HI5017 Managerial Accounting: ABC Model Application in Qube Holding

VerifiedAdded on 2023/06/12

|13

|3180

|321

Report

AI Summary

This report delves into the application of Activity-Based Costing (ABC) within Qube Holding, an ASX-listed company, in the context of HI5017 Managerial Accounting. It highlights the shift from traditional costing methods to modern systems like ABC to improve cost allocation and decision-making. The report outlines the features of the ABC model, its implementation steps, and the benefits Qube Holding can derive from its use, including enhanced cost management, better decision-making, and strategic development. Alternative accounting tools like marginal and absorption costing are also discussed. The analysis underscores the potential of modern cost accounting systems in enhancing operational efficiency and profitability, recommending the installation of ABC models for better cost control and business expansion.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

HI5017 Managerial Accounting

Trimester 1 2018

Individual Assignment

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

HI5017 Managerial Accounting

Trimester 1 2018

Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Qube Holding

Executive Summary

The system of costing has undergone a huge change and in order to derive the benefits it is

essential that the company need to embrace the modern costing system. Such a step leads to

proper allocation of cost. In this report, the system of Activity Based costing is discussed and

the company selected for the purpose is Qube Holding, listed on the ASX. The report is

discussed in the light of this company that initiates with the ABC system followed by the

benefits derived by the company through the use of ABC. Further, other alternative methods

are even discussed. The analysis gives an indication of the potential that consists in the

modern cost accounting system.

2

Executive Summary

The system of costing has undergone a huge change and in order to derive the benefits it is

essential that the company need to embrace the modern costing system. Such a step leads to

proper allocation of cost. In this report, the system of Activity Based costing is discussed and

the company selected for the purpose is Qube Holding, listed on the ASX. The report is

discussed in the light of this company that initiates with the ABC system followed by the

benefits derived by the company through the use of ABC. Further, other alternative methods

are even discussed. The analysis gives an indication of the potential that consists in the

modern cost accounting system.

2

Qube Holding

Contents

Introduction...........................................................................................................................................3

Activity-based costing model and its features.......................................................................................3

Allocating the ABC model with the current goals of an organization....................................................4

Implementation of Activity-based costing model step by step..............................................................5

Ways through which Qube Holding Limited can utilise it......................................................................6

Significance of Activity-based costing model in Qube Holdings Ltd.......................................................6

Using the Activity-based costing model so as to enhance the structure of top management...............6

Technological influence and utility of ABC model.................................................................................7

Recommendation regarding installation of ABC Models in Qube Holding............................................8

Accounting tools used by the management other than ABC model......................................................8

Marginal costing............................................................................................................................9

Absorption costing.........................................................................................................................9

Conclusion...........................................................................................................................................11

Bibliography.........................................................................................................................................12

3

Contents

Introduction...........................................................................................................................................3

Activity-based costing model and its features.......................................................................................3

Allocating the ABC model with the current goals of an organization....................................................4

Implementation of Activity-based costing model step by step..............................................................5

Ways through which Qube Holding Limited can utilise it......................................................................6

Significance of Activity-based costing model in Qube Holdings Ltd.......................................................6

Using the Activity-based costing model so as to enhance the structure of top management...............6

Technological influence and utility of ABC model.................................................................................7

Recommendation regarding installation of ABC Models in Qube Holding............................................8

Accounting tools used by the management other than ABC model......................................................8

Marginal costing............................................................................................................................9

Absorption costing.........................................................................................................................9

Conclusion...........................................................................................................................................11

Bibliography.........................................................................................................................................12

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Qube Holding

Introduction

A huge portion of indirect costs was aligned to the manufactured goods in the traditional

accounting method which was later on observed that such costs are not utilised equally by all

the manufactured goods and therefore the ancient accounting approach was not able to

effectively evaluate and calculate the exact costs associated with the production of such

goods and related services. This also means that the decision taken based on the data

evaluated through such approach might be inappropriate. ABC model is employed so as to

ascertain the total costs assigned to the production of a particular product line and related

services. ABC model not only helps in the identification of evaluation of costs associated

with every activity but also finds out the extent of such activities utilised by particular goods

and services. Therefore, the activities that employs high overhead costs are ascertained which

further helps the management in finding measures for reducing such unnecessary overhead

costs

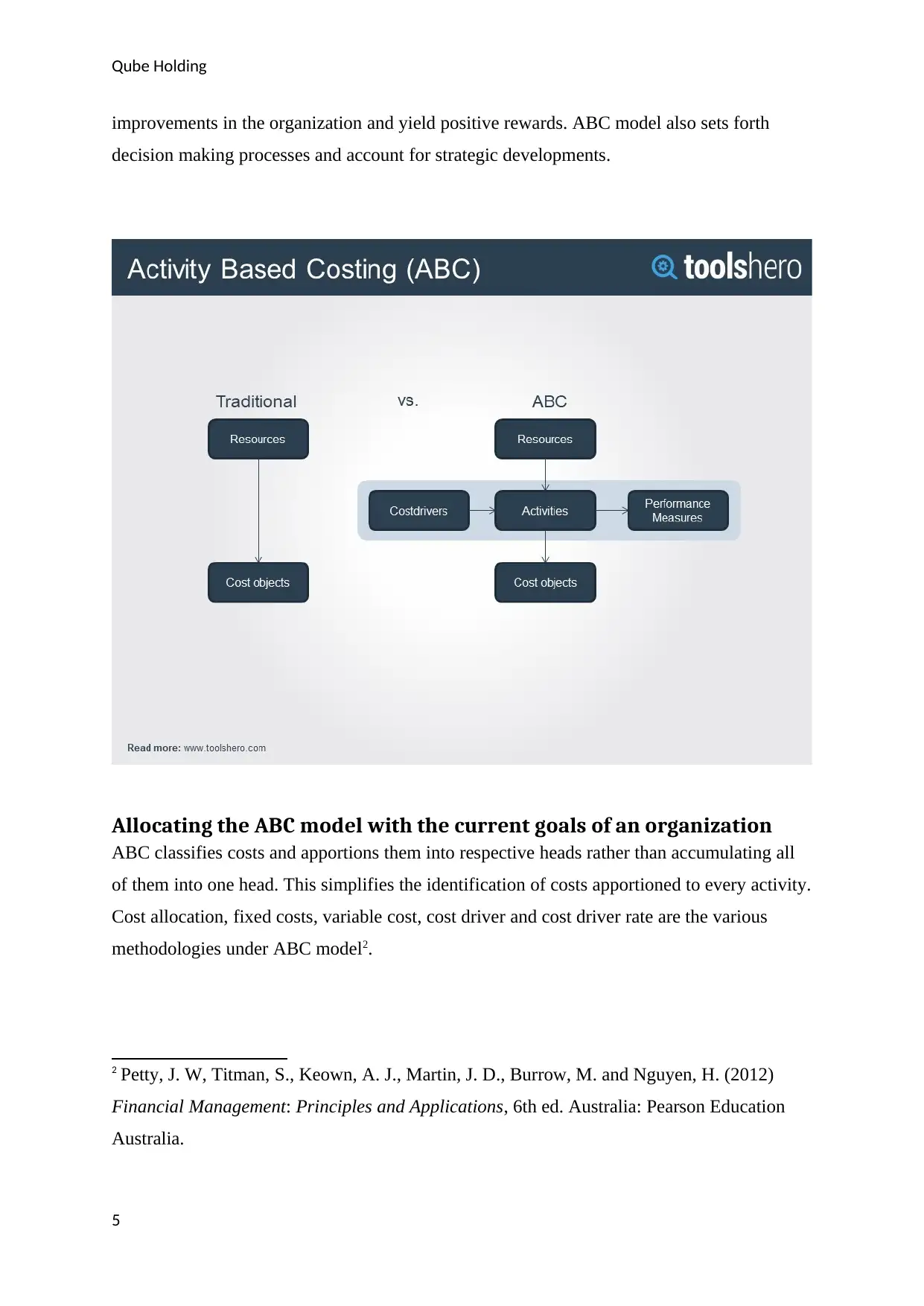

Activity-based costing model and its features

Unlike the traditional costing approach where the allocation of costs was simply on the

machine hours, Activity based costing model distributes manufacturing overhead costs to

goods in a more systematic and appropriate manner. The activities that are the ultimate cause

of the overhead are first assigned costs through ABC model. Later the products that are

actually demanding the activities are assigned the cost of these activities1.

ABC model forms and facilitates a very casual relationship between the cost drivers and

indirect costs unlike traditional cost price systems. A transparent and cost-conscious conduct

is initiated by passing on this insight to the responsible cost drivers. The installation of ABC

model makes it easier for the company’s top management and personnel to have an

understanding of the different cost categories and determining activities that adds value to the

goodwill of the company. It also helps in evaluating and eliminating such activities that

depleted the value of the organization. This way Qube Holdings Limited can look for the

1 Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

4

Introduction

A huge portion of indirect costs was aligned to the manufactured goods in the traditional

accounting method which was later on observed that such costs are not utilised equally by all

the manufactured goods and therefore the ancient accounting approach was not able to

effectively evaluate and calculate the exact costs associated with the production of such

goods and related services. This also means that the decision taken based on the data

evaluated through such approach might be inappropriate. ABC model is employed so as to

ascertain the total costs assigned to the production of a particular product line and related

services. ABC model not only helps in the identification of evaluation of costs associated

with every activity but also finds out the extent of such activities utilised by particular goods

and services. Therefore, the activities that employs high overhead costs are ascertained which

further helps the management in finding measures for reducing such unnecessary overhead

costs

Activity-based costing model and its features

Unlike the traditional costing approach where the allocation of costs was simply on the

machine hours, Activity based costing model distributes manufacturing overhead costs to

goods in a more systematic and appropriate manner. The activities that are the ultimate cause

of the overhead are first assigned costs through ABC model. Later the products that are

actually demanding the activities are assigned the cost of these activities1.

ABC model forms and facilitates a very casual relationship between the cost drivers and

indirect costs unlike traditional cost price systems. A transparent and cost-conscious conduct

is initiated by passing on this insight to the responsible cost drivers. The installation of ABC

model makes it easier for the company’s top management and personnel to have an

understanding of the different cost categories and determining activities that adds value to the

goodwill of the company. It also helps in evaluating and eliminating such activities that

depleted the value of the organization. This way Qube Holdings Limited can look for the

1 Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Qube Holding

improvements in the organization and yield positive rewards. ABC model also sets forth

decision making processes and account for strategic developments.

Allocating the ABC model with the current goals of an organization

ABC classifies costs and apportions them into respective heads rather than accumulating all

of them into one head. This simplifies the identification of costs apportioned to every activity.

Cost allocation, fixed costs, variable cost, cost driver and cost driver rate are the various

methodologies under ABC model2.

2 Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

5

improvements in the organization and yield positive rewards. ABC model also sets forth

decision making processes and account for strategic developments.

Allocating the ABC model with the current goals of an organization

ABC classifies costs and apportions them into respective heads rather than accumulating all

of them into one head. This simplifies the identification of costs apportioned to every activity.

Cost allocation, fixed costs, variable cost, cost driver and cost driver rate are the various

methodologies under ABC model2.

2 Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

5

Qube Holding

Implementation of Activity-based costing model step by step

- Research on processes and costs

- Identify activities and activity pools

- Identification of traceable costs

- Assigning left over costs to activities

- Determining per-activity allocation rates

- Apply costs to objects

- Preparation of management reports

It is easy to trace direct costs apportioned to the manufacturing of certain goods as compared

to indirect costs which are too complicated for there is variety of goods taking in use the

same inputs. The shared activity of different goods utilising the same resources is termed as

cost driver. The ultimate agenda behind implementation of ABC model is to develop and

increase the accuracy and efficiency of cost measurement to a huge extent by means of

reclassification of the maximum of its indirect costs as direct costs3.

The cost drivers are apportioned and aligned to the incurred costs by means of ABC model as

it is the basis of cost price calculation. It is always considered that the products and the

accompanying costs are casually related to one other4. For organizations having strategic

failures and downfall in the graph of corporate results, Activity based costing model acts as a

saviour for it helps in evaluating the unnecessary costs apportioned to activities and formulate

decision making and activities for cost reduction. This will further help such organizations in

garnering operational efficiency5. ABC model also helps in establishing the foundation for

Balanced Scorecard approach in a corporate.

3 Qube Holding Ltd. (2016) Qube Holding Ltd Annual report & accounts 2017 [online].

Available from: http://www.annualreports.com/Company/qube-holdings-ltd [Accessed 23

May 2018]

4 Phua, Y. S., M. A. Abernethy, and A. M. Lillis. (2011) Controls as exit barriers in

multiperiod outsourcing arrangements. The Accounting Review. [online]. 86, p. 1795–1834.

[Accessed 22 May 2018]

5 Parrino, R, Kidwell, D. & Bates, T. (2012). Fundamentals of corporate finance. Hoboken,

6

Implementation of Activity-based costing model step by step

- Research on processes and costs

- Identify activities and activity pools

- Identification of traceable costs

- Assigning left over costs to activities

- Determining per-activity allocation rates

- Apply costs to objects

- Preparation of management reports

It is easy to trace direct costs apportioned to the manufacturing of certain goods as compared

to indirect costs which are too complicated for there is variety of goods taking in use the

same inputs. The shared activity of different goods utilising the same resources is termed as

cost driver. The ultimate agenda behind implementation of ABC model is to develop and

increase the accuracy and efficiency of cost measurement to a huge extent by means of

reclassification of the maximum of its indirect costs as direct costs3.

The cost drivers are apportioned and aligned to the incurred costs by means of ABC model as

it is the basis of cost price calculation. It is always considered that the products and the

accompanying costs are casually related to one other4. For organizations having strategic

failures and downfall in the graph of corporate results, Activity based costing model acts as a

saviour for it helps in evaluating the unnecessary costs apportioned to activities and formulate

decision making and activities for cost reduction. This will further help such organizations in

garnering operational efficiency5. ABC model also helps in establishing the foundation for

Balanced Scorecard approach in a corporate.

3 Qube Holding Ltd. (2016) Qube Holding Ltd Annual report & accounts 2017 [online].

Available from: http://www.annualreports.com/Company/qube-holdings-ltd [Accessed 23

May 2018]

4 Phua, Y. S., M. A. Abernethy, and A. M. Lillis. (2011) Controls as exit barriers in

multiperiod outsourcing arrangements. The Accounting Review. [online]. 86, p. 1795–1834.

[Accessed 22 May 2018]

5 Parrino, R, Kidwell, D. & Bates, T. (2012). Fundamentals of corporate finance. Hoboken,

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Qube Holding

Ways through which Qube Holding Limited can utilise it

- Implementation of ABC model can help in the evaluation of cost price of goods and

services more effectively.

- It simplifies the methods for evaluating and measuring the effect of instant alterations

in set up times, lesser goods etc through stimulation.

- As activity based costing model reflects a clear picture of the pattern of the indirect

costs and this can help in managing overheads more effectively.

- For the benefit of the corporate strategy in the industry, Activity based costing model

provided better techniques so as to calculate cost price.

- ABC model helps in cost reduction by allocating cost drivers to their respective

overhead costs.

Significance of Activity-based costing model in Qube Holdings Ltd

ABC model serves as a management accounting technique in Qube Holdings Ltd which is a

listed company in the Australian Stock Exchange. The utility of ABC model has encouraged

the company in deriving positive results. The characteristics of ABC model are defined and

aligned in accordance with the organization’s strategies, mission and objectives. ABC model

has been of great help to the organization in achieving its goals and objectives. All the above

factors will be highlighted in the following report along with the necessary recommendations

that are required to be considered keeping in mind the size of the business and its number of

operations6. The following report will throw light on balanced scorecard approach as well

along with activity based costing model.

Using the Activity-based costing model so as to enhance the structure

of top management

It is very important to evaluate costs and profitability of the customer derived from the

products and services so as to have a basic understanding of the relationships between them.

6 Parrino, R, Kidwell, D. & Bates, T. (2012). Fundamentals of corporate finance. Hoboken,

7

Ways through which Qube Holding Limited can utilise it

- Implementation of ABC model can help in the evaluation of cost price of goods and

services more effectively.

- It simplifies the methods for evaluating and measuring the effect of instant alterations

in set up times, lesser goods etc through stimulation.

- As activity based costing model reflects a clear picture of the pattern of the indirect

costs and this can help in managing overheads more effectively.

- For the benefit of the corporate strategy in the industry, Activity based costing model

provided better techniques so as to calculate cost price.

- ABC model helps in cost reduction by allocating cost drivers to their respective

overhead costs.

Significance of Activity-based costing model in Qube Holdings Ltd

ABC model serves as a management accounting technique in Qube Holdings Ltd which is a

listed company in the Australian Stock Exchange. The utility of ABC model has encouraged

the company in deriving positive results. The characteristics of ABC model are defined and

aligned in accordance with the organization’s strategies, mission and objectives. ABC model

has been of great help to the organization in achieving its goals and objectives. All the above

factors will be highlighted in the following report along with the necessary recommendations

that are required to be considered keeping in mind the size of the business and its number of

operations6. The following report will throw light on balanced scorecard approach as well

along with activity based costing model.

Using the Activity-based costing model so as to enhance the structure

of top management

It is very important to evaluate costs and profitability of the customer derived from the

products and services so as to have a basic understanding of the relationships between them.

6 Parrino, R, Kidwell, D. & Bates, T. (2012). Fundamentals of corporate finance. Hoboken,

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Qube Holding

For this purpose, the cost system is used as a means so as to manage the relationships

between the costs of the product and the benefit derived from the same product by the

consumer7. It also assists an organization in managing the processes of pricing, outsourcing

and sales. It also assists in decision making for keeping up with the production of a particular

product line.

Technological influence and utility of ABC model

With the evolution of technology it is noticed that the machinery costs have been rising while

the direct labour costs are reduced. It is really difficult for an organization to analyse and

evaluate machinery costs associated with a particular product because such machineries are

not installed and utilised for a particular product rather they are engaged for multiple

products. In order to determine and evaluate such costs easily the activity based model is

been taken into use for it brings out every single costs associated with the products and

therefore helps in consumer classification.

ABC Model not only helps in evaluating costs but also helps in the identification of such

activities that are not cost effective which helps the management to make a decision

regarding shutting down the production of such underpriced goods which is generating losses

for the organization. It is noticed that the chances for sales to rise is directly proportional to

the rise in cost accuracy of the management activities 8. ABC model helps an organization in

making more and more profits as it helps an organization to identify its inefficient products

and departments and forms a decision making for the management whether to stop or better

them. In the absence of illegitimate costs in the department an organization can implement

cost control.

7 Oker, F & Adıguzel, H. (2016) Time‐driven activity‐based costing: An implementation in

manufacturing company. Journal of Corporate Accounting & Finance. [online]. 27(3), p. 39-

56. Doi: https://doi.org/10.1002/jcaf.22144

8 Phua, Y. S., M. A. Abernethy, and A. M. Lillis. (2011) Controls as exit barriers in

multiperiod outsourcing arrangements. The Accounting Review. [online]. 86, p. 1795–1834.

[Accessed 22 May 2018]

8

For this purpose, the cost system is used as a means so as to manage the relationships

between the costs of the product and the benefit derived from the same product by the

consumer7. It also assists an organization in managing the processes of pricing, outsourcing

and sales. It also assists in decision making for keeping up with the production of a particular

product line.

Technological influence and utility of ABC model

With the evolution of technology it is noticed that the machinery costs have been rising while

the direct labour costs are reduced. It is really difficult for an organization to analyse and

evaluate machinery costs associated with a particular product because such machineries are

not installed and utilised for a particular product rather they are engaged for multiple

products. In order to determine and evaluate such costs easily the activity based model is

been taken into use for it brings out every single costs associated with the products and

therefore helps in consumer classification.

ABC Model not only helps in evaluating costs but also helps in the identification of such

activities that are not cost effective which helps the management to make a decision

regarding shutting down the production of such underpriced goods which is generating losses

for the organization. It is noticed that the chances for sales to rise is directly proportional to

the rise in cost accuracy of the management activities 8. ABC model helps an organization in

making more and more profits as it helps an organization to identify its inefficient products

and departments and forms a decision making for the management whether to stop or better

them. In the absence of illegitimate costs in the department an organization can implement

cost control.

7 Oker, F & Adıguzel, H. (2016) Time‐driven activity‐based costing: An implementation in

manufacturing company. Journal of Corporate Accounting & Finance. [online]. 27(3), p. 39-

56. Doi: https://doi.org/10.1002/jcaf.22144

8 Phua, Y. S., M. A. Abernethy, and A. M. Lillis. (2011) Controls as exit barriers in

multiperiod outsourcing arrangements. The Accounting Review. [online]. 86, p. 1795–1834.

[Accessed 22 May 2018]

8

Qube Holding

Recommendation regarding installation of ABC Models in Qube

Holding

For the purpose of minimization of costs to a greater extent Qube Holding has opted to install

ABC model after analyzing its size, nature and any other relatable characteristics. It is quite

evident that the organization is prioritizing the exploration projects in the year 2018 after

taking all the required necessary recommendations into due consideration. Hence, Qube

Holding can improve its overall performance and data processes which can enhance the

utility of the information technology that further assists the organization in the evolution of

technologies and maintain its stability and achieve its goals9. The installation of activity

based costing model will assist the organization in ascertaining and allocating the costs in a

constructive pattern. The cost structure of the organization is also ascertained. The

advantages of employing Activity based model cannot go unnoticed with the involvement of

superior information technology. This facilitates better performance of the business

operations. The size of the business requires the effective utilization of costs since the

organization has been operating since quite a long time. Activity based costing model not

only allows the reduction of costs but also helps in expanding the business.

Accounting tools used by the management other than ABC model

Qube Holding has surpassed all the obstacles and survived strongly against all its competitors

in the industry that reflects its compatibility to face such variations. The management of

Qube Holding has taken all such legitimate strategies into application in order to ascertain

that what works best for the same so as to reduce costs and increase its cash inflows10. The

performance and effectiveness of the management that has been operation as per required

plans and objectives, highly depends on the success of the organization. So, there are various

functions and scenarios on which the accounting tool relies on11. Absorption and marginal

costing are the best mechanisms for the organization to employ.

9

10 Qube Holding Ltd. (2016) Qube Holding Ltd Annual report & accounts 2017 [online].

Available from: http://www.annualreports.com/Company/qube-holdings-ltd [Accessed 23

May 2018]

11 Chapman, C, Hopwood, A & Shields, M. (2007). Handbook of Management Accounting

Research. Oxford, U.K.: Elsevier

9

Recommendation regarding installation of ABC Models in Qube

Holding

For the purpose of minimization of costs to a greater extent Qube Holding has opted to install

ABC model after analyzing its size, nature and any other relatable characteristics. It is quite

evident that the organization is prioritizing the exploration projects in the year 2018 after

taking all the required necessary recommendations into due consideration. Hence, Qube

Holding can improve its overall performance and data processes which can enhance the

utility of the information technology that further assists the organization in the evolution of

technologies and maintain its stability and achieve its goals9. The installation of activity

based costing model will assist the organization in ascertaining and allocating the costs in a

constructive pattern. The cost structure of the organization is also ascertained. The

advantages of employing Activity based model cannot go unnoticed with the involvement of

superior information technology. This facilitates better performance of the business

operations. The size of the business requires the effective utilization of costs since the

organization has been operating since quite a long time. Activity based costing model not

only allows the reduction of costs but also helps in expanding the business.

Accounting tools used by the management other than ABC model

Qube Holding has surpassed all the obstacles and survived strongly against all its competitors

in the industry that reflects its compatibility to face such variations. The management of

Qube Holding has taken all such legitimate strategies into application in order to ascertain

that what works best for the same so as to reduce costs and increase its cash inflows10. The

performance and effectiveness of the management that has been operation as per required

plans and objectives, highly depends on the success of the organization. So, there are various

functions and scenarios on which the accounting tool relies on11. Absorption and marginal

costing are the best mechanisms for the organization to employ.

9

10 Qube Holding Ltd. (2016) Qube Holding Ltd Annual report & accounts 2017 [online].

Available from: http://www.annualreports.com/Company/qube-holdings-ltd [Accessed 23

May 2018]

11 Chapman, C, Hopwood, A & Shields, M. (2007). Handbook of Management Accounting

Research. Oxford, U.K.: Elsevier

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Qube Holding

Marginal costing

It is a costing mechanism where the units of cost are charred by the variable cost while the

fixed cost for the period is completely written off against the contribution. It is the accounting

mechanism for direct cost at the product level but at the same time allows full fixed overhead

cost in an accounting period12. Valuation of costs, profitability, price determination and

classification of cost as fixed and variable costs are the characteristics of marginal

accounting.

Absorption costing

It is also known as full costing for all costs (including fixed overhead charges) are included as

product costs. It includes anything that is a direct cost producing a product as the cost base. It

is a mechanism where the costs are accumulated and assigned with a manufacturing process

and aligned to individual goods. Direct materials, direct labours, variable manufacturing

overheads and fixed manufacturing overheads are the components of absorption costing.

The absorption costing might yield higher revenues if there is an increment in level of

inventory. This will allow the cost of sales to be reduced and the level of period fixed cost

will be carried forward. But in the case of marginal costing it is seen that when the inventory

level falls the marginal costing reflects higher revenues for the fixed overheads gets released

from the inventory13.

Sometimes, it is also seen that the management and the policies of Qube Holding are engaged

in a legitimate pattern and still the organization is going down the slope that is failing in all

the attempts. It might also be as a result of ignorance towards the competitive advantage that

should have been paid due importance by the organization14. This allowed the organization to

fail in its attempt of assessing the information and the efficiency difference highlighted in the

12Peirson, G, Brown, R., Easton, S, Howard, P. and Pinder, S. (2015) Business Finance, 12th

ed. North Ryde: McGraw-Hill Australia.

13 Brown, P. (2013) How can we do better?. Accounting Horizons. 27(4), p. 855–859. DOI

https://doi.org/10.2308/acch-10365 Accessed 22 May 2018

14 Petersen, C. and Plenborg, T. (2012) Financial statement analysis. Harlow, England:

Financial Times/Prentice Hall.

10

Marginal costing

It is a costing mechanism where the units of cost are charred by the variable cost while the

fixed cost for the period is completely written off against the contribution. It is the accounting

mechanism for direct cost at the product level but at the same time allows full fixed overhead

cost in an accounting period12. Valuation of costs, profitability, price determination and

classification of cost as fixed and variable costs are the characteristics of marginal

accounting.

Absorption costing

It is also known as full costing for all costs (including fixed overhead charges) are included as

product costs. It includes anything that is a direct cost producing a product as the cost base. It

is a mechanism where the costs are accumulated and assigned with a manufacturing process

and aligned to individual goods. Direct materials, direct labours, variable manufacturing

overheads and fixed manufacturing overheads are the components of absorption costing.

The absorption costing might yield higher revenues if there is an increment in level of

inventory. This will allow the cost of sales to be reduced and the level of period fixed cost

will be carried forward. But in the case of marginal costing it is seen that when the inventory

level falls the marginal costing reflects higher revenues for the fixed overheads gets released

from the inventory13.

Sometimes, it is also seen that the management and the policies of Qube Holding are engaged

in a legitimate pattern and still the organization is going down the slope that is failing in all

the attempts. It might also be as a result of ignorance towards the competitive advantage that

should have been paid due importance by the organization14. This allowed the organization to

fail in its attempt of assessing the information and the efficiency difference highlighted in the

12Peirson, G, Brown, R., Easton, S, Howard, P. and Pinder, S. (2015) Business Finance, 12th

ed. North Ryde: McGraw-Hill Australia.

13 Brown, P. (2013) How can we do better?. Accounting Horizons. 27(4), p. 855–859. DOI

https://doi.org/10.2308/acch-10365 Accessed 22 May 2018

14 Petersen, C. and Plenborg, T. (2012) Financial statement analysis. Harlow, England:

Financial Times/Prentice Hall.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Qube Holding

mechanism. It is required for the organizations to perform thorough study so as to install

Activity based costing model or absorption costing and marginal costing. All such scenarios

have affected the financial performance of Qube Holding and this can only be rectified by

employing performance measurement technique.

11

mechanism. It is required for the organizations to perform thorough study so as to install

Activity based costing model or absorption costing and marginal costing. All such scenarios

have affected the financial performance of Qube Holding and this can only be rectified by

employing performance measurement technique.

11

Qube Holding

Conclusion

Qube Holding has outdone its performance. It is observed that the organization has

beautifully adapted itself to the ever changing environment and has installed activity based

costing model and many other techniques and tools that have allowed it in a lot many ways to

garner positive results in the years that are yet to come. Apart from considering its financial

measures, Qube Holding also accounted its non financial measures that reveals the actual

reasons behind its economical position and makes it important for Qube Holding to install all

the techniques and measurements to evaluate the same. Since the implementation of ABC

model, Qube Holding has achieved managerial successes and has outdone in its operations.

12

Conclusion

Qube Holding has outdone its performance. It is observed that the organization has

beautifully adapted itself to the ever changing environment and has installed activity based

costing model and many other techniques and tools that have allowed it in a lot many ways to

garner positive results in the years that are yet to come. Apart from considering its financial

measures, Qube Holding also accounted its non financial measures that reveals the actual

reasons behind its economical position and makes it important for Qube Holding to install all

the techniques and measurements to evaluate the same. Since the implementation of ABC

model, Qube Holding has achieved managerial successes and has outdone in its operations.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13