within the organisation. It will include discussions over similarities and differences upon

issues related to activity based costing and its importance in business decisions making and

operations. At the end it will deliver outcomes and usability of management accounting tools

in Australia. This will provide the real nature & behaviour about product and costing.

Activity Base costing system provides not only the accurate cost of product bust also gives us

mechanism for managing costs. This system gave different type of level of utility.

Activity-based costing (ABC) 3

Table of Contents

Executive Summary...................................................................................................................2

Introduction:...............................................................................................................................4

a) Explanation of Activity based Costing:.................................................................................5

b). Explanation of purpose of both journal topics in the context of “Activity Based

Costing”..................................................................................................................................6

c). Similarities and Difference between analysis of findings:....................................................9

d). four outcomes related to Activity based costing: (two from each study)...........................11

Conclusion:..............................................................................................................................13

References:...............................................................................................................................14

Table of Contents

Executive Summary...................................................................................................................2

Introduction:...............................................................................................................................4

a) Explanation of Activity based Costing:.................................................................................5

b). Explanation of purpose of both journal topics in the context of “Activity Based

Costing”..................................................................................................................................6

c). Similarities and Difference between analysis of findings:....................................................9

d). four outcomes related to Activity based costing: (two from each study)...........................11

Conclusion:..............................................................................................................................13

References:...............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-based costing (ABC) 4

Introduction:

The major purpose of making this report is to provide proper acknowledgment of using

management accounting tool in real life organisation. This reading is based on research

journal articles which will explain importance, use and significance of management

accounting tool through detailed analysis. Analysis will be based on accounting and

management journal and articles. Activity based costing is to be chosen as per instructions

and purpose of this study will be explained based on two research management articles. A

proper discussion will be made based on similarities and differences in findings of two

research articles. It will include a recommendations and outcomes out of research findings

which will justify usage of management accounting systems (tools) in Australia Company.

For this purpose, an organisation will be taken as example named CIMIC Group.

Introduction:

The major purpose of making this report is to provide proper acknowledgment of using

management accounting tool in real life organisation. This reading is based on research

journal articles which will explain importance, use and significance of management

accounting tool through detailed analysis. Analysis will be based on accounting and

management journal and articles. Activity based costing is to be chosen as per instructions

and purpose of this study will be explained based on two research management articles. A

proper discussion will be made based on similarities and differences in findings of two

research articles. It will include a recommendations and outcomes out of research findings

which will justify usage of management accounting systems (tools) in Australia Company.

For this purpose, an organisation will be taken as example named CIMIC Group.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-based costing (ABC) 5

a) Explanation of Activity based Costing:

Activity Base costing system succeeded in products and services. ABC view use in

purchasing department. Activity Base Costing acceptable in cost calculation and managerial

accounting as a very useful system. Activity Base Costing is a type of managerial accounting

which define the cost of activities without the effect of other variables that result provided to

management on time. It’s kind of a tool to evaluate operating cost & in result provide method

of understand the underlying activities of existing cost. ABC also gives the accurate

information about cost of resource demands from customers, services, individual products

(Horngren, et al., 2013).

Characteristics of ABC Costing

ABC is a costing system. It’s provided the detail about cost of each activity along with

resource to all service and products. ABC also provides non-production cost. ABC help in

management account. ABC provides more accurate information about product & service that

any other system provides. Activity Base Costing defines the true cost of each product &

service with accuracy. With the help of Activity Base Costing, it recognises business

operations for taking decision. ABC is mostly using by manufacture company. This will help

to manufacture for his business plan. From the Activity Base Costing manufacture earns more

profit & defines the accuracy of investing amount & knows about the actual product cost.

Activity Base Costing processes this in three steps. This can collect the data from cost of

product & assemble the overhead cost. ABC couldn’t collect the data from accumulating all

cost (Rajasekaran & Lalitha, 2011).

Its transfers overhead cost from high rate to low rate. Some time it difficult to know about

the actual cost of product due to some indirect cost, employee salary etc. for these types of

data we unable to understand about the actual cost of product (Fisher, 2015)

a) Explanation of Activity based Costing:

Activity Base costing system succeeded in products and services. ABC view use in

purchasing department. Activity Base Costing acceptable in cost calculation and managerial

accounting as a very useful system. Activity Base Costing is a type of managerial accounting

which define the cost of activities without the effect of other variables that result provided to

management on time. It’s kind of a tool to evaluate operating cost & in result provide method

of understand the underlying activities of existing cost. ABC also gives the accurate

information about cost of resource demands from customers, services, individual products

(Horngren, et al., 2013).

Characteristics of ABC Costing

ABC is a costing system. It’s provided the detail about cost of each activity along with

resource to all service and products. ABC also provides non-production cost. ABC help in

management account. ABC provides more accurate information about product & service that

any other system provides. Activity Base Costing defines the true cost of each product &

service with accuracy. With the help of Activity Base Costing, it recognises business

operations for taking decision. ABC is mostly using by manufacture company. This will help

to manufacture for his business plan. From the Activity Base Costing manufacture earns more

profit & defines the accuracy of investing amount & knows about the actual product cost.

Activity Base Costing processes this in three steps. This can collect the data from cost of

product & assemble the overhead cost. ABC couldn’t collect the data from accumulating all

cost (Rajasekaran & Lalitha, 2011).

Its transfers overhead cost from high rate to low rate. Some time it difficult to know about

the actual cost of product due to some indirect cost, employee salary etc. for these types of

data we unable to understand about the actual cost of product (Fisher, 2015)

Activity-based costing (ABC) 6

Financial mangers taking help of Activity Base Costing for gain more profits by knowing

actual cost of product. For knowing actual product cost, we need a multiple accounting

process & that can take much more time & not providing accurate data. So, we take help of

Activity base Costing & provide the accurate data & that process provides the actual cost of

product. This will exactly know about the profitable or unprofitable amount of nay product &

manufactures taking help of these data in their business. That can be easily earning more

profit. Activity Base Costing very helpful in his filed no any other system that can replace

Activity Base Costing System (Fisher, 2015).

Features of Activity based costing:

1. Activity Based Costing is a costing strategy in which all costing facts and information

related to process, products and departmental data are included.

2. Use of ABC Analysis can be done to compare cost data with previous movement of cost

and administrative cost flows and predetermined facts.

3. ABC analysis supports the management to enable their relevant and accurate

understanding of resources and responds to different cost as per process requirements.

4. Company can be made with the help of ABC analysis, it is moderate management tool that

monitor financial statement as per growth rate of company in business benefit concern

Accounting Based Costing come after more study & research. In this system to provide

accurate data this will change the face of accounting system. At that time when lack of

knowledge of costing & methods this will come & change complete the face of accounting.

It’s traditional way of overhead accounting.

b). Explanation of purpose of both journal topics in the context of “Activity Based

Costing”

In this research analysis based report, two research based article has been taken based on

Activity based costing, which is essential to make this study more reliable and specific in the

Financial mangers taking help of Activity Base Costing for gain more profits by knowing

actual cost of product. For knowing actual product cost, we need a multiple accounting

process & that can take much more time & not providing accurate data. So, we take help of

Activity base Costing & provide the accurate data & that process provides the actual cost of

product. This will exactly know about the profitable or unprofitable amount of nay product &

manufactures taking help of these data in their business. That can be easily earning more

profit. Activity Base Costing very helpful in his filed no any other system that can replace

Activity Base Costing System (Fisher, 2015).

Features of Activity based costing:

1. Activity Based Costing is a costing strategy in which all costing facts and information

related to process, products and departmental data are included.

2. Use of ABC Analysis can be done to compare cost data with previous movement of cost

and administrative cost flows and predetermined facts.

3. ABC analysis supports the management to enable their relevant and accurate

understanding of resources and responds to different cost as per process requirements.

4. Company can be made with the help of ABC analysis, it is moderate management tool that

monitor financial statement as per growth rate of company in business benefit concern

Accounting Based Costing come after more study & research. In this system to provide

accurate data this will change the face of accounting system. At that time when lack of

knowledge of costing & methods this will come & change complete the face of accounting.

It’s traditional way of overhead accounting.

b). Explanation of purpose of both journal topics in the context of “Activity Based

Costing”

In this research analysis based report, two research based article has been taken based on

Activity based costing, which is essential to make this study more reliable and specific in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-based costing (ABC) 7

context of business operational decisions. These research journals will explain the significant

use of Activity Based Costing in the business (CIMIC group).

The first journal “Accounting and Management Accounting systems” which explain the topic

titles” the relationship between activities based costing, business strategy and performance in

Moroccan enterprises”. The second Journal name of Accounting and business management

which depicts about Activity based costing and its strategies. The major purpose of using

both research Journal as supportive article is to make proper understanding of “how Activity

Based Costing” works”, “How it can be used in the business decision of the company.

Purpose:

The purpose of this study and using both journals is to refining more specific general

approaches of defining and evaluating more exact and reliable product cost and business

activity based on process. Activity based costing is accounting analysis methods which

developed by Cooper and Kalpan to assign all overhead end projects, jobs and process. The

use of these research journals attempt to elaborate an important topics related to activity

based costing and its usage in business operations. It major aim is to justify the rectify the

nature of ABC analysis and to determine the projected profit of this application to the

company under research. To research perspective, now a days the light of exploring interest

in the matter of benefit and of the implication of ABC systems in CIMIC Group of the

company (Innes, & Mitchell, 2011)

Both researches Journal attain similar purpose and objective of study:

1. Basically, it will highlight the process and concept of ABC systems in relation to

know and understand the application of ABC analysis.

2. To verify the ways and benefits of implication of ABC systems in the Business

operation.

context of business operational decisions. These research journals will explain the significant

use of Activity Based Costing in the business (CIMIC group).

The first journal “Accounting and Management Accounting systems” which explain the topic

titles” the relationship between activities based costing, business strategy and performance in

Moroccan enterprises”. The second Journal name of Accounting and business management

which depicts about Activity based costing and its strategies. The major purpose of using

both research Journal as supportive article is to make proper understanding of “how Activity

Based Costing” works”, “How it can be used in the business decision of the company.

Purpose:

The purpose of this study and using both journals is to refining more specific general

approaches of defining and evaluating more exact and reliable product cost and business

activity based on process. Activity based costing is accounting analysis methods which

developed by Cooper and Kalpan to assign all overhead end projects, jobs and process. The

use of these research journals attempt to elaborate an important topics related to activity

based costing and its usage in business operations. It major aim is to justify the rectify the

nature of ABC analysis and to determine the projected profit of this application to the

company under research. To research perspective, now a days the light of exploring interest

in the matter of benefit and of the implication of ABC systems in CIMIC Group of the

company (Innes, & Mitchell, 2011)

Both researches Journal attain similar purpose and objective of study:

1. Basically, it will highlight the process and concept of ABC systems in relation to

know and understand the application of ABC analysis.

2. To verify the ways and benefits of implication of ABC systems in the Business

operation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-based costing (ABC) 8

3. Adoption rate of ABC systems in Australia, how it works in the different business

environment of Australia.

4. How ABC strategies impacts on business decisions and usage of ABS concept

impacts business performance (Gosselin, 2017)

5. How it affects the global rises of financial decisions and accounting standards in

business?

From the above points, both Journals want to give proper review related to the concepts of

ABC systems and its decision making process. Journal “Accounting and Management

accounting” depicts the uses of ABC systems. In this research, the study concludes that if

company wants to imply this systems as management tool, they will definitely lead to

efficiency with two major benefits: firstly, able to develop internal management, processes

and acts within the organisation and it observes the indirect and recovery cost than traditional

management systems (Arora, 2013).

Other management journal “ “Journal of accounting business and management” shows an

explanation most specific and to expand the concept of ABC systems. Hence, the major

motive of study such topics related to ABC systems. It explains the number of reasons also to

be stated after ABC adoption. Overall research are to be and on explained topics. It will

provide the number of detection of fraud and ABC Company met their requirement as per

their requirements (Foster & Swenson, 2017) “for the manufacture some product consumes

the activity & activity consume the costing. This system provides directly & indirectly costs

information about the product. This will automatically help in improve the process of

production. These provide more advantage & benefits. So, manufacture just need to know

about this system method & technique. The company must provide training about this system

for his mangers &b Employee. So, they can know about this system & apply this with get

3. Adoption rate of ABC systems in Australia, how it works in the different business

environment of Australia.

4. How ABC strategies impacts on business decisions and usage of ABS concept

impacts business performance (Gosselin, 2017)

5. How it affects the global rises of financial decisions and accounting standards in

business?

From the above points, both Journals want to give proper review related to the concepts of

ABC systems and its decision making process. Journal “Accounting and Management

accounting” depicts the uses of ABC systems. In this research, the study concludes that if

company wants to imply this systems as management tool, they will definitely lead to

efficiency with two major benefits: firstly, able to develop internal management, processes

and acts within the organisation and it observes the indirect and recovery cost than traditional

management systems (Arora, 2013).

Other management journal “ “Journal of accounting business and management” shows an

explanation most specific and to expand the concept of ABC systems. Hence, the major

motive of study such topics related to ABC systems. It explains the number of reasons also to

be stated after ABC adoption. Overall research are to be and on explained topics. It will

provide the number of detection of fraud and ABC Company met their requirement as per

their requirements (Foster & Swenson, 2017) “for the manufacture some product consumes

the activity & activity consume the costing. This system provides directly & indirectly costs

information about the product. This will automatically help in improve the process of

production. These provide more advantage & benefits. So, manufacture just need to know

about this system method & technique. The company must provide training about this system

for his mangers &b Employee. So, they can know about this system & apply this with get

Activity-based costing (ABC) 9

much more accurate information about product costing. At the end it will directly get

beneficial for taking quick decisions & process of production.

c). Similarities and Difference between analysis of findings:

1. Similarities between both Journal study:

Particulars Journal of Business and

Management

Accounting and management

information system

1. Business

strategy

Through this research of study, it

is observed that ABC Model

helps to measure assigned

performance to activities on

consumptions of reliable acts and

data.

This Journal explains about ABC

model that it helps in measuring

business performance and cost

effectiveness through business

decisions making activities.

2. Effectiveness

of costing

Writers in this Journal explain

that ABC model recognises the

usual and casual relationship of

cost and performance in business

operations. It provides not only

cost features and accurate results

through cost analysis after

designing product (exist or new

product) (Pigott , 2012).

The writers of this journal

delivers the same objective of

ABC management tools, they

explain that ABC model of

management accounting compare

projected and actual product of

cost to measure them in time and

give accurate and exact result of

profit.

Performance

appraisal

Through this Journal, it is said

that ABC accounting describes

reliable and accuracy in product

to determine cost and appraise

performance of product

ABC model helps in focusing cost

determination by bringing

reliability and effectiveness in

manufacturing, distribution

performance of product.

Identification of cost

behaviour

THIS Journal explains that ABC

costing recognises reality of cost

behaviour by advanced

technology, environmental

manufacturing activity.

This journal delivers the same

aspects. It is said that ABC Model

explore and helps in identifying

possible behaviour of cost through

control fixed cost overhead and

variable cost in the relation of

manufacturing and distribution

product activities.

ABC brings an accuracy and

effectiveness related to products

on cause and effect relationship

for the incurrence of cost.

It explains that ABC model study

of cost behaviour based on

process and products value which

evaluate the relationship between

cost effectiveness and causes

(Neumann et. al., 2014).

much more accurate information about product costing. At the end it will directly get

beneficial for taking quick decisions & process of production.

c). Similarities and Difference between analysis of findings:

1. Similarities between both Journal study:

Particulars Journal of Business and

Management

Accounting and management

information system

1. Business

strategy

Through this research of study, it

is observed that ABC Model

helps to measure assigned

performance to activities on

consumptions of reliable acts and

data.

This Journal explains about ABC

model that it helps in measuring

business performance and cost

effectiveness through business

decisions making activities.

2. Effectiveness

of costing

Writers in this Journal explain

that ABC model recognises the

usual and casual relationship of

cost and performance in business

operations. It provides not only

cost features and accurate results

through cost analysis after

designing product (exist or new

product) (Pigott , 2012).

The writers of this journal

delivers the same objective of

ABC management tools, they

explain that ABC model of

management accounting compare

projected and actual product of

cost to measure them in time and

give accurate and exact result of

profit.

Performance

appraisal

Through this Journal, it is said

that ABC accounting describes

reliable and accuracy in product

to determine cost and appraise

performance of product

ABC model helps in focusing cost

determination by bringing

reliability and effectiveness in

manufacturing, distribution

performance of product.

Identification of cost

behaviour

THIS Journal explains that ABC

costing recognises reality of cost

behaviour by advanced

technology, environmental

manufacturing activity.

This journal delivers the same

aspects. It is said that ABC Model

explore and helps in identifying

possible behaviour of cost through

control fixed cost overhead and

variable cost in the relation of

manufacturing and distribution

product activities.

ABC brings an accuracy and

effectiveness related to products

on cause and effect relationship

for the incurrence of cost.

It explains that ABC model study

of cost behaviour based on

process and products value which

evaluate the relationship between

cost effectiveness and causes

(Neumann et. al., 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity-based costing (ABC) 10

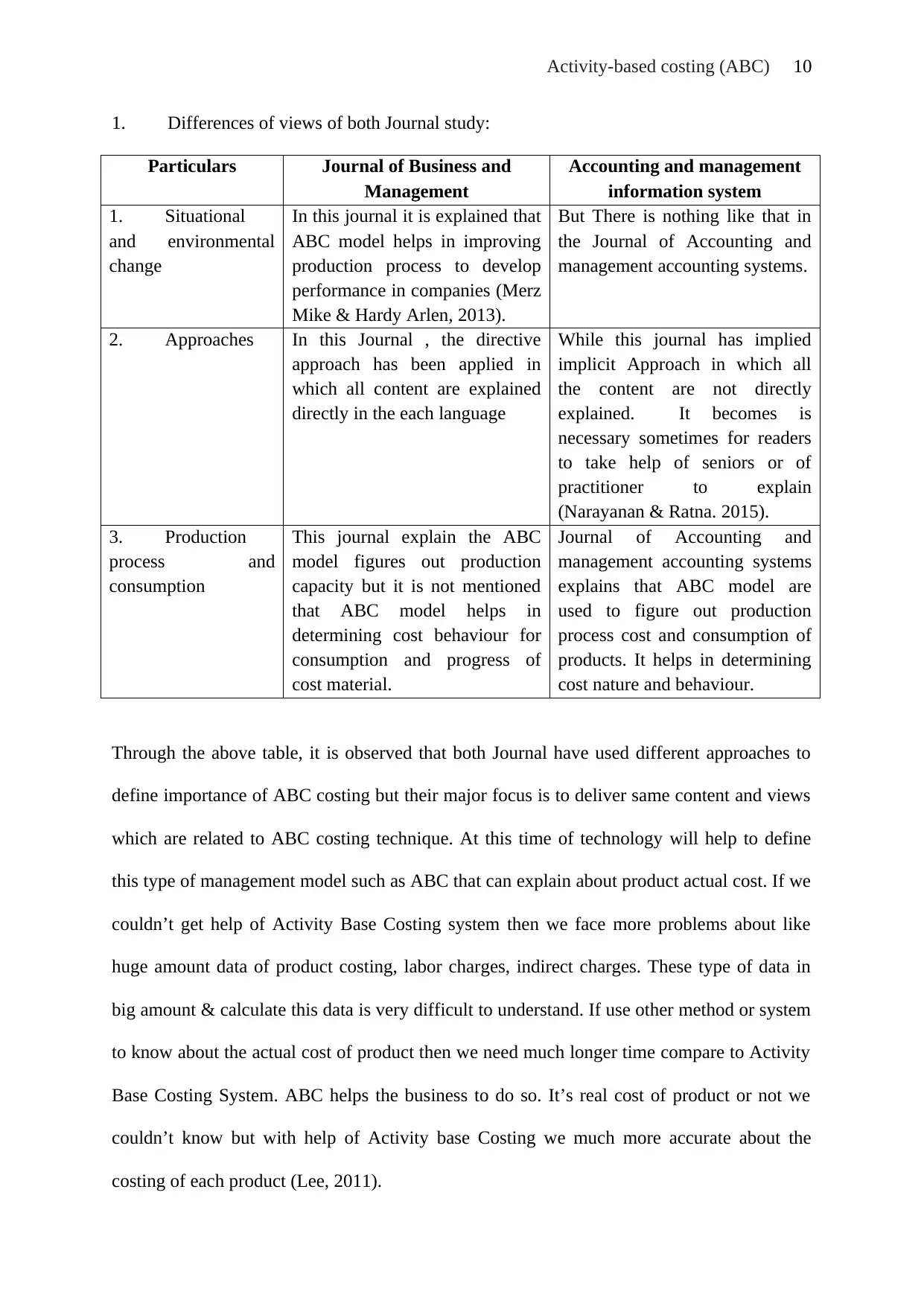

1. Differences of views of both Journal study:

Particulars Journal of Business and

Management

Accounting and management

information system

1. Situational

and environmental

change

In this journal it is explained that

ABC model helps in improving

production process to develop

performance in companies (Merz

Mike & Hardy Arlen, 2013).

But There is nothing like that in

the Journal of Accounting and

management accounting systems.

2. Approaches In this Journal , the directive

approach has been applied in

which all content are explained

directly in the each language

While this journal has implied

implicit Approach in which all

the content are not directly

explained. It becomes is

necessary sometimes for readers

to take help of seniors or of

practitioner to explain

(Narayanan & Ratna. 2015).

3. Production

process and

consumption

This journal explain the ABC

model figures out production

capacity but it is not mentioned

that ABC model helps in

determining cost behaviour for

consumption and progress of

cost material.

Journal of Accounting and

management accounting systems

explains that ABC model are

used to figure out production

process cost and consumption of

products. It helps in determining

cost nature and behaviour.

Through the above table, it is observed that both Journal have used different approaches to

define importance of ABC costing but their major focus is to deliver same content and views

which are related to ABC costing technique. At this time of technology will help to define

this type of management model such as ABC that can explain about product actual cost. If we

couldn’t get help of Activity Base Costing system then we face more problems about like

huge amount data of product costing, labor charges, indirect charges. These type of data in

big amount & calculate this data is very difficult to understand. If use other method or system

to know about the actual cost of product then we need much longer time compare to Activity

Base Costing System. ABC helps the business to do so. It’s real cost of product or not we

couldn’t know but with help of Activity base Costing we much more accurate about the

costing of each product (Lee, 2011).

1. Differences of views of both Journal study:

Particulars Journal of Business and

Management

Accounting and management

information system

1. Situational

and environmental

change

In this journal it is explained that

ABC model helps in improving

production process to develop

performance in companies (Merz

Mike & Hardy Arlen, 2013).

But There is nothing like that in

the Journal of Accounting and

management accounting systems.

2. Approaches In this Journal , the directive

approach has been applied in

which all content are explained

directly in the each language

While this journal has implied

implicit Approach in which all

the content are not directly

explained. It becomes is

necessary sometimes for readers

to take help of seniors or of

practitioner to explain

(Narayanan & Ratna. 2015).

3. Production

process and

consumption

This journal explain the ABC

model figures out production

capacity but it is not mentioned

that ABC model helps in

determining cost behaviour for

consumption and progress of

cost material.

Journal of Accounting and

management accounting systems

explains that ABC model are

used to figure out production

process cost and consumption of

products. It helps in determining

cost nature and behaviour.

Through the above table, it is observed that both Journal have used different approaches to

define importance of ABC costing but their major focus is to deliver same content and views

which are related to ABC costing technique. At this time of technology will help to define

this type of management model such as ABC that can explain about product actual cost. If we

couldn’t get help of Activity Base Costing system then we face more problems about like

huge amount data of product costing, labor charges, indirect charges. These type of data in

big amount & calculate this data is very difficult to understand. If use other method or system

to know about the actual cost of product then we need much longer time compare to Activity

Base Costing System. ABC helps the business to do so. It’s real cost of product or not we

couldn’t know but with help of Activity base Costing we much more accurate about the

costing of each product (Lee, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity-based costing (ABC) 11

d). four outcomes related to Activity based costing: (two from each study)

Journal of Business and management:

1. Accuracy check of Cost behaviour: “Journal of business and management” explain

that ABC model is the concept which checks the accuracy of cost behaviour and

product reliability and durability. Through this Journal, it can be understood that

usage of ABC model in the business help in checking accuracy behaviour, to figure

out causes of treats and trace the area of costs related to managerial responsibility.

2. Performance development: According to this Journal, ABC management tools

improve management process which help in determining cost, it increase the

performance of the cost as per cost opportunity matters. It develops the program and

development performance in order to deliver projects and output on time. It improves

the managerial and financial position based on competitive era of companies (Kaplan

Robert, 2012).

3. Accounting and Management accounting systems:

Measure complexity of projects: ABC model helps in determining and measuring

complexity of big projects, it helps the management of the company to evaluate

business operations cost and product performance based on complex nature of the

projects. ABC model use cost analysis concept in order to determine and control

additional cost. This journal also explains that companies can evaluate their product

transparency and reliability of project in order to make them more productive and

much easier than other projects. It recognises all usual and casual relationship

regarding cost driver to activities. Journal has also explained (Turney Peter & Stratton

Alan. 2018).

4. Providing financial information: Through this Journal, we can understand that ABC

model is able to explore financial and non-financial model both effectively. It helps in

d). four outcomes related to Activity based costing: (two from each study)

Journal of Business and management:

1. Accuracy check of Cost behaviour: “Journal of business and management” explain

that ABC model is the concept which checks the accuracy of cost behaviour and

product reliability and durability. Through this Journal, it can be understood that

usage of ABC model in the business help in checking accuracy behaviour, to figure

out causes of treats and trace the area of costs related to managerial responsibility.

2. Performance development: According to this Journal, ABC management tools

improve management process which help in determining cost, it increase the

performance of the cost as per cost opportunity matters. It develops the program and

development performance in order to deliver projects and output on time. It improves

the managerial and financial position based on competitive era of companies (Kaplan

Robert, 2012).

3. Accounting and Management accounting systems:

Measure complexity of projects: ABC model helps in determining and measuring

complexity of big projects, it helps the management of the company to evaluate

business operations cost and product performance based on complex nature of the

projects. ABC model use cost analysis concept in order to determine and control

additional cost. This journal also explains that companies can evaluate their product

transparency and reliability of project in order to make them more productive and

much easier than other projects. It recognises all usual and casual relationship

regarding cost driver to activities. Journal has also explained (Turney Peter & Stratton

Alan. 2018).

4. Providing financial information: Through this Journal, we can understand that ABC

model is able to explore financial and non-financial model both effectively. It helps in

Activity-based costing (ABC) 12

define accuracy and reliability of each product. It creates high benefits, which helps

the companies to application of ABC model within their organisation effectively. It is

based on new technology which provides transparent and effective results related to

the financial business decisions (Jawahar Lal, 2016).

Activity Base Costing System provide overhead accounting data. This will help to rectify the

inaccurate cost information. This is just because of we choose wrong type of method. From

the Activity Base Costing System, we redesign the structure of any product costing. We

improve over decision of product price.

From this method the manufactures get benefit from known about the actual cost of product.

If manufactures not use this system, then they fear about potential loss of status

&manufacture always feels fear about product pricing.

Just because of the costing calculation amount is big & hard to get accurate data. In this we

use ABC system & break out these barriers of fear.

For use of Activity Base Costing System, every mangers & Employee will be aware of this

system & know about its technique & formulas so that they can study & collect all required

data & process through ABC system (Cooper & Kaplan, 2018).

define accuracy and reliability of each product. It creates high benefits, which helps

the companies to application of ABC model within their organisation effectively. It is

based on new technology which provides transparent and effective results related to

the financial business decisions (Jawahar Lal, 2016).

Activity Base Costing System provide overhead accounting data. This will help to rectify the

inaccurate cost information. This is just because of we choose wrong type of method. From

the Activity Base Costing System, we redesign the structure of any product costing. We

improve over decision of product price.

From this method the manufactures get benefit from known about the actual cost of product.

If manufactures not use this system, then they fear about potential loss of status

&manufacture always feels fear about product pricing.

Just because of the costing calculation amount is big & hard to get accurate data. In this we

use ABC system & break out these barriers of fear.

For use of Activity Base Costing System, every mangers & Employee will be aware of this

system & know about its technique & formulas so that they can study & collect all required

data & process through ABC system (Cooper & Kaplan, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.