Managerial Accounting Report: ABC Model for National Australia Bank

VerifiedAdded on 2021/05/31

|12

|2452

|158

Report

AI Summary

This report provides a comprehensive evaluation of the Activity-Based Costing (ABC) model from a business perspective, specifically focusing on its application to the National Australia Bank (NAB). The report explores the features of the ABC model, its alignment with NAB's goals and strategies, and offers recommendations for its implementation. It also identifies budgetary control as a suitable management accounting tool for NAB. The report highlights how the ABC model can help NAB identify cost-generating activities and allocate costs effectively, ultimately leading to improved decision-making and cost management. The analysis includes a profitability model and emphasizes the importance of top management support and cross-functional teams in implementing the ABC model successfully. The conclusion reinforces the benefits of the ABC model for NAB, including improved cost allocation and enhanced awareness of customer needs, alongside the utility of budgetary control for variance analysis.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The current report intends to provide brief evaluation of the activity-based costing (ABC)

model along with its characteristics from the business perspective. For meeting the purpose of

this report, the model is associated with an ASX listed organisation for improving the

management accounting information present to its top management team. In this report,

National Australia Bank (NAB) is selected, which is one of the biggest financial institutions in

Australia in terms of earnings, market capitalisation and customers. ABC model is of utmost

importance, as this model helps in identifying those departments or activities generating lower

income for the bank. As a result, NAB could assign higher costs to those activities based on the

customer needs for minimising their overall cost along with increasing the awareness of the

customers. Finally, another management accounting tool that is suitable for NAB is identified as

NAB, since the managers of the bank could identify the variances from the actual budget.

Accordingly, corrective actions could be taken to minimise those variances and errors in

external reports.

Executive Summary:

The current report intends to provide brief evaluation of the activity-based costing (ABC)

model along with its characteristics from the business perspective. For meeting the purpose of

this report, the model is associated with an ASX listed organisation for improving the

management accounting information present to its top management team. In this report,

National Australia Bank (NAB) is selected, which is one of the biggest financial institutions in

Australia in terms of earnings, market capitalisation and customers. ABC model is of utmost

importance, as this model helps in identifying those departments or activities generating lower

income for the bank. As a result, NAB could assign higher costs to those activities based on the

customer needs for minimising their overall cost along with increasing the awareness of the

customers. Finally, another management accounting tool that is suitable for NAB is identified as

NAB, since the managers of the bank could identify the variances from the actual budget.

Accordingly, corrective actions could be taken to minimise those variances and errors in

external reports.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................3

a) Explanation of activity-based costing (ABC) model and its features:.........................................3

b) Alignment of ABC model with the current goals and strategies of NAB:....................................4

i) Mission and objectives of NAB:................................................................................................4

ii) Corporate strategies of NAB:...................................................................................................5

iii) Role of ABC model in achieving the strategies of NAB:..........................................................5

c) Two recommendations about the implementation of ABC model for NAB:...............................7

d) Suitable management accounting tool suitable for NAB besides ABC model:...........................8

Conclusion:......................................................................................................................................9

References:....................................................................................................................................10

Table of Contents

Introduction:....................................................................................................................................3

a) Explanation of activity-based costing (ABC) model and its features:.........................................3

b) Alignment of ABC model with the current goals and strategies of NAB:....................................4

i) Mission and objectives of NAB:................................................................................................4

ii) Corporate strategies of NAB:...................................................................................................5

iii) Role of ABC model in achieving the strategies of NAB:..........................................................5

c) Two recommendations about the implementation of ABC model for NAB:...............................7

d) Suitable management accounting tool suitable for NAB besides ABC model:...........................8

Conclusion:......................................................................................................................................9

References:....................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

The current report intends to provide brief evaluation of the activity-based costing (ABC)

model along with its characteristics from the business perspective. For meeting the purpose of

this report, the model is associated with an ASX listed organisation for improving the

management accounting information present to its top management team. In this report,

National Australia Bank (NAB) is selected, which is one of the biggest financial institutions in

Australia in terms of earnings, market capitalisation and customers. Based on the existing goals

and corporate strategies of NAB, the alignment is made with the ABC model for enabling the

top management of the bank so that suitable decisions could be undertaken. In addition, the

report lays emphasis on providing recommendations regarding the ways the ABC model could

be implemented in NAB. Finally, the report sheds light on suggesting another management

accounting tool for NAB that would aid in the decision-making process of the top management.

a) Explanation of activity-based costing (ABC) model and its features:

ABC model is a method of accounting that identifies the activities performed on the part

of an organisation and after this; the indirect costs are allocated to products. In other words,

this model realises the association among activities, costs and products and with the help of

such relationship, the indirect costs are assigned to products less arbitrarily compared to the

conventional models of accounting (Al-Nuaimi, Mohamed and Alekam 2017). ABC model

has certain features, which are enumerated briefly as follows:

Introduction:

The current report intends to provide brief evaluation of the activity-based costing (ABC)

model along with its characteristics from the business perspective. For meeting the purpose of

this report, the model is associated with an ASX listed organisation for improving the

management accounting information present to its top management team. In this report,

National Australia Bank (NAB) is selected, which is one of the biggest financial institutions in

Australia in terms of earnings, market capitalisation and customers. Based on the existing goals

and corporate strategies of NAB, the alignment is made with the ABC model for enabling the

top management of the bank so that suitable decisions could be undertaken. In addition, the

report lays emphasis on providing recommendations regarding the ways the ABC model could

be implemented in NAB. Finally, the report sheds light on suggesting another management

accounting tool for NAB that would aid in the decision-making process of the top management.

a) Explanation of activity-based costing (ABC) model and its features:

ABC model is a method of accounting that identifies the activities performed on the part

of an organisation and after this; the indirect costs are allocated to products. In other words,

this model realises the association among activities, costs and products and with the help of

such relationship, the indirect costs are assigned to products less arbitrarily compared to the

conventional models of accounting (Al-Nuaimi, Mohamed and Alekam 2017). ABC model

has certain features, which are enumerated briefly as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

In this model, costs are segregated into fixed costs and variable costs, which is

significant in providing quality information for developing an appropriate cost system in

a business organisation.

The patterns in cost behaviour could be distinguished properly with the help of this

model (Banker and Byzalov 2014).

The patterns in cost behaviour have direct linkages with volume, diversity, time and

events.

b) Alignment of ABC model with the current goals and strategies of NAB:

For aligning with the goals and strategies of NAB, it is necessary to identify them initially

and then the role of the ABC model has been discussed to aid in achieving the strategies of the

bank.

i) Mission and objectives of NAB:

The mission of NAB is to deliver suitable solutions to its customers by bearing in mind

their needs. The bank believes that profitability is extremely crucial in order to ensure its long-

term success in the Australian financial services sector. In addition, it emphasises on developing

a working environment that would help in strengthening the morale and confidence of its

employees (Nab.com.au 2018). NAB intends to become the most reputed bank in Australia by

aiding in the smooth flow of capital and money in the market for meeting the customer

requirements.

In this model, costs are segregated into fixed costs and variable costs, which is

significant in providing quality information for developing an appropriate cost system in

a business organisation.

The patterns in cost behaviour could be distinguished properly with the help of this

model (Banker and Byzalov 2014).

The patterns in cost behaviour have direct linkages with volume, diversity, time and

events.

b) Alignment of ABC model with the current goals and strategies of NAB:

For aligning with the goals and strategies of NAB, it is necessary to identify them initially

and then the role of the ABC model has been discussed to aid in achieving the strategies of the

bank.

i) Mission and objectives of NAB:

The mission of NAB is to deliver suitable solutions to its customers by bearing in mind

their needs. The bank believes that profitability is extremely crucial in order to ensure its long-

term success in the Australian financial services sector. In addition, it emphasises on developing

a working environment that would help in strengthening the morale and confidence of its

employees (Nab.com.au 2018). NAB intends to become the most reputed bank in Australia by

aiding in the smooth flow of capital and money in the market for meeting the customer

requirements.

5MANAGERIAL ACCOUNTING

ii) Corporate strategies of NAB:

The main corporate strategies that NAB uses for marketing its products and services

constitute of the following:

Emphasis is placed on advertising three kinds of products that include business loans,

home loans and credit cards.

NAB emphasises on its brand awareness for ensuring the growth of the financial

institution along with attaining first mover advantage to maintain competitive

advantage in the long-run.

NAB has adopted certain strategies like minimising the interest rate on loans and

cutting ATM fees for attracting its customers to sustain competitive advantage in the

market (Al-Bawab and Al-Rawashdeh 2016).

iii) Role of ABC model in achieving the strategies of NAB:

Although ABC model is more popular in the global manufacturing sector, its significance

to the services sector could not be ignored because of the varying features of the two types of

industries. As advocated by Butler and Ghosh (2015), there are no direct costs for the financial

institutions, as majority of the costs are treated as overheads. In addition, these institutions do

not hold service stocks, as the services are consumed at the time they are produced.

ABC model contains three sections, which include activity, resource and cost object

(Cooper 2017). In case of NAB, the resource section includes expenses associated with different

departments like cost centres or functions. The grouping of these departments is made at

corporate office, branches, channels such as call centres, direct selling agents, ATM, internet

ii) Corporate strategies of NAB:

The main corporate strategies that NAB uses for marketing its products and services

constitute of the following:

Emphasis is placed on advertising three kinds of products that include business loans,

home loans and credit cards.

NAB emphasises on its brand awareness for ensuring the growth of the financial

institution along with attaining first mover advantage to maintain competitive

advantage in the long-run.

NAB has adopted certain strategies like minimising the interest rate on loans and

cutting ATM fees for attracting its customers to sustain competitive advantage in the

market (Al-Bawab and Al-Rawashdeh 2016).

iii) Role of ABC model in achieving the strategies of NAB:

Although ABC model is more popular in the global manufacturing sector, its significance

to the services sector could not be ignored because of the varying features of the two types of

industries. As advocated by Butler and Ghosh (2015), there are no direct costs for the financial

institutions, as majority of the costs are treated as overheads. In addition, these institutions do

not hold service stocks, as the services are consumed at the time they are produced.

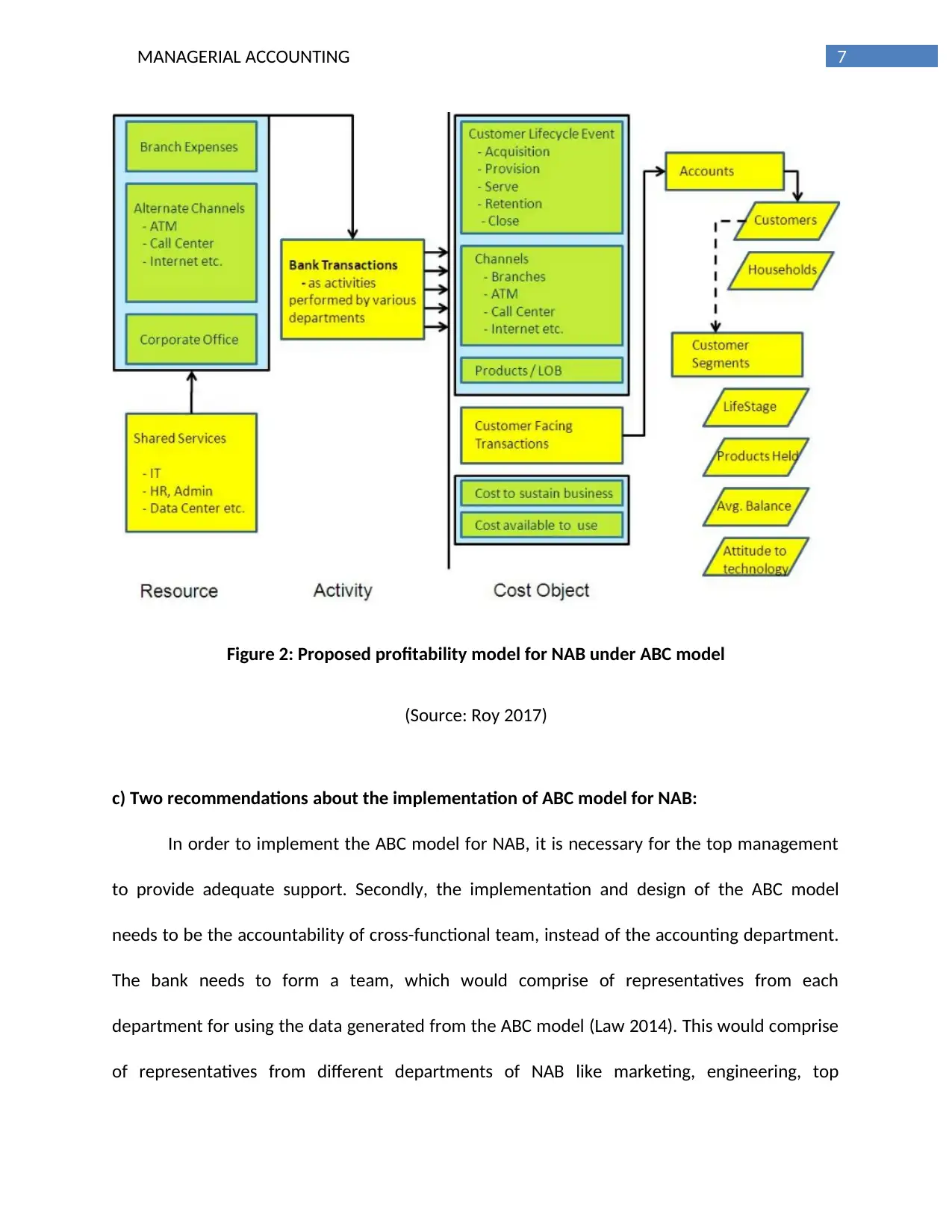

ABC model contains three sections, which include activity, resource and cost object

(Cooper 2017). In case of NAB, the resource section includes expenses associated with different

departments like cost centres or functions. The grouping of these departments is made at

corporate office, branches, channels such as call centres, direct selling agents, ATM, internet

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

and shared service departments such as human resource and information technology. The

services of the shared service departments are described and accordingly, the costs are

computed (Dale and Plunkett 2017). Depending on the service volume of the departments, the

costs are transferred to the other departments.

In NAB, the activities are described in accordance with the transactions that the

customers perform for different products utilising various channels like commercial loan

origination. In this case, the activities might be obtaining the application, interviewing the

applicant, overview of credit history along with evaluation of the applicant, undertaking

decision and loan amount disbursement. After defining all the transactions, they would be

segregated into activities in the ABC model (Edmonds et al. 2016). As a result, NAB could be

able to reduce the burden of ATM costs on customers while the interest on loans could be

lowered as well. Moreover, the cost of adopting new technologies to provide effective support

to the customers could be minimised as well.

In relation to cost object section, it needs to be segregated into two parts. The initial

section computes the different transaction costs that the customers have performed for

different products by using different distribution channels (Keller 2015). This might be in the

form of withdrawing cash via ATM for savings account. In this case, it could be observed that

cash withdrawal for current account and savings account might not differ for NAB; however, it

is necessary to compute the costs separately. Moreover, such identification of accounts would

help NAB to identify the customers making frequent cash withdrawals and accordingly, credit

cards would be provided to them at minimised rate of interest.

and shared service departments such as human resource and information technology. The

services of the shared service departments are described and accordingly, the costs are

computed (Dale and Plunkett 2017). Depending on the service volume of the departments, the

costs are transferred to the other departments.

In NAB, the activities are described in accordance with the transactions that the

customers perform for different products utilising various channels like commercial loan

origination. In this case, the activities might be obtaining the application, interviewing the

applicant, overview of credit history along with evaluation of the applicant, undertaking

decision and loan amount disbursement. After defining all the transactions, they would be

segregated into activities in the ABC model (Edmonds et al. 2016). As a result, NAB could be

able to reduce the burden of ATM costs on customers while the interest on loans could be

lowered as well. Moreover, the cost of adopting new technologies to provide effective support

to the customers could be minimised as well.

In relation to cost object section, it needs to be segregated into two parts. The initial

section computes the different transaction costs that the customers have performed for

different products by using different distribution channels (Keller 2015). This might be in the

form of withdrawing cash via ATM for savings account. In this case, it could be observed that

cash withdrawal for current account and savings account might not differ for NAB; however, it

is necessary to compute the costs separately. Moreover, such identification of accounts would

help NAB to identify the customers making frequent cash withdrawals and accordingly, credit

cards would be provided to them at minimised rate of interest.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

Figure 2: Proposed profitability model for NAB under ABC model

(Source: Roy 2017)

c) Two recommendations about the implementation of ABC model for NAB:

In order to implement the ABC model for NAB, it is necessary for the top management

to provide adequate support. Secondly, the implementation and design of the ABC model

needs to be the accountability of cross-functional team, instead of the accounting department.

The bank needs to form a team, which would comprise of representatives from each

department for using the data generated from the ABC model (Law 2014). This would comprise

of representatives from different departments of NAB like marketing, engineering, top

Figure 2: Proposed profitability model for NAB under ABC model

(Source: Roy 2017)

c) Two recommendations about the implementation of ABC model for NAB:

In order to implement the ABC model for NAB, it is necessary for the top management

to provide adequate support. Secondly, the implementation and design of the ABC model

needs to be the accountability of cross-functional team, instead of the accounting department.

The bank needs to form a team, which would comprise of representatives from each

department for using the data generated from the ABC model (Law 2014). This would comprise

of representatives from different departments of NAB like marketing, engineering, top

8MANAGERIAL ACCOUNTING

management and accounting staffs having technical skills. It needs to appoint an external

consultant specialised in ABC model to seek advice for the team.

The top-level management of NAB needs to support the implementation of ABC model

because of two reasons. Firstly, in the absence of leadership from higher-level management,

the managers of the bank would be resistant towards change (Reider 2016). Secondly, if the top

management of NAB does not support the system, the subordinates might feel that there is less

significance of the ABC model and they might abandon the initiative. In addition, the cross-

functional teams need to be involved in the implementation of ABC model for suitable

allocation of costs to each department. As a result, it would help the bank to use the model for

external financial reports (Subramaniam and Watson 2016).

d) Suitable management accounting tool suitable for NAB besides ABC model:

Budgetary control is identified as another effective tool of management accounting for

NAB, since budgets play a significant part in planning and controlling and the managers use

them for planning, monitoring and controlling different activities at each organisational level.

There are certain benefits that NAB could derive by implementing budgetary control, which are

elucidated as follows:

The managers of NAB could integrate the efforts of the personnel within the bank

towards a common objective. Budgetary control would synchronise all the bank

activities and the bank could coordinate its efforts for accomplishing the set objectives

(Weygandt, Kimmel and Kieso 2015).

management and accounting staffs having technical skills. It needs to appoint an external

consultant specialised in ABC model to seek advice for the team.

The top-level management of NAB needs to support the implementation of ABC model

because of two reasons. Firstly, in the absence of leadership from higher-level management,

the managers of the bank would be resistant towards change (Reider 2016). Secondly, if the top

management of NAB does not support the system, the subordinates might feel that there is less

significance of the ABC model and they might abandon the initiative. In addition, the cross-

functional teams need to be involved in the implementation of ABC model for suitable

allocation of costs to each department. As a result, it would help the bank to use the model for

external financial reports (Subramaniam and Watson 2016).

d) Suitable management accounting tool suitable for NAB besides ABC model:

Budgetary control is identified as another effective tool of management accounting for

NAB, since budgets play a significant part in planning and controlling and the managers use

them for planning, monitoring and controlling different activities at each organisational level.

There are certain benefits that NAB could derive by implementing budgetary control, which are

elucidated as follows:

The managers of NAB could integrate the efforts of the personnel within the bank

towards a common objective. Budgetary control would synchronise all the bank

activities and the bank could coordinate its efforts for accomplishing the set objectives

(Weygandt, Kimmel and Kieso 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

If the managers of NAB identify that the expenses for a particular department are more

than the estimated budget, it requires special management action and attention.

Conclusion:

Based on the above evaluation, it could be cited that the ABC model helps in segregating

costs into variable costs and fixed costs in order to provide quality information to design an

effective cost system in a corporate entity. NAB is focused to maintain competitive advantage in

the Australian banking industry by providing quality services to the customers while minimising

the overall costs for both the customers and the bank. In this context, ABC model is of utmost

importance, as this model helps in identifying those departments or activities generating lower

income for the bank. As a result, NAB could assign higher costs to those activities based on the

customer needs for minimising their overall cost along with increasing the awareness of the

customers. Finally, another management accounting tool that is suitable for NAB is identified as

NAB, since the managers of the bank could identify the variances from the actual budget.

Accordingly, corrective actions could be taken to minimise those variances and errors in

external reports.

If the managers of NAB identify that the expenses for a particular department are more

than the estimated budget, it requires special management action and attention.

Conclusion:

Based on the above evaluation, it could be cited that the ABC model helps in segregating

costs into variable costs and fixed costs in order to provide quality information to design an

effective cost system in a corporate entity. NAB is focused to maintain competitive advantage in

the Australian banking industry by providing quality services to the customers while minimising

the overall costs for both the customers and the bank. In this context, ABC model is of utmost

importance, as this model helps in identifying those departments or activities generating lower

income for the bank. As a result, NAB could assign higher costs to those activities based on the

customer needs for minimising their overall cost along with increasing the awareness of the

customers. Finally, another management accounting tool that is suitable for NAB is identified as

NAB, since the managers of the bank could identify the variances from the actual budget.

Accordingly, corrective actions could be taken to minimise those variances and errors in

external reports.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

References:

Al-Bawab, A.A. and Al-Rawashdeh, H., 2016. The Impact of the Activity Based Costing System

(ABC) in the Pricing of Services Banks in the Jordanian commercial Banks: A Field

Study. International Business Research, 9(4), p.1.

Al-Nuaimi, S.I.M., Mohamed, R. and Alekam, J.M.E., 2017. The Link between Information

Technology, Activity-based Costing Implementation and Organizational

Performance. International Review of Management and Marketing, 7(1).

Baiman, S., 2014. Some ideas for further research in managerial accounting. Journal of

Management Accounting Research, 26(2), pp.119-121.

Banker, R.D. and Byzalov, D., 2014. Asymmetric cost behavior. Journal of Management

Accounting Research, 26(2), pp.43-79.

Butler, S.A. and Ghosh, D., 2015. Individual differences in managerial accounting judgments and

decision making. The British Accounting Review, 47(1), pp.33-45.

Cooper, R., 2017. Target costing and value engineering. Routledge.

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education.

Eldenburg, L.G., Wolcott, S.K., Chen, L.H. and Cook, G., 2016. Cost management: Measuring,

monitoring, and motivating performance. Wiley Global Education.

References:

Al-Bawab, A.A. and Al-Rawashdeh, H., 2016. The Impact of the Activity Based Costing System

(ABC) in the Pricing of Services Banks in the Jordanian commercial Banks: A Field

Study. International Business Research, 9(4), p.1.

Al-Nuaimi, S.I.M., Mohamed, R. and Alekam, J.M.E., 2017. The Link between Information

Technology, Activity-based Costing Implementation and Organizational

Performance. International Review of Management and Marketing, 7(1).

Baiman, S., 2014. Some ideas for further research in managerial accounting. Journal of

Management Accounting Research, 26(2), pp.119-121.

Banker, R.D. and Byzalov, D., 2014. Asymmetric cost behavior. Journal of Management

Accounting Research, 26(2), pp.43-79.

Butler, S.A. and Ghosh, D., 2015. Individual differences in managerial accounting judgments and

decision making. The British Accounting Review, 47(1), pp.33-45.

Cooper, R., 2017. Target costing and value engineering. Routledge.

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Edmonds, T.P., Edmonds, C.D., Tsay, B.Y. and Olds, P.R., 2016. Fundamental managerial

accounting concepts. McGraw-Hill Education.

Eldenburg, L.G., Wolcott, S.K., Chen, L.H. and Cook, G., 2016. Cost management: Measuring,

monitoring, and motivating performance. Wiley Global Education.

11MANAGERIAL ACCOUNTING

Keller, W.D., 2015. Cost and Managerial Accounting II Essentials (Vol. 2). Research & Education

Assoc.

Law, J. ed., 2014. A dictionary of finance and banking. Oxford University Press.

Nab.com.au., 2018. Personal. [online] Available at: https://www.nab.com.au/ [Accessed 9 May

2018].

Reider, B.P., 2016. ACTG 202.02: Principles of Managerial Accounting.

Roy, D.G., 2017. Activity Based Costing in Indian Banks. The Management Accountant

Journal, 52(5), pp.42-52

Subramaniam, C. and Watson, M.W., 2016. Additional evidence on the sticky behavior of costs.

In Advances in Management Accounting (pp. 275-305). Emerald Group Publishing Limited.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons.

Keller, W.D., 2015. Cost and Managerial Accounting II Essentials (Vol. 2). Research & Education

Assoc.

Law, J. ed., 2014. A dictionary of finance and banking. Oxford University Press.

Nab.com.au., 2018. Personal. [online] Available at: https://www.nab.com.au/ [Accessed 9 May

2018].

Reider, B.P., 2016. ACTG 202.02: Principles of Managerial Accounting.

Roy, D.G., 2017. Activity Based Costing in Indian Banks. The Management Accountant

Journal, 52(5), pp.42-52

Subramaniam, C. and Watson, M.W., 2016. Additional evidence on the sticky behavior of costs.

In Advances in Management Accounting (pp. 275-305). Emerald Group Publishing Limited.

Weygandt, J.J., Kimmel, P.D. and Kieso, D.E., 2015. Financial & managerial accounting. John

Wiley & Sons.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.