Activity Based Costing System for Harvey Norman Company

VerifiedAdded on 2023/06/11

|13

|3168

|117

AI Summary

This report discusses the compatibility of activity based costing system with Harvey Norman Company's operations and strategies. It also suggests an alternative management system.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Activity Based Costing System for Inharvey Norman Company 1

ACTIVITY BASED COSTING FOR HARVEY NORMAN COMPANY

Student by (Name)

Professor’s (Name)

College

Course

Date

ACTIVITY BASED COSTING FOR HARVEY NORMAN COMPANY

Student by (Name)

Professor’s (Name)

College

Course

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Activity Based Costing System for Inharvey Norman Company 2

ACTIVITY BASED COSTING FOR HARVEY NORMAN COMPANY

Executive summary

Harvey Norman Company is an Australian based company with massive operations from

its various departments and branches. The company wants to employ an effective management

and costing tool in its operations. Activity based costing is the recommended system. The report

shows the compatibility of the system to the company’s operations. The system is found to be in

line with most of company’s strategies and goals. Alternative system is also discussed. Time

based costing could be used in place of activity based costing due to its outstanding feature as

seen in the report.

ACTIVITY BASED COSTING FOR HARVEY NORMAN COMPANY

Executive summary

Harvey Norman Company is an Australian based company with massive operations from

its various departments and branches. The company wants to employ an effective management

and costing tool in its operations. Activity based costing is the recommended system. The report

shows the compatibility of the system to the company’s operations. The system is found to be in

line with most of company’s strategies and goals. Alternative system is also discussed. Time

based costing could be used in place of activity based costing due to its outstanding feature as

seen in the report.

Activity Based Costing System for Inharvey Norman Company 3

Table of Contents

Introduction...............................................................................................................................................2

Activity based costing and its features.....................................................................................................3

Definition................................................................................................................................................3

Key features of activity based costing..................................................................................................3

How activity based costing aligns with corporate strategies and objectives of Harvey Norman

limited company........................................................................................................................................4

Mission of Harvey Norman Company.................................................................................................4

Objective of Harvey Norman Company..............................................................................................4

Corporate strategies of Harvey Norman Company limited...............................................................6

Alignment of activity based costing with corporate strategies Harvey Norman Company.................8

Recommendations on implementation of activity based costing system in Harvey Norman

company‘s management............................................................................................................................9

Alternative management system that could be used in place of activity based costing........................9

Conclusion................................................................................................................................................10

References................................................................................................................................................11

Table of Contents

Introduction...............................................................................................................................................2

Activity based costing and its features.....................................................................................................3

Definition................................................................................................................................................3

Key features of activity based costing..................................................................................................3

How activity based costing aligns with corporate strategies and objectives of Harvey Norman

limited company........................................................................................................................................4

Mission of Harvey Norman Company.................................................................................................4

Objective of Harvey Norman Company..............................................................................................4

Corporate strategies of Harvey Norman Company limited...............................................................6

Alignment of activity based costing with corporate strategies Harvey Norman Company.................8

Recommendations on implementation of activity based costing system in Harvey Norman

company‘s management............................................................................................................................9

Alternative management system that could be used in place of activity based costing........................9

Conclusion................................................................................................................................................10

References................................................................................................................................................11

Activity Based Costing System for Inharvey Norman Company 4

Introduction

Harvey Norman is a multinational retailer of furniture, bedding, computers,

communications and consumer electrical products. The company is based in Australia. It is a

franchisee of the mother company, Harvey Norman holdings limited. The company runs other

retail outlets all over Australia and outside Australia. This coupled up with the fact that different

departments of the company are managed differently, implies that the company y must be run

using the most effective and efficient. The following report will be discussing activity based

costing and management tool and its applicability in Harvey Norman Company. The evaluation

of compatibility of the system to the company’s operations is done by first understanding the

company’s mission and objectives as well as strategies laid down towards achieving the

objectives. The alignment of activity based costing system to the strategies of Harvey Norman

company is then discussed in the report. Apart from activity based costing management and

costing system, the report also addresses alternative system that can be used in the place of

activity based costing.

Activity based costing and its features

Definition

Activity based costing tool identifies company’s activities and assigns cost to each

activity with respect to resources to all products and services that each activity has consumed.

Activity based costing approach involves tracing resource consumption and costing the final

product and services in a company or an organization. ABC system appreciates the relationship

between cost, activities and products and from this relationship, indirect costs are assigned to

products. The method applies best in manufacturing sector. This is because some costs such as

Introduction

Harvey Norman is a multinational retailer of furniture, bedding, computers,

communications and consumer electrical products. The company is based in Australia. It is a

franchisee of the mother company, Harvey Norman holdings limited. The company runs other

retail outlets all over Australia and outside Australia. This coupled up with the fact that different

departments of the company are managed differently, implies that the company y must be run

using the most effective and efficient. The following report will be discussing activity based

costing and management tool and its applicability in Harvey Norman Company. The evaluation

of compatibility of the system to the company’s operations is done by first understanding the

company’s mission and objectives as well as strategies laid down towards achieving the

objectives. The alignment of activity based costing system to the strategies of Harvey Norman

company is then discussed in the report. Apart from activity based costing management and

costing system, the report also addresses alternative system that can be used in the place of

activity based costing.

Activity based costing and its features

Definition

Activity based costing tool identifies company’s activities and assigns cost to each

activity with respect to resources to all products and services that each activity has consumed.

Activity based costing approach involves tracing resource consumption and costing the final

product and services in a company or an organization. ABC system appreciates the relationship

between cost, activities and products and from this relationship, indirect costs are assigned to

products. The method applies best in manufacturing sector. This is because some costs such as

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Activity Based Costing System for Inharvey Norman Company 5

salaries and administrative cost incurred in a company are hard to assign (Demeere, Stouthuysen,

and Roodhooft 2009).

Key features of activity based costing

Some of the common feature of ABC costing tool that differentiate it from other

traditional costing tools are as follows.

In ABC costing method, total cost is divide into types, that is, fixed cost and variable

cost. The division of total cost is important in providing quality information to design a cost

system. The method also distinguishes the cost behavior patterns. Cost behaviors patterns are

volume related, diversity related, events related and time related (Tse and Gong 2009). The

appropriate cost drivers are identified to ensure track on the overhead to a product. The cost

drivers determine the cost behavior pattern.

How activity based costing aligns with corporate strategies and objectives of Harvey

Norman limited company

Mission of Harvey Norman Company

Harvey Norman main mission is to be the dominant company in retail of the home used

products. To acquire the largest market share all over the world is the key mission that the

company is working toward s achieving. Maintaining the growing trends in terms of financial

performance of the company is also Harvey Norman’s operational mission. The company has

been recording exemplary performance since 2013 to last financial year (Kaplan et.al. 2014).

This growing trend does the company good therefore the management aims at maintaining the

trend. The company is also focused at giving back to the society by supporting women

empowerment programs. Harvey Norman Company supports the Harvey women’s rugby team.

salaries and administrative cost incurred in a company are hard to assign (Demeere, Stouthuysen,

and Roodhooft 2009).

Key features of activity based costing

Some of the common feature of ABC costing tool that differentiate it from other

traditional costing tools are as follows.

In ABC costing method, total cost is divide into types, that is, fixed cost and variable

cost. The division of total cost is important in providing quality information to design a cost

system. The method also distinguishes the cost behavior patterns. Cost behaviors patterns are

volume related, diversity related, events related and time related (Tse and Gong 2009). The

appropriate cost drivers are identified to ensure track on the overhead to a product. The cost

drivers determine the cost behavior pattern.

How activity based costing aligns with corporate strategies and objectives of Harvey

Norman limited company

Mission of Harvey Norman Company

Harvey Norman main mission is to be the dominant company in retail of the home used

products. To acquire the largest market share all over the world is the key mission that the

company is working toward s achieving. Maintaining the growing trends in terms of financial

performance of the company is also Harvey Norman’s operational mission. The company has

been recording exemplary performance since 2013 to last financial year (Kaplan et.al. 2014).

This growing trend does the company good therefore the management aims at maintaining the

trend. The company is also focused at giving back to the society by supporting women

empowerment programs. Harvey Norman Company supports the Harvey women’s rugby team.

Activity Based Costing System for Inharvey Norman Company 6

With the company’s sponsorship the team has achieved a lot and has helped in exploitation of

women’s talents. The company is aiming at continued society participation. Harvey Norman

Company aims at being a global company with locations everywhere on the globe. Opening up

new retail outlets will increase the company’s market share over the world (Shander et.al 2010).

Objective of Harvey Norman Company

The main objective behind the formation of Harvey Norman Company is to retail hose

appliances and other furniture products used domestically. The company has over year strived to

achieve this objective. Adding and maintaining shareholders value is always another objective of

Harvey Norman Company. The shareholder’s value is added by ensuring excellent performance

of the company in terms of amount of profit generated. Harvey Norman Company has laid down

a number of strategies to improve shareholders incomes and revenues (Zott and Amit 2010).

Providing highest quality and latest design of products has always been Harvey’s objective since

its establishment. The company wants to deliver the best products such that the consumer’s

demands are fully addressed. This objective aims at keeping the company on revolution with

changes in consumer’s preferences.

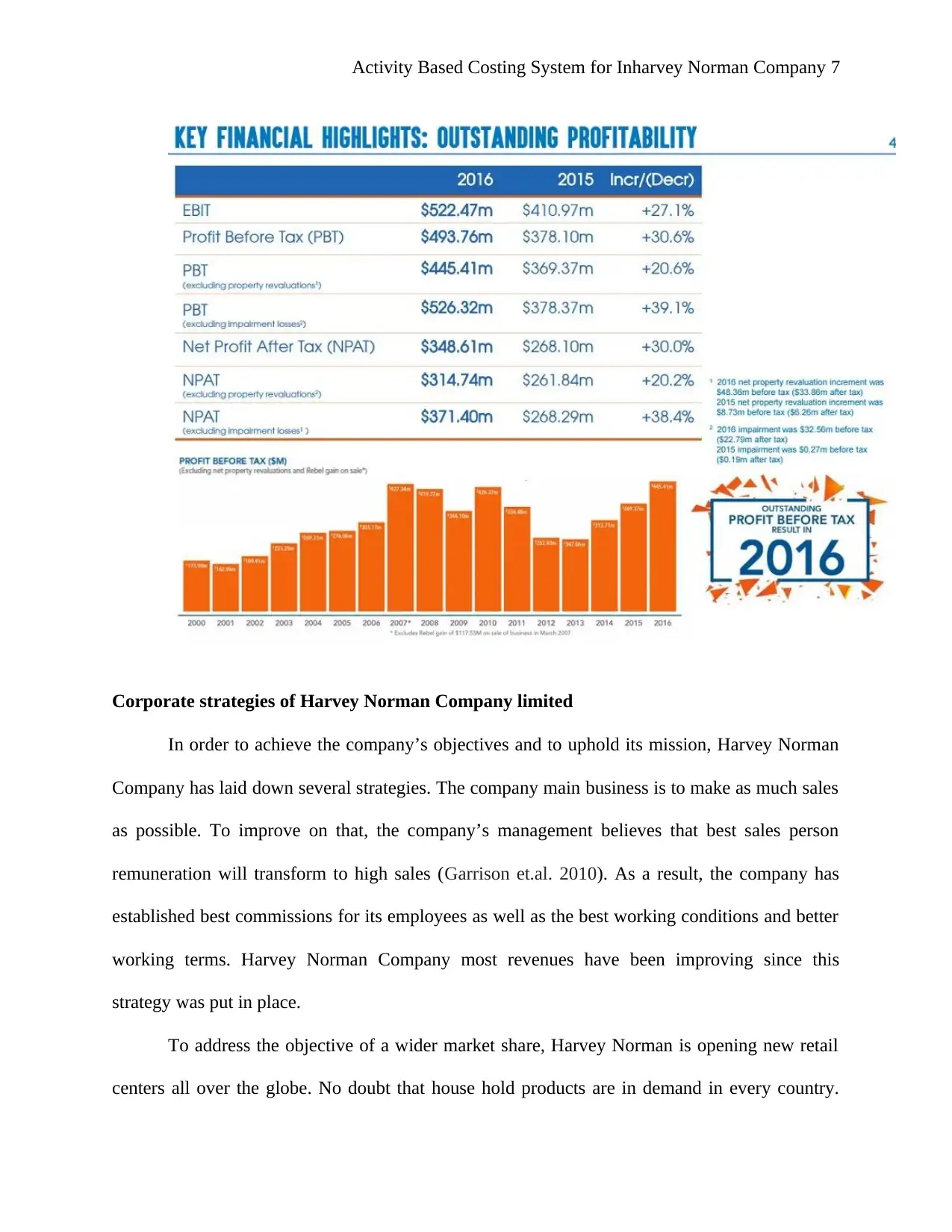

The chart below depicts Harvey’s performance;

With the company’s sponsorship the team has achieved a lot and has helped in exploitation of

women’s talents. The company is aiming at continued society participation. Harvey Norman

Company aims at being a global company with locations everywhere on the globe. Opening up

new retail outlets will increase the company’s market share over the world (Shander et.al 2010).

Objective of Harvey Norman Company

The main objective behind the formation of Harvey Norman Company is to retail hose

appliances and other furniture products used domestically. The company has over year strived to

achieve this objective. Adding and maintaining shareholders value is always another objective of

Harvey Norman Company. The shareholder’s value is added by ensuring excellent performance

of the company in terms of amount of profit generated. Harvey Norman Company has laid down

a number of strategies to improve shareholders incomes and revenues (Zott and Amit 2010).

Providing highest quality and latest design of products has always been Harvey’s objective since

its establishment. The company wants to deliver the best products such that the consumer’s

demands are fully addressed. This objective aims at keeping the company on revolution with

changes in consumer’s preferences.

The chart below depicts Harvey’s performance;

Activity Based Costing System for Inharvey Norman Company 7

Corporate strategies of Harvey Norman Company limited

In order to achieve the company’s objectives and to uphold its mission, Harvey Norman

Company has laid down several strategies. The company main business is to make as much sales

as possible. To improve on that, the company’s management believes that best sales person

remuneration will transform to high sales (Garrison et.al. 2010). As a result, the company has

established best commissions for its employees as well as the best working conditions and better

working terms. Harvey Norman Company most revenues have been improving since this

strategy was put in place.

To address the objective of a wider market share, Harvey Norman is opening new retail

centers all over the globe. No doubt that house hold products are in demand in every country.

Corporate strategies of Harvey Norman Company limited

In order to achieve the company’s objectives and to uphold its mission, Harvey Norman

Company has laid down several strategies. The company main business is to make as much sales

as possible. To improve on that, the company’s management believes that best sales person

remuneration will transform to high sales (Garrison et.al. 2010). As a result, the company has

established best commissions for its employees as well as the best working conditions and better

working terms. Harvey Norman Company most revenues have been improving since this

strategy was put in place.

To address the objective of a wider market share, Harvey Norman is opening new retail

centers all over the globe. No doubt that house hold products are in demand in every country.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing System for Inharvey Norman Company 8

Especially in the developing countries, the demand for these products has not been fully

addressed. Harvey Norman Company is strategically opening up in these countries to take

advantage of this demand gaps. Harvey Norman has most of its retail centers in developed

countries where it has been performing well (Garrison et.al. 2010). This performance could even

be made better by opening in developing countries too.

The market for household products is quickly transforming. There are new innovations

each day. So as to keep up with these innovations, the company is going one step ahead of

competitors to ensure a wide range of products in their retail centers (Zimmerman and Yahya-

Zadeh 2011). This is due to divergent nature of consumers preferences in terms of designs and

quality. The companies suppliers are also filtered out depending on their innovations and

development made on their products.

Participation on society’s activities and supporting governments programs is another

strategy that Harvey Norman is deploying so as to ensure acceptability and popularity. How

acceptable the company is to its target market. The company is currently towards women

empowerment programs which are under world’s millennial goals. By so doing, the team acts as

a promotion tool (Dale and Plunkett 2017). On the other hand, more investors and customers are

attracted to the company. By participating and being successful in sports, the company has

created awareness on its existence and the products it deals with. With this popularity, the

company is in a better position to receive best supply proposal from more advanced suppliers so

that it is always at par with consumer’s trends and demands.

Alliance and franchising with other corporations is a strategic move that Harvey Norman

Company is making. Since the company is working towards expansion, it will be easier and

Especially in the developing countries, the demand for these products has not been fully

addressed. Harvey Norman Company is strategically opening up in these countries to take

advantage of this demand gaps. Harvey Norman has most of its retail centers in developed

countries where it has been performing well (Garrison et.al. 2010). This performance could even

be made better by opening in developing countries too.

The market for household products is quickly transforming. There are new innovations

each day. So as to keep up with these innovations, the company is going one step ahead of

competitors to ensure a wide range of products in their retail centers (Zimmerman and Yahya-

Zadeh 2011). This is due to divergent nature of consumers preferences in terms of designs and

quality. The companies suppliers are also filtered out depending on their innovations and

development made on their products.

Participation on society’s activities and supporting governments programs is another

strategy that Harvey Norman is deploying so as to ensure acceptability and popularity. How

acceptable the company is to its target market. The company is currently towards women

empowerment programs which are under world’s millennial goals. By so doing, the team acts as

a promotion tool (Dale and Plunkett 2017). On the other hand, more investors and customers are

attracted to the company. By participating and being successful in sports, the company has

created awareness on its existence and the products it deals with. With this popularity, the

company is in a better position to receive best supply proposal from more advanced suppliers so

that it is always at par with consumer’s trends and demands.

Alliance and franchising with other corporations is a strategic move that Harvey Norman

Company is making. Since the company is working towards expansion, it will be easier and

Activity Based Costing System for Inharvey Norman Company 9

cheaper to make alliances with other business so as to boost its acceptability and guarantee its

success in new locations. Alliances with suppliers and other m marketing companies will not

only ensure steady supply of products but will also play a great role in improving the company’s

revenues and performance trends. Franchising is the easiest way for the company to achieve

acceptability in the quickest way possible (Drury 2013). Harvey Norman’s success can be based

on the franchisee. Working as a franchisee of another company is a guarantee of consumer’s

loyalty. The company is also forming partnership with an aim of replacing is old management

infrastructure without losing its functionality.

Harvey Norman Company is also working towards strategically improvement of

management as well costing systems. With so much activities going in its various department

and also its locations, the current system is undermining efficiency (Drury 2013). A new system

that can fully address the company’s activities needs to be put in place to counter this challenge.

Alignment of activity based costing with corporate strategies Harvey Norman Company

An effective and efficient management and costing tool is all that Harvey Company

requires. Activity based costing system is ideal for this company. Its alignment with company’s

goals and strategies is discussed below. The company runs multiple departments as well as

outlets all over Australia and outside. This implies that there are many activities going on that the

company needs to evaluate. That activity based system will help the company in assigning cost

to these activities (Van Der Laan and Dean 2010).

With cost assigned to this activities, better decisions can be made on cost planning can be

reached so as to cut down the operation cost and maximize on revenues. Activity based costing

does not only help in assigning cost but it is a management tool. Harvey is on the move to open

up new retail centers in new locations. With activity based costing, the company can make sound

cheaper to make alliances with other business so as to boost its acceptability and guarantee its

success in new locations. Alliances with suppliers and other m marketing companies will not

only ensure steady supply of products but will also play a great role in improving the company’s

revenues and performance trends. Franchising is the easiest way for the company to achieve

acceptability in the quickest way possible (Drury 2013). Harvey Norman’s success can be based

on the franchisee. Working as a franchisee of another company is a guarantee of consumer’s

loyalty. The company is also forming partnership with an aim of replacing is old management

infrastructure without losing its functionality.

Harvey Norman Company is also working towards strategically improvement of

management as well costing systems. With so much activities going in its various department

and also its locations, the current system is undermining efficiency (Drury 2013). A new system

that can fully address the company’s activities needs to be put in place to counter this challenge.

Alignment of activity based costing with corporate strategies Harvey Norman Company

An effective and efficient management and costing tool is all that Harvey Company

requires. Activity based costing system is ideal for this company. Its alignment with company’s

goals and strategies is discussed below. The company runs multiple departments as well as

outlets all over Australia and outside. This implies that there are many activities going on that the

company needs to evaluate. That activity based system will help the company in assigning cost

to these activities (Van Der Laan and Dean 2010).

With cost assigned to this activities, better decisions can be made on cost planning can be

reached so as to cut down the operation cost and maximize on revenues. Activity based costing

does not only help in assigning cost but it is a management tool. Harvey is on the move to open

up new retail centers in new locations. With activity based costing, the company can make sound

Activity Based Costing System for Inharvey Norman Company 10

strategic decisions. Activity based costing system provides the management with ample

information on the expected cost to be incurred in implementation of this strategy the expected

rewards can also be evaluated using this tool (Zutshi, Creed, Holmes and Brain 2016).

The system will also add an extra advantage to the company’s operational decisions

making process. Activity based costing can be used to evaluate the possible returns of engaging

in a certain operation or activity. This way, the company will avoid engaging in activities that

will see it in losses. Harvey’s strategy to form alliances needs a lot of information to back it up.

The benefit of this move needs to be evaluated. That’s where activity based costing come in.

with this tool; the company can point out the possible loopholes and the chances of success of

this strategy. With this information, the company can evaluate the effectiveness of this, move

towards achieving its objectives (Taticchi, Tonelli and Cagnazzo 2010).

Recommendations on implementation of activity based costing system in Harvey Norman

company‘s management

The benefits of incorporating this system as a management and costing tool over the

current systems needs to be evaluated. This will create a better picture of what Harvey Norman

Company will gain from making these changes. Evaluation of this system will also help the

company avoid unnecessary loses as a result of failure of the system (Tavana, Yazdani and Di

Caprio 2017). The limits of these systems can also be pointed out so as to come up with

necessary solutions to cope up with limits. Training the staff on the application of this system is

very vital. This strategy is new to Harvey Norman Company. Therefore creating awareness on

how to handle the system for the best results needs to be passed down to the staff. Training the

employees and management staff will ensure full effectiveness of the company (Verhagen et.al

strategic decisions. Activity based costing system provides the management with ample

information on the expected cost to be incurred in implementation of this strategy the expected

rewards can also be evaluated using this tool (Zutshi, Creed, Holmes and Brain 2016).

The system will also add an extra advantage to the company’s operational decisions

making process. Activity based costing can be used to evaluate the possible returns of engaging

in a certain operation or activity. This way, the company will avoid engaging in activities that

will see it in losses. Harvey’s strategy to form alliances needs a lot of information to back it up.

The benefit of this move needs to be evaluated. That’s where activity based costing come in.

with this tool; the company can point out the possible loopholes and the chances of success of

this strategy. With this information, the company can evaluate the effectiveness of this, move

towards achieving its objectives (Taticchi, Tonelli and Cagnazzo 2010).

Recommendations on implementation of activity based costing system in Harvey Norman

company‘s management

The benefits of incorporating this system as a management and costing tool over the

current systems needs to be evaluated. This will create a better picture of what Harvey Norman

Company will gain from making these changes. Evaluation of this system will also help the

company avoid unnecessary loses as a result of failure of the system (Tavana, Yazdani and Di

Caprio 2017). The limits of these systems can also be pointed out so as to come up with

necessary solutions to cope up with limits. Training the staff on the application of this system is

very vital. This strategy is new to Harvey Norman Company. Therefore creating awareness on

how to handle the system for the best results needs to be passed down to the staff. Training the

employees and management staff will ensure full effectiveness of the company (Verhagen et.al

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Activity Based Costing System for Inharvey Norman Company 11

2012). The employees should also be given an opportunity to build experience on the same. With

necessary skills and experience, the staff and employs can use the tool efficiently which translate

to efficient operations of the company (Garrison and Noreen 2009).

Alternative management system that could be used in place of activity based costing

In case the activity based costing fails, Harvey Norman Company could employ time

driven activity based costing management system. The tool mainly estimates the practical

capacity of committed resources and their cost and the unit times for performing transactional

activities. The system require less information and resources as compare to activity based costing

system hence more cost effective. However, its incorporation is largely determined by the nature

of business a company engages (Shander et.al. 2010).

Conclusion

Harvey Norman’s management issue can all be solved by activity based costing. The

system as seen above is in alignment with most of the company’s strategies and objectives. The

large number of activities in Harvey Norman company makes activity based costing ideal

management and costing tool. The tool will help the company achieve its expansion strategies

and also help build more on shareholder’s value. The financial performance will also improve

greatly with incorporation of this system.

2012). The employees should also be given an opportunity to build experience on the same. With

necessary skills and experience, the staff and employs can use the tool efficiently which translate

to efficient operations of the company (Garrison and Noreen 2009).

Alternative management system that could be used in place of activity based costing

In case the activity based costing fails, Harvey Norman Company could employ time

driven activity based costing management system. The tool mainly estimates the practical

capacity of committed resources and their cost and the unit times for performing transactional

activities. The system require less information and resources as compare to activity based costing

system hence more cost effective. However, its incorporation is largely determined by the nature

of business a company engages (Shander et.al. 2010).

Conclusion

Harvey Norman’s management issue can all be solved by activity based costing. The

system as seen above is in alignment with most of the company’s strategies and objectives. The

large number of activities in Harvey Norman company makes activity based costing ideal

management and costing tool. The tool will help the company achieve its expansion strategies

and also help build more on shareholder’s value. The financial performance will also improve

greatly with incorporation of this system.

Activity Based Costing System for Inharvey Norman Company 12

References

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Demeere, N., Stouthuysen, K. and Roodhooft, F., 2009. Time-driven activity-based costing in an

outpatient clinic environment: development, relevance and managerial impact. Health

policy, 92(2), pp.296-304.

Drury, C.M., 2013. Management and cost accounting. Springer.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial

accounting. Issues in Accounting Education, 25(4), pp.792-793.

Kaplan, R.S., Witkowski, M., Abbott, M., Guzman, A.B., Higgins, L.D., Meara, J.G., Padden, E.,

Shah, A.S., Waters, P., Weidemeier, M. and Wertheimer, S., 2014. Using time-driven activity-

based costing to identify value improvement opportunities in healthcare. Journal of Healthcare

Management, 59(6), pp.399-412.

Shander, A., Hofmann, A., Ozawa, S., Theusinger, O.M., Gombotz, H. and Spahn, D.R., 2010.

Activity‐based costs of blood transfusions in surgical patients at four hospitals. Transfusion, 50(4),

pp.753-765.

Shander, A., Hofmann, A., Ozawa, S., Theusinger, O.M., Gombotz, H. and Spahn, D.R., 2010.

Activity‐based costs of blood transfusions in surgical patients at four

hospitals. Transfusion, 50(4), pp.753-765.

Taticchi, P., Tonelli, F. and Cagnazzo, L., 2010. Performance measurement and management: a

literature review and a research agenda. Measuring business excellence, 14(1), pp.4-18.

References

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Demeere, N., Stouthuysen, K. and Roodhooft, F., 2009. Time-driven activity-based costing in an

outpatient clinic environment: development, relevance and managerial impact. Health

policy, 92(2), pp.296-304.

Drury, C.M., 2013. Management and cost accounting. Springer.

Garrison, R.H., Noreen, E.W., Brewer, P.C. and McGowan, A., 2010. Managerial

accounting. Issues in Accounting Education, 25(4), pp.792-793.

Kaplan, R.S., Witkowski, M., Abbott, M., Guzman, A.B., Higgins, L.D., Meara, J.G., Padden, E.,

Shah, A.S., Waters, P., Weidemeier, M. and Wertheimer, S., 2014. Using time-driven activity-

based costing to identify value improvement opportunities in healthcare. Journal of Healthcare

Management, 59(6), pp.399-412.

Shander, A., Hofmann, A., Ozawa, S., Theusinger, O.M., Gombotz, H. and Spahn, D.R., 2010.

Activity‐based costs of blood transfusions in surgical patients at four hospitals. Transfusion, 50(4),

pp.753-765.

Shander, A., Hofmann, A., Ozawa, S., Theusinger, O.M., Gombotz, H. and Spahn, D.R., 2010.

Activity‐based costs of blood transfusions in surgical patients at four

hospitals. Transfusion, 50(4), pp.753-765.

Taticchi, P., Tonelli, F. and Cagnazzo, L., 2010. Performance measurement and management: a

literature review and a research agenda. Measuring business excellence, 14(1), pp.4-18.

Activity Based Costing System for Inharvey Norman Company 13

Tavana, M., Yazdani, M. and Di Caprio, D., 2017. An application of an integrated ANP–QFD

framework for sustainable supplier selection. International Journal of Logistics Research and

Applications, 20(3), pp.254-275.

Tse, M. and Gong, M., 2009. Recognition of idle resources in time-driven activity-based costing

and resource consumption accounting models. Journal of applied management accounting

research, 7(2), pp.41-54.

Van Der Laan, S. and Dean, G., 2010. Corporate groups in Australia: State of play. Australian

Accounting Review, 20(2), pp.121-133.

Verhagen, W.J., Bermell-Garcia, P., van Dijk, R.E. and Curran, R., 2012. A critical review of

Knowledge-Based Engineering: An identification of research challenges. Advanced Engineering

Informatics, 26(1), pp.5-15.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

Zott, C. and Amit, R., 2010. Business model design: an activity system perspective. Long range

planning, 43(2-3), pp.216-226.

Zutshi, A., Creed, A., Holmes, M. and Brain, J., 2016. Reflections of environmental management

implementation in furniture. International Journal of Retail & Distribution Management, 44(8),

pp.840-859.

Tavana, M., Yazdani, M. and Di Caprio, D., 2017. An application of an integrated ANP–QFD

framework for sustainable supplier selection. International Journal of Logistics Research and

Applications, 20(3), pp.254-275.

Tse, M. and Gong, M., 2009. Recognition of idle resources in time-driven activity-based costing

and resource consumption accounting models. Journal of applied management accounting

research, 7(2), pp.41-54.

Van Der Laan, S. and Dean, G., 2010. Corporate groups in Australia: State of play. Australian

Accounting Review, 20(2), pp.121-133.

Verhagen, W.J., Bermell-Garcia, P., van Dijk, R.E. and Curran, R., 2012. A critical review of

Knowledge-Based Engineering: An identification of research challenges. Advanced Engineering

Informatics, 26(1), pp.5-15.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

Zott, C. and Amit, R., 2010. Business model design: an activity system perspective. Long range

planning, 43(2-3), pp.216-226.

Zutshi, A., Creed, A., Holmes, M. and Brain, J., 2016. Reflections of environmental management

implementation in furniture. International Journal of Retail & Distribution Management, 44(8),

pp.840-859.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.