BIBM703 - Activity Based Management: Enhancing Decision-Making

VerifiedAdded on 2023/06/03

|17

|3825

|186

Report

AI Summary

This report examines the significance of Activity-Based Management (ABM) in improving managerial decision-making within business organizations. It addresses the problem of inaccurate product cost measurement due to overhead allocation difficulties and explores how Activity-Based Costing (ABC) can mitigate these issues. The research reviews the origins, concepts, and models of ABM, highlighting its role in enhancing organizational decision-making, improving operational efficiency, and optimizing resource allocation. It also discusses the changing roles of management accountants, the impact of information technology, and necessary changes in organizational structure for effective ABM implementation. The report concludes with recommended strategies for improved decision-making through ABM, emphasizing its importance in developing corporate strategies, analyzing activities, developing budgets, and reducing customer response time. Desklib provides access to this report and many other solved assignments.

1

Activity Based Management

Activity Based Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Background/Problem Statement......................................................................................................3

Literature Review............................................................................................................................5

Overview of activity based management.....................................................................................5

Origin of Activity based management.........................................................................................5

Concept of activity based management.......................................................................................6

Model of Activity based management given by the CAM-I........................................................7

Role of Activity based management in improving the organization decision making................7

Importance of Activity based management..............................................................................7

Areas of Use in organization....................................................................................................8

Improving the operational and strategic decisions.................................................................10

Recommended Strategies for Improved Decision-Making within Organizations by use of

ABM approach...........................................................................................................................11

Changing Role of Management Accountants.........................................................................11

Changes in Information Technology (IT) Systems & Processes...........................................12

Changes in Organizational Structure.........................................................................................13

Suggested Study.............................................................................................................................13

References......................................................................................................................................15

Contents

Background/Problem Statement......................................................................................................3

Literature Review............................................................................................................................5

Overview of activity based management.....................................................................................5

Origin of Activity based management.........................................................................................5

Concept of activity based management.......................................................................................6

Model of Activity based management given by the CAM-I........................................................7

Role of Activity based management in improving the organization decision making................7

Importance of Activity based management..............................................................................7

Areas of Use in organization....................................................................................................8

Improving the operational and strategic decisions.................................................................10

Recommended Strategies for Improved Decision-Making within Organizations by use of

ABM approach...........................................................................................................................11

Changing Role of Management Accountants.........................................................................11

Changes in Information Technology (IT) Systems & Processes...........................................12

Changes in Organizational Structure.........................................................................................13

Suggested Study.............................................................................................................................13

References......................................................................................................................................15

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Background/Problem Statement

The business organizations at present are largely faced increasing difficulties for

accurately measuring the product cost due to difficulties faced in the allocation of overheads.

The businesses face difficulties in measuring the variable or overhead costs as it tends to

fluctuate with the volume of production level and thus causes problem for allocation of general

expenses. Besides this, the increasing operational expenses due to large number of production

activities and waste generation tend to negatively impact the profitability level of business

organizations. The inaccurate allocation of overhead costs causes the business to face problems

during taking significant decisions regarding price and development of future growth strategies.

The use of Activity-Based Costing (ABC) is increasing among the organizations for measuring

the cost and eliminating the occurrence of undesirable activities that tends to increase the

operational costs. The introduction of activity based costing (ABC) systems by businesses aims

to achieve a more accurate allocation of production costs and thus reducing the operational

expenses for improving their profitability position (Jafari, 2012).

ABC is regarded as a costing system that determines the overall product costs on the

basis of activities carried out for producing products. It relates costs, that is, the overall resource

consumed in relation to the overall products manufactured and thus provides a better tool for

resources allocation. The overall overhead costs are divided into different cost pools on the basis

of the different business activities. The measuring of product costs on the basis of resource

consumed by each overhead activity facilitates in determining the overall production costs on the

basis of output. Activity-based management can be defined as the process of managing the

different processes involved in activity-based costing such as identifying activities, cost drivers,

Background/Problem Statement

The business organizations at present are largely faced increasing difficulties for

accurately measuring the product cost due to difficulties faced in the allocation of overheads.

The businesses face difficulties in measuring the variable or overhead costs as it tends to

fluctuate with the volume of production level and thus causes problem for allocation of general

expenses. Besides this, the increasing operational expenses due to large number of production

activities and waste generation tend to negatively impact the profitability level of business

organizations. The inaccurate allocation of overhead costs causes the business to face problems

during taking significant decisions regarding price and development of future growth strategies.

The use of Activity-Based Costing (ABC) is increasing among the organizations for measuring

the cost and eliminating the occurrence of undesirable activities that tends to increase the

operational costs. The introduction of activity based costing (ABC) systems by businesses aims

to achieve a more accurate allocation of production costs and thus reducing the operational

expenses for improving their profitability position (Jafari, 2012).

ABC is regarded as a costing system that determines the overall product costs on the

basis of activities carried out for producing products. It relates costs, that is, the overall resource

consumed in relation to the overall products manufactured and thus provides a better tool for

resources allocation. The overall overhead costs are divided into different cost pools on the basis

of the different business activities. The measuring of product costs on the basis of resource

consumed by each overhead activity facilitates in determining the overall production costs on the

basis of output. Activity-based management can be defined as the process of managing the

different processes involved in activity-based costing such as identifying activities, cost drivers,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

performance measures and activity costs for determination of accurate product costs. The major

goal is to improve the value delivered to customers and improving the profitability position of a

company (Pete, 2011).

In this context, the present research is undertaken for examining the significance of

Activity-Based Management (ABC) for improving manager’s decision-making within business

organizations. As such, the problem statement developed for the research proposal can be stated

as ‘How does Activity-Based Management (ABM) approach facilitates improved decision-

making of the management accountants?

The research topic selected holds high significance for providing an in-depth

understanding to the management accountants for the potential benefits that they can derive with

the use of activity-based costing system. It will be highly pertinent to the business managers for

developing knowledge in relation to the strategies that can be adopted by them for maximizing

the operational efficiency. It will help in accurately identifying the cost drivers for optimizing

resources for business so that they can produce more accurate costing results. The proposal

developed presently as provided a brief overview in relation to the research topic by undertaking

its theoretical analysis with the use of literature review section. The research in this context has

examined the various issues related with the topic through presenting a critical analysis of some

selected academic articles. This is carried out to provide a deep insight into the various topics

related with activity-based management such as activity-based costing, activity-based budgeting

and the implementation strategies that can be adopted by business managers for their integration

to derive improved business results. It has also included a section of providing suggestions for

the research that could be conducted on the basis of the proposal developed.

performance measures and activity costs for determination of accurate product costs. The major

goal is to improve the value delivered to customers and improving the profitability position of a

company (Pete, 2011).

In this context, the present research is undertaken for examining the significance of

Activity-Based Management (ABC) for improving manager’s decision-making within business

organizations. As such, the problem statement developed for the research proposal can be stated

as ‘How does Activity-Based Management (ABM) approach facilitates improved decision-

making of the management accountants?

The research topic selected holds high significance for providing an in-depth

understanding to the management accountants for the potential benefits that they can derive with

the use of activity-based costing system. It will be highly pertinent to the business managers for

developing knowledge in relation to the strategies that can be adopted by them for maximizing

the operational efficiency. It will help in accurately identifying the cost drivers for optimizing

resources for business so that they can produce more accurate costing results. The proposal

developed presently as provided a brief overview in relation to the research topic by undertaking

its theoretical analysis with the use of literature review section. The research in this context has

examined the various issues related with the topic through presenting a critical analysis of some

selected academic articles. This is carried out to provide a deep insight into the various topics

related with activity-based management such as activity-based costing, activity-based budgeting

and the implementation strategies that can be adopted by business managers for their integration

to derive improved business results. It has also included a section of providing suggestions for

the research that could be conducted on the basis of the proposal developed.

6

Literature Review

Overview of activity based management

In the views of Ansari & Bell (2008), the success factor of activity based management

has attracted the interest of many researchers and scholars to conduct the research and provide

their viewpoints on the same. Activity based management has been emerged from the activity

based costing and they both interrelated to each other. Activity based costing has been developed

to as an important management approach to solve the problems associated with the traditional

cost management systems. The traditional costing management has many issues such as it has

inability to accurately calculate the actual production, manufacturing cost and service cost. Also,

it was not able to provide the useful information that helps the managers to make the operating

decisions. Due to all such deficiencies in the traditional cost management system, the managers

faced problems in making the decisions and they have to be dependent on the inaccurate data for

making the judgments. To overcome the deficiencies in the traditional cost management system,

a new system known as activity based costing/management system has been introduced. This

management system helps to solve the issues faced in older management system and provide

very useful information that helps in making the decisions more accurately (Ansari & Bell,

2008).

Origin of Activity based management

In the views of Brierley (2008), activity based costing and activity based management has

brought a major change in the cost management systems. It can be said that activity based

management has grown mainly with efforts of the Texas based “Consortium for Advanced

Manufacturing-International (CAM-I)”. CAM-I is an international based organization that helps

manufacturing companies, government, service companies, professional bodies, and other

Literature Review

Overview of activity based management

In the views of Ansari & Bell (2008), the success factor of activity based management

has attracted the interest of many researchers and scholars to conduct the research and provide

their viewpoints on the same. Activity based management has been emerged from the activity

based costing and they both interrelated to each other. Activity based costing has been developed

to as an important management approach to solve the problems associated with the traditional

cost management systems. The traditional costing management has many issues such as it has

inability to accurately calculate the actual production, manufacturing cost and service cost. Also,

it was not able to provide the useful information that helps the managers to make the operating

decisions. Due to all such deficiencies in the traditional cost management system, the managers

faced problems in making the decisions and they have to be dependent on the inaccurate data for

making the judgments. To overcome the deficiencies in the traditional cost management system,

a new system known as activity based costing/management system has been introduced. This

management system helps to solve the issues faced in older management system and provide

very useful information that helps in making the decisions more accurately (Ansari & Bell,

2008).

Origin of Activity based management

In the views of Brierley (2008), activity based costing and activity based management has

brought a major change in the cost management systems. It can be said that activity based

management has grown mainly with efforts of the Texas based “Consortium for Advanced

Manufacturing-International (CAM-I)”. CAM-I is an international based organization that helps

manufacturing companies, government, service companies, professional bodies, and other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

entities in solving their management problems and provide resolutions based on critical business

issues that are common for many organizations. The role of activity based management system is

no longer limited to the manufacturing companies and can be applied equally to the service

companies, government organizations and other form of organisations (Brierley, 2008).

Concept of activity based management

According to Brierley (2011), the concept of activity based management has been derived

from the activity based costing. The activity based management has been defined as a set of

actions that focuses on the management of various activities within the organization in order to

improve the value received by the customer and profit earned through providing all such values.

The process of activity based management includes the analysis of cost drivers, analysis of all

the management activities and measuring of performance. In short it can be said that activity

based management is derived from the activity based costing. ABC tends to answer the question

“What do activities cost?”, whereas, ABM as management process tends to answer the question

“What factors causes the cost to occur?” Activity based management uses the information

gathered from the activity based costing to improve and redirect the allocation and use of

resources in order to increase the value created for the customers and all other stakeholders

(Brierley, 2011).

entities in solving their management problems and provide resolutions based on critical business

issues that are common for many organizations. The role of activity based management system is

no longer limited to the manufacturing companies and can be applied equally to the service

companies, government organizations and other form of organisations (Brierley, 2008).

Concept of activity based management

According to Brierley (2011), the concept of activity based management has been derived

from the activity based costing. The activity based management has been defined as a set of

actions that focuses on the management of various activities within the organization in order to

improve the value received by the customer and profit earned through providing all such values.

The process of activity based management includes the analysis of cost drivers, analysis of all

the management activities and measuring of performance. In short it can be said that activity

based management is derived from the activity based costing. ABC tends to answer the question

“What do activities cost?”, whereas, ABM as management process tends to answer the question

“What factors causes the cost to occur?” Activity based management uses the information

gathered from the activity based costing to improve and redirect the allocation and use of

resources in order to increase the value created for the customers and all other stakeholders

(Brierley, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

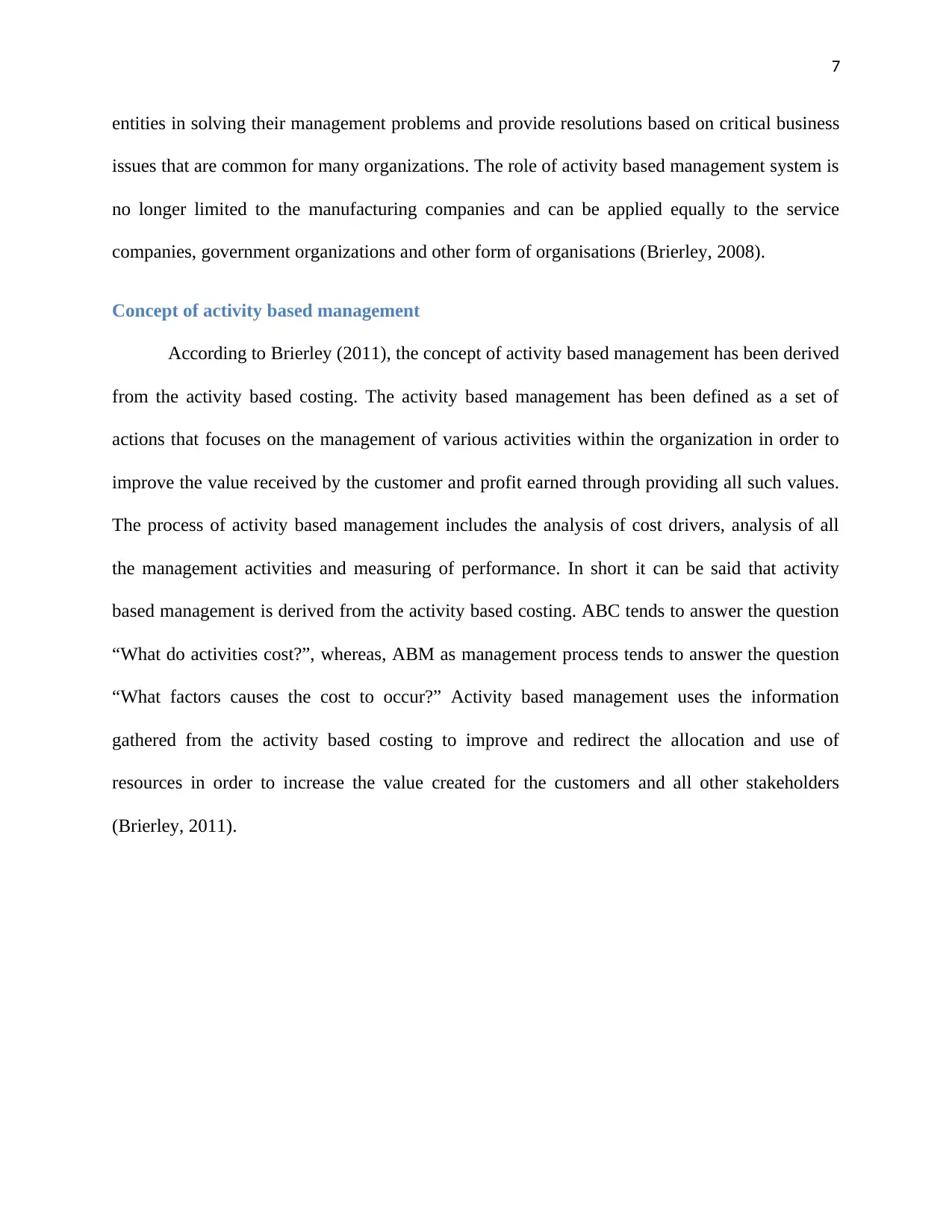

Model of Activity based management given by the CAM-I

(Source: http://www.cimaglobal.com/Documents/ImportedDocuments/ABM_techrpt_0401.pdf)

Role of Activity based management in improving the organization decision making

Importance of Activity based management

As per the thoughts of DeFreitas, Gillett, Fink & Cox (2013), activity based management

concerns mainly for the accountability for the activities rather than cost associated with the

processes. It lay emphasis on the system wide performance and completely ignores the

performance at individual end. According the ABM control, improving the performance of

individual cannot always increases the efficiency of the system as a whole. Activity based

management control assigns all the costs of each unit of organization and after that it is

responsibility of unit manager to assign the costs to each process of that particular unit. The

actual outcomes from each activity are measured with the budgeted figures to measure the

Model of Activity based management given by the CAM-I

(Source: http://www.cimaglobal.com/Documents/ImportedDocuments/ABM_techrpt_0401.pdf)

Role of Activity based management in improving the organization decision making

Importance of Activity based management

As per the thoughts of DeFreitas, Gillett, Fink & Cox (2013), activity based management

concerns mainly for the accountability for the activities rather than cost associated with the

processes. It lay emphasis on the system wide performance and completely ignores the

performance at individual end. According the ABM control, improving the performance of

individual cannot always increases the efficiency of the system as a whole. Activity based

management control assigns all the costs of each unit of organization and after that it is

responsibility of unit manager to assign the costs to each process of that particular unit. The

actual outcomes from each activity are measured with the budgeted figures to measure the

9

performance. Activity based management is mainly concerned for the financial performance but

does not completely ignores the non financial performance. Activity based management

promotes the use of reward system for unit managers and also for individual for managing the

overall cost and increasing the operating efficiency of the organizational units. It means there is

requirement to trace the cost incurred by the individual for deciding the basis of reward system.

So both financial and non financial measures are applied to measure the performance of each

individual in the activity based management system (DeFreitas, Gillett, Fink & Cox, 2013).

As per Euske & Vercio (2007), activity based management mainly improves the decision

making power of the management and also provide a platform where they link the overall cost of

the organization to each activity so that cost allocation can be done on optimum basis. The cost

identification and allocation is two main processes that are carried out while implementing

activity based costing. Activity based management is one step ahead as it links the cost with

activity so that performance derived from each activity can be successfully measured and any

discrepancies against the budgeted norms can be rectified with ease (Euske & Vercio, 2007).

Areas of Use in organization

Fetzer & Kren (2012), has defined various use of activity based management within the

organization. Some of major uses of activity based management are as under:

Developing or framing of the corporate strategy: The major use of ABM is to develop

the company strategies, budgets and long term plans through involving managers and

focusing on each management activities. It leads to find out the competitive advantage

that every organization posses and it helps to produce the low cost products through

effective management of activities. It is easy to cut the cost through closing down the

performance. Activity based management is mainly concerned for the financial performance but

does not completely ignores the non financial performance. Activity based management

promotes the use of reward system for unit managers and also for individual for managing the

overall cost and increasing the operating efficiency of the organizational units. It means there is

requirement to trace the cost incurred by the individual for deciding the basis of reward system.

So both financial and non financial measures are applied to measure the performance of each

individual in the activity based management system (DeFreitas, Gillett, Fink & Cox, 2013).

As per Euske & Vercio (2007), activity based management mainly improves the decision

making power of the management and also provide a platform where they link the overall cost of

the organization to each activity so that cost allocation can be done on optimum basis. The cost

identification and allocation is two main processes that are carried out while implementing

activity based costing. Activity based management is one step ahead as it links the cost with

activity so that performance derived from each activity can be successfully measured and any

discrepancies against the budgeted norms can be rectified with ease (Euske & Vercio, 2007).

Areas of Use in organization

Fetzer & Kren (2012), has defined various use of activity based management within the

organization. Some of major uses of activity based management are as under:

Developing or framing of the corporate strategy: The major use of ABM is to develop

the company strategies, budgets and long term plans through involving managers and

focusing on each management activities. It leads to find out the competitive advantage

that every organization posses and it helps to produce the low cost products through

effective management of activities. It is easy to cut the cost through closing down the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

operations that lead to increase in cost but it does not solve the real problem of quality

goods with increase in quantity. In this regard ABM plays an important role as it leads to

decrease in cost while maintaining the quality and quantity required by the management

(Fetzer & Kren, 2012).

Activity Analysis with the organization: The major aim of activity based management

is to achieve the continuous improvement through performing the activity analysis. It

means ABM helps in classifying each activity performed within the organization as value

added or non value added through evaluating its role and substance achieved through it.

In this context, a value added activity is defined as activity that adds some value to

product or service from the point of consumer while non value added activity refers to an

activity that does not tends to add value to the product or service. It can be said that

activities that adds some value to the product increases the brand image of the

organization and also allows charging extra for such value added. ABM supports value

chain analysis in which each activity performed within the organization are classified,

reclassified, terminated and improved as per the requirement of achieving the success in

business. As non value added activity leads to unnecessary increase in product or service

cost without any value addition. So it is important to terminate such activities through

classifying them as non value activity and introduce new activity that helps to achieve

some value to the product or service.

Development of Budgets: The main purpose of ABM is to help the managers to forecast

the budgets through using the past information of each process and allocate the cost in

such activity that add some value to the goods and services deliver by the company.

Activity based budgeting is performed within the activity based management which

operations that lead to increase in cost but it does not solve the real problem of quality

goods with increase in quantity. In this regard ABM plays an important role as it leads to

decrease in cost while maintaining the quality and quantity required by the management

(Fetzer & Kren, 2012).

Activity Analysis with the organization: The major aim of activity based management

is to achieve the continuous improvement through performing the activity analysis. It

means ABM helps in classifying each activity performed within the organization as value

added or non value added through evaluating its role and substance achieved through it.

In this context, a value added activity is defined as activity that adds some value to

product or service from the point of consumer while non value added activity refers to an

activity that does not tends to add value to the product or service. It can be said that

activities that adds some value to the product increases the brand image of the

organization and also allows charging extra for such value added. ABM supports value

chain analysis in which each activity performed within the organization are classified,

reclassified, terminated and improved as per the requirement of achieving the success in

business. As non value added activity leads to unnecessary increase in product or service

cost without any value addition. So it is important to terminate such activities through

classifying them as non value activity and introduce new activity that helps to achieve

some value to the product or service.

Development of Budgets: The main purpose of ABM is to help the managers to forecast

the budgets through using the past information of each process and allocate the cost in

such activity that add some value to the goods and services deliver by the company.

Activity based budgeting is performed within the activity based management which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

means activity based budgeting is the integral part of ABM. Budgets are drawn for each

activity and performances are measured on the basis of information gathered for each

activity.

Reduction in customer response time: Through implementation of ABM in the

management process, the response time from customers get reduced through

identification of activities that does not give value and consume resources. In this way,

ABM supports the management activities through valuing the customers and increasing

the value of satisfaction achieved by them (Kocakulah & David Austill, 2017).

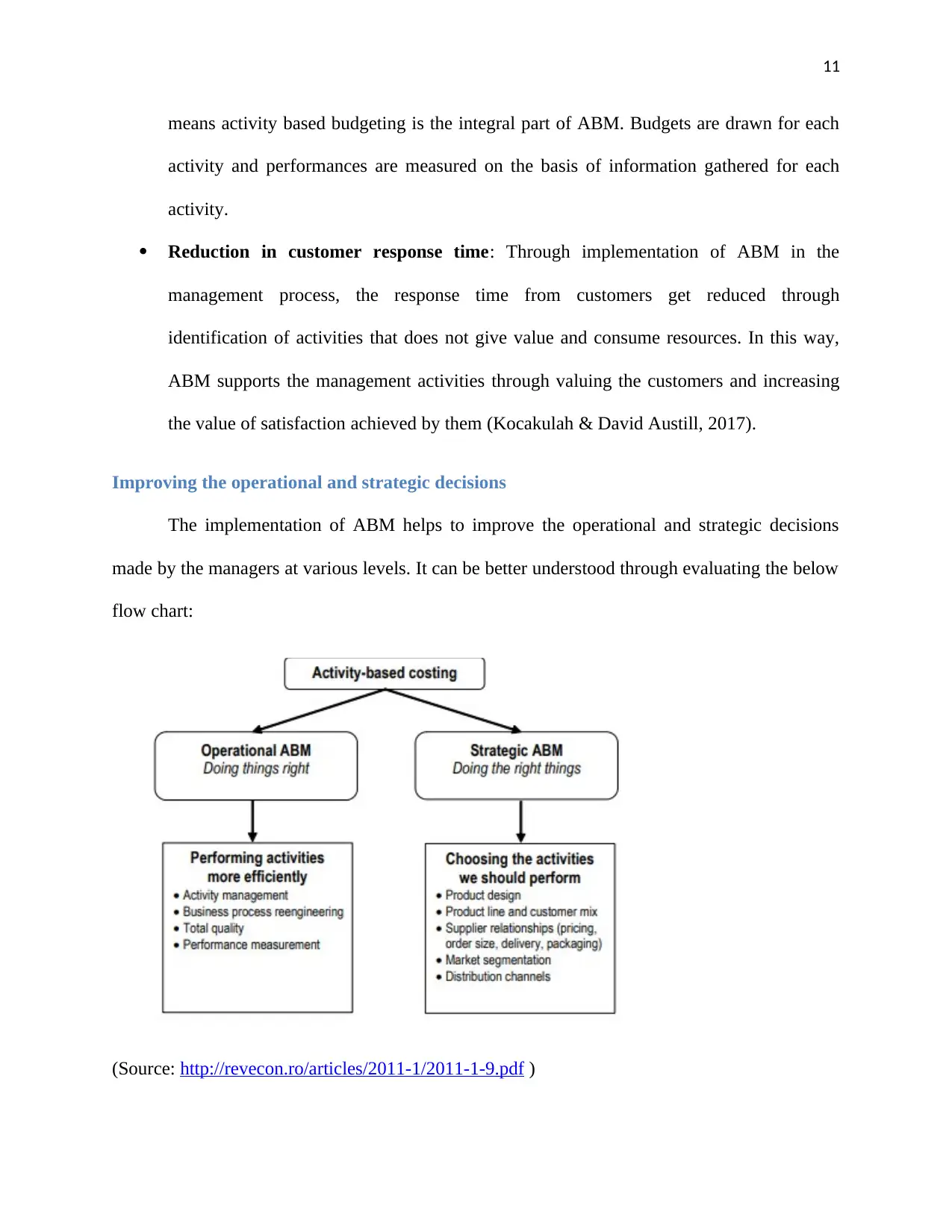

Improving the operational and strategic decisions

The implementation of ABM helps to improve the operational and strategic decisions

made by the managers at various levels. It can be better understood through evaluating the below

flow chart:

(Source: http://revecon.ro/articles/2011-1/2011-1-9.pdf )

means activity based budgeting is the integral part of ABM. Budgets are drawn for each

activity and performances are measured on the basis of information gathered for each

activity.

Reduction in customer response time: Through implementation of ABM in the

management process, the response time from customers get reduced through

identification of activities that does not give value and consume resources. In this way,

ABM supports the management activities through valuing the customers and increasing

the value of satisfaction achieved by them (Kocakulah & David Austill, 2017).

Improving the operational and strategic decisions

The implementation of ABM helps to improve the operational and strategic decisions

made by the managers at various levels. It can be better understood through evaluating the below

flow chart:

(Source: http://revecon.ro/articles/2011-1/2011-1-9.pdf )

12

According to Maiga & Jacobs (2007), the decisions taken by the managers are mainly

divided into two major parts: Operational and Strategic. There is very important role of ABM in

both kind of decision making. The operational decision making aims to improve the efficiency,

lower the cost and also makes sure for the asset utilization. Through use of ABM operation

manager can formulate the functional budgets that help gaining an idea of futures operations cost

in each activity and leads to create more accurate budgets as compare to traditional budgets.

ABM helps to explore various ways through which company can create and retain the

competitive advantage in the market place (Maiga & Jacobs, 2007).

Recommended Strategies for Improved Decision-Making within Organizations by use of

ABM approach

Changing Role of Management Accountants

According to Scheumann (2010), the development of the concept of Activity-based

Management (ABM) is causing major changes in the role of accountants in recent times. This is

because there is major transition in the nature of accounting systems and processes used for

identifying and determining the product costs. Activity-based management requires management

accountants to determine costs on the basis of overall business activities and therefore requires

transition in their role from maintaining the overall functioning of the accounting systems to

more business-oriented role. As such, the responsibility of management accountants has

becoming increasing important in designing of an ABC system. ABC system has placed

increased emphasis on managing costs and thus requires managers to identify and focus on the

activities that give rise to the costs. The successful implementation of the ABC costing system

requires the managers to accurately identify and distinguish between the value-added and non-

value added costs. Value-added are the costs that are required to be incurred by businesses for

According to Maiga & Jacobs (2007), the decisions taken by the managers are mainly

divided into two major parts: Operational and Strategic. There is very important role of ABM in

both kind of decision making. The operational decision making aims to improve the efficiency,

lower the cost and also makes sure for the asset utilization. Through use of ABM operation

manager can formulate the functional budgets that help gaining an idea of futures operations cost

in each activity and leads to create more accurate budgets as compare to traditional budgets.

ABM helps to explore various ways through which company can create and retain the

competitive advantage in the market place (Maiga & Jacobs, 2007).

Recommended Strategies for Improved Decision-Making within Organizations by use of

ABM approach

Changing Role of Management Accountants

According to Scheumann (2010), the development of the concept of Activity-based

Management (ABM) is causing major changes in the role of accountants in recent times. This is

because there is major transition in the nature of accounting systems and processes used for

identifying and determining the product costs. Activity-based management requires management

accountants to determine costs on the basis of overall business activities and therefore requires

transition in their role from maintaining the overall functioning of the accounting systems to

more business-oriented role. As such, the responsibility of management accountants has

becoming increasing important in designing of an ABC system. ABC system has placed

increased emphasis on managing costs and thus requires managers to identify and focus on the

activities that give rise to the costs. The successful implementation of the ABC costing system

requires the managers to accurately identify and distinguish between the value-added and non-

value added costs. Value-added are the costs that are required to be incurred by businesses for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.